Indian Farming Market Size, Share, Trends and Forecast by Crop Type, Application, Distribution Channel, Crop Seasonality, and Region, 2026-2034

Indian Farming Market Summary:

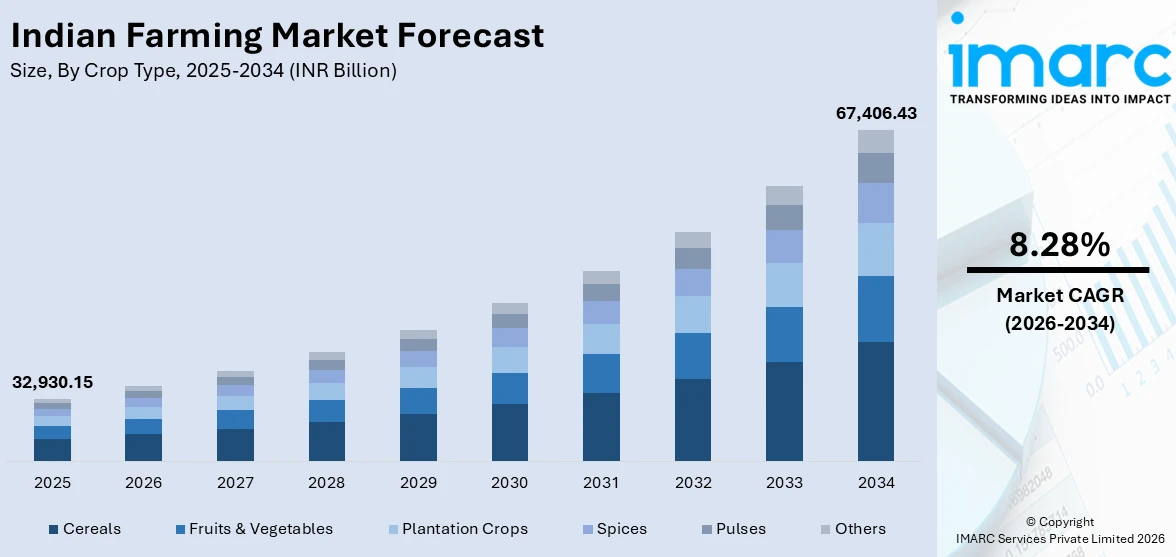

The Indian farming market size was valued at INR 32,930.15 Billion in 2025 and is projected to reach INR 67,406.43 Billion by 2034, growing at a compound annual growth rate of 8.28% from 2026-2034.

The market is driven by rising demand for food security, government-backed agricultural initiatives, expanding irrigation infrastructure, and the adoption of modern farming technologies. Additionally, increasing crop diversification, favorable monsoon patterns, and supportive rural credit policies are accelerating growth across India. The growing emphasis on sustainable agricultural practices, organic farming, and enhanced supply chain connectivity through digital platforms and farmer-producer organizations is further bolstering the Indian farming market share.

Key Takeaways and Insights:

- By Crop Type: Cereals dominate the market with a share of 30% in 2025, driven by extensive monsoon-fed cultivation across major agrarian states and strong government procurement mechanisms supporting rainy season crop output.

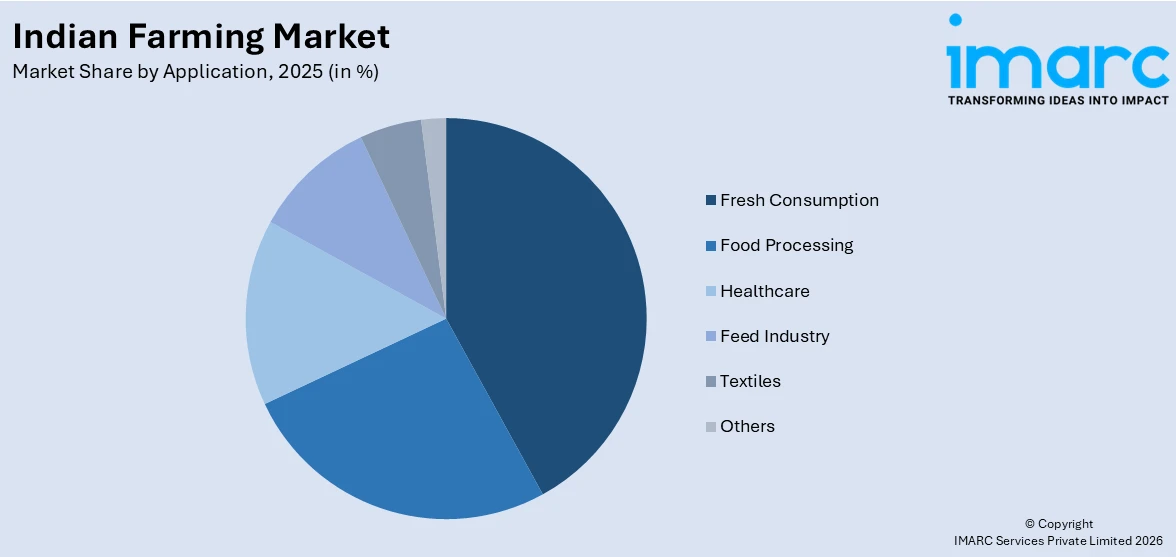

- By Application: Fresh consumption leads the market with a share of 41% in 2025, owing to their foundational role in Indian dietary frameworks and large-scale cultivation supported by minimum support price mechanisms.

- By Distribution Channel: Self consumption represents the largest segment with a market share of 33% in 2025, driven by deeply ingrained cultural preferences for fresh produce and expansive local mandi networks facilitating farm-to-consumer supply chains.

- By Crop Seasonality: Kharif dominates the market with a share of 48% in 2025, owing to the large proportion of subsistence and smallholder farming households retaining significant produce for household consumption.

- Key Players: The Indian farming market exhibits a fragmented competitive landscape, with a diverse mix of government-supported cooperatives, private agribusiness conglomerates, and regional input manufacturers operating across multiple value chain segments including seeds, fertilizers, equipment, and distribution.

To get more information on this market Request Sample

The Indian farming market is propelled by a convergence of structural and policy-driven factors that continue to reshape the agricultural landscape. The government's sustained emphasis on doubling farmer incomes through targeted subsidies, crop insurance schemes, and direct benefit transfers has significantly enhanced rural economic participation. According to reports, the Union Budget introduced ‘Bharat Vistar’, a multilingual AI tool to modernize farming by integrating AgriStack with scientific advisories for farmers across crop cycles. Expanding irrigation networks, including micro-irrigation and drip systems, are reducing monsoon dependency and enabling year-round cultivation across previously rain-fed regions. Furthermore, the growing adoption of precision agriculture technologies, farm mechanization, and digital platforms for market access is improving productivity and supply chain efficiency. Rising domestic food demand fueled by population growth and urbanization, coupled with increasing exports of agricultural commodities, continues to reinforce the market's expansion trajectory.

Indian Farming Market Trends:

Rising Adoption of Digital Agriculture and Smart Farming Solutions

The Indian farming sector is witnessing a transformative shift toward digital agriculture, with farmers increasingly leveraging mobile-based advisory platforms, satellite imagery, and drone technology for crop monitoring and resource optimization. According to reports, the Government of Maharashtra selected Findability Sciences under the Maha Agri‑AI Policy 2025‑29 to accelerate the use of AI, GenAI, and other digital technologies in the agricultural ecosystem, underscoring state support for data‑driven farming tools. Government-led digital initiatives are facilitating real-time weather forecasting, soil health assessment, and market price transparency for farmers across remote regions.

Expansion of Organic and Sustainable Farming Practices

India is experiencing a notable transition toward organic and regenerative farming methods, driven by rising consumer health consciousness and export market requirements for chemical-free produce. According to reports, India recorded 15 lakh hectares under organic farming, with 52,289 clusters formed and 25.30 lakh farmers benefitted under the Paramparagat Krishi Vikas Yojana (PKVY). Natural farming techniques, including zero-budget natural farming and integrated pest management, are gaining traction across multiple states through dedicated government programs and training initiatives. The establishment of organic certification frameworks and dedicated procurement channels is incentivizing farmers to transition away from conventional chemical-intensive cultivation, fostering soil health restoration and long-term agricultural sustainability.

Growing Emphasis on Crop Diversification and High-Value Agriculture

Indian agriculture is progressively moving beyond traditional cereal-centric cultivation toward diversified cropping patterns that include horticulture, floriculture, medicinal herbs, and specialty crops. As per sources, in January 2026, the Ministry of Agriculture and Farmers’ Welfare notified special incentives specifically for high‑value sandalwood and medicinal plant cultivation to boost diversification and farmer incomes under the Union Budget’s ‘Viksit Bharat’ roadmap. State-level agricultural policies are actively promoting the cultivation of high-value crops through dedicated subsidies, infrastructure support, and market linkage programs to enhance farmer profitability.

Market Outlook 2026-2034:

The Indian farming market revenue is projected to witness robust expansion over the forecast period, driven by sustained policy support, technological modernization, and escalating domestic and international demand for agricultural commodities. Government investments in rural infrastructure, cold chain logistics, and farm mechanization are expected to significantly enhance productivity and market access for millions of smallholder farmers. The growing integration of agritech platforms, expansion of contract farming arrangements, and strengthening of food processing linkages will further accelerate revenue generation across the agricultural value chain through the forecast horizon. The market generated a revenue of INR 32,930.15 Billion in 2025 and is projected to reach a revenue of INR 67,406.43 Billion by 2034, growing at a compound annual growth rate of 8.28% from 2026-2034.

Indian Farming Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

| Crop Type | Cereals | 30% |

| Application | Fresh Consumption | 41% |

| Distribution Channel | Self Consumption | 33% |

| Crop Seasonality | Kharif | 48% |

Crop Type Insights:

- Cereals

- Fruits & Vegetables

- Plantation Crops

- Spices

- Pulses

- Others

Cereals dominate with a market share of 30% of the total Indian farming market in 2025.

