European Frozen Seafood Market Size, Share, Trends and Forecast by Product Type, Distribution Channel, and Country 2026-2034

European Frozen Seafood Market Size, Share, Trends & Forecast (2026-2034)

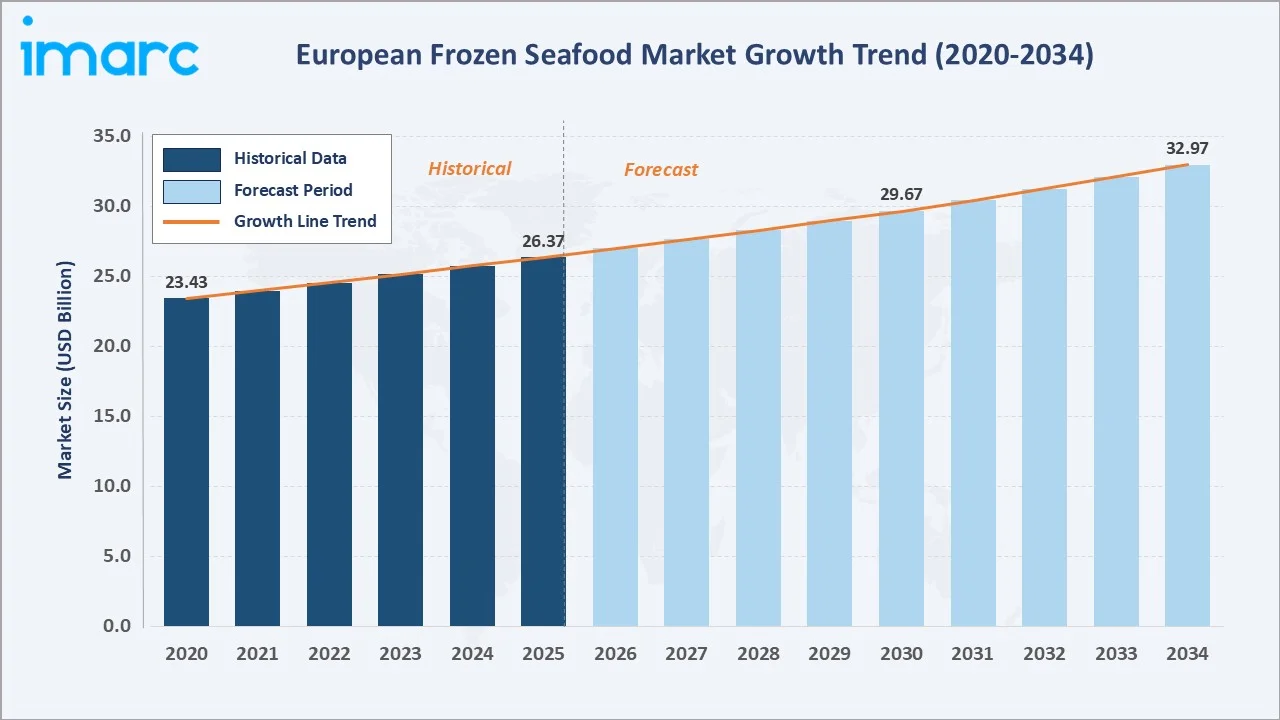

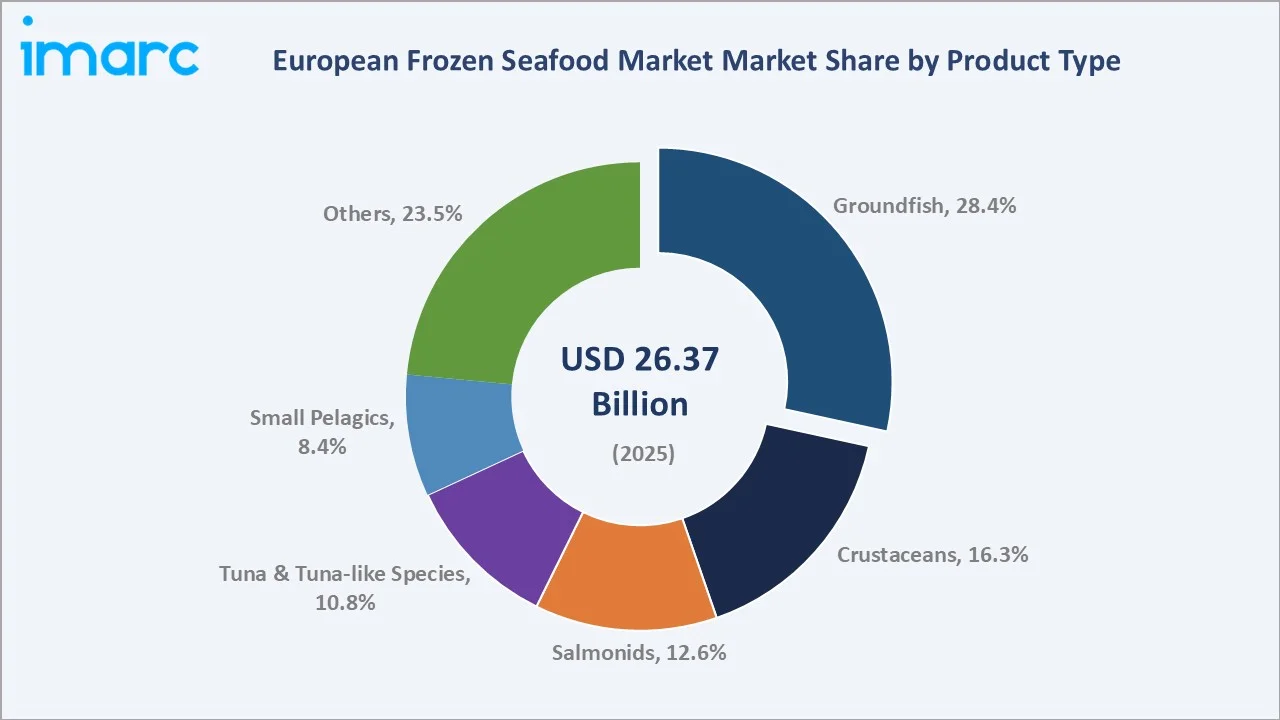

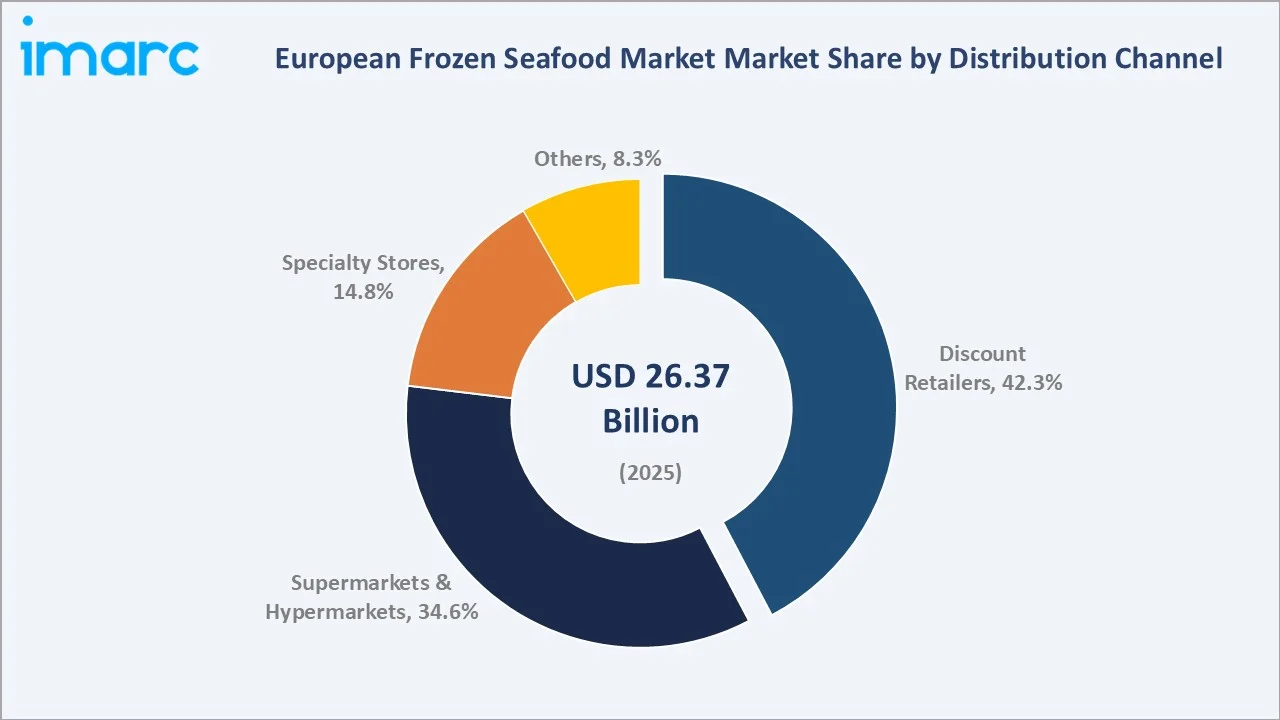

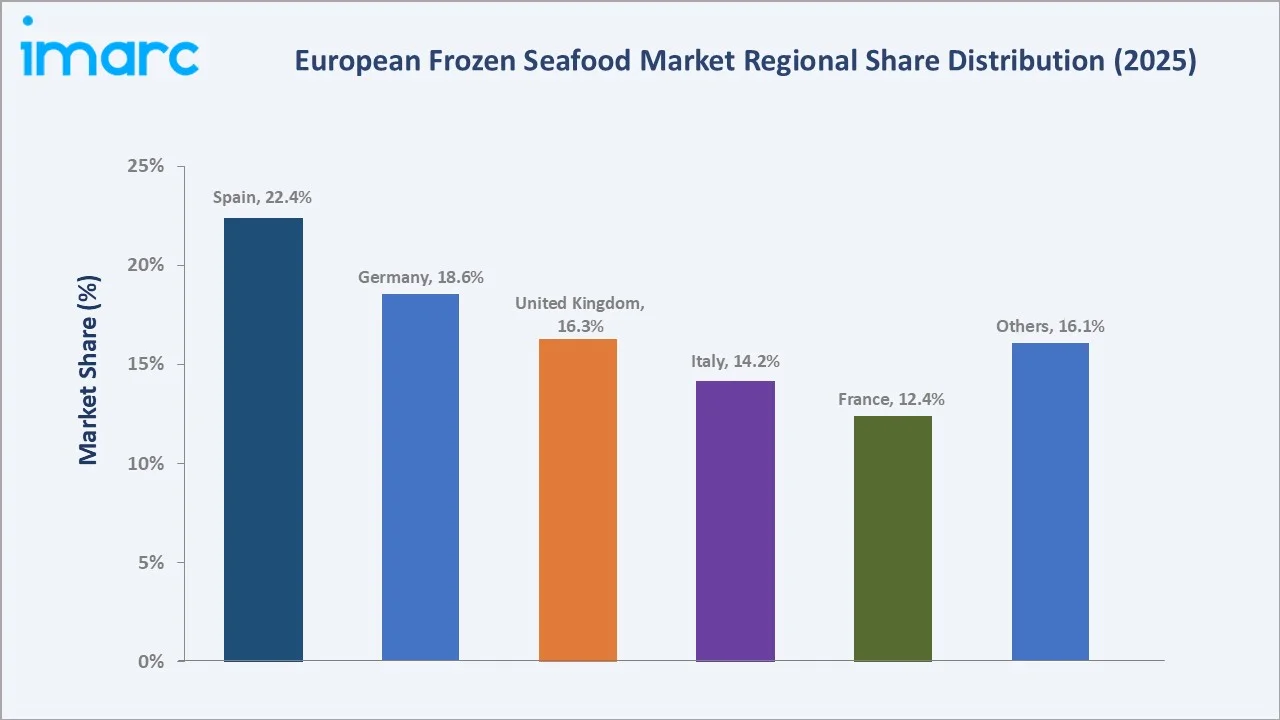

The European frozen seafood market size was valued at USD 26.37 Billion in 2025 and is projected to reach USD 32.97 Billion by 2034, growing at a CAGR of 2.39% during 2026-2034. The market is supported by rising consumer preference for convenient, protein-rich meal options, expanding cold-chain infrastructure, and the increasing penetration of discount retail channels. Groundfish dominates product demand with a 28.4% share in 2025, while Discount Retailers account for 42.3% of distribution. Spain leads regional demand at 22.4%, followed by Germany (18.6%) and the United Kingdom (16.3%).

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 26.37 Billion |

|

Forecast Market Size (2034) |

USD 32.97 Billion |

|

CAGR (2026-2034) |

2.39% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Country |

Spain (22.4% share, 2025) |

|

Fastest Growing Country |

Poland |

|

Leading Product Type |

Groundfish (28.4%, 2025) |

|

Leading Distribution Channel |

Discount Retailers (42.3%, 2025) |

The chart below illustrates European frozen seafood market expansion from 2020 to 2034, tracking post-pandemic recovery and structural growth driven by consumer demand trends.

