Europe PET Packaging Market Size, Share, Trends and Forecast by Packaging Type, Form, Pack Type, Filling Technology, End User, and Country, 2026-2034

Europe PET Packaging Market Size & Forecast 2026-2034

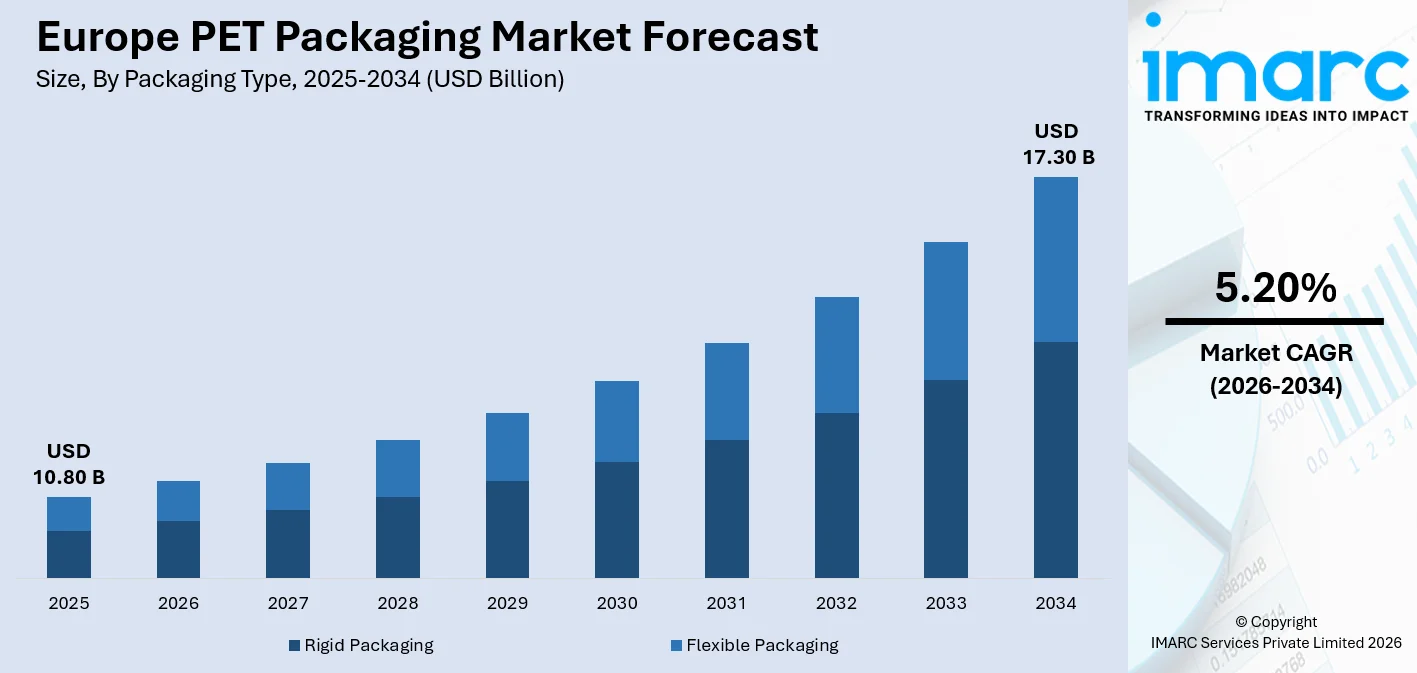

The Europe PET packaging market size was valued at USD 10.80 Billion in 2025 and is projected to reach USD 17.30 Billion by 2034, growing at a compound annual growth rate of 5.20% during 2026-2034, driven by the EU's Packaging and Packaging Waste Regulation (PPWR), rising demand for bottled water in cold-fill PET bottles, and rapid adoption of recycled PET (rPET) across rigid packaging applications, all reinforcing Europe PET packaging market share.

To get more information on this market Request Sample

Europe PET Packaging Industry Analysis - Key Insights

- Rigid Packaging holds a 75.0% share of the packaging type segment in 2025- its structural integrity, excellent barrier properties, and compatibility with cold-fill bottled water applications make it the dominant format across European beverage, food, and pharmaceutical end-user markets.

