Europe Payment Gateways Market Size, Share, Trends and Forecast by Application, Mode of Interaction, and Country, 2026-2034

Europe Payment Gateways Market Summary:

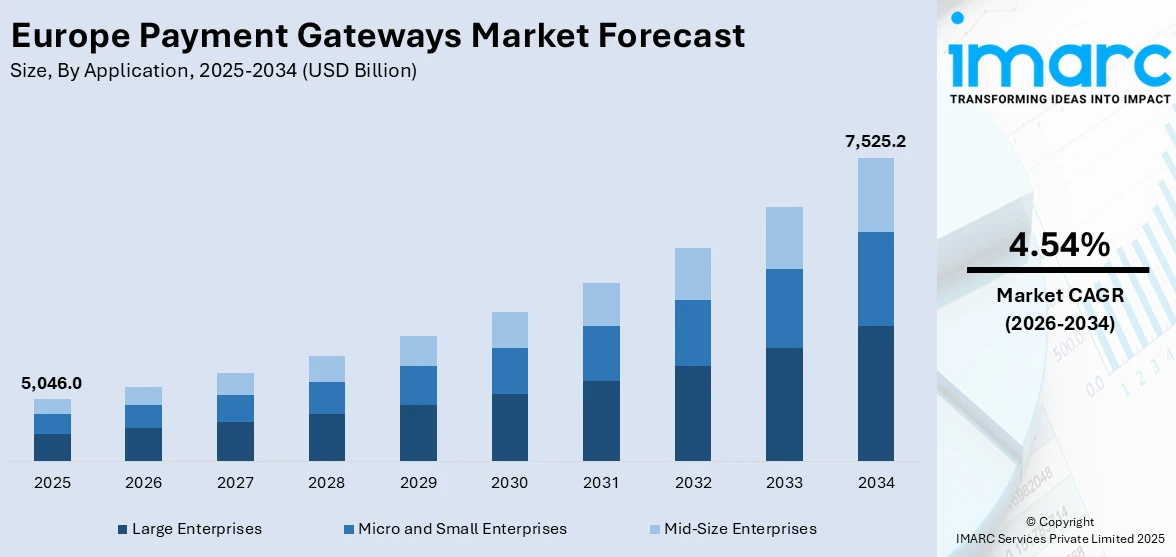

The Europe payment gateways market size was valued at USD 5,045.99 Billion in 2025 and is projected to reach USD 7,525.21 Billion by 2034, growing at a compound annual growth rate of 4.54% from 2026-2034.

The Europe payment gateways market is expanding as the region accelerates its shift from cash-based transactions toward digital and contactless payment ecosystems. Growing e-commerce penetration, rising mobile wallet adoption, and the implementation of regulatory frameworks promoting open banking and instant payments are reinforcing demand. Advancements in artificial intelligence-driven fraud prevention, tokenization technologies, and seamless cross-border payment capabilities are reshaping merchant and consumer expectations. Furthermore, the integration of payment gateways with enterprise resource planning systems, point-of-sale platforms, and omnichannel retail strategies is strengthening the Europe payment gateways market share.

Key Takeaways and Insights:

- By Application: Large enterprises dominate the market with a share of 45% in 2025, owing to their need for robust, scalable payment processing capable of handling high transaction volumes across multiple currencies and regions. Complex checkout requirements and stringent security demands further reinforce enterprise-level adoption.

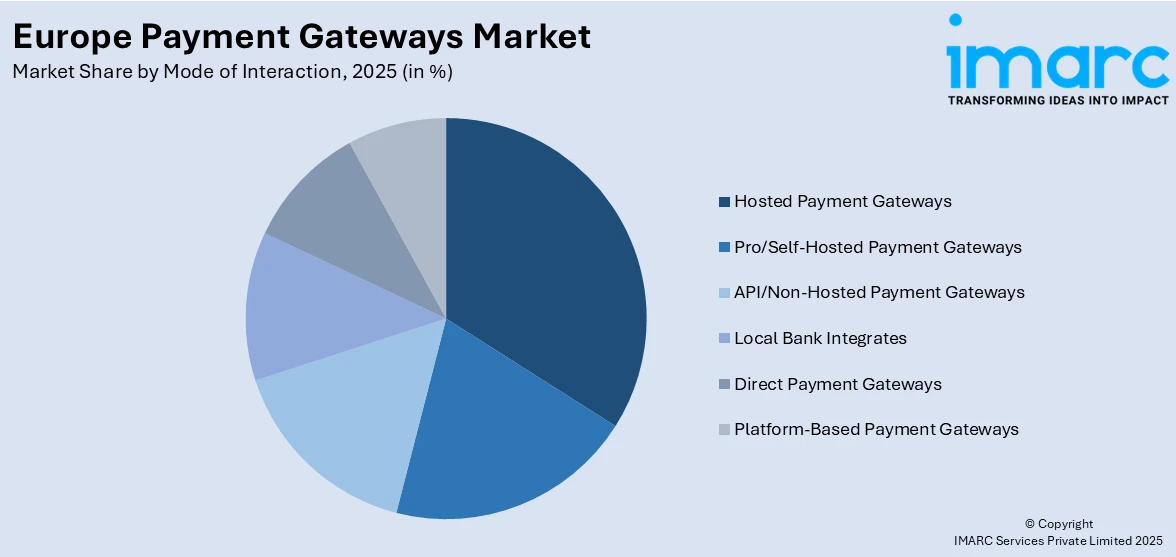

- By Mode of Interaction: API/Non-hosted payment gateways lead the market with a share of 28% in 2025, driven by the growing preference among businesses for fully customizable payment experiences that offer seamless integration with existing digital infrastructure while maintaining complete control over transaction data and user interfaces.

- Key Players: Key players drive the Europe payment gateways market by investing in advanced security technologies, expanding cross-border capabilities, integrating innovative checkout solutions, and forming strategic partnerships with banks, fintechs, and e-commerce platforms to strengthen merchant services and enhance consumer payment experiences across the region.

To get more information on this market Request Sample

The Europe payment gateways market is advancing as digital commerce continues to reshape the region's financial infrastructure. A major factor fueling this progress is the rapid expansion of open banking and instant payment frameworks, which provide merchants and consumers with faster, more secure transaction options. The growing preference for seamless digital checkout experiences, coupled with increasing smartphone penetration and contactless payment adoption, is accelerating the shift away from traditional cash-based transactions. Regulatory developments promoting payment interoperability, strong customer authentication, and real-time settlement capabilities are further enhancing the efficiency of cross-border payment processing. Additionally, the rising integration of artificial intelligence-driven fraud prevention tools, tokenization technologies, and embedded finance solutions within payment gateway platforms is enabling businesses to deliver personalized, secure, and frictionless payment experiences that align with evolving consumer expectations across European markets.

Europe Payment Gateways Market Trends:

Rising Adoption of Account-to-Account Payment Solutions

Europe is experiencing a significant shift toward account-to-account payment methods as consumers and merchants seek alternatives to traditional card networks. Regulatory initiatives such as PSD2 and the mandatory SEPA Instant Credit Transfer scheme are enabling faster and more cost-effective transactions across the region. The growing availability of pan-European digital wallets and instant payment platforms is further accelerating this transition, as both consumers and businesses embrace real-time bank-initiated transfers that offer lower processing costs, enhanced transparency, and seamless cross-border interoperability, supporting Europe payment gateways market growth.

Expansion of Biometric Authentication and AI-Driven Fraud Prevention

Payment gateway providers across Europe are increasingly integrating biometric authentication and artificial intelligence-based fraud detection to strengthen transaction security. Tokenization technologies and advanced risk-scoring algorithms are reducing unauthorized payment attempts while improving approval rates for legitimate transactions. For example, Adyen implemented its AI-powered optimization tool, Adyen Uplift, which improved payment conversion rates by approximately six percent across its European merchant portfolio, demonstrating how intelligent systems are enhancing the reliability and efficiency of digital payment processing.

Growing Integration of Embedded Finance and Omnichannel Payment Solutions

European merchants are increasingly embedding payment capabilities directly into their applications and retail environments to create unified commerce experiences. API-first payment gateways are enabling businesses of all sizes to deploy pay-by-bank, split-pay, and buy-now-pay-later functionalities with minimal integration effort. The rise of pre-built, cloud-native payment frameworks is further simplifying integration, allowing enterprise retailers to connect with multiple payment service providers through a single platform, reducing development complexity and accelerating time-to-market across omnichannel operations.

Market Outlook 2026-2034:

The Europe payment gateways market is positioned for sustained growth as digital transformation, regulatory modernization, and evolving consumer expectations converge to reshape the payments landscape. The expansion of open banking frameworks, the rollout of instant payment mandates, and the increasing adoption of mobile wallets and contactless technologies are expected to accelerate transaction volumes across the region. Additionally, rising investments in artificial intelligence-driven fraud prevention, payment orchestration platforms, and cross-border payment solutions are anticipated to enhance the efficiency and security of digital payment ecosystems, positioning Europe as a leading market for innovative gateway technologies. The market generated a revenue of USD 5,045.99 Billion in 2025 and is projected to reach a revenue of USD 7,525.21 Billion by 2034, growing at a compound annual growth rate of 4.54% from 2026-2034.

Europe Payment Gateways Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Application |

Large Enterprises |

45% |

|

Mode of Interaction |

API/Non-Hosted Payment Gateways |

28% |

Application Insights:

- Large Enterprises

- Micro and Small Enterprises

- Mid-Size Enterprises

Large enterprises dominate the market with a share of 45% of the total Europe payment gateways market in 2025.

Large enterprises represent the primary adopters of payment gateway solutions in Europe, driven by the need to process high-volume, multi-currency transactions securely across diverse sales channels. These organizations require robust payment infrastructure that integrates seamlessly with enterprise resource planning, customer relationship management, and point-of-sale systems. The growing emphasis on omnichannel commerce, where online, in-store, and mobile transactions converge, has intensified demand for scalable gateway solutions. Furthermore, the increasing complexity of managing cross-border payment flows, regulatory compliance across multiple jurisdictions, and real-time fraud monitoring is compelling large enterprises to adopt advanced gateway platforms that offer unified transaction management, dynamic routing capabilities, and comprehensive analytics to optimize payment performance and enhance customer experiences.

Large enterprises also prioritize advanced security frameworks, real-time fraud monitoring, and compliance with evolving regulations such as PSD2 and GDPR across their payment operations. The requirement for customizable API-based gateways that support dynamic currency conversion, subscription billing, and multi-acquirer routing further distinguishes enterprise payment needs from smaller business segments. The increasing complexity of cross-border commerce and the need for seamless omnichannel integration are compelling large organizations to invest in sophisticated gateway platforms that deliver operational efficiency, regulatory adherence, and scalable transaction management across diverse European markets.

Mode of Interaction Insights:

Access the comprehensive market breakdown Request Sample

- Hosted Payment Gateways

- Pro/Self-Hosted Payment Gateways

- API/Non-Hosted Payment Gateways

- Local Bank Integrates

- Direct Payment Gateways

- Platform-Based Payment Gateways

API/non-hosted payment gateways lead with a share of 28% of the total Europe payment gateways market in 2025.

API/non-hosted payment gateways are increasingly favored by businesses seeking full control over the payment experience, enabling customized checkout flows that align with brand identity and customer engagement strategies. These gateways allow merchants to process payments directly on their websites or applications without redirecting users to third-party pages, reducing cart abandonment and enhancing conversion rates. The growing adoption of headless commerce architectures and microservices-based platforms across Europe has accelerated demand for API-driven payment solutions. Additionally, the rising need for seamless integration with fraud detection systems, real-time analytics dashboards, and multi-acquirer routing capabilities is reinforcing the preference for non-hosted gateways among businesses that prioritize operational flexibility, data ownership, and personalized transaction management across diverse European markets.

The preference for API/non-hosted gateways is further reinforced by the need for advanced data control, personalized analytics, and seamless integration with fraud detection and risk management systems at the enterprise level. Businesses with high transaction volumes particularly value the flexibility of non-hosted solutions for implementing multi-acquirer strategies, dynamic routing, and real-time authorization optimization. The expanding ecosystem of open banking frameworks and instant payment rails across Europe is further driving adoption, as API-based gateways enable merchants to incorporate account-to-account transfers, digital wallet acceptance, and embedded finance functionalities within unified checkout experiences. This shift toward software-driven, hardware-independent payment architectures is allowing businesses to reduce infrastructure costs while delivering secure, frictionless, and brand-consistent payment journeys across multiple channels and geographies.

Country Insights:

- Germany

- France

- United Kingdom

- Italy

- Spain

- Others

Germany is further developing the digital payment gateway landscape with the improvement of e-commerce infrastructure as well as the growth of open banking and instant payment products. The introduction of Wero by the European Payments Initiative in the German market in mid-2024, with the support of major banks provide digital wallets to millions of users.

France is solidifying its position in the European payment gateways market through robust digital commerce growth and increasing use of alternative payment methods. French retailers are increasingly adopting payment orchestration platforms to optimize multi-acquirer strategies and authorization rates.

The United Kingdom has continued to be a key driver for innovative payment gateway solutions, given its advanced fintech infrastructure, high rate of digital payment adoption, and favorable rules and regulations. With its open banking legislation at an advanced state and its IT-savvy citizens embracing contactless payment solutions, the UK presents an expanding market for advanced payment gateway solutions across online and instore transactions.

Italy is witnessing notable developments in the payment gateway domain, driven by increasing digital commerce adoption and expanding strategic partnerships between payment processors and merchants. The integration of domestic mobile payment technologies with pan-European acquiring platforms is strengthening digital payment capabilities, while growing consumer preference for contactless and card-based transactions is encouraging retailers to modernize their payment infrastructure across both online and physical channels.

Spain is observing an increasing requirement for the infrastructure of the payment gateway due to an improvement in the penetration of digital commerce and the continued growth in contactless payment. The availability of mobile payment platforms and improvements in cross-border payment facilities are improving the merchant payment experience in Spain.

Market Dynamics:

Growth Drivers:

Why is the Europe Payment Gateways Market Growing?

Accelerating E-Commerce Expansion and Digital Shopping Adoption

The rapid growth of online retail across Europe is fundamentally driving demand for secure, efficient payment gateway solutions. Consumers increasingly prefer digital shopping channels, which require seamless payment processing capabilities across websites, mobile applications, and social commerce platforms. The European Union’s Single Digital Market strategy continues to reduce cross-border trade barriers, encouraging merchants to adopt gateway solutions that support multiple currencies and localized payment methods. For instance, according to European Commission, approximately 23.8% of European enterprises generated e-commerce sales in 2023, underscoring the structural shift toward digital commerce that sustains payment gateway demand. Merchants are increasingly integrating global payment solutions to ensure smooth transactions across jurisdictions, driving investment in advanced gateway infrastructure that can handle complex routing, dynamic currency conversion, and regulatory compliance across different European markets.

Regulatory Modernization and Open Banking Frameworks

European regulatory frameworks are actively reshaping the payment landscape and creating favorable conditions for payment gateway expansion. The Revised Payment Services Directive has mandated strong customer authentication and opened banking data to third-party providers, enabling innovative payment initiation services that compete with traditional card-based transactions. The mandatory implementation of SEPA Instant Credit Transfers by October 2025 further accelerates the transition toward real-time payment processing across the euro area. For instance, the European Central Bank reported that contactless card payments in the euro area increased by 13.2 percent to 25.8 Billion transactions in the first half of 2024 compared with the same period in 2023, reflecting the broader shift toward digital payment methods driven by regulatory enablement. Open banking is creating new opportunities for payment gateway providers to offer account-to-account payment rails that reduce interchange costs and provide instant settlement for merchants. As PSD3 proposals advance and the digital euro project progresses through its preparation phase, payment gateway providers are positioning themselves to accommodate emerging regulatory requirements while delivering enhanced functionality to consumers and businesses.

Rising Mobile Wallet and Contactless Payment Penetration

The wide spread of mobile wallets and contactless payment technologies across Europe maintains the demand for payment gateways that can process a variety of digital payment instruments. Consumers are increasingly using smartphones, wearables, and digital wallets to make both online and in-store transactions, mandating merchants to deploy gateway solutions that support near-field communication, tokenized credentials, and multi-wallet acceptance. In addition, mobile payment adoption is being consolidated by the emergence of pan-European digital wallets. Initiatives such as Wero and the EuroPA alliance are interoperably connecting national mobile payment platforms across multiple countries, creating an expanded addressable market for gateway providers. As these wallets extend their propositions from peer-to-peer transfers toward merchant payments and e-commerce checkout, payment gateways will be required to adapt to new payment flows and settlement mechanisms.

Market Restraints:

What Challenges the Europe Payment Gateways Market is Facing?

Complex and Fragmented Regulatory Compliance Requirements

Europe’s diverse regulatory landscape presents significant compliance challenges for payment gateway providers operating across multiple jurisdictions. Each country maintains distinct requirements related to data protection, consumer authentication, anti-money laundering, and cross-border transaction reporting. The ongoing evolution of PSD2 toward PSD3, combined with General Data Protection Regulation enforcement and varying national payment regulations, creates a complex compliance environment that increases operational costs and slows market entry for newer providers.

Cybersecurity Threats and Evolving Fraud Patterns

The increasing sophistication of cyberattacks targeting digital payment systems poses a persistent challenge to the payment gateways market. As transaction volumes grow and new payment methods proliferate, fraudsters continually develop more advanced techniques to exploit vulnerabilities in payment processing infrastructure. Payment gateway providers must invest heavily in artificial intelligence-driven fraud detection, encryption technologies, and security audits to maintain consumer trust and regulatory compliance, adding significant cost pressures to their operations.

High Market Competition and Margin Compression

Intense competition among payment gateway providers in Europe is compressing transaction fees and challenging profitability, particularly for mid-tier providers. The presence of global platforms alongside established European processors creates pricing pressure as merchants increasingly leverage multi-acquirer strategies and payment orchestration platforms to negotiate lower processing costs. Additionally, the growth of account-to-account payments and instant transfer networks threatens to reduce card-based interchange revenue streams that have traditionally supported gateway business models.

Competitive Landscape:

The Europe payment gateways market involves tough competition among global technology-driven platforms, established European processors, and emerging fintech challengers. Companies compete across multiple dimensions, from transaction security to integration flexibility, cross-border capabilities, and pricing transparency. Strategic acquisitions, bank partnerships, and integrations across platforms have been pivotal in reshaping these competitive dynamics, while providers seek to expand merchant portfolios and geographic coverage. Where payment processing has converged with enterprise software, retail platforms, and financial services, it has forced gateway providers to provide comprehensive solutions with value addition beyond the core transaction processing to retain and acquire merchants.

Recent Developments:

- In December 2025, Deutsche Bank launched Wero for all its Deutsche Bank and Postbank customers across Germany, enabling instant peer-to-peer money transfers and merchant payments through the pan-European digital wallet operated by the European Payments Initiative (EPI). The integration marked a significant milestone in expanding Wero’s reach across Europe’s largest economy.

- In May 2024, Nexi announced a strategic collaboration with Shopreme, an Austria-based software company, to integrate self-checkout solutions into Nexi’s merchant propositions across Europe. The partnership aims to enhance the digital payment experience in retail environments by combining Nexi’s payment processing capabilities with Shopreme’s mobile and self-service checkout technologies.

Europe Payment Gateways Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Applications Covered | Large Enterprises, Micro and Small Enterprises, Mid-Size Enterprises |

| Mode of Interactions Covered | Hosted Payment Gateways, Pro/Self-Hosted Payment Gateways, API/Non-Hosted Payment Gateways, Local Bank Integrates, Direct Payment Gateways, Platform-Based Payment Gateways |

| Countries Covered | Germany, France, United Kingdom, Italy, Spain, Others |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Europe Payment Gateways Market Report

The Europe payment gateways market size was valued at USD 5,045.99 Billion in 2025.

The Europe payment gateways market is expected to grow at a compound annual growth rate of 4.54% from 2026-2034 to reach USD 7,525.21 Billion by 2034.

Large enterprises dominated the market with a share of 45%, driven by their need for scalable, multi-currency payment processing, advanced security frameworks, and seamless integration with enterprise systems across omnichannel retail environments.

Key factors driving the Europe payment gateways market include accelerating e-commerce expansion, regulatory modernization through open banking and instant payment mandates, rising mobile wallet adoption, growing cross-border digital commerce, and advancing payment security technologies.

Major challenges include complex and fragmented regulatory compliance requirements across jurisdictions, increasing cybersecurity threats and evolving fraud patterns, intense market competition driving margin compression, and the disruptive impact of alternative payment methods on traditional gateway revenue models.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)