Extra Neutral Alcohol (ENA) Market in India Size, Share, Trends and Forecast by Application, and State, 2026-2034

India Extra Neutral Alcohol (ENA) Market Size, Share, Trends & Forecast (2026-2034)

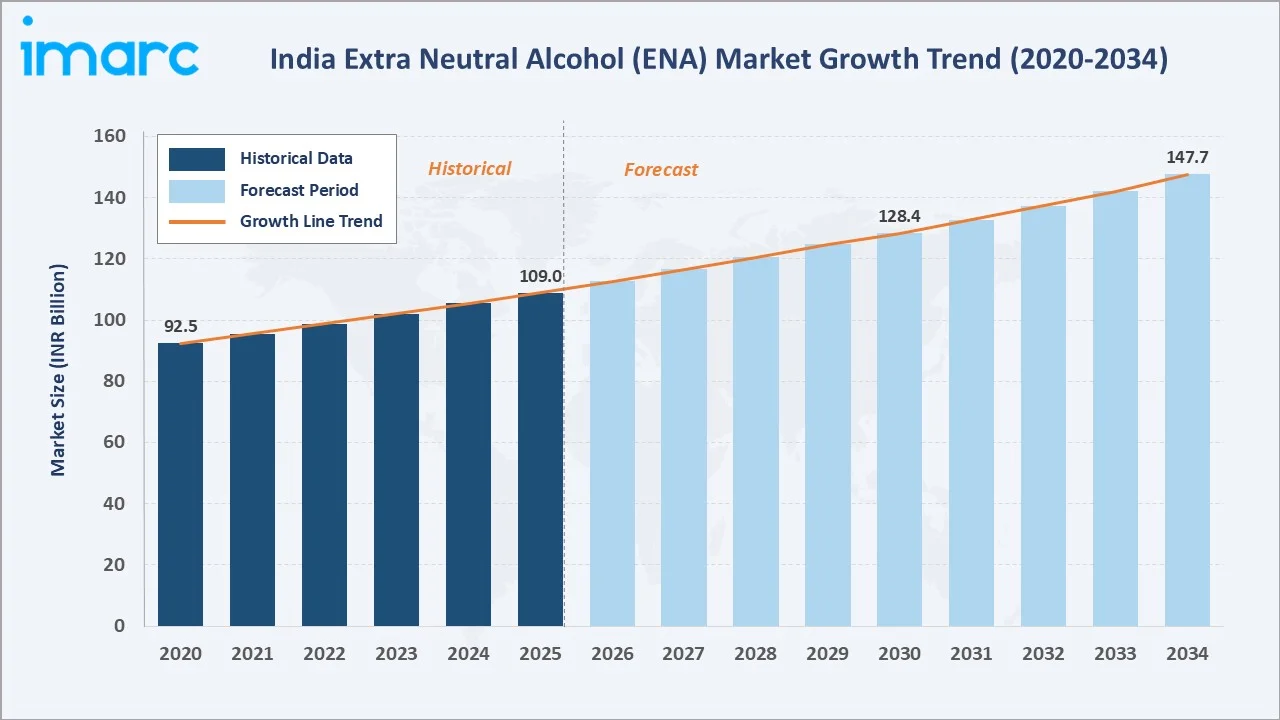

The India Extra Neutral Alcohol (ENA) market size was valued at INR 109.0 Billion in 2025 and is projected to reach INR 147.7 Billion by 2034, exhibiting a CAGR of 3.33% during the forecast period 2026-2034. The India ENA market growth is propelled by rising IMFL and premium spirits consumption, steady pharmaceutical and flavour-fragrance demand, surplus sugarcane availability, and supportive policies under India's Ethanol Blending Programme. Alcoholic beverages dominate at 62.8% share in 2025, while Punjab leads state-level production at 18.7% and Andhra Pradesh & Telangana leads consumption at 17.9%.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

INR 109.0 Billion |

|

Forecast Market Size (2034) |

INR 147.7 Billion |

|

CAGR (2026-2034) |

3.33% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Application |

Alcoholic Beverages (62.8%, 2025) |

|

Largest Producing State |

Punjab (18.7% production share, 2025) |

|

Largest Consuming State |

Andhra Pradesh & Telangana (17.9%, 2025) |

The India ENA market growth trajectory from 2020 through 2034 reflects a steady climb powered by rising IMFL volumes, expanding pharmaceutical usage, and the incremental shift toward grain-based and sugarcane-juice ENA routes under the country's ethanol policy framework.

To get more information on this market, Request Sample

Segment-level CAGR benchmarks highlight pharmaceuticals and Andhra Pradesh & Telangana as the fastest-growing categories within the India ENA market forecast through 2034, outpacing the blended 3.33% industry growth rate.

Executive Summary

The India Extra Neutral Alcohol (ENA) market is undergoing a structural evolution driven by rising IMFL consumption, growing premiumisation, and expanding industrial demand. Valued at INR 109.0 Billion in 2025, the market is forecast to reach INR 147.7 Billion by 2034 at a CAGR of 3.33%. Rising disposable incomes, urbanisation, and broader retail availability of premium spirits are the strongest growth anchors through 2034.

Alcoholic beverages command a dominant 62.8% share in 2025, driven by IMFL, whisky, vodka, rum, and gin production. Pharmaceuticals follow at 12.4%, supported by India's large generic formulations base. Flavours and fragrances contribute 9.6% while cosmetics hold 8.1%, reflecting steady industrial demand from domestic and export-oriented manufacturers.

Punjab leads state-level production with 18.7% share in 2025, followed by Uttar Pradesh (12.8%) and Maharashtra (11.4%). On the demand side, Andhra Pradesh & Telangana together account for 17.9% consumption share, the highest in the country, followed by Uttar Pradesh (12.6%) and Maharashtra (11.8%). The India ENA market outlook remains positive as premiumisation, pharma expansion, and expanding distillery capacity converge through 2034.

Key Market Insights

|

Insight |

Data |

|

Largest Application |

Alcoholic Beverages - 62.8% share (2025) |

|

Second Application |

Pharmaceuticals - 12.4% share (2025) |

|

Fastest Growing Application |

Pharmaceuticals - 4.2% CAGR (2026-2034) |

|

Largest Producing State |

Punjab - 18.7% production share (2025) |

|

Largest Consuming State |

Andhra Pradesh & Telangana - 17.9% share (2025) |

|

Leading Feedstock |

Molasses and grain-based distilleries dominate supply |

|

Key Players |

India Glycols Limited, Triveni Engineering & Industries Ltd., Pioneer Industries Private Limited, Radical Bio Organics Limited, Zenith Biochemical Industries Private Limited |

Key Analytical Observations Supporting the Above Data:

- Alcoholic beverages' 62.8% dominance in 2025 reflects India's position as one of the world's largest whisky markets. IMFL volumes have crossed 400 million cases annually, with ENA as the primary feedstock input for blended and premium whiskies.

- Pharmaceuticals' 12.4% share is supported by India's status as the world's third-largest generic drugs producer by volume, where ENA is a critical solvent and carrier in syrups, tinctures, and liquid formulations.

- Punjab's 18.7% production lead is anchored by grain-based distilleries operating on surplus wheat and rice stocks. Leading Punjab-based players include BCL Industries, Piccadily Agro, and Chadha Sugars, supplying both captive IMFL units and external buyers.

- Andhra Pradesh & Telangana's 17.9% consumption lead reflects one of the country's highest per-capita IMFL consumption zones, government-run retail distribution through TSBCL and APSBCL, and strong southern state revenue reliance on alcohol excise.

