Europe Smart Grid Security Market Size, Share, Trends and Forecast by Component, Subsystem, Deployment Type, Security Type, and Country, 2026-2034

Europe Smart Grid Security Market Summary:

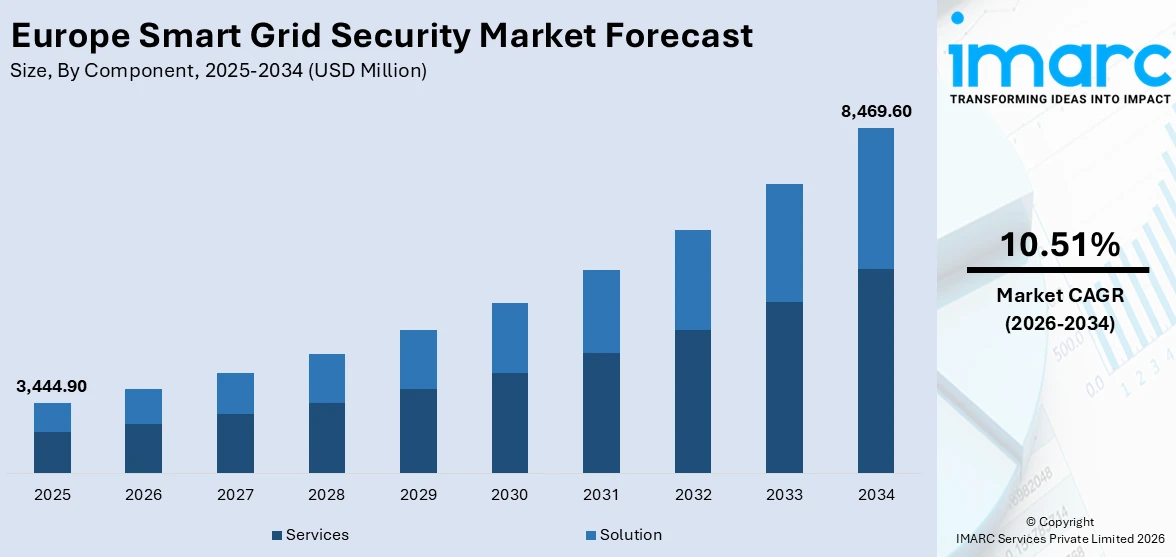

The Europe smart grid security market size was valued at USD 3,444.90 Million in 2025 and is projected to reach USD 8,469.60 Million by 2034, growing at a compound annual growth rate of 10.51% from 2026-2034.

The market is driven by increasing digitalization of energy infrastructure, growing cyber threat sophistication, regulatory mandates for grid modernization, and rising demand for real-time monitoring capabilities. Enhanced data protection requirements, integration of renewable energy sources, and need for operational resilience further accelerate adoption. European utilities prioritize advanced security frameworks to safeguard critical infrastructure investments and maintain consumer trust while ensuring Europe smart grid security market share.

Key Takeaways and Insights:

- By Component: Services dominate the market with a share of 55% in 2025, driven by cybersecurity implementation complexity requiring specialized expertise, ongoing maintenance needs, and regulatory compliance consulting demands across European utilities.

