EV Charging Management Software Platform Market Size, Share, Trends and Forecast by Module, Deployment, Charger Type, Application, and Region, 2026-2034

EV Charging Management Software Platform Market Size, Share, Trends & Forecast (2026-2034)

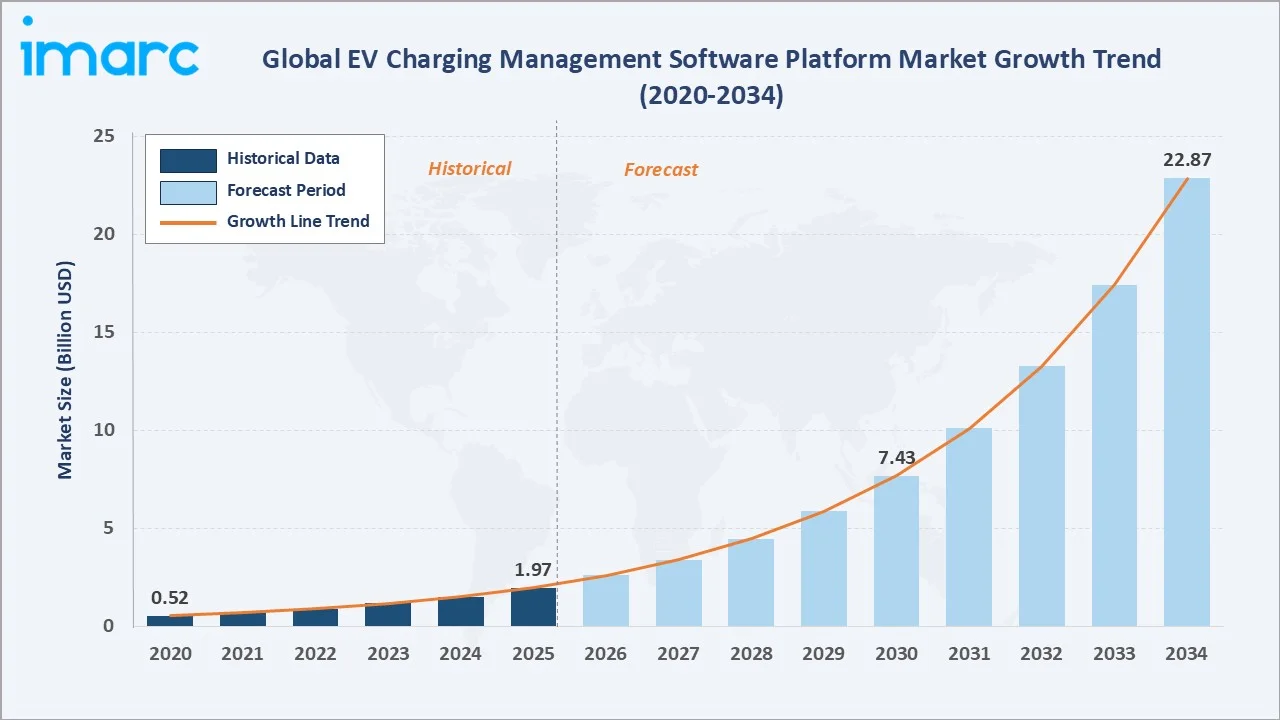

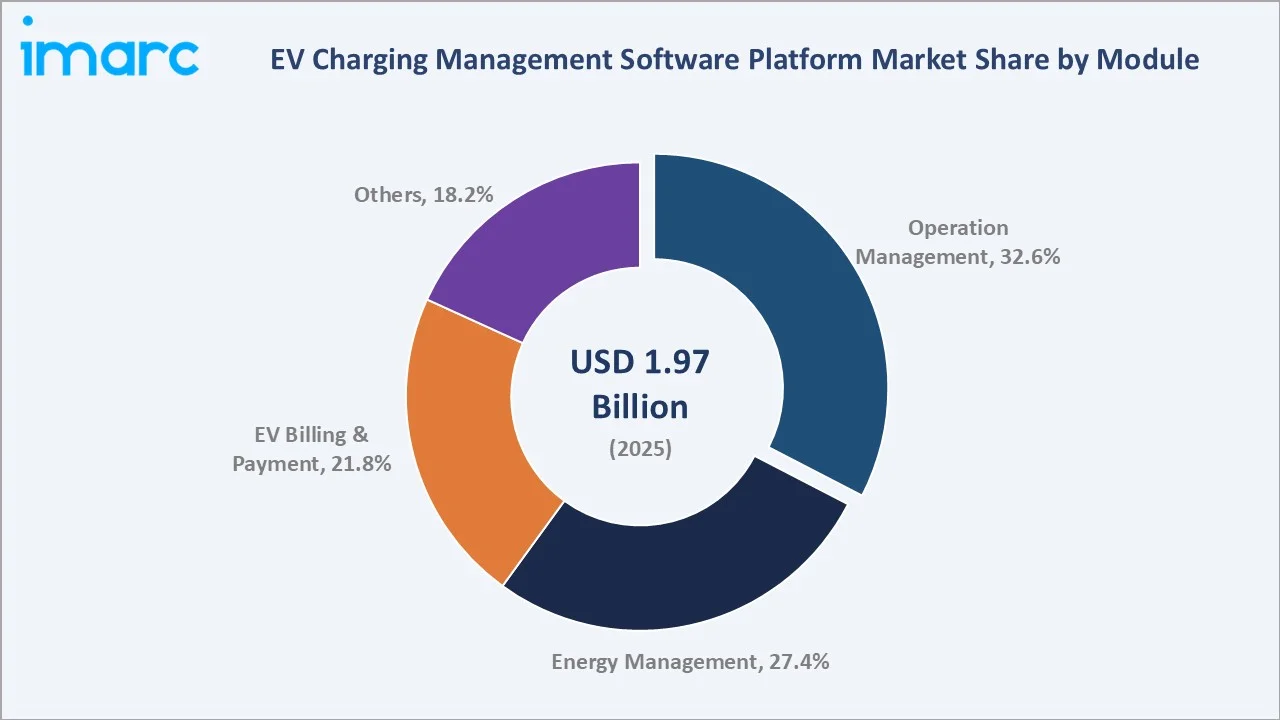

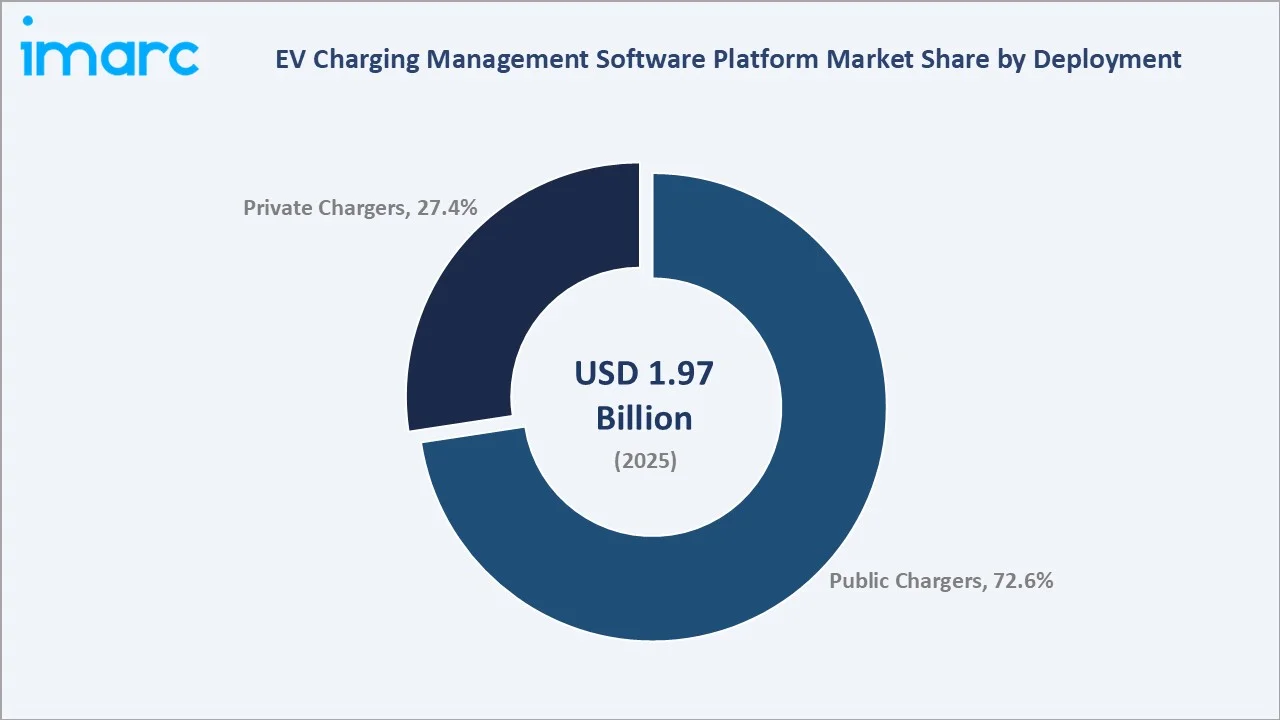

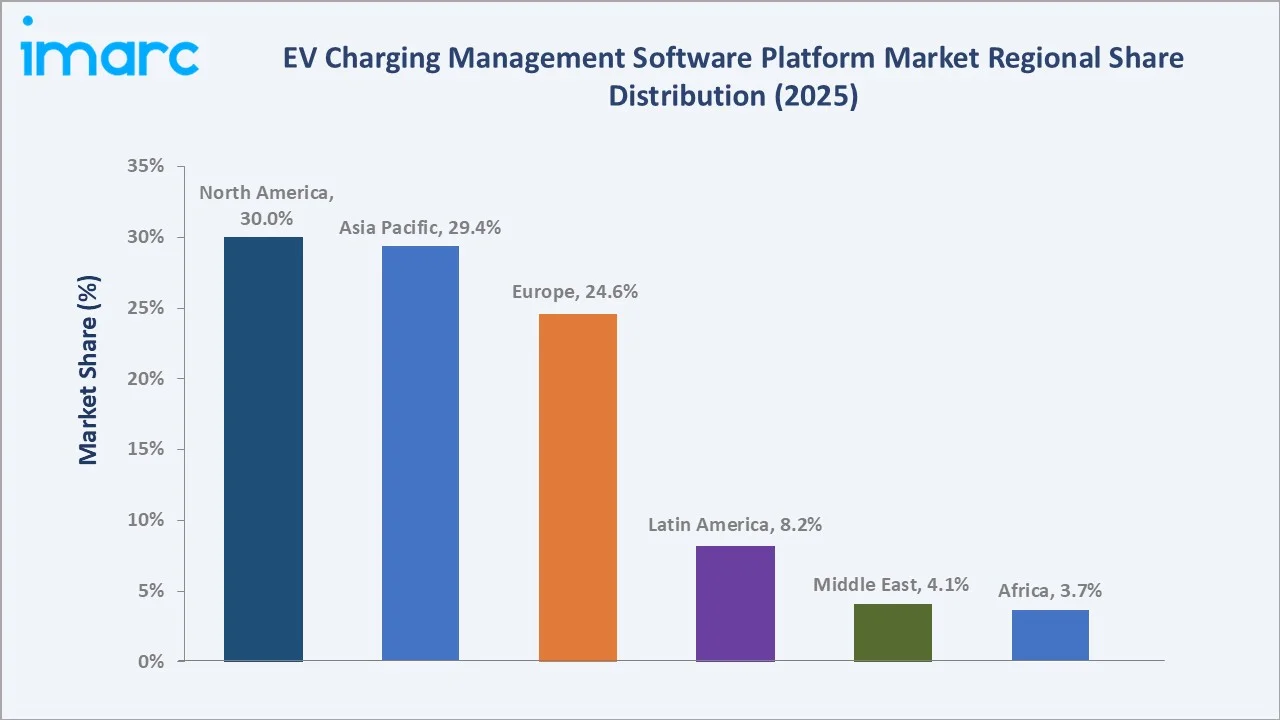

The EV charging management software platform market reached USD 1.97 Billion in 2025 and is projected to reach USD 22.87 Billion by 2034, growing at a CAGR of 30.35% during 2026-2034. The market is driven by rising EV adoption, expanding public and private charging infrastructure, and the need for real-time charger monitoring, payment management, and energy optimization. Electric car sales surpassed 20 million units in 2025, registering a 20% year-on-year increase, with China contributing more than 13 million sales and nearly 60% of global demand. Growing smart grid integration and fleet electrification are further supporting demand. The operation management leads module at 32.6%. Public chargers dominate deployment at 72.6%. North America leads regionally at 30.0%.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 1.97 Billion |

|

Forecast Market Size (2034) |

USD 22.87 Billion |

|

CAGR (2026-2034) |

30.35% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Module |

Operation Management (32.6%, 2025) |

|

Dominant Deployment |

Public Chargers (72.6%, 2025) |

|

Leading Region |

North America (30.0%, 2025) |

The EV charging management software platform market expanded from USD 0.52 Billion in 2020 to USD 1.97 Billion in 2025, anchored at USD 7.43 Billion in 2030, and forecast to reach USD 22.87 Billion by 2034. Charging management software platform represents the software intelligence layer of the EV charging infrastructure stack, the cloud-based platforms, backend management systems, and API-connected applications that enable charge point operators (CPOs), fleet managers, utilities, and property owners to monitor, control, optimize, and monetize EV charging infrastructure.

To get more information on this market, Request Sample

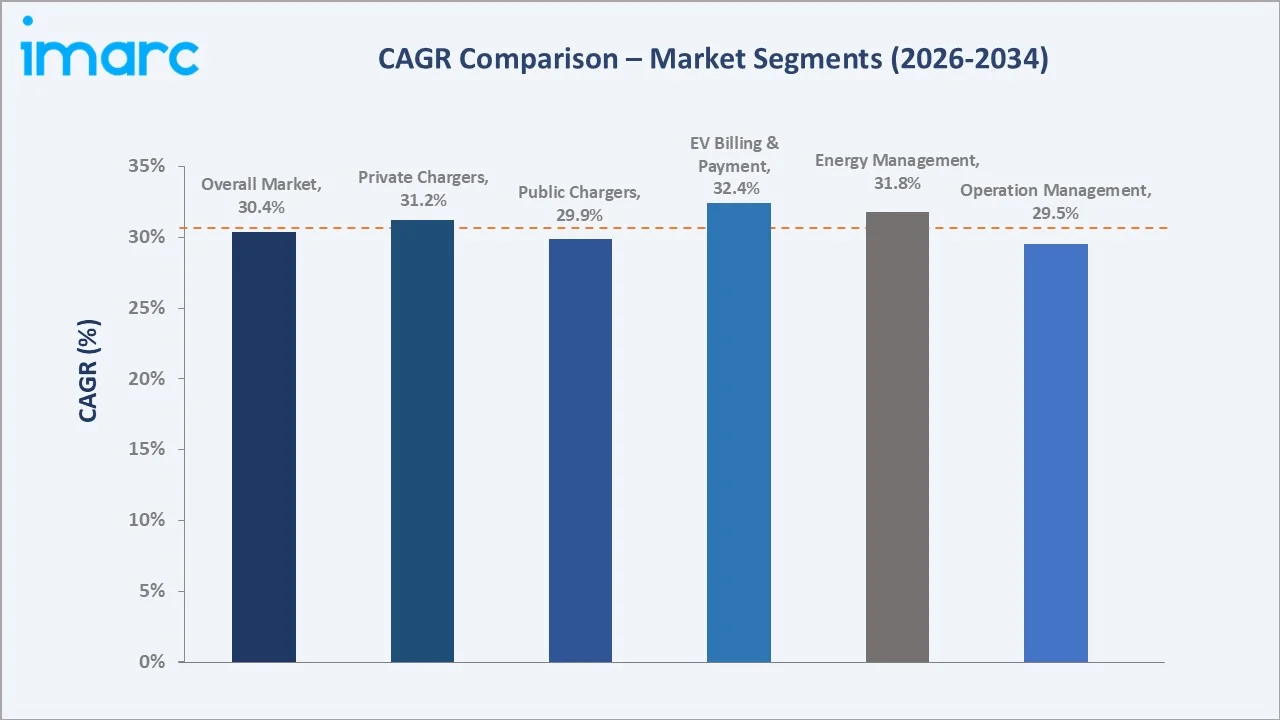

EV billing and payment grow fastest at ~32.4% CAGR through plug & charge, roaming payment aggregation, dynamic pricing, and subscription billing model adoption. Private chargers grow at ~31.2% CAGR through fleet depot electrification, workplace charging, and multi-family residential charging management software platform demand.

Executive Summary

The EV charging management software platform market at USD 1.97 Billion in 2025 represents one of the most commercially high-velocity software market growth trajectories globally, with global EV adoption acceleration, government infrastructure mandates, and the progressive sophistication of charging management software platforms from basic charger on/off control toward AI-powered energy optimization, V2G (vehicle-to-grid) energy trading, and autonomous demand-response charging. The market is projected to reach USD 22.87 Billion by 2034.

Operation management at 32.6% leads through the CPO network's fundamental charge-point monitoring and uptime management. Public Chargers at 72.6% reflect the CPO network scale and government-mandated public deployment. North America leads regionally at 30.0% through regional commercial stimulus.

Key Market Insights

|

Insight |

Data |

|

Dominant Module |

Operation Management - 32.6% share (2025) |

|

Dominant Deployment |

Public Chargers - 72.6% market share (2025) |

|

Leading Region |

North America - 30.0% share (2025) |

|

Market Opportunity |

V2G energy trading platform; AI-powered dynamic load management; fleet depot for logistics; MaaS charging integration; interoperability hub for multi-network roaming |

Key Analytical Observations Supporting the Above Data:

- Operation Management at 32.6%: The operation management segment is dominant as charging operators need software to monitor charger uptime, manage sessions, handle faults, optimize energy use, and ensure smooth network performance. Rising deployment of public and fleet charging stations further increases demand for centralized operational control.

- Public Chargers at 72.6%: Public chargers are dominant as they require centralized software for real-time monitoring, user access, payments, load management, and maintenance tracking. Expanding highway, urban, workplace, and retail charging networks is further increasing demand for charging management platforms.

- North America at 30.0%: North America is dominant due to rapid EV adoption, strong charging infrastructure investments, and the presence of leading EV charging network operators and software providers. Government incentives, fleet electrification, and smart charging initiatives further support platform demand across the region.

EV Charging Management Software Platform Market Overview

The EV charging management software platform market operates within the broader EV infrastructure ecosystem as the fastest-growing segment through intelligence, data, and energy optimization's value premium. The market's commercial uniqueness is the platform's simultaneous role as operational tool, commercial platform, and energy asset, creating the most commercially multi-stakeholder software platform serving CPOs, fleet managers, utilities, property managers, and EV drivers through a single charging management software platform.

The global charging management software platform ecosystem integrates EVSE hardware manufacturers, CPMS platform vendors, cloud and connectivity providers, charge point operators, utilities and grid operators, and EV driver-facing apps. Macroeconomic factors include rising EV sales, government incentives, charging infrastructure funding, and growing investments in clean mobility.

Market Dynamics

To evaluate market opportunities, Request Sample

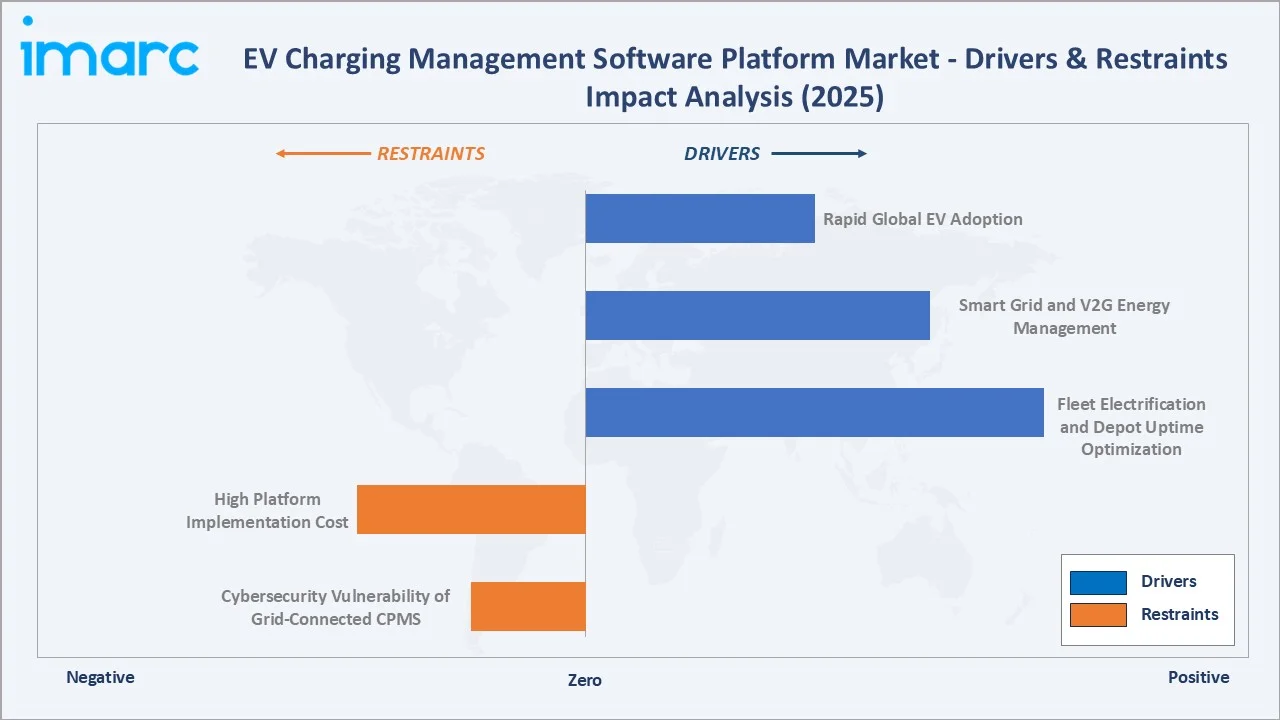

Market Drivers

- Rapid Global EV Adoption: The global electric car market continued its strong momentum in 2025, with sales surpassing 20 million units, representing a 20% increase compared to 2024. China remained the largest EV market worldwide, recording over 13 million electric car sales and accounting for approximately 60% of global EV purchases. Europe experienced a significant rebound, with electric car sales rising by more than 30% year-on-year to reach 4.2 million units, representing 28% of all new vehicle sales. This rapid global EV adoption is increasing the number of charging stations that need centralized monitoring and control. As EV users demand reliable, accessible, and fast charging, operators are adopting software for charger uptime, payment processing, load balancing, and remote diagnostics. Growing fleet electrification and public charging networks further raise the need for scalable platform solutions. This is accelerating demand for smart charging, energy optimization, and network management software worldwide.

- Smart Grid and V2G Energy Management: Smart grid and V2G energy management are enabling chargers to balance electricity demand, optimize charging schedules, and reduce grid stress. V2G capabilities allow EVs to return power to the grid during peak demand, creating new revenue opportunities for fleet operators and charging networks. This increases demand for software that manages real-time energy flows, pricing, battery health, and grid communication. Growing renewable energy integration further supports adoption of smart charging management platforms.

- Fleet Electrification and Depot Uptime Optimization: Fleet electrification and depot uptime optimization are driving the market as fleet operators need reliable, scheduled, and cost-efficient charging for buses, trucks, taxis, and delivery vehicles. Software platforms help manage charging queues, monitor charger performance, reduce downtime, and optimize energy costs during off-peak hours. They also support route planning, battery health tracking, and preventive maintenance. As commercial fleets scale, demand for centralized depot charging management solutions is increasing.

Market Restraints

- High Platform Implementation Cost: High platform implementation cost is hampering the market as operators need to invest in software licenses, hardware integration, cloud infrastructure, cybersecurity, and maintenance. Small charging networks and fleet operators may delay adoption due to limited budgets. Integration with chargers, payment systems, energy management tools, and grid platforms further increases deployment complexity and cost. This can slow platform adoption, especially in emerging markets and smaller charging networks.

- Cybersecurity Vulnerability of Grid-Connected CPMS: Cybersecurity vulnerability of grid-connected CPMS (Charging Point Management System) is hampering the market as charging platforms are linked with payment systems, user data, chargers, utilities, and grid networks. Any cyberattack can disrupt charging operations, manipulate energy flows, expose customer information, or create grid stability risks. This increases the need for stronger encryption, access control, monitoring, and compliance, raising implementation costs. As a result, some operators may delay large-scale CPMS deployment due to security and risk concerns.

Market Opportunities

- AI-Powered Autonomous Charging Optimization: AI-powered autonomous charging optimization enabling real-time decisions on charging schedules, energy pricing, load balancing, and charger availability. It helps operators reduce electricity costs, prevent grid overload, improve charger utilization, and enhance user experience. In May 2025, Noodoe introduced an AI-powered charging management system to support next-generation transportation. Highlighted in an AWS case study, its AI Advisor uses generative AI to optimize charging station pricing, improve revenue, increase station utilization, and support future autonomous vehicle integration.

- Mobility-as-a-Service Integration: MaaS integration linking EV charging platforms with ride-hailing, car-sharing, public transport, and fleet mobility systems. This enables seamless route planning, charger booking, payments, and real-time charging availability within mobility apps. As cities promote shared and electric mobility, CPMS providers can expand into integrated digital transport ecosystems. This supports higher charger utilization and better customer experience.

Market Challenges

- Grid Capacity Constraints and Peak-Load Management Challenges: Grid capacity constraints and peak-load management challenges are creating difficulties as large numbers of EVs charging simultaneously can strain local electricity networks. Charging operators must invest in advanced software to balance loads, schedule charging sessions, and prevent grid overloads. Variations in renewable energy generation and electricity demand further increase operational complexity. These challenges can raise infrastructure costs and slow the expansion of large-scale charging networks.

- Data Privacy and User Authentication Concerns: Data privacy and user authentication concerns challenge the market as CPMS platforms handle sensitive user data, payment details, charging behavior, and vehicle information. Weak authentication or poor data protection can expose users to fraud, identity theft, and unauthorized access. Compliance with privacy regulations also increases operational and software development costs. As a result, operators must invest in secure login systems, encryption, and data governance, which can slow platform deployment.

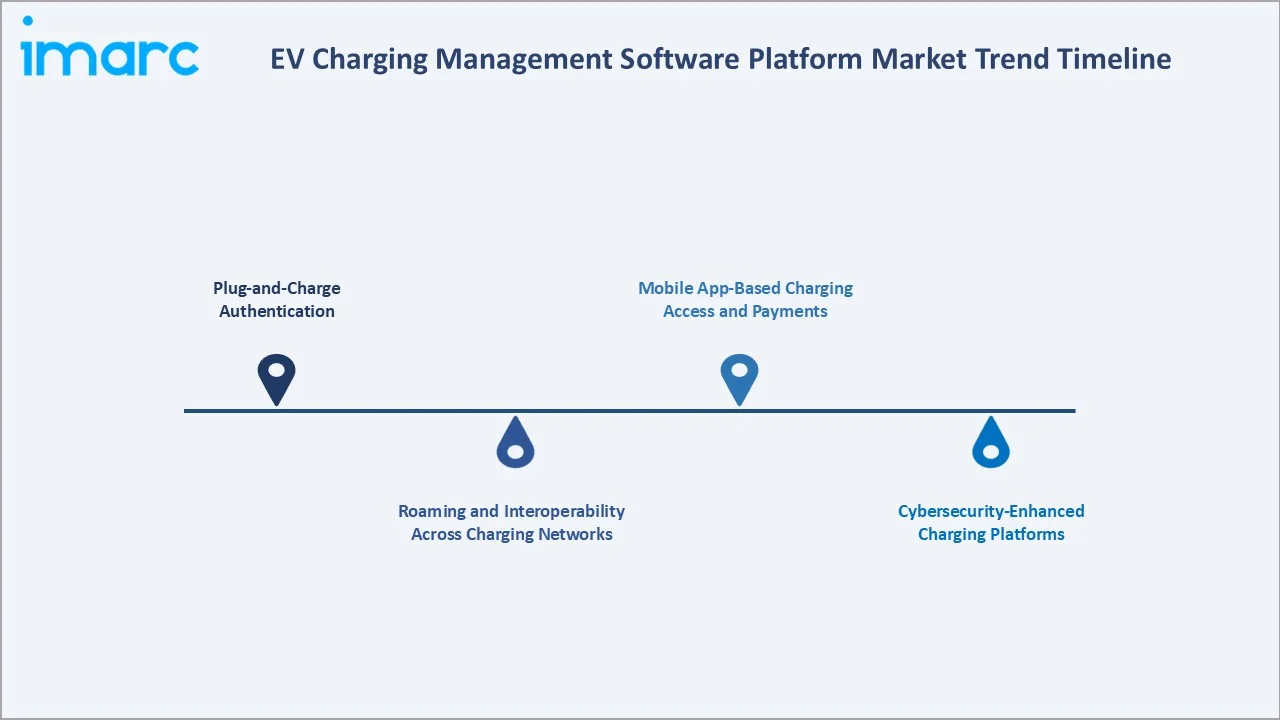

Emerging Market Trends

1. Plug-and-Charge Authentication

Plug-and-charge authentication is emerging as a key trend as it allows EV users to start charging automatically by simply connecting the vehicle to the charger. It improves user convenience by removing the need for apps, RFID cards, or manual payment steps. In April 2026, Hubject, Mer, and BMW Group launched Plug&Charge Direct in Germany and Austria, enabling automated EV charging authentication with direct credit card payment. The service simplifies the charging process by combining secure vehicle recognition and payment into one seamless flow for EV drivers. This trend is supporting more seamless, secure, and scalable EV charging network operations.

2. Roaming and Interoperability Across Charging Networks

Roaming and interoperability across charging networks are emerging as EV users need seamless access to chargers operated by different providers. CPMS platforms enable cross-network authentication, billing, charger availability visibility, and payment settlement. This improves user convenience and reduces range anxiety during long-distance travel. As charging networks expand, interoperability is becoming essential for scalable and connected EV charging ecosystems.

3. Cybersecurity-Enhanced Charging Platforms

Cybersecurity-enhanced charging platforms are emerging as EV chargers become connected to payment systems, user accounts, vehicles, and power grids. CPMS providers are adding encryption, secure authentication, threat monitoring, and access controls to prevent data breaches and operational disruption. This is especially important for public charging networks and fleet depots with high transaction volumes. As EV infrastructure scales, cybersecurity is becoming a core feature of reliable charging management software.

4. Mobile App-Based Charging Access and Payments

Mobile app-based charging access and payments are emerging as EV users prefer convenient charger discovery, booking, authentication, and payment through smartphones. CPMS platforms are integrating mobile apps to show real-time charger availability, pricing, charging status, and digital receipts. In February 2026, A-1 Sureja Industries introduced the “Yellow EV” mobile app to improve management of its electric two-wheeler operations. Aligned with its digital-first approach, the app supports onboarding, service coordination, workflow management, operational efficiency, and customer engagement. This improves user experience and supports cashless, contactless transactions. As public charging networks expand, mobile app integration is becoming essential for customer engagement and network utilization.

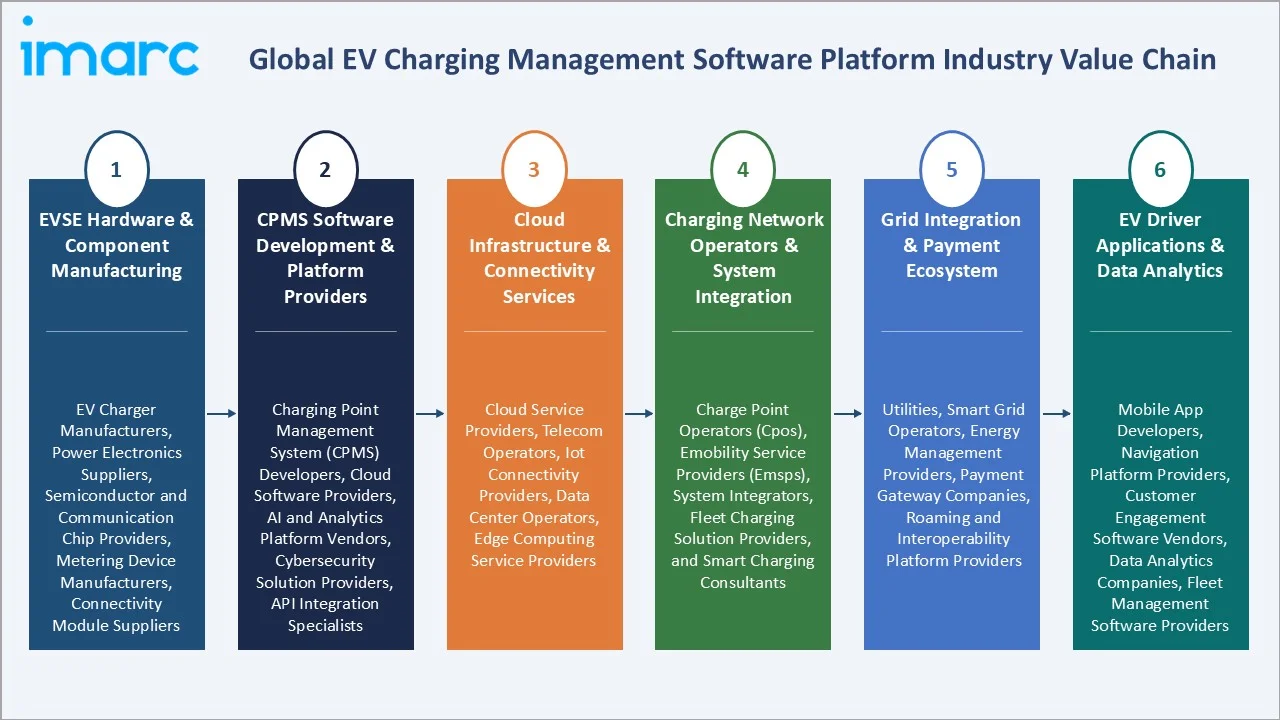

Industry Value Chain Analysis

The EV charging management software platform value chain integrates EVSE hardware & component manufacturing, CPMS software development & platform providers, cloud infrastructure & connectivity services, charging network operators & system integration, grid integration & payment ecosystem, and EV driver applications & data analytics.

|

Stage |

Key Participants |

|

EVSE Hardware & Component Manufacturing |

EV charger manufacturers, power electronics suppliers, semiconductor and communication chip providers, metering device manufacturers, connectivity module suppliers |

|

CPMS Software Development & Platform Providers |

Charging Point Management System (CPMS) developers, cloud software providers, AI and analytics platform vendors, cybersecurity solution providers, API integration specialists |

|

Cloud Infrastructure & Connectivity Services |

Cloud service providers, telecom operators, IoT connectivity providers, data center operators, edge computing service providers |

|

Charging Network Operators & System Integration |

Charge Point Operators (CPOs), eMobility Service Providers (eMSPs), system integrators, fleet charging solution providers, and smart charging consultants |

|

Grid Integration & Payment Ecosystem |

Utilities, smart grid operators, energy management providers, payment gateway companies, roaming and interoperability platform providers |

|

EV Driver Applications & Data Analytics |

Mobile app developers, navigation platform providers, customer engagement software vendors, data analytics companies, fleet management software providers |

CPMS software development & platform providers represent the most value-added stage in the EV charging management software platform value chain, as they enable charger monitoring, network management, smart charging, billing, interoperability, energy optimization, AI-driven analytics, and seamless user experiences across charging ecosystems.

Technology Landscape in the EV Charging Management Software Platform Industry

AI and Machine Learning in CPMS

AI and machine learning are enabling predictive analytics, intelligent load balancing, and automated charging optimization. These technologies help operators forecast charging demand, optimize energy consumption, and improve charger utilization rates. AI-driven platforms can also detect equipment faults early, support predictive maintenance, and enhance user experience through dynamic pricing and personalized charging recommendations. As charging networks expand, AI and ML are becoming essential for efficient, scalable, and data-driven charging operations.

Ultra-Fast Charging

Ultra-fast charging is increasing the need for advanced power management, real-time monitoring, and intelligent load balancing capabilities. CPMS platforms are being enhanced to manage high-power chargers efficiently, optimize energy distribution, and minimize grid congestion during peak usage. In March 2026, SK Signet introduced its new 400kW all-in-one ultra-fast EV charger. The next-generation charger uses high-density silicon carbide (SiC) power modules and a high-efficiency power design to improve both energy efficiency and space utilization. These systems also support predictive maintenance and dynamic pricing to maximize charger uptime and profitability. As demand grows for faster charging experiences, software platforms are evolving to support large-scale ultra-fast charging networks with greater reliability and efficiency.

Renewable Energy and Battery Storage Integration

Renewable energy and battery storage integration enable chargers to utilize solar, wind, and stored energy more efficiently. CPMS platforms help manage energy flows, optimize charging schedules, and reduce dependence on the grid during peak demand periods. Battery storage systems support load balancing, improve charging reliability, and lower electricity costs for operators. As sustainability goals and renewable energy adoption increase, software platforms are incorporating advanced energy management capabilities to maximize operational efficiency and carbon reduction.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Module |

Operation Management |

32.6% |

2025 |

|

Deployment |

Public Chargers |

72.6% |

2025 |

|

Charger Type |

Level 2 |

53.2% |

2025 |

|

Application |

Commercial |

82.6% |

2025 |

|

Region |

North America |

30.0% |

2025 |

By Module

Operation management leads at 32.6% (2025). CPMS operation management encompasses charge point monitoring, remote diagnostics, uptime reporting, and firmware management.

To access detailed market analysis, Request Sample

Energy management at 27.4% encompasses load balancing, dynamic scheduling, V2G control, demand-response integration, and renewable energy optimization. EV billing and payment at 21.8% encompasses session billing, plug & charge, roaming settlement, dynamic pricing, and subscription management. Others at 18.2% include analytics and reporting, driver mobile app, and fleet telematics integration.

By Deployment

Public chargers lead at 72.6% (2025), through government-mandated public charging network deployment across highways, urban centers, and retail locations, creating CPMS's most commercial procurement channel.

Private chargers at 27.4% grow fastest at ~31.2% CAGR through fleet depot, workplace, and multi-family residential CPMS deployment.

Regional Market Insights

|

Region |

Share (2025) |

Key EV Charging Management Software Platform Market Drivers & Characteristics |

|

North America |

30.0% |

Driven by strong EV adoption, extensive public charging network expansion, fleet electrification initiatives, and significant investments in smart charging and grid integration technologies. |

|

Asia Pacific |

29.4% |

Benefits from rapid EV deployment, large-scale charging infrastructure development, supportive government policies, and growing demand for cloud-based charging management solutions. |

|

Europe |

24.6% |

Driven by stringent emission regulations, widespread EV adoption, cross-border charging interoperability initiatives, and increasing investments in smart charging and renewable energy integration. |

|

Latin America |

8.2% |

Witnessing growing demand for charging management platforms as EV adoption increases, supported by urban electrification programs, public charging investments, and the expansion of sustainable mobility initiatives. |

|

Middle East |

4.1% |

Supported by smart city projects, government-led sustainability programs, EV infrastructure investments, and rising demand for intelligent charging network management solutions. |

|

Africa |

3.7% |

Gradually expanding with the emergence of EV mobility initiatives, pilot charging infrastructure projects, renewable energy integration, and increasing interest in digital charging management platforms. |

North America's 30.0%, supported by strong EV adoption, extensive charging infrastructure investments, and advanced smart charging technologies. Asia Pacific's 29.4% driven by large-scale EV deployment and rapid charging network expansion, particularly in China. Europe's 24.6% reflects stringent emission regulations, high EV penetration, and growing interoperability initiatives.

Latin America's 8.2%, the Middle East's 4.1%, and Africa's 3.7% are emerging markets benefiting from rising electrification efforts, sustainability programs, and increasing investments in EV charging infrastructure.

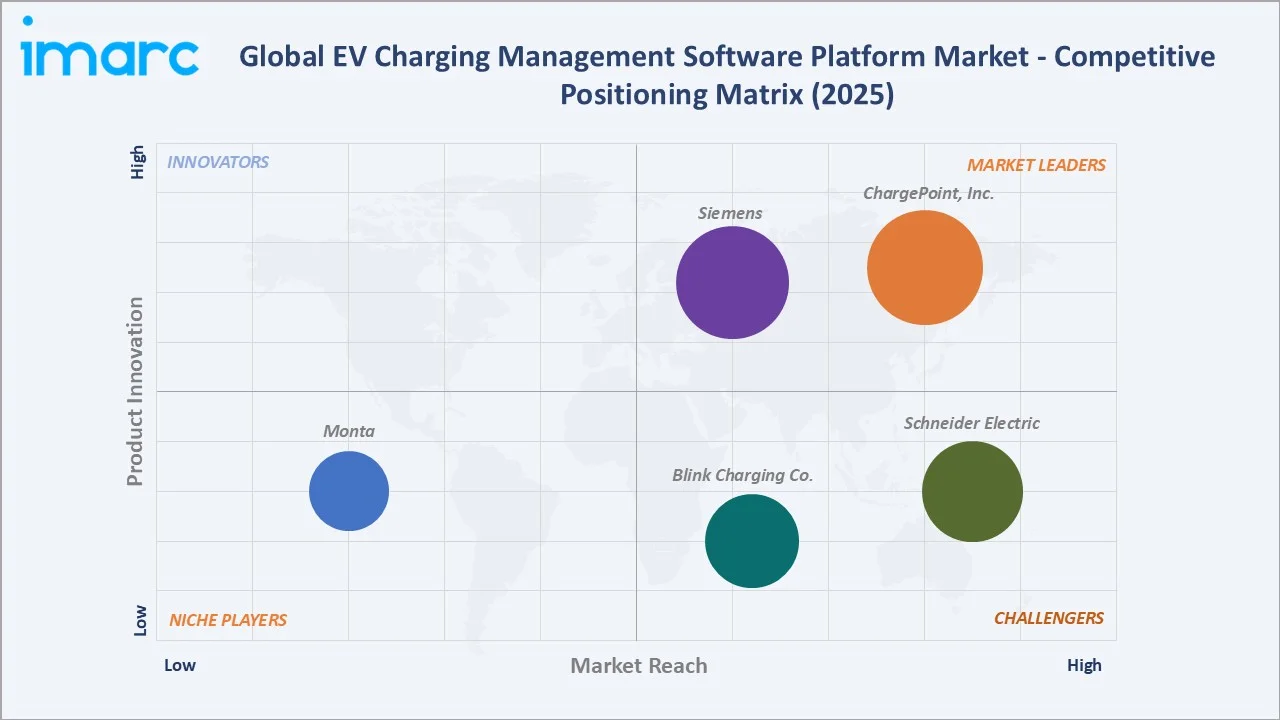

Competitive Landscape

The EV charging management software platform's competitive landscape is commercially stratified between vertically integrated hardware-software companies, pure-play software CPMS vendors, and energy company CPMS platforms.

|

Company |

Key Platforms |

Market Position |

Core Strength |

|

ChargePoint, Inc. |

ChargePoint Platform |

Market Leader |

ChargePoint, Inc. provides a comprehensive, cloud-native EV charging management software platform designed to manage, monitor, and optimize charging operations for businesses, fleets, and drivers. |

|

Siemens |

eMobility software |

Market Leader |

Siemens provides comprehensive, IoT-enabled EV charging management software designed for public, workplace, and depot applications, focusing on maximizing uptime, energy efficiency, and intelligent load balancing. |

|

Schneider Electric |

EcoStruxure EV Charging Expert |

Strong Challenger |

Schneider Electric plays a central role in EV charging management software by providing intelligent, energy-efficient solutions through the platform, EcoStruxure EV Charging Expert. |

|

Blink Charging Co. |

Blink Network |

Strong Challenger |

Blink Charging Co. plays a central role in EV charging management through its proprietary, cloud-based Blink Network, which operates, monitors, and tracks charging stations, data, and payment processing. |

|

Monta |

Monta Hub |

Niche Player |

Monta is an end-to-end EV charging management platform that acts as an operating system connecting EV drivers, site owners, and charge point operators (CPOs). |

The competitive landscape is being reshaped by three forces: white-label platform commoditization, AI differentiation, and energy company market entry.

Key Company Profiles

ChargePoint, Inc.

ChargePoint, Inc. is one of the leading providers of EV charging solutions and charging management software platforms globally. The company offers a comprehensive cloud-based charging point management system (CPMS) that enables charge point operators, fleet managers, businesses, and property owners to monitor, manage, optimize, and monetize EV charging networks.

- Key Platform: ChargePoint Platform.

- Recent Developments: In November 2025, ChargePoint introduced a next-generation ChargePoint Platform, a flexible software solution designed to transform EV charging operations. Built from the ground up, the platform helps operators optimize charging infrastructure across single sites or global networks while enabling smooth integration with evolving energy systems.

- Strategic Focus: Expanding its cloud-based charging point management system (CPMS) capabilities to improve charger monitoring, network management, analytics, and operational efficiency.

Schneider Electric

Schneider Electric is a global leader in energy management, automation, and sustainable infrastructure solutions, with a growing presence in the EV charging management software platform market. Through its EcoStruxure platform and global partner network, Schneider Electric remains a key participant in the evolving EV charging ecosystem.

- Key Platforms: EcoStruxure EV Charging Expert.

- Strategic Focus: Expanding its smart EV charging management capabilities through the EcoStruxure platform, enabling real-time monitoring, control, and optimization of charging infrastructure.

Market Concentration Analysis

The EV charging management software platform market is moderately concentrated, with a mix of global technology providers, charging network operators, and specialized software vendors competing for market share. Market competition is increasingly driven by advancements in AI-enabled charging optimization, interoperability, fleet charging management, and smart energy integration. At the same time, emerging CPMS providers are gaining traction by offering cloud-native, scalable, and white-label solutions tailored to regional charging operators. Strategic collaborations, acquisitions, and investments in smart charging technologies continue to shape the competitive landscape.

Investment & Growth Opportunities

Highest Growth Segments

EV billing and payment (~32.4% CAGR), private/fleet CPMS (~31.2% CAGR), energy management/V2G (~31.8% CAGR through grid services), AI-powered CPMS premium tier (~35-40% CAGR from a smaller base through predictive analytics), Asia Pacific CPMS (~32-34% CAGR through China and India EV mandate), and MaaS-CPMS API integration (~28-32% CAGR through ride-sharing fleet EV transition) represent the highest-growth CPMS investment vectors through 2034.

Investment Themes

- V2G-integrated fleet depot CPMS for logistics operators: Electric fleet depots requiring V2G-capable CPMS, creating additional grid-services revenue beyond charging fees through large fleet batteries can act as grid-stabilization assets. Investment in V2G-integrated fleet depot CPMS with demand-response API creates fleet depot's premium pricing.

- AI CPMS analytics SaaS for CPO network optimization: AI CPMS analytics SaaS for CPO network optimization is emerging as charging network operators seek data-driven tools to improve charger utilization, energy efficiency, and revenue generation. AI-powered analytics platforms enable predictive maintenance, dynamic pricing, demand forecasting, and real-time load balancing across charging networks. As EV infrastructure scales globally, investors are increasingly focusing on SaaS-based CPMS solutions that offer recurring revenue models, operational efficiency, and scalable network optimization capabilities.

Future Market Outlook (2026-2034)

The EV charging management software platform market is projected to grow from USD 1.97 Billion in 2025 to USD 22.87 Billion by 2034, delivering a 30.35% CAGR over the forecast period. The market's anchor value of USD 7.43 Billion in 2030 represents the CPMS industry at a commercial maturity threshold. Fleet depot CPMS is expected to generate higher revenue per port than public CPO deployments due to higher utilization and energy-management requirements, AI-powered energy management replacing rule-based load balancing as standard deployment, and V2G energy trading creating CPMS's first above-charging-fee single energy revenue stream at commercial scale.

Three structural forces define the CPMS market through 2034: exponential EV deployment creating above-linear CPMS demand through each new charge point requiring CPMS subscription, CPMS intelligence premium above hardware commodity through AI's continuous improvement energy optimization creating above-standard software premium justification for CPMS as an enterprise analytics platform, and V2G energy trading creating CPMS's new revenue model through energy arbitrage, demand-response payment, and capacity market participation.

Research Methodology

Primary Research

Primary research comprised structured interviews and discussions with key stakeholders across the EV charging management software platform ecosystem, including charge point operators (CPOs), e-mobility service providers (eMSPs), software platform vendors, EV charging infrastructure companies, fleet operators, and utility providers.

Secondary Research

Secondary research encompassed company websites, annual reports, investor presentations, product brochures, EV charging software white papers, and industry publications. It also included government EV policy documents, charging infrastructure databases, regulatory frameworks, smart grid reports, and news releases to validate market trends, technology adoption, competitive developments, and growth opportunities.

Forecasting Models

Market revenue forecasts developed using a managed port subscription model: Global public and private charge point installed base multiplied by CPMS adoption rate multiplied by average CPMS revenue per port per month.

EV Charging Management Software Platform Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Modules Covered | Operation Management, Energy Management, EV Billing and Payment, Others |

| Deployments Covered | Private Charges, Public Charges |

| Charger Types Covered | Level 1, Level 2, Level 3 |

| Applications Covered | Residential, Commercial |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | ChargePoint, Inc., Siemens, Schneider Electric, Blink Charging Co., Monta, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the EV charging management software platform market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global EV charging management software platform market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the EV charging management software platform industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the EV Charging Management Software Platform Market Report

The EV charging management software platform market reached USD 1.97 Billion in 2025, driven by rapid EV adoption, expanding public and fleet charging networks, and the need for centralized charger monitoring and control. Rising demand for smart charging, load balancing, payment management, and remote diagnostics is increasing platform adoption. Integration with renewable energy, battery storage, and smart grids is further supporting market growth.

The EV charging management software platform market grows at 30.35% CAGR during 2026-2034, reaching USD 22.87 Billion by 2034. The overall 30.35% CAGR reflects the market's exponential EV adoption driver, government infrastructure mandates, AI premium tier development, and V2G energy trading, creating CPMS's revenue growth trajectory through EVs' compounding hardware-to-software value migration.

Operation management leads at 32.6% through every CPO's above-optional single essential requirement for charge-point monitoring, remote diagnostics, and uptime reporting, creating the most commercially advanced CPMS module.

Public chargers lead at 72.6% through government-mandated public charging deployment, creating the most commercially CPMS procurement volume through public charging mandate requiring high annual public charging capital investment.

North America leads at 30.0% due to strong EV adoption, large-scale charging infrastructure investments, and advanced deployment of smart charging technologies. Supportive government funding, fleet electrification, and the presence of major charging network operators further strengthen regional growth.

Leading companies include ChargePoint, Inc., Siemens, Schneider Electric, Blink Charging Co., and Monta, among others.

The market is projected to reach approximately USD 7.43 Billion by 2030, with fleet depot CPMS surpassing public CPO CPMS as the largest single deployment revenue category, AI CPMS predictive maintenance tier, and Asia Pacific surpassing as the largest single CPMS market.

Three priority investment opportunities: V2G-integrated fleet depot CPMS for logistics fleet, white-label CPMS for energy retailer, and AI-powered CPMS predictive maintenance SaaS.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)