- Amorphous PET accounts for 65.0% of the form segment in 2025- its superior optical clarity, ease of thermoforming, and adaptability for bottles and trays sustain its commanding lead over crystalline PET, particularly in single-use beverage and food packaging applications.

- Bottles and Jars lead pack type at 60.0% in 2025- driven by surging bottled water consumption, carbonated soft drink packaging volumes, and ongoing lightweight bottle design innovations that reduce material usage while maintaining rigidity and consumer appeal across the region.

- Cold Fill represents the leading filling technology at 45.0% in 2025- non-carbonated water, juices, and isotonic beverage segments rely heavily on cold-fill PET lines, which offer cost efficiency, faster throughput, and compatibility with lightweight bottle designs.

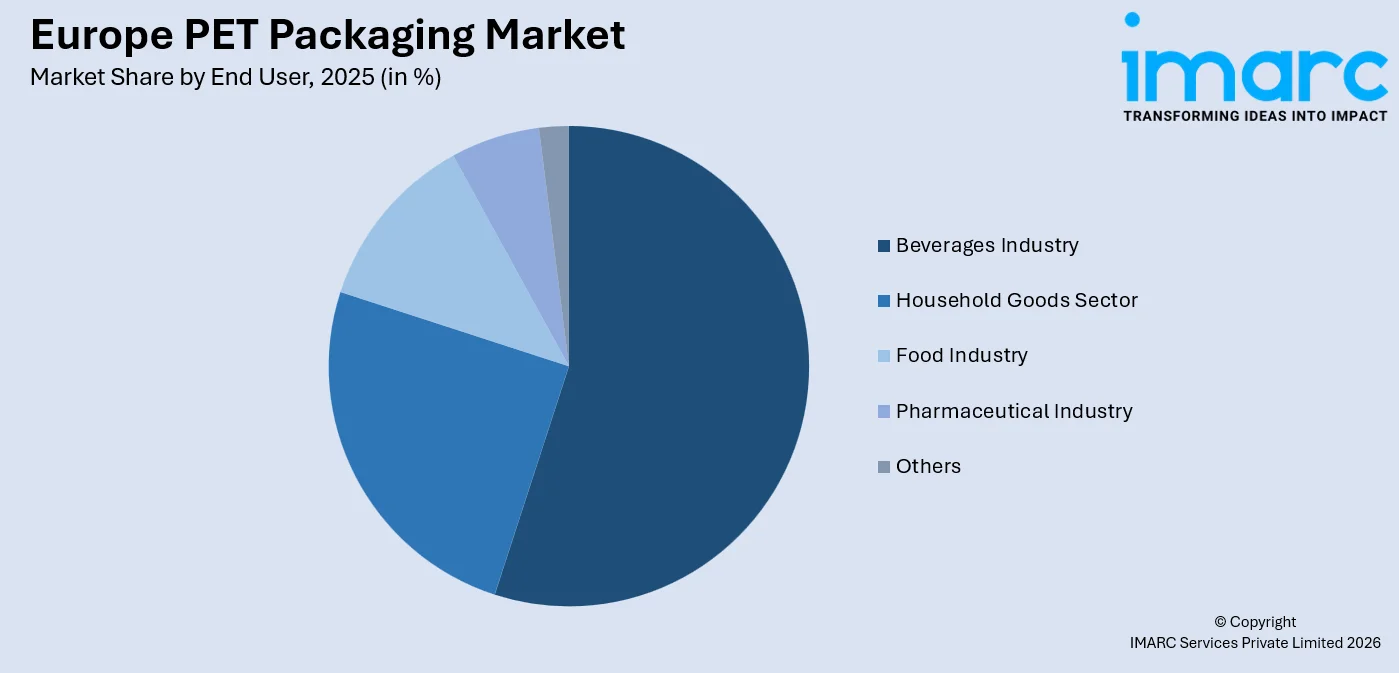

- Beverages Industry leads end user share at 55.0% in 2025- Europe's robust deposit-return infrastructure, premium mineral water culture, and widening consumer health consciousness collectively sustain PET as the dominant packaging format for bottled water across the continent.

