Europe Mobile Payment Market Size, Share, Trends and Forecast by Mode of Transaction, Application, and Country, 2026-2034

Europe Mobile Payment Market Summary:

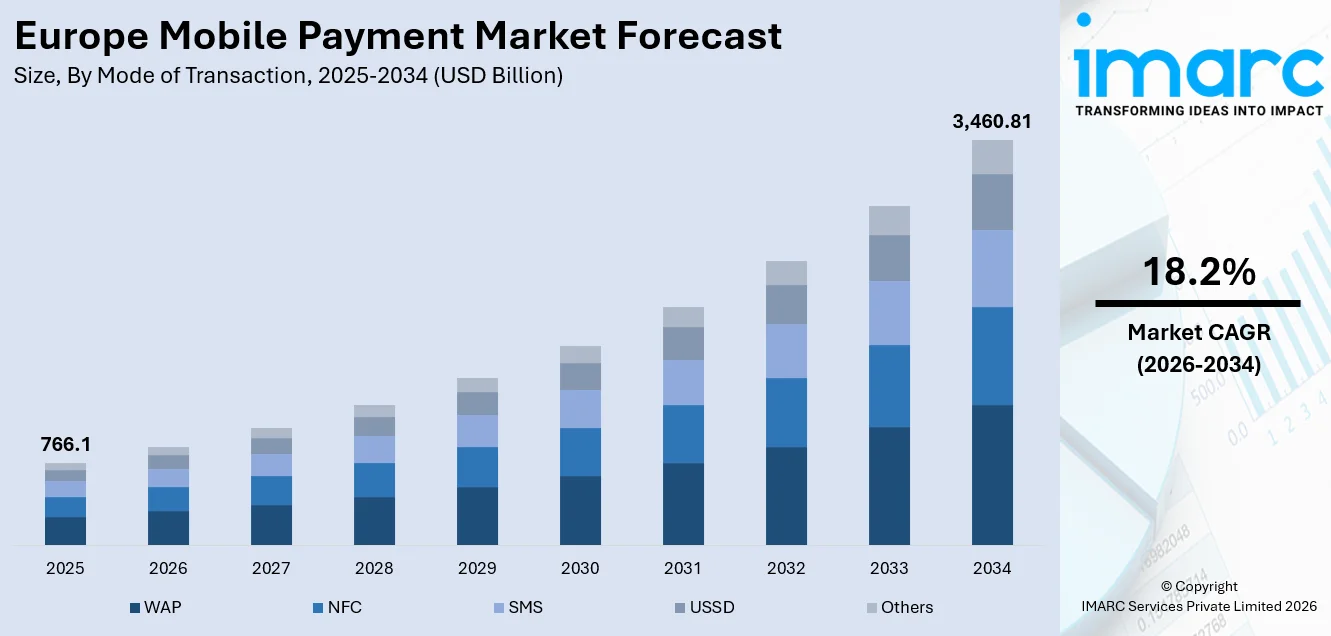

The Europe mobile payment market size was valued at USD 766.1 Billion in 2025 and is projected to reach USD 3,460.81 Billion by 2034, growing at a compound annual growth rate of 18.2% from 2026-2034.

The market for mobile payments in Europe is witnessing healthy growth as it moves closer to attaining an entirely cashless financial system. With the rise in the number of smartphones and consumers looking forward to a cashless economy, alongside the increasing adoption of contactless payments, mobile payments in Europe are significantly transforming. Open banking and Instant Payments, coupled with the growing developments in digital wallet technology and near-field communications, are also serving as catalysts and helping the market for mobile payments in Europe achieve higher market share.

Key Takeaways and Insights:

-

By Mode of Transaction: WAP dominates the market with a share of 38% in 2025, driven by the increasing reliance on mobile web-based payment gateways that offer secure connectivity across devices and enable real-time transactions across e-commerce and retail platforms.

