Europe Seaweed Market Size, Share, Trends and Forecast by Environment, Product, Application, and Country, 2026-2034

Europe Seaweed Market Size, Share, Trends & Forecast (2026-2034)

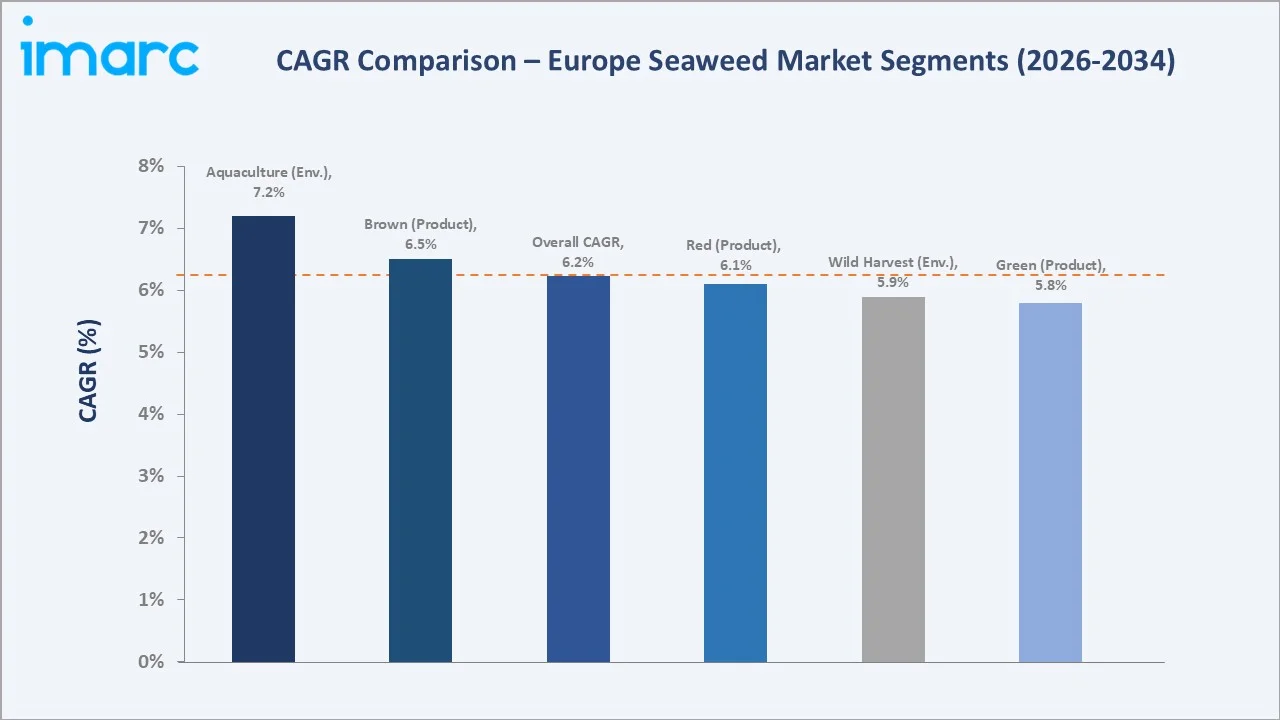

The Europe seaweed market was valued at USD 671.98 Million in 2025 and is forecast to reach USD 1,177.93 Million by 2034, expanding at a CAGR of 6.24% during 2026-2034. Growth is primarily driven by rising demand for plant-based ingredients, expanding aquaculture output, and supportive EU regulatory frameworks under the Blue Economy strategy.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 671.98 Million |

|

Forecast Market Size (2034) |

USD 1,177.93 Million |

| Historical Period | 2020-2025 |

|

CAGR (2026-2034) |

6.24% (2026-2034) |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Largest Country |

France (22.4%, 2025) |

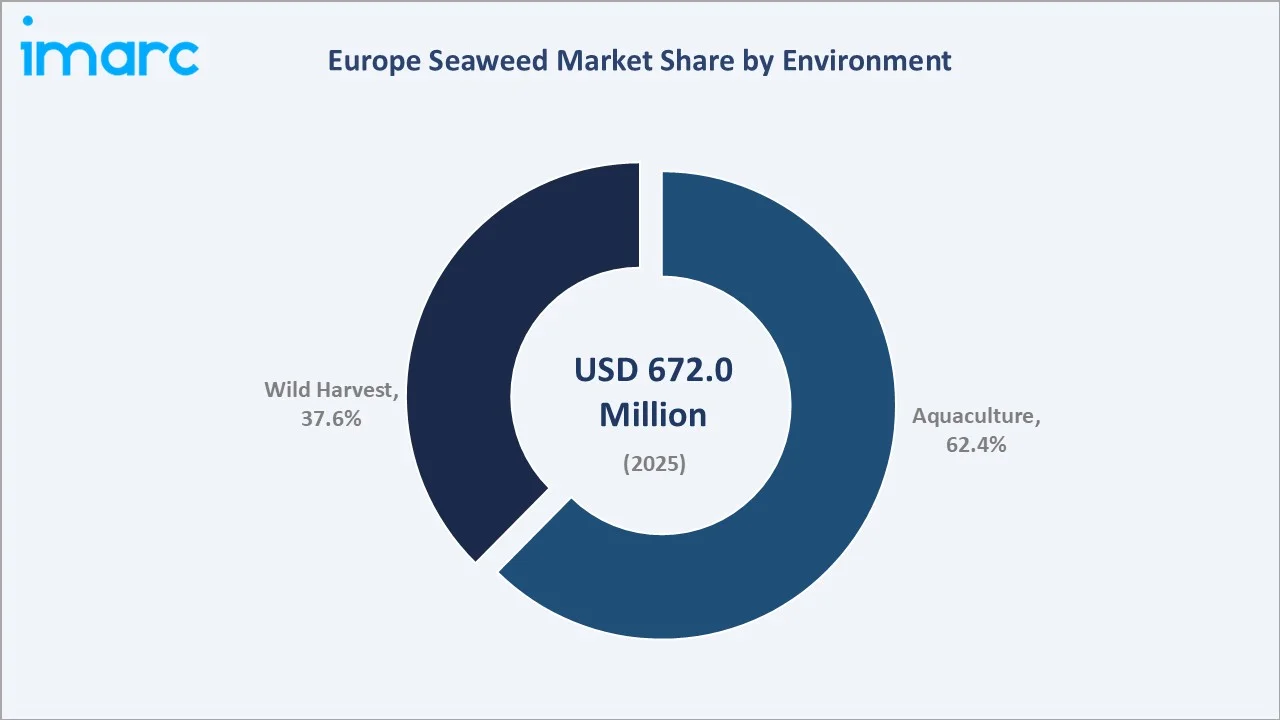

| Leading Environment | Aquaculture (62.4%, 2025) |

|

Leading Product |

Brown (42.3%, 2025) |

To get more information on this market, Request Sample

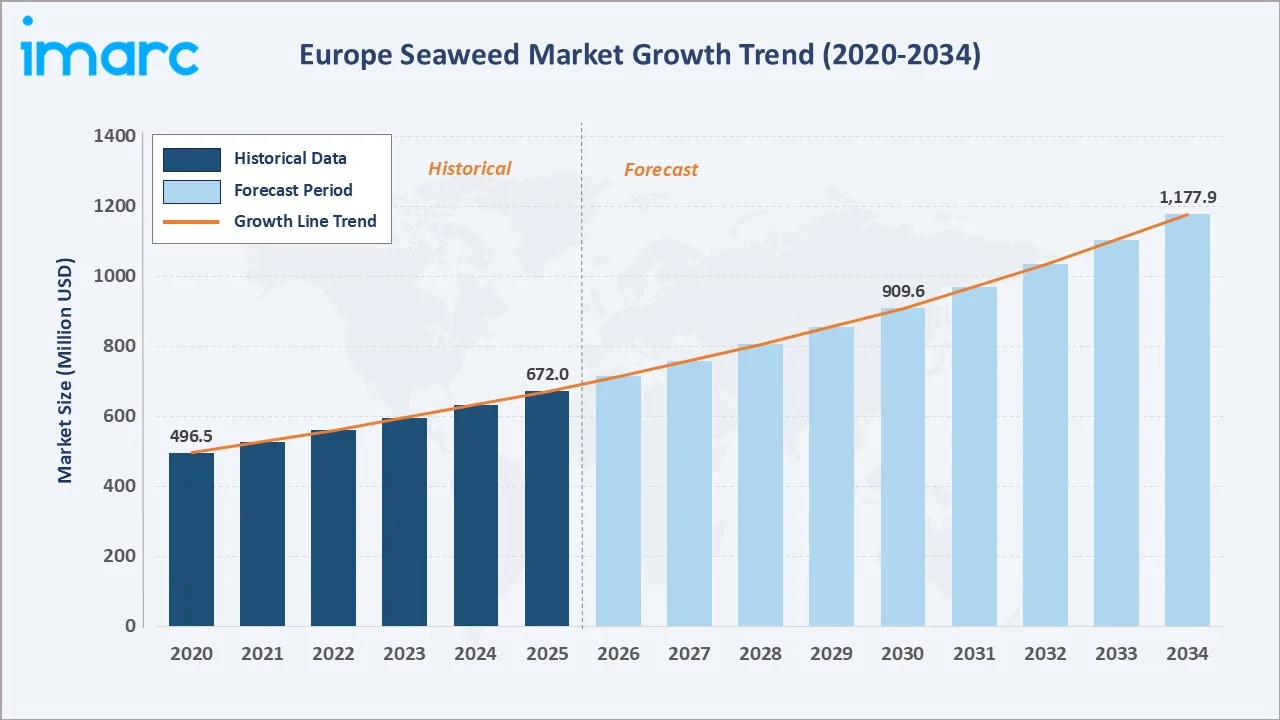

The Europe seaweed market growth trajectory from 2020 through 2034, contrasting historical expansion against a sustained forecast curve powered by rising demand for plant-based nutrition, expanding applications in food, agriculture, and cosmetics, and increasing investments in sustainable aquaculture across regional markets.

The chart above illustrates steady revenue expansion from USD 496.45 Million in 2020 to a projected USD 1,177.93 Million by 2034, underscoring sustained demand across food, agriculture, and pharmaceutical end-use sectors.

Executive Summary

The Europe seaweed market has grown from USD 496.45 Million in 2020 to USD 671.98 Million in 2025, driven by expanding consumer interest in plant-based nutrition and seaweed-derived hydrocolloids such as carrageenan and agar. The forecast period anticipates the market reaching USD 909.57 Million by 2030 and USD 1,177.93 Million by 2034, reflecting a CAGR of 6.24%. Europe's well-established coastal harvesting infrastructure, especially in France, and the United Kingdom, provides a strong supply-side foundation for accelerated expansion.

Among the key growth catalysts are the European Union's Blue Economy Action Plan and increasing R&D investment in seaweed-based bioplastics and bio-fertilizers. The food and beverage industry accounts for a significant share of demand, with processed food applications and direct human consumption segments recording steady uptake. Furthermore, the animal feed additives segment is gaining momentum, as seaweed-based methane-inhibiting supplements attract attention from the livestock sector.

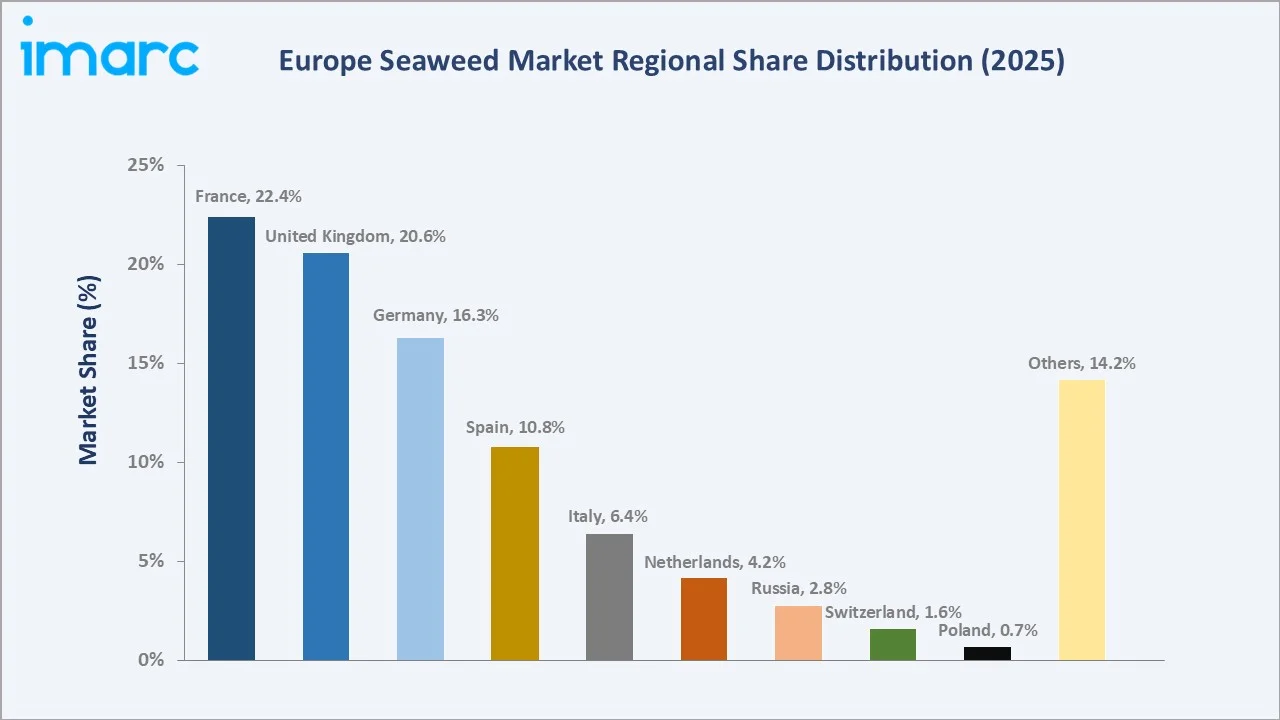

France leads the regional market with a 22.4% share in 2025, driven by advanced seaweed cultivation infrastructure and well-developed B2B supply chains. The United Kingdom 20.6% and Germany 16.3% follow, with Germany increasingly investing in seaweed-based pharmaceutical applications.

Key Market Insights

|

Insight Category |

Key Data Point |

|

Market Size (2025) |

USD 671.98 Million |

| Forecast Market Size (2034) | USD 1,177.93 Million |

|

Overall CAGR (2026-2034) |

6.24% |

|

Largest Environment |

Aquaculture (62.4% in 2025) |

|

Fastest Growing Environment |

Aquaculture (Est. CAGR ~7.2%) |

| Largest Product | Brown Seaweed (42.3% in 2025) |

| Leading Country | France (22.4% share in 2025) |

| Second Largest Country | United Kingdom (20.6% in 2025) |

| Key Application | Food & Beverages, Hydrocolloids |

| Top Companies | Cargill, Incorporated., Tate & Lyle, Gelymar, IFF, Ingredion, and BioAtlantis Ltd. |

Key Insight Highlights:

- Aquaculture dominates the environment segment at 62.4% in 2025, driven by consistent output from France-based seaweed farms and growing EU investment in controlled marine cultivation.

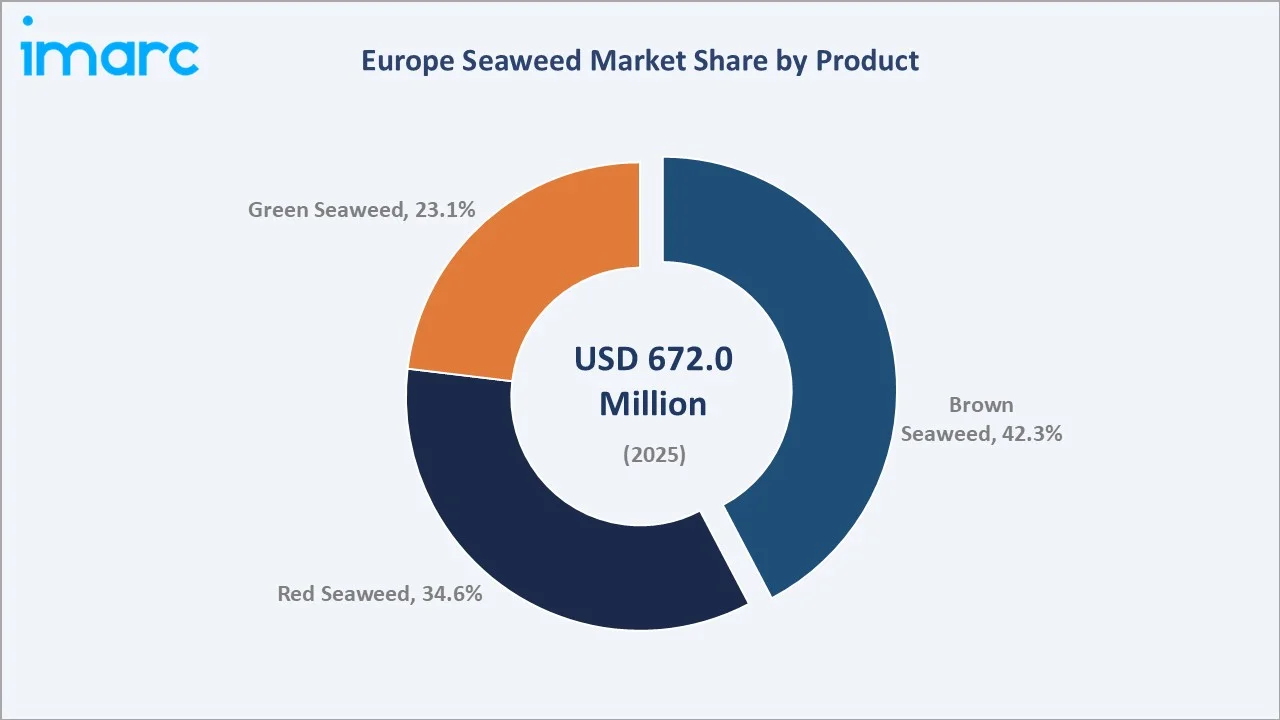

- Brown seaweed leads the product mix at 42.3%, primarily attributed to its rich alginate content that drives demand from the food processing and pharmaceutical sectors across Western Europe.

- Red seaweed commands 34.6% of product-type revenue in 2025, underpinned by strong demand for carrageenan - a key hydrocolloid used in dairy, meat processing, and personal care formulations.

- France's 22.4% country share reflects decades of Breton seaweed cultivation expertise, robust processing infrastructure, and strong government support under national blue economy programs.

- The United Kingdom and Germany together account for approximately 36.9% of the regional market, positioning Western Europe as the core demand hub for seaweed-based ingredients.

- Emerging applications in seaweed-based bioplastics and agricultural bio-stimulants represent incremental growth vectors, with the EU's Farm to Fork Strategy accelerating adoption across member states.

Europe Seaweed Market Overview

Seaweed, a macroalgae, encompasses numerous species broadly classified as brown (Phaeophyta), red (Rhodophyta), and green (Chlorophyta). In Europe, the industry spans wild harvesting from Atlantic and North Sea coastlines as well as structured aquaculture operations in France, Ireland, and Scotland. Applications extend across food processing, hydrocolloid manufacturing, pharmaceutical intermediates, agricultural bio-stimulants, animal feed, and emerging bio-based materials.

Macroeconomic drivers include the EU's Blue Economy Action Plan - generated EUR 890 billion in 2022, and increasing policy alignment between seaweed cultivation and climate-neutral agricultural targets. The European market benefits from a mature regulatory framework, strong R&D ecosystems, and established supply chains connecting coastal producers with industrial end users across key consumption markets.

The ecosystem map above captures the integrated flow from raw biomass sourcing through multi-stage processing, advanced product manufacturing, and channel-specific distribution to diverse European end-use markets.

Market Dynamics

To evaluate market opportunities, Request Sample

Market Drivers

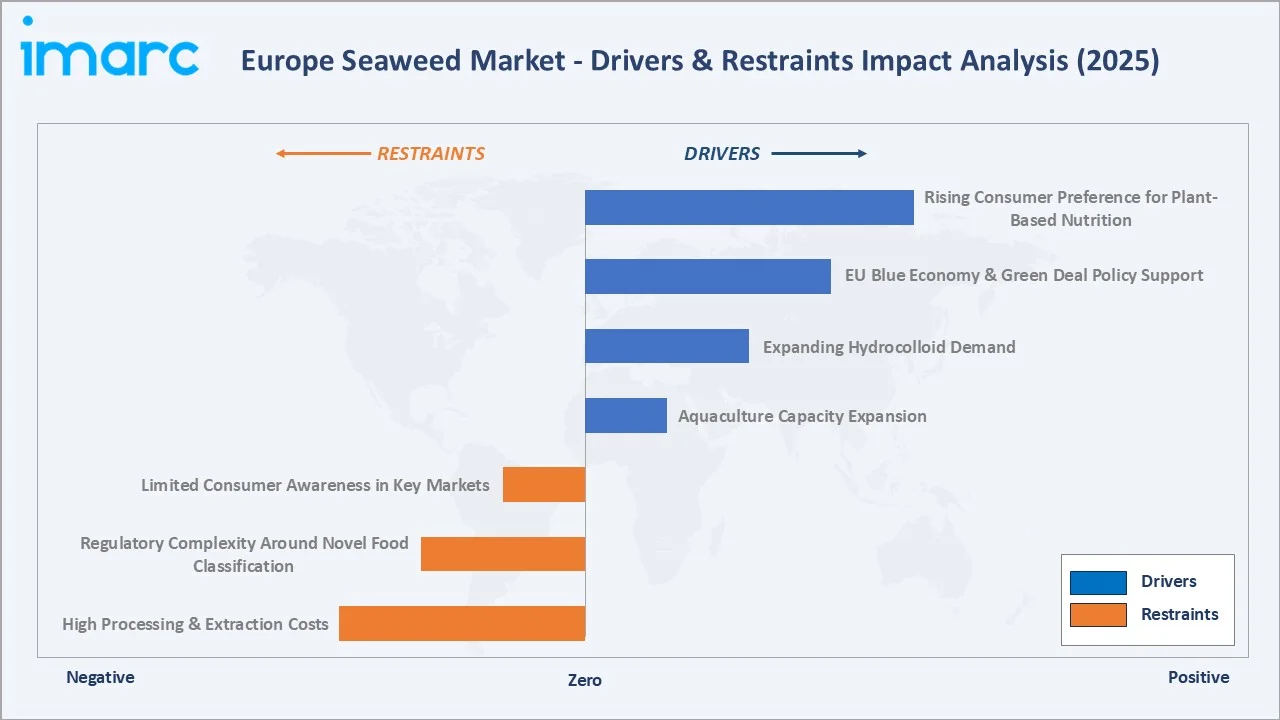

The Europe seaweed market is propelled by converging demand-side and supply-side forces.

- Rising Consumer Preference for Plant-Based Nutrition: Health remains the top reason for increasing plant-based consumption, with 47% of European consumers, significantly expanding the addressable market for seaweed-based functional food ingredients.

- EU Blue Economy & Green Deal Policy Support: The European Commission's Blue Economy report highlights seaweed as a priority marine crop, with significant funding allocated to marine bioeconomy research and development programs through Horizon Europe.

- Expanding Hydrocolloid Demand: Carrageenan and agar demand from the European food processing sector is a key driver of red and brown seaweed procurement volumes.

- Aquaculture Capacity Expansion: Norway, which produces approximately 120,000-180,000 tonnes of the kelp tangle (Laminaria hyperborea) and 20,000 tonnes of rockweed (Ascophylum nodosum) annually, is expanding cultivation acreage, ensuring consistent supply for downstream processors.

Market Restraints

- High Processing & Extraction Costs: Advanced hydrocolloid extraction processes require capital-intensive equipment. Processing costs account for a significant share of total production expenses, limiting margin expansion for smaller seaweed processors.

- Regulatory Complexity Around Novel Food Classification: The EU Novel Food Regulation (EU) 2015/2283 imposes stringent authorization timelines for certain seaweed species used in food applications, creating market entry barriers.

- Limited Consumer Awareness in Key Markets: While awareness is rising, seaweed remains a niche ingredient in Central and Eastern European markets. Germany, Poland, and Switzerland collectively show relatively low retail penetration.

Market Opportunities

- Seaweed-Based Bioplastics & Packaging: The European bioplastics market is expected to witness strong growth in the coming years. Seaweed-derived polysaccharides are emerging as a commercially viable raw material for compostable packaging.

- Agricultural Bio-stimulants: Europe's bio-stimulants market has expanded significantly in recent years. Seaweed extracts, recognized under the EU Fertilizing Products Regulation 2019/1009, represent a high-growth application area.

- Pharmaceutical & Nutraceutical Ingredients: European pharmaceutical demand for fucoidan, laminarin, and carrageenan-derived ingredients is expanding. The nutraceuticals segment represents a notable incremental growth opportunity in the coming years.

Market Challenges

- Climate Change & Coastal Ecosystem Disruption: Rising sea temperatures and ocean acidification threaten wild harvest yields, particularly along Atlantic coastlines of France and Ireland.

- Supply Chain Fragmentation: The industry lacks standardized quality frameworks, creating consistency challenges for industrial buyers in food and pharmaceutical sectors.

- Competition from Asian Low-Cost Imports: Asian seaweed producers (China, South Korea, Indonesia) supply lower-cost alternatives, creating pricing pressure on European domestically produced seaweed.

Emerging Market Trends

The trend timeline above identifies pivotal development milestones shaping the Europe seaweed market from the post-pandemic aquaculture expansion phase through to projected market maturation by 2034.

1. Seaweed-Based Functional Food Mainstreaming

European consumers are increasingly incorporating seaweed-enriched snacks, condiments, and dairy alternatives into regular diets. Seaweed-infused product launches across Europe grew steadily, with the United Kingdom and Germany leading product innovation activity.

2. Precision Aquaculture & Offshore Farming

Advanced offshore seaweed cultivation platforms integrating IoT sensors and automated harvesting equipment are being piloted across Norwegian fjords and Scottish coastlines. These systems reduce operational costs compared to traditional near-shore methods.

3. Circular Bio-Economy Applications

Seaweed is increasingly integrated into circular bio-economy frameworks. The EU aims to generate a significant portion of coastal economies through marine bio-resources, with seaweed-based animal feed, bio-fertilizers, and bioplastics positioned as critical contributors.

4. Clean-Label & Organic Certification Growth

Demand for organically certified seaweed products is rising sharply. European organic seaweed revenues are projected to grow steadily, driven by health-conscious consumers and premium food and cosmetics brands seeking clean-label bio-ingredients.

5. R&D Investment in Seaweed-Derived Pharmaceuticals

EU-funded research programs are investigating fucoidan and laminarin for anti-inflammatory, anti-viral, and anti-cancer properties. Demand for pharmaceutical-grade seaweed extracts is expected to grow steadily at a premium rate.

Industry Value Chain Analysis

The Europe seaweed industry value chain spans six interconnected stages, from biomass sourcing through final end-use consumption. Each stage adds incremental value and presents specific investment opportunities.

| Value Chain Stage | Key Activities | Representative Players |

| Wild Harvest & Aquaculture | Ocean harvesting, seaweed farming, biomass collection | Coastal cooperatives (France, Ireland) |

| Processing & Extraction | Drying, milling, hydrocolloid extraction, fermentation | Gelymar, Algaia |

| Product Manufacturing | Food ingredients, nutraceuticals, bio-fertilizers, pharma intermediates | Cargill, Incorporated., Tate & Lyle |

| Technology Integration | IoT aquaculture monitoring, precision extraction, biorefinery platforms | Biotechnology firms, EU-funded R&D labs |

| Distribution Channels | B2B industrial supply, food service, specialty retail, e-commerce | Distributors, food ingredient wholesalers |

|

End Users |

Food & Beverages, Agriculture, Pharmaceuticals, Cosmetics, Animal Feed | Multinational FMCGs, specialty brands |

The linear value chain captures the flow from ocean-sourced biomass through successive transformation stages to end-consumer delivery, reflecting high levels of integration between European aquaculture operators and multinational ingredient manufacturers.

Technology Landscape in the European Seaweed Industry

Advanced Aquaculture Technologies

Offshore seaweed cultivation in Europe is increasingly adopting modular longline systems equipped with real-time growth monitoring sensors. Automated underwater drones for biomass assessment are being deployed across Norwegian and Scottish farms, reducing labor costs per harvest cycle.

Extraction & Biorefinery Innovation

Next-generation hydrocolloid extraction platforms utilizing enzymatic and ultrasonic processing achieve higher purity yields with lower energy consumption versus conventional alkali-based extraction. European biorefineries are investing in multi-stream processing facilities that simultaneously extract food-grade carrageenan, agricultural bio-stimulants, and pharmaceutical intermediates from a single seaweed batch.

Digital Traceability & Blockchain Integration

Consumer demand for sustainable and traceable ingredients is driving blockchain-based supply chain platforms across European seaweed supply chains. Verified traceability from harvest origin to product formulation is becoming a competitive requirement for premium food and cosmetics brands.

Bio-Based Materials Technology

Research into seaweed-derived bioplastics has accelerated considerably, with the EU backing multiple pilot projects under Horizon Europe's bio-economy programs. Seaweed-based films and coatings for food packaging are expected to achieve commercial viability in the coming years, representing an incremental market opportunity within the European bio-packaging sector.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Environment |

Aquaculture |

62.4% |

2025 |

|

Product |

Brown |

42.3% |

2025 |

|

Application |

🔒 |

🔒 |

2025 |

|

Country |

France |

22.4% |

2025 |

By Environment

To access detailed market analysis, Request Sample

The environment-based segmentation reveals that aquaculture-sourced seaweed accounts for 62.4% of total market value in 2025, while wild harvest contributes the remaining 37.6%. Aquaculture is growing faster, driven by controlled yield consistency and regulatory preferences for farmed over wild-harvested marine resources.

By Product

Brown seaweed holds the leading product share at 42.3% in 2025, driven by high alginate demand from the food, pharmaceutical, and cosmetics sectors. Red seaweed accounts for 34.6%, primarily serving the carrageenan market. Green seaweed captures 23.1%, with growing utilization in nutraceuticals and emerging bio-economy applications.

Regional Market Insights

France leads with 22.4%, followed by the United Kingdom at 20.6% and Germany at 16.3%. Spain, Italy, Netherlands, Russia, Switzerland, Poland and others collectively account for the remaining market.

|

Country |

Market Share (2025) |

Key Growth Drivers |

Major Applications |

| France |

22.4% |

Breton coastal harvesting tradition, government blue economy initiatives, established processing infrastructure | Food ingredients, hydrocolloids, cosmetics |

| United Kingdom |

20.6% |

Growing seaweed aquaculture in Scotland and Wales, rising functional food demand, government R&D grants | Food & beverage, pharmaceuticals, bioplastics |

| Germany |

16.3% |

High pharmaceutical grade ingredient demand, strong food tech innovation ecosystem, sustainability mandates |

Pharma intermediates, nutraceuticals, food processing |

| Spain | 10.8% | Atlantic coastal wild harvest, growing food service demand for seaweed-based ingredients, EU-funded projects | Direct consumption, food processing, cosmetics |

| Italy | 6.4% | Rising consumer health awareness, functional food market growth, R&D in seaweed nutraceuticals | Nutraceuticals, food ingredients, cosmetics |

| Netherlands | 4.2% | Innovation hub for bio-based economy, green seaweed research, strong logistics infrastructure | Bioplastics R&D, food tech, agricultural inputs |

| Russia | 2.8% | Far East and Barents Sea wild harvest traditions, expanding domestic food processing demand | Direct consumption, food ingredients |

| Switzerland | 1.6% | Premium nutraceuticals market, pharmaceutical demand, high consumer spending power | Nutraceuticals, cosmetics, premium food |

| Poland | 0.7% | Emerging market, rising functional food awareness, growing pharmaceutical ingredient imports | Food processing, early-stage nutraceuticals |

| Others | 14.2% | Emerging nutraceuticals market, increasing spending power | Food & beverage, pharmaceuticals |

Competitive Landscape

The Europe seaweed market is characterized by a mix of global ingredient majors with established seaweed extraction divisions alongside specialized regional producers. Key competitive dimensions include extraction technology proprietary capabilities, sustainable sourcing certifications, product portfolio breadth, and proximity to European processing hubs.

|

Company Name |

Brand / Division |

Market Position |

Strategic Focus |

| Cargill, Incorporated. | Cargill Texturizing Solutions | Leader | Global hydrocolloid supply, food-grade carrageenan, customer co-innovation |

|

Tate & Lyle |

GENUVISCO |

Leader | Pectin and carrageenan innovation, biopolymer platforms, European R&D centers |

| Gelymar | Gelymar Carrageenan | Leader |

Carrageenan specialist, vertically integrated supply chain, food & pharma |

| IFF | Danisco / Grindsted | Challenger | Specialty hydrocolloids, food texture innovation, pharmaceutical excipients |

| Ingredion | Ingredion Europe | Challenger | Starch-seaweed hybrid texturizers, clean-label ingredient portfolio |

| BioAtlantis Ltd. | SuperFifty Prime | Emerging | Seaweed-based animal feed additives, bio-stimulants, R&D partnerships |

The competitive positioning matrix maps key market participants across Market Presence (geographic reach) and Innovation Score axes. Cargill, Incorporated., Tate & Lyle occupy the Leaders quadrant, reflecting broad geographic distribution and advanced R&D capabilities.

Key Company Profiles

Cargill, Incorporated.

Cargill Incorporated is a U.S.‑based multinational food, agriculture, and industrial products corporation founded in 1865 by William Wallace Cargill and headquartered in Minnetonka, Minnesota, with operations in around 70 countries and a workforce of over 155,000 employees.

- Product Portfolio: Carrageenan, locust bean gum, pectins, and seaweed-derived food texturizers for dairy, meat, confectionery, and personal care sectors.

- Recent Developments: In 2024, Cargill enhanced the sustainability of its aquaculture feeds by diversifying raw materials, improving sourcing, and reducing reliance on wild fish stocks. Efforts include using plant-based and algae/seaweed-derived ingredients to lower environmental impact and support responsible aquaculture.

- Strategic Focus: Sustainable sourcing partnerships with certified seaweed farms, customer co-creation labs, and expansion into plant-based food formulations.

Tate & Lyle

Tate & Lyle is a British multinational food ingredients company headquartered in London, UK, and listed on the London Stock Exchange as a LON: TATE. Originally founded in 1921 as a sugar refining business, it has since transformed into a global supplier of ingredient solutions for food, beverage, and industrial markets.

- Product Portfolio: GENUVISCO carrageenan, pectin, and xanthan gum solutions for texturizing, stabilizing, and gelling applications.

- Recent Developments: In 2024, Tate & Lyle completed the acquisition of CP Kelco, a leading global provider of pectin, specialty gums, and other nature-based ingredients, from J.M. Huber Corporation. The combination creates a global speciality food and beverage solutions business, enhancing capabilities in sweetening, mouthfeel, fortification, and seaweed-derived hydrocolloids.

- Strategic Focus: Biopolymer innovation, European production network consolidation, and clean-label ingredient development for the growing organic food segment.

Gelymar

Gelymar is a Chile‑based global producer of natural seaweed‑derived hydrocolloids and textural ingredient solutions for the food, pharmaceutical, and personal care industries. Founded in the early 1990s, Gelymar has more than 30 years of experience processing carrageenan, alginates, and other hydrocolloids from sustainably harvested seaweed along Chile’s pristine coastline, supported by a worldwide distribution network across more than 50 countries.

- Product Portfolio: Semi-refined and refined carrageenan grades serving dairy, processed meat, pharmaceutical, and cosmetics applications across Europe.

- Recent Developments: In 2025, Gelymar has introduced Gely Nova, a natural ingredient derived from Chilean seaweed, designed to meet growing demand for clean-label, sustainable food solutions. Harvested under strict environmental standards in the Humboldt Current region, Gely Nova preserves essential micronutrients like calcium, magnesium, iodine, and iron without chemicals or additives.

- Strategic Focus: Vertical integration from farm-sourced seaweed to refined finished ingredients, quality consistency, and sustainability certification alignment with EU standards.

Market Concentration Analysis

The Europe seaweed market exhibits a moderately fragmented competitive structure. The top five players - Cargill, Incorporated., Tate & Lyle, Gelymar, IFF, Ingredion - are estimated to collectively account for approximately 55-60% of the total market value in 2025, with the remainder distributed across regional producers, specialty seaweed companies, and vertically integrated aquaculture operators.

This fragmentation reflects the market's dual-nature structure: a concentrated upper tier dominated by global hydrocolloid ingredient companies, and a dispersed lower tier comprising national seaweed cooperatives, family-owned coastal harvesters, and biotech start-ups primarily operating within domestic markets.

Consolidation trends are gradually emerging. Several acquisition activities between 2021 and 2024 involved European specialty seaweed companies being absorbed into larger ingredient conglomerates seeking to strengthen sustainable raw material supply chains. The rate of consolidation is projected to accelerate as sustainability-linked procurement policies raise the competitive premium for certified supply chain integration.

Investment & Growth Opportunities

Fastest Growing Segments

- Aquaculture Environment Segment: Driven by EU aquaculture expansion, precision farming technology adoption, and growing demand for farmed versus wild-harvested seaweed, the market is expected to grow steadily through 2034.

- Bio-stimulants Application: Europe's bio-stimulants market is growing rapidly. Seaweed-derived bio-stimulants qualify under EU Fertilizing Products Regulation 2019/1009, creating a scalable near-term market.

- Pharmaceutical & Nutraceutical Grade Ingredients: Premium segment demand from European pharmaceutical manufacturers for high purity fucoidan and laminarin extracts is growing steadily.

Emerging Market Opportunities

- Seaweed-Based Bioplastics: The European bioplastics market is expected to triple by 2030. Seaweed polysaccharide films represent a commercially viable, compostable alternative to petroleum-based packaging, attracting EU innovation funding.

- Central & Eastern European Markets: Poland, Czech Republic, and Hungary represent under-penetrated markets where rising disposable incomes and growing functional food awareness present early-mover advantages for ingredient suppliers.

- Carbon Credit & Blue Carbon Market: European seaweed farms qualify for emerging blue carbon credit mechanisms, providing an additional revenue stream for aquaculture operators and creating environmentally motivated investor interest.

Venture & Strategic Investment Trends

- European venture investment in marine biotech and seaweed-focused companies has increased significantly, reflecting growing investor confidence in the commercial scalability of seaweed ingredient and bio-material platforms.

- EU Horizon Europe has allocated significant funding to marine bio-economy R&D programs through 2027, creating co-investment frameworks for private sector participation in seaweed technology scaling.

Future Market Outlook (2026-2034)

The Europe seaweed market is positioned for sustained expansion through 2034, with the market projected to reach USD 1,177.93 Million - representing a net absolute growth of USD 505.94 Million from the 2025 baseline of USD 671.98 Million. The 6.24% CAGR reflects balanced growth across established food and hydrocolloid applications and emerging high-value segments including pharmaceuticals, bioplastics, and precision agriculture.

Technological disruptions - particularly automation in offshore aquaculture, next-generation biorefinery platforms, and AI-driven marine ecosystem monitoring - are expected to drive efficiency gains that compress production costs and expand addressable application markets. By 2030, the market is expected to reach USD 909.57 Million, reflecting solid mid-period momentum.

Policy alignment under the EU Green Deal, Farm to Fork Strategy, and Blue Economy Action Plan will continue to provide a supportive regulatory framework, accelerating the integration of seaweed into mainstream European food systems and bio-based industrial supply chains. France and the United Kingdom are expected to retain their leadership positions, while Germany, and emerging markets in Spain and Italy are anticipated to record above-average growth rates through 2034.

Research Methodology

Primary Research

Primary data collection involved structured interviews with seaweed industry professionals including aquaculture operators, hydrocolloid processing plant managers, food ingredient procurement executives, and regulatory affairs specialists across France, the United Kingdom, and Germany. These interviews validated market sizing assumptions and provided qualitative intelligence on competitive dynamics, pricing trends, and emerging application areas.

Secondary Research

Secondary data sources included European Commission Blue Economy reports, EU Aquaculture Advisory Council publications, Eurostat trade and production data, FAO fisheries and aquaculture statistics, corporate annual reports and investor presentations, trade association publications from the European Seaweed Association, and peer-reviewed academic literature from marine biotechnology journals.

Forecasting Models

Market sizing and forecasting employed a bottom-up methodology validated through top-down cross-checks. Key modeling parameters included historical production volume trends from 2020 to 2025, application-level demand projections, country-level macroeconomic variables (GDP growth, food industry output, agricultural spend), and policy scenario weighting under the EU Green Deal and Blue Economy frameworks. Forecast confidence levels were further validated through triangulation across multiple independent data sources.

Europe Seaweed Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Environments Covered | Aquaculture, Wild Harvest |

| Products Covered | Red, Brown, Green |

| Applications Covered | Processed Foods, Direct Human Consumption, Hydrocolloids, Fertilizers, Animal Feed Additives, Others |

| Regions Covered | Germany, United Kingdom, France, Italy, Russia, Spain, Netherlands, Switzerland, Poland, Others |

| Companies Covered | Cargill, Incorporated., Tate & Lyle, Gelymar, IFF, Ingredion, BioAtlantis Ltd., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Europe seaweed market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the Europe seaweed market.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Europe seaweed industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Europe Seaweed Market Report

The Europe seaweed market was valued at USD 671.98 Million in 2025, growing steadily at a CAGR of approximately 6.24%.

The market is projected to reach USD 1,177.93 Million by 2034, expanding at a CAGR of 6.24% during the 2026-2034 forecast period.

The Europe seaweed market is expected to exhibit a CAGR of 6.24% between 2026 and 2034, reflecting robust demand across food, agriculture, and pharmaceutical end-use sectors.

France holds the largest country share at 22.4% in 2025, driven by advanced Breton coastal harvesting traditions, established processing infrastructure, and government blue economy investment.

Aquaculture dominates with a 62.4% share in 2025, driven by controlled yield output from France, and Ireland-based farms, outpacing traditional wild harvest volumes.

Brown seaweed leads with a 42.3% market share in 2025, driven by high alginate demand from food processing, pharmaceutical, and cosmetics manufacturers across Western Europe.

Key drivers include rising plant-based food demand, EU Green Deal and Blue Economy policy support, expanding hydrocolloid applications, and growth in seaweed-based bio-stimulants and bio-economy applications.

Leading companies include Cargill, Incorporated., Tate & Lyle, Gelymar, IFF, Ingredion, and BioAtlantis Ltd.

Emerging trends include seaweed-based bioplastics, precision offshore aquaculture, clean-label organic certifications, pharmaceutical ingredient applications, and integration into EU circular bio-economy frameworks.

The Europe seaweed market was valued at USD 496.45 Million in 2020, representing the beginning of the historical period covered in this report.

The Europe seaweed market is projected to reach USD 909.57 Million by 2030, reflecting continued mid-period growth driven by aquaculture expansion and rising functional food ingredient demand.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade