Europe Wine Market Size, Share, Trends and Forecast by Product Type, Color, Distribution Channel, and Region, 2026-2034

Europe Wine Market Size, Share, Trends & Forecast (2026-2034)

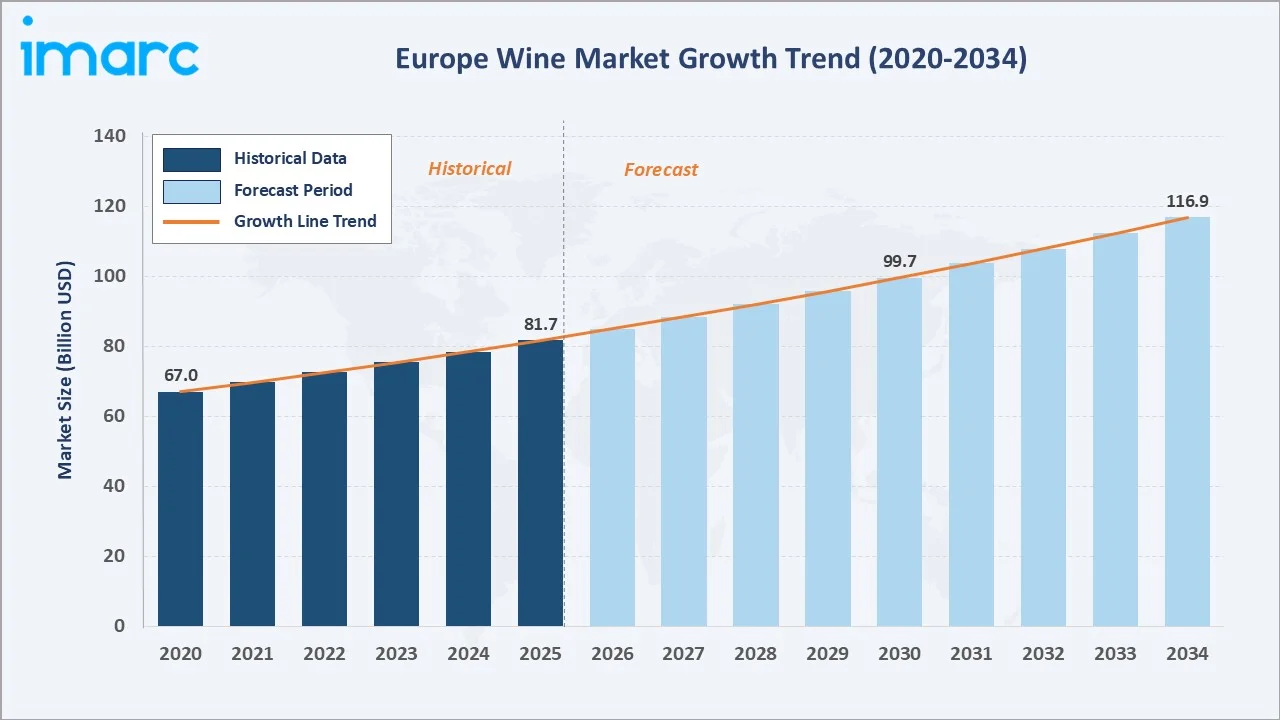

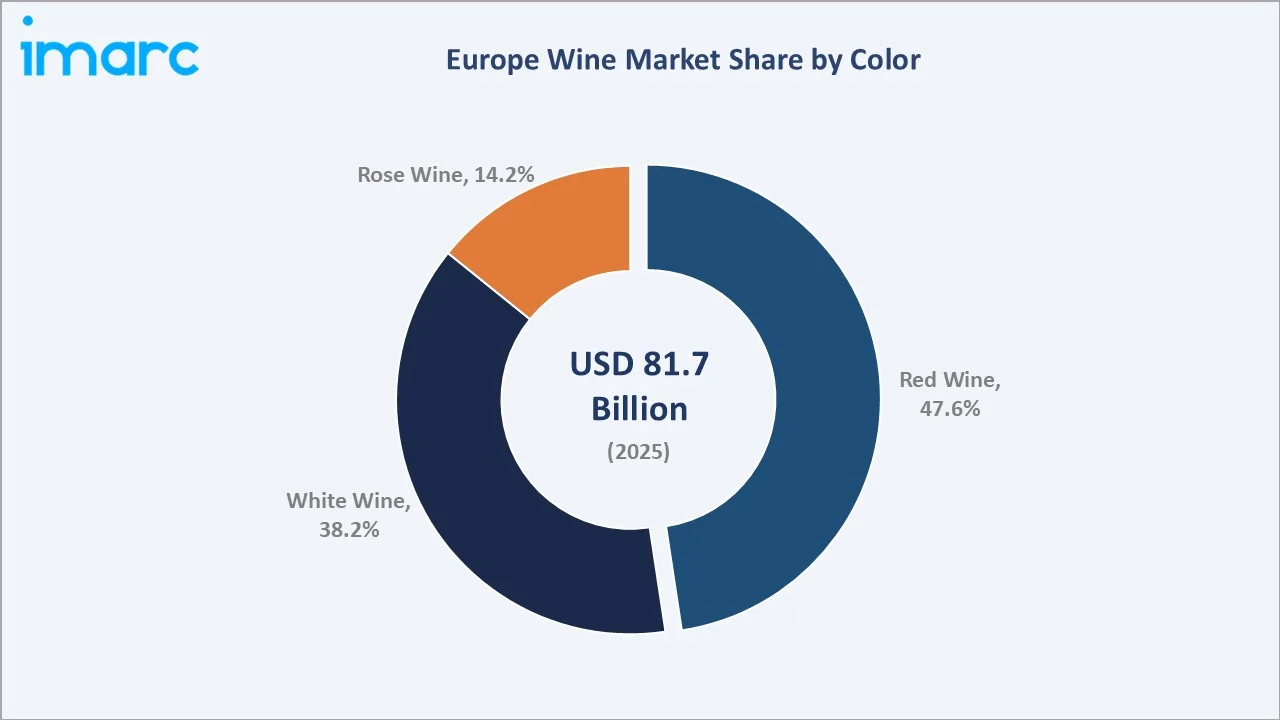

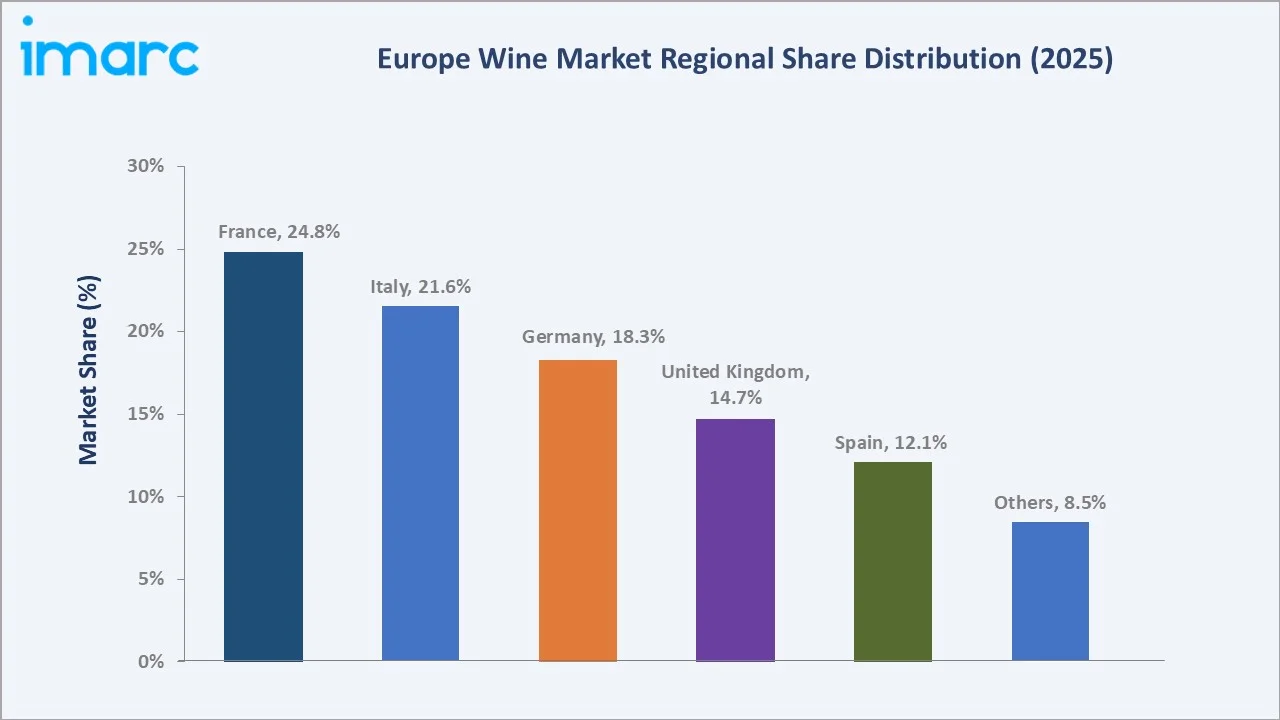

The Europe wine market reached USD 81.7 Billion in 2025 and is projected to reach USD 116.9 Billion by 2034, growing at a CAGR of 4.06% during 2026-2034. The market is driven by strong cultural consumption, premiumization, tourism-linked demand, and the region’s established wine-producing heritage. Growth is also supported by rising demand for organic, sustainable, and low-alcohol wine varieties. The European Union remains the leading wine producer, with an average annual production of 157 million hectolitres between 2020 and 2025. This strong production base supports Europe’s wine market by ensuring wide availability, export strength, product variety, and continued investment in vineyards, wineries, and premium wine categories. Still wine dominates at 68.4%. Red wine leads color at 47.6%. France commands 24.8% of the European market.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 81.7 Billion |

|

Forecast Market Size (2034) |

USD 116.9 Billion |

|

CAGR (2026-2034) |

4.06% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Product Type |

Still Wine (68.4%, 2025) |

|

Dominant Color |

Red Wine (47.6%, 2025) |

|

Leading Country |

France (24.8%, 2025) |

The Europe wine market expanded from USD 67.0 Billion in 2020 to USD 81.7 Billion in 2025, anchored at USD 99.7 Billion in 2030, and forecast to reach USD 116.9 Billion by 2034. The COVID-19 pandemic shifted European wine consumption from on-trade to off-trade, with e-commerce wine sales. The post-COVID on-trade recovery, combined with sustained off-trade volumes, created the highest simultaneous on-trade and off-trade wine demand in European market history.

To get more information on this market, Request Sample

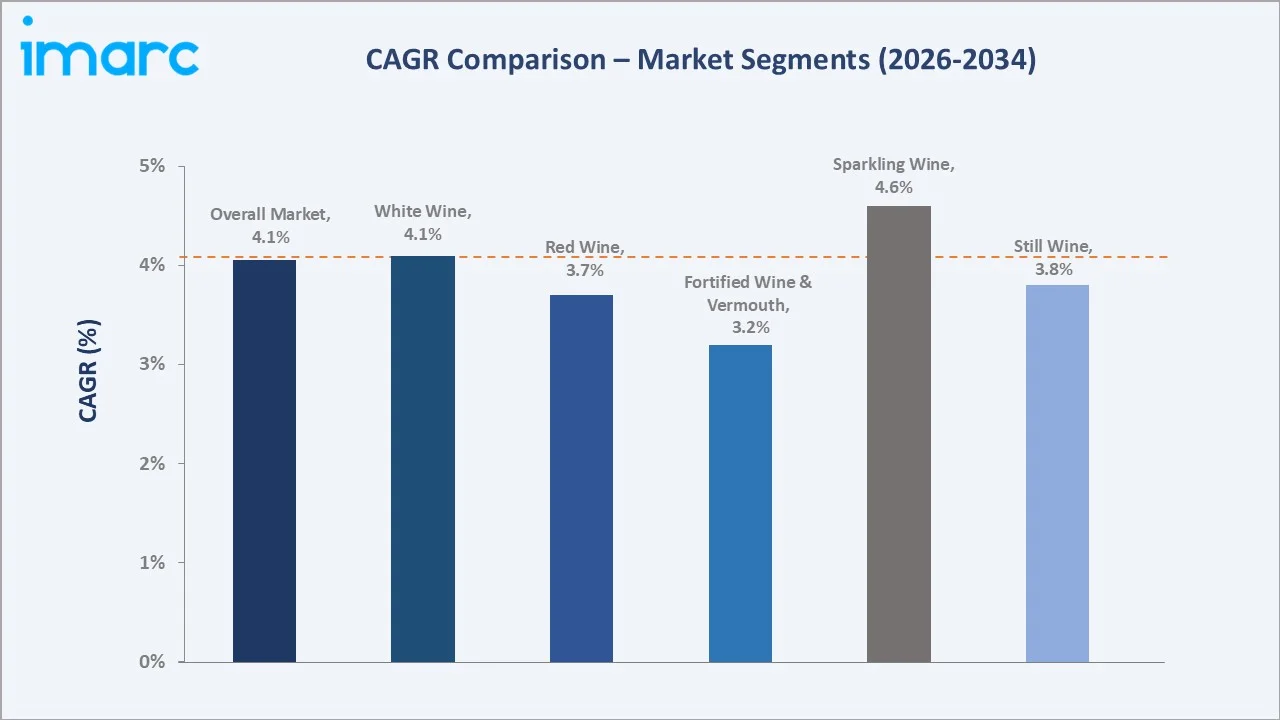

Sparkling wine grows fastest at ~4.6% CAGR through high penetration, Champagne's continued luxury premiumization, accessibility positioning, and English sparkling wine's emerging premium credibility. White wine at ~4.1% CAGR due to mass market reach and growing premium positioning.

Executive Summary

The Europe wine market reached USD 81.7 Billion in 2025, representing one of the largest wine markets by both production value and consumption expenditure. Europe encompasses the world's most prestigious wine designations. The market is projected to reach USD 116.9 Billion by 2034.

Still wine at 68.4% dominates through the breadth of European still wine from entry-level through the complete fine wine hierarchy. Red wine at 47.6% leads color classification through the dominance in both fine wine and everyday drinking occasions. France, at 24.8%, leads by market value through Champagne and luxury pricing concentration.

Key Market Insights

|

Insight |

Data |

|

Dominant Product Type |

Still Wine - 68.4% share (2025) |

|

Dominant Color |

Red Wine - 47.6% market share (2025) |

|

Leading Country |

France - 24.8% market share |

|

Market Opportunity |

Low/no-alcohol wine; organic and biodynamic certified wines; Asian export premium growth; e-commerce; wine tourism; sustainable packaging |

Key Analytical Observations Supporting the Above Data:

- Still Wine at 68.4%: Still wine dominates due to its deep cultural relevance, strong everyday consumption, and wide availability across red, white, and rosé varieties. Its broad use in dining, retail, hospitality, and exports keeps demand consistently higher than sparkling or fortified wine segments.

- Red Wine at 47.6%: Red wine dominates due to its strong association with traditional European dining, especially in major wine-consuming countries such as France, Italy, and Spain. Its wide availability, premium positioning, aging potential, and pairing with regional cuisines sustain strong consumer preference across retail and hospitality channels.

- France at 24.8%: France dominates due to its strong wine heritage, premium vineyard regions, and reputation for high-quality wines. Strong domestic consumption, exports, wine tourism, and established appellation systems further support its leading market position.

Europe Wine Market Overview

The European wine market encompasses production, trade, and consumption across the full range of wine categories. The European wine market operates within the wine sector regulations. The European wine ecosystem integrates vineyards across Europe, individual wine producers ranging from single-hectare artisan vignerons to industrial cooperative wineries, regional wine trade organizations, national wine institutes, and global wine trade organizations. Macroeconomic factors include stable disposable incomes, strong tourism activity, hospitality sector growth, and export-oriented wine trade.

Market Dynamics

To evaluate market opportunities, Request Sample

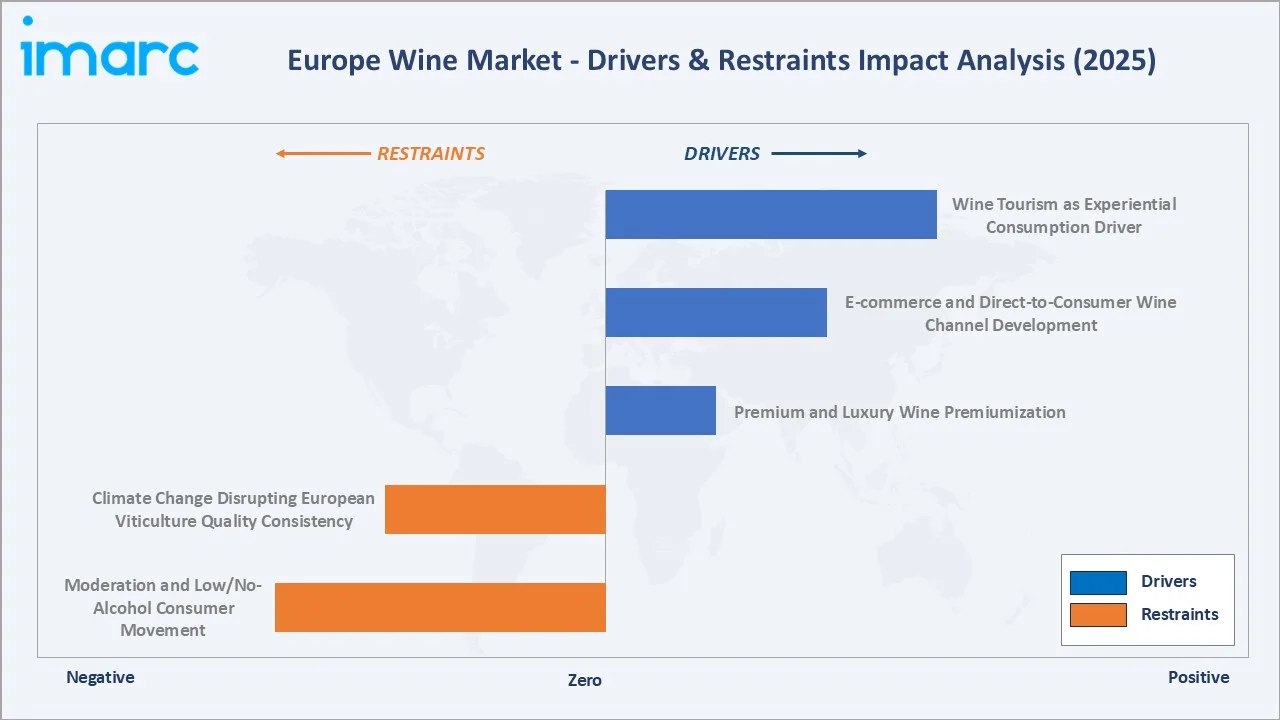

Market Drivers

- Premium and Luxury Wine Premiumization: Premium and luxury wine premiumization demand is boosting as consumers increasingly prefer high-quality, heritage-led and origin-certified wines. Demand for aged wines, limited editions, organic labels and wines from renowned regions supports higher-value sales. Premiumization also benefits wineries by improving margins and encouraging investment in branding, packaging and wine tourism. This trend is especially strong across gifting, fine dining and export-oriented channels.

- E-commerce and Direct-to-Consumer Wine Channel Development: E-commerce and direct-to-consumer wine channels are making wine discovery, comparison and purchasing more convenient for consumers. Online platforms help wineries reach customers beyond traditional retail and hospitality channels. D2C models also allow producers to build stronger customer relationships, offer subscriptions, curated boxes and exclusive labels. This supports premium wine sales and improves brand visibility across regional and international markets.

- Wine Tourism as Experiential Consumption Driver: France, Italy and Spain lead Europe’s wine tourism market, followed by Portugal and Greece. Germany, Hungary, Romania, Austria and Bulgaria are also gaining recognition as emerging wine tourism destinations. This rising European wine tourism is turning wine consumption into an experiential activity linked to vineyard visits, tastings, festivals and regional food culture. It helps wineries build direct relationships with consumers and promote premium, local and heritage wines.

Market Restraints

- Climate Change Disrupting European Viticulture Quality Consistency: Climate change is affecting grape quality, harvest timing, and yield consistency across key wine-producing regions. Rising temperatures, droughts, heatwaves and extreme weather events can alter grape composition and impact traditional wine profiles. Producers may face higher costs for irrigation, vineyard adaptation and climate-resilient cultivation practices. These challenges create uncertainty in production quality and long-term viticulture sustainability.

- Moderation and Low/No-Alcohol Consumer Movement: The moderation and low/no-alcohol movement is limiting Europe’s wine market as younger consumers increasingly reduce drinking frequency or shift toward lighter alternatives. Health awareness, wellness lifestyles and changing social habits are weakening traditional wine consumption occasions. This trend can affect volume sales, especially in everyday still wine categories. Producers may need to adapt through low-alcohol wines, smaller formats and lifestyle-focused branding.

Market Opportunities

- Low and No-Alcohol Wine Category Development: Low and no-alcohol wine category development offers an opportunity by addressing the growing health-conscious and moderation-focused consumer base. These products allow wineries to retain younger consumers who are reducing alcohol intake without leaving the wine category. Innovation in taste, aroma preservation and premium positioning can help improve acceptance. This creates new growth potential across retail, e-commerce and hospitality channels.

- Organic and Biodynamic Wine Mainstream Adoption: Organic and biodynamic wine adoption is creating an opportunity as consumers increasingly prefer natural, sustainable and environmentally responsible products. These wines support premium positioning and help producers differentiate through certified, terroir-focused offerings. Growing demand from health-conscious and eco-aware consumers strengthens retail, hospitality and export potential. This trend also encourages wineries to invest in sustainable vineyard practices and cleaner production methods.

Market Challenges

- Fine Wine Market Cycles Creating Revenue Volatility: Fine wine market cycles create fluctuations in demand, pricing and investment activity. Premium and collectible wines are often influenced by economic confidence, luxury spending and investor sentiment. During weaker market cycles, buyers may delay purchases or shift toward lower-priced wines. This can reduce revenue predictability for producers, distributors and merchants focused on high-end wine segments.

- Counterfeit Fine Wine Market Creating Consumer Trust and Provenance Challenges: Counterfeit fine wine is weakening consumer confidence in premium and collectible bottles. Fake labels, refilled bottles and unclear provenance can make buyers cautious, especially in secondary and auction markets. This increases the need for authentication, traceability and secure supply chains. For producers and merchants, counterfeit risks can damage brand reputation and reduce trust in high-value wine transactions.

Emerging Market Trends

1. Natural Wine Movement Reshaping Consumer Expectations and European Wine Culture

The natural wine movement is increasing demand for minimal-intervention, artisanal and terroir-driven wines. Consumers are showing greater interest in authenticity, transparency, organic farming and unique flavor profiles. This trend is influencing wine bars, restaurants and specialty retailers to expand natural wine selections. It is also encouraging producers to experiment with traditional methods, lower additives and more sustainable vineyard practices.

2. Climate Change Enabling English Sparkling Wine and New European Wine Regions

Climate change is enabling new wine-producing areas, including English sparkling wine regions and emerging viticulture zones across parts of Northern and Central Europe. Warmer temperatures and longer growing seasons are improving grape cultivation conditions in areas previously considered unsuitable for winemaking. This is diversifying Europe’s wine landscape and encouraging investment in new vineyards and production regions. The trend is also creating opportunities for innovative wine styles and regional differentiation.

3. Growth of Wine Subscriptions and Personalized Wine Discovery Platforms

Wine subscriptions and personalized discovery platforms are emerging as consumers seek convenient, curated and experience-led wine purchasing. These platforms use preferences, tasting profiles and purchase history to recommend wines suited to individual tastes. They help smaller wineries reach new consumers while supporting repeat purchases and brand loyalty. This trend is strengthening D2C sales and making wine discovery more engaging for younger digital consumers.

4. Low-Carbon Packaging Solutions Transforming European Wine Branding

Low-carbon packaging solutions are transforming European wine branding as producers use lightweight bottles, recycled materials, cans, bag-in-box and paper-based formats to reduce environmental impact. These formats help wineries communicate sustainability, modernity and convenience to eco-conscious consumers. Packaging innovation also lowers transport emissions and supports differentiation on retail shelves. In April 2026, Puklavec Family Wines partnered with Vaider and JRE-Jeunes Restaurateurs to launch Trois Femmes wine, combining its long winemaking heritage with modern, lower-carbon packaging. The project uses Vaider’s carbon-neutral wine bottle, helping lower the product’s overall environmental footprint.

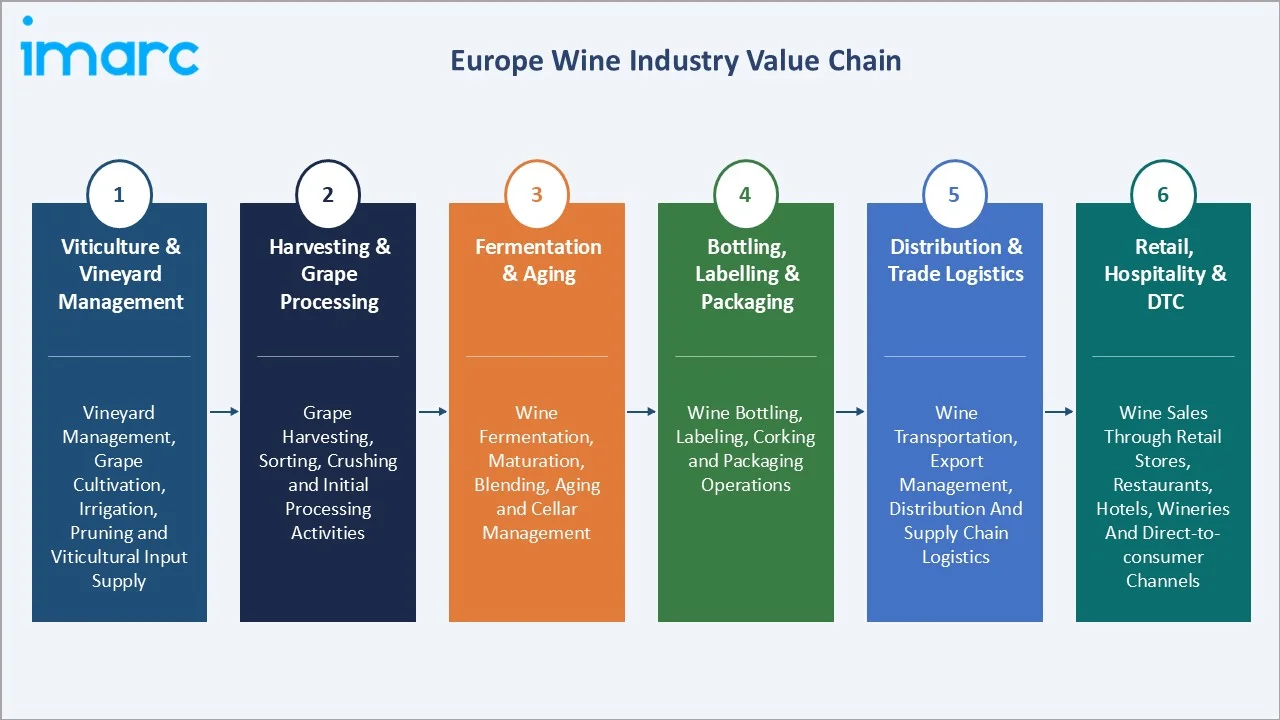

Industry Value Chain Analysis

The European wine value chain integrates viticulture and vineyard management, harvesting and grape processing, fermentation and aging, bottling and packaging, distribution and trade logistics, and retail and hospitality sales.

|

Stage |

Key Participants |

|

Viticulture & Vineyard Management |

Vineyard management, grape cultivation, irrigation, pruning and viticultural input supply |

|

Harvesting & Grape Processing |

Grape harvesting, sorting, crushing and initial processing activities |

|

Fermentation & Aging |

Wine fermentation, maturation, blending, aging and cellar management |

|

Bottling, Labelling & Packaging |

Wine bottling, labeling, corking and packaging operations |

|

Distribution & Trade Logistics |

Wine transportation, export management, distribution and supply chain logistics |

|

Retail, Hospitality & DTC |

Wine sales through retail stores, restaurants, hotels, wineries and direct-to-consumer channels |

The distribution stage is particularly complex in European wine through the three-tier system operating across most European markets' regulated wholesaler framework. The emergence of DTC as a disintermediating channel is progressively challenging the three-tier distribution model's margin capture, with each developing brand-controlled DTC channels alongside traditional distribution.

Technology Landscape in the Europe Wine Industry

Precision Viticulture and Smart Vineyard Technology

Precision viticulture and smart vineyard technology enable data-driven vineyard management and improved crop monitoring. Technologies such as sensors, drones, satellite imaging, IoT devices and AI analytics help optimize irrigation, disease detection and harvest planning. These tools improve grape quality, resource efficiency and climate resilience. As sustainability and productivity become priorities, smart viticulture is modernizing traditional winemaking practices across Europe.

Wine E-commerce and Digital Distribution Technology

Wine e-commerce and digital distribution technology improve online discovery, purchasing and direct consumer engagement. Digital platforms, AI-based recommendations, subscription models and mobile applications help wineries reach broader audiences beyond traditional retail channels. These technologies also enhance inventory management, customer analytics and personalized marketing. As digital wine sales grow, producers are strengthening omnichannel strategies and direct-to-consumer distribution models.

Dealcoholization and Low-Alcohol Wine Technology

Dealcoholization and low-alcohol wine technology enable producers to develop reduced-alcohol alternatives while preserving taste, aroma and wine characteristics. Technologies such as vacuum distillation, membrane filtration and spinning cone systems help remove alcohol with minimal impact on quality. In October 2025, a new dealcoholization facility by Solos opened in Valencia, Spain, giving premium wine producers in Southern Europe access to advanced technology for no- and low-alcohol wine production. The plant will help wineries reduce alcohol content while preserving flavor quality and premium brand positioning. These innovations support the growing moderation and wellness trend among consumers. As demand rises, wineries are investing more in low- and no-alcohol product development and production capabilities.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product Type |

Still Wine |

68.4% |

2025 |

|

Color |

Red Wine |

47.6% |

2025 |

|

Distribution Channel |

🔒 |

🔒 |

2025 |

|

Country |

France |

24.8% |

2025 |

By Product Type

Still wine leads at 68.4% (2025). The still wine category's commercial architecture spans from everyday table wine through regional PDO wines, through premium appellations, to the fine wine tier. Still wine's broad price ladder sustains consistent consumer trading along the premiumization curve from one price tier to the next.

To access detailed market analysis, Request Sample

Sparkling wine at 21.7% growing at ~4.6% CAGR is the market's most commercially dynamic segment. Fortified wine and vermouth at 9.9% encompasses port and sherry as heritage categories alongside Vermouth's cocktail culture revival, sustaining above-wine-average growth in the vermouth sub-segment.

By Color

Red wine leads at 47.6% (2025). Red wine's market leadership reflects its dominance in European food culture and its concentration in the fine wine investment market.

White wine at 38.2% is growing fastest at ~4.1% CAGR through its dominance, mass market accessibility, and emerging premium whites. Rose wine at 14.2% is sustained by Provence Rose's lifestyle positioning.

Regional Market Insights

|

Country |

Share (2025) |

Key Wine Market Drivers & Characteristics |

|

France |

24.8% |

Driven by strong wine heritage, premium appellations, global exports and an established wine tourism ecosystem. |

|

Italy |

21.6% |

Supported by large-scale wine production, diverse wine regions, strong domestic consumption and export-oriented wineries. |

|

Germany |

18.3% |

Benefits from growing demand for premium, organic and low-alcohol wines, supported by strong retail and wine import activity. |

|

United Kingdom |

14.7% |

Driven by high wine consumption, premiumization trends, expanding sparkling wine production and strong off-trade channels. |

|

Spain |

12.1% |

Supported by extensive vineyard areas, wine exports, tourism-driven consumption and growing premium wine demand. |

|

Others |

8.5% |

Other European countries contribute through emerging wine regions, specialty wines, wine tourism and niche premium offerings. |

France's commercial leadership is reinforced by Champagne's exceptional premium pricing concentration. Italy's volume production leadership, combined with annual bottle production and prestige, creates the most commercially diverse European wine value creation model. Germany's dual role as consumer and producer creates a distinct market structure where domestic prestige coexists with industrial history.

The UK's fine wine trading infrastructure sustains its market share above domestic production, making London uniquely the world's fine wine commercial capital despite minimal wine production. Spain's growing premium wine recognition sustains Spain's above-GDP wine market value growth. Others represent Europe's most commercially dynamic emerging premium wine value creation opportunities.

Competitive Landscape

The European wine market's competitive landscape is highly fragmented at the production tier but increasingly concentrated at the premium and luxury tier, where Champagne and fine wine estate portfolios command a disproportionate share of fine wine consumer spending through the brand architecture.

|

Company Name |

Key Brands |

Market Position |

Core Strength |

|

LVMH |

Moët & Chandon, Dom Pérignon, Veuve Clicquot, Krug, Ruinart, Château d'Yquem, Chandon, Cloudy Bay |

Market Leader |

LVMH is a dominant force in the European wine industry, focusing on ultra-premium, historic Maisons. |

|

Pernod Ricard |

G.H. MUMM, Perrier-Jouet |

Strong Challenger |

Pernod Ricard is a major player in the European wine and spirits market, acting as one of the largest producers, boasting a comprehensive portfolio of premium brands. |

|

E. & J. Gallo Winery |

BAREFOOT, ALAMOS, ANDRE, BLACK BOX, DARK HORSE |

Market Leader |

E. & J. Gallo Winery serves as a massive importer and distributor in Europe, bridging California wines with European consumers while also acting as an importer of premium European wines into the US. |

|

Constellation Brands, Inc. |

Kim Crawford, Mount Veeder Winery |

Strong Challenger |

Constellation Brands acts as a major international producer and premium marketer with key strategic footprints in Europe, specifically focusing on high-end, iconic Italian wines. |

|

Treasury Wine Estates Ltd |

Penfolds, Matua, 19 Crimes, St Hubert's The Stag, Pepperjack |

Strong Challenger |

Treasury Wine Estates Ltd acts as a major premium wine player in Europe, importing and distributing New World brands like Penfolds, 19 Crimes, and Matua while fostering bottling efficiency to strengthen its market share. |

The competitive landscape is being progressively reshaped by wine investment in European estates and by US wine company acquisitions of European origins. These cross-continental ownership changes are creating hybrid marketing approaches that leverage European authenticity with wine marketing investment infrastructure.

Key Company Profiles

LVMH

LVMH is a leading luxury conglomerate and one of the most influential players in Europe’s wine market. The company owns a portfolio of premium wine and champagne brands. LVMH focuses on premiumization, luxury positioning, heritage branding and global distribution, with a strong presence across fine wines, champagne, hospitality and wine tourism.

- Key Brands: Moët & Chandon, Dom Pérignon, Veuve Clicquot, Krug, Ruinart, Château d'Yquem, Chandon, Cloudy Bay

- Recent Developments: In October 2024, Moët Hennessy, LVMH’s Wines and Spirits division, made a strategic minority investment in French Bloom, a leading prestige alcohol-free sparkling wine brand. The partnership highlights both companies’ ambition to shape the future of premium non-alcoholic sparkling wines.

- Strategic Focus: Centered on premium and luxury wine leadership, leveraging heritage brands, exclusive experiences and strong distribution networks.

Pernod Ricard

Pernod Ricard is one of the leading players in Europe’s wine and spirits market, operating a diversified portfolio of premium wines, champagnes and spirits. Pernod Ricard focuses on premiumization, sustainability, innovation and global brand expansion while leveraging strong distribution networks across retail, hospitality and travel retail channels.

- Key Brands: G.H. MUMM, Perrier-Jouët.

- Strategic Focus: Premiumization, portfolio diversification and strengthening premium wine and champagne brands through innovation and experiential marketing.

Market Concentration Analysis

The European wine market's concentration level is unusually low relative to most consumer goods categories. This fragmentation is structurally embedded in European wine through the appellation system, each appellation creating a legally protected production zone that sustains hundreds of independent producers whose wines are non-substitutable for each other in a strict sense. Concentration is notably higher in sparkling wine.

Investment & Growth Opportunities

Highest Growth Segments

Sparkling wine (~4.6% CAGR), white wine (~4.1% CAGR), low/no-alcohol wine (~15-20% CAGR from small base), organic/biodynamic certified wine (~8-10% CAGR), wine e-commerce DTC (~12% CAGR), Provence rose (~8% CAGR), and Asian export premium wine (~6-8% CAGR) represent the highest-growth European wine investment vectors through 2034.

Emerging Investment Opportunities

English sparkling wine represents Europe's highest-risk, highest-reward emerging wine production investment, climate change creating optimum traditional method sparkling wine conditions in Southern England's chalk, limestone, and Greensand geology, with English sparkling wine achieving Champagne-competitive critical quality while commanding premium pricing that sustains investment returns above new vineyard economics.

Investment Themes

- Organic and biodynamic wine estate acquisition for sustainability-premium product differentiation: Certified organic and biodynamic European wine estate acquisition provides dual commercial benefit, above-market pricing premium and sustainability narrative investment that creates brand differentiation in increasingly ESG-conscious retail buyer procurement.

- Low/no-alcohol wine production technology investment capturing the moderation consumer trend's premium product opportunity: The European low/no-alcohol wine category requires spinning cone column or reverse osmosis dealcoholization technology investment to produce quality no-alcohol wine above the thermal vacuum evaporation alternatives that have historically dominated and produced inferior aromatic profile products.

Future Market Outlook (2026-2034)

The Europe wine market is projected to grow from USD 81.7 Billion in 2025 to USD 116.9 Billion by 2034, delivering a 4.06% CAGR over the forecast period. The market's anchor value of USD 99.7 Billion in 2030 represents a European wine industry at its most transformative commercial inflection in the modern wine era. The low/no-alcohol wine category will have achieved mainstream consumer adoption, climate change will have visibly restructured established wine regions, and digital DTC channels will have reached 20-25% of total European wine value distribution, progressively displacing the traditional negociant-distributor-retailer three-tier chain for premium wine.

Three structural forces define European wine market growth through 2034 with confidence. Premiumization as a structural consumer evolution. Emerging market export demand growth is creating a revenue base above European domestic consumption. The digital transformation of the wine trade is creating structural DTC channel growth that sustains above-inflation fine wine producer revenues by disintermediating traditional distribution margin capture.

Research Methodology

Primary Research

Primary research comprised structured interviews with 55+ industry stakeholders (2025) including general directors from Champagne houses; Export Directors; UK wine buyers; wine technology specialists; and wine tourism consultants.

Secondary Research

Secondary research encompassed World Wine Report; Drinks Market Analysis European Wine Report; Champagne annual shipment statistics; annual production data; wine export statistics; company annual reports; Fine Wine Market Report; UK wine production statistics; Wine Intelligence Portraits consumer research. Over 65 secondary sources reviewed.

Forecasting Models

Market revenue forecasts developed using country-segment matrix model: (i) volume component from national wine institute production and consumption data, adjusted for import/export net flow per country; (ii) price component derived from wine category ASP growth rate by segment; (iii) channel mix evolution from IWSR digital direct data.

Europe Wine Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Still Wine, Sparkling Wine, Fortified Wine and Vermouth |

| Colors Covered | Red Wine, Rose Wine, White Wine |

| Distribution Channels Covered | Off-Trade, On-Trade |

| Countries Covered | Germany, France, United Kingdom, Italy, Spain |

| Companies Covered | LVMH, Pernod Ricard, E. & J. Gallo Winery, Constellation Brands, Inc., Treasury Wine Estates Ltd, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Europe wine market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the Europe wine market.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Europe wine industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Europe Wine Market Report

The European wine market reached USD 81.7 Billion in 2025, representing one of the largest wine markets by production value and consumption expenditure. Still wine dominates at 68.4% through the breadth of European still wine, from everyday table wine. France leads by country at 24.8%, driven by Champagne luxury concentration and fine wine trade value. Red wine leads color at 47.6% through fine wine auction market concentration and European dining culture centrality.

The European wine market grows at 4.06% CAGR during 2026-2034, reaching USD 116.9 Billion by 2034. Sparkling wine is the fastest-growing segment at ~4.6% CAGR through continued expansion, Champagne luxury premiumization, and English sparkling wine's commercial emergence.

Still wine leads at 68.4% due to its strong cultural significance, everyday consumption patterns and wide availability across red, white and rosé varieties. It is deeply integrated into European dining traditions and accounts for the largest share of retail, hospitality and export sales.

Red wine leads at 47.6% through its dominance in European fine wine auction trading, cultural centrality in European dining tradition, and the critical mass of premium European red wine appellations.

France leads at 24.8% due to its recognized wine heritage, premium appellations, strong domestic consumption and export leadership.

Leading companies include LVMH, Pernod Ricard, E. & J. Gallo Winery, Constellation Brands, Inc., and Treasury Wine Estates Ltd, among others.

The European wine market is projected to reach approximately USD 99.7 Billion by 2030, with English sparkling wine premium positioning, low/no-alcohol wine growth creating dedicated no-alcohol wine sections, organic and biodynamic wine achieving European wine retail high value, and export premium wine growth.

Three priority opportunities: organic and biodynamic wine estate acquisition at below-PDO-premium valuation; low/no-alcohol wine production technology investment in reverse osmosis dealcoholization enabling premium no-alcohol wine production to capture the moderation consumer trend's price premium category that standard dealcoholized wine cannot reach; and English sparkling wine vineyard and winery investment.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)