- Germany leads country-level share at 22.0% in 2025- the country's world-leading Pfand deposit-return system achieving 98% container return rates, its large beverage manufacturing base, and stringent sustainability regulations collectively reinforce Germany's position as Europe's largest single national PET packaging market.

Europe PET Packaging Market Trends and Dynamic 2026:

Market Trends:

Mandatory rPET Content Thresholds Reshaping Procurement Strategies:

The EU's PPWR mandates 30% recycled content in contact-sensitive PET packaging (excluding beverage bottles) by 2025 and 50% by 2040, converting voluntary brand pledges into enforceable procurement obligations. In September 2025, Eastman and Doloop launched a 100% recycled PET beverage bottle using Eastman's Eastar Renew EN031 resin produced via molecular recycling, signalling the commercial maturity of next-generation rPET solutions.

Expanding Deposit-Return Schemes Elevating PET Collection Infrastructure:

Mandatory deposit-return schemes (DRS) under the PPWR require 90% plastic bottle collection by 2029. Austria launched its nationwide DRS for PET bottles on 1 January 2025, with a EUR 0.25 per container deposit. In 2025, DRS reached a monthly collection rate of 73% within its first 200 days, positioning Ireland strongly to achieve its EU target, exemplifying the model's effectiveness in rapidly boosting PET collection volumes and rPET feedstock quality across Europe.

Lightweight and Mono-Material Bottle Design Reducing Material Intensity:

Brands are embedding circularity through lightweighting, label-free designs, tethered closures, and mono-material construction to enhance PET recyclability. In 2025, Coca-Cola European Partners introduced a new 850ml 100% rPET bottle in Germany designed for smaller households. Simplified designs reduce sorting contamination, improve rPET output quality, and lower production carbon footprints, directly supporting the EU Green Deal and corporate decarbonisation reporting obligations.

- Cold-Fill Line Efficiency Gains: Manufacturers are investing in high-speed cold-fill lines to accommodate growing non-carbonated water and juice volumes, improving throughput while enabling adoption of thinner, lighter PET bottle preforms.

Growth Drivers:

EU Regulatory Mandates Driving Recycled Content and Circular Infrastructure Investment:

The EU's PPWR, which entered into force in February 2025, mandates recyclability for all packaging by 2030. These binding obligations are compelling brand owners, converters, and recyclers to invest in rPET production, bottle-to-bottle systems, and lightweight packaging design, structurally expanding the market for compliant PET packaging formats and technologies throughout Europe.

Surging Bottled Water Consumption Sustaining PET Beverage Bottle Demand:

Bottled water leads the Europe PET packaging end-user segment with 55% share, supported by rising consumer health consciousness, growing out-of-home consumption, and robust premium mineral water markets in Germany, France, Italy, and Spain. Euromonitor's 2025 consumer survey found that price remains the top purchasing criterion for 47% of food and drink consumers, sustaining demand for lightweight, cost-effective PET bottles over glass and aluminium alternatives.

Germany's World-Leading DRS Infrastructure Ensuring Premium rPET Feedstock Supply:

Germany's Pfand deposit-return system achieves a 98% container return rate, the world's highest, generating a consistent supply of high-quality post-consumer PET for food-grade recycling.

- Growth in Pharmaceutical PET Packaging: Pharmaceutical demand for tamper-evident, lightweight, and chemically resistant PET containers is growing, driven by Europe's aging population and expanding generic drug distribution channels.

- E-Commerce Packaging Expansion: PET's shatter-resistance, lightweight properties, and compatibility with automated packaging lines make it increasingly preferred for e-commerce food, beverage, and personal care distribution across European logistics networks.

- Aseptic Fill Technology Adoption: Food and dairy producers are shifting to aseptic PET filling to extend shelf life without refrigeration, expanding PET's application into ambient milk, juice, and ready-to-drink beverage categories across European markets.

Market Restraints:

rPET Price Premium Over Virgin PET Compressing Manufacturer Margins: In Europe, food-grade rPET commands approximately USD 750–800 per ton above virgin PET, creating a significant cost disadvantage for converters under pressure to increase recycled content to meet PPWR mandates. This price gap is slowing voluntary rPET adoption rates and straining packaging manufacturer margins, particularly for smaller converters lacking scale to absorb elevated raw material costs under binding compliance timelines.

Insufficient European Recycling Capacity to Meet PPWR Targets: Europe's PET recycling industry growth is near stagnant due to high production and energy costs, weak domestic demand for EU-recycled plastics, and competitive pressure from cheaper virgin and recycled PET imports. Industry experts warned that current European recycling capacity is insufficient to meet PPWR-mandated recycled content targets, creating structural supply shortfalls for food-grade rPET through the forecast period.

Competition from Alternative Packaging Materials Constraining PET Share: Metal beverage cans and glass bottles are recording stronger volume growth rates than PET in certain European segments. Coca-Cola's investment in refillable glass lines in Europe requires 50% of beverages in reusable packaging by 2030, and is beginning to divert some beverage volume away from single-use PET bottles in premium and on-premise market channels.

Europe PET Packaging Market Report Segmentation:

| Segment | Leading Category | Market Share | Year |

|---|---|---|---|

|

Packaging Type |

Rigid Packaging |

75.0% |

2025 |

|

Form |

Amorphous PET |

65.0% |

2025 |

|

Pack Type |

Bottles and Jars |

60.0% |

2025 |

|

Filling Technology |

Cold Fill |

45.0% |

2025 |

|

End User |

Beverages Industry |

55.0% |

2025 |

|

Country |

Germany |

22.0% |

2025 |

Packaging Type Insights

Rigid Packaging – 75.0% Market Share (2025) | Leading Packaging Type

Rigid PET packaging dominates due to its superior mechanical strength, clarity, and compatibility with high-volume cold-fill and aseptic beverage bottling lines. The EU's PPWR mandates 30% recycled content in contact-sensitive PET packaging (excluding beverage bottles) by 2025 and 50% by 2040, accelerating investment in bottle-to-bottle rPET systems. Germany's 98% DRS container return rate ensures premium rPET feedstock, supporting rigid bottle quality and enabling compliance with escalating mandatory recycled content thresholds through the forecast period.

|

Segment Breakdown Rigid Packaging (75.0%) · Flexible Packaging |

Form Insights

Amorphous PET – 65.0% Market Share (2025) | Leading Form

Amorphous PET dominates as the form of choice for transparent bottle and tray production, enabling manufacturers to achieve lightweight designs with consistent wall thickness. Its compatibility with both virgin and recycled PET streams simplifies rPET incorporation. In March 2025, Jokey launched new injection stretch blow moulded amorphous rPET containers for pharmaceutical and food applications, demonstrating expanding use cases beyond beverage bottles.

|

Segment Breakdown Amorphous PET (65.0%) · Crystalline PET |

Pack Type Insights

Bottles and Jars – 60.0% Market Share (2025) | Leading Pack Type

Bottles and jars dominate, driven by Europe's per-capita bottled water consumption culture, established carbonated soft drink packaging volumes, and expanding rPET bottle adoption. Coca-Cola European Partners' launch of an 850ml 100% rPET bottle in Germany in 2025 reflects brand-level commitment to rPET scaling. Lightweighting innovations continue to reduce per-unit PET resin requirements without compromising structural integrity, improving cost efficiency for high-volume beverage producers.

|

Segment Breakdown Bottles and Jars (60.0%) · Bags and Pouches · Trays · Lids/Caps and Closures · Others |

Filling Technology Insights

Cold Fill – 45.0% Market Share (2025) | Leading Filling Technology

Cold fill dominates because it enables faster bottling speeds, lower energy costs, and compatibility with lightweight thin-wall PET preforms that are unviable in hot-fill processes. Europe's large mineral water producers in France, Germany, and Italy rely primarily on cold-fill PET lines. The technology's efficiency advantages align directly with cost reduction priorities amid inflationary energy costs, reinforcing its dominant share across beverage end users.

|

Segment Breakdown Hot Fill · Cold Fill (45.0%) · Aseptic Fill · Others |

End User Insights

Access the comprehensive market breakdown Request Sample

Beverages Industry – 55.0% Market Share (2025) | Leading End User

Bottled water anchors Europe's PET packaging end-user market, driven by widespread consumer preference for hydration-on-the-go, tourism activity in water-rich markets like Italy, France, and Germany's DRS expansion to include juices and non-carbonated drinks further broadened the PET beverage packaging base.

|

Segment Breakdown Beverages Industry- (Bottled Water, Carbonated Soft Drinks, Milk and Dairy Products, Juices, Beer, and Others) (55.0%) · Household Goods Sector · Food Industry · Pharmaceutical Industry · Others |

Country Insights

Germany – 22.0% Market Share (2025) | Leading Country

Germany's Pfand DRS, first implemented in 2003 and most recently expanded in 2024 to include milk-based drinks in PET, generates premium post-consumer rPET volumes that directly feed the country's bottle-to-bottle recycling supply chain. Its commitment to circular economy mandates and high-quality packaging standards alongside a large food, beverage, and pharmaceutical manufacturing base positions Germany as the primary demand driver for both virgin and recycled PET packaging in Europe.

|

Country Breakdown Germany (22.0%) · United Kingdom · Italy · Spain · Others |

France:

France is the second-largest PET packaging market, supported by large mineral water brands including Evian and Volvic, active sustainability legislation under the Anti-Waste for a Circular Economy (AGEC) law, and growing demand for rPET in food and beverage formats. France's DRS rollout is anticipated to further boost PET bottle collection rates and domestic rPET supply.

United Kingdom:

The United Kingdom has a significant PET packaging market anchored by carbonated soft drink and bottled water consumption. England's DRS scheme for beverage containers is in the planning pipeline following Scotland's deferred launch, and the UK's Plastic Packaging Tax requiring 30% recycled content is directly driving rPET demand across British packaging converters and brand owners.

Italy:

Italy is a major bottled water market, ranking among Europe's highest per-capita consumers of packaged mineral water. Its large beverage and food packaging manufacturing sector generates consistent demand for PET bottles, trays, and jars. Italy's established PET recycling infrastructure and growing investments in mechanical and chemical recycling are enhancing domestic rPET availability.

Spain:

Spain's PET packaging market is supported by its large beverage and food processing industries, particularly in carbonated drinks, olive oil, and water packaging. Spain's SDDR (deposit-return) pilot programs are expanding, and its food industry's adoption of PET trays for fresh produce and ready meals is broadening end-user demand beyond the core beverage segment.

Others:

The remaining European markets, including Poland, the Netherlands, Belgium, Sweden, Austria, and others, represent a growing collective share. Austria launched its nationwide PET bottle DRS on 1 January 2025. Sweden's DRS achieves 87.6% PET bottle returns, exemplifying the performance potential of established schemes.

Market Outlook (2026-2034)

What is the future outlook of the Europe PET Packaging Market?

The Europe PET packaging market is projected to expand from USD 10.8 Billion in 2025 to USD 17.3 Billion by 2034, growing at a compound annual growth rate of 5.20%. The EU's PPWR mandates 30% recycled content in contact-sensitive PET packaging (excluding beverage bottles) by 2025 and 50% by 2040, and growing bottled water and aseptic beverage volumes will collectively sustain demand. Germany's continued regulatory leadership and expanding recycling infrastructure across France, Italy, and Eastern Europe will broaden the market's circular base through 2034.

Europe PET Packaging Market - Leading Key Players:

The Europe PET packaging market features global packaging conglomerates and regional specialists competing on rPET integration, lightweighting innovation, DRS compliance infrastructure, and pharmaceutical-grade container capabilities. Key players are expanding European recycling capacity and rPET supply chain partnerships to meet escalating PPWR-mandated content requirements.

| Company | Core Products | Strategic Highlights |

|---|---|---|

| Indorama Ventures | PET resin, rPET flake, bottle preforms. | Recycled over 150 billion post-consumer PET bottles since 2011; 20+ recycling facilities in 11 countries; 789 bottles recycled per second. |

| Alpla Group | PET bottles, preforms, recycled PET. | Opened EUR 60M PET recycling plant in 2024; targeting European rPET supply expansion to meet PPWR mandates. |

| Berry Global Group | PET bottles, containers, closures. | Expanding clarified PET container lines; growing pharmaceutical and food-grade packaging presence across Europe. |

Some of the other key players existing in the Europe PET packaging market include Amcor plc, Graham Packaging, Plastipak Holdings, Resilux NV, and RETAL Industries, among others.

Latest Development & News:

- September 2025: Eastman and PET packaging specialist Doloop announced a partnership to launch a 100% recycled PET beverage bottle utilising Eastman's Eastar Renew EN031 molecular recycling resin. The collaboration marks a commercial milestone for chemically recycled rPET in single-serve beverage packaging, offering brands a compliant solution for meeting EU 30% recycled content mandates by 2030.

- March 2025: Jokey disclosed new transparent packaging lines for the pharmaceutical and food sectors using injection stretch blow moulding of recycled PET. The containers address demand for food-contact-safe rPET transparent packaging, expanding rPET's commercial footprint into regulated pharmaceutical and specialty food packaging categories across European markets.

- January 2025: Austria launched a nationwide deposit-return scheme for single-use PET bottles and aluminium cans from 0.1 to 3 litres, with a EUR 0.25 per container refundable deposit operated by EWP Recycling Pfand Österreich gGmbH. The launch positions Austria to meet EU collection targets and generate high-quality rPET feedstock for the national and regional recycling supply chain.

Europe PET Packaging Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Packaging Types Covered | Rigid Packaging, Flexible Packaging |

| Forms Covered | Amorphous PET, Crystalline PET |

| Pack Types Covered | Bottles and Jars, Bags and Pouches, Trays, Lids/Caps and Closures, Others |

| Filling Technologies Covered | Hot Fill, Cold Fill, Aseptic Fill, Others |

| End Users Covered |

|

| Countries Covered | Germany, France, United Kingdom, Italy, Spain, Others |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Europe PET packaging market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the Europe PET packaging market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Europe PET packaging industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Europe PET Packaging Market Report

The Europe PET packaging market was valued at USD 10.80 Billion in 2025.

The Europe PET packaging market is projected to reach USD 17.30 Billion by 2034.

Rigid Packaging dominates the market with a 75.0% share, driven by its structural integrity, barrier properties, and widespread use in beverage, food, and pharmaceutical PET containers across Europe's high-volume cold-fill and aseptic bottling production lines.

Amorphous PET leads the form segment at 65.0%, valued for its optical clarity, thermoformability, and versatility in beverage bottles and food trays, with growing rPET integration driven by EU mandatory recycled content thresholds.

Bottles and Jars account for 60.0% of pack type share, sustained by Europe's large bottled water and carbonated soft drink sectors, lightweighting innovations, and regulatory mandates supporting rPET bottle adoption across major beverage markets.

Cold Fill leads at 45.0%, preferred for bottled water and carbonated beverage lines due to its cost efficiency, faster throughput, and compatibility with lightweight thin-wall PET preforms, incompatible with hot-fill thermal demands.

The Beverages Industry – Bottled Water segment commands 55.0% share, anchored by Europe's mineral water culture, rising health-oriented hydration trends, and PET's unmatched cost and weight advantages over glass for high-volume bottled water packaging.

Germany leads with a 22.0% country share, supported by the world's highest-performing Pfand deposit-return system, achieving 98% container returns, a large beverage manufacturing base, and stringent circular economy regulations.

Key players include Indorama Ventures, Alpla Group, Berry Global, Amcor plc, Graham Packaging, Plastipak Holdings, Resilux NV, RETAL Industries, Esterform Packaging, and Greiner Packaging, competing through rPET integration, lightweighting, and PPWR compliance innovation.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)