Europe Pet Food Market Size, Share, Trends and Forecast by Pet Type, Product Type, Pricing Type, Ingredient Type, Distribution Channel, and Country, 2026-2034

Europe Pet Food Market Size, Share, Trends & Forecast (2026-2034)

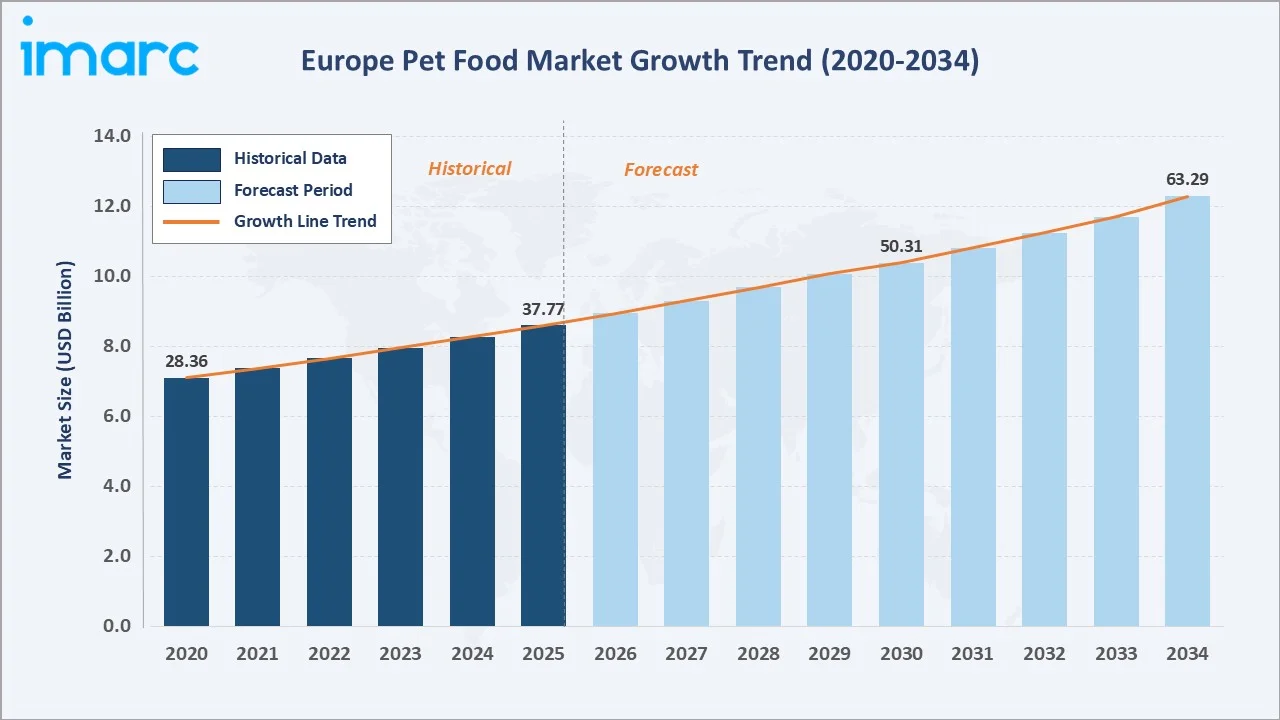

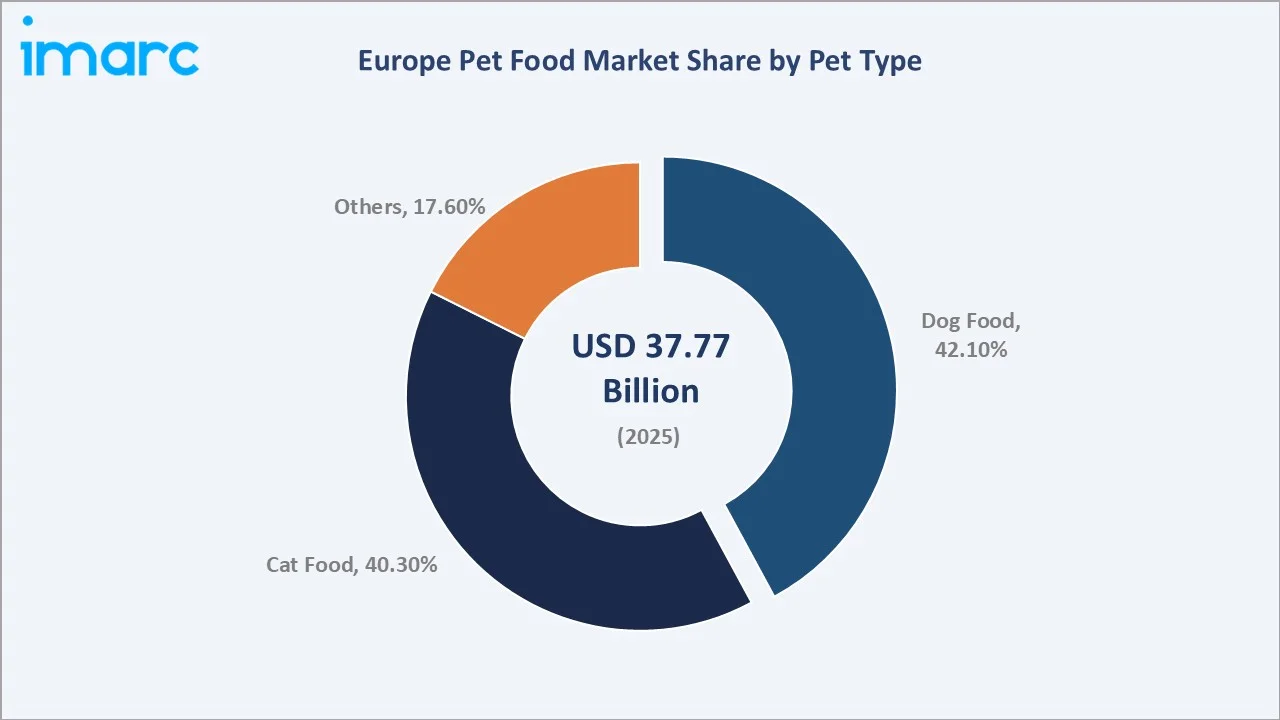

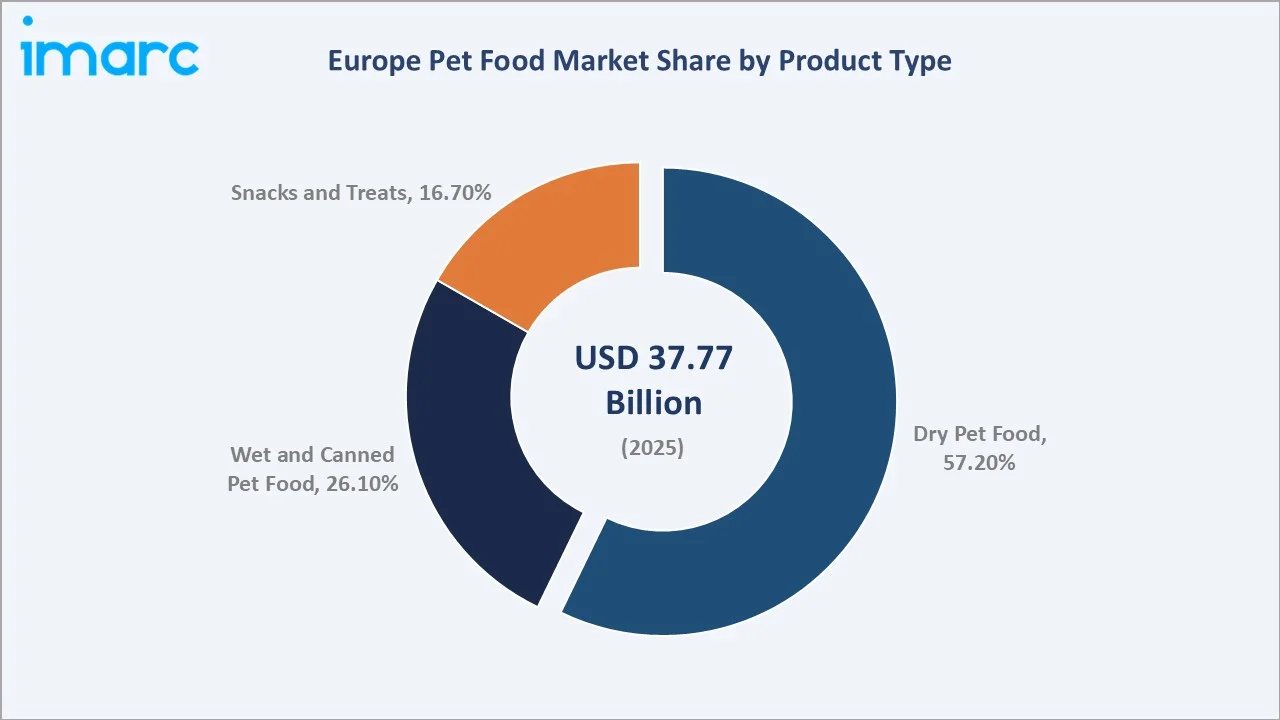

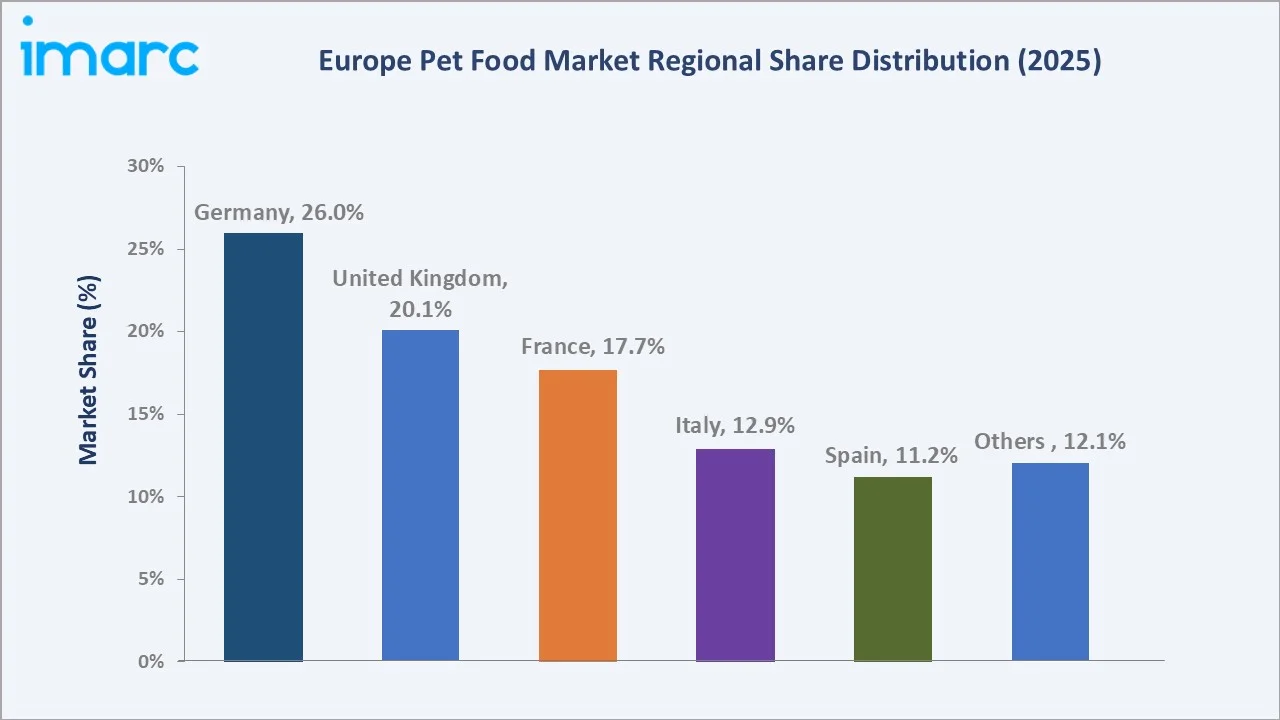

The Europe pet food market size was valued at USD 37.77 Billion in 2025 and is projected to reach USD 63.29 Billion by 2034, exhibiting a CAGR of 5.90% during the forecast period 2026-2034. Accelerating pet humanization trends, rising ownership across 139 million European households (49% of all households in 2025), and sustained demand for premium and functional nutrition formulations are the primary drivers of Europe pet food market growth. Dog food leads with the largest pet type share at 42.09% in 2025, while dry pet food commands a 57.18% product type share. Germany (26.0%) and the United Kingdom (20.1%) are the two largest country markets in 2025.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 37.77 Billion |

|

Forecast Market Size (2034) |

USD 63.29 Billion |

|

CAGR (2026-2034) |

5.90% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Country |

Germany (26.0% share, 2025) |

|

Second Largest Country |

United Kingdom (20.1% share, 2025) |

|

Leading Pet Type |

Dog Food (42.09%, 2025) |

|

Leading Product Type |

Dry Pet Food (57.18%, 2025) |

The Europe pet food market growth trajectory from 2020 through 2034, illustrating steady historical expansion alongside an accelerating forecast underpinned by premiumization, e-commerce penetration, and widening pet ownership demographics across the continent.

To get more information on this market, Request Sample

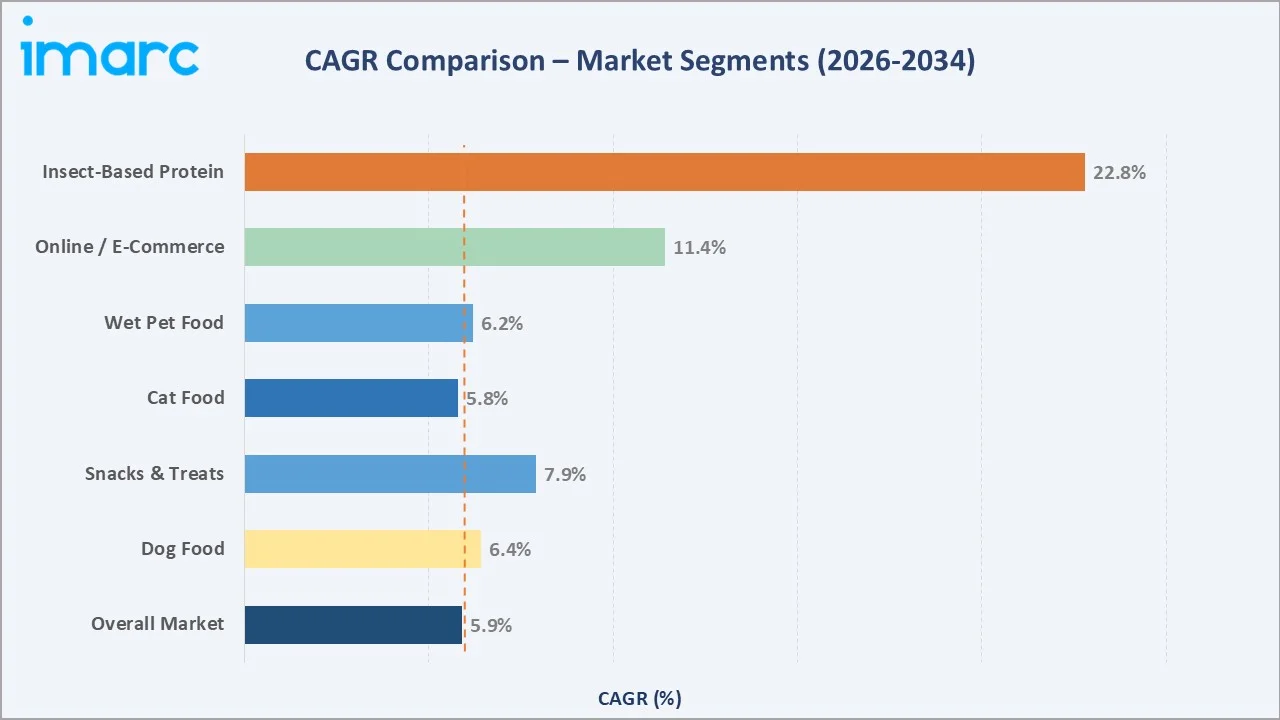

CAGR comparisons across key product and channel segments, revealing insect-based protein and online e-commerce distribution as the standout high-growth categories within the Europe pet food industry analysis through 2034.

Executive Summary

Europe's 299 million pets across 139 million pet-owning households in 2025, representing 49% of all European households, provide an exceptionally deep and recurring demand base. Post-pandemic lifestyle transformations deepened human-animal bonds and drove an increase in single-person households across the EU.

Dog food dominates pet type demand at 42.09% of Europe's pet food market share in 2025, reflecting both Europe's dog ownership scale with approximately 104 million dogs in 2025 and the higher per-unit revenue premium of breed-specific, life-stage, and functional nutrition formulations for dogs versus other pet categories. Cat food follows at 40.31% in 2025, while the Others category (birds, fish, small animals) accounts for 17.60%.

Germany (26.0%) and the United Kingdom (20.1%), reflecting the continent's most mature and highest-spend pet care markets. France follows at 17.7%, Italy at 12.9%, Spain at 11.2%, and Others at 12.1%.

Key Market Insights

|

Insight |

Data |

|

Largest Pet Type |

Dog Food - 42.09% share (2025) |

|

Largest Product Type Format |

Dry Pet Food - 57.18% share (2025) |

|

Largest Country Market |

Germany - 26.0% revenue share (2025) |

|

Second Country Market |

United Kingdom - 20.1% revenue share (2025) |

|

Top Companies |

Mars Petcare, Nestlé Purina, Hill's, Royal Canin, Affinity, Zooplus |

Key Analytical Observations Supporting the Above Data:

- Dog food commands a 42.09% share in 2025, nearly half of the entire European pet food market, driven by Europe's 104 million dog population and the high average revenue per dog due to breed-specific formulations, life-stage nutrition (puppy, adult, senior), and functional health products targeting joint support, digestive health, and dental care.

- Dry pet food leads product type formats at 57.18% in 2025. High-pressure processing advances have enabled premium dry kibble to reach protein inclusion rates on a dry matter basis, significantly narrowing the historical nutritional gap versus wet alternatives and sustaining consumer confidence in dry food quality.

- Germany leads country-level revenue at 26.0% in 2025, representing approximately EUR 8.5 Billion in annual pet food sales. 45% of German households owned a pet, and 14% of households have two pets or more as of 2023. This totals approximately 34.3 million pets.

- The United Kingdom, at 20.1%, is Europe's second-largest pet food market and its most innovation-receptive. The UK’s European insect-based pet food retail sales, despite representing only 20.1% of market revenue, reflect a highly engaged, premium and sustainability-conscious consumer base that actively embraces novel nutrition formats.

Europe Pet Food Market Overview

The European pet food market encompasses commercially formulated food products for companion animals, including dogs, cats, birds, fish, and small mammals. Products span dry kibble, wet and canned formulations, semi-moist foods, and the rapidly expanding snacks and treats category. The ecosystem integrates raw material suppliers, meat renderers, grain processors, fish meal producers, and insect farms, alongside ingredient processors, pet food manufacturers, co-packers, packaging innovators, and a multi-channel distribution network encompassing supermarkets and hypermarkets, pet specialty stores, veterinary clinics, and fast-growing e-commerce platforms.

The industry is governed by the FEDIAF (European Pet Food Industry Federation) regulatory framework, EU food safety legislation, the Packaging and Packaging Waste Directive (70% recyclability target by 2030), and the overarching European Green Deal sustainability agenda reshaping ingredient sourcing and packaging standards.

Macroeconomic influences, including household income growth, rising urbanization, the structural shift toward smaller household sizes, and the deepening perception of pets as family members position the Europe pet food market for continued above-GDP growth.

Market Dynamics

To evaluate market opportunities, Request Sample

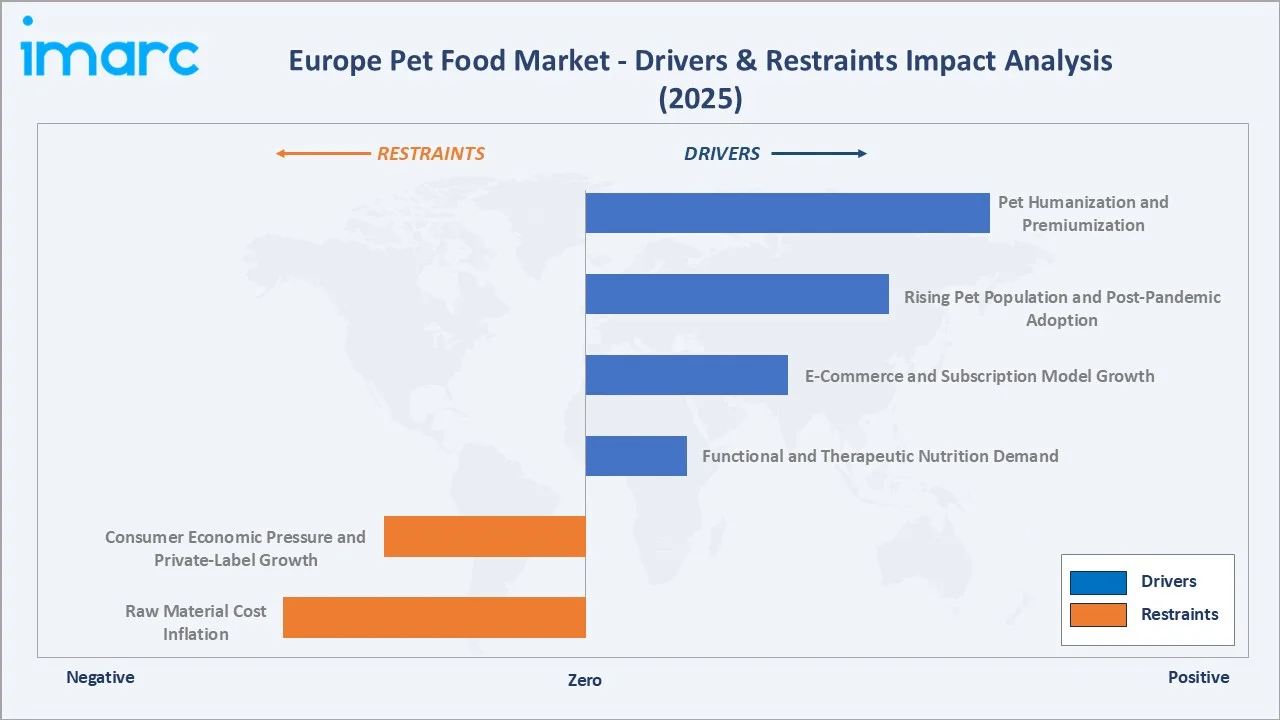

Market Drivers

- Pet Humanization and Premiumization: Transparency in ingredient sourcing, functional health claims, and veterinary-recommended formulations has become non-negotiable for premium segment buyers.

- Rising Pet Population and Post-Pandemic Adoption: As of 2021, 88 million households own a pet (38%) in Europe, with around 110 million cats, 90 million dogs, 52 million birds, 30 million small mammals, 15 million aquaria and 9 million reptiles. This permanently enlarged ownership base, now 299 million pets across 139 million households, continues to generate recurring annual nutrition expenditure that persists well beyond the pandemic catalyst, creating a structurally enlarged revenue base for manufacturers.

- E-Commerce and Subscription Model Growth: Subscription platforms for dry and fresh pet food have achieved customer retention rates in Germany and the UK, generating highly predictable recurring revenue streams.

- Functional and Therapeutic Nutrition Demand: Veterinary-recommended and condition-specific formulas, targeting digestive health, joint support, weight management, and dental care.

Market Restraints

- Raw Material Cost Inflation: Key protein commodities, chicken meal, fish meal, and beef by-products increased substantially between 2021 and 2024, directly compressing manufacturer margins and contributing to shelf price increases.

- Consumer Economic Pressure and Private-Label Growth: Private-label dry pet food volume share are raising, compressing branded player revenues and forcing pricing strategy reassessments.

Market Opportunities

- Insect-Based and Novel Protein Ingredients: As of February 2025, 8 insect protein species have received EU Novel Food approval for pet food use.

- Snacks and Treats Premiumization: Functional treat formulations incorporating dental care enzymes, probiotic cultures, calming botanicals, and joint support complexes are commanding 2-3x premium price points versus commodity treat alternatives, creating a high-margin innovation frontier.

- Central and Eastern European (CEE) Expansion: Per-pet spending in CEE markets remains 15-20 percentage points below Western European benchmarks, presenting a structural catch-up growth pathway as disposable incomes and pet humanization trends converge with Western European norms over 2026-2034.

Market Challenges

- Sustainability Packaging Transformation Costs: The transition to mono-material flexible films, paper-based pouches, and compostable treat packaging requires high cost in industry-wide capital investment through 2030.

- Private-Label Competition Intensification: Major European retailers such as Lidl, Aldi, Tesco, Carrefour, and Rewe are aggressively expanding private-label pet food ranges.

- Regulatory Fragmentation Post-Brexit: The UK's divergence from EU packaging regulations, labelling standards, and novel ingredient approval timelines post-2020 creates dual compliance requirements for manufacturers serving both markets simultaneously.

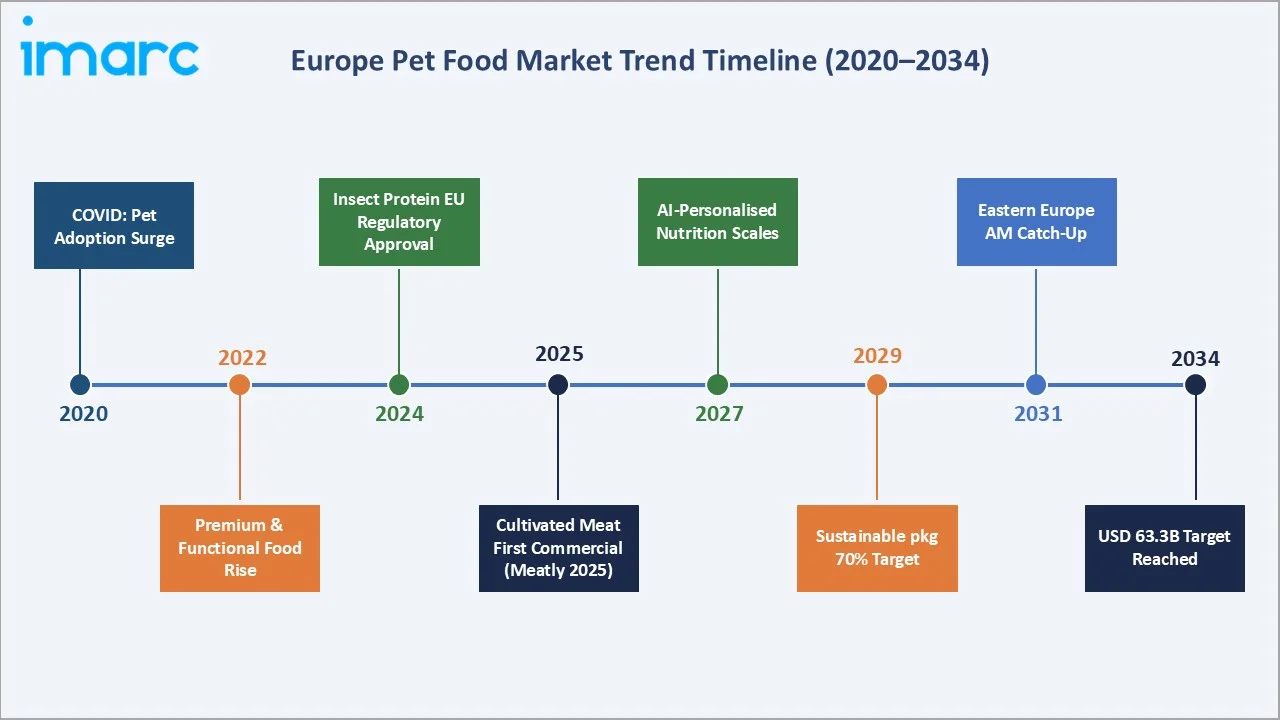

Emerging Market Trends

1. Pet Humanization Driving Premium Formulation Standards

European pet parents' evolving perception of animals as family members is fundamentally transforming product expectations continent-wide. Formulations now routinely incorporate probiotics, omega-3 fatty acids, glucosamine, antioxidant complexes, and veterinary-recommended micronutrient profiles.

2. Cultivated Meat Entering Commercial Reality

In February 2025, Meatly became the first company globally to commercialise cultivated meat for pet food, launching 'Chick Bites' in partnership with THE PACK at Pets at Home in London. Lab-grown meat offers a resource-efficient, ethically compelling protein source with no antibiotic contamination risk.

3. EU-Mandated Sustainable Packaging Transformation

The EU Packaging and Packaging Waste Regulation mandating 70% recyclable packaging by 2030 is driving comprehensive material innovation across the industry. Paper-based wet food pouches, mono-material flexible films, and compostable treat packaging are transitioning from pilot to mainstream rollout across premium and mid-tier brands.

4. Snacks & Treats Becoming a Functional Nutrition Category

Snacks and treats (16.69% share, 2025) are evolving from impulse purchases into deliberate functional nutrition investments. Dental chew products clinically proven to reduce plaque by up to 70%, calming treats containing L-theanine and chamomile for anxiety-prone pets, and probiotic treats enriched with Lactobacillus strains for digestive support.

5. E-Commerce and AI-Personalised Nutrition Scaling Rapidly

Online channels are growing at ~11.4% CAGR, nearly double the market average as subscription delivery models gain mass-market adoption. Zooplus serves customers across 30 European countries.

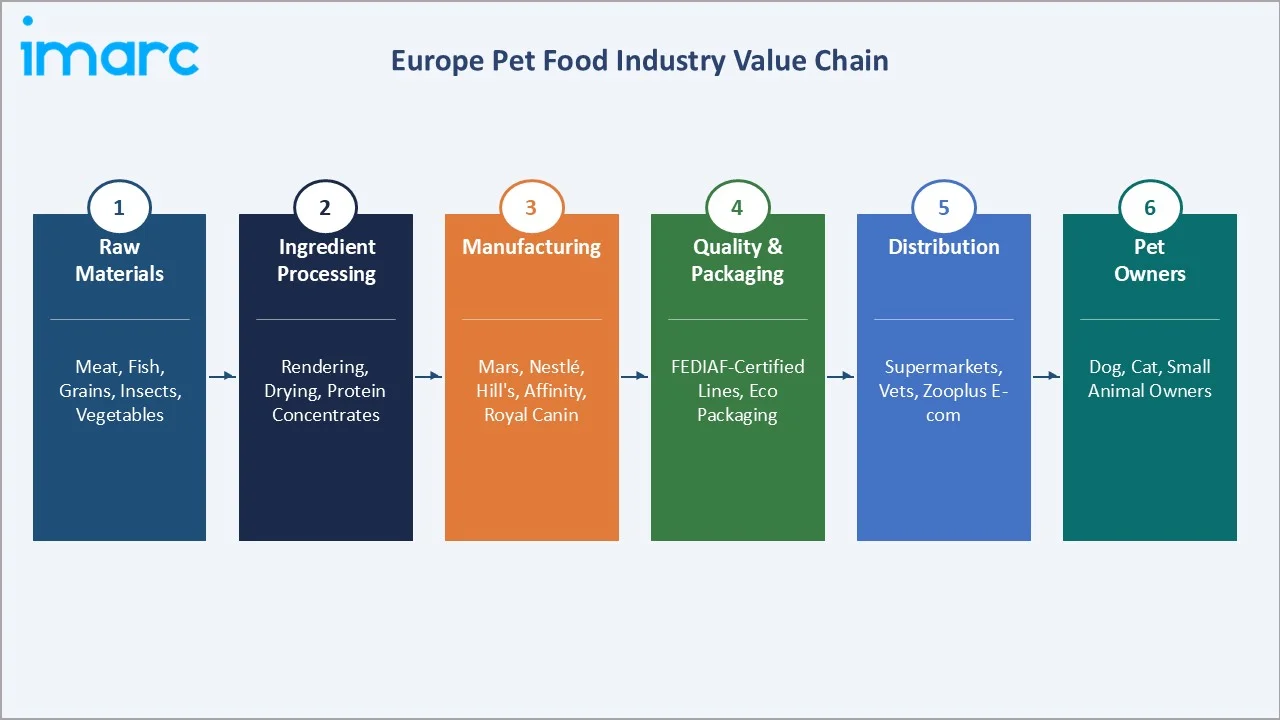

Industry Value Chain Analysis

The Europe pet food value chain spans six integrated stages from raw material procurement to end-consumer delivery. Each stage presents distinct competitive intensity, sustainability challenges, and innovation imperatives for domestic and global participants through 2034.

|

Stage |

Key Players / Examples |

|

Raw Materials |

Chicken/beef renderers (PHW Group, Tönnies), fish meal suppliers (FF Skagen), insect farms (Ynsect), grain processors |

|

Ingredient Processing |

DSM-Firmenich (vitamins, enzymes), Cargill Animal Nutrition, ADM Pet Nutrition, Lallemand Animal Nutrition |

|

Manufacturing |

Mars Petcare, Nestlé Purina, Hill's Pet Nutrition, Affinity Petcare, Royal Canin, Josera, Brit (VAFO Group) |

|

Quality Control & Packaging |

SGS Group (testing), Amcor (flexible packaging), Mondi (paper-based solutions), Coveris, DS Smith |

|

Distribution & Retail |

Zooplus AG, Amazon Pets, Tesco, Carrefour, Lidl, Rewe, Fressnapf, Maxi Zoo, veterinary clinics |

|

End Consumers |

Dog owners, cat owners, small animal owners across 139 million European pet-owning households (2025) |

Manufacturers dominate value capture in Europe's pet food chain, benefiting from brand equity, formulation IP, and manufacturing scale efficiencies. However, retailers are capturing increasing margin share through private-label expansion, reaching 28% of dry pet food volume in 2024, while insect farms and novel protein start-ups are building strategic positions in the raw materials stage as EU regulatory approvals enable commercial-scale ingredient supply.

Technology Landscape in the Europe Pet Food Industry

Advanced Formulation Science and Functional Nutrition Technology

Precision nutrition science is transforming European pet food formulations. Genomic profiling for breed-specific micronutrient tailoring is in a commercial pilot with Zoetis following its Basepaws acquisition in 2022. Encapsulation technologies are extending probiotic (Lactobacillus, Bifidobacterium) and omega-3 stability through thermal processing and storage, enabling guaranteed viable cell counts at consumption.

Novel Protein Technologies: Insect and Cultivated Meat

EU Novel Food approvals for eight insect protein species by February 2025 have opened commercial-scale production pathways for companies. Insect protein delivers a lower carbon footprint versus beef, 13x less water usage, and 7.5x less feed per kg of protein, aligning with European Green Deal mandates.

Sustainable Packaging Technology

European pet food manufacturers are deploying mono-material flexible film technology, paper-based barrier coatings, and compostable bio-based films to meet EU recyclability mandates. Digital printing enables customised packaging at smaller batch sizes without excess material waste.

AI-Powered Personalisation and Digital Commerce

Machine learning algorithms deployed by DTC platforms (Butternut Box, Tails.com, Edgard & Cooper) analyse pet profile data to generate customised meal plans with regular reformulation as pets age or health conditions evolve. These platforms report 3-4x higher customer lifetime values versus retail channel equivalents, validating the commercial case for personalisation technology investment.

Dry Food Technology: High-Protein Extrusion and HPP

High-pressure processing (HPP) and advanced extrusion technology advances have enabled dry kibble manufacturers to achieve protein inclusion on a dry matter basis in premium lines, reducing the nutritional gap versus wet alternatives that have historically limited dry food's premium positioning potential.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Pet Type |

Dog Food |

42.09% |

2025 |

|

Product Type |

Dry Pet Food |

57.18% |

2025 |

|

Pricing Type |

Mass Products |

70.04% |

2025 |

|

Ingredient Type |

Animal Derived |

65.05% |

2025 |

|

Distribution Channel |

Supermarkets and Hypermarkets |

62.76% |

2025 |

|

Country |

Germany |

26.0% |

2025 |

By Pet Type

Dog food commands a 42.09% majority share of Europe's pet food market in 2025, the largest single pet type segment on a proportional basis. This dominance reflects Europe's deep-rooted dog ownership culture, with approximately 104 million dogs living across the Europe. Per-unit revenue for dog food consistently exceeds cat food owing to larger portion sizes, a wider range of breed-specific formulations, and a premium positioning landscape featuring functional health claims across joint, digestive, dental, and cognitive wellness sub-categories.

To access detailed market analysis, Request Sample

Cat food at 40.31% in 2025 reflects Europe's 127 million domestic cats. Within cat food, wet and canned formats are significantly higher than regional averages, reflecting the continent's strong preference for high-moisture, high-palatability formulations aligned with feline biology.

By Product Type

Dry pet food leads at 57.18% in 2025, but its share is notably lower than in other markets, reflecting Europe's strong wet food culture. Advanced extrusion and HPP technologies are improving dry food's nutritional profile and palatability, gradually sustaining its market position. Dry food's competitive advantage in shelf stability (18-24 months without refrigeration), cost-per-serving economics, and easy portioning ensure its continued leadership through 2034 despite wet food's growing appeal.

Regional Market Insights

|

Country |

Share (2025) |

Key Growth Drivers |

|

Germany |

26.0% |

Highest per-pet spend, premium adoption, advanced e-commerce |

|

United Kingdom |

20.1% |

Post-Brexit premium market, DTC subscription leadership, insect protein commercialisation |

|

France |

17.7% |

Cat-heavy ownership, organic & grain-free demand, high wet food culture |

|

Italy |

12.9% |

Pet humanization rising, wet food dominance (cats), and natural ingredient preference |

|

Spain |

11.2% |

Growing middle-class pet spending, outdoor lifestyle, and functional snacks demand |

|

Others |

12.1% |

Eastern Europe rapid income growth; the Nordics sustainability premium; the Benelux premium urban market |

Germany leads the Europe pet food market with a 26.0% revenue share in 2025, representing approximately EUR 8.5 Billion in annual pet food sales. German consumers demonstrate Europe's highest per-pet annual expenditure, with premium dry kibble and veterinary prescription diets performing particularly well.

The United Kingdom, with a 20.1% share in 2025, is Europe's second-largest pet food market and its most innovation-receptive. Meatly's February 2025 commercial cultivated meat launch at Pets at Home in London further underscores the UK's position as Europe's leading frontier for novel protein pet food adoption.

Competitive Landscape

The Europe pet food competitive landscape features moderate-to-high concentration among branded manufacturers at the premium end, led by Mars Petcare and Nestlé Purina, alongside a vibrant and growing mid-market populated by regional specialists, private-label producers for major retailers, and a rapidly expanding cohort of DTC challenger brands focused on natural, sustainable, and personalised nutrition.

|

Company Name |

Brand Name |

Market Position |

Core Strength |

|

Mars Petcare |

Pedigree, Whiskas, Royal Canin |

Leader |

Premiumisation, sustainable packaging, vet channel expansion |

|

Nestlé Purina PetCare |

Purina Pro Plan, Felix, Gourmet |

Leader |

Science nutrition, online expansion, DTC platform build |

|

Hill's Pet Nutrition |

Science Diet, Prescription Diet |

Leader |

Veterinary therapeutic, Hill's to Home DTC subscription |

|

Affinity Petcare |

Ultima, Advance |

Challenger |

Spain/South EU leadership, functional & allergen-free ranges |

|

Zooplus AG |

Wolf of Wilderness, Rocco, Briantos, Cosma |

Challenger |

Europe's largest online pet retailer, AI recommendation engine |

|

Versele-Laga |

Opti Life, Prestige, Happy Life |

Challenger |

Small animal, bird, Belgium/Benelux primary market focus |

|

Animonda |

Integra Protect, vom Feinsten |

Challenger |

Germany veterinary & wellness nutrition specialist |

|

Brit (VAFO Group) |

Brit Care, Brit Premium |

Emerging |

CEE leadership, natural ingredients, value-premium segment |

|

Edgard & Cooper |

Edgard & Cooper |

Emerging |

Natural, sustainable, B Corp certified DTC challenger brand |

|

Butternut Box |

Butternut Box Fresh |

Emerging |

UK-led personalised fresh pet food DTC subscription model |

|

Josera |

Josera Nature, Holistic |

Emerging |

German engineering quality, grain-free innovation, mid-market |

The competitive positioning of key Europe pet food market participants across market presence and strategic investment dimensions in 2025 illustrates the clear separation between multinational leaders, established challengers, and emerging DTC and sustainability-focused brands.

Key Company Profiles

Mars Petcare

Mars Petcare is the world's largest pet food company and Europe's dominant market leader. Its portfolio spans value, mainstream, and ultra-premium segments across dog, cat, and veterinary nutrition.

- Product Portfolio: Pedigree, Whiskas, Royal Canin, Cesar, Dreamies, IAMS.

- Recent Developments: Mars Petcare committed EUR 1 Billion to sustainable packaging transformation globally in 2024, with European lines targeted for recyclable or reusable materials by 2027, ahead of EU mandate timelines.

- Strategic Focus: Mars Petcare's Europe strategy centres on Royal Canin premiumisation through veterinary partnership deepening, sustainable packaging leadership ahead of regulatory requirements, and digital commerce capability, including AI-powered personalised nutrition services via the Royal Canin digital ecosystem, targeting DTC subscription growth.

Nestlé Purina PetCare

Nestlé Purina PetCare is the world's second-largest pet food company. In Europe, Purina operates across the economy to ultra-premium segments with a portfolio covering both dog and cat nutrition.

- Product Portfolio: Purina Pro Plan, Felix, Gourmet, Beneful, Purina ONE, Friskies.

- Recent Developments: The company introduced its 'Beyond' organic and plant-enriched pet food line across 12 European markets and drove its online channel to represent 25%+ of European revenue through subscription growth.

- Strategic Focus: Nestlé Purina's Europe strategy emphasises digital retail channel capture, science nutrition credibility through veterinary partnerships, and sustainability leadership through its 'For Better Pets.

Zooplus AG

Zooplus AG is Europe's largest online pet supplies retailer, headquartered in Munich, Germany, serving active customers across 30 European countries.

- Product Portfolio: Briantos, Rocco, Purizon, Cosma.

- Recent Developments: In November 2025, zooplus SE relaunched its loyalty program in all 26 shops and made pet parenting even more rewarding.

- Strategic Focus: Zooplus's strategy focuses on private-label margin expansion, AI personalisation to increase customer lifetime value, and geographic deepening into Eastern European markets where pet e-commerce penetration remains below 15%, significantly below Germany's 28% benchmark, presenting a substantial structural expansion runway.

Market Concentration Analysis

The Europe pet food market exhibits moderate-to-high concentration among branded manufacturers, with the top two players, Mars Petcare and Nestlé Purina, commanding a combined estimated share of 38-44% of total European pet food revenue in 2025.

The top 5 players collectively hold approximately 47-59% of Europe's pet food market in 2025. The remaining 41-53% is distributed across a large and fragmented tail of regional brands, private-label manufacturers, DTC challenger brands, and national champions in specific country markets – reflecting the structurally diverse and competitive nature of the European pet food landscape.

The European pet food market is structurally bifurcated: highly concentrated among top branded manufacturers at the value creation layer, yet highly fragmented at the DTC, service, and distribution ends. Mars Petcare's dual ownership of Royal Canin (ultra-premium) and mainstream brands (Pedigree, Whiskas) creates formidable cross-segment competitive coverage.

Investment & Growth Opportunities

Fastest-Growing Segments

Snacks and Treats are the fastest-growing mainstream product segment at ~7.9% CAGR through 2034, driven by functional treat innovation, impulse purchase behavior, and the human-pet bonding ritual of reward-based feeding. Insect-based protein pet food is the highest-growth innovation investment theme at ~22.8% CAGR through 2034. EU approval of eight insect species for pet food by 2025 enables commercial-scale ingredient supply at scale.

Emerging Market Expansion

Central and Eastern European markets, Poland, Czech Republic, Romania, Hungary, and the Baltic states, represent Europe's highest-growth geographic pet food opportunity at 8-10% annually through 2034. Rising disposable incomes, Western lifestyle adoption, and improving retail infrastructure are driving rapid convergence. First-mover distribution advantages in CEE pet specialty retail are achievable for brands that establish presence before market saturation through 2027.

Venture & Private Equity Investment Trends

European pet food attracted EUR 1.2 Billion in recorded M&A and private investment activity between 2022 and 2025. Representative transactions include Ynsect, Meatly, Edgard & Cooper, and Brit VAFO Group PE sale (2024). Global PE firms including KKR, Ardian, and Partners Group are actively monitoring European premium pet food EBITDA-positive assets as the sector's resilient 5.9% CAGR through 2022-2024 economic headwinds establishes it as a defensive consumer staples investment warranting premium acquisition multiples.

Future Market Outlook 2026-2034

The Europe pet food market forecast projects measured but sustained expansion from USD 37.77 Billion in 2025 to USD 63.29 Billion by 2034 at a CAGR of 5.90%. This trajectory reflects a stable, mature Western European base growing at 4-6% annually, augmented by faster-growing CEE sub-regions (8-10%), online channel components (~11.4% CAGR), and novel protein sub-segments (~22.8% CAGR) that elevate the blended market growth rate through 2034.

Three technology shifts are most likely to reshape Europe's pet food landscape through 2034. Cultivated meat cost parity, targeted before 2030 by Meatly and competitor labs, will disrupt conventional animal protein supply chains while delivering unimpeachable welfare and sustainability credentials. Biodegradable smart packaging incorporating freshness biosensors and blockchain-verified sustainability credentials will become standard across premium segments by 2030, establishing new minimum category quality thresholds.

By 2034, the European pet food industry is expected to operate as a digitally-integrated, sustainability-mandated ecosystem where AI personalisation is standard, novel proteins, and all packaging meets EU recyclability standards. Europe's leading pet food brands will increasingly function as total pet wellness ecosystem providers, fundamentally expanding value capture per pet-owning household by 2034.

Research Methodology

Primary Research

Primary research encompassed over 65 structured interviews and consultations conducted in 2024-2025 with key European pet food value chain participants including pet food brand managers and R&D directors, ingredient suppliers, category managers at major European retailers, FEDIAF-affiliated veterinary nutritionists, insect protein producers, and institutional investors and PE funds active in the European pet food space.

Secondary Research

Secondary sources consulted include FEDIAF European Pet Food Industry Federation annual reports (2020-2024), Euromonitor International pet care market data, GfK European retail scanner panel data, European Commission food safety and packaging regulation publications, EFSA novel ingredient approval records, company annual reports, investor presentations, PE deal databases, and reputed trade publications including Pet Business World, Petfood Industry Magazine, and Zoomark International conference proceedings.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating GDP growth rates, urbanization indices, consumer expenditure data, and historical market evolution patterns. Scenario analysis (base, optimistic, and conservative cases) was performed to account for macroeconomic uncertainty.

Europe Pet Food Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Pet Types Covered | Dog Food, Cat Food, Others |

| Product Types Covered | Dry Pet Food, Wet and Canned Pet Food, Snacks and Treats |

| Pricing Types Covered | Mass Products, Premium Products |

| Ingredient Types Covered | Animal Derived, Plant Derived |

| Distribution Channels Covered | Supermarkets and Hypermarkets, Specialty Stores, Online Stores, Others |

| Countries Covered | Germany, France, United Kingdom, Italy, Spain, Others |

| Companies Covered | Mars Petcare, Nestlé Purina PetCare, Hill's Pet Nutrition, Affinity Petcare, Zooplus AG, Versele-Laga, Animonda, Brit (VAFO Group), Edgard & Cooper, Butternut Box, Josera |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Europe Pet Food Market Report

The Europe pet food market was valued at USD 37.77 Billion in 2025, reflecting steady growth from USD 28.36 Billion in 2020 across 139 million European pet-owning households

Dog food leads with a 42.09% share in 2025, driven by Europe's 104 million dog population and higher per-unit revenue from breed-specific and functional nutrition formulations.

Dry pet food leads at 57.18%, followed by wet and canned pet food at 26.13%, and snacks and treats at 16.69% in 2025, reflecting Europe's high affinity for both dry convenience and wet palatability.

Germany leads with a 26.0% revenue share in 2025, supported by Europe's highest per-pet annual expenditure of EUR 520, strong premium adoption, and 28% online sales penetration.

The United Kingdom holds a 20.1% share in 2025, Europe's second-largest market – and is its most innovation-receptive, accounting for ~40% of European insect-based pet food sales in 2024.

Snacks and treats is the fastest-growing product segment at ~7.9% CAGR through 2034, while insect-based protein ingredients represent the highest-growth innovation sub-segment at ~22.8% CAGR.

Leading companies include Mars Petcare (Pedigree, Whiskas, Royal Canin), Nestlé Purina (Pro Plan, Felix), Hill's Pet Nutrition, Affinity Petcare, and online retailer Zooplus AG.

Key drivers include pet humanization trends, rising single-person household spending on pets, premium functional nutrition demand, and rapid online subscription delivery channel expansion.

The EU Packaging Waste Regulation mandating 70% recyclability by 2030 is driving widespread adoption of mono-material packaging, paper-based pouches, and biodegradable films across leading European brands.

Following EU approval of nine insect species for pet food by 2025, insect protein is growing at ~22.8% CAGR in Europe, offering 40-60% lower carbon footprint versus beef-based equivalents.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade