Europe Renewable Energy Market Size, Share, Trends and Forecast by Type, End User, and Country, 2026-2034

Europe Renewable Energy Market Size, Share, Trends & Forecast (2026-2034)

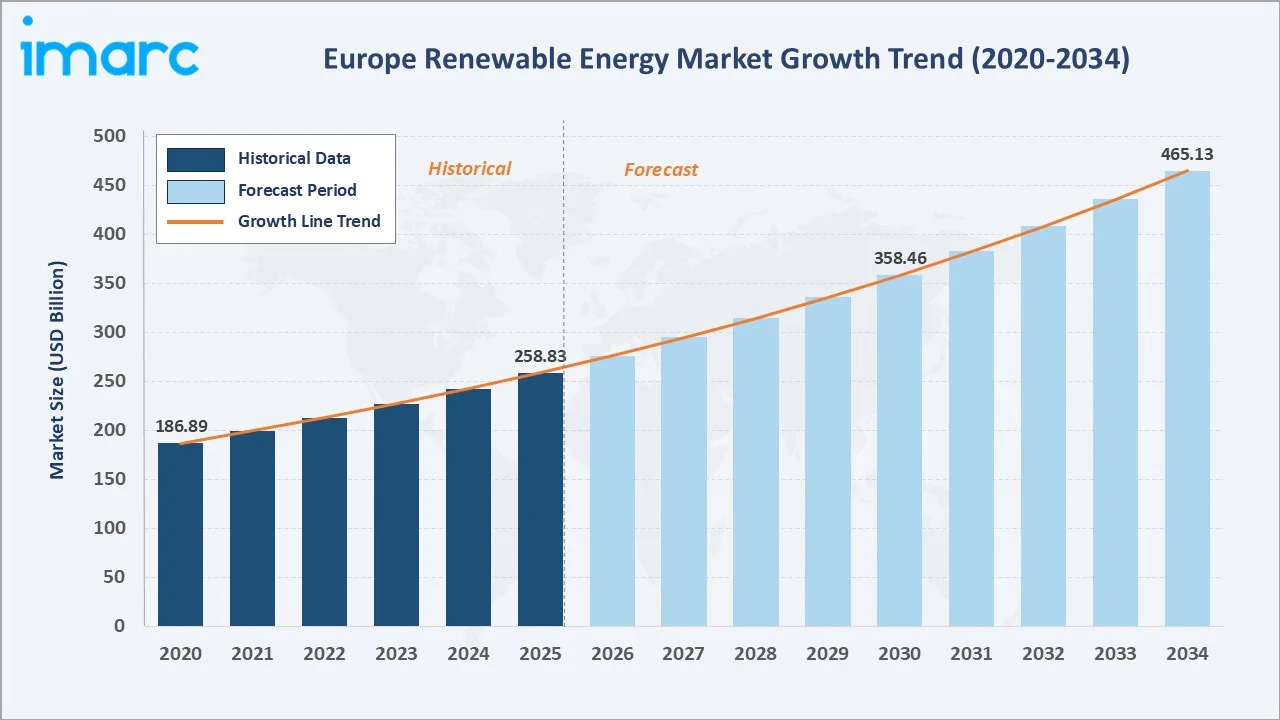

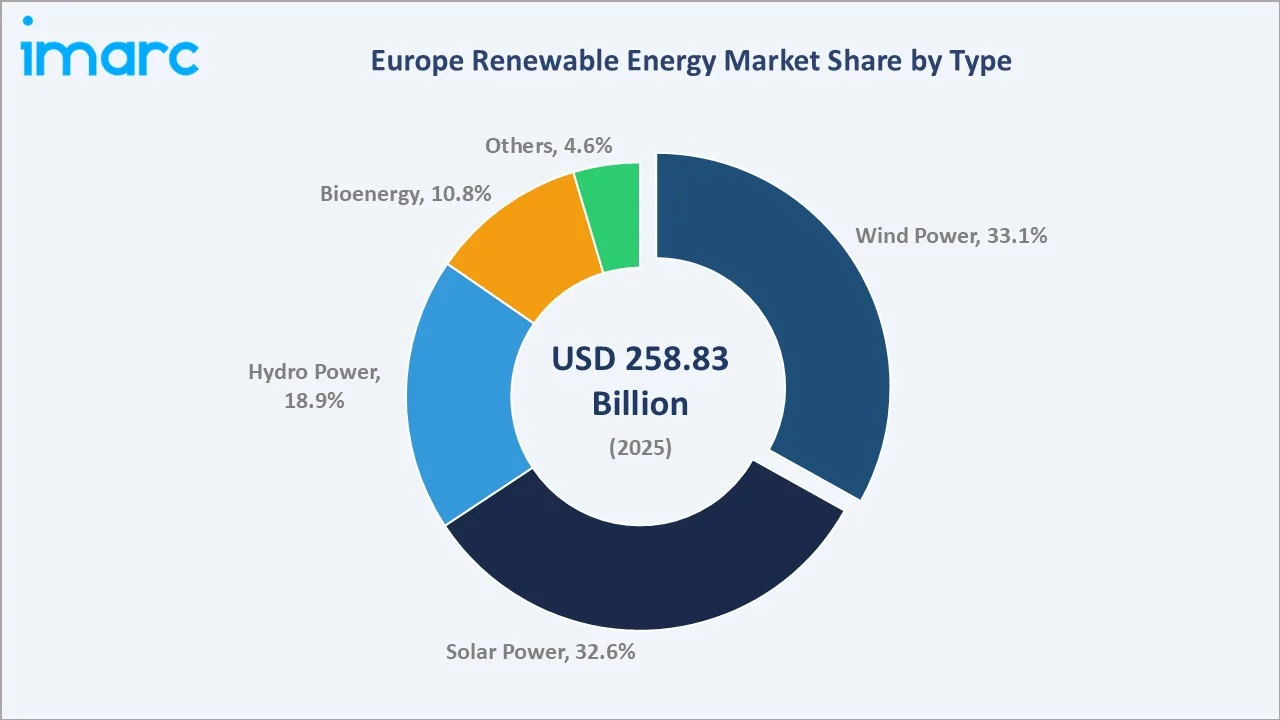

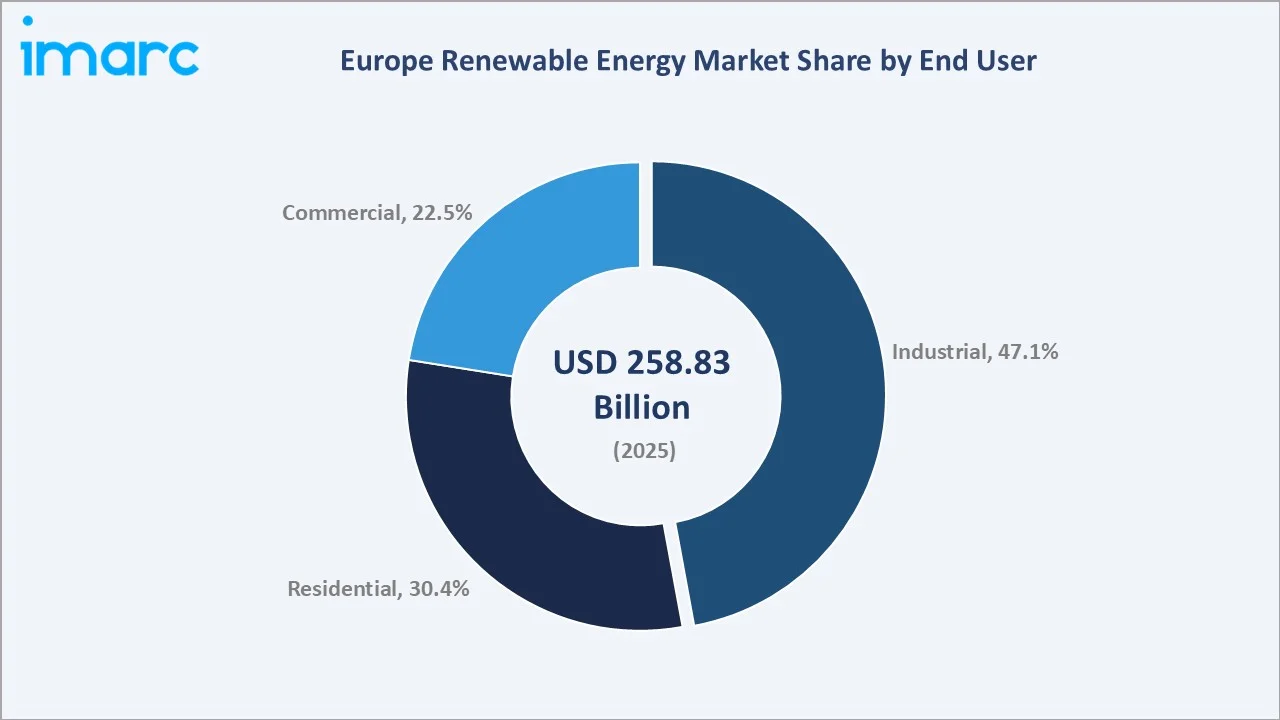

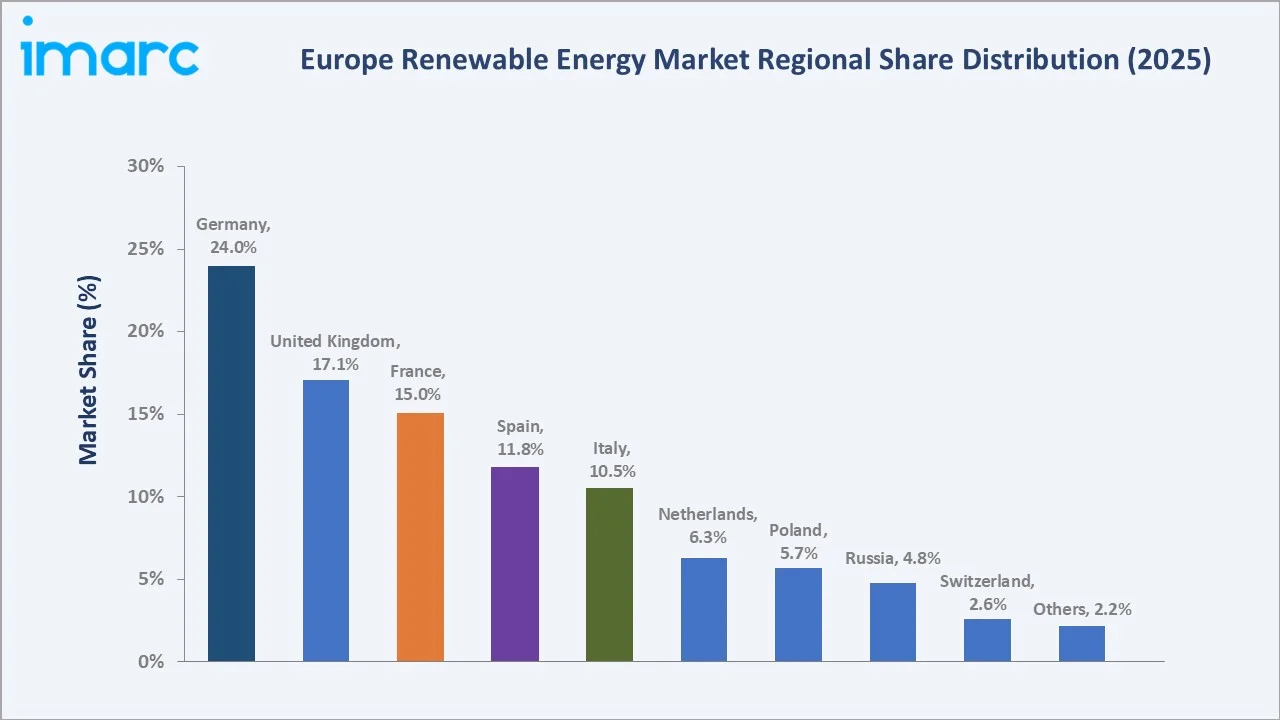

The Europe renewable energy market size was valued at USD 258.83 Billion in 2025 and is projected to reach USD 465.13 Billion by 2034, exhibiting a CAGR of 6.73% during the forecast period 2026-2034. The acceleration of the EU Green Deal and Fit for 55, the REPowerEU plan's response to energy-security imperatives, falling levelised cost of electricity (LCOE) for wind and solar, rapid scale-up of offshore wind in the North Sea and Baltic, corporate PPA expansion, and the emergence of green hydrogen are driving the Europe renewable energy market growth. Wind power leads the technology mix at 33.1% share in 2025, industrial users account for 47.1% of demand, and Germany dominates country revenue with 24.0% of regional output.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 258.83 Billion |

|

Forecast Market Size (2034) |

USD 465.13 Billion |

|

CAGR (2026-2034) |

6.73% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Country |

Germany (24.0% share, 2025) |

|

Leading Type |

Wind Power (33.1%, 2025) |

|

Leading End User |

Industrial (47.1%, 2025) |

The Europe renewable-energy market growth trajectory from 2020 through 2034 reflects the continent's decisive pivot from fossil fuels to clean generation, propelled by the EU Green Deal, the REPowerEU plan, rapid cost declines in wind and solar, and record corporate and utility power-purchase-agreement activity across Germany, the UK, France, Spain, and Italy.

To get more information on this market, Request Sample

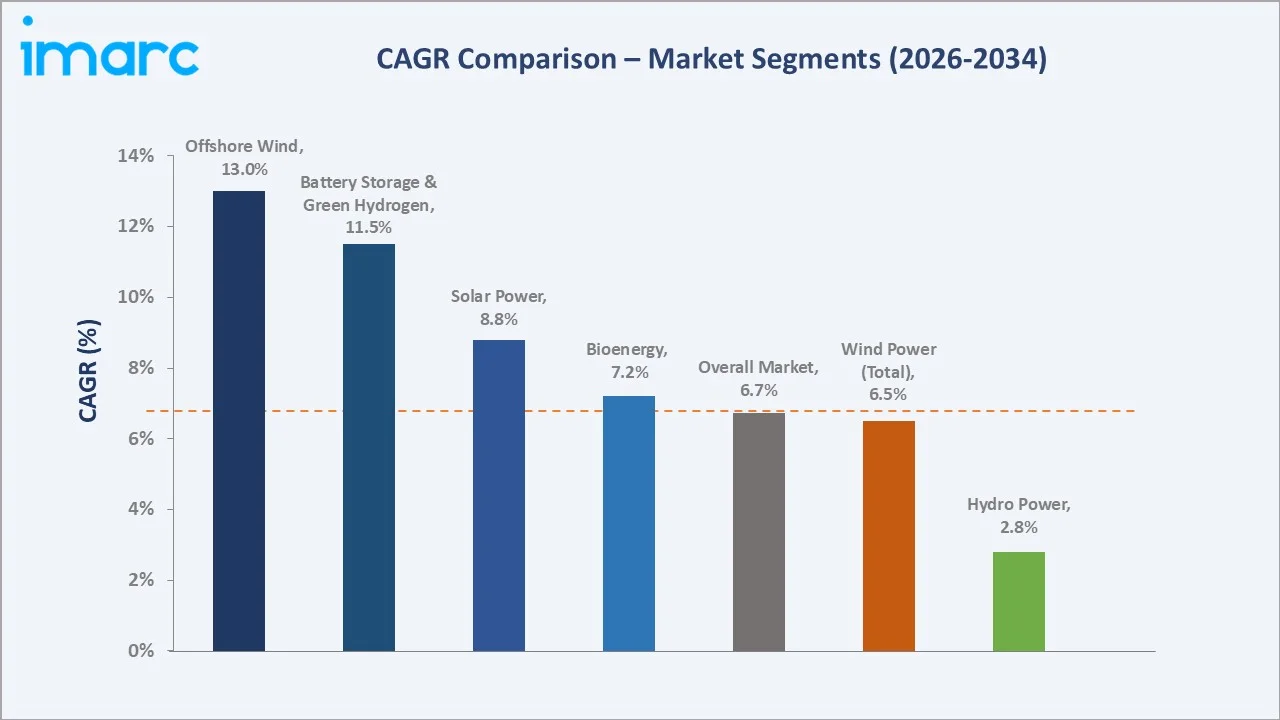

Segment-level CAGR comparisons highlight Offshore Wind and Battery Storage & Green Hydrogen as the fastest-growing sub-categories within the Europe renewable energy market forecast through 2034, outpacing traditional hydro infrastructure and slower-growth conventional energy segments.

Executive Summary

The Europe renewable energy market is entering its most consequential growth decade, driven by climate policy, energy security, industrial decarbonisation, and the electrification of end-use demand. Valued at USD 258.83 Billion in 2025, the market is forecast to reach USD 465.13 Billion by 2034 at a CAGR of 6.73%, representing over USD 206 billion of incremental investment and revenue across generation, grid, and storage assets.

Wind power leads the technology mix at 33.1% share in 2025, anchored by onshore and rapidly expanding offshore capacity in the North Sea, Baltic, and Atlantic basins. Solar power follows closely at 32.6%, underpinned by REPowerEU's solar roll-out, record rooftop and utility-scale installations in Germany, Spain, the Netherlands, and Italy, and continued module-cost deflation. Hydro power (18.9%), bioenergy (10.8%), and other sources (4.6%) complete the generation mix.

Industrial users account for 47.1% of consumption, reflecting the decarbonisation of steel, chemicals, cement, and manufacturing through corporate PPAs and on-site generation. Residential (30.4%) and commercial (22.5%) segments are scaling fast, supported by rooftop solar, heat electrification, and EV charging. Germany leads with 24.0% share, followed by the UK (17.1%), France (15.0%), Spain (11.8%), and Italy (10.5%). The Europe renewable energy market outlook remains highly positive as offshore wind, green hydrogen, grid reinforcement, and storage scale-up reshape the continental energy system through 2034.

Key Market Insights

|

Insight |

Data |

|

Largest Type |

Wind Power – 33.1% share (2025) |

|

Second Type |

Solar Power – 32.6% share (2025) |

|

Third Type |

Hydro Power – 18.9% share (2025) |

|

Largest End User |

Industrial – 47.1% share (2025) |

|

Second End User |

Residential – 30.4% share (2025) |

|

Third End User |

Commercial – 22.5% share (2025) |

|

Largest Country |

Germany – 24.0% share (2025) |

|

Forecast CAGR (2026-2034) |

6.73% |

|

Top Companies |

Iberdrola, RWE, Ørsted, EDF, Enel Green Power |

Key Analytical Observations Supporting the Above Data:

- Wind power's 33.1% leadership reflects the scale of onshore capacity across Germany, Spain, France, and the UK, combined with the acceleration of offshore projects in the North Sea, Baltic Sea, Irish Sea, and Atlantic coast under the European Wind Power Action Plan.

- Solar's 32.6% share is propelled by REPowerEU's solar deployment target of over 600 GW by 2030, rapid rooftop penetration in Germany and the Netherlands, record utility-scale additions in Spain and Italy, and continued PV module cost deflation.

- Industrial users' 47.1% majority is anchored by the decarbonisation of heavy industry, rapid growth in corporate PPAs (Amazon, Google, Microsoft, Meta, Stellantis, ArcelorMittal), and the scale-up of green hydrogen and electrified process heat across Germany, France, and the Nordics.

- Residential's 30.4% share reflects the Solar Rooftop Initiative, the revised Energy Performance of Buildings Directive, and the rapid scale-up of residential PV and heat-pump installations across Germany, the Netherlands, Belgium, and Austria.

- Germany's 24.0% country lead reflects its installed wind and solar base, the Energiewende framework, the federal EUR 500 billion climate and infrastructure fund, and a strong industrial-decarbonisation pipeline supported by H2Global and the National Hydrogen Strategy.

Europe Renewable Energy Market Overview

The Europe renewable energy market encompasses the generation, transmission, and consumption of electricity and heat from renewable sources, including onshore and offshore wind, utility-scale and distributed solar photovoltaic and concentrated solar power, large-scale and run-of-river hydro, bioenergy (solid biomass, biogas, biomethane, liquid biofuels), and a growing 'others' layer that includes geothermal, marine energy, and emerging technologies such as green hydrogen. The market covers project development, equipment manufacturing, EPC services, grid integration, storage, and off-take through utilities, corporate PPAs, and retail supply.

Demand is shaped by binding EU climate targets (Fit for 55, Net-Zero Industry Act, REPowerEU), national net-zero commitments, the EU Emissions Trading System carbon price, and rapid electrification of transport, heat, and industry. Supply-side dynamics revolve around capex cycles, supply-chain localisation for wind and solar manufacturing, permitting reform under RED III, grid expansion by ENTSO-E member TSOs, and the scale-up of storage and flexibility resources. Together, these forces are reshaping Europe's energy system from a fossil-fuel-dominant model to one structured around clean generation, flexible demand, and decarbonised molecules.

Market Dynamics

To evaluate market opportunities, Request Sample

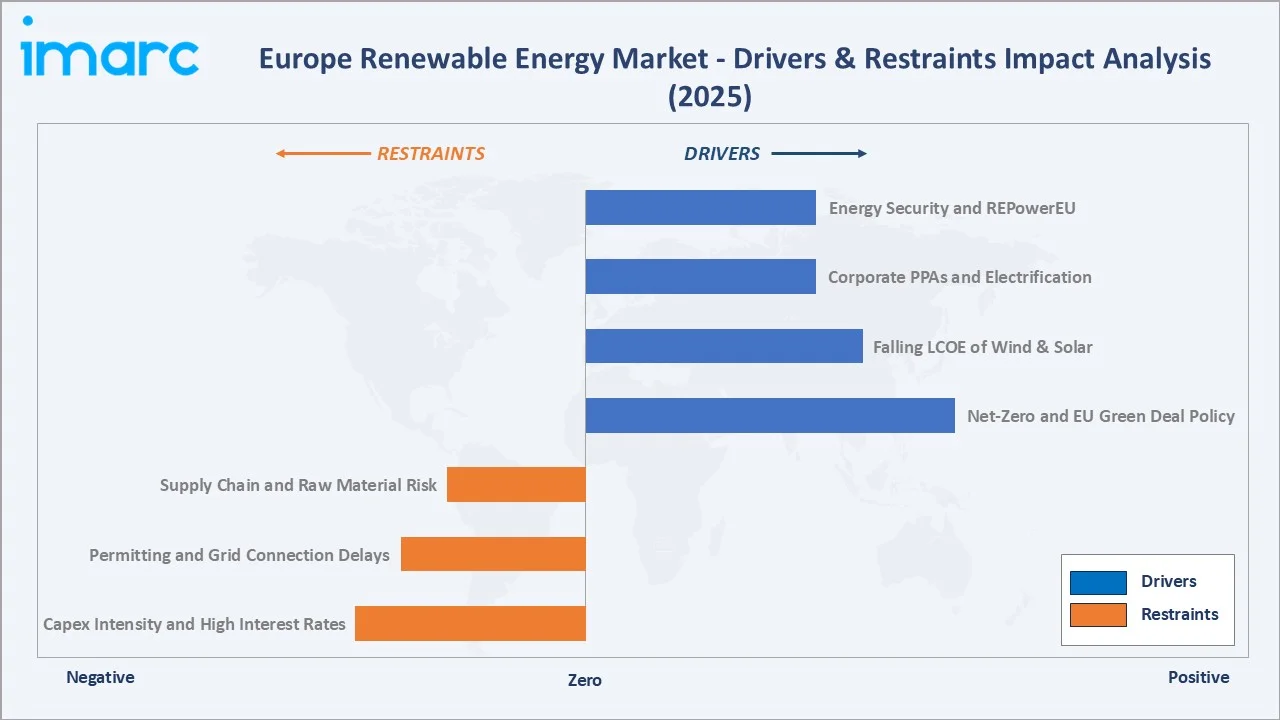

Market Drivers

- Net-Zero and EU Green Deal Policy: The EU's binding 2030 target of at least 42.5% renewable energy share under RED III, the Fit for 55 package, and national net-zero commitments across Germany, the UK, France, and the Nordics provide a decade-long policy tailwind for new generation capacity and supporting infrastructure.

- Energy Security and REPowerEU: REPowerEU, adopted in 2022 in response to the Russia-Ukraine conflict, mobilised up to EUR 300 billion to accelerate renewables, reduce fossil-fuel imports, and scale hydrogen. The programme dramatically elevated the political priority of wind, solar, and storage deployment across member states.

- Falling LCOE of Wind and Solar: Continued cost declines in solar PV modules, inverters, and onshore and offshore wind turbines have made new-build renewables competitive with wholesale power prices across most European markets, unlocking subsidy-free project pipelines and competitive auction outcomes.

- Corporate PPAs and Electrification: Record corporate PPA signings by hyperscale cloud operators, automotive groups, steel, chemicals, and fast-moving-consumer-goods companies, combined with the structural electrification of heat (heat pumps), transport (EVs), and industry, is expanding clean-electricity demand well beyond the traditional utility off-take channel.

Market Restraints

- Capex Intensity and High Interest Rates: Renewables and grid assets are highly capital-intensive. The 2023-2025 interest-rate environment compressed returns on offshore-wind projects, triggered selective project cancellations, and increased the cost of capital for pipeline projects.

- Permitting and Grid Connection Delays: Lengthy permitting timelines in Germany, France, and the UK, combined with constrained grid-connection capacity and TSO queues, remain the single largest deployment bottleneck across wind, solar, and storage assets.

- Supply Chain and Raw Material Risk: European wind OEMs (Vestas, Siemens Gamesa, Nordex) faced persistent margin and quality challenges in 2023-2024, while solar supply chains remain heavily dependent on Chinese imports, exposing the sector to trade and security policy risk.

- Intermittency and Storage Gap: Rising variable renewable penetration is creating structural demand for flexibility, storage, and interconnection that is not keeping pace with generation build-out, occasionally leading to curtailment, negative price events, and political backlash.

Market Opportunities

- Offshore Wind Scale-up: The European Wind Power Action Plan, national North Sea and Baltic Sea agreements, and UK Contracts for Difference rounds are unlocking over 300 GW of planned offshore-wind capacity by 2050, representing a multi-hundred-billion-euro opportunity for developers, EPCs, OEMs, and supply-chain investors.

- Green Hydrogen and Power-to-X: REPowerEU targets 20 million tonnes of renewable hydrogen (10 Mt domestic production, 10 Mt imports) by 2030, supported by the European Hydrogen Bank, H2Global, and Important Projects of Common European Interest (IPCEI), anchoring a new demand layer for dedicated renewables and electrolysers.

- Grid Reinforcement and Storage: The EU's 10-Year Network Development Plan and national TSO investment plans together require over EUR 584 billion of grid investment by 2030, alongside rapidly expanding battery-storage deployment, providing long-duration opportunities for grid specialists and storage integrators.

Market Challenges

- Workforce and Skills Gap: Europe faces a structural shortage of wind-turbine technicians, solar installers, grid engineers, and offshore construction specialists, threatening to slow deployment of the 2030 capacity targets across multiple member states.

- Social Acceptance and Land Use: Local opposition to onshore wind, large-scale solar, and transmission infrastructure continues to lengthen approval timelines, requiring more sophisticated community-engagement and benefit-sharing models.

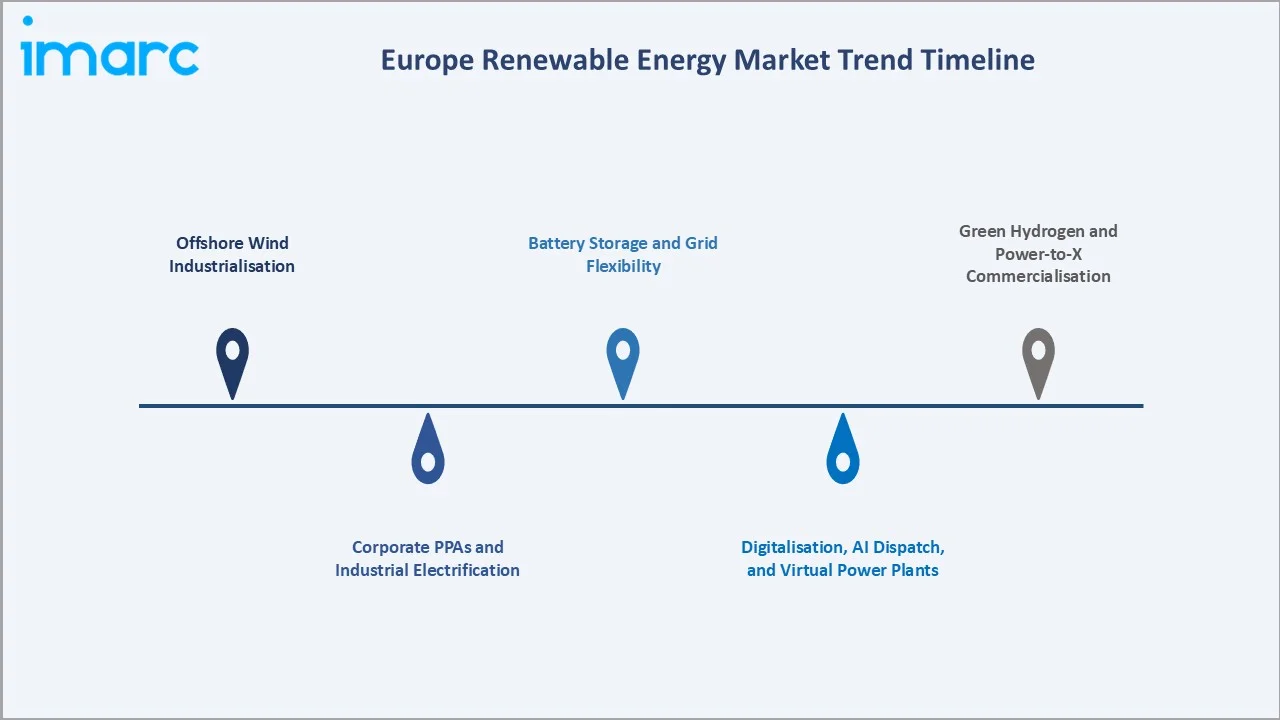

Emerging Market Trends

1. Offshore Wind Industrialisation

Offshore wind is moving from project-led deployment to industrialised delivery across the North Sea, Baltic Sea, Irish Sea, and Atlantic coasts. Denmark, the UK, Germany, the Netherlands, and Belgium are jointly scaling cross-border cooperation, with floating offshore wind now advancing from prototype to commercial-scale projects in France, Norway, and the UK.

2. Green Hydrogen and Power-to-X Commercialisation

Electrolyser manufacturing capacity is scaling rapidly in Germany, Spain, Denmark, and the Netherlands. Flagship green-hydrogen projects such as H2Global, HyDeal, and NortH2 are moving toward final investment decisions, catalysed by the European Hydrogen Bank and Important Projects of Common European Interest (IPCEI) funding.

3. Corporate PPAs and Industrial Electrification

Corporate power-purchase-agreement volumes have set successive records across Europe, led by hyperscale cloud operators, steel and aluminium producers, and automotive OEMs. Industrial electrification – heat pumps for process heat, electric arc furnaces, and green-hydrogen-based DRI steel – is converting a large share of heavy-industry demand into clean-electricity demand through 2034.

4. Battery Storage and Grid Flexibility

Grid-scale battery storage is expanding rapidly in the UK, Germany, Italy, and Spain, supported by capacity-market reforms, ancillary-services revenues, and rising price volatility. Long-duration storage, pumped hydro upgrades, and demand-side flexibility platforms are scaling in parallel to address increasing variable-renewable penetration.

5. Digitalisation, AI Dispatch, and Virtual Power Plants

AI-driven forecasting, virtual power plants, and smart-meter-enabled flexibility are becoming core competitive tools for utilities, IPPs, and aggregators. Statkraft, Iberdrola, Engie, and Octopus Energy are investing heavily in digital platforms to optimise dispatch, trading, and customer engagement across European power markets.

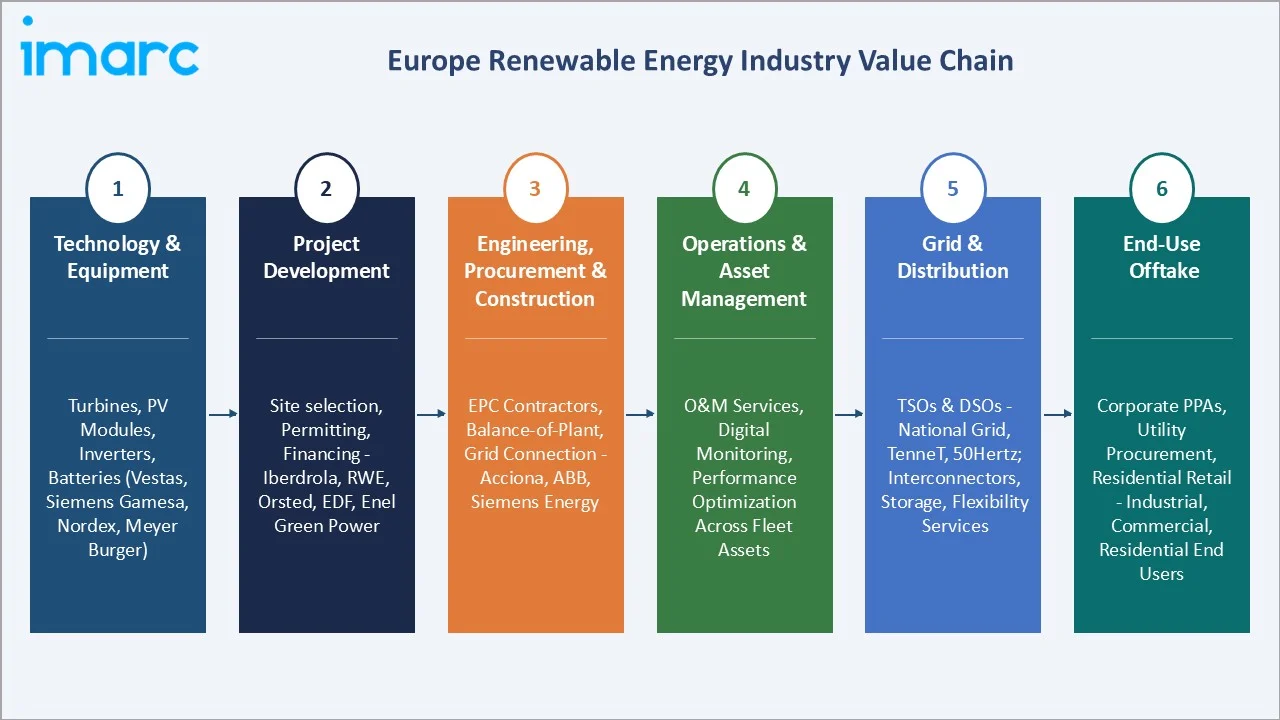

Industry Value Chain Analysis

The Europe renewable energy industry value chain spans five integrated stages from equipment manufacturing through end-consumer off-take. Each stage features distinct competitive dynamics, margin profiles, and technology-investment requirements relevant to the overall Europe renewable energy market analysis.

|

Value Chain Stage |

Key Participants / Description |

|

Equipment & OEMs |

Wind turbines, PV modules, inverters, electrolysers, cables |

|

EPC & Installation |

Project construction, balance-of-plant, grid connection |

|

Project Development & IPPs |

Utilities, independent power producers, infrastructure |

|

Grid, Storage & Flexibility |

TSOs, DSOs, battery integrators, flexibility aggregators |

|

Off-Take & Consumption |

Utilities, corporate PPAs, retail supply – Industrial, commercial, and residential consumers across EU 27, UK, Switzerland, Norway, Russia |

Project developers and utilities capture the highest strategic value by integrating origination, financing, construction, and long-term asset ownership. Equipment OEMs and grid specialists capture technology- and scale-driven margins, while TSOs and DSOs occupy regulated but structurally critical positions at the heart of Europe's clean-energy transition.

Technology Landscape in the Europe Renewable Energy Industry

Offshore and Floating Wind

Fixed-bottom offshore wind is scaling rapidly in the North Sea, Baltic, and Irish Sea. Floating offshore wind is advancing from prototype to commercial scale through projects in Scotland (Hywind Tampen extension, MarramWind, CampionWind), Norway, and France, opening deep-water sites that were previously inaccessible.

Solar PV and Agri-PV

Utility-scale solar continues to benefit from record low module pricing, bifacial and TOPCon technology adoption, and dedicated European manufacturing initiatives under the Net-Zero Industry Act. Agri-PV, floating solar, and solar-plus-storage hybrids are emerging sub-segments across Germany, France, the Netherlands, and Spain.

Green Hydrogen and Electrolysers

European electrolyser manufacturing is scaling through investment by Siemens Energy, Nel, Thyssenkrupp Nucera, Sunfire, McPhy, and ITM Power. Alkaline, PEM, and emerging SOEC technologies are being deployed in large-scale projects across Germany, Denmark, the Netherlands, and Spain, supported by IPCEI, the Innovation Fund, and the European Hydrogen Bank.

Battery Storage and Grid Digitalisation

Grid-scale lithium-ion batteries are expanding rapidly in the UK, Germany, and Italy. Virtual power plants, AI-powered dispatch platforms, and smart-grid infrastructure are scaling in parallel, integrating variable renewables, storage, EVs, and flexible industrial loads into unified operational systems.

Market Segmentation Analysis

IMARC Group provides an analysis of the key trends in each segment of the Europe renewable energy market, along with forecasts at the regional and country levels from 2026 to 2034. The market has been categorized based on type and end user.

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Type | Wind Power | 33.12% | 2025 |

| End User | Industrial | 47.08% | 2025 |

| Country | Germany | 24.0% | 2025 |

Market Breakup by Type

Wind power leads the Europe renewable energy market with a 33.1% share in 2025. Onshore wind remains the dominant installed capacity base, concentrated in Germany, Spain, France, and the UK, while offshore wind is the fastest-growing generation segment, driven by the North Sea and Baltic Sea agreements, UK Contracts for Difference allocations, and accelerating German and Dutch tender pipelines. Floating offshore wind is transitioning from demonstration to commercial scale in the UK, France, and Norway.

To access detailed market analysis, Request Sample

Solar power accounts for 32.6% of the market, powered by REPowerEU's 600+ GW solar target for 2030, record rooftop penetration in Germany and the Netherlands, and utility-scale additions in Spain, Italy, and Poland. Hydro power (18.9%) remains the largest renewable baseload source, anchored by large reservoir assets in Norway, Sweden, Austria, France, and Switzerland, supporting grid flexibility alongside variable renewables.

Bioenergy contributes 10.8%, driven by biomass power, biogas, and biomethane, particularly in Germany, Sweden, Finland, and Italy. The 'others' category (4.6%) captures geothermal, marine energy, and emerging technologies such as green hydrogen-to-power and concentrated solar power, all positioned as long-duration growth frontiers through 2034.

|

Type |

Share (2025) |

Key Demand Drivers |

|

Wind Power |

33.1% |

Onshore + offshore; North Sea and Baltic scale-up; Germany, UK, Spain, France lead |

|

Solar Power |

32.6% |

REPowerEU 600+ GW target; rooftop in Germany and Netherlands; utility-scale in Spain and Italy |

|

Hydro Power |

18.9% |

Reservoir and run-of-river; Norway, Sweden, Austria, France, Switzerland; grid flexibility |

|

Bioenergy |

10.8% |

Biomass, biogas, biomethane; Germany, Sweden, Finland, Italy |

|

Others |

4.6% |

Geothermal, marine energy, green hydrogen-to-power, CSP |

Market Breakup by End User

Industrial end users represent 47.1% of demand in 2025, reflecting Europe's intensified industrial decarbonisation push. Heavy industry segments – steel, cement, chemicals, aluminium, refining – are procuring renewable electricity through long-term corporate PPAs, direct on-site generation, and green-hydrogen supply agreements. Hyperscale cloud operators (Amazon, Microsoft, Google, Meta) are now among the largest corporate PPA buyers across the Nordics, Iberia, and Ireland.

Residential end users account for 30.4%, supported by rooftop solar, residential battery storage, and heat-pump electrification under the Energy Performance of Buildings Directive. Germany, the Netherlands, Belgium, Austria, and Italy lead residential PV penetration, while rooftop solar grants and net-billing schemes continue to accelerate adoption across member states.

Commercial users capture 22.5%, anchored by retail, logistics, healthcare, education, and office sectors deploying rooftop solar, behind-the-meter storage, and corporate PPAs to meet CSRD-aligned emissions targets. EV-charging infrastructure is emerging as a significant commercial-demand driver, particularly in Germany, France, the UK, and the Nordics.

|

End User |

Share (2025) |

Key Demand Drivers |

|

Industrial |

47.1% |

Corporate PPAs, heavy-industry decarbonisation, hyperscale data centres, green hydrogen |

|

Residential |

30.4% |

Rooftop solar, heat pumps, EV charging, residential storage, EPBD-aligned retrofit |

|

Commercial |

22.5% |

Rooftop solar and PPAs for retail, logistics, healthcare; CSRD-aligned targets; EV charging |

Regional (Country-Level) Market Insights

Germany commands 24.0% of Europe renewable energy revenue in 2025, reflecting the scale of its installed onshore-wind and solar base, the Energiewende framework, The EU has mobilised over €700 billion through the Recovery and Resilience Facility, the core instrument of NextGenerationEU, to fund reforms and investments supporting the green transition and infrastructure development across member states. Germany is also the European leader in residential rooftop solar, heat-pump deployment, and emerging green-hydrogen infrastructure under the National Hydrogen Strategy and H2Global.

The United Kingdom contributes 17.1% of regional revenue, anchored by the world's most developed offshore-wind cluster, the Contracts for Difference framework, and the Future System Operator reforms. UK grid-scale battery storage is the most liquid market in Europe, and the UK also leads on nascent floating-offshore-wind deployment and the Hydrogen Business Model.

France accounts for 15.0%, with a balanced portfolio of hydro, onshore wind, solar, and a rapidly scaling offshore-wind pipeline. France’s energy transition is supported by the €54 billion France 2030 investment plan and the Multiannual Energy Programme (PPE), which together drive long-term investment in renewables, low-carbon technologies, and energy infrastructure. Spain captures 11.8% on the back of Europe's most active utility-scale solar market, a strong onshore-wind base, corporate PPA leadership, and Andalusia- and Aragón-focused green-hydrogen valleys.

Italy represents 10.5%, underpinned by the PNRR Recovery Plan, the PNIEC energy-and-climate plan, and rapid utility-scale solar deployment. The Netherlands (6.3%) leads Europe in rooftop-solar density, offshore-wind tendering, and green-hydrogen infrastructure. Poland (5.7%) is scaling onshore wind, solar, and early-stage offshore wind in the Baltic. Russia (4.8%), Switzerland (2.6%), and Others (2.2%) complete the regional mix, with the Nordics, Ireland, Austria, Greece, and the Balkans continuing to expand wind, solar, hydro, and geothermal deployment through 2034.

|

Country |

Share (2025) |

Key Growth Drivers |

|

Germany |

24.0% |

Energiewende, offshore wind, rooftop solar, National Hydrogen Strategy, EUR 500B fund |

|

United Kingdom |

17.1% |

Offshore wind leadership, CfD rounds, battery storage, floating wind, hydrogen business model |

|

France |

15.0% |

Hydro + nuclear backbone, offshore wind pipeline, France 2030, PPE plan |

|

Spain |

11.8% |

Utility-scale solar, onshore wind, green hydrogen valleys, corporate PPAs |

|

Italy |

10.5% |

PNRR Recovery Plan, PNIEC, utility-scale solar, bioenergy, geothermal |

|

Netherlands |

6.3% |

Rooftop solar density, offshore-wind tenders, NortH2 green-hydrogen project |

|

Poland |

5.7% |

Onshore wind, solar, early-stage Baltic offshore wind, coal-to-renewables pivot |

|

Russia |

4.8% |

Hydro dominant, limited wind and solar; structural constraints under sanctions |

|

Switzerland |

2.6% |

Hydro-anchored, solar and storage scale-up, grid flexibility |

|

Others |

2.2% |

Nordics, Ireland, Austria, Balkans, Greece – wind, hydro, solar, geothermal |

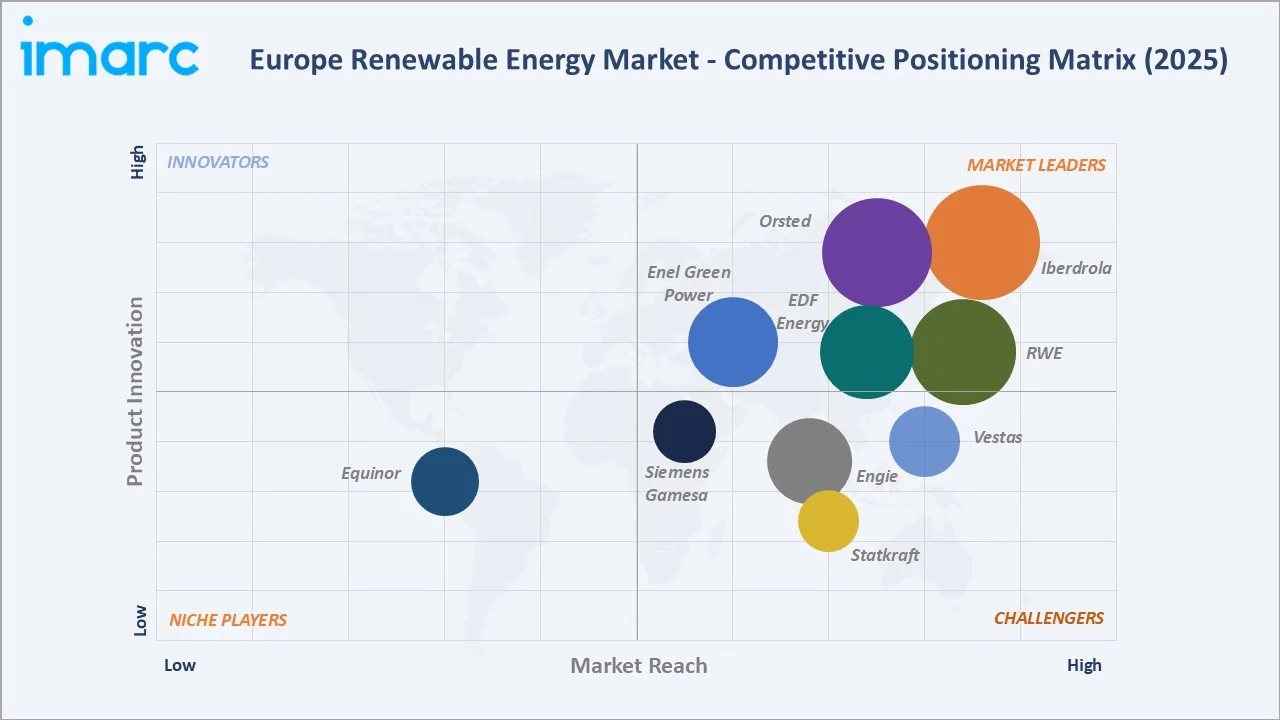

Competitive Landscape

|

Company Name |

Key Platform / Brand |

Market Position |

Core Strength |

|

Iberdrola |

Offshore Wind, Onshore Wind, Photovoltaic solar energy |

Leader |

Europe's largest renewables operator, UK & Iberian strongholds |

|

RWE |

Solar Energy, Offshore Wind, Onshore Wind |

Leader |

Offshore wind leadership, German base, global footprint |

|

Ørsted |

Offshore Wind, Onshore Wind, Solar Energy, Bio Energy |

Leader |

Global offshore-wind pioneer, Danish heritage, North Sea dominance |

|

EDF Energy |

Wind Power, Solar Power |

Leader |

Pan-European portfolio, offshore and solar scale-up |

|

Enel Green Power |

Hydro Energy, Wind Energy |

Leader |

Italy base, utility-scale solar and wind leadership |

|

Engie |

Bio Methane, Wind Enery, Solar Energy |

Challenger |

Diversified renewables plus energy-services platform |

|

Statkraft |

Hydro Power, Wind Power, Solar Power |

Challenger |

Europe's largest hydro producer, Nordic base |

|

Vestas |

Onshore Wind, Offshore Wind, |

Challenger |

Global #1 wind-turbine OEM, Danish base |

|

Siemens Gamesa |

Siemens Gamesa Renewable Energy |

Challenger |

Leading offshore-wind turbine OEM, Spanish-German heritage |

|

Equinor |

Offshore and Onshore Wind |

Emerging |

Floating offshore-wind pioneer, Norwegian base |

The Europe renewable energy market's competitive landscape is moderately concentrated at the utility and offshore-wind tier, with Iberdrola, RWE, Ørsted, EDF, and Enel Green Power collectively operating a significant share of installed capacity. A strong challenger tier (Engie, Statkraft, Vattenfall, Equinor) competes alongside equipment OEMs (Vestas, Siemens Gamesa, Nordex), infrastructure funds (Copenhagen Infrastructure Partners, Macquarie Green Investment Group), and a rapidly growing layer of independent developers and storage specialists. Strategic consolidation around offshore wind, hydrogen, and storage platforms is reshaping the competitive landscape through 2034.

Key Company Profiles

Iberdrola

Iberdrola is Europe's largest renewable-energy operator by installed capacity, headquartered in Bilbao, Spain. Founded in 1992, Iberdrola operates across generation, networks, and retail supply, with more than 42 GW of renewable capacity globally and a deep pan-European footprint led by Spain, the UK, and Portugal.

- Product & Platform Portfolio: Iberdrola's portfolio spans onshore and offshore wind, utility-scale solar, hydro, battery storage, and green hydrogen. Its operating brands include Iberdrola Renovables in Spain, ScottishPower in the UK, and a rapidly expanding European offshore-wind pipeline.

- Recent Developments: In 2025, Iberdrola continued to scale its offshore-wind pipeline in the UK, Germany, and the US, commissioned new Iberian solar and storage assets, and expanded green-hydrogen projects across Puertollano and Bilbao.

- Strategic Focus: Iberdrola's strategy centres on long-term asset ownership, pan-European offshore wind leadership, green-hydrogen integration, and regulated-networks investment to capture the electrification of industry, transport, and heat across Europe.

RWE

RWE is Germany's largest power generator and a global leader in renewable energy, headquartered in Essen. Post-restructuring, RWE has pivoted decisively toward renewable and flexible generation, targeting over 65 GW of renewable capacity by 2030 through its Growing Green strategy.

- Product & Platform Portfolio: RWE's portfolio spans offshore and onshore wind, utility-scale solar, battery storage, and flexible gas/hydrogen-ready generation. It is a cornerstone partner in North Sea and Baltic Sea offshore-wind projects and operates across Germany, the UK, the Netherlands, the US, and Australia.

- Recent Developments: In 2025, RWE continued delivery of major German offshore-wind projects, expanded its UK and Iberian solar-and-storage portfolio, and advanced several green-hydrogen-linked FID decisions under H2Global.

- Strategic Focus: RWE's strategy emphasises scaled offshore-wind delivery, hybrid solar-plus-storage projects, and the development of hydrogen-ready flexible generation to underpin Germany's and Europe's net-zero pathway.

Ørsted

Ørsted is the world's most established offshore-wind pure-play, headquartered in Fredericia, Denmark. The company pioneered commercial offshore wind and remains the largest owner and operator of offshore-wind assets globally, with a European portfolio anchored by the UK, Denmark, Germany, and the Netherlands.

- Product & Platform Portfolio: Ørsted's portfolio includes offshore and onshore wind, utility-scale solar, storage, and green-hydrogen/Power-to-X projects across Europe, North America, and Asia.

- Recent Developments: In 2025, Ørsted refined its project pipeline following 2023-2024 portfolio repricing, progressed UK Hornsea extensions, and advanced the FlagshipONE and H2RES green-fuels projects.

- Strategic Focus: Ørsted's strategy centres on disciplined offshore-wind project delivery, selective Power-to-X investment, and geographic diversification to stabilise cash flows and sustain its offshore-wind leadership through 2034.

Market Concentration Analysis

The Europe renewable energy market exhibits moderate concentration at the utility and offshore-wind tier. The top five renewable operators – Iberdrola, RWE, Ørsted, EDF Renewables, and Enel Green Power – collectively control approximately 25-30% of regional renewable generation capacity in 2025. The remaining share is distributed across a strong challenger tier (Engie, Statkraft, Equinor, Acciona Energía), infrastructure funds, equipment OEMs, and an expanding layer of independent developers and storage integrators.

The market is experiencing a bifurcated dynamic. At the top, scaled utilities and IPPs consolidate around offshore wind, hydrogen, and storage platforms to capture the capital-intensive next wave of deployment. Simultaneously, specialist developers, infrastructure funds, and corporate buyers are redefining origination and financing models, while equipment OEMs undergo a period of strategic restructuring to restore margins and localise supply chains. This dual dynamic is intensifying competition across every renewable sub-segment through 2034.

Investment & Growth Opportunities

Fastest-Growing Segments

Offshore wind is among the fastest-growing renewable energy segments, supported by strong policy frameworks and technological advancements, with double-digit annual growth required through 2030 to meet global net-zero targets. Grid-scale battery storage and green hydrogen are the next most dynamic layers, supported by EU flexibility reforms, the European Hydrogen Bank, and IPCEI funding through 2034.

Emerging Country Expansion

Poland, Greece, Romania, and the Western Balkans represent the highest-potential emerging markets in Europe, supported by EU cohesion funds, coal-to-renewables transitions, and new wind and solar tender regimes. The Nordics remain strategic for onshore and offshore wind, hydropower upgrades, and green-hydrogen exports, while Spain and Italy continue to lead Southern European utility-scale solar and corporate PPA activity.

Venture and Strategic Investment Trends

Strategic capital continues to concentrate in offshore-wind platforms, battery storage, green hydrogen, digital grid tools, and virtual-power-plant operators. Copenhagen Infrastructure Partners, Macquarie Green Investment Group, Brookfield, KKR, and EQT Infrastructure are among the most active pan-European investors, alongside corporate venture arms of Iberdrola, Engie, EDF, and TotalEnergies.

Future Market Outlook (2026-2034)

The Europe renewable energy market forecast projects strong value expansion from USD 258.83 Billion in 2025 to USD 465.13 Billion by 2034 at a CAGR of 6.73%. Germany, the UK, France, Spain, and Italy will retain their combined majority of regional revenue, while the Netherlands, Poland, and the Nordics will outpace the regional average on the back of offshore wind, green hydrogen, and corporate-PPA-led industrial electrification.

Three key shifts will reshape the Europe renewable energy market through 2034. First, offshore wind will transition from project-led delivery to industrialised, cross-border scale-up, becoming the single largest incremental generation source by 2030. Second, green hydrogen and Power-to-X will move from pilot to commercial deployment, anchoring a new demand layer for dedicated renewables and grid expansion. Third, battery storage, grid digitalisation, and flexibility platforms will become structural revenue engines, determining system resilience as variable-renewable penetration approaches 60-70% of generation in leading markets.

Research Methodology

Primary Research

Primary research encompassed structured interviews conducted in 2024-2025 with renewable-energy industry stakeholders, including senior executives at utilities and IPPs, project developers, TSO and DSO representatives, procurement leaders at corporate PPA buyers, and institutional investors in European energy-transition funds. Primary insights validated market sizing, segmentation estimates, and technology-adoption timelines.

Secondary Research

Secondary sources include Eurostat energy statistics, the European Commission's DG ENER and DG CLIMA publications, the International Energy Agency (IEA), IRENA, ENTSO-E's Ten-Year Network Development Plan, WindEurope and SolarPower Europe reports, national TSO data (TenneT, National Grid, RTE, Amprion, Terna, REE), company annual reports, and trade publications including Windpower Monthly, PV Magazine, Recharge, and Montel.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating installed-capacity data, auction and CfD results, wholesale power-price curves, LCOE evolution, and policy-driven capacity-addition targets. Scenario analysis (base, optimistic, and conservative cases) was performed to account for macroeconomic, policy, and supply-chain uncertainty.

Europe Renewable Energy Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Types Covered | Hydro Power, Wind Power, Solar Power, Bioenergy, Others |

| End Users Covered | Industrial, Residential, Commercial |

| Countries Covered | Germany, United Kingdom, France, Italy, Russia, Spain, Netherlands, Switzerland, Poland, Others |

| Companies Covered | Iberdrola, RWE, Ørsted, EDF Energy, Enel Green Power, Engie, Statkraft, Vestas, Siemens Gamesa, Equinor, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Europe Renewable Energy Market Report

The Europe renewable energy market was valued at USD 258.83 Billion in 2025, driven by the EU Green Deal, REPowerEU, record offshore-wind and solar deployment, corporate PPAs, and accelerating industrial and residential electrification.

The market is projected to reach USD 465.13 Billion by 2034, growing at a CAGR of 6.73% during 2026-2034, supported by offshore-wind scale-up, green hydrogen, battery storage, grid reinforcement, and ongoing electrification of heat, transport, and industry.

Wind power leads with a 33.1% share in 2025, driven by installed onshore capacity and rapid offshore-wind scale-up in the North Sea and Baltic. Solar power follows closely at 32.6%, powered by REPowerEU's 600+ GW solar target and record rooftop and utility-scale additions.

Industrial end users account for 47.1% of demand in 2025, driven by corporate PPAs, heavy-industry decarbonisation, and hyperscale data-centre electricity consumption. Residential (30.4%) and commercial (22.5%) users complete the end-use mix.

Germany dominates with a 24.0% share in 2025, followed by the United Kingdom (17.1%), France (15.0%), Spain (11.8%), and Italy (10.5%). Germany's leadership reflects its installed base, Energiewende framework, and the federal EUR 500 billion climate and infrastructure fund.

Key drivers include the EU Green Deal and Fit for 55, the RED III binding renewable target of 42.5%, REPowerEU, falling LCOE of wind and solar, record corporate PPA volumes, electrification of heat and transport, and the European Hydrogen Bank's green-hydrogen roadmap.

Major players include Iberdrola, RWE, Ørsted, EDF, Enel Green Power, Engie, Statkraft, Vestas, Siemens Gamesa, and Equinor.

Offshore wind is the fastest-growing technology, expected to expand at roughly 12-14% CAGR through 2030 as North Sea and Baltic Sea agreements translate into commissioned capacity. Battery storage and green hydrogen are the next most dynamic segments.

Key opportunities include offshore and floating wind, green hydrogen and Power-to-X, utility-scale solar and solar-plus-storage, grid-scale batteries, grid reinforcement and interconnectors, corporate PPA platforms, and digital flexibility and virtual-power-plant operators.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)