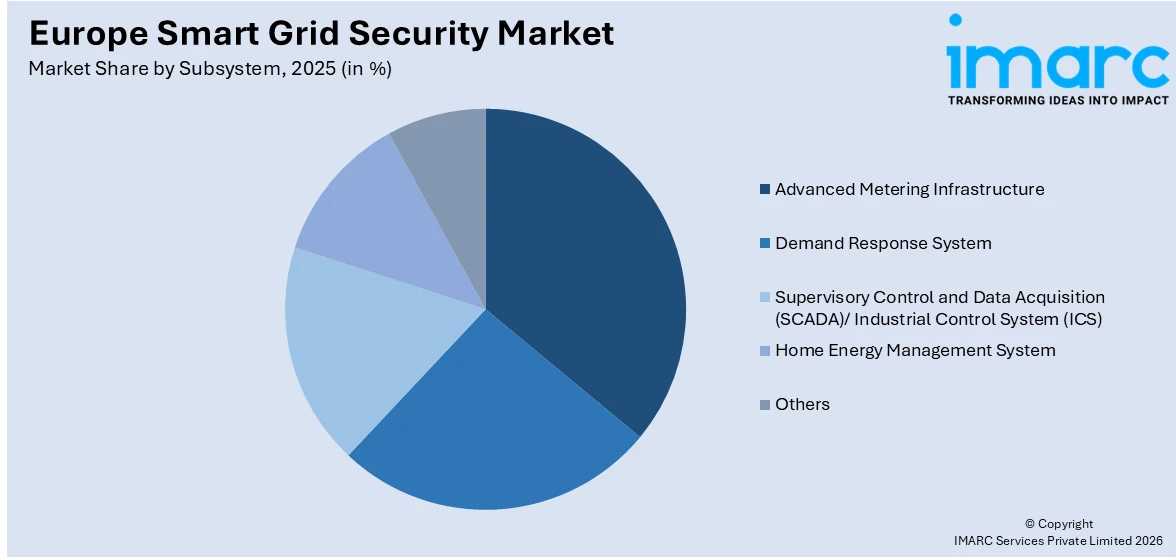

- By Subsystem: Advanced metering infrastructure leads the market with a share of 30% in 2025, owing to widespread smart meter deployments, real-time data collection requirements, and enhanced consumer engagement initiatives driving modernization.

- By Deployment Type: On-premise represents the largest segment with a market share of 62% in 2025, driven by data sovereignty concerns, regulatory compliance requirements, direct infrastructure control preferences, and enhanced security perceptions among operators.

- By Security Type: Network security dominates the market with a share of 38% in 2025, owing to critical importance of protecting communication channels, preventing unauthorized access, and maintaining operational continuity across infrastructure.

- Key Players: The Europe smart grid security market has a highly dynamic competitive landscape, with cybersecurity leaders and energy technology specialists competing with each other over comprehensive security solution sets and emerging threat protection.

To get more information on this market Request Sample

The Europe smart grid security market experiences robust growth driven by accelerating digital transformation across energy infrastructure, where traditional grid systems evolve into intelligent networks requiring sophisticated protection mechanisms. Increasing cyber threat sophistication compels utilities to invest in advanced security architectures that safeguard critical operational technology and information systems from malicious attacks and unauthorized access attempts. As per sources, European Commission advanced implementation of the NIS2 cybersecurity directive to strengthen protection of critical energy infrastructure and digital networks across member states. Regulatory frameworks mandate comprehensive cybersecurity standards, driving compliance-focused investments across European utilities seeking to meet stringent security requirements. Rising integration of renewable energy sources, distributed generation systems, Internet of Things (IoT) devices, and electric vehicle (EV) infrastructure creates complex attack surfaces requiring multi-layered security approaches that ensure operational resilience, grid stability, and consumer confidence while protecting sensitive data and maintaining service reliability across interconnected energy networks.

Europe Smart Grid Security Market Trends:

Enhanced Artificial Intelligence Integration

Artificial intelligence (AI) and machine learning (ML) technologies increasingly power smart grid security solutions, enabling predictive threat detection, automated incident response, and behavioral analytics capabilities. These advanced systems analyze vast data streams from grid sensors, identifying anomalous patterns that indicate potential cybersecurity incidents before they escalate into operational disruptions. As per sources, Europe launched the EU AI GRID at Vilnius TV Tower, establishing the first continental sovereign AI infrastructure network, ensuring GDPR compliance and digital sovereignty for critical AI applications. AI-driven security platforms enhance threat intelligence capabilities, enabling proactive defense mechanisms that adapt to evolving attack methodologies while reducing false positive rates and improving overall security effectiveness.

Zero Trust Architecture Adoption

European utilities increasingly embrace zero trust security frameworks that eliminate implicit trust assumptions across grid infrastructure, requiring continuous verification for every access request regardless of location or user credentials. This architectural approach implements granular access controls, continuous monitoring, and dynamic policy enforcement across operational technology and information technology environments. In 2026, Siemens partnered with Enemalta plc to digitalize Malta’s electricity grid, deploying OT Companion for real-time OT monitoring, vulnerability management, and enhanced cybersecurity—demonstrating practical zero trust-aligned measures across operational technology networks. Zero trust models enhance security posture by reducing attack surfaces, minimizing lateral movement opportunities, and ensuring comprehensive visibility across interconnected grid systems and communication networks.

Edge Computing Security Evolution

Edge computing proliferation across smart grid infrastructure drives demand for specialized security solutions that protect distributed processing capabilities at grid endpoints, substations, and generation facilities. These localized computing environments require tailored security architectures that address unique vulnerabilities while maintaining real-time operational requirements. According to reports, the EU‑backed Eider project in Spain’s Basque Country deployed edge computing architectures for medium‑ and low‑voltage grids, integrating real‑time data processing and cybersecurity measures at distributed grid nodes. Enhanced edge security frameworks incorporate hardware-based root of trust, secure boot processes, and encrypted communication protocols that ensure data integrity and system authenticity across geographically dispersed grid infrastructure components.

Market Outlook 2026-2034:

The Europe smart grid security market demonstrates promising growth trajectory through the forecast period, supported by accelerating grid modernization initiatives, evolving cybersecurity threat landscapes, and strengthening regulatory requirements across European markets. Technological advancement in artificial intelligence, quantum-resistant encryption, and autonomous threat response capabilities will drive solution sophistication and market expansion. Revenue growth reflects increasing utility investments in comprehensive security architectures that address operational technology vulnerabilities while ensuring compliance with emerging cybersecurity directives and maintaining consumer trust in digital energy infrastructure. The market generated a revenue of USD 3,444.90 Million in 2025 and is projected to reach a revenue of USD 8,469.60 Million by 2034, growing at a compound annual growth rate of 10.51% from 2026-2034.

Europe Smart Grid Security Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Component |

Services |

55% |

|

Subsystem |

Advanced Metering Infrastructure |

30% |

|

Deployment Type |

On-premise |

62% |

|

Security Type |

Network Security |

38% |

Component Insights:

- Solution

- Encryption

- Antivirus and Antimalware

- Identity and Access Management (IAM)

- Firewall

- Others

- Services

- Managed Services

- Professional Services

- Others

Services dominate with a market share of 55% of the total Europe smart grid security market in 2025.

Services dominate the market through comprehensive cybersecurity consulting, implementation support, and ongoing maintenance requirements across European smart grid deployments. Professional services encompass threat assessment, security architecture design, compliance consulting, and incident response capabilities that address complex utility-specific requirements. In September 2025, Atos secured a €326 million European Commission contract to provide technical cybersecurity services, including incident response, threat monitoring, and vulnerability management across EU institutions. Managed security services gain prominence as utilities seek specialized expertise to monitor, detect, and respond to sophisticated cyber threats while maintaining focus on core energy operations and infrastructure management responsibilities.

Services growth reflects increasing complexity of cybersecurity implementation across diverse grid architectures, requiring specialized knowledge of both operational technology and information technology environments. European utilities prioritize professional services partnerships that provide continuous threat intelligence, vulnerability management, and regulatory compliance support. The segment benefits from Europe’s ongoing digital transformation initiatives, requiring expert guidance to securely integrate emerging technologies, maintain operational resilience, and ensure regulatory compliance across utility networks, including distributed grids and edge-enabled energy infrastructure.

Subsystem Insights:

Access the comprehensive market breakdown Request Sample

- Demand Response System

- Supervisory Control and Data Acquisition (SCADA)/ Industrial Control System (ICS)

- Home Energy Management System

- Advanced Metering Infrastructure

- Others

Advanced metering infrastructure leads with a share of 30% of the total Europe smart grid security market in 2025.

Advanced metering infrastructure represents the leading subsystem category, driven by extensive smart meter deployments across European markets and associated cybersecurity requirements for protecting consumer data and grid communications. These intelligent measurement systems create multiple entry points that require robust authentication, encryption, and access control mechanisms to prevent unauthorized access and data manipulation. Security solutions address communication protocol vulnerabilities, device authentication challenges, and data privacy requirements while ensuring operational reliability and consumer trust.

The subsystem’s prominence highlights the extensive modernization of European electricity distribution networks, where conventional meters are being replaced with intelligent devices that enable two-way communication and real-time data exchange. Advanced metering infrastructure (AMI) security integrates device-level safeguards, communication network protections, and robust data management system controls to counter evolving cyber threats. These measures not only ensure operational resilience but also enhance grid visibility, facilitate consumer engagement, and support smart grid initiatives across a variety of European utility environments.

Deployment Type Insights:

- Cloud-based

- On-premise

On-premise exhibits a clear dominance with a 62% share of the total Europe smart grid security market in 2025.

On-premise dominates European smart grid security implementations, reflecting strong preferences for direct infrastructure control, data sovereignty compliance, and enhanced security perceptions among utility operators. These locally hosted security architectures provide utilities with complete oversight of cybersecurity systems, enabling customized configurations that address specific operational requirements and regulatory mandates. According to reports, Portugal strengthened national cybersecurity by transposing the EU NIS2 Directive into law, mandating advanced technical measures, continuous monitoring, and executive accountability across critical infrastructure sectors.

European utilities favor on-premise deployments due to stringent data protection regulations, critical infrastructure security requirements, and operational technology integration needs that benefit from local control and management capabilities. These solutions provide utilities with flexibility to implement customized security policies, maintain air-gapped environments where necessary, and ensure compliance with evolving regulatory frameworks. On-premise architectures support integration with existing utility systems while providing enhanced visibility and control over cybersecurity operations across grid infrastructure.

Security Type Insights:

- Endpoint Security

- Application Security

- Database Security

- Network Security

- Others

Network security leads with a market share of 38% of the total Europe smart grid security market in 2025.

Network security represents the largest security type segment, addressing the critical importance of protecting communication channels, preventing unauthorized access, and maintaining operational continuity across interconnected grid infrastructure. These solutions encompass firewalls, intrusion detection systems, secure communication protocols, and network segmentation technologies that safeguard data transmission between grid components. In November 2025, Slovenia’s transmission system operator ELES joined the European Network for Cyber Security, gaining shared threat intelligence and expertise to enhance network security and protect high‑voltage grid communications.

The segment's prominence reflects the foundational role of secure communications in smart grid operations, where reliable and protected data exchange enables real-time monitoring, control, and optimization capabilities. Network security solutions address evolving threats targeting communication protocols, wireless networks, and interconnected systems that support grid modernization initiatives. European utilities prioritize network security investments that protect against sophisticated attack vectors while enabling secure integration of renewable energy sources, distributed generation systems, and advanced grid management technologies.

Country Insights:

- Germany

- France

- United Kingdom

- Italy

- Spain

- Others

Germany maintains Europe smart grid security adoption through extensive industrial automation expertise, robust cybersecurity frameworks, and comprehensive energy transition initiatives driving grid modernization investments. Strong regulatory compliance culture, advanced manufacturing capabilities, and emphasis on operational technology protection accelerate security solution deployments. German utilities prioritize sophisticated threat detection systems, network segmentation technologies, and industrial control system security.

France demonstrates significant smart grid security growth through centralized energy infrastructure modernization, nuclear sector cybersecurity expertise, and government-backed digitalization programs supporting utility transformation initiatives. Strong emphasis on national security considerations, critical infrastructure protection mandates, and advanced threat intelligence capabilities drive comprehensive security architecture investments across French electricity distribution networks and transmission systems.

United Kingdom shows robust smart grid security development through regulatory innovation, competitive energy market dynamics, and post-Brexit cybersecurity sovereignty initiatives driving domestic technology adoption. British utilities emphasize network resilience, consumer data protection, and operational continuity solutions that address evolving threat landscapes while supporting renewable energy integration and distributed generation security requirements.

Italy exhibits growing smart grid security investments through infrastructure modernization programs, renewable energy integration initiatives, and enhanced cybersecurity awareness following critical infrastructure incidents. Italian utilities focus on legacy system protection, communication network security, and regulatory compliance solutions that address operational technology vulnerabilities while supporting sustainable energy transition and grid resilience objectives.

Spain demonstrates expanding smart grid security adoption through renewable energy leadership, smart city initiatives, and comprehensive digitalization strategies supporting grid transformation across diverse regional markets. Spanish utilities prioritize distributed generation security, advanced metering protection, and cross-border energy trading cybersecurity solutions that enable secure integration of solar and wind resources.

Other European markets including Netherlands, Belgium, Austria, and Nordic countries show increasing smart grid security investments through regional cooperation initiatives, technology innovation programs, and harmonized cybersecurity standards supporting continental grid integration. These markets emphasize interoperability, cross-border security protocols, and emerging technology protection solutions addressing diverse regulatory and operational requirements.

Market Dynamics:

Growth Drivers:

Why is the Europe Smart Grid Security Market Growing?

Energy Transition and Renewable Integration

Accelerating transition toward renewable energy sources across European markets drives substantial smart grid security investments as utilities integrate distributed generation systems, energy storage facilities, and bidirectional energy flows requiring sophisticated protection mechanisms. Renewable integration creates complex operational environments where traditional security approaches prove insufficient for protecting dynamic grid configurations, variable generation patterns, and decentralized energy resources. As per sources, the European Investment Bank agreed on a €120 million loan with Iberdrola to support renewable energy generation, power grid digitalization, and enhanced cybersecurity resilience in Spain’s electricity infrastructure. Enhanced security architecture has become essential for managing renewable energy volatility, ensuring grid stability, and protecting against cyber threats targeting distributed energy infrastructure components.

Cross-Border Energy Trading Expansion

The increasing interconnectivity among European electricity markets through the facilitation of cross-border energy trading platforms requires the development and implementation of effective cybersecurity systems that guarantee the security of international energy transactions and data exchanges between and among European countries. Utilities are investing heavily in the development and implementation of cutting-edge security systems that guarantee safe participation in the European energy market, while at the same time protecting commercial information and maintaining sovereignty over the grid operations.

Industrial IoT and Sensor Proliferation

Massive deployment of Internet of Things (IoT) devices, smart sensors, and monitoring equipment across European grid infrastructure drives demand for comprehensive security solutions that protect countless connected endpoints from cyber threats and unauthorized access attempts. Industrial IoT proliferation creates exponentially expanded attack surfaces where traditional perimeter security approaches become inadequate for protecting distributed sensor networks, automated control systems, and real-time monitoring capabilities. In October 2025, E.ON SE partnered with Nokia to modernize telecommunications infrastructure for distribution system operators in Germany, enhancing secure communications and resilience across connected grid endpoints. Utilities require scalable security architectures that provide device-level protection, secure authentication, and encrypted communications across thousands of connected grid components and operational technology endpoints.

Market Restraints:

What Challenges the Europe Smart Grid Security Market is Facing?

High Implementation Costs

Comprehensive smart grid security implementations require substantial capital investments encompassing software licensing, hardware infrastructure, professional services, and ongoing maintenance expenses that strain utility budgets already facing infrastructure modernization pressures. Cost considerations include integration complexity, training requirements, and potential operational disruptions during deployment phases that impact financial planning and project timelines across European utilities.

Legacy System Integration Complexity

Existing grid infrastructure relies heavily on legacy operational technology systems that lack modern cybersecurity capabilities, creating integration challenges when implementing contemporary security solutions across hybrid environments. Compatibility issues, communication protocol limitations, and operational reliability concern complicate security modernization efforts while requiring specialized expertise and extensive testing procedures that extend implementation timelines.

Skills Shortage and Expertise Gap

Limited availability of qualified cybersecurity professionals with specialized smart grid knowledge constrains market growth as utilities struggle to recruit, train, and retain personnel capable of managing sophisticated security architectures. Expertise requirements span operational technology, information technology, and energy sector knowledge domains that demand rare skill combinations difficult to source across European labor markets.

Competitive Landscape:

The Europe smart grid security market features diverse competitive dynamics encompassing established cybersecurity vendors, specialized energy technology providers, and emerging startups focused on operational technology protection. Market participants compete through comprehensive solution portfolios, vertical expertise, regulatory compliance capabilities, and strategic partnerships with utility organizations. Competition intensifies around artificial intelligence integration, threat intelligence capabilities, and managed security service offerings that address complex utility requirements. Vendor differentiation emerges through industry-specific knowledge, proven deployment experience, and ability to address evolving threat landscapes while maintaining operational reliability across diverse European utility environments and regulatory frameworks.

Recent Developments:

- In November 2025, TECNALIA presented its latest smart grid technologies at ENLIT EUROPE in Bilbao, showcasing cybersecurity solutions, digitalisation tools, energy storage systems, and automated inspection technologies to support European utilities in enhancing grid flexibility, operational efficiency, and secure integration of distributed energy resources.

Europe Smart Grid Security Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Components Covered |

|

| Subsystems Covered | Demand Response System, Supervisory Control and Data Acquisition (SCADA)/ Industrial Control System (ICS), Home Energy Management System, Advanced Metering Infrastructure, Others |

| Deployment Types Covered | Cloud-based, On-premise |

| Security Types Covered | Endpoint Security, Application Security, Database Security, Network Security, Others |

| Countries Covered | Germany, France, United Kingdom, Italy, Spain, Others |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Europe Smart Grid Security Market Research Report Report

The Europe smart grid security market size was valued at USD 3,444.90 Million in 2025.

The Europe smart grid security market is expected to grow at a compound annual growth rate of 10.51% from 2026-2034 to reach USD 8,469.60 Million by 2034.

Services held the largest Europe smart grid security market share, driven by comprehensive cybersecurity consulting, implementation support, ongoing maintenance requirements, and specialized expertise demands across European smart grid deployments and regulatory compliance initiatives.

Key factors driving the Europe smart grid security market include regulatory compliance mandates, critical infrastructure protection requirements, digital transformation acceleration, and increasing cyber threat sophistication across European energy infrastructure modernization initiatives.

Major challenges include high implementation costs, legacy system integration complexity, skills shortage and expertise gaps, regulatory compliance burdens, operational technology vulnerabilities, and evolving cyber threat landscapes requiring continuous security architecture adaptation and investment.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)