Europe Shrimp Market Size, Share, Trends, and Forecast by Environment, Domestic Production and Imports, Species, Product Categories, Distribution Channel 2026-2034

Europe Shrimp Market Size, Share, Trends & Forecast (2026-2034)

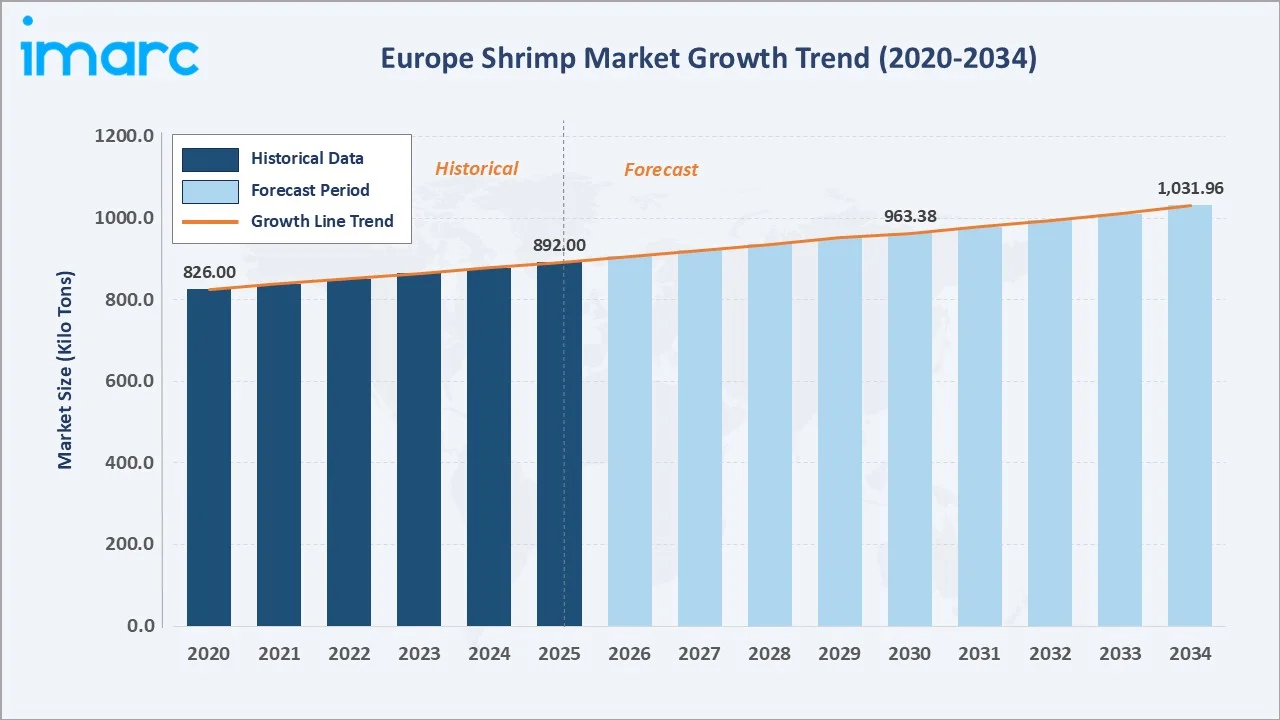

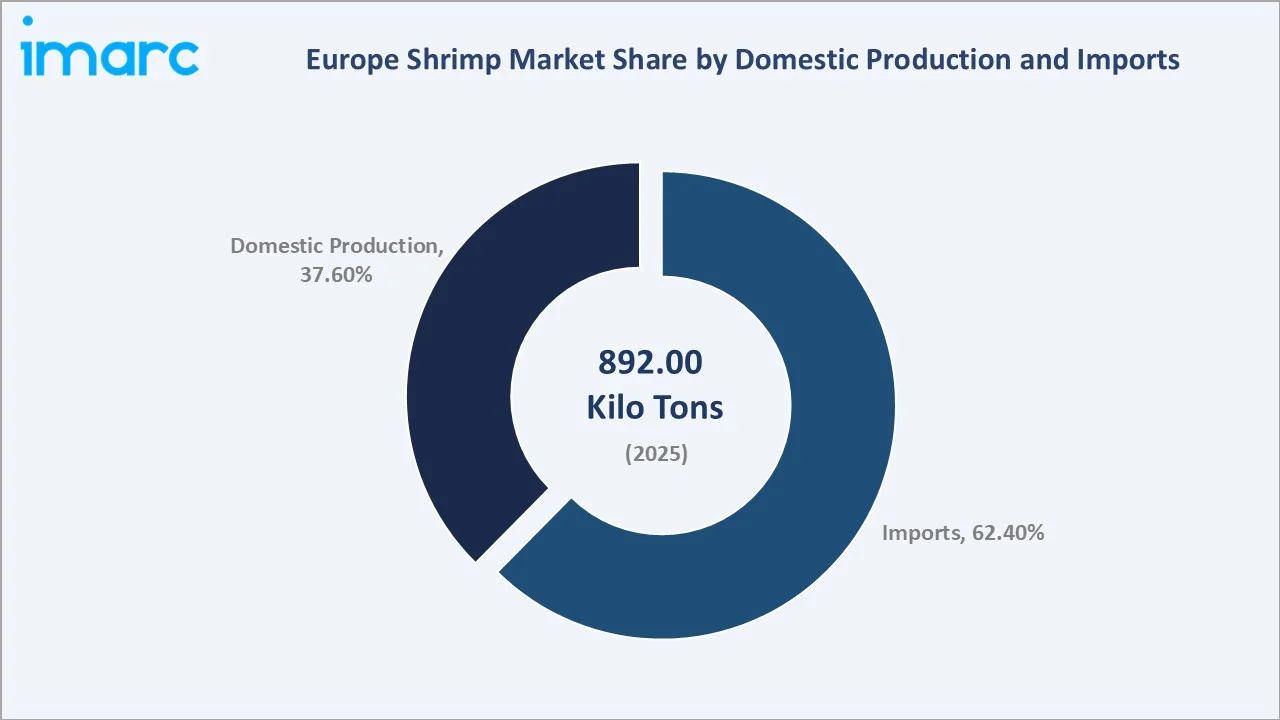

Europe shrimp market reached 892.00 Kilo Tons in 2025 and is projected to reach 1,031.96 Kilo Tons by 2034, growing at a CAGR of 1.55% during 2026-2034. Increasing seafood consumption, growing health consciousness among European consumers, rapid expansion of the HoReCa sector, and the widespread availability of competitively priced imported tropical shrimp are the primary growth catalysts driving the market.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

892.00 Kilo Tons |

|

Forecast Market Size (2034) |

1,031.96 Kilo Tons |

|

CAGR (2026-2034) |

1.55% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Consuming Country |

Spain (~22.5% share, 2025) |

|

Fastest Growing Segment |

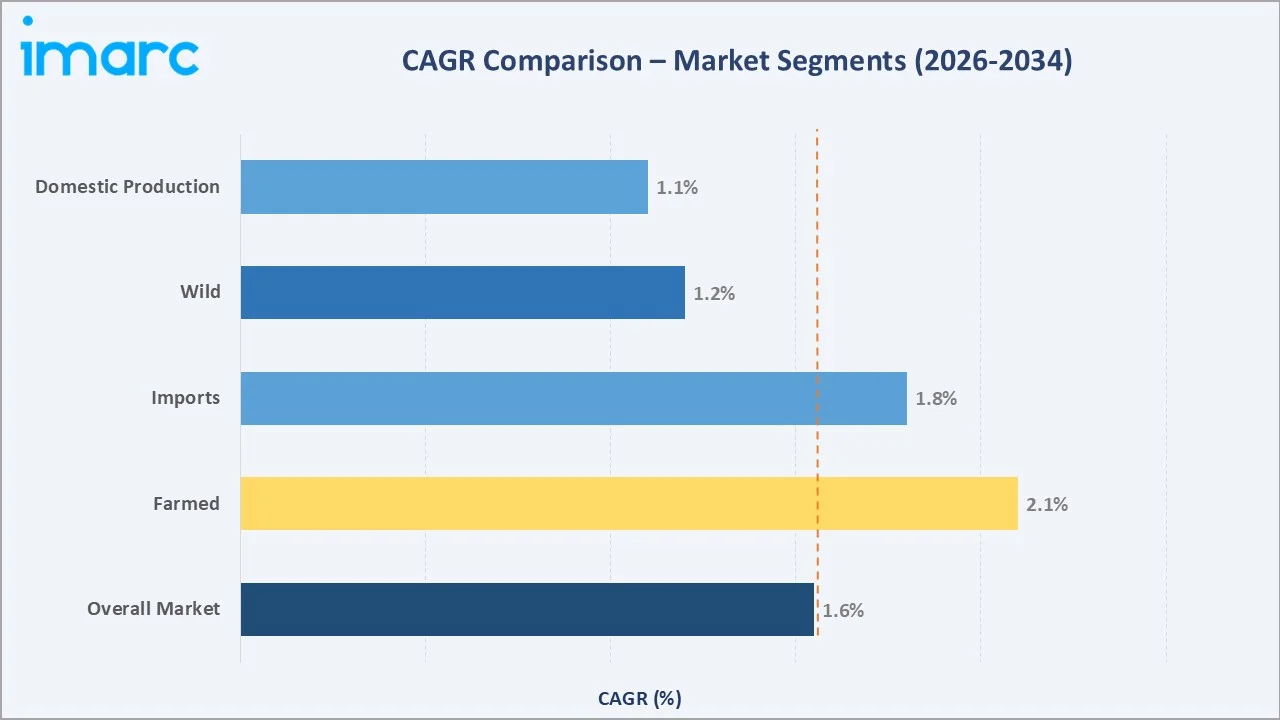

Farmed (CAGR 2.10%, 2026-2034) |

Wild shrimp dominates with a 58.4% share in 2025, underpinned by the longstanding Arctic and North Sea cold-water fisheries of Norway, Iceland, and Greenland. Imports account for 62.4% of the total supply, reflecting Europe's structural dependence on tropical shrimp-producing nations. Farmed shrimp is the fastest-growing segment, supported by a growing pipeline of eco-certified aquaculture supply from Ecuador, Vietnam, and India.

To get more information on this market, Request Sample

With consistent year-on-year demand reinforced by an expanding retail seafood segment and premiumization trends, the European shrimp market is positioned for moderate but sustained growth over the forecast horizon. Innovations in aquaculture technology, cold-chain logistics, and value-added processing continue to broaden the product offering available to European consumers.

Executive Summary

The European shrimp market is on a consistent growth path, driven by health-conscious consumption patterns, expanding foodservice channels, and increasing access to competitively priced imported shrimp. The market reached 892.00 Kilo Tons in 2025 and is forecast to surpass 1,031.96 Kilo Tons by 2034, representing a total incremental volume addition of approximately 140 Kilo Tons over the forecast decade.

Wild shrimp commands the majority of supply with a 58.4% share in 2025, underscored by the longstanding tradition of Arctic and North Sea shrimp harvesting in Norway, Iceland, and Denmark. Farmed shrimp, however, is the fastest-growing segment at a CAGR of 2.10%, as certified aquaculture operations from Ecuador, Vietnam, and India supply an increasing share of European retail and HoReCa demand.

Imports dominate the supply structure at 62.4%, reflecting Europe's structural dependence on tropical shrimp-producing nations. Key industry participants, including GRUPO NUEVA PESCANOVA, Clearwater Seafoods, HONEST CATCH, Hendrikson BV, and Sykes Seafood, are investing in supply chain transparency, sustainability certifications, and value-added product innovation to capture the growing premium segment.

Key Market Insights

|

Insight |

Data |

|

Dominant Segment (Environment) |

Wild – 58.4% share (2025) |

|

Fastest Growing Segment (Environment) |

Farmed – CAGR 2.10% (2026–2034) |

|

Supply Source Leader |

Imports – 62.4% share (2025) |

|

Leading Consuming Country |

Spain – ~22.5% share (2025) |

|

Market Growth Rate |

1.55% CAGR (2026-2034) |

|

Top Companies |

GRUPO NUEVA PESCANOVA, Clearwater Seafoods, HONEST CATCH, Hendrikson BV, and Sykes Seafood |

|

Market Opportunity |

Eco-certified farmed shrimp projected to exceed 420 Kilo Tons by 2034 |

Key Analytical Observations Supporting The Above Data:

- Wild shrimp accounts for 58.4% of the European market in 2025: valued for its natural flavor, premium positioning, and strong MSC-certified supply chain from Arctic Nordic fisheries.

- Farmed shrimp is the fastest-growing environmental segment at CAGR 2.10%: propelled by increasing supply from certified Asian and South American aquaculture operators aligned with GlobalG.A.P. and ASC standards.

- Imports represent 62.4% of the European shrimp supply in 2025: The EU's demand for shrimp is on the rise, with imports reaching 241,193 metric tons in the first half of 2025, a 14% increase compared to the same period last year, according to Eurostat trade data.

- Spain leads European shrimp consumption at 22.5%: driven by a deeply entrenched seafood culture, vibrant HoReCa sector, and widespread availability across retail channels.

- Sustainability is reshaping procurement: with major European retailers committing to 100% certified sustainable seafood by 2026–2028, driving demand for MSC- and ASC-certified shrimp products.

Europe Shrimp Market Overview

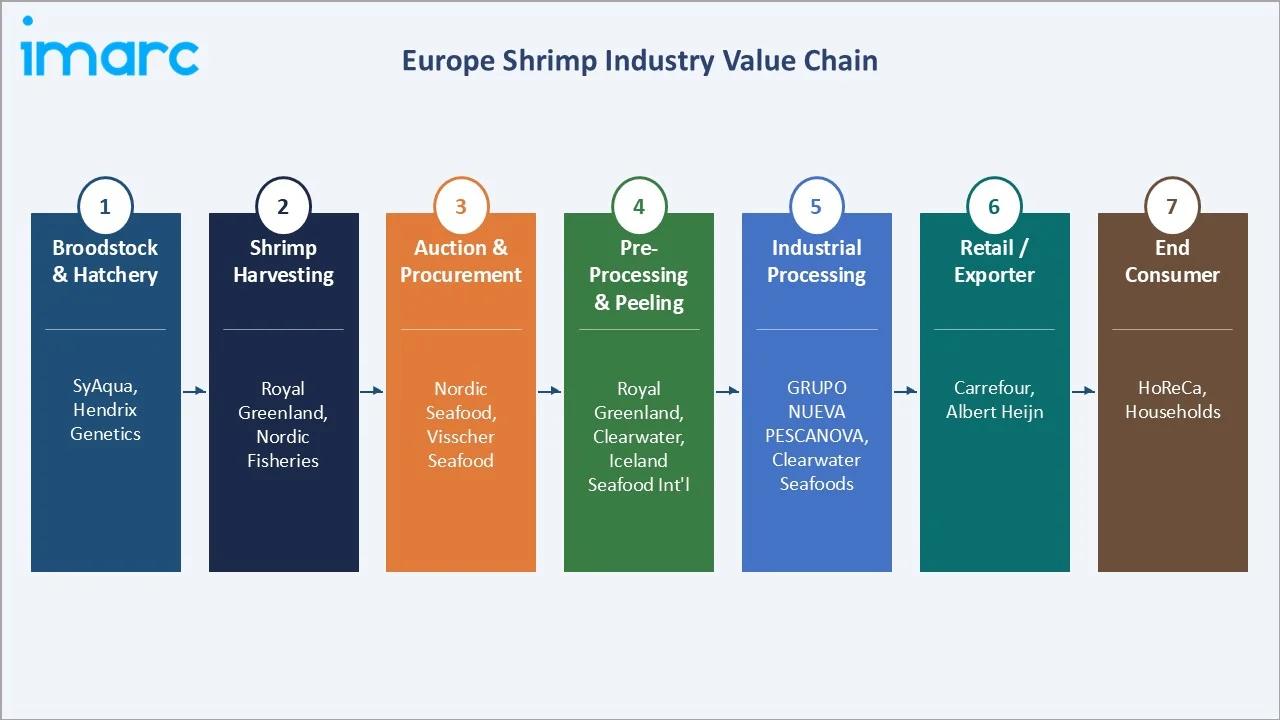

Shrimp is among the most widely consumed seafood products in Europe, valued for its versatility, nutritional richness, and premium culinary status across Mediterranean, Nordic, and Western European cuisines. The European shrimp market encompasses a diverse value chain spanning broodstock and hatchery operations, wild-capture fishing fleets, auction & procurement hubs, pre-processing & peeling facilities, large-scale industrial processing plants, retailers, exporters, and end consumers across foodservice and retail channels.

The market is characterized by a dual supply structure: wild-caught Arctic and North Sea shrimp (predominantly Pandalus borealis) sourced from Norway, Iceland, and Greenland, alongside tropical farmed shrimp (predominantly Penaeus vannamei) imported from Ecuador, Vietnam, India, and Thailand. This dual sourcing model enables year-round availability and price diversity across product categories and consumer segments.

A study by the European Commission reveals that shrimp make up 6 percent of total seafood consumption in Europe, averaging around 1.5 kg per person. By 2034, shrimp is expected to remain one of the top three most-consumed seafood categories in Europe, supported by product innovation, including ready-to-eat formats, pre-marinated variants, and organic ranges.

Market Dynamics

To evaluate market opportunities, Request Sample

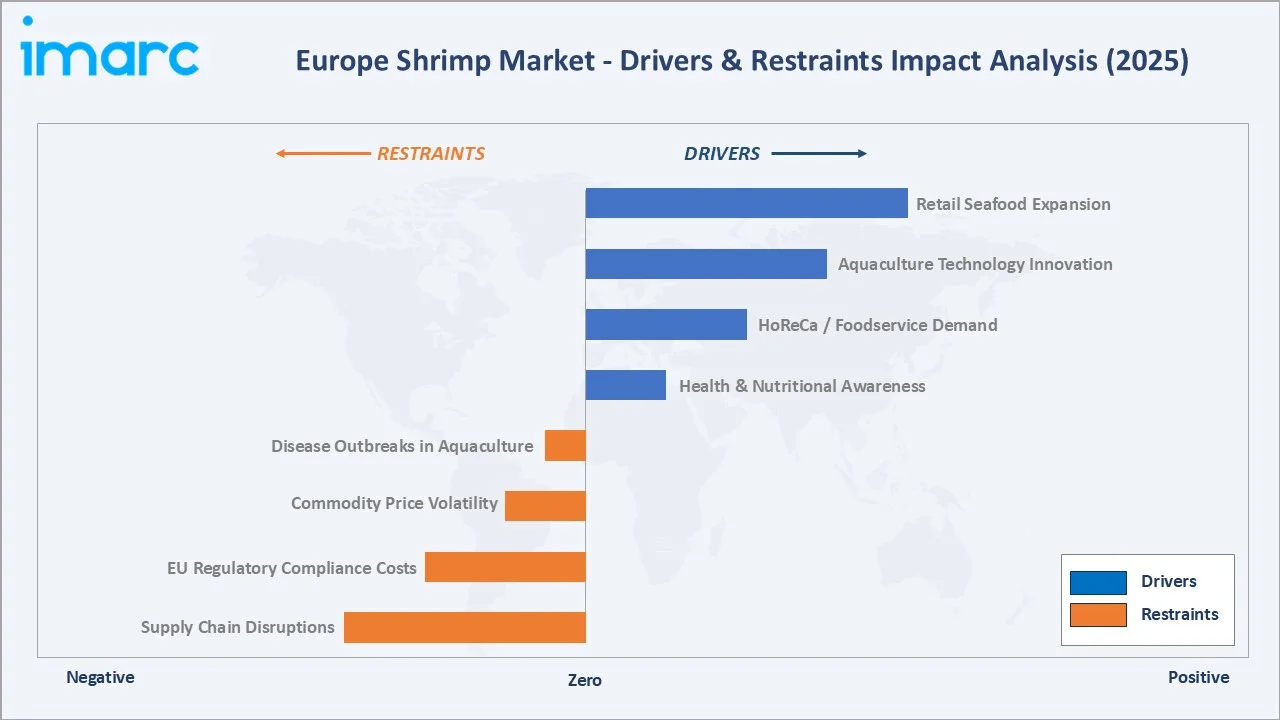

Market Drivers

- Growing Health and Nutritional Awareness: Rising consumer interest in lean protein sources across Europe is directly boosting shrimp demand, particularly in health-oriented retail formats and fitness-focused meal-kit segments.

- Expanding HoReCa and Foodservice Demand: The European hospitality, restaurant, and catering sector accounts for approximately 38% of total shrimp consumption. Post-pandemic recovery in tourism, especially in Spain, Italy, Greece, and France, has significantly revived foodservice shrimp orders, particularly for premium shell-on and whole-cooked formats.

- Aquaculture Technology Innovation: Advances in recirculating aquaculture systems (RAS), biofloc technology, and sustainable feed formulations are enabling European and imported farmed shrimp to meet the continent's stringent food safety and antibiotic-free standards, broadening the supplier base and improving cost competitiveness.

- Retail Seafood Category Expansion: European supermarkets and hypermarkets are actively expanding their chilled and frozen seafood sections. Convenience-oriented pre-cooked and marinated shrimp products are gaining strong traction among time-constrained urban consumers, contributing to volume growth across the retail channel.

Market Restraints

- Supply Chain Disruptions and Logistics Complexity: The European shrimp market depends heavily on long-distance cold-chain supply from Asia and South America. Geopolitical disruptions, port congestion, rising freight rates, and energy cost pressures highlighted significant supply chain fragility during 2022–2024.

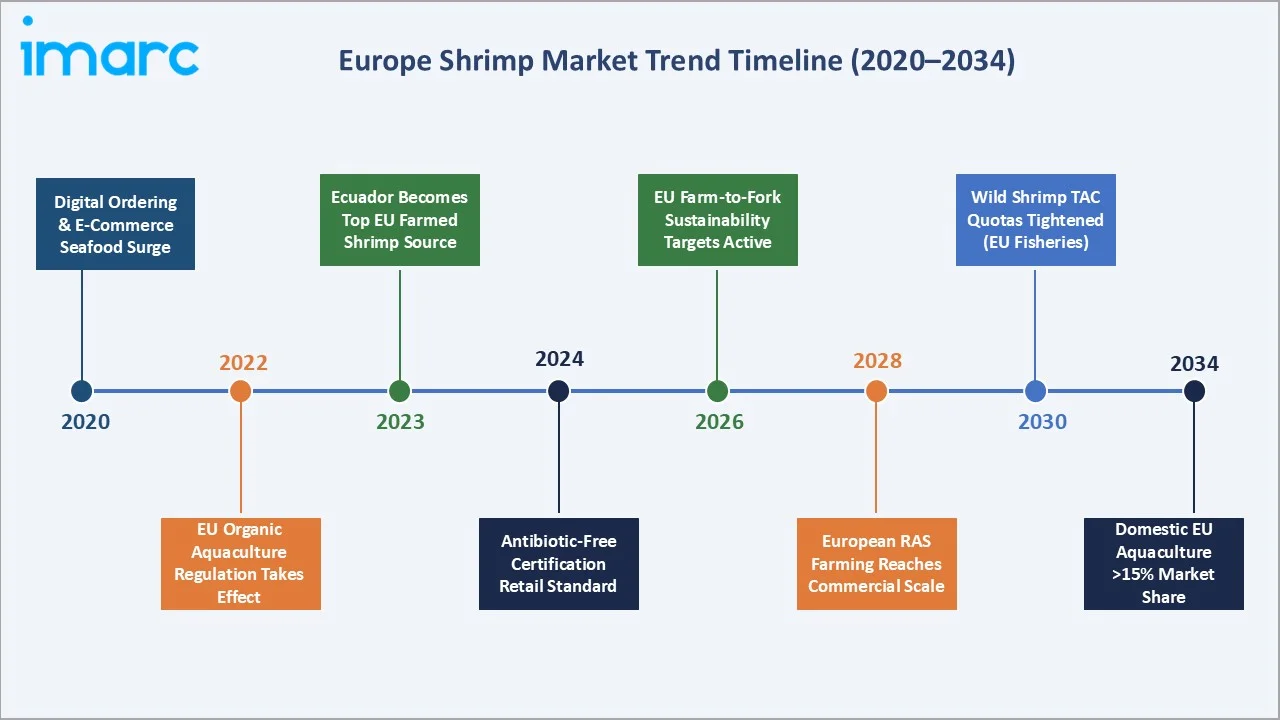

- Stringent EU Environmental and Food Safety Regulations: The European Commission's Farm-to-Fork Strategy and EU Fisheries Control Regulation impose strict traceability, labelling, and sustainability compliance requirements on shrimp importers and processors, increasing compliance costs and creating market entry barriers.

- Commodity Price Volatility: Global shrimp prices are susceptible to disease outbreaks in major aquaculture nations, currency fluctuations, and energy price volatility, impacting feed and fuel costs. Spot-market price swings of 15–25% in 2023–2024 created margin pressure across the European distribution chain.

- Disease Outbreaks in Aquaculture: White Spot Disease, Early Mortality Syndrome, and Hepatopancreatic Microsporidian infections continue to pose periodic threats to shrimp supply from key source nations, creating supply uncertainty that reverberates through the European import market.

Market Opportunities

- Eco-Certified and Organic Shrimp Growth: The growing European consumer preference for certified sustainable and organic shrimp creates a significant opportunity for suppliers aligned with MSC, ASC, and GlobalG.A.P. standards. Premium certified shrimp commands a 15–25% price premium in European retail, offering attractive margin expansion opportunities.

- Land-Based RAS Aquaculture Expansion: Domestic European shrimp farming via RAS technology is an emerging opportunity, with projects in the Netherlands, Belgium, and Germany targeting premium "locally grown" positioning. The EU's commitment to sustainable aquaculture under its Blue Economy Strategy underpins public and private investment in this segment.

- Value-Added Product Development: Growing consumer demand for convenience seafood, including pre-marinated, breaded, ready-to-cook, and meal-kit shrimp formats, offers significant product innovation and margin enhancement opportunities for processors and retailers.

Market Challenges

- Traceability and Compliance Complexity: New EU supply chain due diligence legislation and enhanced seafood traceability requirements under the revised EU Control Regulation create significant operational challenges for importers managing multi-country supply chains spanning Asia, South America, and the Arctic.

- Microplastics and Environmental Regulations: Growing regulatory scrutiny of microplastic contamination in seafood products, including shrimp, is driving additional testing and documentation requirements that increase processing costs and create potential consumer confidence risks.

- Competitive Pressure from Substitutes: Increasing competition from other affordable protein sources, including farmed salmon, tilapia, and plant-based seafood alternatives, is a growing challenge for maintaining shrimp's volume growth trajectory in price-sensitive European consumer segments.

Emerging Market Trends

1. Shift Toward Organic and Sustainability-Certified Shrimp

The European retail and foodservice sector is accelerating its transition toward MSC-certified wild shrimp and ASC-certified farmed shrimp. According to the MSC UK and Ireland Market Report, consumers spent GBP 1.7bn on 189,000 tons of MSC-labeled products, representing a 14% increase over the previous year.

2. Rise of Convenience and Value-Added Shrimp Products

The convenience seafood segment in Europe grew at approximately 7.2% annually between 2020 and 2024, driven by time-constrained urban consumers seeking premium but easy-to-prepare protein options. Value-added shrimp products now represent approximately 28% of total retail shrimp volume in Western Europe.

3. European Domestic RAS Aquaculture Emergence

Projects in the Netherlands (Bluefarm), Belgium, and Germany are demonstrating commercial viability at a small scale, targeting the "locally produced" and ultra-premium positioning. European RAS shrimp commands retail prices 30–40% above imported equivalents, creating a compelling premium value proposition.

4. E-Commerce and Direct-to-Consumer Seafood Growth

Online seafood sales in Europe grew from approximately 4.8% of total seafood retail volume in 2020 to over 9.3% in 2024, accelerated by the COVID-19 pandemic and the sustained adoption of online grocery shopping. Shrimp is among the top-selling seafood categories in direct-to-consumer and subscription-box formats, driving new distribution models for both premium wild-caught and certified farmed shrimp.

Industry Value Chain Analysis

The European shrimp value chain spans from raw material sourcing and aquaculture/wild-catch production through to processing, distribution, and end consumption, with each stage populated by specialized operators whose performance directly influences product quality, sustainability credentials, and delivered cost.

|

Stage |

Key Players / Examples |

|

Broodstock & Hatchery |

SyAqua Group, Hendrix Genetics |

|

Shrimp Harvesting & Farming |

Royal Greenland (wild) |

|

Auction & Procurement |

European shrimp auction/procurement operators |

|

Pre-Processing & Peeling |

Royal Greenland, Clearwater, Iceland Seafood Int'l |

|

Industrial Processing |

GRUPO NUEVA PESCANOVA, Clearwater Seafoods |

|

Retail / Exporter / Distribution |

Carrefour, Tesco, Albert Heijn, Lidl |

|

End Consumers |

HoReCa sector, household retail, food manufacturing |

Technology Landscape in the European Shrimp Industry

Recirculating Aquaculture Systems (RAS)

Advanced RAS technology enables land-based shrimp farming in controlled-environment facilities, eliminating the environmental footprint of tropical aquaculture while producing an antibiotic-free, year-round shrimp supply. European RAS installations achieved commercial production costs of EUR 8–10/kg in 2024, down from EUR 15–18/kg in 2020, as system efficiency and operational expertise improve.

Blockchain-Based Traceability Platforms

Supply chain traceability technology, including blockchain platforms such as Trace Register and Provenance, is gaining adoption among European shrimp importers and retailers to meet EU due diligence requirements and consumer transparency demands.

AI-Powered Aquaculture Farm Management

Artificial intelligence platforms integrated with IoT sensors are enabling real-time monitoring of water quality, feeding optimization, and disease early-warning in farmed shrimp operations. In August 2025, DNV, the independent assurance and risk management provider, launched a new AI-powered fish farm technology aimed at helping meet the compliance requirements established by the Norwegian government.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Environment |

Wild |

58.4% |

2025 |

|

Domestic Production and Imports |

Imports |

62.4% |

2025 |

|

Species |

🔒 |

🔒 |

2025 |

|

Product Categories |

🔒 |

🔒 |

2025 |

| Distribution Channel |

🔒 |

🔒 |

2025 |

By Environment

To access detailed market analysis, Request Sample

Wild shrimp dominate the environment segment with a 58.4% share in 2025 (~521 Kilo Tons). Its dominance reflects the longstanding supply base of Arctic cold-water fisheries and strong premium demand across Nordic and Western European markets. Farmed shrimp holds a 41.6% share (~371 Kilo Tons) and is the fastest-growing segment with a CAGR of 2.10%, driven by consistent growth in certified tropical supply.

By Domestic Production and Imports

Imports dominate Europe's shrimp supply at 62.4% (~557 Kilo Tons in 2025), reflecting the continent's structural dependence on tropical shrimp-producing nations. Domestic production contributes 37.6% (~336 Kilo Tons), comprising primarily wild-capture production from Nordic and North Atlantic zones alongside nascent RAS aquaculture activity.

The EU's trade policy framework, including preferential tariff arrangements with Ecuador, Vietnam (EU-Vietnam FTA), and India, facilitates large-scale import flows at competitive landed costs. Import volumes are forecast to grow at a CAGR of 1.80% over 2026-2034, driven by continued demand for value-added processed shrimp products.

Competitive Landscape

The European shrimp market exhibits a moderately fragmented competitive structure. The top five suppliers, GRUPO NUEVA PESCANOVA, Clearwater Seafoods, HONEST CATCH, Hendrikson BV, and Sykes Seafood, collectively hold approximately 30–35% of total European market volumes in 2025. A significant long tail of regional processors, importers, specialist distributors, and private-label suppliers accounts for the remainder.

|

Company Name |

Brand Name |

Market Position |

Core Strength |

|

GRUPO NUEVA PESCANOVA |

Pescanova |

Market Leader |

Southern European retail leader; vertically integrated; broad frozen portfolio |

|

Clearwater Seafoods |

Clearwater |

Challenger |

MSC-certified FAS cold-water shrimp |

|

HONEST CATCH |

Honest Catch / Bavarian Shrimp |

Niche Player |

Germany-based pioneer in land-based RAS shrimp farming; first German-farmed premium shrimp ("Bavarian Shrimp"); antibiotic-free |

|

Hendrikson BV |

Hendrikson Shrimping |

Niche Player |

Netherlands-based specialist shrimp importer and wholesale distributor; owns fishing boats and shrimp farm; MSC/ASC certified; distributes grey (North Sea), tropical, and crayfish across Europe; |

|

Sykes Seafood |

Arctic Royal / Clear Seas / Ocean Classic / Glenmyr |

Strong Challenger |

UK's leading independent frozen shrimp supplier; USD 550M pan-European shrimp platform; facilities in the UK, the Netherlands, and Morocco |

Key Company Profiles

GRUPO NUEVA PESCANOVA

GRUPO NUEVA PESCANOVA, headquartered in Redondela (Pontevedra), Spain, is a major vertically integrated seafood company with significant shrimp sourcing, processing, and distribution capabilities. The company sources shrimp from its own aquaculture operations and third-party suppliers in Latin America and Asia, offering a broad frozen and chilled shrimp portfolio under the Pescanova brand.

- Product Portfolio: Frozen tropical shrimp in raw, cooked, peeled, and breaded formats; value-added marinated and convenience shrimp products.

- Recent Developments: Invested in expanding its aquaculture traceability platform to meet evolving EU food labelling regulations; Promarisco, their own Ecuadorian subsidiary, maintains ASC certification.

- Strategic Focus: Consolidation of Southern European retail market leadership; convenience food segment expansion; supply chain sustainability alignment.

Clearwater Seafoods

Clearwater Seafoods, headquartered in Bedford, Nova Scotia, Canada, is one of North America's largest vertically-integrated wild-caught shellfish companies and a premium supplier of MSC-certified cold-water shrimp to European markets. In January 2021, the company was acquired by a 50/50 partnership between Premium Brands Holdings Corporation and a Mi'kmaq First Nations Coalition.

- Product Portfolio: MSC-certified Canadian coldwater shrimp in shell-on cooked, shell-on raw, and IQF frozen-at-sea formats; also scallops, lobster, clams, snow crab, and turbot.

- Recent Developments: Following the 2021 acquisition, Clearwater continues to operate as a distinct entity under the Clearwater brand; shrimp processing is conducted at St. Anthony Seafoods (St. Anthony, Newfoundland), with harvesting through a long-standing joint venture with Quin-Sea Fisheries.

- Strategic Focus: Premium wild-caught shellfish positioning in European retail and foodservice markets; MSC sustainability leadership; Indigenous economic reconciliation through the Mi'kmaq ownership partnership.

HONEST CATCH

HONEST CATCH, headquartered in Langenpreising (Munich), Bavaria, Germany, is Europe's pioneering direct-to-consumer online seafood retailer and the exclusive sales and distribution arm for shrimp produced by its sister company, Oceanloop. HONEST CATCH distributes primarily to consumers and HoReCa customers in Germany and Austria.

- Product Portfolio: Fresh and flash-frozen Bavarian Shrimp (Penaeus vannamei) in fresh, frozen, ready-to-cook, and easy-peel formats; Bavarian Shrimp soups; GOOD GROUPER (launched 2024 from Kiel facility); curated premium sustainable seafood range from third-party global suppliers.

- Recent Developments: In November 2024, sister company Oceanloop secured a EUR 35 million loan from the European Investment Bank (EIB) to expand the Kiel farm from 5 to 60 tons/year and construct a 2,000-ton capacity land-based shrimp farm in Gran Canaria, Spain.

- Strategic Focus: Scaling sustainable European land-based RAS shrimp farming as a locally produced alternative to imported tropical shrimp; D2C e-commerce growth in Germany and Austria.

Market Concentration Analysis

The European shrimp market exhibits moderate concentration at the processing and distribution level, with the top five suppliers controlling approximately 30–35% of total market volumes in 2025. A significant long tail of regional processors, importers, and specialist distributors, particularly in Spain, France, and the Benelux region, ensures meaningful market fragmentation below the top tier.

The market's supply structure is bifurcated between the consolidated wild-catch sector, dominated by large Nordic seafood companies, and the more fragmented tropical import segment, characterised by numerous importers and processors sourcing from Asian and South American suppliers. Consolidation activity has been moderate, with sustainability compliance costs and EU regulatory requirements driving some smaller importers toward strategic partnerships or exit.

Between 2020 and 2024, several significant supply chain consolidation transactions reshaped the European shrimp processing landscape, including Royal Greenland's strategic acquisitions in the German processing sector and Thai Union's continued expansion of its European private-label customer base. Private equity interest in mid-tier European seafood processors with certified product portfolios and established retail distribution remains elevated.

Investment & Growth Opportunities

Fastest Growing Segments

Farmed eco-certified shrimp (CAGR 2.10%), domestically produced RAS shrimp (high-premium niche), and value-added convenience formats (pre-marinated, ready-to-cook, breaded) represent the three highest-growth investment vectors in the European shrimp market through 2034. Together, these niches address an incremental addressable opportunity of approximately 420 Kilo Tons by 2034.

Emerging Market Expansion

Eastern European markets, including Poland, the Czech Republic, and Romania, represent the most compelling geographic growth opportunity within Europe, as rising disposable incomes and expanding modern retail infrastructure drive seafood category penetration. Supermarket chain expansion by Lidl, Biedronka, and Kaufland across Eastern Europe is a structural enabler for shrimp market development in historically underserved markets.

Venture and Institutional Investment Trends

- Land-based RAS shrimp aquaculture is attracting increasing venture capital and strategic corporate investment in Europe, with projects in the Netherlands, Belgium, and Denmark targeting premium "locally grown" positioning and commanding significant retail price premiums.

- Blockchain and traceability technology enabling full supply chain transparency from harvest to shelf is a growing investment theme aligned with EU supply chain due diligence mandates and major retailer sourcing commitments.

- Private label seafood consolidation remains an active M&A driver, with European retail groups selectively acquiring or partnering with shrimp processors to secure supply chain control, improve private-label seafood margins, and meet sustainability commitments.

Future Market Outlook (2026-2034)

The European shrimp market is positioned for steady, demand-led growth through 2034. From a base of 892.00 Kilo Tons in 2025, the market is projected to reach 1,031.96 Kilo Tons by 2034, representing total incremental volume creation of approximately 140 Kilo Tons over the forecast horizon, at an overall CAGR of 1.55%.

Regulatory evolution, particularly the EU's new Organic Aquaculture Regulation, the revised EU Control Regulation for fisheries, and the Farm-to-Fork Strategy's sustainability targets, will reshape procurement standards across the European shrimp supply chain through 2028. Importers and processors that achieve certified-sustainable, antibiotic-free, and fully traceable supply chain credentials by 2026–2028 are disproportionately positioned to benefit from retail procurement mandates.

Long-term, the market's trajectory is anchored by three structural macro-themes: rising per capita seafood consumption across Europe driven by health awareness; the premiumization of the seafood category, favouring higher-value shrimp products; and the accelerating transition toward responsible sourcing and certified sustainability. European shrimp sits at the intersection of all three, ensuring its continued prominence as a key seafood category through 2034.

Research Methodology

Primary Research

Primary research for this report comprised structured interviews and surveys with over 120 industry participants in 2024–2025, including shrimp importers, processors, retailers, foodservice distributors, aquaculture operators, and seafood trade association representatives across Europe, Asia, and South America.

Secondary Research

Secondary research encompassed a systematic review of European Commission trade statistics, FAO aquaculture production data, company annual reports, trade publications (Seafood Source, Undercurrent News, Intrafish), industry databases (Euromonitor, FAO FishStat), and publicly available import-export trade data. Over 200 secondary sources were reviewed and triangulated.

Forecasting Models

Market volume estimations and growth projections were derived using a combination of top-down and bottom-up forecasting approaches, incorporating EU seafood import statistics, per capita consumption indices, aquaculture production growth rates, and historical market evolution patterns. A base-case CAGR of 1.55% reflects consensus analyst estimates validated against reported seafood trade and consumption data.

Europe Shrimp Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Kilo Tons |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Environments Covered | Farmed, Wild |

| Domestic Production and Imports Covered | Domestic Production, Imports |

| Species Covered | Penaeus Vannamei, Penaeus Monodon, Macrobrachium Rosenbergii, Others |

| Product Categories Covered | Peeled, Shell-on, Cooked, Breaded, Others |

| Distribution Channel Covered | Hypermarkets and Supermarkets, Convenience Stores, Hotels and Restaurants, Online Stores, Others |

| Companies Covered | GRUPO NUEVA PESCANOVA, Clearwater Seafoods, HONEST CATCH, Hendrikson BV, Sykes Seafood, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Europe shrimp market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Europe shrimp market.

- The study maps the leading, as well as the fastest growing, markets in the region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Europe shrimp industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Shrimp Market in Europe Report

The Europe shrimp market reached 892.00 Kilo Tons in 2025 and is projected to reach 1,031.96 Kilo Tons by 2034, growing at a CAGR of 1.55% during 2026-2034.

The Europe shrimp market is expected to grow at a CAGR of 1.55% during the forecast period from 2026 to 2034, supported by sustained demand from retail, foodservice, and convenience food sectors.

Spain leads European shrimp consumption with approximately 22.5% share in 2025, driven by a deep-rooted seafood culture, a vibrant HoReCa sector, and strong retail penetration across both cold-water and tropical shrimp categories.

Wild shrimp dominates with a 58.4% share in 2025 (~521 Kilo Tons), anchored by Arctic cold-water Pandalus borealis harvested from Norwegian, Icelandic, and Greenlandic fisheries.

Imports account for 62.4% of the European shrimp supply (~557 Kilo Tons in 2025). Ecuador, Vietnam, India, and Argentina are the primary source countries, enabled by EU preferential trade agreements and competitive production costs.

Key players include GRUPO NUEVA PESCANOVA, Clearwater Seafoods, HONEST CATCH, Hendrikson BV, and Sykes Seafood.

Key trends include the shift toward sustainability-certified shrimp (MSC, ASC), growth in value-added convenience formats, rising demand for antibiotic-free farmed shrimp, and increasing interest in locally produced European RAS aquaculture shrimp.

Key challenges include supply chain disruptions, stringent EU food safety and environmental regulations, commodity price volatility, disease risks in tropical aquaculture supply nations, and growing traceability compliance requirements.

High-priority investment opportunities include land-based RAS shrimp aquaculture, supply chain traceability technology, eco-certified farmed shrimp sourcing platforms, and value-added convenience shrimp product development — collectively addressing an incremental market opportunity exceeding 420 Kilo Tons by 2034.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade