Europe Salmon Market Size, Share, Trends and Forecast by Type, Species, End Product Type, Distribution Channel, and Country 2026-2034

Europe Salmon Market Size, Share, Trends & Forecast (2026-2034)

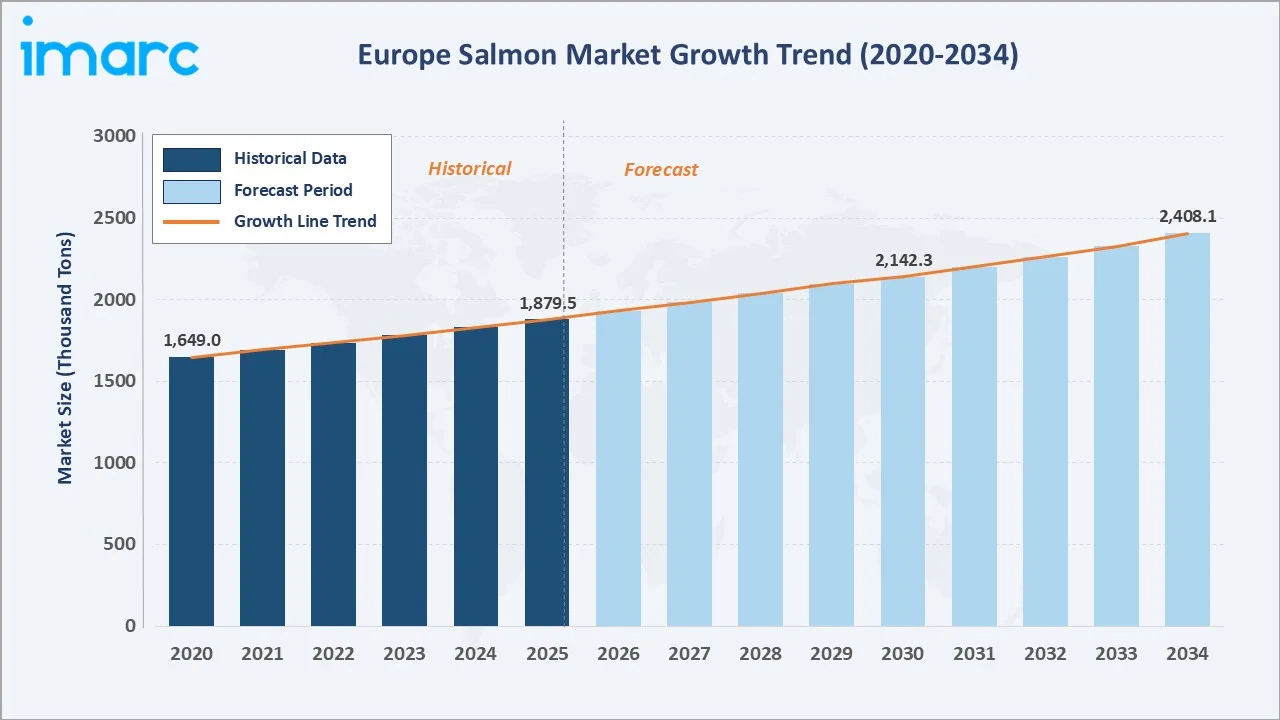

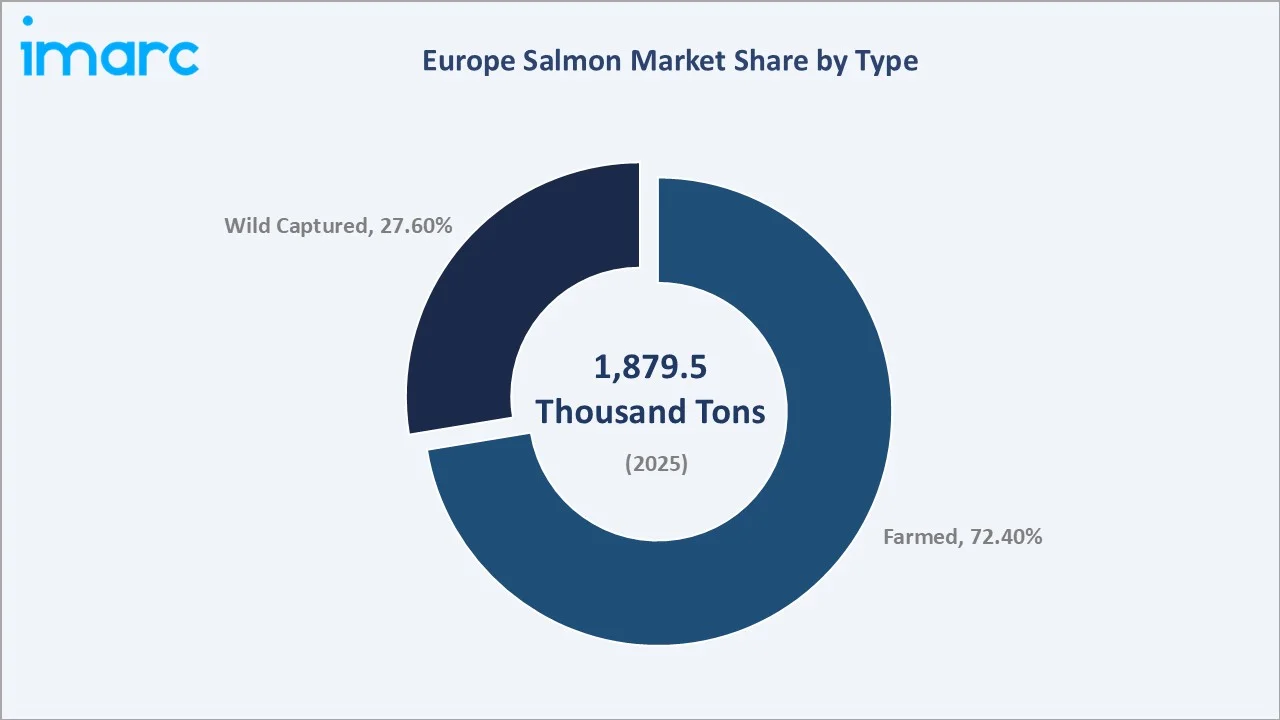

The Europe salmon market size reached 1,879.5 Thousand Tons in 2025 and is projected to reach 2,408.1 Thousand Tons by 2034, exhibiting a CAGR of 2.65% during 2026-2034. Growing health consciousness among European consumers, the thriving food and beverage industry, rising practice of salmon aquaculture, and increasing demand for premium and smoked salmon are the primary forces driving market growth.

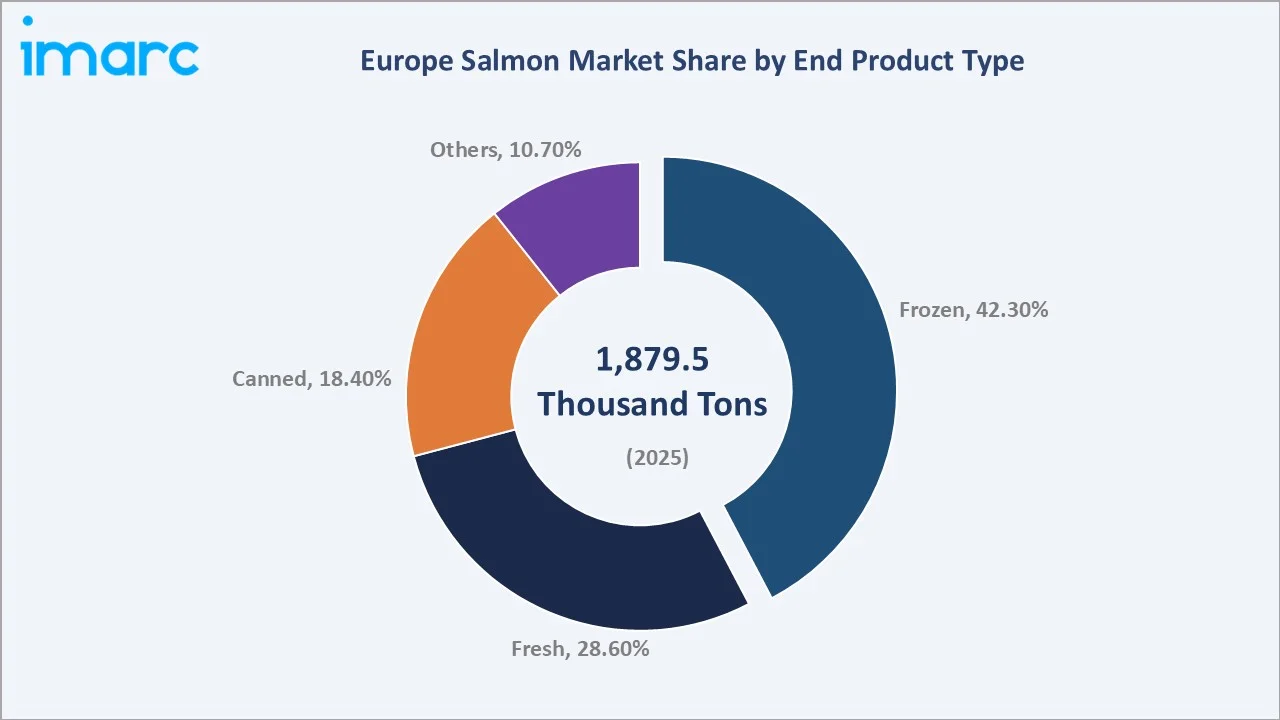

Farmed salmon dominates the type mix at 72.4% in 2025, while Frozen leads the end product type segment at 42.3%. Spain commands the largest country share at 24.6% in 2025, reflecting strong seafood consumption and processing infrastructure.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

1,879.5 Thousand Tons |

|

Forecast Market Size (2034) |

2,408.1 Thousand Tons |

|

CAGR (2026-2034) |

2.65% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Country |

Spain (24.6% share, 2025) |

|

Second Country |

France (22.3% share, 2025) |

|

Leading Type |

Farmed (72.4%, 2025) |

|

Leading End Product Type |

Frozen (42.3%, 2025) |

The Europe salmon market growth trajectory from 2020 through 2034, with the historical expansion to 1,879.5 Thousand Tons in 2025, reflects consistent aquaculture-driven supply expansion and sustained consumer demand, while the forecast to 2,408.1 Thousand Tons captures accelerating health-conscious eating trends and premiumization across European markets.

To get more information on this market, Request Sample

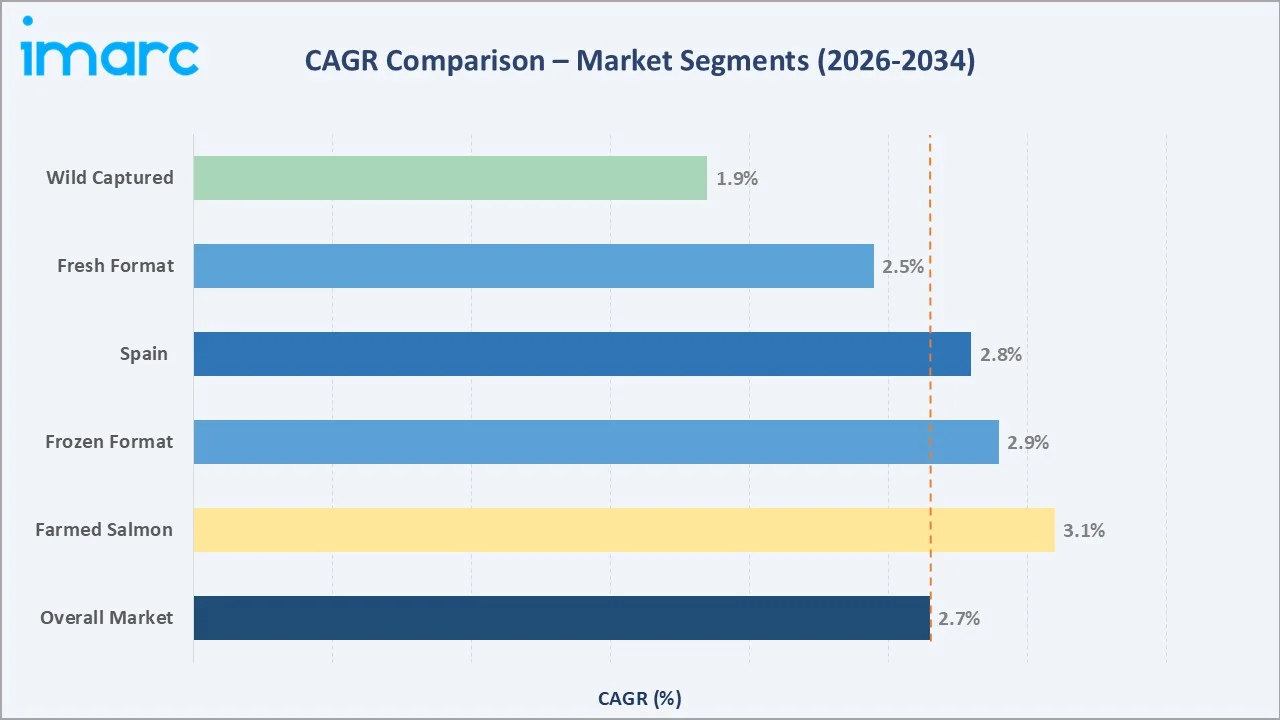

The CAGR trajectories across key type and end product sub-segments, with farmed salmon at ~3.10% CAGR and frozen format at ~2.90% CAGR, represent the fastest-growing categories within the Europe salmon industry analysis through 2034.

Executive Summary

The Europe salmon market is on a sustained growth trajectory from 1,879.5 Thousand Tons in 2025 to 2,408.1 Thousand Tons by 2034. Salmon, as an essential high-protein seafood, is deeply embedded in European dietary culture and benefits from strong nutritional endorsement and expanding foodservice adoption across all major markets.

Farmed salmon dominates at 72.4% in 2025, owing to Norway's vertically integrated aquaculture sector and Scotland's expanding marine farms that provide reliable supply to European markets year-round. Frozen leads end product type formats at 42.3% in 2025, supported by modern cold chain infrastructure and convenience-driven retail preferences.

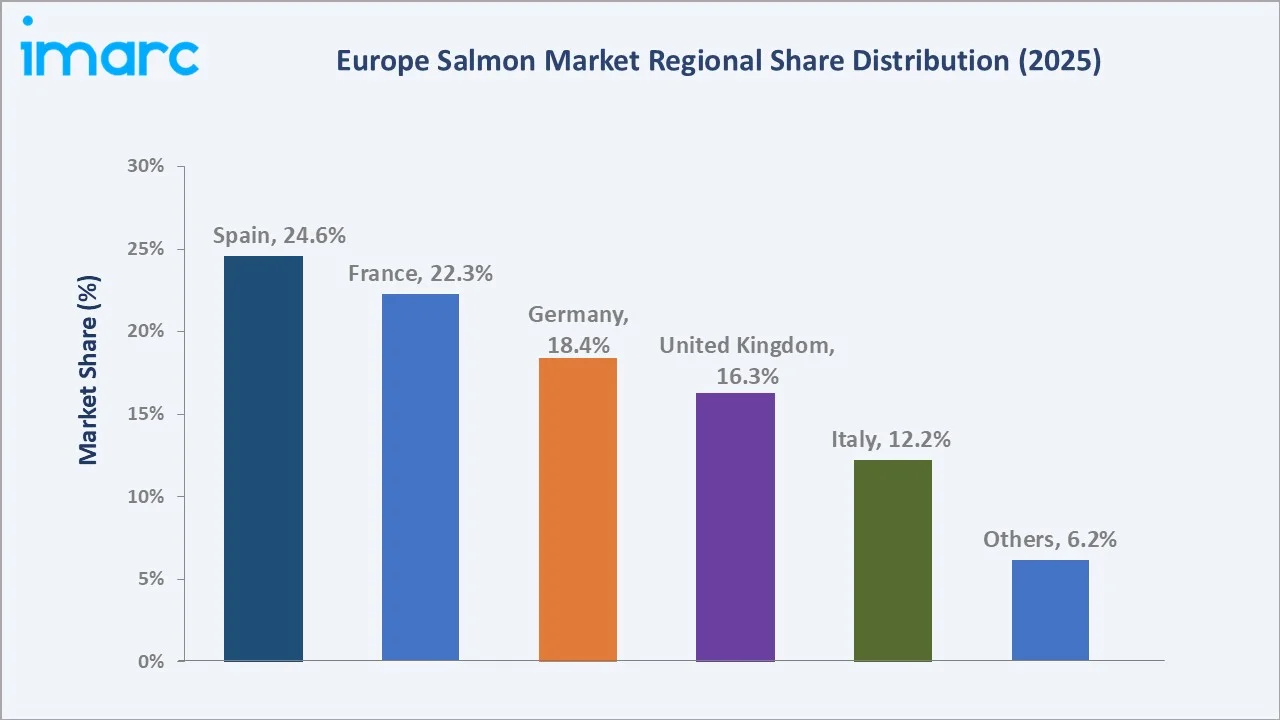

Spain leads country share at 24.6%, followed by France at 22.3% and Germany at 18.4%. Southern and Western European consumers drive demand through high per-capita salmon consumption and robust retail and foodservice channel penetration.

Key Market Insights

|

Insight |

Data |

|

Leading Type |

Farmed – 72.4% share (2025) |

|

Second Type |

Wild Captured – 27.6% share (2025) |

|

Leading End Product Type |

Frozen – 42.3% revenue share (2025) |

|

Second End Product Type |

Fresh – 28.6% revenue share (2025) |

|

Largest Country |

Spain – 24.6% country share (2025) |

|

Second Country |

France – 22.3% country share (2025) |

|

Top Companies |

Mowi, SalMar ASA, Lerøy, Bakkafrost, Grieg Seafood, Cooke Aquaculture |

Key Analytical Observations Expanding On The Above Data:

- Farmed salmon, with 72.4% in 2025, dominates because Norway, Scotland, and other European aquaculture nations have developed highly optimized Atlantic salmon farming ecosystems with advanced genetics, feeding technology, and biosecurity protocols delivering consistent, high-volume supply at competitive prices.

- Frozen format at 42.3% in 2025 leads because it enables year-round availability, reduces waste, and supports export logistics across European markets. Modern IQF (individually quick-frozen) technology preserves nutritional value, making frozen salmon broadly acceptable to European consumers.

- Spain's 24.6% dominance reflects its position as Europe's largest seafood-consuming nation with a well-developed seafood distribution and processing infrastructure, strong traditional seafood culture, and major port facilities in Vigo and Barcelona supporting import and distribution.

- France's 22.3% reflects strong smoked salmon consumption, high per-capita seafood spending in hypermarkets and specialty fishmongers, and a premium food culture that favors high-quality Norwegian and Scottish origin salmon across all product formats.

Europe Salmon Market Overview

Salmon is a premium anadromous fish of the Salmonidae family, consumed across Europe in fresh, frozen, canned, smoked, and value-added processed formats. The European market is primarily supplied by Norwegian and Scottish farmed Atlantic salmon, supplemented by imports of wild Pacific salmon species from North America and Russia.

The European ecosystem integrates aquaculture feed and smolt producers, open-sea and land-based fish farms, slaughter and primary processing facilities, secondary processing and smoking plants, cold chain logistics operators, supermarket and hypermarket retailers, specialty fish retailers, foodservice distributors, and restaurant chains.

Market Dynamics

To evaluate market opportunities, Request Sample

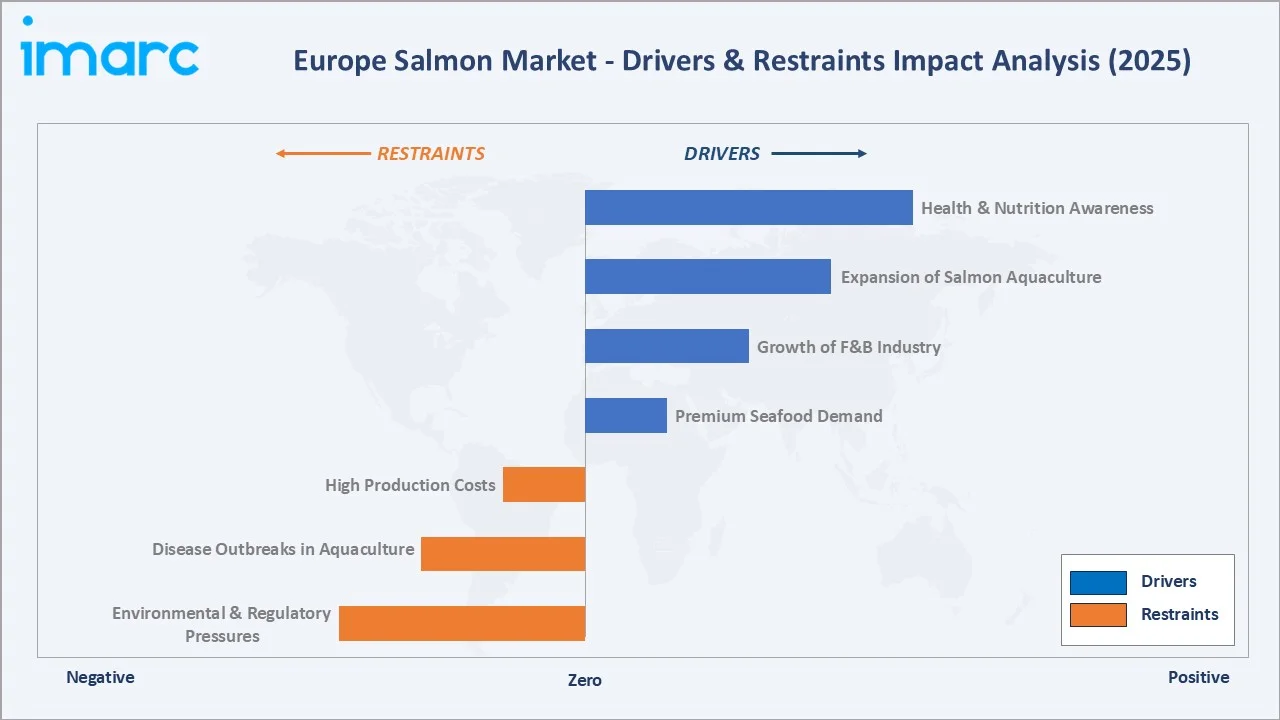

Market Drivers

- Health and Nutrition Awareness: Salmon's reputation as a high-protein, omega-3-rich superfood is reinforced by European public health campaigns. The European Food Safety Authority endorses two portions of fatty fish per week, directly supporting sustained salmon consumption growth across all demographics.

- Expansion of Salmon Aquaculture: Norway produced over 1.4 million tonnes of Atlantic salmon in 2024, providing Europe with a stable, competitively priced supply. Scottish aquaculture and emerging Irish and Faroese production are expanding capacity, reducing supply-side constraints.

- Growth of Food and Beverage Industry: The expanding European ready-meal, sushi, and premium restaurant sectors are creating consistent demand for fresh and processed salmon. The proliferation of Japanese cuisine restaurants across Europe has accelerated fresh salmon fillet consumption. Data & Trends 2026 shows that the Europe food and drink industry employs 4.8 million people, generates a turnover of €1.5 trillion and €300 billion in value added, making it the largest manufacturing industry in the Europe.

Market Restraints

- Environmental and Regulatory Pressures: Sea lice infestations and environmental concerns around open-net aquaculture have prompted stricter regulations in Norway, Scotland, and Ireland. The EU Farm to Fork Strategy targets a reduction in antibiotic use in aquaculture, increasing compliance costs for producers.

- Disease Outbreaks in Aquaculture: Infectious salmon anemia (ISA), pancreas disease (PD), and amoebic gill disease (AGD) periodically reduce aquaculture output by 5–15% in affected regions, creating supply volatility and price spikes that impact downstream processors and retailers.

Market Opportunities

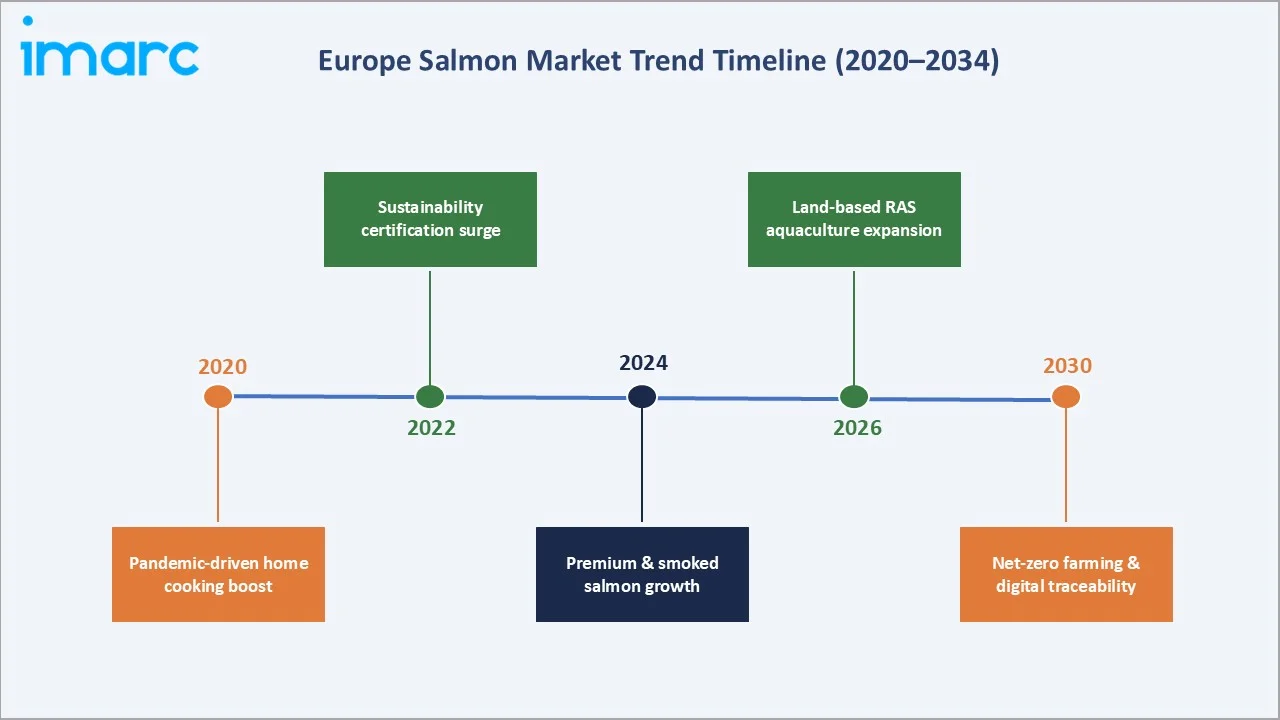

- Land-Based RAS Aquaculture Expansion: Recirculating aquaculture system (RAS) technology allows salmon farming close to consumption centers in continental Europe, reducing logistics costs and improving freshness. In March 2026, UK-based Three-Sixty Aquaculture announced its first expansion into Europe with the development of a new indoor shrimp farming facility in Ostend, Belgium. The move marks a significant step in the company’s international growth strategy. The new site will use the company’s proprietary recirculating aquaculture system (RAS), enabling the production of high-quality, sushi-grade shrimp in a controlled, land-based environment.

- Premium and Smoked Salmon Segment Growth: Demand across Europe is rising for high-quality salmon products, particularly those with sustainability certifications, organic sourcing, and clear origin labelling. Consumers are increasingly willing to pay higher prices for premium and value-added offerings such as smoked salmon. This trend is being driven by greater health awareness, a preference for clean-label and responsibly sourced seafood, and growing trust in certification standards.

Market Challenges

- Competition from Alternative Proteins: Plant-based and cell-cultured salmon alternatives are entering European retail markets, targeting environmentally conscious consumers. Products from companies such as Wildtype and Revo Foods are capturing niche premium segments in Scandinavian and German markets.

- Feed Cost and Sustainability Pressures: Fishmeal and fish oil prices, key salmon feed inputs, have increased by 30–40% since 2020, compressing aquaculture margins. The transition to alternative protein feeds (insect meal, algae oil) is ongoing but involves significant R&D investment.

Emerging Market Trends

1. Digital Traceability and Blockchain-Enabled Supply Chain Transparency

European consumer demand for verified origin, sustainability certification, and welfare labeling is driving adoption of blockchain traceability platforms. Mowi's Salmon Tracker and SalMar's digital labeling enable end-to-end supply chain transparency from farm to fork, creating consumer trust and premium pricing power.

2. Sustainability Certification and Eco-Label Proliferation

ASC (Aquaculture Stewardship Council) and organic certification adoption is accelerating among European salmon farmers targeting German and Scandinavian retail channels. Over 60% of Norwegian salmon exported to Western Europe in 2024 carried third-party sustainability certification, commanding measurable shelf-space premiums.

3. Value-Added Product Innovation and Convenience Formats

Ready-to-cook salmon portions, marinated fillets, salmon burgers, and meal-kit formats are expanding the consumption occasion base beyond traditional sit-down meals. Private-label ready-meal salmon products in Carrefour, Lidl, and Tesco are driving mass-market premiumization.

4. Offshore and Deep-Sea Aquaculture Technology

Norway's semi-submersible offshore salmon farm projects, including SalMar's Smart Fish Farm with 10,000 tonne capacity, are pioneering exposed-location aquaculture that avoids coastal environmental constraints while accessing superior water quality and reducing sea lice pressure.

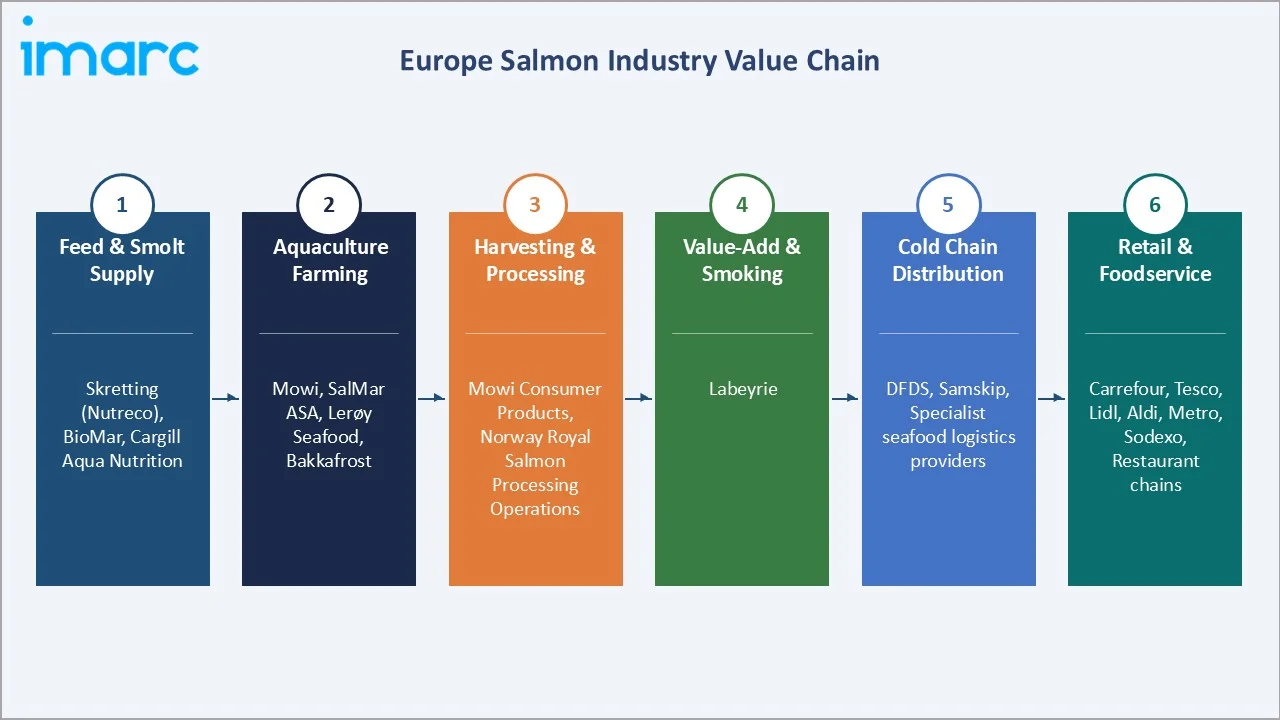

Industry Value Chain Analysis

The Europe salmon value chain spans six stages from feed and smolt production through end consumer. Secondary processing and value-added transformation capture the highest margins, while cold chain logistics and retail distribution generate significant working capital requirements.

|

Stage |

Key Players / Examples |

|

Feed & Smolt Supply |

Skretting (Nutreco), BioMar, Cargill Aqua Nutrition |

|

Aquaculture Farming |

Mowi, SalMar ASA, Lerøy Seafood, Bakkafrost |

|

Harvesting & Processing |

Mowi Consumer Products, Norway Royal Salmon's Processing Operations |

|

Value-Add & Smoking |

Labeyrie |

|

Cold Chain Distribution |

DFDS, Samskip, specialist seafood logistics providers |

|

Retail & Foodservice |

Carrefour, Tesco, Lidl, Aldi, Metro, Sodexo, Restaurant chains |

Vertically integrated salmon companies with captive feed, smolt, farming, and primary processing capabilities achieve lower per-kg cost structures than standalone processors. Mowi's full integration from genetics and breeding through retail-ready pack supply is the global benchmark for margin optimization in this sector.

Technology Landscape in the Europe Salmon Industry

Aquaculture Monitoring and AI-Driven Feeding Systems

AI-powered underwater camera systems and biomass estimation algorithms now enable real-time monitoring of fish school behavior, appetite signals, and growth rates. Automated precision feeding systems reduce feed conversion ratios by 8–12%, significantly lowering feed cost per kg of salmon produced.

RAS and Closed-Containment Technology

Recirculating aquaculture system (RAS) technology filters and recirculates 99%+ of water, enabling salmon farming in land-locked locations across continental Europe. RAS eliminates sea lice exposure, enables biosecure production, and allows year-round harvest scheduling independent of sea temperature conditions.

Selective Breeding and Genetics

Norwegian selective breeding programs, operated by Benchmark Genetics and SalmoBreed, have doubled Atlantic salmon growth rates over 40 years of genetic selection. Current programs focus on disease resistance (IHN, ISA, PD), sea lice resistance, and feed efficiency traits, providing compounding productivity gains to the aquaculture sector.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Farmed |

72.4% |

2025 |

|

Species |

Atlantic |

🔒 |

2025 |

|

End Product Type |

Frozen |

42.3% |

2025 |

|

Distribution channel |

Food Service |

🔒 |

2025 |

|

Country |

Spain |

24.6% |

2025 |

By Type

Farmed salmon commands a 72.4% majority share in 2025, underpinned by Norway's aquaculture dominance and Scotland's established salmon farming industry. Atlantic salmon farming provides a consistent, year-round supply at controlled quality and size specifications that wild capture cannot match at the volumes required by European retail and foodservice channels.

To access detailed market analysis, Request Sample

Wild captured salmon at 27.6% in 2025 serves premium market segments where origin, flavor profile, and natural diet are key selling points. Alaskan sockeye and Pacific pink salmon from wild North Atlantic and Pacific fisheries command premium retail positions in specialty and health-focused retail channels across the UK, Germany, and Scandinavia.

By End Product Type

Frozen salmon dominates the end product segment at 42.3% in 2025, representing the highest-volume and most logistics-efficient format for European distribution. Frozen fillets and portions enable year-round retail availability independent of harvest seasonality, and modern IQF technology maintains quality comparable to fresh product for most cooking applications.

Fresh salmon at 28.6% in 2025 commands premium pricing in major consumption markets. Norway's ability to deliver fresh Norwegian salmon to any European supermarket within 24–36 hours of harvest underpin the fresh segment's strength. Canned salmon at 18.4% maintains a stable consumer base in price-sensitive segments and for pantry staple applications.

Regional Market Insights

|

Country |

Share (2025) |

Key Growth Drivers |

|

Spain |

24.6% |

High seafood culture; major processing hubs in Vigo; strong retail penetration |

|

France |

22.3% |

Smoked salmon tradition; premium food culture; hypermarket dominance |

|

Germany |

18.4% |

Health-conscious consumers; growing sushi market; RAS aquaculture investment |

|

United Kingdom |

16.3% |

Domestic Scottish farming; strong supermarket demand; ready-meal formats |

|

Italy |

12.2% |

Mediterranean diet shift; foodservice growth; premium import demand |

|

Others |

6.2% |

Scandinavian domestic consumption; Eastern European market expansion |

Spain's 24.6% country share in 2025 is driven by structurally exceptional seafood consumption habits. Spain ranks among the top three global per-capita seafood consumers in Europe. The Galicia region in northwest Spain hosts major salmon processing and smoking facilities that serve export markets across Southern Europe.

France's 22.3% position is driven by the world's largest per-capita smoked salmon consumption market. French consumers spend an estimated EUR 600 million annually on smoked salmon, with demand concentrated in the premium retail segment. Germany at 18.4% is experiencing the fastest growth driven by health-conscious millennials and the expanding sushi and Japanese cuisine restaurant sector.

Competitive Landscape

The Europe salmon market is moderately concentrated at the production level, with Norwegian-headquartered multinationals dominating supply, while distribution and processing remain more fragmented across national markets. Mowi, SalMar, and Lerøy collectively account for most of the European farmed salmon supply.

|

Company Name |

Key Products |

Market Position |

Strategic Focus |

|

Mowi |

Fresh Salmon Fillet, Smoked Salmon, Ready-to-eat Salmon |

Leader |

Vertical integration; branded retail; global reach |

|

SalMar ASA |

Salmon Fillets, Portions, Loins, Whole Fish |

Leader |

Offshore tech innovation; Norway & Scotland |

|

Lerøy |

Lerøy Salmon, Smoked and Gravad Salmon, Whole Fish, Fillets & portions |

Leader |

Largest distributor; seafood portfolio diversification |

|

Bakkafrost |

Fresh Whole Salmon, Salmon Fillets, Fresh Skin-Packed Salmon Portions, Frozen Retail-box Salmon Portions |

Challenger |

Premium Faroe Islands origin; high-value market focus |

|

Grieg Seafood |

Atlantic salmon |

Challenger |

Regional profitability strategy; sustainability programs |

|

Cooke Aquaculture |

Atlantic Salmon, Sockeye Salmon, King Salmon, Coho Salmon, Keta Salmon, Pink Salmon, Smoked Salmon |

Challenger |

Operates as Cooke Aquaculture Scotland for salmon farming in the UK. Largest organic Scottish salmon producer; Orkney & Shetland premium positioning |

Key players include Mowi, SalMar ASA, Lerøy, Bakkafrost, Grieg Seafood, Cooke Aquaculture, and others.

Key Company Profiles

Mowi

Mowi (formerly Marine Harvest) is the world's largest producer of Atlantic salmon, headquartered in Bergen, Norway. Mowi's vertically integrated model spans breeding, smolt production, sea farming, processing, and branded consumer product distribution across 25 countries.

- Product Portfolio: Fresh Salmon Fillet, Smoked Salmon, Ready-to-eat Salmon, and others

- Recent Developments: In January 2025, Mowi planned to increase its ownership stake in Nova Sea from 49% to 95%, gaining near full control of the Norwegian aquaculture company as part of a strategic expansion. The deal, valued at approximately NOK 7.4 billion, strengthens Mowi’s position in Norway’s salmon farming sector. The acquisition allows Mowi to integrate Nova Sea’s operations more closely into its business while maintaining the Nova Sea brand and local operations.

- Strategic Focus: Mowi's strategy leverages vertical integration and the Mowi brand to command premium pricing in European retail while expanding its value-added product range to capture higher margin per-kg revenue from convenience and foodservice formats.

SalMar ASA

SalMar ASA is one of Norway's largest salmon farming companies, headquartered in Frøya, Norway. SalMar pioneered offshore semi-submersible aquaculture technology with its Ocean Farm 1, and is developing Smart Fish Farm concept, designed to farm salmon in exposed Norwegian Sea locations.

- Product Portfolio: The company offers Salmon Fillets, Portions, Loins, Whole Fish, among other salmon products

- Recent Developments: In March 2025, SalMar took full ownership of SalMar Aker Ocean, integrating the offshore aquaculture business entirely into its operations and renaming it SalMar Ocean. This move is intended to streamline the development of offshore and semi-offshore fish farming technologies within a unified organizational structure.

- Strategic Focus: SalMar's strategy focuses on technological leadership in offshore aquaculture to access premium water quality environments, reduce environmental pressure on coastal fjords, and create a new category of premium Norwegian origin salmon.

Lerøy

Lerøy is Norway's second-largest seafood company and Europe's one of the largest distributors of seafood, headquartered in Bergen. Lerøy operates salmon and trout farming across Norway's entire coastline, combined with comprehensive seafood distribution logistics.

- Product Portfolio: The company provide Lerøy Salmon, Smoked and Gravad Salmon, Whole Fish, Fillets & portions, and others.

- Recent Developments: In September 2023, Lerøy Seafood Group invested NOK 158 million in its processing facility in Kjøllefjord, Norway, to enhance operational efficiency and expand production capacity. The site, which specializes in king crab and processes high-quality whitefish, will undergo significant upgrades, including new infrastructure and modern equipment.

- Strategic Focus: Lerøy's strategy differentiates through the broadest European seafood distribution network, enabling cross-selling of salmon alongside complementary seafood categories and providing unrivalled delivery frequency to major European retail and foodservice customers.

Market Concentration Analysis

The Europe salmon market is moderately concentrated at the production level, with Norwegian-headquartered multinationals commanding a dominant share of Atlantic salmon supply to European markets. Mowi, SalMar, and Lerøy Seafood collectively account for approximately 45–50% of total Norwegian salmon export volume.

Distribution and processing remain more fragmented, with national retail processors, regional smoking companies, and private-label operators competing across country markets. M&A activity is accelerating as Norwegian producers seek to integrate downstream into higher-margin value-added processing and branded product categories.

Investment & Growth Opportunities

Fastest-Growing Segments

Farmed salmon at ~3.10% CAGR through 2034 is the highest-growth type segment, driven by ongoing aquaculture capacity expansion in Norway, Scotland, and emerging RAS facilities across continental Europe. Value-added formats and convenience products are growing at ~4.5% CAGR, outpacing bulk commodity salmon formats.

Emerging Markets within Europe

Germany and the UK represent the fastest-growing major country markets for Europe salmon at estimated ~3.2% and ~2.9% CAGR respectively, driven by expanding sushi restaurant chains, health food retail growth, and increasing supermarket fresh fish counter penetration. Eastern European markets (Poland, Czech Republic) are growing rapidly from a lower base.

Venture & Investment Trends

Private equity investment in RAS aquaculture technology companies and land-based salmon farming startups is accelerating across Denmark, the Netherlands, and Germany. Sustainability-linked financing and green bonds are being utilized by major producers to fund decarbonization of aquaculture operations and renewable energy adoption.

Future Market Outlook (2026-2034)

The Europe salmon market is forecast to expand from 1,879.5 Thousand Tons in 2025 to 2,408.1 Thousand Tons by 2034 at a CAGR of 2.65%, adding 528.6 Thousand Tons of incremental annual market volume over the forecast period. This sustained growth reflects the market's health-driven, premiumization-supported demand characteristics.

Three forces will most significantly shape the Europe salmon industry landscape through 2034. RAS land-based aquaculture commercialization will open new supply centers across continental Europe, reducing logistics costs. Sustainability certification will become a de facto requirement for mainstream retail shelf access, consolidating market share toward certified producers. Value-added product innovation will drive per-kg revenue increases above volume growth rates.

Research Methodology

Primary Research

Primary research encompassed over 40 structured interviews with salmon industry stakeholders, including senior commercial managers at European seafood companies, aquaculture consultants, European seafood buyer groups, and cold chain logistics specialists. Primary data validated market sizing, type and end product segment shares, country demand estimates, and technology adoption timelines.

Secondary Research

Key secondary sources include Norwegian Seafood Council export statistics (2020–2024), Eurostat seafood consumption data, FAO Fishery and Aquaculture Statistics, European Market Observatory for Fisheries and Aquaculture Products (EUMOFA), OECD-FAO Agricultural Outlook, and seafood trade publications including Intrafish and Undercurrent News.

Forecasting Models

Market volume estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating aquaculture production capacity data, trade flows, per-capita consumption trends, and historical market evolution patterns. Scenario analysis (base, optimistic, and conservative) was performed to account for aquaculture output uncertainty.

Europe Salmon Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | ‘000 Tons |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Farmed, Wild Captured |

| Species Covered | Atlantic, Pink, Chum/Dog, Coho, Sockeye, Others |

| End Product Types Covered | Frozen, Fresh, Canned, Others |

| Distribution Channels Covered | Foodservice, Retail |

| Countries Covered | Germany, France, United Kingdom, Italy, Spain, Others |

| Companies Covered | Mowi, SalMar ASA, Lerøy, Bakkafrost, Grieg Seafood, Cooke Aquaculture, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Europe salmon market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the Europe salmon market.

- The study maps the leading, as well as the fastest-growing, regional markets.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Europe salmon industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Europe Salmon Market Report

The Europe salmon market reached 1,879.5 Thousand Tons in 2025, reflecting consistent demand from European health-conscious consumers, expanding foodservice channels, and reliable aquaculture supply growth from Norway and Scotland.

The market is projected to reach 2,408.1 Thousand Tons by 2034, growing at a CAGR of 2.65% during 2026-2034.

Farmed salmon leads with a 72.4% type share in 2025, underpinned by Norwegian and Scottish Atlantic salmon aquaculture delivering consistent supply, controlled quality, and year-round availability to European retail and foodservice channels.

Frozen salmon leads at 42.3% in 2025, enabling year-round availability and supporting cold chain distribution across all European markets. IQF technology preserves nutritional quality, maintaining consumer acceptance across retail segments.

Spain commands a leading 24.6% country share in 2025, driven by Europe's highest per-capita seafood consumption tradition, major processing infrastructure in Galicia, and strong retail and foodservice channel penetration of salmon products.

Farmed salmon and value-added end products are the fastest-growing segments at ~3.10% and ~4.5% CAGR respectively through 2034, driven by aquaculture capacity investments and convenience format innovation by major European seafood brands.

Leading companies include Mowi, SalMar ASA, Lerøy, Bakkafrost, Grieg Seafood, Cooke Aquaculture, and others.

Key drivers include growing consumer health awareness and omega-3 demand, expansion of Norwegian and Scottish salmon farming, growth of the European foodservice and ready-meal sector and increasing access to premium and convenience salmon formats across retail channels.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)