- Top 10 state concentration accounts for over 92% of India's ENA production and about 89% of consumption in 2025, indicating structurally concentrated supply and demand clusters.

- Ethanol Blending Programme (EBP) impact continues to tighten molasses availability for ENA producers. India achieved 15% ethanol blending in 2024 and is targeting 20% (E20) by 2025-26, creating feedstock competition between ENA and ethanol streams.

India ENA Market Overview

Extra Neutral Alcohol (ENA) is a high-purity distilled alcohol with a minimum strength of 96% alcohol by volume (ABV), used as a key raw material in alcoholic beverages, pharmaceuticals, cosmetics, flavours, fragrances, and industrial solvents. In India, ENA is predominantly produced from sugarcane molasses, though grain-based and sugarcane-juice-based routes are rising under the national ethanol programme. ENA production is regulated at both central and state levels, with each state controlling licensing, excise, and inter-state movement.

The industry operates at the convergence of agricultural policy, excise taxation, and industrial demand. Macroeconomic drivers include rising per-capita disposable incomes crossing INR 2.1 lakh in 2024 (MoSPI), urbanisation trends, and the expanding pharmaceutical and FMCG export base. The National Policy on Biofuels 2018 (amended 2022) and the push toward 20% ethanol blending by 2025-26 are reshaping feedstock economics, while state-level excise reforms continue to influence both production and inter-state distribution patterns.

Market Dynamics

To evaluate market opportunities, Request Sample

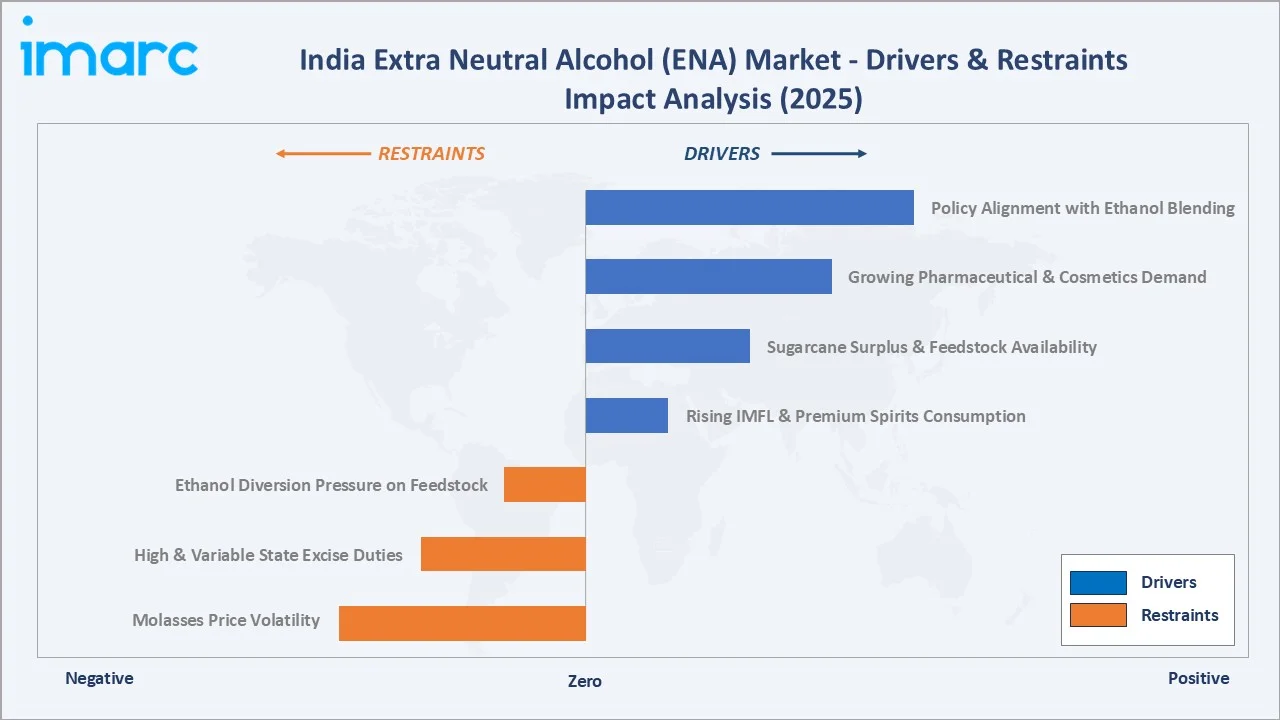

Market Drivers

- Rising IMFL and Premium Spirits Consumption: India's IMFL market crossed 400 million cases in 2024 per CIABC data, with whisky alone accounting for over 60% of the category. Premium and semi-premium segments are growing at pace annually, driving structural ENA demand from leading IMFL manufacturers.

- Sugarcane Surplus and Feedstock Availability: India crushed approximately 333 lakh tonnes of sugarcane in the 2023-24 season per ISMA, generating substantial molasses output. This feedstock base continues to anchor the country's 350+ licensed distilleries producing ENA and ethanol.

- Growing Pharmaceutical and Cosmetics Demand: India's pharmaceutical sector was valued at around USD 50 billion in 2024, and cosmetics at USD 15 billion. Both use ENA as a high-purity solvent, with steady volume growth annually supporting the non-beverage application base.

- Policy Alignment with Ethanol Blending Programme: India achieved 15% ethanol blending with petrol in 2024 and is progressing toward 20% by 2025-26. Shared distillery infrastructure between ENA and ethanol streams is driving large-scale capacity expansion among molasses and grain-based distilleries.

Urbanisation, rising spirits penetration in tier-2 and tier-3 cities, and premiumisation are reinforcing these drivers. Distillery players are committing multi-year capex programs to expand capacity, upgrade to multi-pressure distillation, and diversify feedstock between molasses and grain.

Market Restraints

- Ethanol Diversion Pressure on Feedstock: With molasses and sugarcane juice increasingly routed toward fuel ethanol under EBP, ENA producers face tighter input availability. Sugar season 2023-24 saw the Government of India partially restrict sugarcane juice for ethanol, reshaping feedstock economics sharply.

- High and Variable State Excise Duties: Excise duty on IMFL is often levied as a percentage of manufacturing (ex-distillery) cost or via state-specific structures. This creates pricing distortions and limits cross-state supply optimisation.

- Molasses Price Volatility: Molasses prices surged from approximately INR 600-700 per quintal in 2020 to over INR 1,400 per quintal in 2024, squeezing distillery margins. The volatility is directly linked to sugar output cycles and state policy interventions.

Market Opportunities

- Grain-Based and Broken-Rice ENA Expansion: FCI allocations of surplus rice to distilleries, combined with expanding grain-based capacity in Punjab, Haryana, and UP, are opening a structural growth route. Grain-based ENA is projected to grow at above-market CAGR through 2030.

- Export-Oriented Pharma-Grade ENA: Indian pharma-grade ENA exports, particularly to the EU and Africa, present a growing premium-margin opportunity. Compliance with USP, EP, and BP specifications is becoming a strategic differentiator for domestic producers.

Market Challenges

- Inter-State Movement Restrictions: Each state restricts import and export of ENA under its own excise rules, creating fragmented logistics. Permits, transport passes, and varying inspection protocols add working-capital and compliance costs for pan-India suppliers.

- Regulatory Uncertainty on Taxation: The GST Council's October 2023 decision kept ENA for alcoholic beverages outside GST, retaining state VAT, while industrial ENA moved under GST. Ongoing clarifications at state level continue to affect pricing and compliance strategies.

- Environmental and Effluent Management: Distillery spent wash management, CPCB zero-liquid-discharge (ZLD) mandates, and rising compliance costs are key operational challenges, particularly for smaller and mid-sized producers across central and eastern India.

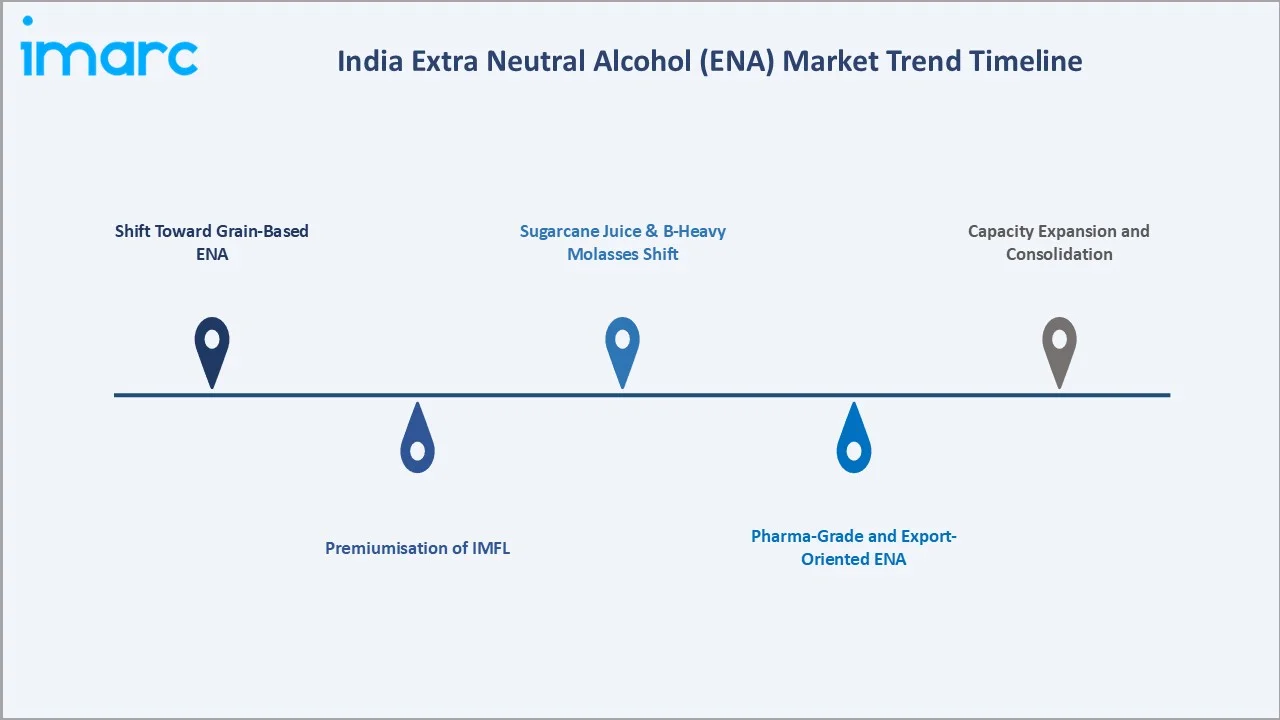

Emerging Market Trends

1. Shift Toward Grain-Based ENA

Grain-based distilleries are expanding rapidly in India, with maize emerging as a leading ethanol feedstock and driving a shift in the feedstock mix. Increased capacity additions across key states such as Punjab, Haryana, and Uttar Pradesh are supporting this transition, as grain-based production gains a larger share of overall output.

2. Premiumisation of IMFL

Premium whisky, single malts, craft gins, and super-premium vodkas are driving higher-grade ENA consumption. Diageo-owned United Spirits, Pernod Ricard India, and Radico Khaitan report double-digit volume growth in their premium portfolios through 2024, translating to steady premium-grade ENA demand.

3. Pharma-Grade and Export-Oriented ENA

Pharma-grade ENA meeting USP, EP, and BP specifications is emerging as a higher-margin category. India’s ENA and ethanol production is largely directed toward domestic consumption, particularly for fuel blending and beverage applications, with exports remaining limited and opportunistic rather than a major demand driver.

4. Sugarcane Juice and B-Heavy Molasses Shift

Policy incentives under the National Biofuels Policy are pushing distilleries toward B-heavy molasses and sugarcane juice routes. While primarily aimed at ethanol, these shifts are reshaping the ENA feedstock pool and pricing across the 2022-2030 window.

5. Capacity Expansion and Consolidation

Leading players such as India Glycols Limited, Triveni Engineering & Industries Ltd., Pioneer Industries Private Limited are actively expanding their distillation capacities to meet rising demand. At the same time, smaller regional distilleries are facing consolidation pressure due to increasing compliance requirements and higher working-capital intensity.

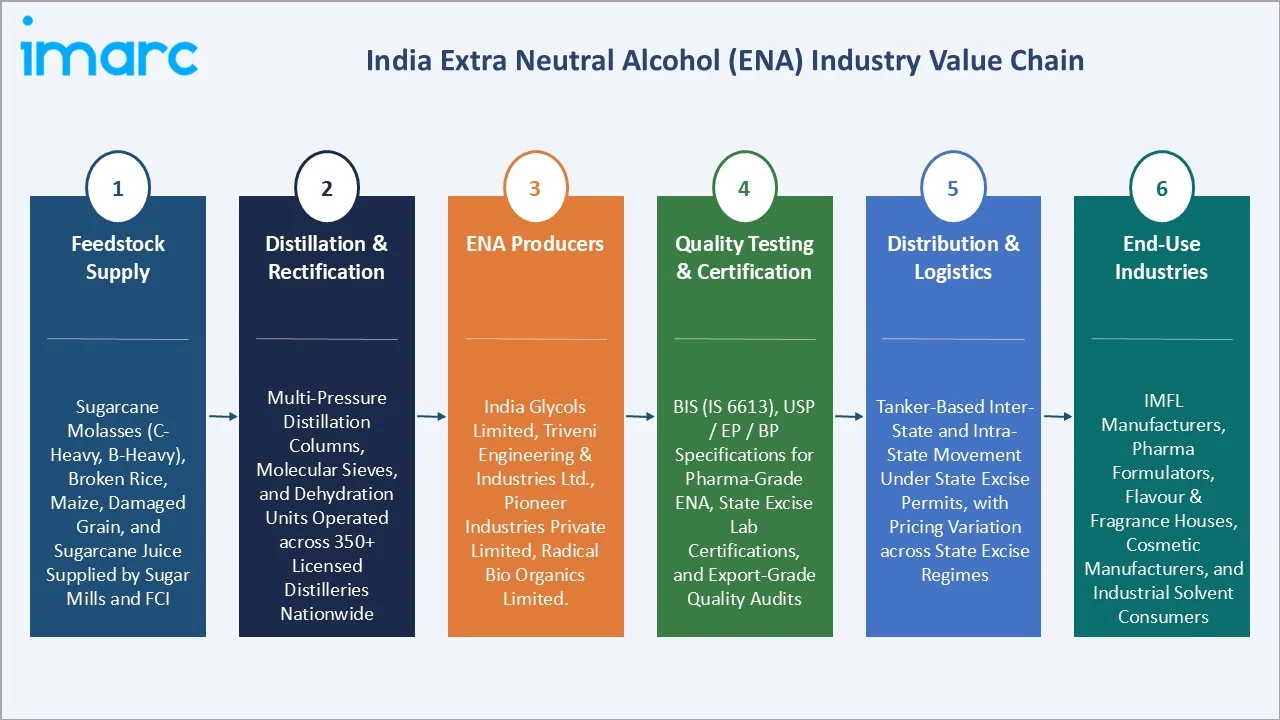

Industry Value Chain Analysis

The India ENA value chain spans six integrated stages from feedstock supply through end-use consumption. Each stage presents distinct competitive dynamics, policy exposure, and margin profiles relevant to the overall India ENA market analysis.

|

Value Chain Stage |

Key Participants / Description |

|

Feedstock Supply |

Sugarcane molasses (C-heavy, B-heavy), broken rice, maize, damaged grain, and sugarcane juice supplied by sugar mills and FCI |

|

Distillation & Rectification |

Multi-pressure distillation columns, molecular sieves, and dehydration units operated across 350+ licensed distilleries nationwide |

|

ENA Producers |

India Glycols Limited, Triveni Engineering & Industries Ltd., Pioneer Industries Private Limited, Radical Bio Organics Limited, Zenith Bio Chemical Industries Private Limited |

|

Quality Testing & Certification |

BIS (IS 6613), USP / EP / BP specifications for pharma-grade ENA, state excise lab certifications, and export-grade quality audits |

|

Distribution & Logistics |

Tanker-based inter-state and intra-state movement under state excise permits, with pricing variation across state excise regimes |

|

End-Use Industries |

IMFL manufacturers, pharma formulators, flavour & fragrance houses, cosmetic manufacturers, and industrial solvent consumers |

Integrated sugar-and-distillery players capture the highest value by combining feedstock security with distillation scale. Meanwhile, grain-based standalone distilleries are emerging as high-margin specialists, particularly in northern India, reshaping economics from legacy molasses-centric models to a diversified, policy-aligned portfolio.

Technology Landscape in the India ENA Industry

Multi-Pressure Distillation Technology

Multi-pressure distillation columns have become the industry standard, replacing conventional atmospheric columns. Advanced distillation technologies, including heat-integrated and multi-column configurations, are improving energy efficiency by reducing steam consumption. At the same time, ethanol purification is constrained by the azeotropic limit at around 96% alcohol by volume, which defines the standard purity level for ENA without additional dehydration steps.

Molecular Sieve Dehydration

Molecular sieve units are widely adopted across distilleries producing both ENA and fuel ethanol, enabling flexible switching between product streams. Capacity additions under the ethanol blending program have accelerated the installation of large-scale dehydration systems, with leading players significantly expanding their processing capabilities in recent years.

Feedstock Flexibility and Dual-Feed Plants

Dual-feed distilleries capable of processing both molasses and grain are increasingly standard. This feedstock flexibility helps producers manage molasses availability swings and policy-driven shifts, with over 60 dual-feed plants operating across India in 2025, up from fewer than 20 in 2020.

Effluent Management and Zero Liquid Discharge

CPCB-mandated zero-liquid-discharge (ZLD) compliance has driven installation of spent-wash concentration, incineration boilers, and bio-composting systems. Capex on ZLD systems represents approximately 15-20% of a modern distillery project cost, with leading producers reporting 100% ZLD compliance by 2024.

Market Segmentation Analysis

IMARC Group provides an analysis of the key trends in each segment of the India ENA market, along with forecasts at the state and country level from 2026 to 2034. The market has been categorised by application, with state-level production and consumption analysed under the Regional Market Insights section that follows.

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Production | Punjab | 18.7% | 2025 |

| Consumption | Andhra Pradesh and Telangana | 17.9% | 2025 |

| Application | Alcoholic Beverages | 62.8% | 2025 |

By Application

Alcoholic beverages dominate the India ENA market with a 62.8% share in 2025. IMFL (whisky, rum, vodka, gin, brandy) forms the largest downstream demand pool, supported by country-liquor production in select states. India's IMFL volumes crossed 400 million cases in 2024, with whisky alone accounting for most share of the category, translating into sustained high-volume ENA offtake from major IMFL manufacturers.

_market_charts-6.webp)

To access detailed market analysis, Request Sample

Pharmaceuticals account for 12.4% of application demand in 2025 and are the fastest-growing non-beverage category, advancing at an estimated 4.2% CAGR through 2034. ENA is used as a critical solvent, carrier, and preservative in syrups, tinctures, and liquid formulations. India's USD 50 billion pharmaceutical sector, anchored by the top 10 formulators including Sun Pharma, Dr. Reddy's, and Cipla, provides durable volume support.

Flavours & fragrances contribute 9.6% of demand, driven by domestic FMCG majors and F&F houses such as Givaudan, Firmenich, and S H Kelkar operating across Mumbai, Pune, and Bengaluru. Cosmetics account for 8.1%, supported by India's rapidly expanding personal-care market with brands such as Hindustan Unilever, Godrej Consumer, and Dabur. The Others segment at 7.1% spans industrial solvents, printing inks, sanitisers, and specialty chemical applications, providing residual but stable demand.

Regional Market Insights

Since India is the single national market for this report, regional insights are analysed at state level across both production and consumption. India's ENA landscape is highly concentrated, with the top 10 states accounting for over 92% of national production and around 89% of national consumption in 2025, reflecting deeply rooted feedstock geography, distillery clustering, and state excise regimes.

Production Share by State

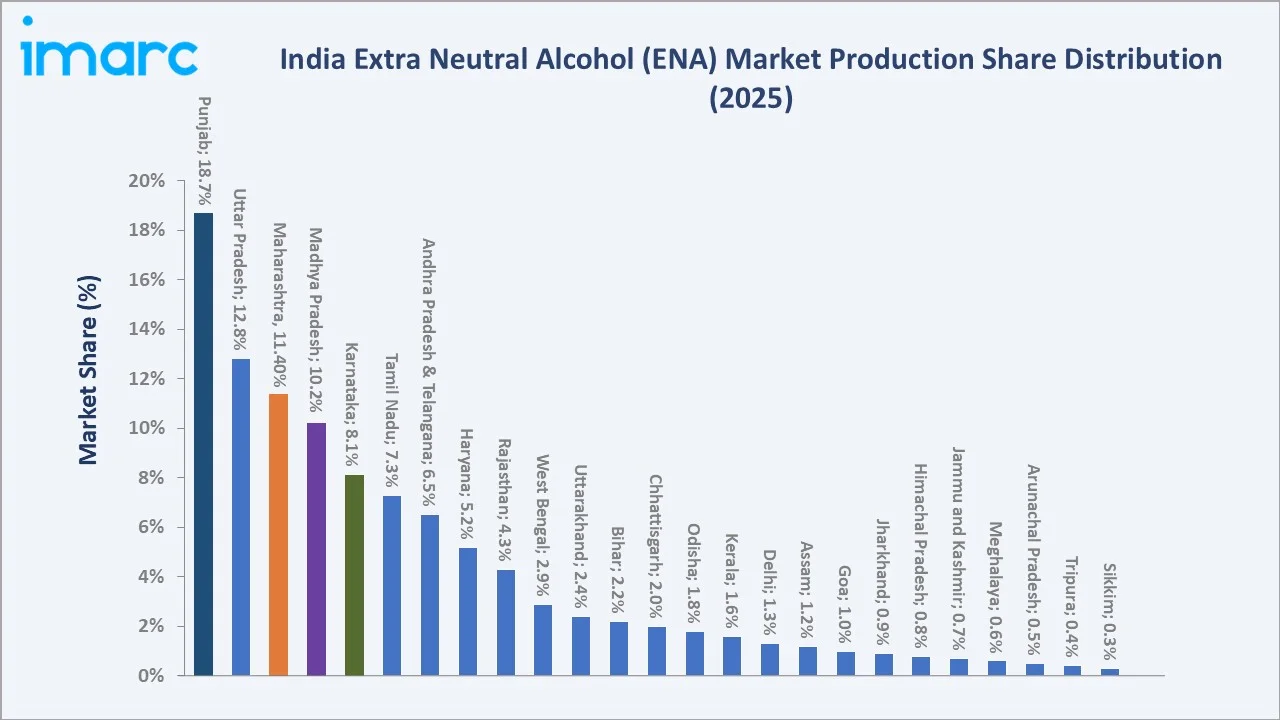

State-level production is anchored in the sugarcane and grain belts of northern and western India. Punjab leads national production at 18.7% share in 2025, driven by large grain-based distilleries operating on surplus rice and wheat stocks. Uttar Pradesh follows at 12.8%, supported by one of India's largest sugar and molasses bases, while Maharashtra's 11.4% share reflects both molasses-based and grain-based capacity across western Maharashtra.

|

State (Production) |

Share (2025) |

Key Production Drivers |

|

Punjab |

18.7% |

Grain-based distilleries on surplus rice/wheat, strong IMFL linkages |

|

Uttar Pradesh |

12.8% |

Largest sugar-molasses base in India, dual-feed distilleries |

|

Maharashtra |

11.4% |

Integrated sugar-distillery cluster across western Maharashtra |

|

Madhya Pradesh |

10.2% |

Grain-based capacity, low-cost distillery economics |

|

Karnataka |

8.1% |

South India's leading molasses-based distillery hub |

|

Tamil Nadu |

7.3% |

EID Parry-led sugar-distillery integration |

|

Andhra Pradesh & Telangana |

6.5% |

State-run and private distilleries serving regional IMFL |

|

Haryana |

5.2% |

Grain-based distilleries, proximity to Delhi-NCR demand |

|

Rajasthan |

4.3% |

Emerging distillery base, grain-based capacity growth |

|

West Bengal |

2.9% |

Smaller molasses-based distilleries, IFB Agro clusters |

|

Uttarakhand |

2.4% |

Grain-based distilleries supported by tax-favorable industrial policy |

|

Bihar |

2.2% |

ENA produced for inter-state supply despite state prohibition on consumption |

|

Chhattisgarh |

2.0% |

Grain-based distilleries leveraging local rice surplus |

|

Odisha |

1.8% |

Molasses-based units with incremental grain-based capacity additions |

|

Kerala |

1.6% |

Limited molasses-based capacity catering to state-controlled IMFL demand |

|

Delhi |

1.3% |

Small-scale, demand-led production for the NCR market |

|

Assam |

1.2% |

Northeast molasses-based hub serving regional IMFL demand |

|

Goa |

1.0% |

Tourism-driven spirits demand, niche local distillery capacity |

|

Jharkhand |

0.9% |

Small grain-based distillery footprint |

|

Himachal Pradesh |

0.8% |

Limited grain-based units serving hill-state demand |

|

Jammu and Kashmir |

0.7% |

Modest molasses/grain capacity for regional supply |

|

Meghalaya |

0.6% |

Marginal Northeast production, primarily for local IMFL demand |

|

Arunachal Pradesh |

0.5% |

Marginal Northeast production, state-level demand |

|

Tripura |

0.4% |

Marginal Northeast capacity, limited installed base |

|

Sikkim |

0.3% |

Smallest installed capacity, niche local supply |

Consumption Share by State

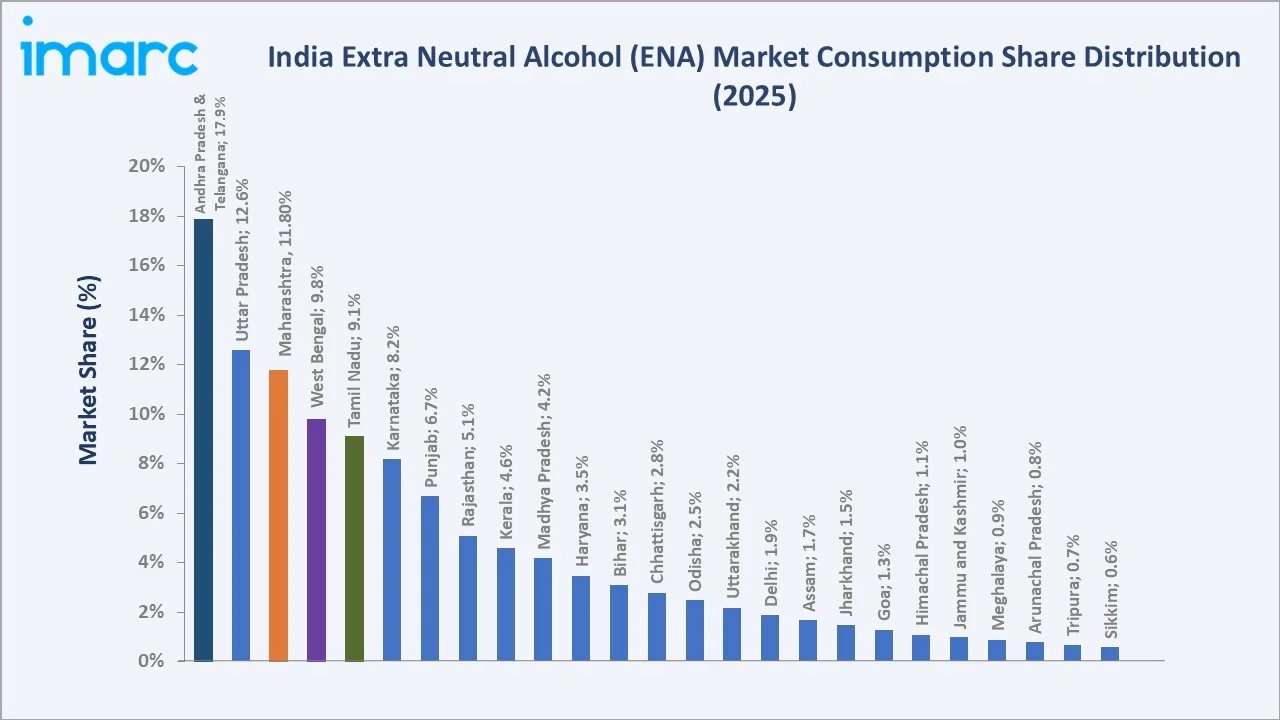

Consumption patterns differ meaningfully from production, reflecting state-wise IMFL retail markets, country-liquor frameworks, and excise-linked policy. Andhra Pradesh & Telangana lead consumption at a combined 17.9% in 2025, followed by Uttar Pradesh at 12.6% and Maharashtra at 11.8%. Southern states collectively account for over 45% of national ENA consumption, driven by higher per-capita IMFL volumes, legal availability, and strong government-run retail distribution through bodies such as TSBCL, APSBCL, TASMAC, and KSBCL.

|

State (Consumption) |

Share (2025) |

Key Consumption Drivers |

|

Andhra Pradesh & Telangana |

17.9% |

High per-capita IMFL use, state-run retail, strong southern demand |

|

Uttar Pradesh |

12.6% |

Large urban population, country-liquor and IMFL growth |

|

Maharashtra |

11.8% |

Mumbai-Pune urban demand, premium IMFL and beer markets |

|

West Bengal |

9.8% |

Kolkata demand, and regional IMFL brands |

|

Tamil Nadu |

9.1% |

TASMAC-led monopoly retail, high volume throughput |

|

Karnataka |

8.2% |

Bengaluru premium market, strong IMFL ecosystem |

|

Punjab |

6.7% |

Strong rural-urban IMFL consumption base |

|

Rajasthan |

5.1% |

Growing urban centres, rising disposable incomes |

|

Kerala |

4.6% |

KSBC monopoly, premium IMFL and heritage brands |

|

Madhya Pradesh |

4.2% |

Diversified IMFL consumption, country-liquor bases |

|

Haryana |

3.5% |

Strong IMFL consumption supported by NCR proximity |

|

Bihar |

3.1% |

Consumption captured via leakage and inter-state flows despite prohibition |

|

Chhattisgarh |

2.8% |

State-controlled retail driving consistent country-liquor and IMFL demand |

|

Odisha |

2.5% |

Growing IMFL volumes alongside traditional country-liquor base |

|

Uttarakhand |

2.2% |

Tourism-driven demand and steady IMFL offtake |

|

Delhi |

1.9% |

Premium IMFL consumption hub, high per-capita spend |

|

Assam |

1.7% |

Largest Northeast consumption base, IMFL-led demand |

|

Jharkhand |

1.5% |

Country-liquor and IMFL demand across mining and urban belts |

|

Goa |

1.3% |

Tourism-led premium IMFL consumption, lower-tax retail |

|

Himachal Pradesh |

1.1% |

Tourism and hill-state IMFL demand |

|

Jammu and Kashmir |

1.0% |

Tourism-supported IMFL demand, regulated retail |

|

Meghalaya |

0.9% |

Northeast IMFL consumption, regional demand base |

|

Arunachal Pradesh |

0.8% |

Limited IMFL demand, small consumer base |

|

Tripura |

0.7% |

Marginal Northeast IMFL consumption |

|

Sikkim |

0.6% |

Smallest consumption base, tourism-led offtake |

The production-consumption mismatch is a defining feature of the India ENA market. States such as Punjab and Madhya Pradesh produce more ENA than they consume, making them net suppliers to consumption-heavy states in the south and east. Conversely, Andhra Pradesh & Telangana, Tamil Nadu, and West Bengal consume substantially more ENA than their domestic production, driving significant inter-state movement under state excise permits.

Top producing clusters include Punjab (grain belt), Uttar Pradesh (sugar-molasses belt), Maharashtra (western sugar belt), and Madhya Pradesh (grain-based). Top consumption clusters include Andhra Pradesh & Telangana (17.9%), Uttar Pradesh (12.6%), Maharashtra (11.8%), and West Bengal (9.8%). These ten combined states form the commercial core of India's ENA economy, representing over 92% of production and 89% of consumption as of 2025.

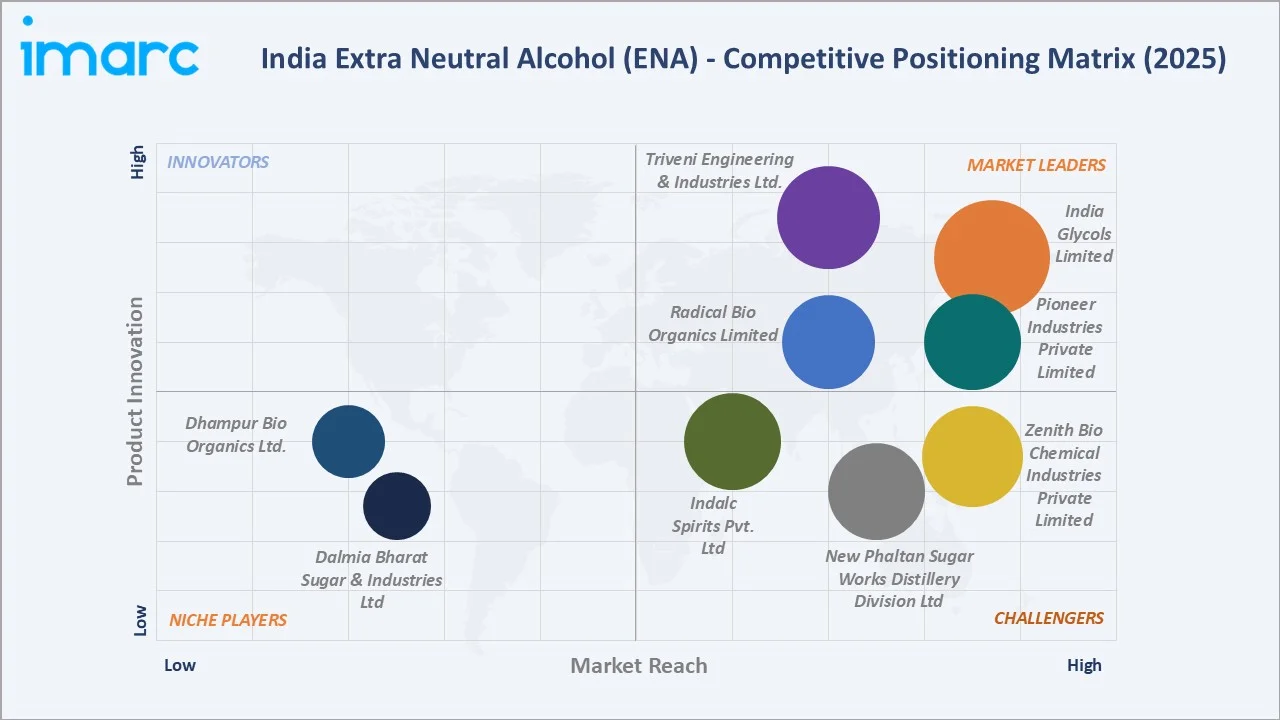

Competitive Landscape

The India ENA market competitive landscape comprises integrated sugar-and-distillery players, dedicated grain-based distilleries, and large IMFL manufacturers with captive distillation. Leading players compete on feedstock flexibility, distillation capacity, quality certifications (pharma-grade, export-grade), and pan-India logistics capability. The TOC for this report lists key company profiles publicly known major Indian ENA ecosystem participants.

|

Company Name |

Market Position |

Core Strength |

|

India Glycols Limited |

Leader |

Integrated bio-based chemicals and ENA producer; diversified industrial and potable alcohol portfolio |

|

Triveni Engineering & Industries Ltd. |

Leader |

Large multi-location distillery operations; strong molasses-based ENA and ethanol integration |

|

Pioneer Industries Private Limited |

Leader |

Established ENA supplier with niche positioning; presence in industrial and potable alcohol segments |

|

Radical Bio Organics Limited. |

Leader |

Grain-based ENA production; focus on high-purity alcohol for industrial and beverage use |

|

Zenith Bio Chemical Industries Private Limited. |

Challenger |

Diversified ENA applications across pharma, cosmetics, and industrial segments |

|

New Phaltan Sugar Works Distillery Division Ltd |

Challenger |

Integrated sugar and distillery operations; ENA and ethanol production in Western India |

|

Indalc Spirits Pvt. Ltd |

Challenger |

Regional molasses-based ENA producer; strong presence in industrial alcohol supply |

|

Dhampur Bio Organics Ltd. |

Emerging |

Integrated sugar-to-ethanol platform; growing ENA production capacity |

|

Dalmia Bharat Sugar & Industries Ltd |

Emerging |

Expanding distillery footprint with grain and molasses-based ENA production |

The Indian ENA market is moderately fragmented with a long tail of state-level distilleries. Strategic capacity expansion is active, with Globus Spirits commissioning new grain-based capacity in Bihar and Uttar Pradesh in 2023-2024, and Radico Khaitan investing in the greenfield Sitapur distillery with commissioning during 2022-2024. Consolidation and integration pressure continue to build as compliance, feedstock, and working-capital requirements rise.

Key Company Profiles

India Glycols Limited

India Glycols Limited (IGL) is one of India's largest grain- and molasses-based ENA producers, headquartered in Noida and founded in 1983. IGL manufactures Extra Neutral Alcohol from both molasses and grain feedstocks for use across alcoholic beverages, pharmaceuticals, perfumery, and personal hygiene, with operations spanning bio-based chemicals, potable spirits, biofuel ethanol, and bio-pharma.

- Plant & Production Details: IGL's three principal manufacturing complexes are located at Kashipur (Uttarakhand), Gorakhpur (Uttar Pradesh), and Saharanpur. Following capacity enhancements, the grain-based distillery at Kashipur stands at 500 KLPD, with a 590 KLPD biofuel-ethanol (ethanol-to-biofuel conversion) facility at the same site. The Gorakhpur complex's combined grain-distillery and biofuel-ethanol capacity now stands at 310 KLPD post the recent 200 KLPD addition. The plants are multi-feed and integrated with co-generation power, enabling flexible production of ENA, RS, absolute alcohol, and fuel-grade ethanol.

- Recent Developments: India Glycols recorded its highest-ever quarterly net turnover and EBITDA in Q3 FY26, with Q3 net revenue up 13% YoY and EBITDA up 36.1%, anchored by strength in the Potable Spirits segment. The Board has also approved a composite scheme of arrangement under which the bio-pharma undertakings and potable spirits undertakings will be demerged into IGL Spirits Limited, while the bio-pharma undertaking will be hived off into Ennature Bio Pharma Limited, subject to NCLT and other regulatory approvals.

- Strategic Focus: IGL's strategy is built around premiumization in spirits, value realization in bio-based chemicals, and capacity scaling to capture India's accelerating ethanol-blending mandate. The proposed demerger is intended to unlock segment-specific value and allow each vertical — chemicals, spirits, biofuel, and bio-pharma — to pursue its own growth trajectory, while the existing manufacturing footprint at Kashipur and Gorakhpur continues to anchor ENA supply for both captive use and external IMFL customers.

Triveni Engineering & Industries Ltd.

Triveni Engineering & Industries Limited (TEIL) is one of India's largest integrated sugar and ethanol manufacturers, headquartered in Noida and incorporated in 1932. TEIL produces both potable alcohol and fuel-grade ethanol across its distillery network, with multi-feed plants capable of producing Ethanol, Extra Neutral Alcohol (ENA), Rectified Spirit (RS), and Denatured Spirit (SDS) using a mix of sugarcane-based feedstocks and grain.

- Plant & Production Details: Triveni operates state-of-the-art distilleries at Muzaffarnagar (two facilities), Sabitgarh, Milak Narayanpur, and Rani Nangal — all in Uttar Pradesh — and the ENA produced at its Muzaffarnagar facility is used by leading Indian distillers for several iconic potable alcohol brands. Total distillation capacity stands at 860 KLPD, supported by eight sugar mills at Khatauli, Deoband, Sabitgarh, Chandanpur, Rani Nangal, Milak Narayanpur, Ramkola, and Shamli, alongside six co-generation plants. The Muzaffarnagar complex also houses a bottling unit for Triveni's IMIL and IMFL operations, with Tetra Pak and PET filling lines.

- Recent Developments: The company has announced plans to invest over ₹1,000 crore to scale ethanol capacity to 860 KLPD, while also progressing a composite scheme to amalgamate Sir Shadi Lal Enterprises with TEIL and demerge its Power Transmission business.

- Strategic Focus: TEIL's strategy is anchored on the integration of its sugar–ethanol value chain, scaling grain-based ethanol to align with India's 20% blending target, and selectively growing its IMIL and IMFL footprint in Uttar Pradesh. The company is also actively optimising its feedstock mix between molasses, maize, and FCI rice to manage input-cost volatility, while strengthening corporate structure through the proposed amalgamation and PTB demerger to unlock value across its diversified businesses.

Pioneer Industries Private Limited

Pioneer Industries Private Limited (PIPL) is a Pathankot, Punjab–based agro-processing and distillery company, incorporated in 1997 as part of the Pioneer Group. The company manufactures a diversified portfolio spanning vital wheat gluten, ENA/ethanol, DDGS, Punjab Medium Liquor, and maltodextrin, supplying premium FMCG and IMFL customers as well as public-sector Oil Marketing Companies.

- Plant & Production Details: PIPL operates a 400 KLPD ENA/ethanol unit alongside a wheat-gluten processing unit at its Pathankot complex. The plant is strategically located at the Industrial Growth Centre developed by the Punjab government, in the heart of the state's grain belt, which supports efficient procurement of grains and other agro-based feedstocks. Under the ENA/ethanol segment, PIPL counts Dabur India, United Spirits, Radico Khaitan, BPCL, HPCL, and IOCL among its institutional buyers.

- Recent Developments: In June 2025, BCL Industries Limited increased its shareholding in Pioneer Industries from 4.36% to 19.57%, picking up an additional 69.7 lakh equity shares at ₹44.18 per share for a total consideration of approximately ₹30.8 crore. The move was framed as a strategic step to deepen BCL's position in the grain-based ethanol sector.

- Strategic Focus: Pioneer's strategy leverages its decades-long grain procurement and processing expertise to operate as a B2B ENA and ethanol supplier of scale in northern India. The company is focused on capacity utilization of its 400 KLPD grain-based distillery, deepening tie-ups with OMCs under the Ethanol Blended Petrol programme, and maintaining diversified ENA off-take with leading IMFL houses, while its association with the BCL Industries / Mittal Group ecosystem positions it for continued co-investment and operational synergies in the grain-distillery value chain.

Market Concentration Analysis

The India ENA market is moderately fragmented, with supply distributed across grain-based standalone distilleries, sugar-mill-linked units, and integrated chemical-and-spirits players. The top merchant ENA producers — India Glycols Limited, Triveni Engineering & Industries Ltd., Dalmia Bharat Sugar & Industries Ltd, and Dhampur Bio Organics Ltd. — collectively account for an estimated 28-34% of merchant ENA volumes in 2025. The competitive landscape is further shaped by sugar-mill-linked distilleries such as New Phaltan Sugar Works Distillery Division Ltd in Maharashtra, alongside grain-based specialists Pioneer Industries Private Limited and Indalc Spirits Pvt. Ltd, with regional / niche players Radical Bio Organics Limited and Zenith Bio Chemical Industries Private Limited completing the merchant supply base.

The market is experiencing a dual-track dynamic. Sugar-mill-linked distilleries — represented by Triveni Engineering, Dhampur Bio Organics, Dalmia Bharat Sugar, and New Phaltan Sugar Works — remain dominant across Uttar Pradesh and Maharashtra, leveraging molasses-feedstock economics and integrated co-generation infrastructure. Simultaneously, grain-based standalone distilleries — led by India Glycols, Pioneer Industries, and Indalc Spirits — are scaling rapidly across Punjab, Haryana, Uttar Pradesh, and Uttarakhand, intensifying merchant-market competition. Smaller specialty producers such as Radical Bio Organics and Zenith Bio Chemical are carving out niche positions through regional supply contracts and B2B tie-ups, sustaining a moderately fragmented structure that is expected to persist through 2034.

Investment & Growth Opportunities

Fastest-Growing Segments

Pharmaceutical-grade ENA is the highest-growth application segment, projected to expand at approximately 4.2% CAGR through 2034. Grain-based ENA is the fastest-growing supply segment, with capacity additions in Punjab, Haryana, and Uttar Pradesh driving capacity growth in the 6-8% CAGR band during 2023-2030.

Emerging State Opportunities

Bihar, Jharkhand, Uttar Pradesh, and Chhattisgarh represent the highest-potential emerging state opportunities for new distillery capacity, driven by state-level ethanol policies, land availability, and proximity to grain surplus zones. Bihar's new state distillation policy and central EBP-linked incentives are catalyzing multi-player capex commitments through 2027.

Strategic and Financial Investment Trends

Strategic investment continues in grain-based distillery capacity expansion. Leading players such as India Glycols Limited, Triveni Engineering & Industries Ltd., Pioneer Industries Private Limited have undertaken significant capital expenditure toward expanding grain-based distillation and ethanol capacity, driven by the ethanol blending program and rising demand for ENA and fuel ethanol. Capital market access has also expanded, with Allied Blenders & Distillers' July 2024 IPO signaling sustained equity investor interest in the Indian alcohol value chain.

Future Market Outlook (2026-2034)

The India ENA market forecast projects steady value expansion from INR 109.0 Billion in 2025 to INR 147.7 Billion by 2034 at a CAGR of 3.33%. Punjab, Uttar Pradesh, and Maharashtra will continue to lead national production, while Andhra Pradesh & Telangana, Uttar Pradesh, and Maharashtra will dominate consumption through 2034. Southern and eastern states will retain premium consumption-to-production ratios, sustaining inter-state ENA movement flows.

Three key structural shifts will reshape the India ENA market through 2034. First, grain-based distillation will capture a rising share of feedstock mix, as EBP ambitions tighten molasses availability and FCI grain allocations support grain-based expansion. Second, premiumization in IMFL will drive higher-grade ENA demand, with single malts, premium whiskies, and craft spirits gaining share. Third, policy harmonization between state excise and central GST frameworks will progressively reduce compliance friction, gradually improving pan-India supply chain efficiency through 2030.

Research Methodology

Primary Research

Primary research encompassed structured interviews conducted in 2024-2025 with India ENA industry stakeholders, including managing directors and commercial heads at leading distilleries, procurement heads at IMFL and pharmaceutical manufacturers, industry body representatives (ISMA, CIABC, AIDA), and state excise officials. Primary insights validated market sizing, segmentation estimates, and state-level production and consumption flows.

Secondary Research

Secondary sources include data from the Ministry of Consumer Affairs, Food & Public Distribution, Indian Sugar Mills Association (ISMA), Confederation of Indian Alcoholic Beverage Companies (CIABC), All India Distillers' Association (AIDA), state excise departments, DGFT trade data, CPCB compliance records, company annual reports, SEBI filings, and trade publications including Ambrosia, Spiritz, and Drinks International India.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating GDP growth, IMFL case volumes, pharmaceutical output, molasses and grain availability, state excise trajectories, and ethanol blending policy scenarios. Scenario analysis (base, optimistic, and conservative cases) was performed to account for feedstock and policy uncertainty.

Extra Neutral Alcohol (ENA) Market in India Report Scope

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | INR Billion, Million Litres |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Applications Covered | Alcoholic Beverages, Flavors and Fragrances, Pharmaceuticals, Cosmetics, Others |

| States Covered | Punjab, Maharashtra, Madhya Pradesh, Uttar Pradesh, Karnataka, Andhra Pradesh and Telangana, Tamil Nadu, Haryana, Rajasthan, Chhattisgarh, West Bengal, Uttarakhand, Kerala, Bihar, Odisha, Goa, Assam, Delhi, Himachal Pradesh, Jammu and Kashmir, Arunachal Pradesh, Meghalaya, Jharkhand, Tripura, Sikkim |

| Companies Covered | India Glycols Limited, Triveni Engineering & Industries Ltd., Pioneer Industries Private Limited, Radical Bio Organics Limited., Zenith Bio Chemical Industries Private Limited., New Phaltan Sugar Works Distillery Division Ltd, Indalc Spirits Pvt. Ltd, Dhampur Bio Organics Ltd., Dalmia Bharat Sugar & Industries Ltd, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the extra neutral alcohol (ENA) market in India from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the extra neutral alcohol (ENA) market in India.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the extra neutral alcohol (ENA) market in India industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Extra Neutral Alcohol Market in India Report

The India ENA market was valued at INR 109.0 Billion in 2025, driven by rising IMFL consumption, expanding pharmaceutical demand, growing cosmetics usage, and steady industrial applications across domestic and export markets.

The market is projected to reach INR 147.7 Billion by 2034, growing at a CAGR of 3.33% during 2026-2034, supported by premiumisation in IMFL, grain-based capacity expansion, and diversification into pharma-grade and export-oriented ENA output.

Alcoholic beverages lead with a 62.8% share in 2025, driven by India's large IMFL industry where whisky alone commands the biggest category share. Pharmaceuticals follow at 12.4%, while flavours and fragrances, cosmetics, and others make up the balance of demand.

Punjab leads India's ENA production with an 18.7% share in 2025, anchored by grain-based distilleries using surplus rice and wheat stocks. Uttar Pradesh follows at 12.8% and Maharashtra at 11.4%, together forming the northern-western production spine.

Andhra Pradesh and Telangana combined lead India's ENA consumption at 17.9% share in 2025, driven by high per-capita IMFL consumption and government-run retail distribution. Uttar Pradesh (12.6%) and Maharashtra (11.8%) follow as key consumption hubs.

Key drivers include rising IMFL and premium spirits consumption, steady pharmaceutical and flavour-fragrance demand, abundant sugarcane and grain feedstock availability, expanding distillery capacity, and supportive government policies under the Ethanol Blending Programme and National Biofuels Policy framework.

Key challenges include ethanol diversion pressure on molasses feedstock, high and variable state excise duties, strict inter-state movement restrictions, molasses price volatility, and stringent environmental compliance including CPCB zero-liquid-discharge mandates on distilleries nationwide.

Major players include India Glycols Limited, Triveni Engineering & Industries Ltd., Pioneer Industries Private Limited, Radical Bio Organics Limited, Zenith Bio Chemical Industries Private Limited, New Phaltan Sugar Works Distillery Division Ltd, Indalc Spirits Pvt. Ltd, Dhampur Bio Organics Ltd., Dalmia Bharat Sugar & Industries Ltd.

Sugarcane molasses (C-heavy and B-heavy) remains the dominant feedstock, accounting for over 65% of national ENA output in 2025. Grain-based production using broken rice, maize, and damaged grains is growing rapidly, with sugarcane juice and syrup routes used selectively based on national ethanol policy guidelines.

The Ethanol Blending Programme has reshaped feedstock economics by diverting molasses and sugarcane juice toward fuel ethanol. India achieved 15% blending in 2024 and targets 20% by 2025-26, tightening feedstock availability for beverage and industrial ENA and accelerating capacity diversification into grain-based routes.

ENA is high-purity alcohol (96%+ ABV) used mainly for beverages, pharma, and cosmetics. Fuel ethanol (99.5%+ ABV) is anhydrous alcohol blended with petrol. Rectified spirit (around 95% ABV) is an intermediate industrial-grade alcohol used for technical and industrial applications, including country liquor production.

Grain-based ENA is projected to be the fastest-growing supply segment, expanding at approximately 6-8% CAGR through 2030. Policy support under the Ethanol Blending Programme, FCI grain allocations, and capacity expansion in Punjab, Haryana, Uttar Pradesh, and Madhya Pradesh are the primary growth catalysts through 2034.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)