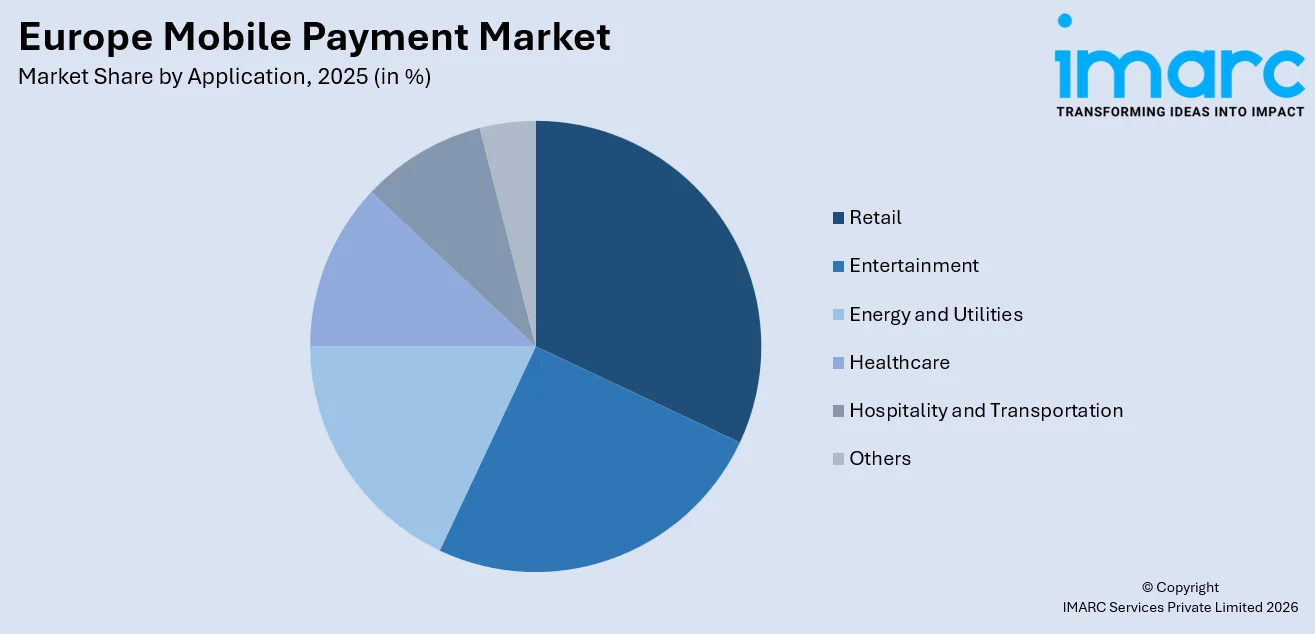

- By Application: Retail leads the market with a share of 23% in 2025, owing to widespread adoption of contactless payment technologies, expanding e-commerce penetration, and the growing demand for fast, secure, and convenient transaction experiences both in-store and online.

- Key Players: The Europe mobile payment market features intense competition among established payment processors, technology conglomerates, digital banking platforms, and emerging fintech innovators, all vying to expand their merchant networks and consumer adoption.

To get more information on this market Request Sample

The market for mobile payments in Europe is developing, considering that various governments, financial industries, and technology sectors are working towards connecting the digital payment system across the European region. In February 2026, major European payment leaders, including Bancomat, Bizum, SIBS‑MB WAY, Vipps MobilePay, and EPI Company, signed a Memorandum of Understanding to build a sovereign pan‑European interoperable payments network aimed at enabling seamless cross‑border transactions by 2027, serving around 130 million users across 13 countries, and strengthening Europe’s payment sovereignty. The focus on payment sovereignty, along with evolving interoperability, is stimulating the development and evolution of overall mobile payment solutions that can easily work across borders or countries. The evolving expectations towards payment, along with the integration of various biometric and tokenization technologies, is enhancing the level and degree of security and convenience being offered by mobile payments. The development and growth of digital wallets, along with advancements in near-field communication technologies, are facilitating the deepening use of mobile payments across various platforms such as transportation, healthcare, and hospitality services, etc. The development of account-to-account-based payment solutions along with buy-now-and-pay-later services is contributing significantly to driving more consumers towards mobile payments, developing more opportunities within the overall European mobile payment market.

Europe Mobile Payment Market Trends:

Rising Adoption of Contactless and Tap-to-Pay Solutions Across Retail Ecosystems

Contactless payment adoption is accelerating rapidly across European retail environments as merchants and consumers embrace tap-to-pay solutions enabled by near-field communication technology. For example, fintech firm Klarna recently rolled out Tap to Pay across 14 European markets, enabling its mobile wallet users to complete in‑store purchases with a simple contactless tap, helping bring digital payment acceptance deeper into physical retail settings. The widespread availability of compatible point-of-sale terminals and the integration of mobile wallets into everyday purchasing habits are transforming in-store transaction experiences, reducing checkout times and enhancing consumer convenience across the region.

Expansion of Pan-European Interoperable Digital Payment Frameworks

European institutions and payment providers are collaborating to develop cross-border interoperable mobile payment networks that facilitate seamless transactions across national boundaries. In June 2025, the European Payments Initiative (EPI) and the EuroPA Alliance, comprising mobile payment players such as Bancomat, Bizum, MB WAY/SIBS, and Vipps MobilePay, signed a landmark agreement to enable users to conduct both online and in‑store cross‑border mobile payments across 15 European countries, leveraging interoperability of domestic solutions and SEPA instant‑payment standards to serve over 380 million inhabitants. These initiatives aim to reduce reliance on external payment infrastructure while promoting sovereignty and resilience in the digital payments ecosystem, enabling consumers and merchants to transact effortlessly using their preferred mobile payment solutions throughout the continent.

Integration of Flexible Payment Options Within Mobile Wallet Platforms

Mobile wallet providers are increasingly embedding flexible financing options, including installment-based purchasing and deferred payment capabilities, directly within their platforms. For instance, in November 2025, Swedish fintech Klarna expanded its “pay later” and installment options directly into Apple Pay across several European markets, including Denmark, Spain, and Sweden, with France soon to follow, allowing eligible users to split purchases into three monthly interest‑free payments or defer payment up to 30 days right at checkout within the mobile wallet. This convergence of payment and consumer lending functionalities within a single digital interface is reshaping purchasing behaviors, enabling consumers to manage spending more transparently while providing merchants with higher conversion rates and enhanced Europe mobile payment market growth.

Market Outlook 2026-2034:

The Europe mobile payment market is set for sustained growth over the forecast period, fueled by advancing digital infrastructure, shifting consumer preferences toward seamless transactions, and regulatory frameworks promoting open banking and instant settlement. Expanding smartphone penetration, rising adoption of wearable devices, and the integration of embedded payment technologies across retail, transportation, and service industries are expected to significantly broaden market reach. Additionally, growing merchant acceptance of contactless solutions and the development of cross-border interoperable payment ecosystems are reinforcing long-term adoption across diverse European markets. The market generated a revenue of USD 766.1 Billion in 2025 and is projected to reach a revenue of USD 3,460.81 Billion by 2034, growing at a compound annual growth rate of 18.2% from 2026-2034.

Europe Mobile Payment Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Mode of Transaction |

WAP |

38% |

|

Application |

Retail |

23% |

Mode of Transaction Insights:

- WAP

- NFC

- SMS

- USSD

- Others

The WAP dominates with a market share of 38% of the total Europe mobile payment market in 2025.

The dominance of mobile payment schemes, like WAP-based mobile payments, has been evidenced through its strong presence within the European landscape of digital transactions. This is due to the provision of safe and flexible connectivity options, which allow for real-time transactions. Such a facility allows users to access payment services through mobile devices equipped with browsers, eliminating the need to access specific applications. As a result, WAP has been highly popular among e-commerce and online retail environments, where a strong need exists to cater to the requirements of multiple users seeking speed and convenience.

The prolonged usage dominance experienced by WAP transactions also finds reinforcement through this technology's capability to work well with different types of banking systems, merchant systems, and electronic wallet infrastructures that exist within different regions of Europe. Also, with increasingly improved mobile internet technology and complexities within web-based payment systems, WAP technology is allowing improved authentication, encryption, and enhanced user experience with mobile payment systems to contribute to recurring usage and increased consumer engagement with mobile payment systems across Europe.

Application Insights:

Access the comprehensive market breakdown Request Sample

- Entertainment

- Energy and Utilities

- Healthcare

- Retail

- Hospitality and Transportation

- Others

The retail leads with a share of 23% of the total Europe mobile payment market in 2025.

The retail sector has emerged as the leading application segment in the Europe mobile payment market, driven by the rapid transformation of in-store and online shopping experiences through mobile-enabled transaction technologies. The widespread deployment of contactless point-of-sale terminals, integration of digital wallets into omnichannel retail strategies, and growing consumer demand for fast and secure checkout processes are collectively reinforcing the sector’s dominant position. Retailers across the region are increasingly leveraging mobile payment capabilities to streamline operations, reduce cash handling costs, and enhance customer loyalty programs.

The expansion of e-commerce and mobile commerce across European markets has further amplified the retail segment’s reliance on mobile payment infrastructure. As consumers increasingly shop through smartphones and tablets, retailers are investing in embedded payment technologies, tokenization, and biometric verification to deliver seamless purchasing experiences. The convergence of physical and digital retail environments through unified commerce platforms is accelerating mobile payment adoption, with merchants utilizing transaction data to personalize offerings and strengthen customer engagement across diverse retail formats throughout Europe.

Country Insights:

- Germany

- France

- United Kingdom

- Italy

- Spain

- Others

Germany represents a significant market for mobile payments in Europe, supported by increasing digital wallet adoption, a robust banking infrastructure, and growing consumer willingness to shift from cash-based transactions toward mobile-enabled payment solutions. The expanding integration of contactless technologies across retail and e-commerce channels, along with rising merchant acceptance of digital payment methods, is further strengthening market momentum.

France is a key contributor to the European mobile payment landscape, driven by advanced digital banking ecosystems, high smartphone penetration, and proactive regulatory support for open banking initiatives. The seamless integration of mobile wallets across merchant networks, coupled with strong consumer preference for account-to-account transfers and contactless solutions, is accelerating adoption across both online and in-store environments.

The United Kingdom holds a prominent position in the mobile payment market, benefiting from near-universal contactless payment acceptance, a mature fintech ecosystem, and early adoption of open banking frameworks. These factors have collectively positioned the country as a leading hub for mobile payment innovation, with strong consumer engagement across digital wallets, peer-to-peer transfers, and embedded financial services.

Italy is experiencing accelerating mobile payment adoption, fueled by government mandates promoting digital transactions, expanding contactless terminal infrastructure, and increasing consumer interest in mobile wallet solutions. The regulatory push to integrate point-of-sale terminals with fiscal compliance systems is further encouraging merchants to embrace digital payment acceptance, driving broader penetration across retail and service sectors.

Spain is emerging as a dynamic mobile payment market within Europe, characterized by rapid growth in peer-to-peer payment platforms and strong adoption of domestic mobile payment solutions. The increasing integration of mobile wallets into everyday consumer transactions across retail and hospitality sectors, supported by a digitally engaged population, is reinforcing sustained market expansion.

Market Dynamics:

Growth Drivers:

Why is the Europe Mobile Payment Market Growing?

Accelerating Transition Toward Cashless Economies Supported by Regulatory Frameworks

The Europe mobile payment market is experiencing significant growth as governments and regulatory bodies across the region implement policies that encourage the transition from cash-based to digital payment ecosystems. Regulatory initiatives promoting open banking, instant payment settlement, and standardized digital transaction protocols are creating a conducive environment for mobile payment adoption. For example, from October 2025, the European Union’s Verification of Payee (VoP) mandate came into effect, requiring all euro‑denominated payments, including SEPA Instant Credit Transfers, to include real‑time name verification to reduce fraud in cross‑border and domestic digital transactions. The establishment of unified payment area frameworks that mandate real-time credit transfers and interoperable payment systems is reducing barriers to cross-border digital transactions. Central banking authorities are actively supporting the development of instant payment infrastructure that enables account-to-account transfers to settle within seconds, eliminating traditional clearing delays and enhancing consumer confidence in mobile payment solutions. These regulatory tailwinds are complemented by fiscal incentives and digital identity verification standards that simplify merchant onboarding and consumer authentication processes across the region.

Widespread Smartphone Penetration and Expanding Digital Infrastructure

The pervasive adoption of smartphones across European markets is serving as a fundamental catalyst for mobile payment expansion, as these devices increasingly function as primary instruments for financial transactions. According to data from the European Central Bank, mobile payments made with phones, smartwatches, or other connected devices accounted for about 6% of all point‑of‑sale (POS) transactions in the euro area in 2024, up from just 1% in 2019, showing a clear shift toward smartphone‑enabled payments at retail checkout points. The region’s advanced telecommunications infrastructure, characterized by extensive high-speed mobile internet coverage and growing deployment of next-generation network technologies, is enabling seamless connectivity that supports real-time payment processing. The proliferation of near-field communication-enabled devices and the integration of biometric authentication capabilities such as fingerprint scanning and facial recognition into smartphones are significantly enhancing both the security and convenience of mobile transactions.

Growing E-Commerce and Omnichannel Retail Transformation

The rapid expansion of e-commerce and the transformation of retail toward omnichannel models are powerfully driving the adoption of mobile payment solutions across European markets. The Europe e-commerce market size was valued at USD 3.96 Trillion in 2024, and it is projected to reach USD 8.46 Trillion by 2033, according to IMARC Group, highlighting the enormous scale of digital commerce growth that is directly fueling mobile payment usage. As consumers increasingly engage in online shopping through smartphones and tablets, merchants are prioritizing the integration of mobile-optimized payment gateways that deliver frictionless checkout experiences. The convergence of physical and digital retail environments through unified commerce platforms is necessitating flexible payment infrastructure that seamlessly bridges in-store and online transactions. Digital wallets and mobile payment applications are becoming essential components of the modern retail ecosystem, enabling consumers to complete purchases with minimal friction while allowing merchants to capture valuable transaction data for personalization and loyalty programs. The growing preference for one-click payments, stored credentials, and integrated financing options within mobile shopping applications is further accelerating adoption.

Market Restraints:

What Challenges the Europe Mobile Payment Market is Facing?

Persistent Consumer Attachment to Cash in Select Markets

In spite of the increasing pace of the digital payment trend, a number of markets across Europe still demonstrate high levels of consumer affinity for cash-based transactions, particularly across senior age groups and industries with a high level of tradition surrounding cash handling. This represents a significant limitation for the ultimate adoption of mobile payments across the population, as a large portion of consumers are still highly resistant to adopting digital alternatives to established forms of payment.

Regulatory Fragmentation Across National Jurisdictions

The mobile payment ecosystem faces challenges brought about by the regulatory complexities in various jurisdictions across Europe, which are fragmented and create challenges for mobile payment service providers due to differences in compliance criteria and data protection regulations. This complexity adds to the operational cost for mobile payments.

Elevated Merchant Transaction Fees for Small Businesses

The comparatively high fee structure for mobile payment processing by small and micro-merchants in various European regions makes such merchant segments less attracted to mobile payment systems as compared to traditional cash payment systems or local debit card systems due to the relatively lower financial attractiveness offered by mobile payment systems.

Competitive Landscape:

The Europe mobile payment market has a highly competitive environment, where mobile payment solutions providers, payment processor companies, technology platforms, digital banking, and fintech companies are competing for more market share in terms of various payment scenarios. The competition level is rising, and established companies are focusing on building extensive merchant acquirement networks, improving security services, and introducing innovative loyalty rewards programs. As time is passing, mobile payment market players are showing stronger trends towards more convergence between banking services and mobile payment services. Traditional banking service providers are incorporating digital wallet services and other instant transfer services extensively. Emerging mobile payment market players are continuously enhancing their services quality, reducing payment processing costs, and delivering innovative services related to underserved segments such as micro merchants and cross-border payments.

Recent Developments:

- In June 2025, Wero, the new pan‑European mobile wallet by the European Payments Initiative (EPI), has launched across major markets including Belgium, France and Germany, enabling secure, instant bank‑to‑bank money transfers and payments with just a phone number or email. The service is expanding merchant and online payment capabilities as adoption grows.

Europe Mobile Payment Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Mode of Transactions Covered | WAP, NFC, SMS, USSD, Others |

| Applications Covered | Entertainment, Energy and Utilities, Healthcare, Retail, Hospitality and Transportation, Others |

| Countries Covered | Germany, France, United Kingdom, Italy, Spain, Others |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Europe Mobile Payment Market Report

The Europe mobile payment market size was valued at USD 766.1 Billion in 2025.

The Europe mobile payment market is expected to grow at a compound annual growth rate of 18.2% from 2026-2034 to reach USD 3,460.81 Billion by 2034.

WAP, holding the largest share of 38%, remains pivotal for Europe’s mobile payment adoption, enabling secure web-based transactions across devices and seamless real-time payment processing across

Key factors driving the Europe mobile payment market include regulatory support for cashless economies, rising smartphone penetration, expanding e-commerce activity, growing adoption of contactless technologies, open banking initiatives, and increasing consumer demand for convenient digital transaction solutions.

Major challenges include persistent cash preference in select markets, regulatory fragmentation across national jurisdictions, elevated merchant processing fees for small businesses, data privacy and cybersecurity concerns, and uneven digital infrastructure development across different European regions.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade