Europe Secondhand Luxury Goods Market Size, Share, Trends and Forecast by Product Type, Demography, Distribution Channel, and Country, 2026-2034

Europe Secondhand Luxury Goods Market Size, Share, Trends & Forecast (2026-2034)

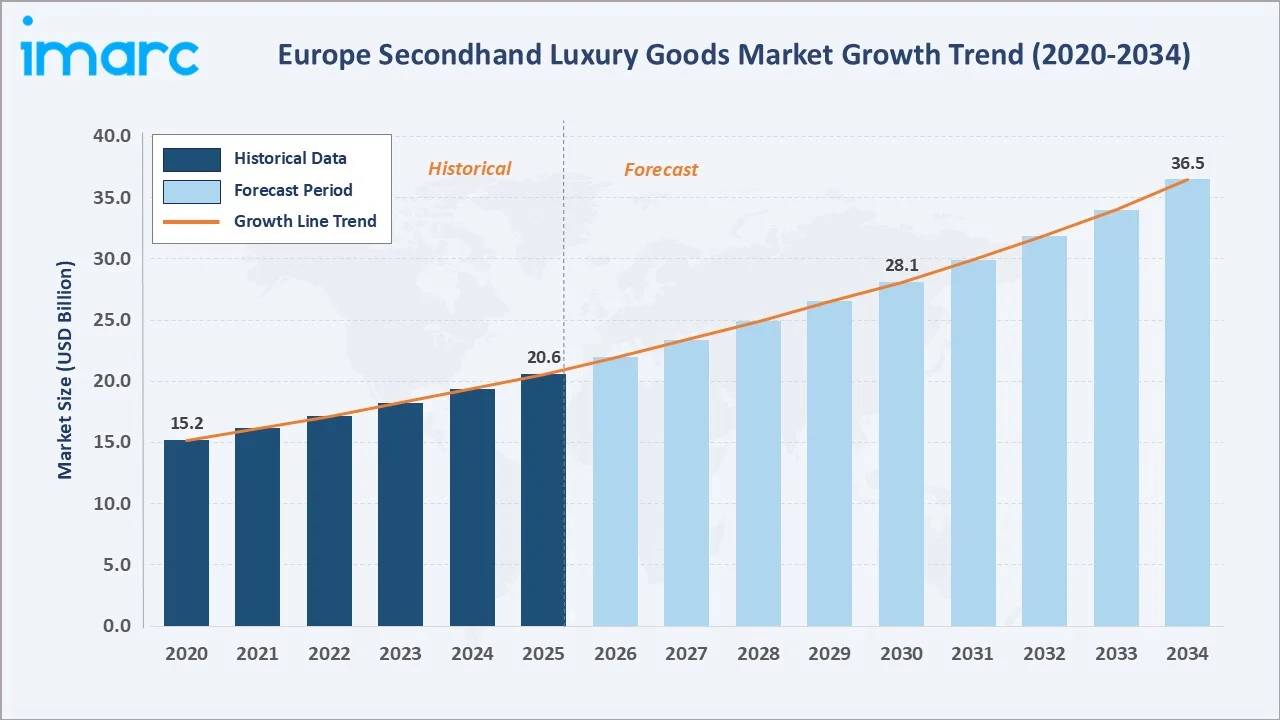

The Europe secondhand luxury goods market reached USD 20.6 Billion in 2025 and is projected to reach USD 36.5 Billion by 2034, growing at a CAGR of 6.34% during 2026-2034. Shifting consumer values toward sustainability and circular fashion, growing Millennial and Gen Z participation in the luxury resale ecosystem, rising inflation making pre-owned luxury more accessible, and the rapid proliferation of AI-powered authentication platforms are the primary growth catalysts driving the market forward.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 20.6 Billion |

|

Forecast Market Size (2034) |

USD 36.5 Billion |

|

CAGR (2026-2034) |

6.34% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Leading Country |

France (28.4% share, 2025) |

To get more information on this market, Request Sample

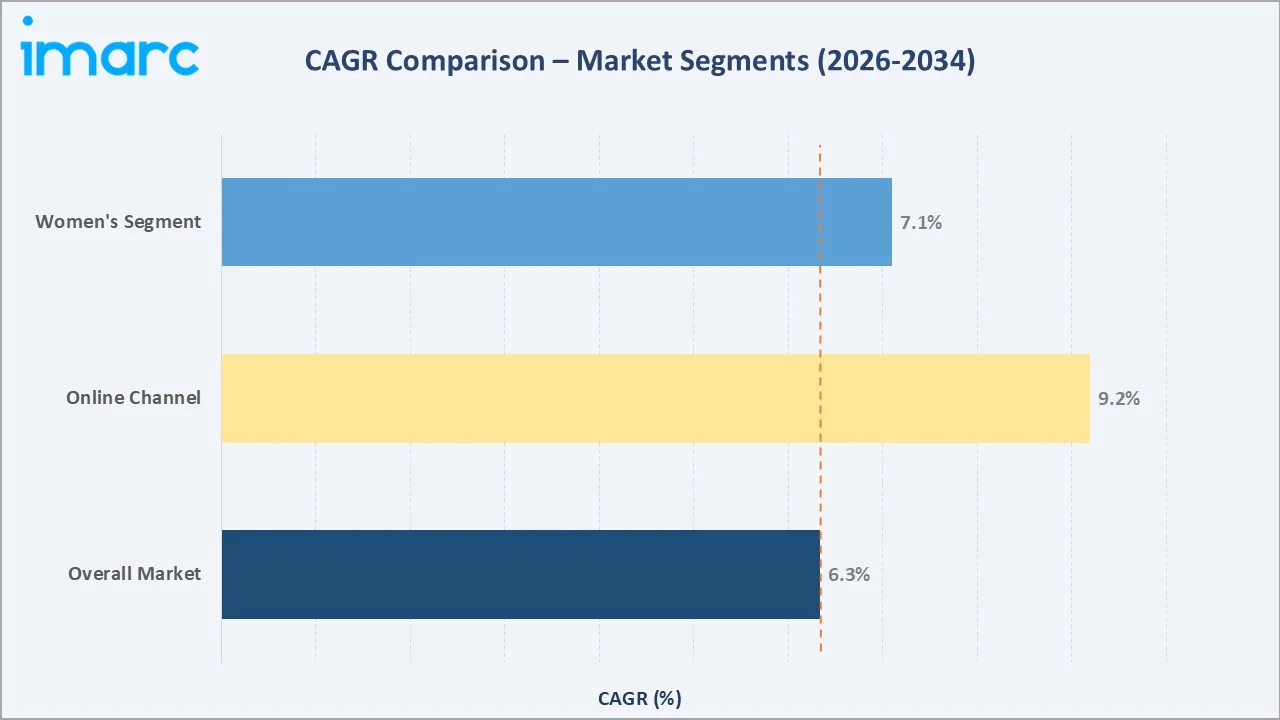

Offline channels dominate with a 62.4% share in 2025, driven by the enduring consumer preference for in-person authentication, tactile product inspection, and the curated boutique experience inherent to luxury retail. Online channels, however, are the fastest-growing distribution mode at CAGR 9.2%, underpinned by the explosive growth of digital resale platforms including Vestiaire Collective, Vinted, and Chrono24.

With consistent double-digit growth in online resale platforms, growing institutional participation from luxury houses in their own certified pre-owned programs, and increasing adoption of blockchain-based provenance tracking, the European secondhand luxury goods market is positioned for sustained, structurally driven expansion through 2034.

Executive Summary

The European secondhand luxury goods market is on a sustained structural growth trajectory, driven by a fundamental realignment of consumer values toward sustainability, affordability, and conscious consumption. The market reached USD 20.6 Billion in 2025 and is forecast to surpass USD 36.5 Billion by 2034 at a CAGR of 6.34%, representing cumulative incremental revenue creation of approximately USD 15.9 Billion over the forecast decade.

Offline retail channels retain market leadership at 62.4% in 2025, anchored by the luxury consumer's expectation for authenticated, curated, in-person purchasing experiences. Online channels, commanding 37.6% in 2025, are growing at more than twice the overall market CAGR, driven by platform scale advantages, social commerce integration, and AI-powered authentication technology that is rapidly closing the trust gap for digital luxury resale.

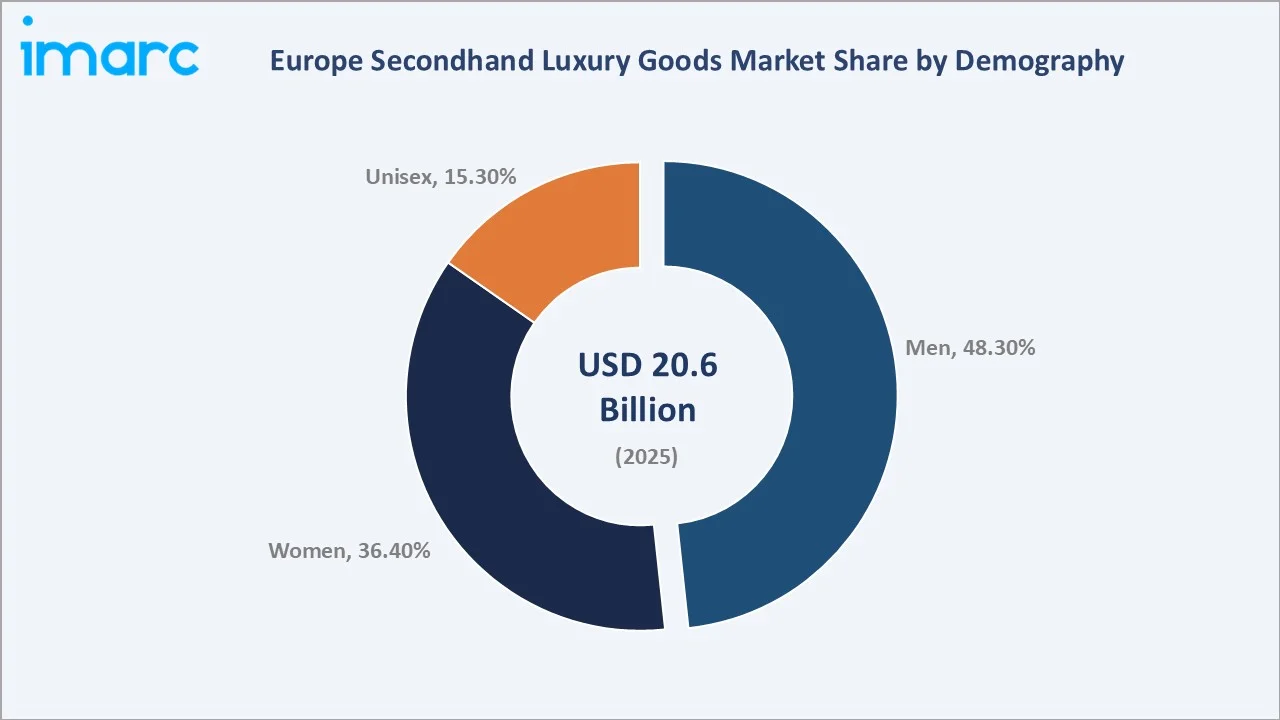

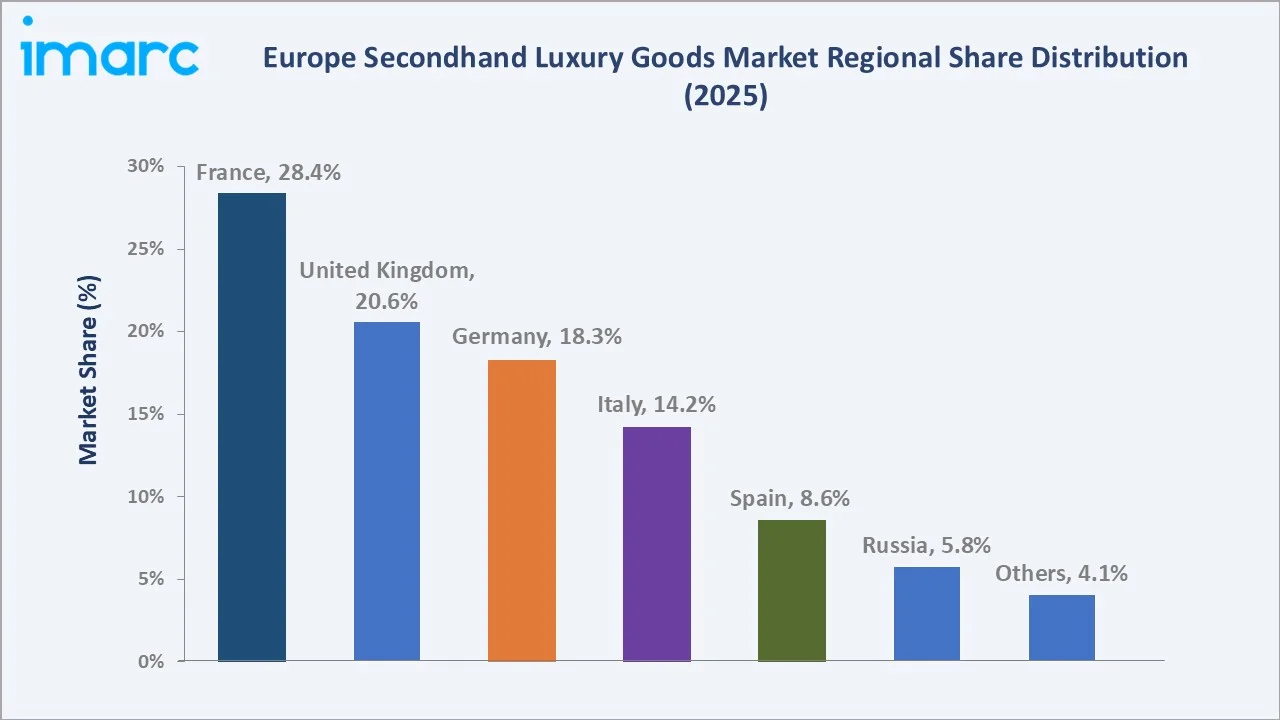

Men represent the largest demographic at 48.3%, reflecting historically strong male participation in watch, jewelry, and tailored clothing resale categories. Women's segment (36.4%) is the fastest-growing demographic CAGR at 7.1%, driven by surging demand for pre-owned designer handbags, accessories, and ready-to-wear. France (28.4%) leads the European market, followed by the United Kingdom (20.6%) and Germany (18.3%).

Key Market Insights

|

Insight |

Data |

|

Dominant Segment (Distribution Channel) |

Offline – 62.4% share (2025) |

|

Fastest Growing Channel |

Online – CAGR 9.2% (2026-2034) |

|

Largest Demographic Segment |

Men – 48.3% share (2025) |

|

Fastest Growing Demographic |

Women – CAGR 7.1% (2026-2034) |

|

Leading Country |

France – 28.4% share (2025) |

|

Market Growth Rate |

6.34% CAGR (2026-2034) |

|

Top Companies |

Vestiaire Collective, Vinted, Chrono24, Sellier Knightsbridge, and Buddy&Selly |

Key Analytical Observations Supporting The Above Data:

- Offline channels hold 62.4% of the European secondhand luxury goods market in 2025: anchored by the luxury consumer's preference for in-person authentication, physical inspection of condition and provenance, and the aspirational retail environment of specialist resale boutiques.

- Online channels are the fastest-growing distribution mode at CAGR 9.2%: driven by platform network effects, social commerce integration, AI-powered authentication tools (Entrupy, Real Authentication), and a generation of digital-native luxury consumers comfortable with high-value online transactions.

- Men constitute the largest demographic segment at 48.3%: reflecting strong participation in the watch, fine jewelry, and tailored clothing pre-owned categories, particularly across Chrono24 and specialist watch auction platforms operating across Germany and Switzerland.

- France leads European secondhand luxury consumption at 28.4%: as the birthplace and global headquarters of leading luxury houses (LVMH, Kering, Hermès) and digital resale platforms (Vestiaire Collective), with a deeply embedded culture of appreciating pre-owned luxury as heritage rather than compromise.

Europe Secondhand Luxury Goods Market Overview

The European secondhand luxury goods market encompasses the resale, consignment, auction, peer-to-peer trading, and certified pre-owned (CPO) sale of authenticated luxury articles, including jewelry, watches, handbags, clothing, small leather goods, footwear, accessories, and other premium branded items.

The market operates across multiple channels, dedicated resale platforms, consignment boutiques, luxury auction houses, department store pre-owned sections, and peer-to-peer digital marketplaces, each serving distinct consumer segments with varying price sensitivity, authentication requirements, and service expectations. The European pre-owned luxury market ecosystem increasingly mirrors the primary luxury market in its curation, service standards, and brand environment.

The market's structural drivers, shifting consumer sustainability values, increasing cost-of-living pressures, broadening the addressable consumer base for pre-owned luxury, and the growing catalogue of authenticated inventory available on digital platforms, create a self-reinforcing growth cycle that is expected to sustain above-GDP growth rates through 2034.

Market Dynamics

To evaluate market opportunities, Request Sample

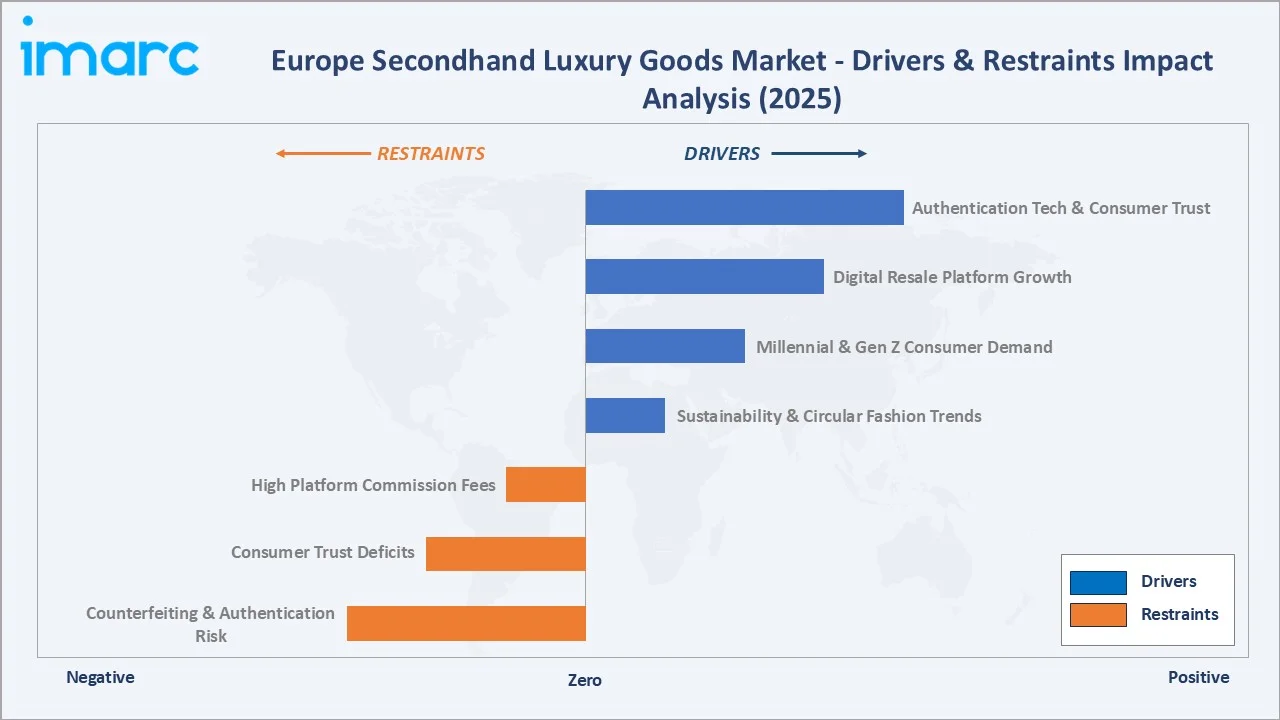

Market Drivers

- Sustainability & Circular Fashion Trends: Consumer awareness of the fashion industry's environmental footprint, accounting for approximately 10% of global carbon emissions, is driving increasing adoption of pre-owned luxury as an ethical consumption alternative.

- Growing Millennial & Gen Z Demand: The 25–40 age demographic has emerged as the primary growth engine for European secondhand luxury. They represent approximately 62% of digital resale platform transaction volumes in Europe.

- Digital Resale Platform Proliferation: The rapid scaling of dedicated secondhand luxury platforms, Vestiaire Collective (5 million items with 20,000 daily new-ins), Vinted (105M+ users), Chrono24 (500K+ watch listings), has created accessible, authenticated, and socially engaging marketplaces that are attracting mainstream luxury consumers.

- Authentication Technology Advances: AI-powered authentication tools, including Entrupy (microscopically identifies material provenance), real authentication, and blockchain-based digital ownership passports, are reducing consumer concerns about counterfeits, directly elevating transaction confidence for high-value pre-owned luxury purchases on digital platforms.

Market Restraints

- Counterfeiting & Authentication Risk: Europe remains one of the highest-volume markets for luxury counterfeits. In 2024, authorities throughout the European Union confiscated more than 112 million counterfeit items, with an estimated retail value of EUR 3.8 billion.

- Consumer Trust Deficits in Online Channels: Despite improvements in platform authentication standards, a significant segment of European luxury consumers, particularly Baby Boomers and older Gen X, remains reluctant to complete high-value transactions online without physical inspection. Platform return rates for luxury goods average 22-25%, reflecting condition and authenticity disappointment post-purchase.

- High Platform Commission Fees: Leading secondhand luxury platforms charge seller commissions of 20–35% of sale price, significantly compressing seller returns compared to private sale alternatives. This creates a price tension that reduces the supply-side incentive to list premium inventory on platforms, potentially constraining inventory growth on digital channels.

Market Opportunities

- Luxury Brand Certified Pre-Owned Program Expansion: The entry of primary luxury brands, including Richemont (Watchfinder & Co.), Rolex (Certified Pre-Owned program), and LVMH, into the certified pre-owned segment represents a structural opportunity to elevate the category's prestige and expand the addressable consumer base.

- Blockchain Provenance & Digital Ownership Passports: The EU's Digital Product Passport initiative (mandatory from 2030) and luxury brands' proprietary NFT-based ownership verification systems are creating a new infrastructure layer that will simplify authentication, transfer of ownership, and warranty management for pre-owned luxury.

- Eastern European Market Penetration: Rising consumer affluence and fashion awareness in Poland, the Czech Republic, Hungary, and Romania are creating nascent but high-growth secondhand luxury market opportunities from a low base.

Market Challenges

- Regulatory Complexity & Cross-Border Trade Compliance: VAT rules for secondhand goods across 27 EU member states add further compliance complexity for pan-European platform operators. Under EU VAT rules, second‑hand goods, including luxury items, can be taxed under a special margin scheme, where VAT is charged only on the difference between the resale price and the original purchase price rather than the full selling price.

- Inventory Sourcing & Quality Curation at Scale: As digital resale platforms scale, maintaining consistent inventory quality, accurate condition grading, and comprehensive authentication at increasing transaction volumes creates significant operational challenges.

- Luxury Brand Legal Challenges to Resale Platforms: Primary luxury brands, including Chanel and Hermès, have pursued legal actions against unauthorized resale platforms in multiple European jurisdictions, challenging platform rights to use brand names, imagery, and trademark-protected terminology in listings and marketing.

Emerging Market Trends

1. Luxury Brand Re-Commerce Programs

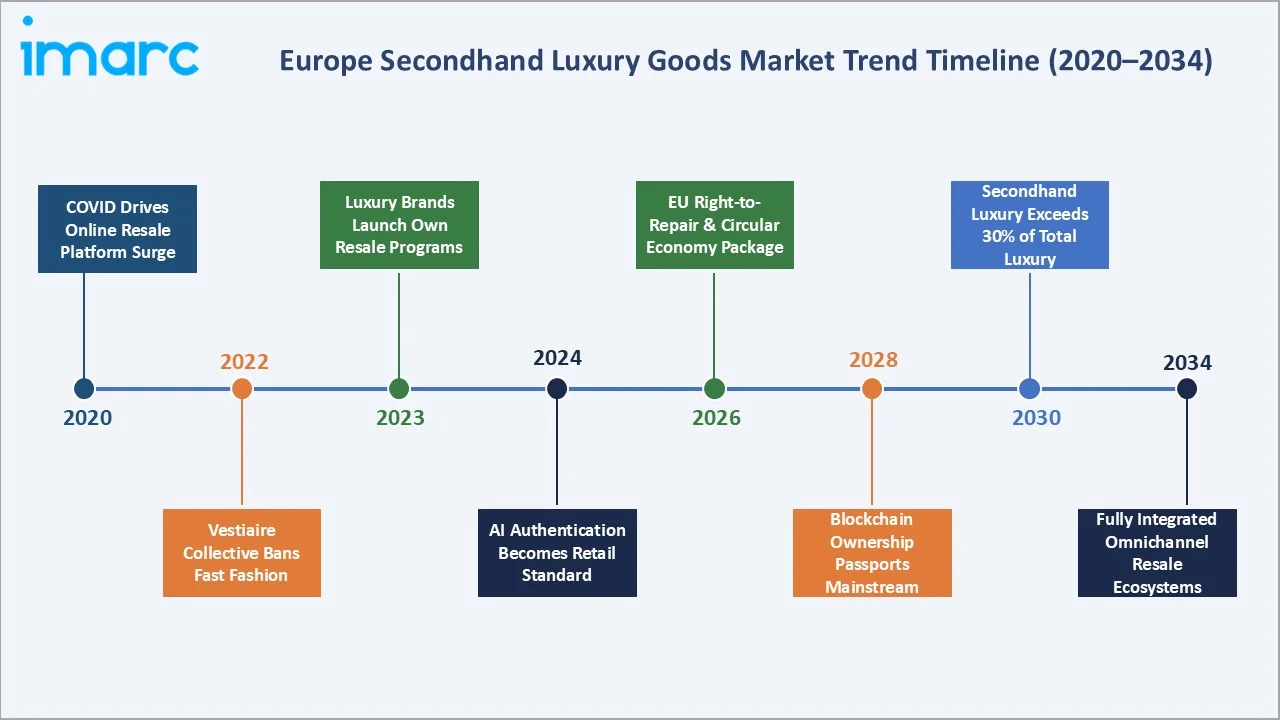

Primary luxury brands are increasingly launching proprietary certified pre-owned programs, fundamentally legitimizing the secondhand luxury category. Rolex's Certified Pre-Owned program (launched in 2022, expanded across Europe in 2023–2024) and Richemont's investment in Watchfinder & Co. are the landmark examples.

2. Social Commerce and Influencer-Driven Resale

European fashion influencers with millions of followers are hosting live resale events on Vestiaire Collective and Vinted, creating discovery and demand-generation mechanisms that are reshaping the traditional buyer journey for pre-owned luxury items.

3. AI-Powered Personalisation & Curation

Vestiaire Collective's AI curation and Vinted's recommendation engine report 35–45% improvements in purchase conversion rates versus non-personalized browsing, demonstrating the commercial value of data-driven curation in high-consideration category purchases.

4. Rental & Subscription Luxury Models as Adjacent Market

The growth of luxury rental and subscription services, including By Rotation (UK), Hurr (UK), and LaFrenchArm (France), is creating an adjacent circular luxury market segment that introduces new consumer cohorts to luxury brand experiences. These models serve as a pipeline to eventual pre-owned purchase adoption, particularly among younger consumers who begin their luxury journey through access rather than ownership.

Industry Value Chain Analysis

The European secondhand luxury goods value chain begins with luxury goods originating from original owners, private individuals, estate liquidations, and corporate gift returns, and flows through authentication, curation, platform listing, and distribution to reach the next generation of luxury consumers.

|

Stage |

Key Players / Examples |

|

Luxury Goods Origination |

Private individuals, estate liquidators, corporate gift programs, and luxury rental return cycles |

|

Collection & Acquisition |

Consignment boutiques, platform seller onboarding, brand buyback programs |

|

Authentication & Grading |

Entrupy, Real Authentication, and in-house platform authentication teams |

|

Refurbishment & Curation |

Platform restoration partners, luxury servicing specialists, professional photography studios |

|

Platform / Resale Listing |

Vestiaire Collective, Vinted, Chrono24, luxury consignment boutiques |

|

Distribution & Logistics |

FedEx International Priority, Brinks for high-value items, DPD |

|

End Consumers |

Luxury resale buyers: digital platform purchasers, boutique shoppers, auction bidders |

Technology Landscape in the European Secondhand Luxury Goods Industry

AI-Powered Authentication Technology

Entrupy uses computer-vision microscopical analysis to authenticate luxury bags with 99.86% accuracy. Real Authentication combines machine learning with human expert review for watches and jewelry. These tools are being integrated by platforms as API services, directly reducing both platform counterfeit liability and consumer abandonment due to authenticity concerns.

Blockchain Digital Ownership Passports

LVMH's Aura Blockchain Consortium (shared across Louis Vuitton, Bulgari, and Prada) provides immutable ownership and provenance records transferable upon resale. The EU's mandatory DPP regulation, applying to fashion and luxury goods from 2030, will standardize ownership and material transparency data, creating the infrastructure for frictionless, trustworthy secondhand luxury transactions at scale.

Dynamic Pricing & Real-Time Market Intelligence

Data platforms, including WP Diamonds, Cardboard Box (watch market intelligence), and Vestiaire Collective's internal pricing algorithm, provide real-time secondary market pricing signals that are replacing the historically opaque consignment pricing of traditional boutiques.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product Type |

Jewelry and Watches |

🔒 |

2025 |

|

Demography |

Men |

48.3% |

2025 |

|

Distribution Channel |

Offline |

62.4% |

2025 |

|

Country |

France |

28.4% |

2025 |

By Distribution Channel

To access detailed market analysis, Request Sample

Offline channels dominate with a 62.4% share in 2025, encompassing specialist consignment boutiques, luxury department store pre-owned sections, auction houses (Christie's, Sotheby's, Artcurial), and brand-operated certified pre-owned retail environments. Online channels account for 37.6% (~USD 7.75 Billion) and represent the market's primary growth engine at CAGR 9.2% over 2026-2034.

By Demography

Men represent the largest demographic at 48.3% of market value in 2025 (~USD 9.95 Billion), driven primarily by the high average transaction value in men's luxury watch resale (average Chrono24 European transaction: ~EUR 4,800), fine jewelry, and tailored clothing categories. Women account for 36.4% (~USD 7.50 Billion), with the Unisex segment comprising 15.3% (~USD 3.15 Billion).

Regional Market Insights

France's market leadership (28.4%, 2025) is structurally anchored by its position as the global headquarters of leading luxury conglomerates, LVMH, Kering, and Hermès, whose brands dominate secondhand luxury transaction volumes globally, and as the home of Vestiaire Collective,

|

Country |

Share (2025) |

Key Growth Drivers |

Regulatory Impact |

|

France |

28.4% |

Luxury goods heritage; Vestiaire Collective HQ; strong Gen Z resale culture; Videdressing |

EU Consumer Rights Directive; French Loi Pacte circular economy targets; DPP readiness |

|

United Kingdom |

20.6% |

Strong consignment boutique culture; luxury auction house leadership (Christie's); growing digital platform adoption |

UK Consumer Rights Act; HMRC VAT margin scheme for second-hand goods; post-Brexit import complexity |

|

Germany |

18.3% |

World's largest watch resale market (Chrono24 HQ); strong luxury consumer base; growing online resale platforms |

German UWG unfair competition rules; ZAW advertising standards; strict consumer protection enforcement |

|

Italy |

14.2% |

Heritage luxury goods origination (Gucci, Versace, Prada resale depth); strong offline boutique culture in Milan/Florence |

Italian Codice del Consumo; fashion IP enforcement; regional luxury resale boutique licensing |

|

Spain |

8.6% |

Growing digital native consumer base; Vinted leading platform; increasing sustainability awareness among urban consumers |

Spanish LGDCU consumer protection; e-commerce regulations; online marketplace VAT compliance |

|

Russia |

5.8% |

High-net-worth collector market; strong watch and jewellery resale demand; specialist offline boutiques in Moscow |

Sanctions impact on cross-border flows; Russian consumer protection legislation; payment restriction complexity |

|

Others |

4.1% |

Growing adoption in Netherlands, Belgium, Switzerland, Sweden, Poland; cross-border platform penetration |

Varied national regulations; EU CFP compliance; increasing pan-European platform access |

Western Europe, France, the UK, Germany, and Italy collectively account for 71.1% of the European secondhand luxury market value in 2025, reflecting the concentration of affluent, fashion-literate consumers, established luxury retail infrastructure, and dominant platform headquarters in these four markets.

Competitive Landscape

The European secondhand luxury goods market exhibits a moderately concentrated digital platform segment dominated by Vestiaire Collective, Vinted, Chrono24, Sellier Knightsbridge, and Buddy&Selly. The top five digital platforms collectively facilitate approximately 40–45% of European online secondhand luxury transaction value in 2025.

|

Company Name |

Brand Name |

Market Position |

Core Strength |

|

Vestiaire Collective |

Vestiaire Collective |

Market Leader |

Europe's leading curated luxury resale platform; 20M+ members; AI authentication; pan-European coverage |

|

Vinted |

Vinted |

Market Leader |

Europe's largest C2C fashion platform; 65M+ users; dominant in accessible luxury; strong Gen Z base |

|

Chrono24. |

Chrono24 |

Strong Challenger |

World's watch marketplace; 500K+ watch listings; USD 1B+ annual transactions; expert authentication |

|

Sellier Knightsbridge |

Sellier |

Niche Specialist |

UK's fastest growing pre-loved luxury platform; specializes in rare Hermès, Chanel, and Dior; prominent years of authentication expertise |

|

Buddy&Selly |

Buddy&Selly |

Strong Challenger |

AI-powered patented purchasing software for instant pricing and authentication; serves Germany, Austria, and Luxembourg |

Key Company Profiles

Vestiaire Collective

Vestiaire Collective, headquartered in Paris, France, is Europe's leading curated luxury resale platform, operating a peer-to-peer marketplace for authenticated pre-owned luxury items across fashion, accessories, watches, and jewelry.

- Product Portfolio: Pre-owned luxury fashion, handbags, shoes, accessories, watches, jewelry, and fine arts across 12,000+ designer brands; Direct Shipping and Expert Authentication services.

- Recent Developments: Banned fast fashion brands from the platform (2022); launched AI-powered Direct Authentication technology (2023); expanded seller direct shipping model to reduce authentication turnaround times.

- Strategic Focus: Curated sustainability positioning; platform authentication technology leadership; expansion into luxury watches and fine jewelry categories; geographic expansion in Germany, the UK, and Italy.

Vinted

Vinted, headquartered in Vilnius, Lithuania, is Europe's largest peer-to-peer fashion resale platform with 105 million registered users across 20+ European markets. Founded in 2008, the platform democratizes pre-owned fashion across all price points, with a growing accessible luxury segment.

- Product Portfolio: Second-hand clothing, footwear, and accessories across all price tiers; Vinted Go logistics service; Vinted Premium for authenticated luxury items.

- Recent Developments: Launched Vinted Premium, an authenticated luxury tier in 2023; expanded Vinted Go pan-European parcel delivery network; reached EUR 596M revenue in 2023, up 61% YoY; launched in Romania, Denmark, and Finland.

- Strategic Focus: European market penetration and user acquisition; authenticated luxury tier development; logistics network self-sufficiency via Vinted Go; adjacent market expansion into electronics and home goods.

Chrono24.

Chrono24., headquartered in Karlsruhe, Germany, is the world's largest online marketplace for pre-owned and new luxury watches, connecting buyers and sellers across 125 countries. The platform lists over 500,000 watches with a combined value exceeding EUR 6B+, making it the defining price-discovery and transaction platform for the global secondary watch market.

- Product Portfolio: Pre-owned and new luxury watches from Rolex, Patek Philippe, Audemars Piguet, IWC, Cartier, and 1,500+ other brands; Trusted Checkout escrow payment and buyer protection services.

- Recent Developments: Launched enhanced AI-powered watch authentication in 2024; expanded Chrono24 Finance watch loans service across Europe; entered a strategic data partnership with Swiss watch industry associations.

- Strategic Focus: Watch market platform dominance; financial services expansion (loans, insurance); direct-to-consumer brand partnerships; geographic expansion in Asia Pacific and US markets.

Market Concentration Analysis

The European secondhand luxury goods market exhibits a bifurcated concentration structure: relatively moderate concentration in digital platforms, where Vestiaire Collective, Vinted, and Chrono24 collectively dominate online transaction volumes; and high fragmentation in the offline segment, where thousands of independent consignment boutiques, auction specialists, and pawn operations each hold sub-1% market shares.

Consolidation in the digital platform segment is accelerating through M&A (Kering's Vestiaire investment, Richemont's Watchfinder ownership) and organic platform expansion. The offline segment is characterized by geographic specialization, with Paris, London, Milan, and Geneva as the highest-concentration offline luxury resale cities, and brand specialization (watch-focused boutiques, handbag specialists, full-portfolio consignment stores).

Investment & Growth Opportunities

Fastest Growing Segments

Online luxury resale (CAGR 9.2%), women's luxury accessories resale (CAGR 7.1%), and certified pre-owned luxury watches (CAGR 8.0%) represent the three highest-growth investment vectors in the European market through 2034. Together, these segments address an incremental addressable opportunity of approximately USD 8.5 Billion by 2034.

Emerging Market Expansion

Eastern European markets — Poland, Czech Republic, Hungary, and Romania — represent the most compelling geographic growth frontier within Europe for secondhand luxury, with platform-led adoption growing at 15–20% annually from a low base. Rising disposable incomes, expanding Vinted and Vestiaire Collective penetration, and growing sustainability awareness among urban millennials are structural adoption enablers in these markets.

Venture and Institutional Investment Trends

- Authentication technology startups (Entrupy, Real Authentication, Legitmark): are attracting Series A–B funding as platform dependencies on third-party AI authentication services scale with transaction volumes.

- Blockchain DPP infrastructure companies: aligned with EU Digital Product Passport regulation (mandatory 2030), are attracting strategic investment from luxury conglomerates and logistics providers building the infrastructure for frictionless pre-owned luxury provenance tracking.

- Luxury resale logistics specialists, including white-glove luxury parcel carriers, secure vaulting operators (for high-value watches and jewelry), and platform-integrated returns management providers, are attracting growth equity as platform transaction volumes scale.

Future Market Outlook (2026-2034)

The European secondhand luxury goods market is positioned for sustained, structurally driven growth through 2034. From a base of USD 20.6 Billion in 2025, the market is projected to reach USD 36.5 Billion by 2034 at a CAGR of 6.34%, representing cumulative incremental market value creation of approximately USD 15.9 Billion.

Regulatory tailwinds, the EU Digital Product Passport (2030), the EU Right-to-Repair Regulation, and the EU Sustainable Products Regulation, will collectively reinforce circular economy momentum and create a more transparent, trusted infrastructure for secondhand luxury transactions. Luxury brand participation through CPO programs will continue to expand, progressively elevating the category's prestige and broadening the addressable consumer base beyond current secondhand luxury purchasers.

Three structural macro-themes anchor the market's long-term trajectory: the irreversible shift in consumer values toward conscious consumption and circular fashion among younger demographic cohorts; the continuing deflationary impact of digital platform efficiency on transaction costs, expanding the addressable consumer base; and the technology-driven resolution of authentication trust barriers.

Research Methodology

Primary Research

Primary research for this report comprised structured interviews and surveys with over 135 industry participants in 2024–2025, including luxury resale platform executives, consignment boutique operators, luxury auction specialists, brand CPO program managers, authentication technology providers, and consumer associations across France, Germany, the UK, Italy, and Spain.

Secondary Research

Secondary research encompassed a systematic review of European Commission retail and sustainability policy documentation, luxury brand annual reports, platform company disclosures, trade publications (Business of Fashion, WWD, Europa Star), industry databases (Euromonitor, Statista, Bain & Company Luxury Study), and publicly available transaction and platform data. Over 230 secondary sources were reviewed and triangulated.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting approaches, incorporating European consumer spending indices, platform transaction growth rates, demographic adoption curves, and historical market evolution patterns. A base-case CAGR of 6.34% reflects consensus analyst estimates validated against reported platform GMV growth trajectories and consumer survey data.

Europe Secondhand Luxury Goods Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Product Types Covered | Jewelry and Watches, Handbags, Clothing, Small Leather Goods, Footwear, Accessories, Others |

| Demographies Covered | Men, Women, Unisex |

| Distribution Channels Covered | Offline, Online |

| Countries Covered | France, Italy, United Kingdom, Germany, Russia, Spain, OthersS |

| Companies Covered | Vestiaire Collective, Vinted, Chrono24., Sellier Knightsbridge, Buddy&Selly, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Europe secondhand luxury goods market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the Europe secondhand luxury goods market.

- The study maps the leading, as well as the fastest-growing, regional markets.

- Porter's Five Forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Europe secondhand luxury goods industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Europe Secondhand Luxury Goods Market Report

The Europe secondhand luxury goods market reached USD 20.6 Billion in 2025 and is projected to reach USD 36.5 Billion by 2034, growing at a CAGR of 6.34% during 2026-2034.

Offline channels dominate with a 62.4% share in 2025, driven by consumer preference for in-person authentication and the curated boutique experience. However, online channels at 37.6% are growing at CAGR 9.2%, the fastest-growing segment in the market.

Men represent the largest demographic at 48.3% in 2025, primarily driven by high-value watch and fine jewelry resale. Women's segment (36.4%) is the fastest-growing demographic CAGR at 7.1%, fueled by designer handbag and accessories resale demand.

France leads with a 28.4% share in 2025, reflecting its luxury heritage, the headquarters of Vestiaire Collective, and a deeply embedded cultural appreciation for pre-owned luxury goods as objects of heritage and quality.

Key players include Vestiaire Collective, Vinted, Chrono24., Sellier Knightsbridge, and Buddy&Selly, among others.

Key trends include luxury brand CPO program expansion, social commerce-driven resale discovery, AI-powered authentication technology adoption, blockchain digital product passports, and the emergence of rental and subscription luxury as an adjacent access model.

Key challenges include counterfeiting and authentication risks in online channels, high platform commission structures limiting seller participation, post-Brexit cross-border trade friction, and luxury brand legal challenges to unauthorized resale platform practices.

High-priority opportunities include authentication technology platforms, blockchain DPP infrastructure aligned with EU 2030 mandate, luxury resale logistics specialists, and Eastern European market entry through digital platform expansion.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)