To get more information on this market, Request Sample

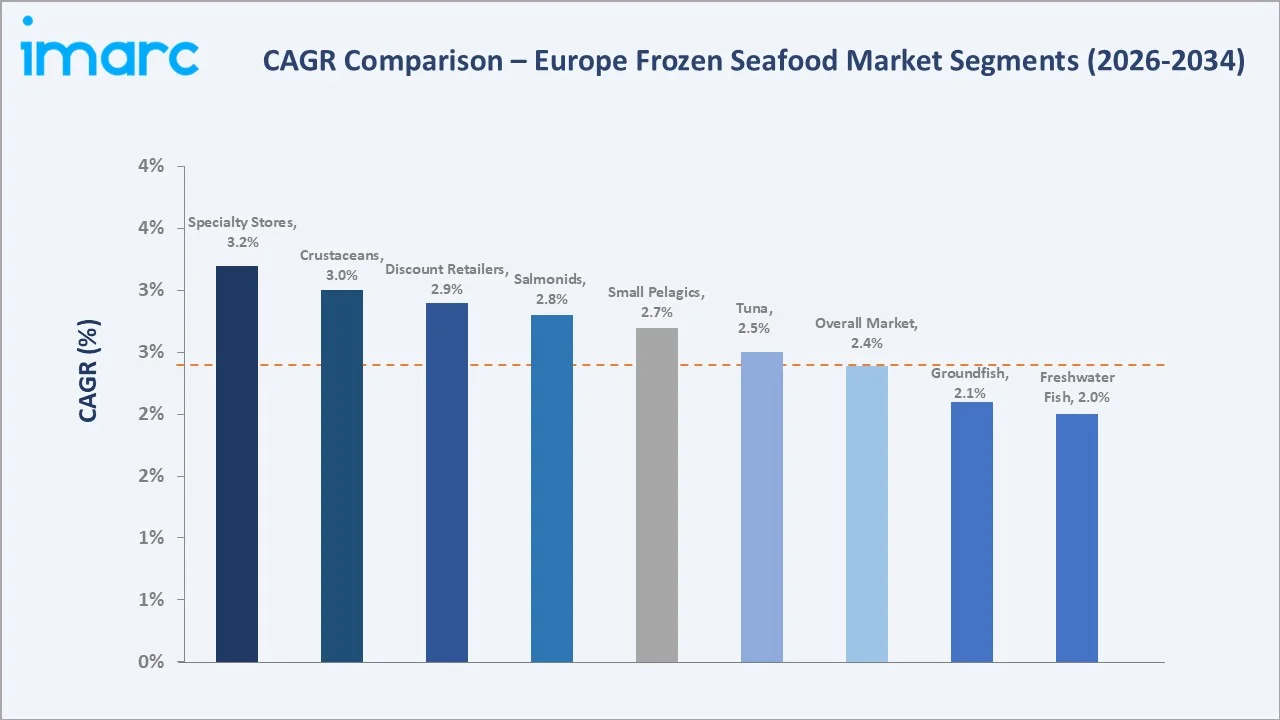

CAGR analysis highlights Crustaceans, Specialty Stores, and Salmonids as the fastest-growing segments in the European frozen seafood market through 2034.

Executive Summary

The European frozen seafood market is steadily evolving due to changing consumer lifestyles, growth of value-focused retail formats, and advancements in freezing and packaging technologies. Valued at USD 26.37 billion in 2025, the market is expected to reach USD 32.97 billion by 2034, growing at a CAGR of 2.39%, supported by increasing demand for convenient and nutritious meal options across retail and foodservice channels.

Groundfish leads the market with a 28.4% share in 2025, followed by crustaceans (16.3%) and salmonids (12.6%). Discount retailers dominate distribution with 42.3% share, while supermarkets and hypermarkets hold 34.6%, driven by private-label growth. Increasing adoption of MSC and ASC sustainability certifications is also shaping consumer preferences and supply chains.

Spain leads with a 22.4% country share in 2025, anchored by deep cultural seafood consumption and a well-developed cold-chain infrastructure. Germany (18.6%) and the United Kingdom (16.3%) follow, with the UK market recovering post-Brexit trade normalization. Poland (8.6%) is emerging as the fastest-growing country, supported by expanding processed seafood production and rising domestic consumption.

Key Market Insights

|

Insight |

Data |

|

Largest Product Type Segment |

Groundfish – 28.4% share (2025) |

|

Second Largest Product Segment |

Crustaceans – 16.3% share (2025) |

|

Leading Distribution Channel |

Discount Retailers – 42.3% share (2025) |

|

Leading Country |

Spain – 22.4% revenue share (2025) |

|

Second Country |

Germany – 18.6% revenue share (2025) |

|

Top Companies |

Nomad Foods, Mowi ASA, Thai Union, Pescanova, Frosta AG, A. Espersen |

Key Analytical Observations Supporting The Above Data:

- Groundfish dominance at 28.4% in 2025 reflects Europe's long-standing preference for cod, haddock, and pollock – anchored by strong demand across the UK, Germany, and Scandinavia in both retail and institutional food service.

- Crustaceans at 16.3% in 2025 are supported by rising demand for premium frozen shrimp and prawns across Southern European markets, particularly Spain, Portugal, and Italy.

- Discount Retailers' 42.3% channel dominance reflects European consumers' price-driven purchasing behavior, particularly post-2022 inflationary pressure, making frozen seafood an accessible protein substitute.

- Spain's 22.4% country share in 2025 is underpinned by approximately 44.92 kg per capita annual seafood consumption – among the highest globally – supported by a sophisticated cold-chain and processing ecosystem.

- Poland's rapid growth trajectory is driven by expanding domestic seafood processing capacity, serving both local consumption and as a re-export hub to Western European markets.

- Nomad Foods generated over EUR 3 Billion in revenue in 2024, reinforcing its leadership position in the European frozen food and seafood category.

European Frozen Seafood Market Overview

Frozen seafood includes fish, shellfish, and other aquatic products preserved at sub-zero temperatures to maintain quality and extend shelf life. It covers whole fish, fillets, breaded products, ready-to-cook items, and shellfish, supported by a value chain spanning wild catch, aquaculture, processing, cold-chain logistics, and retail and foodservice distribution.

The European frozen seafood market operates under strict EU food safety, labeling, and sustainability regulations, along with national trade policies. Market dynamics are influenced by income trends, food inflation, and rising cold-chain energy costs, while growing sustainability awareness is driving retailers to prioritize certified sustainable sourcing, especially for private-label products.

Market Dynamics

To evaluate market opportunities, Request Sample

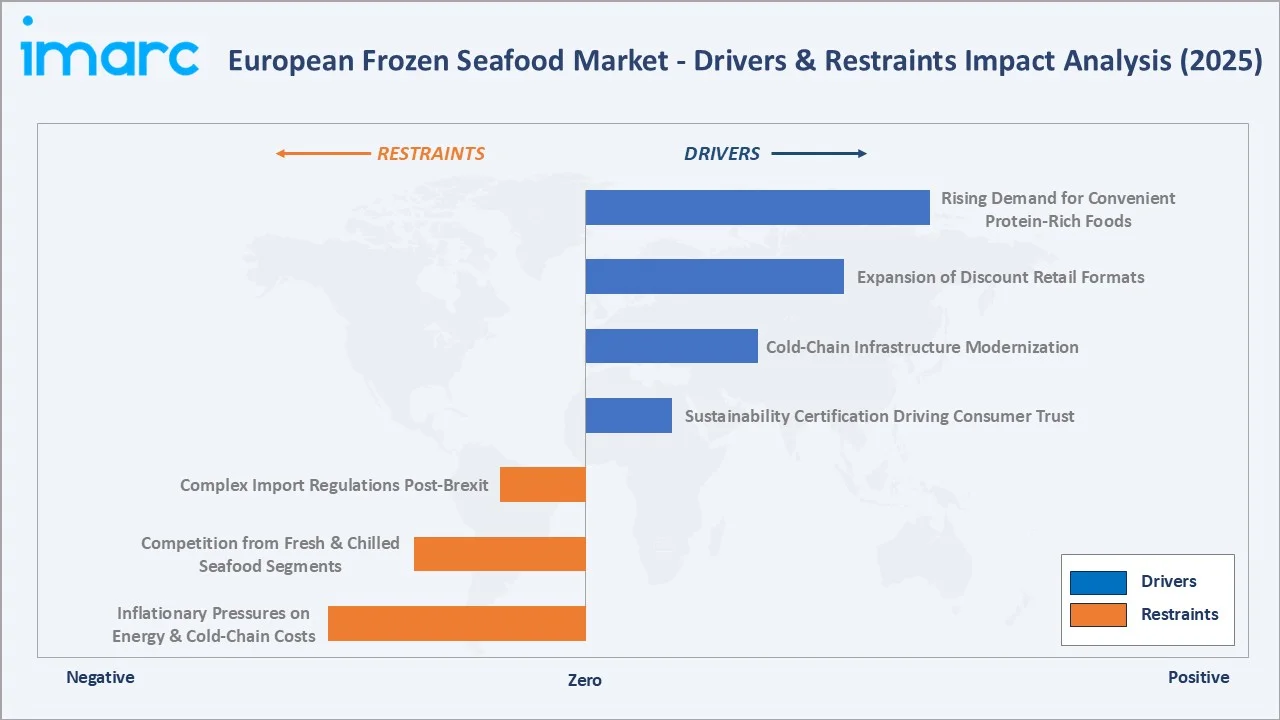

Market Drivers

- Rising Demand for Convenient, Protein-Rich Foods: Shifting European lifestyles and increasing dual-income households are driving demand for quick-preparation frozen seafood. Products offering easy meal solutions – such as breaded fish fillets and marinated shrimp.

- Expansion of Discount Retail Formats: The rapid expansion of discount retailers such as Lidl and ALDI across Europe is improving access to frozen seafood, with competitively priced private-label offerings attracting cost-conscious consumers.

- Cold-Chain Infrastructure Modernization: Investments in cold storage and refrigerated logistics across Europe, particularly in Poland, Italy, and Portugal, are improving availability and quality, while IQF technology helps maintain nutrition comparable to fresh seafood.

- Sustainability Certification Driving Consumer Trust: MSC-certified frozen seafood products are gaining traction across EU markets, as growing retail mandates for sustainably sourced products encourage manufacturers to certify supply chains and expand consumer appeal.

Market Restraints

- Inflationary Pressures on Energy and Cold-Chain Costs: Rising energy costs between 2022 and 2024 increased cold-chain operational expenses across key European markets, putting pressure on margins for processors, logistics providers, and retailers handling frozen seafood.

- Competition from Fresh and Chilled Seafood Segments: In markets such as Spain, France, and Italy – where fresh seafood enjoys strong cultural preference – frozen products compete for share, limiting growth rates particularly in premium retail channels.

- Complex Import Regulations Post-Brexit: The UK's post-Brexit import control framework introduced additional certification and labelling requirements, increasing operational complexity and costs for EU-to-UK frozen seafood trade flows.

Market Opportunities

- Value-Added Frozen Seafood Product Growth: Ready-to-cook and marinated frozen seafood formats are among the fastest-growing segments, with meal-kit integration creating significant incremental growth opportunities across Europe.

- Emerging Eastern European Market Penetration: Countries like Poland, Czech Republic, and Hungary represent under-penetrated growth markets with rising disposable incomes and increasing seafood consumption awareness.

- Aquaculture Production Expansion: Growth in European salmon and sea bass aquaculture – Norway's aquaculture production exceeded 1.5 million tonnes in 2024 – provides stable raw material supply to support frozen processing capacity expansion.

Market Challenges

- Supply Chain Volatility from Climate and Geopolitical Factors: Climate change impacts on wild-catch volumes and geopolitical disruptions create raw material supply uncertainty, particularly for species like cod and tuna dependent on specific geographic fisheries.

- Consumer Perception Gaps on Nutritional Quality: Despite advances such as IQF technology that preserve most nutritional value, many European consumers still perceive frozen seafood as inferior to fresh products, limiting premiumization and higher-value product adoption.

- Increasing Regulatory Complexity Around Seafood Labelling: EU seafood labelling regulations requiring detailed origin, catch method, and thaw status declarations impose compliance costs on manufacturers and retailers across the value chain.

Emerging Market Trends

1. Sustainability and Certification-Led Purchasing

European retailers, including Lidl, ALDI, and Carrefour, are increasingly prioritizing MSC and ASC-certified frozen seafood. Expanding sustainable sourcing policies are driving supply chain adjustments among producers and processors, while accelerating growth in the premium frozen seafood market segment.

2. Private-Label Frozen Seafood Expansion

Discount and supermarket chains are expanding private-label frozen seafood ranges to improve margins and attract price-sensitive consumers. Growing adoption of retailer brands across Europe is outpacing branded products, prompting supply chain shifts and intensifying competition in the frozen seafood market.

3. Ready-to-Cook and Value-Added Format Growth

Breaded, battered, marinated, and portioned frozen seafood products are growing faster than whole or unprocessed categories. Consumers across Germany, the UK, and France increasingly prefer value-added formats, with products like battered cod fillets and garlic prawn packs gaining strong traction through both retail and food service channels.

4. Cold-Chain Technology Optimization

Advances in IQF, cryogenic freezing, and IoT-based temperature monitoring are improving frozen seafood quality and reducing cold-chain losses. Smart cold-storage investments enhance energy efficiency, strengthen traceability, and support compliance with EU sustainability and food safety regulations.

5. Plant-Based Seafood Alternatives Entering the Frozen Category

Plant-based frozen seafood alternatives, including vegan fish and tuna products, are expanding across European retail. Companies such as Good Catch and Nestlé’s Garden Gourmet are targeting flexitarian and health-conscious consumers, creating a growing structural segment within frozen seafood market dynamics.

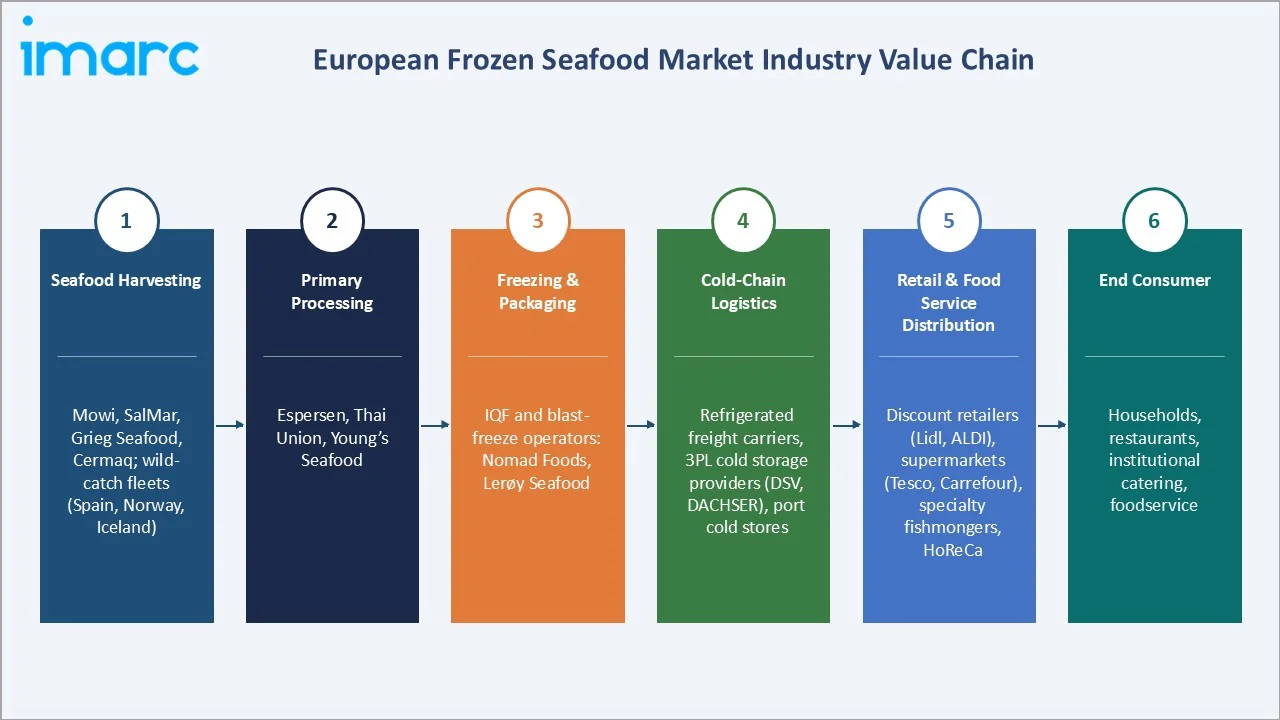

Industry Value Chain Analysis

The European frozen seafood value chain spans six stages, from primary harvest to end-consumer delivery, encompassing complex cold-chain logistics and multi-tier processing operations.

|

Stage |

Key Players / Examples |

|

Seafood Harvesting |

Mowi, SalMar, Grieg Seafood, Cermaq; wild-catch fleets (Spain, Norway, Iceland) |

|

Primary Processing |

Espersen, Thai Union, Young’s Seafood |

|

Freezing & Packaging |

IQF and blast-freeze operators: Nomad Foods, Lerøy Seafood |

|

Cold Chain Logistics |

Refrigerated freight carriers, 3PL cold storage providers (DSV, DACHSER), port cold stores |

|

Retail & Food Service Distribution |

Discount retailers (Lidl, ALDI), supermarkets (Tesco, Carrefour), specialty fishmongers, HoReCa |

|

End Consumers |

Households, restaurants, institutional catering, foodservice |

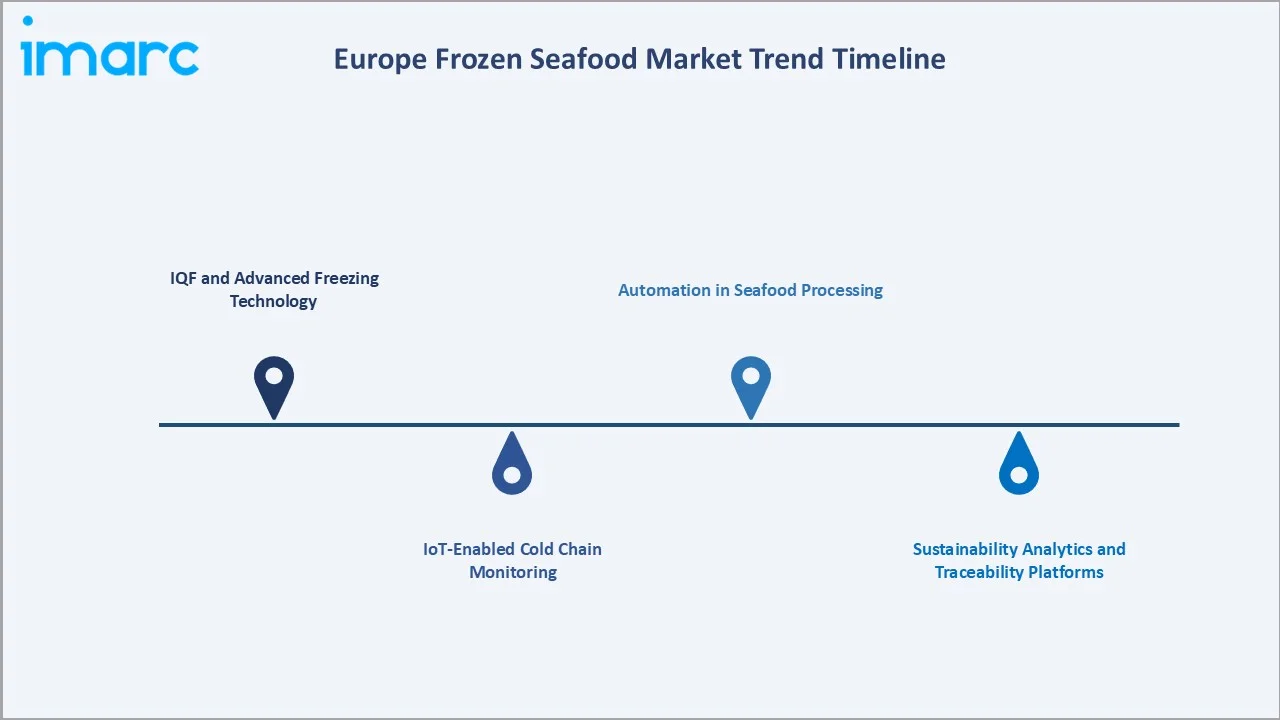

Technology Landscape in the Frozen Seafood Industry

IQF and Advanced Freezing Technology

IQF technology preserves cell structure, improving taste, texture, and nutritional retention, while cryogenic freezing using liquid nitrogen enables ultra-rapid freezing, minimizing ice crystal formation and significantly enhancing premium frozen seafood quality.

IoT-Enabled Cold Chain Monitoring

Real-time temperature and humidity monitoring through IoT sensor networks ensures regulatory compliance and reduces product losses from cold-chain breaks. Leading logistics providers now offer blockchain-integrated traceability platforms, enabling retailers to verify catch location, processing date, and temperature history for each frozen seafood SKU.

Automation in Seafood Processing

Robotic filleting, automated portioning, and AI-based defect detection are reducing labor dependency in seafood plants. Automated processing systems improve yield, minimize waste, and deliver consistent portioning accuracy compared to manual operations.

Sustainability Analytics and Traceability Platforms

Digital catch-to-consumer traceability platforms, supported by FisheryProgress, MSC certification, and retailer disclosure requirements, are becoming standard in Europe. These systems reduce mislabelling risks and support compliance with evolving EU seafood traceability regulations.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product Type |

Groundfish |

28.4% |

2025 |

|

Distribution Channel |

Discount Retailers |

42.3% |

2025 |

|

Country |

Spain |

22.4% |

2025 |

By Product Type

To access detailed market analysis, Request Sample

Groundfish holds the dominant 28.4% share in 2025, driven by European demand for cod, haddock, and pollock – consumed extensively across the UK, Germany, and Scandinavian markets. Its versatility in breaded, battered, and fillet formats sustains strong retail volumes.

Crustaceans, accounting for 16.3% in 2025, are driven by rising demand for frozen shrimp and prawns in Southern Europe, particularly Spain and Italy, with cooked, peeled, and marinated formats supporting premiumization. Salmonids (12.6%) benefit from expanding Norwegian aquaculture, ensuring consistent supply and competitive pricing for frozen salmon portions and fillets.

Tuna and Tuna-like Species account for 10.8% in 2025, supported by canned and frozen tuna applications in both retail and food service. Small Pelagics (8.4%) – comprising sardines, anchovies, and mackerel – are consumed across Mediterranean markets with strong price-to-nutrition value positioning.

By Distribution Channel

Discount retailers dominate with a 42.3% channel share in 2025, driven by rapid expansion of hard-discount formats across Europe. Lidl and ALDI, operating thousands of stores across the region, have positioned frozen seafood as a core category through competitively priced private-label offerings.

Supermarkets and hypermarkets hold 34.6% in 2025, supported by extensive frozen food aisles, strong branded portfolios, and expanding private-label seafood offerings. Specialty stores (14.8%) cater to premium and artisanal frozen seafood demand, particularly in urban markets seeking MSC-certified and high-value species.

Regional Market Insights

|

Country |

Share (2025) |

Key Growth Drivers |

|

Spain |

22.4% |

Highest per-capita seafood consumption in Europe; deep cultural affinity; strong processing industry |

|

Germany |

18.6% |

Large retail frozen food sector; strong demand for cod and salmon; value-oriented private-label growth |

|

United Kingdom |

16.3% |

Cultural preference for battered fish; post-Brexit supply chain normalization; strong branded market |

|

Italy |

14.2% |

Mediterranean diet seafood integration; growing demand for frozen shellfish and cephalopods |

|

France |

12.4% |

Strong foodservice frozen seafood demand; growing sustainability certification requirements in retail |

|

Poland |

8.6% |

Fastest growing; expanding processing capacity; rising domestic consumption; export hub role |

|

Portugal |

4.8% |

High per-capita seafood culture; growing frozen cod (bacalhau) and sardine processing base |

|

Others |

2.7% |

Includes Netherlands, Belgium, Sweden with growing frozen seafood consumption |

Spain leads the European frozen seafood market with a 22.4% share in 2025, driven by one of the highest per-capita seafood consumption rates globally – approximately 41.92 kg per capita annually. A mature and highly developed domestic frozen seafood processing industry, anchored in Galicia and the Basque Country, supports both local consumption and export volumes.

Germany (18.6%) is driven by a large value-oriented retail landscape and strong discount format penetration. The United Kingdom (16.3%) shows resilient demand for breaded and battered frozen fish products. Poland (8.6%) is emerging as the fastest-growing market, supported by rising seafood consumption and expanding processing and export capabilities backed by EU investment.

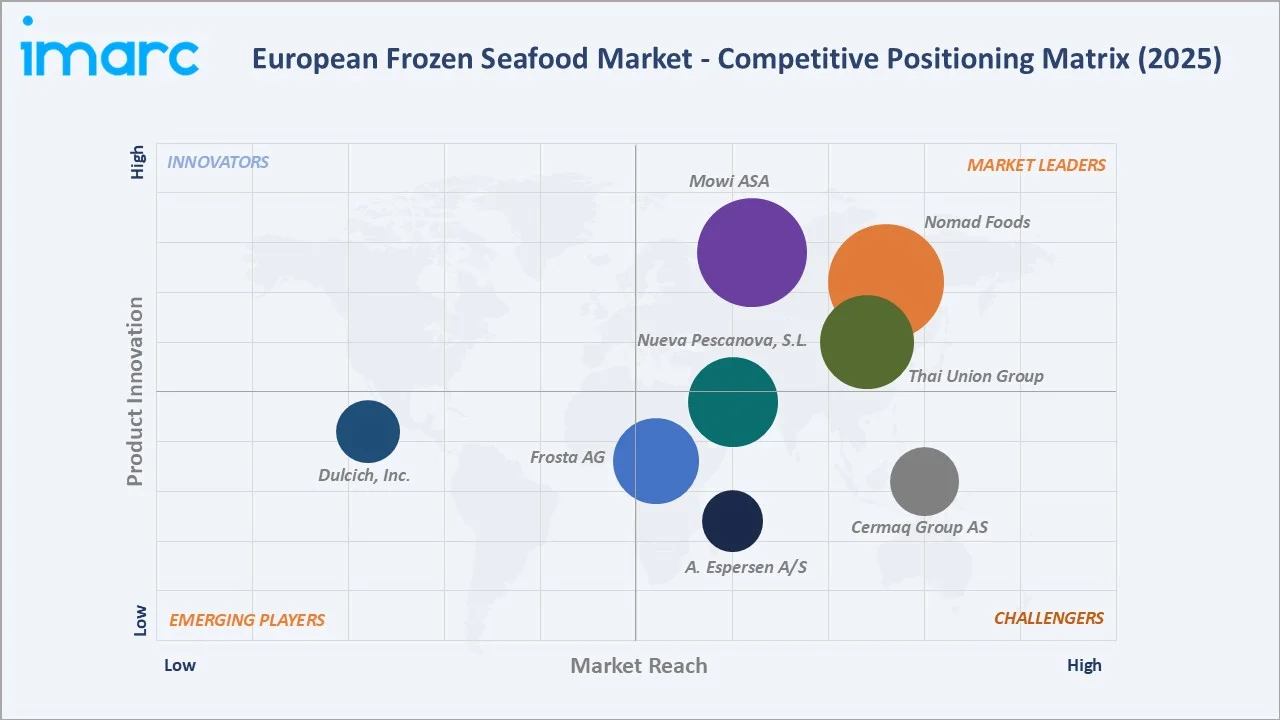

Competitive Landscape

|

Company Name |

Key Brand / Platform |

Market Position |

Core Strength |

|

Nomad Foods Ltd. |

Birds Eye, Iglo, Frikom |

Leader |

Largest European frozen food group; broad country coverage; strong R&D |

|

Mowi ASA |

Mowi |

Leader |

Vertically integrated salmon; from aquaculture to consumer pack |

|

Thai Union Group |

John West, Petit Navire, Mareblu |

Leader |

Global tuna sourcing; strong UK and European retail presence |

|

Nueva Pescanova, S.L. |

Pescanova |

Leader |

Integrated Spanish seafood processor; aquaculture + wild catch |

|

Frosta AG |

FRoSTA |

Challenger |

German premium frozen seafood; clean-label positioning |

|

A. Espersen A/S |

Rahbek |

Challenger |

Major cod processor; private-label supply to European retailers |

|

Cermaq Group AS |

True Arctic Salmon |

Challenger |

Salmon aquaculture; sustainable supply to European processors |

|

Dulcich, Inc. |

Pacific Seafood |

Emerging |

US-based with European market entry; growing frozen export volumes |

The European frozen seafood market is led by Nomad Foods, the continent's largest frozen food company, which reported approximately EUR 3.1 billion revenue in 2024. Nomad Foods' Birds Eye and Findus brands command strong retail positions across the UK, Germany, Italy, and the Nordic markets, leveraging significant brand equity in value-added frozen seafood categories.

Key Company Profiles

Nomad Foods Ltd.

Nomad Foods, headquartered in Feltham, UK, is Europe's largest frozen food company and a dominant force in the frozen seafood segment. The company reported approximately EUR 3.1 billion in revenue in 2024, with primary market positions across the UK, Italy, Germany, Sweden, and Norway.

- Product & Service Portfolio: Birds Eye (UK, Ireland), Findus (France, Italy, Nordics), Iglo (Germany and Western Europe), Frikom (Serbia and Balkans), and La Cocinera (Spain), covering frozen fish fillets, fish fingers, breaded seafood, coated fish, and shrimp products.

- Recent Developments: In 2024, Nomad Foods achieved 99.6% MSC/ASC-certified seafood sourcing and reduced absolute greenhouse gas emissions by 40.8% since 2019, according to its 2024 sustainability report, reinforcing its leadership in sustainable frozen seafood.

- Strategic Focus: Brand-led growth, value-added product innovation, sustainability certification expansion, and private-label competition mitigation through superior product quality

Mowi ASA

Mowi ASA, headquartered in Bergen, Norway, is the world's largest salmon aquaculture company, reporting revenue of approximately EUR 5.62 billion in 2024, with significant frozen salmon supply volumes into European processing and retail markets.

- Product & Service Portfolio: Farmed Atlantic salmon (whole, fillet, portion, fresh and frozen), smoked and marinated salmon, and value-added ready-to-cook seafood under the Mowi brand.

- Recent Developments: In 2025 Mowi increased its ownership in Nova Sea from 49% to 95%, boosting harvest volumes and strengthening its European salmon supply, with production expected to approach 600,000 tonnes annually. Mowi is developing a 6,000-tonne post-smolt RAS facility in Norway, with first deliveries expected in 2026, strengthening long-term salmon supply.

- Strategic Focus: Vertical integration from egg to consumer pack, operational efficiency, sustainability certifications (ASC), and premium consumer brand development across European markets

Nueva Pescanova, S.L.

Nueva Pescanova, headquartered in Vigo, Spain, is one of Europe's leading integrated seafood companies, generating approximately EUR 1.05 billion in annual revenue in FY25, with strong positions in the Spanish, Portuguese, and Italian frozen seafood markets.

- Product & Service Portfolio: Frozen shrimp, prawns, hake, squid, and value-added breaded and ready-to-cook seafood under the Pescanova brand across European retail markets.

- Recent Developments: In July 2025, company announced a €16 million investment in a new seafood processing facility in Spain, aimed at expanding value-added frozen seafood production capacity.

- Strategic Focus: Integrated supply chain management, aquaculture investment diversification, Mediterranean market leadership, and sustainability-driven production transformation

Market Concentration Analysis

The European frozen seafood market exhibits moderate concentration at the top tier. The top 5 companies – Nomad Foods, Mowi, Thai Union, Nueva Pescanova, and Frosta – collectively account for approximately 30–35% of European market revenue in 2025. However, the presence of numerous regional processors, private-label suppliers, and country-specific operators maintains a degree of fragmentation, particularly at the national market level.

The European frozen seafood market remains highly fragmented, with numerous regional processors supplying private-label products to discount and supermarket chains. This strong presence of retailer-branded offerings limits the dominance of leading branded players and intensifies competitive dynamics across the market.

Consolidation activity is gradually accelerating, driven by sustainability compliance costs, technology investment requirements for cold-chain modernization, and scale advantages in procurement. Smaller processors facing certification compliance costs and margin pressure from energy inflation are increasingly becoming acquisition targets for larger integrated operators and European private equity-backed food consolidators.

Investment & Growth Opportunities

Fastest-Growing Segments

Value-added and ready-to-cook frozen seafood formats, including breaded, battered, marinated, and meal-kit products, are emerging as the fastest-growing category, driven by rising consumer demand for convenience and easy-to-prepare seafood options, outpacing overall market growth.

Emerging Markets

Central and Eastern European markets, particularly Poland, the Czech Republic, Hungary, and Romania, present significant underpenetrated opportunities. Rising disposable incomes, expanding cold-chain infrastructure, and increasing seafood consumption are supporting growth, while Poland is emerging as a key regional processing and distribution hub.

Venture & Strategic Investment Trends

Investment activity in the European frozen seafood market is increasingly focused on cold-chain upgrades, IQF processing automation, and digital traceability platforms. At the same time, land-based aquaculture technologies such as RAS are attracting strong investment momentum, with Norway and the Netherlands emerging as key innovation hubs for sustainable seafood production.

Future Market Outlook (2026-2034)

The European frozen seafood market forecast projects value expansion from USD 26.37 Billion in 2025 to USD 32.97 Billion by 2034 at a CAGR of 2.39% – representing a cumulative value addition of approximately USD 6.6 Billion. Growth will be underpinned by expanding distribution in Eastern European markets, premiumization of value-added formats, and sustainability-led supply chain restructuring.

Three key forces are expected to reshape the European frozen seafood market: increasing sustainability mandates and certification requirements favouring integrated suppliers, and accelerating private-label expansion shifting value from branded products to retailer-owned offerings.

Third, technological innovation in freezing, packaging, and traceability will enable development of premium frozen seafood products comparable in quality and consumer perception to fresh offerings. By 2034, the European frozen seafood market is expected to evolve into a more segmented, sustainability-focused, and technology-enabled category, with clear differentiation between value, mainstream, and premium tiers across each national market.

Research Methodology

Primary Research

Primary research comprised structured interviews and surveys conducted in 2024–2025 with European frozen seafood market participants including procurement managers at major European retailers, operations directors at frozen seafood processors, trade association representatives (Europêche, ANFACO-CECOPESCA), cold-chain logistics managers, and foodservice category buyers.

Secondary Research

Secondary sources include company annual reports (Nomad Foods, Mowi ASA, Thai Union Group, Nueva

Pescanova, S.L.), European Commission fisheries statistics, EUROSTAT food consumption data, FAO aquaculture production reports, EU food safety regulatory publications (EFSA), and retail market data from Nielsen and Euromonitor International.

Forecasting Models

Market size estimations and growth projections utilized a combination of bottom-up and top-down forecasting methodologies, incorporating per-capita seafood consumption trends, cold-chain infrastructure development indices, retail format growth trajectories, aquaculture production expansion data, and scenario modelling under base, optimistic, and conservative macroeconomic assumptions.

European Frozen Seafood Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD, Million Tons |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Product Types Covered | Groundfish, Small Pelagics, Tuna and Tuna like Species, Salmonids, Bivalves and Other Molluscs, and Aquatic Invertebrates, Crustaceans, Other Marine Fish, Cephalapods, Freshwater Fish, Others |

| Distribution Channels Covered | Discount Retailers, Supermarkets and Hypermarkets, Specialty Stores, Others |

| Countries Covered | Poland, Spain, Italy, Portugal, Germany, United Kingdom, France, Others |

| Companies Covered | Nomad Foods Ltd., Mowi ASA, Thai Union Group, Nueva Pescanova, S.L., Frosta AG, A. Espersen A/S, Cermaq Group AS, Dulcich, Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the European frozen seafood market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the European frozen seafood market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the European frozen seafood industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the European Frozen Seafood Market Report

The European frozen seafood market was valued at USD 26.37 Billion in 2025, supported by growing retail penetration, rising protein demand, and expanding cold-chain distribution infrastructure.

The market is projected to reach USD 32.97 Billion by 2034, growing at a CAGR of 2.39% during 2026-2034, driven by value-added product growth, Eastern European expansion, and sustainability-led premiumization.

Groundfish leads with a 28.4% share in 2025, driven by strong European demand for cod, haddock, and pollock in both retail and institutional food service channels.

Discount Retailers command a 42.3% share in 2025, driven by expansion of hard-discount formats like Lidl and ALDI offering competitive private-label frozen seafood at accessible price points.

Spain leads with a 22.4% country share in 2025, anchored by one of the highest per-capita seafood consumption rates in Europe at approximately 41.92 kg per capita annually.

Key drivers include rising convenience food demand, cold-chain infrastructure expansion, discount retail growth, sustainability certification adoption, and aquaculture supply chain development.

Poland is the fastest-growing country, supported by expanding domestic consumption, growing food processing capacity, and an increasing role as a regional seafood re-export hub.

Leading companies include Nomad Foods Ltd., Mowi ASA, Thai Union Group, Nueva Pescanova, S.L., Frosta AG, A. Espersen A/S, Cermaq Group AS, and Dulcich, Inc.

Crustaceans account for 16.3% of the European frozen seafood market in 2025, driven by rising demand for frozen shrimp and prawns across Southern European markets.

Salmonids (12.6% share in 2025) benefit from expanding Norwegian salmon aquaculture, consistent supply, and premium consumer positioning in value-added frozen salmon formats.

MSC and ASC certification mandates, EU sustainability regulations, and growing consumer awareness are reshaping seafood supply chains and accelerating adoption of certified frozen seafood across Europe.

Spain is the largest country market, combining high per-capita seafood consumption, a mature domestic processing industry, and strong retail and food service distribution infrastructure.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)