Europe Organic Food Market Size, Share, Trends and Forecast by Product Type, Distribution Channel, Application, and Country, 2026-2034

Europe Organic Food Market Size, Share, Trends & Forecast (2026-2034)

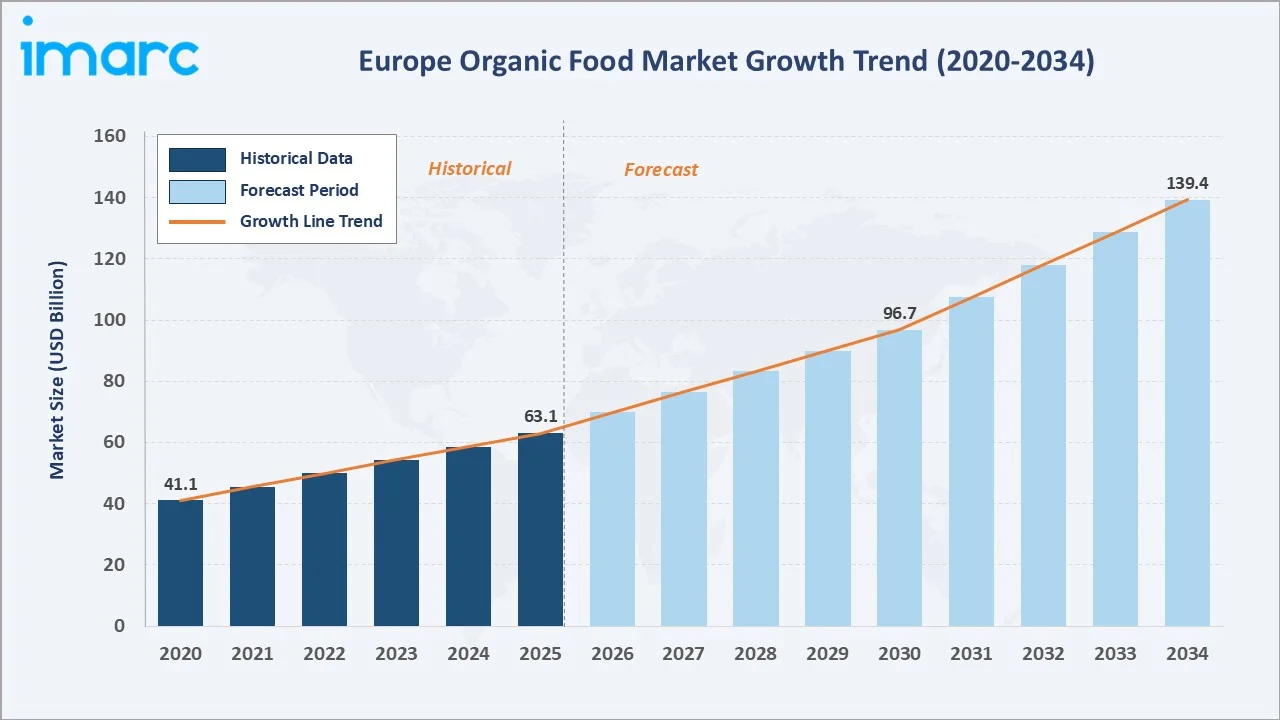

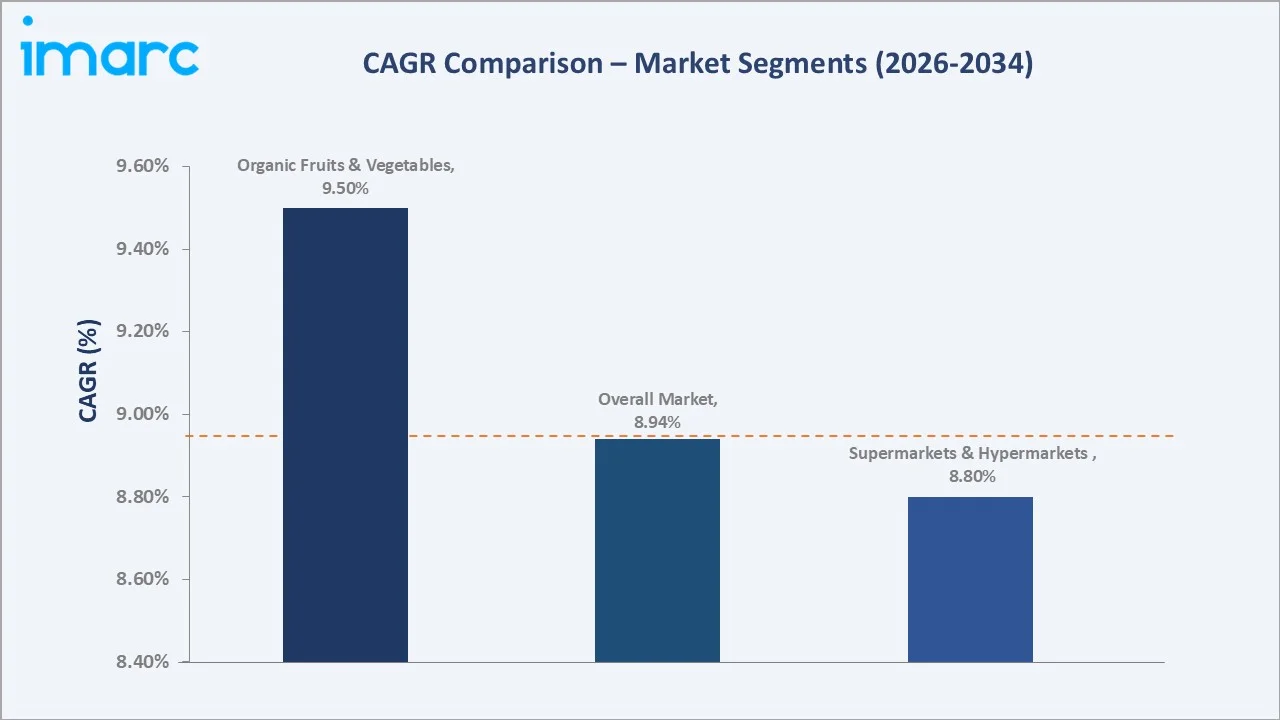

The Europe organic food market reached USD 63.1 Billion in 2025 and is projected to reach USD 139.4 Billion by 2034, growing at a CAGR of 8.94% during 2026-2034. Rising consumer demand for sustainable products, heightened health consciousness, supportive EU regulatory frameworks, and the mainstreaming of organic food across major retail channels are key growth drivers.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 63.1 Billion |

|

Forecast Market Size (2034) |

USD 139.4 Billion |

|

CAGR (2026-2034) |

8.94% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Country |

Germany (22.4% share, 2025) |

|

Fastest Growing Country |

Spain |

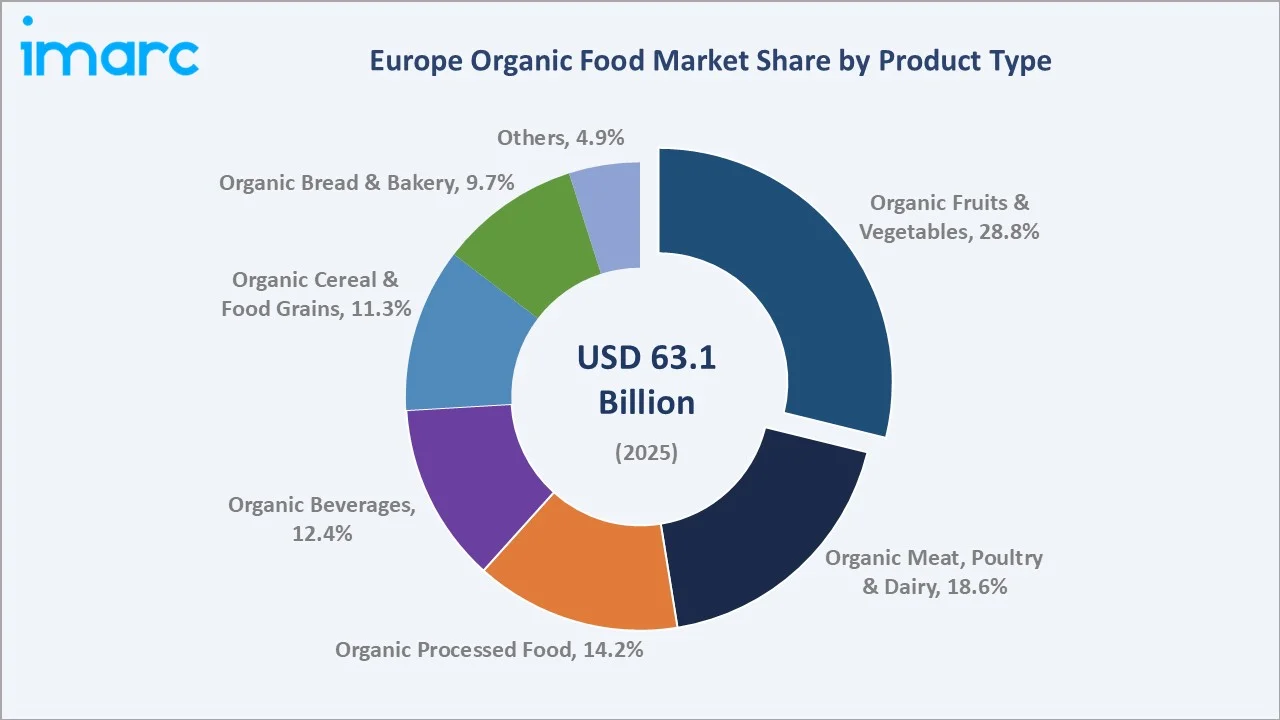

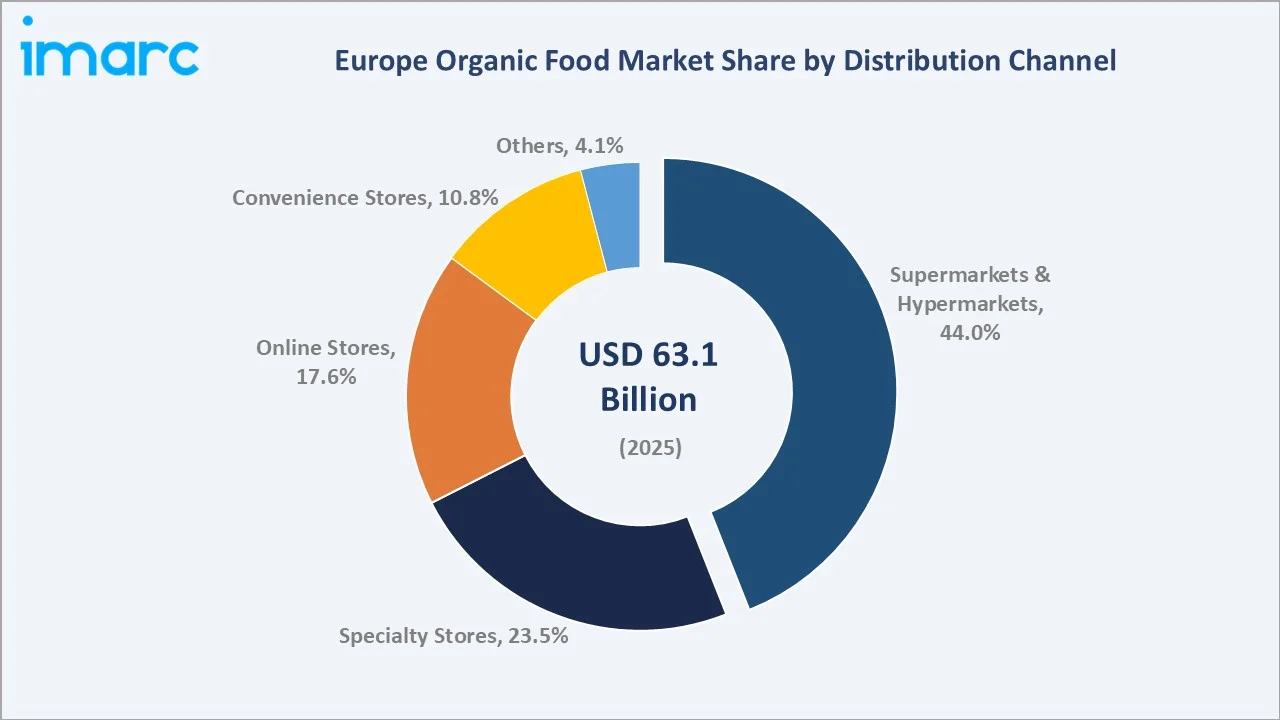

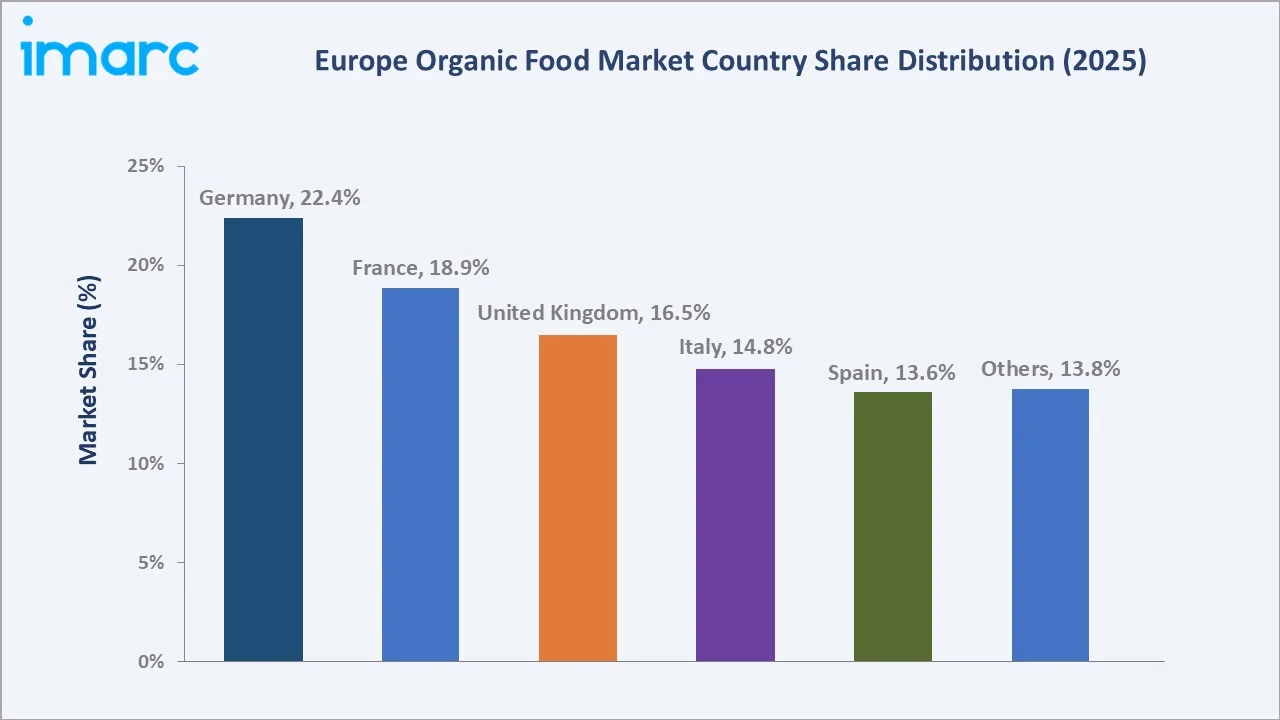

Germany dominates, holding a 22.4% market share in 2025, while organic fruits and vegetables lead product type demand at 28.8%. Supermarkets and hypermarkets remain the dominant distribution channel with a 44.0% share. Organic food offers consumers a credible pathway to healthier, chemical-free nutrition while aligning with broader sustainability values, making it a preferred choice across European households, food service operators, and institutional buyers.

To get more information on this market, Request Sample

With product categories spanning organic produce, dairy, meat, beverages, cereals, and processed foods, the market is expected to continue expanding, supported by innovations in organic farming technology, expansion of certified supply chains, and increasing mainstream retail and e-commerce penetration across all European sub-markets.

Executive Summary

The Europe organic food market is on a sustained growth path, underpinned by rising consumer health awareness, the expansion of certified organic farming infrastructure, and the proliferation of organic product ranges across both specialist and mainstream retail formats throughout the region. The market reached USD 63.1 Billion in 2025 and is forecast to surpass USD 139.4 Billion by 2034, reflecting a healthy CAGR of 8.94% over the forecast period.

Germany leads with a 22.4% revenue share in 2025, driven by an established organic culture, government subsidies for organic conversion, and extensive retail availability of certified products. France (18.9%) is supported by the government's Ambition Bio 2027 program, while the United Kingdom (16.5%) benefits from strong Soil Association certification recognition and rapidly expanding online organic grocery channels.

Organic fruits and vegetables command the largest product segment at 28.8% in 2025, followed by organic meat, poultry, and dairy at 18.6%. Supermarkets and hypermarkets lead distribution at 44.0%, reflecting the successful mainstreaming of organic ranges by major European grocery groups. Leading market participants continue to invest in sustainable packaging, blockchain-based traceability, and product innovation to align with consumer expectations and tightening EU environmental standards.

Key Market Insights

|

Insight |

Data |

|

Largest Segment (Product Type) |

Organic Fruits & Vegetables – 28.8% share (2025) |

|

Largest Distribution Channel |

Supermarkets & Hypermarkets – 44.0% share (2025) |

|

Leading Country |

Germany – 22.4% revenue share (2025) |

|

Fastest Growing Country |

Spain (organic farmland expansion + domestic demand growth) |

|

Top Companies |

Alnatura Produktions- und Handels GmbH, REWE Group, Carrefour, Windmill Organics, dm-drogerie markt GmbH + Co. KG, and Waitrose & Partners |

|

Market Opportunity |

Online organic food retail projected at USD 24.5 Billion by 2034 |

Key Analytical Observations Supporting the Above Data:

- Organic fruits and vegetables account for 28.8% of the European organic food market in 2025, preferred by health-conscious consumers for their non-GMO, pesticide-free attributes and alignment with plant-based diet adoption trends.

- Supermarkets and hypermarkets dominate distribution at 44.0% (2025), driven by strategic organic product placement, private-label organic ranges, and broad geographic reach across urban and suburban consumer segments.

- Germany holds 22.4% of the European organic food market in 2025, supported by an advanced certification ecosystem, approximately 35,881 farms operating under organic farming standards, and one of Europe's highest per-capita organic food expenditure rates.

- Spain is emerging as a faster-growing market, driven by its status as Europe's largest organic agricultural area by hectare and rapidly increasing domestic organic consumption alongside its traditionally export-oriented model.

- E-commerce is reshaping organic food distribution, with online organic grocery sales in Europe growing rapidly as subscription-based delivery models and specialized platforms gain mainstream consumer adoption.

Europe Organic Food Market Overview

Organic food encompasses agricultural goods cultivated and processed without synthetic fertilizers, pesticides, artificial additives, or genetically modified organisms. The European organic food market ecosystem spans certified organic farmers, processing and manufacturing facilities, certification bodies, wholesale distributors, specialist organic retailers, mainstream grocery chains, and e-commerce platforms.

Europe has long been the global leader in organic food consumption, supported by a dense regulatory framework anchored in EU Regulation 2018/848, which entered full effect in 2022, establishing comprehensive standards for organic production, labeling, and controls across all member states.

Macroeconomic factors driving the market include rising per capita disposable incomes, growing urbanization, increasing awareness of the health consequences of pesticide-laden conventional diets, and policy alignment with the European Green Deal and Farm to Fork Strategy, which aims to have at least 25% of EU agricultural land under organic farming by 2030.

The organic food value chain in Europe is increasingly characterized by direct integration between certified growers and major retail chains, investments in agri-technology to improve organic yield efficiency, and growing corporate commitments to sustainability-linked procurement standards.

Market Dynamics

To evaluate market opportunities, Request Sample

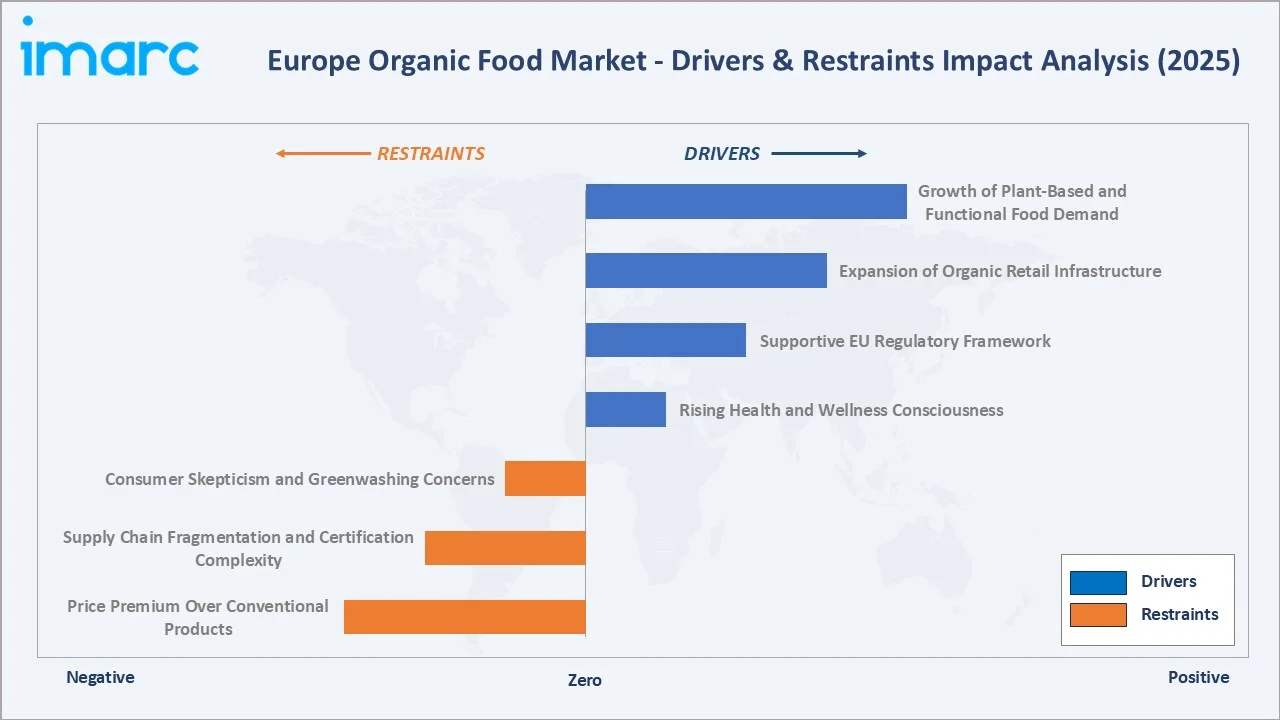

Market Drivers

- Rising Health and Wellness Consciousness: Consumer awareness of the health risks associated with synthetic pesticides, chemical preservatives, and GMO ingredients is accelerating the structural shift toward certified organic food products across all European demographic segments.

- Supportive EU Regulatory Framework: The implementation of EU Regulation 2018/848 and the Farm to Fork Strategy, committing to 25% organic agricultural land by 2030, provides enduring structural demand support.

- Expansion of Organic Retail Infrastructure: The proliferation of dedicated organic aisles within mainstream supermarket chains, alongside rapid growth of specialty organic retail formats and e-commerce platforms, has dramatically increased product accessibility across European consumer income brackets.

- Growth of Plant-Based and Functional Food Demand: Accelerating adoption of plant-based diets across Europe, combined with growing interest in functional foods enriched with vitamins, probiotics, and adaptogens, has significantly expanded the addressable market for organic food producers, creating powerful cross-category demand synergies.

Market Restraints

- Price Premium Over Conventional Products: Certified organic food products typically command a 50-75% price premium over conventional equivalents, limiting mass-market penetration among lower-income consumer segments and price-sensitive households, particularly in Southern and Eastern European markets.

- Supply Chain Fragmentation and Certification Complexity: Maintaining organic certification across complex, multi-country European supply chains involves a significant administrative and financial burden. Smallholder producers face disproportionate certification costs that constrain supply-side scalability and geographic diversity of organic supply.

- Consumer Skepticism and Greenwashing Concerns: Inconsistent labeling standards and publicized incidents of fraudulent organic certification have eroded consumer trust in some markets, requiring sustained investment in supply chain traceability and independent regulatory enforcement to maintain category credibility.

Market Opportunities

- E-Commerce and Direct-to-Consumer Expansion: Digital platforms are fundamentally transforming organic food distribution. Subscription-based organic delivery services, farm-to-doorstep platforms, and mobile-first grocery applications have opened new addressable consumer segments, particularly among time-constrained urban professionals across Northern and Western Europe.

- Organic Private Label Growth: Major European retailers are rapidly expanding proprietary organic label ranges, offering consumers certified organic products at reduced price premiums. This strategy is accelerating mainstream adoption and reducing the price barrier that has historically constrained organic category growth into mid-income household segments.

- Emerging Demand in Eastern Europe: Countries including Poland, the Czech Republic, Romania, and Hungary represent significant untapped growth opportunities as rising incomes and growing health awareness align with the well-established Western European organic consumption model, creating high-potential new market frontiers.

Market Challenges

- Climate Variability and Yield Uncertainty: Organic farming's prohibition on synthetic inputs makes crop yields more susceptible to climate-driven disruptions, including droughts, flooding events, and pest pressures, introducing supply-side volatility that complicates long-term pricing stability and inventory planning for retailers and manufacturers.

- Regulatory Divergence Post-Brexit: The United Kingdom's departure from the EU organic regulatory framework has created dual compliance requirements for producers supplying both EU and UK markets, increasing administrative costs and operational complexity for cross-border participants in the organic supply chain.

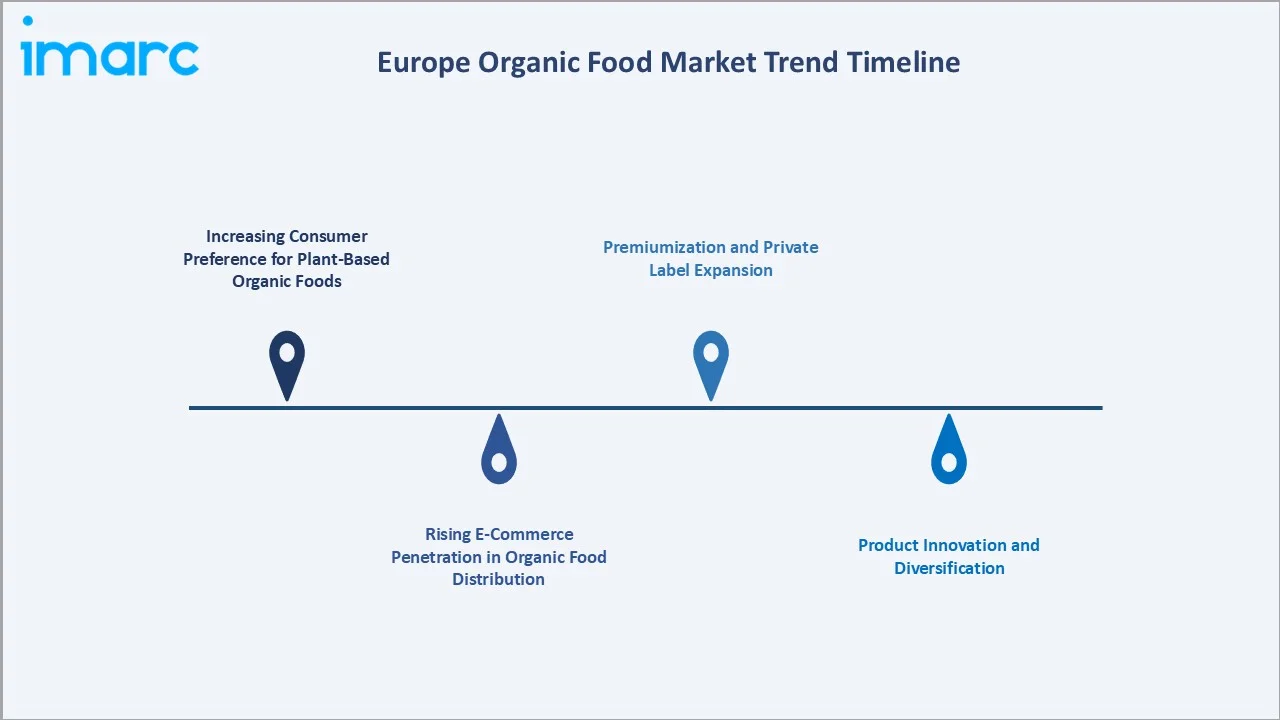

Emerging Market Trends

1. Increasing Consumer Preference for Plant-Based Organic Foods

In December 2024, the European innovation project Delicious, backed by Horizon Europe with EUR 5 million, launched in Barcelona to revolutionize plant-based dairy using microbial fermentation and machine learning for sustainable, nutritious alternatives. Aligned with a plant-based food market projected to reach €40 billion by 2027, the initiative aims to cut dairy production emissions by up to 30% while accelerating the shift toward sustainable diets in Europe.

2. Rising E-Commerce Penetration in Organic Food Distribution

The rapid expansion of digital grocery infrastructure, combined with heightened post-pandemic comfort with online food purchasing, has made organic food more accessible to geographically dispersed consumer segments. Subscription-based organic delivery services, farm-to-doorstep platforms offering curated seasonal produce, and mainstream online grocery channels have collectively lowered barriers to the trial and repeat purchase of organic food.

3. Product Innovation and Diversification

Organic beverages, including cold-pressed juices, kombucha, botanical waters, and plant-based milk alternatives, have posted strong growth. In September 2024, Marigold Health Foods and Sonoco introduced a fully recyclable can composed of 95% paper and 60% recycled fiber, setting a new benchmark for sustainable organic food packaging. This commitment to continuous innovation drives both new consumer acquisition and retention, supporting sustained market growth.

4. Premiumization and Private Label Expansion

Major European grocery retailers are expanding their private-label organic ranges, bringing certified organic products within reach of mainstream shoppers at significantly reduced price premiums compared to branded alternatives. In February 2024, Alnatura announced the launch of a complete range of organic pasture milk products, including cream fraiche, yogurt, and fresh milk, with expansion planned to over 30 products, setting a new commercial benchmark for organic dairy quality standards in Germany.

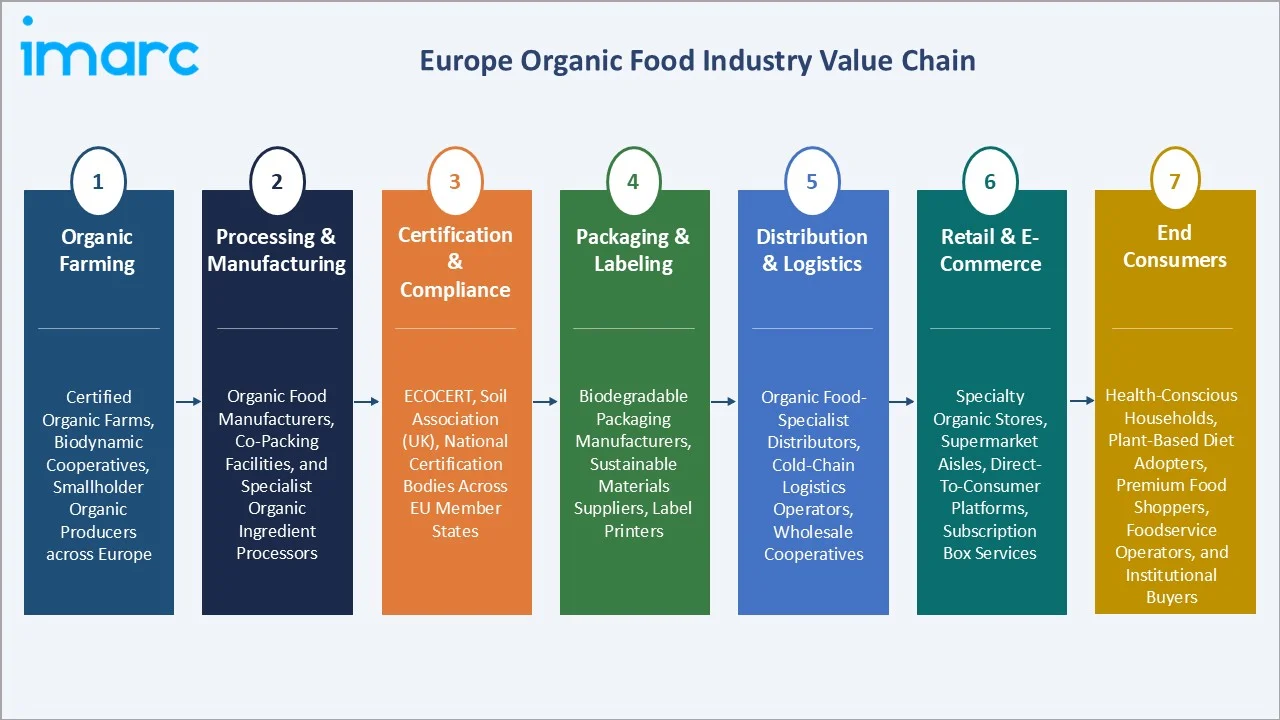

Industry Value Chain Analysis

The Europe organic food value chain spans certified raw material production through end-consumer purchase, with each stage populated by specialized operators whose performance directly influences product quality, sustainability credentials, and final retail price positioning. The integration between these stages is increasingly characterized by direct sourcing agreements, cooperative farming models, and digital traceability platforms.

|

Stage |

Key Participants / Examples |

|

Organic Farming |

Certified organic farms, biodynamic cooperatives, and smallholder organic producers across Germany, France, Italy, and Spain |

|

Processing & Manufacturing |

Organic food manufacturers, co-packing facilities with organic certification, and specialist organic ingredient processors |

|

Certification & Compliance |

ECOCERT, Soil Association (UK), and national certification bodies across EU member states |

|

Packaging & Labeling |

Biodegradable packaging manufacturers, sustainable materials suppliers, and label printers meeting organic and clean-label requirements |

|

Distribution & Logistics |

Organic food-specialist distributors, cold-chain logistics operators, and organic wholesale cooperatives |

|

Retail & E-Commerce |

Specialty organic stores, supermarket organic aisles, direct-to-consumer platforms, subscription box services |

|

End Consumers |

Health-conscious households, plant-based diet adopters, premium food shoppers, foodservice operators, and institutional buyers |

Technology Landscape in the Europe Organic Food Industry

Precision Organic Farming Technology

Remote sensing via satellite and drone platforms provides real-time crop health monitoring, while AI-driven soil analytics optimize natural fertilization and irrigation scheduling. Precision organic farming adoption grew approximately 28% in 2024 across Western European markets, with cost premiums over conventional precision farming declining as technology scales across the organic farming community.

Blockchain-Based Supply Chain Traceability

Distributed ledger platforms allow consumers and regulators to verify the provenance of organic products at any point in the supply chain, from a certified farm of origin through processing, certification, and retail. Several European retailers and certification bodies deployed blockchain traceability pilots in 2024, targeting full-chain transparency on high-value organic produce categories by 2026, directly addressing consumer skepticism around organic certification authenticity.

Smart Cold Chain and Logistics Innovation

Real-time temperature and humidity monitoring across storage and transport stages reduces organic food waste, a key sustainability metric for organic brands. Smart cold chain adoption is growing particularly strongly in the organic dairy, meat, and fresh produce categories, where maintaining certification integrity through the distribution chain is paramount.

Sustainable Packaging Innovation

Compostable, biodegradable, and reusable packaging formats are gaining commercial scale, with cost premiums declining from approximately 35% to 15% over 2020–2024 as production volumes increase. In September 2024, Marigold Health Foods and Sonoco introduced a fully recyclable can comprising 95% paper and 60% recycled fiber, establishing a new benchmark for sustainable organic food packaging across the European market.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Product Type | Organic Fruits and Vegetables | 28.8% | 2025 |

| Distribution Channel | Supermarkets and Hypermarkets | 44.0% | 2025 |

| Application | 🔒 | 🔒 | 2025 |

| Country | Germany | 22.4% | 2025 |

By Product Type

Organic fruits and vegetables dominate the product type segment with a 28.8% share in 2025. This leading position reflects the category's long-established consumer appeal as the most intuitive entry point into organic food purchasing, strongly supported by widespread awareness of pesticide residue risks in conventionally farmed produce and the accelerating adoption of plant-based dietary patterns across European markets.

To access detailed market analysis, Request Sample

Organic meat, poultry, and dairy holds 18.6%, driven by consumer concern over antibiotic use and animal welfare in conventional livestock production. Organic processed food accounts for 14.2%, growing as manufacturers reformulate mainstream convenience products with organic-certified ingredients. Organic beverages (12.4%) are among the fastest-growing sub-segments, with cold-pressed juices, kombucha, and plant-based milk driving premium consumption occasions.

By Distribution Channel

Supermarkets and hypermarkets lead distribution with a commanding 44.0% share in 2025. This dominance reflects strategic decisions by Europe's largest grocery retailers to position organic food as a mainstream category, through expanded organic assortments, private-label organic ranges at competitive price points, and prominent in-store positioning.

Specialty stores represent the second-largest channel at 23.5%, serving the most engaged organic consumer segment that prioritizes product provenance, certification transparency, and specialist product knowledge. Online stores have grown to 17.6% of distribution, driven by accelerating e-commerce adoption post-pandemic and the emergence of specialist organic delivery platforms and subscription box services that offer curated organic assortments with doorstep delivery.

Regional Market Insights

Germany's market leadership (22.4%, 2025) reflects decades of investment in organic farming infrastructure, a highly developed certification ecosystem, and one of the highest per-capita organic food expenditure rates globally. Organic sales in the country reached a record EUR 17 billion (USD 20.14 billion) in 2024, marking a 5.7% increase compared to the previous year.

|

Country |

Share (2025) |

Key Growth Drivers |

|

Germany |

22.4% |

Organic culture, premium retail, govt farm subsidies |

|

France |

18.9% |

Ambition Bio 2027 program; local sourcing preference; agri-tourism |

|

United Kingdom |

16.5% |

Post-Brexit sustainability focus; online organic grocery growth |

|

Italy |

14.8% |

Largest EU organic farmland area; strong agri-food heritage; tourism |

|

Spain |

13.6% |

Largest organic area by hectare; rising domestic demand; tourism sector |

|

Others |

13.8% |

Netherlands, Switzerland, Austria, Poland – rising organic consumption |

France (18.9%) has undergone one of the fastest organic farming expansion trajectories in Europe, supported by the Ambition Bio 2027 plan with 27 measures to boost organic production and consumption, targeting 18% of farmland under organic cultivation by 2027. The United Kingdom (16.5%) has maintained strong momentum despite post-Brexit regulatory divergence, supported by Soil Association recognition and accelerating online organic grocery adoption.

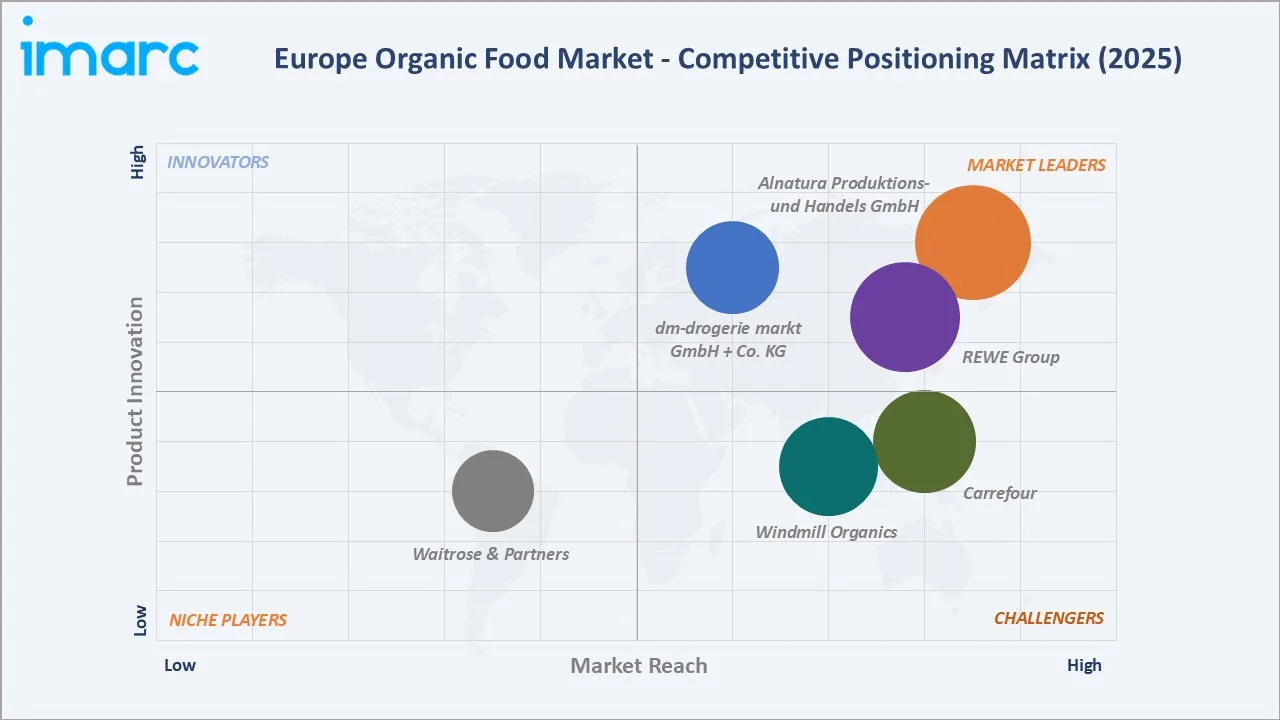

Competitive Landscape

The Europe organic food market exhibits a moderately fragmented competitive structure. The top five participants, Alnatura Produktions- und Handels GmbH, REWE Group, Carrefour, Windmill Organics, and dm-drogerie markt GmbH + Co. KG, collectively hold approximately 22–26% of European organic food retail revenue in 2025. Specialist organic chains, retailer-owned private-label brands, and regional organic cooperatives account for the balance, ensuring a diverse and competitive landscape across product categories and geographies.

|

Company Name |

Brand Name |

Market Position |

Core Strength |

|

Alnatura Produktions- und Handels GmbH |

Alnatura |

Market Leader |

Germany's leading organic supermarket chain, vertically integrated from farm to shelf, with 1,300 own-brand certified organic SKUs |

|

REWE Group |

REWE Bio |

Market Leader |

Pan-German organic private label with 1k+ certified products; extensive distribution through 3,800+ REWE stores |

|

Carrefour |

Carrefour Bio |

Strong Challenger |

Pan-European organic private label; strong in-store placement and digital channel integration across France and Southern Europe |

|

Windmill Organics |

Biona Organic |

Strong Challenger |

UK's leading organic branded manufacturer; 400+ certified products with strength in bread, bakery, pantry staples, and condiments |

|

dm-drogerie markt GmbH + Co. KG |

dm Bio |

Leader |

Health and beauty retailer dm's organic food label; accessible price positioning widely distributed across DACH and CEE markets |

|

Waitrose & Partners |

Waitrose Duchy Organic |

Niche Player |

Premium UK organic brand under royal warrant; rigorous animal welfare standards and premium positioning in grocery retail |

Market consolidation is gradually accelerating as large food and beverage groups acquire established organic brands to quickly access certified supply chains, loyal consumer bases, and premium category positioning. E-commerce has meaningfully disrupted traditional competitive dynamics by enabling smaller organic producers to access pan-European consumer audiences without requiring large-scale retail distribution agreements.

Key Company Profiles

Alnatura Produktions- und Handels GmbH

Alnatura, headquartered in Germany, is one of Europe's leading specialist organic supermarket chains and a fully integrated organic food company, operating over 150 organic supermarkets across Germany.

- Product Portfolio: Full-spectrum certified organic products including dairy, bakery, fresh produce, beverages, baby food, and personal care items across Alnatura-branded and private-label formats.

- Recent Developments: In February 2024, Alnatura became the first brand to offer a complete range of organic pasture milk products from a single source, converting its core dairy lineup to this standard and expanding from six products to over 30 by mid-2024.

- Strategic Focus: Vertical integration expansion; investment in regenerative organic farming partnerships; digital commerce channel development; sustainable packaging transition program.

REWE Group

REWE Group, headquartered in Cologne, Germany, operates one of Europe's largest food retail networks with over 3,800 REWE stores across Germany and over 1,300+ BILLA stores in Austria, both part of REWE Group. The company's REWE Bio private label is one of the most widely recognized organic food brands in the German-speaking market.

- Product Portfolio: Over 600 certified organic products spanning fresh produce, dairy, meat, bakery, beverages, frozen foods, and pantry staples under the REWE Bio label.

- Recent Developments: In December 2025, REWE partnered with Bioland, Germany’s largest organic farming association, to expand its range of certified organic products, particularly locally sourced fresh items such as fruits, vegetables, and dairy.

- Strategic Focus: Private-label organic expansion; sustainability certification programs across the supplier base; digital grocery platform integration for online organic ordering; supplier partnership programs supporting organic conversion.

Windmill Organics

Windmill Organics, headquartered in the United Kingdom, is one of Europe's leading branded organic food manufacturers, offering over 400 certified organic products across bakery, bread, condiments, pasta, beverages, and specialty food categories.

- Product Portfolio: Organic bread, bakery products, condiments, pasta, beverages, and health food staples with Soil Association certification and non-GMO verification.

- Recent Developments: Biona, a brand under Windmill Organics, launched its Organic Super Seed Bread in September 2024, a protein-rich sliced loaf containing sunflower, flax, and pumpkin seeds, targeting demand for nutritious, minimally processed bakery products.

- Strategic Focus: Product innovation in clean-label organic categories; expansion of foodservice organic supply; digital channel growth; sustainable packaging transition.

Market Concentration Analysis

The Europe organic food market exhibits moderate concentration at the branded and private-label retail level, with the top five participants collectively holding approximately 22–26% of total organic food retail revenue in 2025. However, a substantial long tail of regional and national organic food brands, certified cooperatives, farm-direct operators, and specialist importers ensures significant market fragmentation below the leading-player tier, particularly across Southern and Eastern European markets.

Consolidation activity is gradually accelerating, driven by the scale advantages available to vertically integrated organic retailers, the certification compliance costs that favor larger supply chain participants, and the growing investment by mainstream food and beverage groups in organic brand acquisitions to access the premium category. Between 2020 and 2025, several notable M&A transactions reshaped the European organic food landscape, including acquisitions of regional organic brands by major grocery retail groups.

Investment & Growth Opportunities

Fastest Growing Segments

Organic plant-based beverages (estimated CAGR 11.2%), organic functional foods enriched with probiotics and vitamins (9.8% CAGR), and organic convenience ready-to-eat meals (10.5% CAGR) represent the three highest-growth investment vectors in the European organic food market through 2034. Together, these sub-segments address a total addressable market of approximately USD 18 billion by 2030, driven by converging consumer health, convenience, and sustainability trends.

Emerging Market Expansion

Eastern Europe and the Scandinavian markets collectively represent an incremental USD 12 billion organic food opportunity by 2034. Poland, the Czech Republic, and Romania are experiencing rapidly rising organic food demand as income levels increase and health awareness grows among urban consumer segments. Entry via joint ventures with established local food distributors, alignment with national organic farming support programs, and targeted digital marketing to younger urban demographics are the preferred market entry modalities for international organic food brands.

Venture and Institutional Investment Trends

- Key investment themes include blockchain-based organic supply chain traceability platforms, precision organic farming technology, biodegradable and compostable organic food packaging, and direct-to-consumer organic subscription models.

- Family offices and private equity firms are targeting vertical integration plays, consolidating certified organic farming, processing, distribution, and branded retail into single platform companies to capture margin across the organic food value chain.

- Impact investors are increasingly targeting organic farming conversion financing, providing capital to conventional farmers undertaking the 2–3 year transition to full organic certification, addressing a key supply-side bottleneck in the European organic food market.

Future Market Outlook (2026-2034)

The Europe organic food market is positioned for sustained, broad-based growth through 2034. From a base of USD 63.1 Billion in 2025, the market is projected to reach USD 139.4 Billion by 2034, representing total incremental value creation of USD 76.3 Billion over the forecast decade at a CAGR of 8.94%.

Regulatory evolution, particularly the EU Farm to Fork Strategy's 25% organic farmland target by 2030 and the stricter organic compliance standards effective from 2025, will drive meaningful structural changes in both supply capacity and consumer demand dynamics. Producers achieving full regulatory compliance, verifiable supply chain traceability, and strong environmental credentials will capture a disproportionate share of the institutional and premium consumer procurement growth anticipated through 2034.

Long-term, the market's trajectory is aligned with three enduring structural themes: growing health consciousness driving premiumization of everyday food purchasing decisions; an accelerating regulatory and corporate sustainability agenda reinforcing organic food's environmental positioning; and the continued mainstreaming of organic food through digital commerce platforms and mainstream retail private-label expansion.

Research Methodology

Primary Research

Primary research for this report comprised structured interviews and surveys with over 120 industry participants during 2024–2025, including certified organic food producers, retail procurement managers, specialist organic retail operators, e-commerce platform executives, certification body representatives, and food policy experts across Germany, France, the United Kingdom, Italy, and Spain.

Secondary Research

Secondary research encompassed a systematic review of company annual reports, EU regulatory publications, European Commission Farm to Fork Strategy documentation, IFOAM Organics Europe market statistics, Euromonitor organic food data, trade publications, and publicly available agricultural and retail statistical data from national statistics bureaus and EU-level bodies. Over 220 secondary sources were reviewed and triangulated.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting approaches, incorporating macroeconomic indicators, organic farmland conversion rates, per-capita organic food expenditure trends, retail sales data, and historical market evolution. A base-case CAGR of 8.94% reflects consensus estimates validated against reported organic food retail sales data across key European country markets.

Europe Organic Food Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Organic Fruits and Vegetables, Organic Meat, Poultry and Dairy, Organic Processed Food, Organic Bread and Bakery, Organic Beverages, Organic Cereal and Food Grains, Others |

| Distribution Channels Covered | Supermarkets and Hypermarkets, Specialty Stores, Convenience Stores, Online Stores, Others |

| Applications Covered | Bakery and Confectionery, Ready-to-eat Food Products, Breakfast Cereals, Others |

| Countries Covered | Germany, France, United Kingdom, Italy, Spain, Others. |

| Companies Covered | Alnatura Produktions- und Handels GmbH, REWE Group, Carrefour, Windmill Organics, dm-drogerie markt GmbH + Co. KG, Waitrose & Partners, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Europe organic food market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the Europe organic food market.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Europe organic food industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Europe Organic Food Market Report

The Europe organic food market reached USD 63.1 Billion in 2025. It is projected to reach USD 139.4 Billion by 2034.

The Europe organic food market is expected to grow at a CAGR of 8.94% during the forecast period from 2026-2034, supported by consistent demand growth across all product and distribution channel segments.

Germany leads the market with a 22.4% revenue share in 2025, driven by an established organic consumer culture, a highly developed certification ecosystem, extensive retail availability of certified organic products, and one of Europe's highest per-capita organic food expenditure rates.

Organic fruits and vegetables dominate the product type segment with a 28.8% share in 2025, valued at approximately USD 18.2 Billion. Its dominance is driven by strong consumer preference for pesticide-free, non-GMO fresh produce and the accelerating adoption of plant-based diets across Europe.

Supermarkets and hypermarkets hold the largest distribution channel share at 44.0% in 2025, driven by the strategic expansion of organic product assortments, private-label organic ranges, and mainstream grocery retail accessibility across urban and suburban European markets.

Key players include Alnatura Produktions- und Handels GmbH, REWE Group, Carrefour, Windmill Organics, dm-drogerie markt GmbH + Co. KG, and Waitrose & Partners, among other regional organic brands and certified cooperatives.

E-commerce platforms are increasingly central to organic food distribution across Europe, particularly for residential and urban consumer segments. Online organic grocery channels, subscription delivery services, and farm-to-doorstep platforms collectively represent 17.6% of European organic food distribution in 2025, with this share growing rapidly as consumer comfort with digital grocery channels increases.

Key challenges include the persistent 20–60% price premium of organic over conventional food products, supply chain fragmentation and certification complexity, consumer skepticism around greenwashing, climate variability impacting organic crop yields, and post-Brexit regulatory divergence creating dual compliance requirements for cross-border operators.

Significant opportunities exist in organic plant-based beverages and functional foods, direct-to-consumer digital platforms, Eastern European organic market expansion, blockchain-based traceability technology, sustainable organic packaging innovation, and organic farming conversion financing. The market is projected to create USD 76.3 Billion in incremental value between 2025 and 2034.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade