Europe Mobile Gaming Market Size, Share, Trends and Forecast by Type, Device Type, Platform, Business Model, and Country, 2026-2034

Europe Mobile Gaming Market Summary:

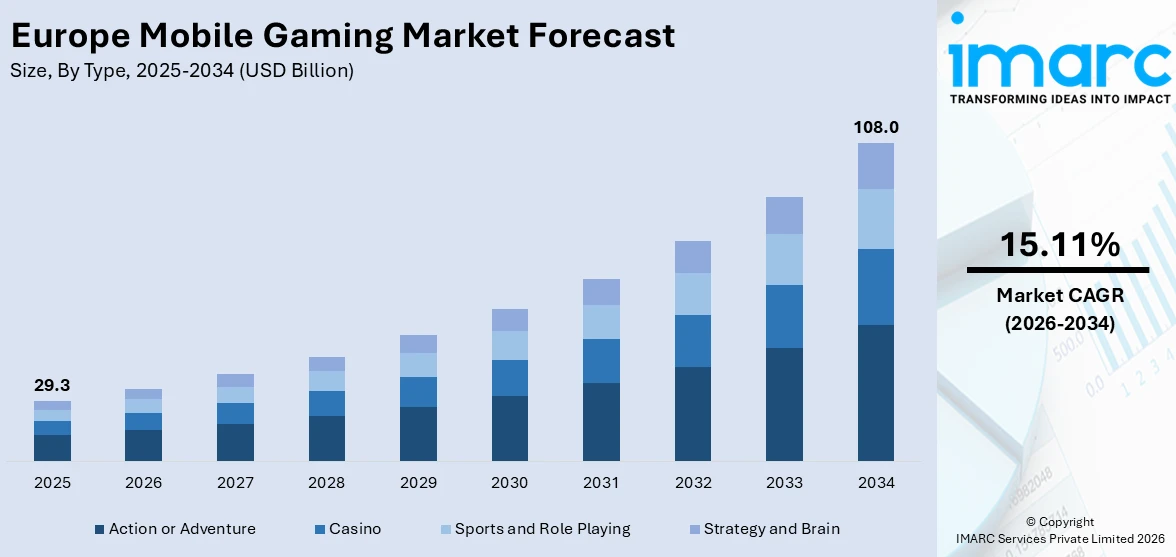

The Europe mobile gaming market size was valued at USD 29.3 Billion in 2025 and is projected to reach USD 108.0 Billion by 2034, growing at a compound annual growth rate of 15.11% from 2026-2034.

The Europe mobile gaming market is witnessing robust expansion driven by the widespread penetration of smartphones, the proliferation of high-speed 5G networks, and the rising demand for interactive digital entertainment. Growing consumer preference for immersive gaming experiences, advances in cloud gaming technologies, and evolving monetization strategies are strengthening market fundamentals across the region, boosting the Europe mobile gaming market share.

Key Takeaways and Insights:

- By Type: Action or adventure dominates the market with a share of 35% in 2025, owing to the strong consumer preference for narrative-driven and visually immersive gameplay experiences. Continuous innovation in mobile game design and real-time multiplayer integration are fueling segment expansion.

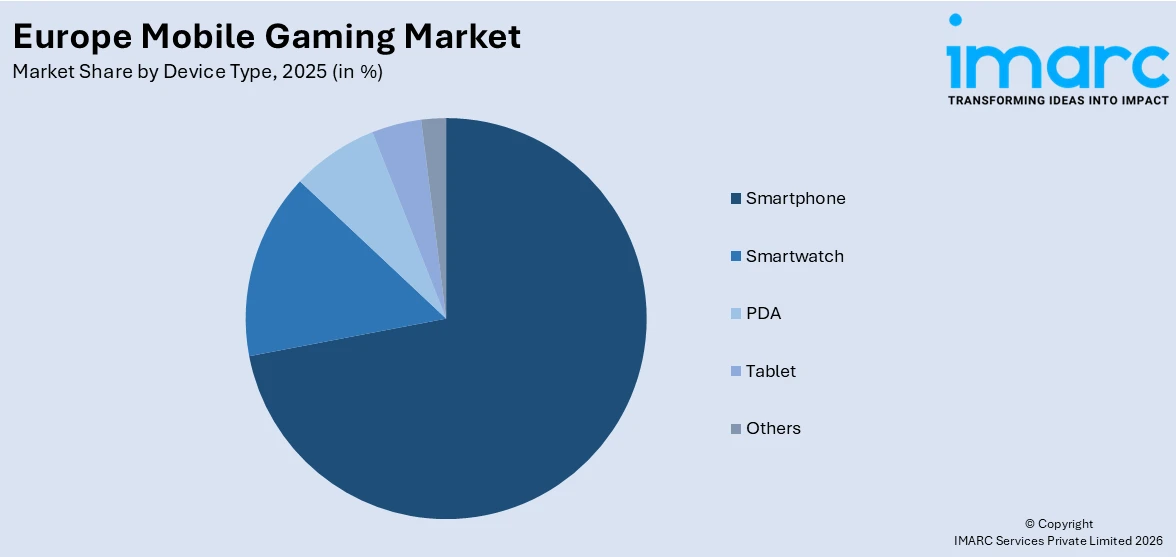

- By Device Type: Smartphone leads the market with a share of 72% in 2025, driven by the widespread accessibility and advanced processing capabilities of modern smartphones. Growing 5G adoption and improved mobile hardware are reinforcing smartphone dominance across player demographics.

- By Platform: Android exhibits a clear dominance in the market with 56% share in 2025, reflecting the platform’s affordability, open ecosystem, and extensive device diversity across European markets. Broader availability of Android-powered devices across Southern and Eastern Europe accelerates adoption.

- By Business Model: Freemium represents the largest segment with a market share of 70% in 2025, underpinned by the effectiveness of free-to-play models that drive widespread user acquisition and sustained monetization through in-app purchases and seasonal content passes.

- Key Players: Key players drive the Europe mobile gaming market by expanding game portfolios, advancing cloud gaming capabilities, investing in cross-platform technologies, and forming strategic partnerships with telecom operators and technology firms to enhance distribution, engagement, and competitive positioning across the region.

To get more information on this market Request Sample

The Europe mobile gaming market is advancing as technological innovation, expanding digital infrastructure, and shifting consumer preferences converge to reshape the entertainment landscape across the continent. A major factor supporting this growth is the rapid rollout of 5G connectivity, which enables seamless cloud gaming and richer mobile experiences. The widespread adoption of smartphones as the preferred gaming platform is reinforcing mobile-first engagement patterns across key European markets. Mobile platforms are capturing an increasing share of overall gaming revenue, reflecting the accelerating shift toward on-the-go digital entertainment. Policy developments such as the Digital Markets Act are also opening up new distribution channels, further supporting competitive dynamics. Rising consumer engagement, evolving monetization strategies, and growing interest in social and multiplayer gaming experiences are positioning the region as a maturing hub for mobile gaming innovation and investment.

Europe Mobile Gaming Market Trends:

Rising Adoption of Cloud Gaming Services

Cloud gaming is rapidly transforming the European mobile gaming landscape by enabling players to access premium-quality titles directly on smartphones without relying on high-performance hardware. For instance, in August 2025, Samsung Electronics expanded its mobile cloud gaming platform into Europe, launching a beta rollout in the United Kingdom and Germany to provide Galaxy device users instant access to top mobile titles without downloads. Improvements in 5G infrastructure and network optimization are reinforcing Europe mobile gaming market growth through lower latency and higher-fidelity mobile experiences.

Growing Integration of Social and Multiplayer Features

European mobile gamers are increasingly seeking interactive and community-driven gaming experiences, prompting developers to integrate real-time multiplayer modes, cross-platform play, and social connectivity features. Guild systems, live chat functions, and cooperative challenges are becoming standard elements that foster deeper community bonds among players. Developers are also leveraging social media integration and in-game content sharing to amplify user interaction beyond traditional gameplay boundaries. This shift toward collaborative and socially immersive gaming is strengthening player engagement and retention across the region.

Expansion of Alternative App Distribution Channels

Regulatory developments in Europe are reshaping how mobile games are distributed, opening up new pathways for players and developers beyond traditional app stores. For example, in August 2024, Epic Games launched its mobile store on iOS in the European Union, facilitated by the Digital Markets Act, bringing Fortnite back to iPhones in Europe after a four-year absence. These distribution shifts are intensifying competition and broadening consumer access to diverse gaming content across the continent.

Market Outlook 2026-2034:

The Europe mobile gaming market is positioned for sustained expansion, supported by continuing 5G deployment, cloud gaming adoption, and evolving consumer engagement patterns. The market generated a revenue of USD 29.3 Billion in 2025 and is projected to reach a revenue of USD 108.0 Billion by 2034, growing at a compound annual growth rate of 15.11% from 2026-2034. Higher income streams are anticipated as a result of growing investments in cross-platform gaming technology, social and multiplayer capabilities, and sophisticated monetization strategies. The competitive landscape is expected to be strengthened and wider accessibility promoted by the growth of alternative distribution channels, legislative support provided by the Digital Markets Act, and the increasing desire for immersive mobile entertainment experiences. Further factors that are expected to boost interest and expenditure include growing smartphone adoption, enhancing mobile hardware capabilities, and further integrating artificial intelligence into game creation. Over the course of the projection period, these convergent dynamics are anticipated to make Europe one of the world's most vibrant and developed mobile gaming ecosystems, providing substantial growth prospects for publishers, developers, and platform providers.

.webp)

Europe Mobile Gaming Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Type |

Action or Adventure |

35% |

|

Device Type |

Smartphone |

72% |

|

Platform |

Android |

56% |

|

Business Model |

Freemium |

70% |

Type Insights:

- Action or Adventure

- Casino

- Sports and Role Playing

- Strategy and Brain

Action or adventure dominates with a share of 35% of the total Europe mobile gaming market in 2025.

Due to the high demand from consumers for skill-based, graphically stunning, and narratively driven gameplay, the action/adventure genre continues to dominate the European mobile gaming market. This genre's games include open-world exploration, dynamic combat systems, and periodic content releases that promote consistent player involvement. Cross-platform capability helps the market by enabling customers to go on with their experiences on consoles and cellphones with ease. As creators place a higher priority on controller compatibility, specific accessibility features, and easy-to-use touch controls in order to provide immersive experiences on portable devices, the popularity of console-quality action games is growing even more.

European publishers and developers are consistently making investments in top-notch action and adventure games that use cooperative multiplayer features, live-service content formats, and cinematic narrative. Access to visually demanding action games on mid-range smartphones is being further expanded by the increasing use of cloud gaming platforms throughout Europe. Major industry gatherings around the area also operate as important venues for introducing new action and adventure books, creating a lot of media interest and building customer expectation that strengthens the genre's leading position in the marketplace.

Device Type Insights:

Access the comprehensive market breakdown Request Sample

- Smartphone

- Smartwatch

- PDA

- Tablet

- Others

Smartphone leads the market with a share of 72% of the total Europe mobile gaming market in 2025.

Smartphones remain the predominant gaming device in Europe, driven by their ubiquitous ownership, advanced processing capabilities, and seamless integration with high-speed mobile networks. The growing availability of 5G-enabled smartphones has enhanced the quality and responsiveness of mobile gaming, enabling richer graphics and lower-latency cloud gaming experiences. European consumers increasingly use smartphones for both casual and competitive gaming, supported by improved battery life, larger display sizes, and dedicated gaming modes. For instance, according to the German Games Industry Association, approximately 22.9 Million people in Germany played games on smartphones in 2024, maintaining the smartphone’s position as the country’s most widely used gaming platform.

The smartphone segment’s dominance is further reinforced by telecom operator initiatives that integrate gaming services directly into mobile subscriptions. In December 2025, Deutsche Telekom expanded its 5G+ Gaming offering with NVIDIA GeForce NOW, making Germany’s largest 5G network the first in Europe to offer latency-optimized mobile cloud gaming based on 5G standalone technology. Such collaborations between device manufacturers, telecom providers, and gaming platforms are creating a richer ecosystem for smartphone-based gaming across Europe, attracting both casual and dedicated mobile players.

Platform Insights:

- Android

- iOS

- Others

Android is the largest segment, accounting for 56% of the total Europe mobile gaming market in 2025.

Thanks to its open environment, diverse range of devices, and affordability in all countries, the Android platform is the industry leader in European mobile gaming. Android's dominant market share is fueled by its wide presence in Southern, Eastern, and Central Europe, where low- and mid-range smartphones are common. The Digital Markets Act has strengthened the platform's interoperability with several app stores and third-party distribution channels, giving developers more options for distribution and revenue. Customers' access to a wider range of mobile gaming distribution channels is being further increased by collaborations between big game publishers and telecom carriers to preinstall alternative app stores on Android smartphones in strategic European regions.

A large collection of free-to-play and freemium games that appeal to a wide range of player demographics, as well as Android's connectivity with cloud gaming services, further contribute to its supremacy. The platform gains from frequent revisions to developer tools and app store regulations, which enhance user engagement and discoverability. Furthermore, paid video ads are still widely accepted by Android users in Europe, and advertising-supported models are becoming more popular as developers investigate hybrid monetization tactics that combine contextual advertising and in-app payments throughout the Android ecosystem.

Business Model Insights:

- Freemium

- Paid

- Free

- Paymium

Freemium holds the largest share at 70% of the total Europe mobile gaming market in 2025.

By facilitating the mass acquisition of users through free downloads and producing consistent income through in-app purchases, seasonal battle passes, and cosmetic microtransactions, the freemium business model dominates the European mobile gaming industry. By decreasing the entrance barrier and providing optional premium content, this model appeals to a wide range of gamers, from casual to devoted. Free-to-play games continue to provide the bulk of mobile gaming income, with in-app purchases continuing to be the main source of revenue in the area. Freemium products' accessibility keeps drawing in new player categories, such as first-time players and elderly audiences.

European game companies are advancing freemium revenue models by introducing time-limited events, seasonal content passes, and social interaction tactics that promote repeat purchases and long-term retention. By combining voluntary in-app purchases with rewarded video advertisements, hybrid monetization techniques are becoming more and more popular, expanding revenue streams without compromising user happiness. With the advent of privacy-compliant advertising technologies that adhere to the General Data Protection Regulation, developers may now include targeted marketing campaigns into mobile games. As a result, the European freemium gaming business may now generate income from sources other than microtransactions.

Country Insights:

- Germany

- France

- United Kingdom

- Italy

- Spain

- Others

Germany is a leading force in Europe's mobile gaming landscape, supported by a large and active smartphone gaming population. The country's advanced 5G infrastructure, strong consumer spending power, and prominent industry events drive continuous engagement and innovation. Telecom operators are pioneering cloud gaming solutions, while a thriving developer community reinforces Germany's position as a major mobile gaming hub within Europe.

France stands as a dynamic mobile gaming market in Europe, recognized for having one of the highest gaming penetration rates on the continent. Increasing smartphone adoption, a vibrant independent game development ecosystem, and growing interest in social and casual gaming experiences are contributing to sustained mobile gaming expansion and reinforcing the country's influential role in shaping regional trends.

The United Kingdom represents a significant share of the European mobile gaming market, supported by high digital literacy, strong consumer spending on in-app purchases, and a well-established developer ecosystem. The country serves as a key testing ground for new gaming technologies, distribution models, and regulatory developments that continue to shape the broader European mobile gaming landscape.

As smartphone penetration increases and younger demographics embrace digital entertainment more and more, the mobile gaming business in Italy is growing. Wider acceptance across a range of age groups is being driven by rising engagement in casual puzzle, simulation, and social game forms. Italy's contribution to the regional gaming ecosystem is being strengthened by growing interest in mobile-first experiences and enhanced network infrastructure.

Thanks to rising smartphone ownership and increased high-speed internet, Spain is becoming a more significant player in the European mobile gaming business. Through collaborations between telecom operators and game publishers, additional app distribution channels are being introduced, increasing consumer access to a variety of gaming content and creating a more competitive distribution market nationwide.

Market Dynamics:

Growth Drivers:

Why is the Europe Mobile Gaming Market Growing?

Accelerating 5G Network Deployment and Cloud Gaming Integration

With higher download speeds, ultra-low latency, and more dependable connectivity, the quick rollout of 5G infrastructure throughout Europe is radically changing the mobile gaming experience. This change in technology makes it possible to broadcast graphically demanding games to smartphones with ease, decreasing the need for pricey local gear and increasing the number of players that can be reached. By developing compelling use cases that encourage subscriber engagement and the adoption of premium services, telecom operators are aggressively incorporating cloud gaming services into their 5G offers. The combination of cloud gaming platforms and high-speed internet is anticipated to open up new income streams and transform how European customers access and engage with mobile games as 5G coverage spreads throughout the continent. Europe is at the vanguard of next-generation mobile entertainment delivery because to network slicing capabilities and latency optimization technologies, which are also improving the quality and consistency of mobile cloud gaming experiences.

Rising Smartphone Penetration and Evolving Consumer Preferences

The growing popularity of smartphones with sophisticated CPUs, sharper screens, and better battery life is making gamers in Europe more numerous and more competent. Players may enjoy graphically complex and computationally intensive games on mobile devices thanks to modern smartphones' console-comparable performance. Additionally, consumer preferences are changing in favor of short-term interactive experiences, casual social gaming, and entertainment that can be enjoyed while on the go, all of which are in line with smartphone usage trends. Demand for mobile gaming material is being supported by the region's large and varied player base as well as rising average weekly playtime. Improved device accessibility across all income levels and the increasing appeal of mobile gaming among older demographics further broaden the market's growth trajectory, while cross-platform functionality and dedicated gaming modes on modern handsets continue to attract new player segments.

Supportive Regulatory Environment and Expanding Distribution Channels

The competitive dynamics of the mobile gaming ecosystem are being altered by European legislative frameworks, especially the Digital Markets Act, which requires more openness in app distribution and lowers platform gatekeeper hurdles. By allowing developers to access users through direct installations, alternative app stores, and operator-bundled distribution agreements, these legislative changes are expanding player choice and promoting a more competitive market. Beyond established platform store channels, consumers now have more access to a variety of gaming content thanks to the launch of third-party app markets on hitherto limited mobile operating systems. Together with preinstallation agreements between telecom carriers and game publishers, these legislative changes are reducing distribution costs, expanding reach, and bolstering the general development momentum of the European mobile gaming sector. Smaller publishers and independent studios are also being better equipped to compete with more established industry players thanks to more distribution options.

Market Restraints:

What Challenges the Europe Mobile Gaming Market is Facing?

Evolving Consumer Protection and Monetization Regulations

Mobile game companies are being forced to rethink their monetization strategies due to Europe's increasingly strict consumer protection rules, which might limit income creation and increase compliance expenses. The updated Consumer Rights Directive from the European Commission limits direct purchase prompts aimed at minors and requires the open disclosure of loot box chances. Furthermore, major platform providers' new App Store standards mandate spending limitations and age gating for European developers, upending long-standing engagement loops and necessitating large architectural modifications to in-app purchase systems.

Data Privacy Compliance Complexities

Mobile game developers must adhere to the guidelines set out by the General Data Protection Regulation on the collection, storage, and use of user data for tailored content delivery and targeted advertising. A significant investment in data management infrastructure, privacy-first advertising technologies, and legal supervision are required to achieve complete compliance. Smaller developers and independent studios, which might not have the means to establish thorough data governance frameworks while preserving efficient user acquisition and revenue-generating tactics, are especially challenged by these needs.

Market Saturation and Player Acquisition Costs

As download numbers plateau in established areas and competition for players' attention heats up, the European mobile gaming market is becoming increasingly saturated. 2024 saw a drop in mobile game downloads worldwide, which was indicative of a larger trend away from user acquisition and toward retention-focused tactics. Developer budgets are under increasing strain, and the sustainable expansion of up-and-coming studios is being threatened by rising cost-per-install rates in Western European markets as well as growing competition for consumer screen time from social media platforms and streaming services.

Competitive Landscape:

Established publishers, up-and-coming studios, and technological platform suppliers are engaged in fierce rivalry for player engagement and market share in the European mobile gaming sector. In order to provide smooth cross-platform experiences, companies are concentrating on expanding their game portfolios, improving monetization techniques through hybrid models, and investing in cloud gaming infrastructure. Innovation and distribution reach are being accelerated by strategic alliances between telecom companies, gadget makers, and game creators. More market openness and competitive differentiation through specialized content, sophisticated social features, and customized gaming experiences are being promoted by the regulatory environment, which has been influenced by the Digital Markets Act and consumer protection guidelines. In order to improve user retention and take advantage of the growing mobile gaming audience in the area, market participants are constantly improving their strategies.

Europe Mobile Gaming Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Types Covered | Action or Adventure, Casino, Sports and Role Playing, Strategy and Brain |

| Device Types Covered | Smartphone, Smartwatch, PDA, Tablet, Others |

| Platforms Covered | Android, iOS, Others |

| Business Models Covered | Freemium, Paid, Free, Paymium |

| Countries Covered | Germany, France, United Kingdom, Italy, Spain, Others |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Europe Mobile Gaming Market Report

The Europe mobile gaming market size was valued at USD 29.3 Billion in 2025.

The Europe mobile gaming market is expected to grow at a compound annual growth rate of 15.11% from 2026-2034 to reach USD 108.0 Billion by 2034.

Action or adventure dominated the market with a share of 35%, driven by strong consumer demand for narrative-driven, visually immersive, and skill-based gameplay experiences that offer dynamic content updates and cross-platform functionality.

Key factors driving the Europe mobile gaming market include accelerating 5G network deployment, expanding cloud gaming adoption, rising smartphone penetration, evolving consumer preferences for mobile entertainment, and supportive regulatory frameworks opening new distribution channels.

Major challenges include evolving consumer protection regulations targeting monetization practices, data privacy compliance complexities under GDPR, rising player acquisition costs in saturated Western European markets, intensifying competition for screen time, and increasing compliance burdens on developers.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)