The cereals command a significant share of the Indian farming market, anchored by the country's position as one of the world's largest producers and consumers of rice and wheat. Cereal cultivation benefits from deeply established agronomic practices, extensive institutional support through minimum support prices, and guaranteed procurement by government agencies for public distribution and buffer stock maintenance. In May 2025, India’s central pool rice stocks exceeded 59 MT more than four times the buffer norm due to robust procurement under MSP, highlighting the scale of government cereal accumulation and food security focus.

Ongoing advancements in cereal crop research, including the development of biofortified and climate-resilient varieties, are further strengthening the segment's growth trajectory. Government programs promoting millets and coarse cereals as nutritional alternatives are expanding the cereal cultivation portfolio beyond traditional rice and wheat dominance. The integration of mechanized harvesting, improved storage infrastructure, and digital market platforms is enhancing cereal supply chain efficiency, reducing wastage, and improving farmer price realization across producing regions.

Application Insights:

Access the comprehensive market breakdown Request Sample

- Fresh Consumption

- Food Processing

- Healthcare

- Feed Industry

- Textiles

- Others

Fresh consumption leads with a share of 41% of the total Indian farming market in 2025.

The fresh consumption leads the Indian farming market, reflecting the deeply entrenched cultural and dietary preference for fresh fruits, vegetables, grains, and produce in Indian households. The extensive network of local agricultural mandis, weekly markets, and direct farmer-to-consumer channels facilitates widespread availability of fresh agricultural products across urban and rural areas. India's tropical and subtropical climate enables year-round production of diverse fresh produce, supporting continuous supply to meet the daily consumption requirements of the country's large population.

The growing health and wellness consciousness among Indian consumers is further reinforcing demand for fresh and minimally processed agricultural products over packaged alternatives. Expanding cold chain logistics and last-mile delivery infrastructure are improving the shelf life and accessibility of fresh produce in tier-two and tier-three cities. Government initiatives promoting farm-to-fork traceability and quality certification are enhancing consumer confidence in fresh agricultural products, while the emergence of online grocery platforms is creating additional distribution channels for farm-fresh commodities.

Distribution Channel Insights:

- Self Consumption

- Traditional Retail

- Business to Business

- Modern Retail

- Online

Self consumption exhibits a clear dominance with a 33% share of the total Indian farming market in 2025.

The self consumption holds the largest share in the Indian farming market distribution landscape, driven by the predominance of smallholder and subsistence farming that characterizes India's agrarian economy. A significant proportion of farming households retain a substantial portion of their agricultural output for household nutritional needs before directing surplus quantities to commercial markets. This pattern is particularly pronounced in rain-fed and tribal agricultural regions where market access remains limited and traditional farming practices prioritize food self-sufficiency.

The persistence of self-consumption as the leading distribution channel reflects the structural characteristics of Indian agriculture, where fragmented landholdings and limited commercial orientation influence produce allocation decisions. However, progressive government initiatives aimed at improving market connectivity through electronic trading platforms, farmer producer organizations, and rural road infrastructure are gradually facilitating the transition from subsistence to commercially oriented farming. The expanding reach of agricultural extension services and digital literacy programs is empowering farming communities to optimize the balance between household consumption and market-directed output.

Crop Seasonality Insights:

- Rabi

- Kharif

- Zaid

Kharif leads with a market share of 48% of the total Indian farming market in 2025.

The kharif maintains its leading position in the Indian farming market, driven by the country's heavy reliance on monsoon-fed agricultural production during the June to October growing season. Major kharif crops including rice, cotton, sugarcane, and oilseeds form the backbone of India's agricultural output, benefiting from extensive government procurement programs, minimum support price guarantees, and widespread access to subsidized inputs. According to reports, in July 2025, total kharif crop sowing jumped by 11.3% year‑on‑year, propelled by above‑normal southwest monsoon rains and expanded acreage in rice and pulses.

The sustained dominance of kharif cultivation is further reinforced by the expanding irrigation infrastructure that supplements monsoon variability and enables consistent crop establishment. Government initiatives focused on improving water management, promoting drought-resistant seed varieties, and enhancing post-harvest storage facilities specifically for kharif outputs are strengthening the segment's productivity profile. Additionally, the strong linkage between kharif crop production and the public distribution system ensures guaranteed demand, providing economic stability to millions of farming households dependent on rainy season agriculture.

Regional Insights:

- North India

- South India

- East India

- West India

North India represents a dominant position in the farming market, driven by the fertile Indo-Gangetic plains that support extensive cultivation of wheat, rice, and sugarcane. The region benefits from well-developed canal irrigation networks, strong government procurement infrastructure, and established mandi systems. Progressive adoption of farm mechanization and favorable agro-climatic conditions further reinforce the region's leading agricultural productivity and output contribution.

South India holds a significant share in the farming market, supported by diversified cropping patterns encompassing rice, millets, spices, plantation crops, and horticulture. The region benefits from advanced irrigation management through tank systems and micro-irrigation adoption. Strong cooperative farming structures established agri-export networks for spices and tropical produce, and progressive state-level agricultural policies contribute to sustained agricultural growth and market expansion.

East India represents a growing segment in the farming market, characterized by abundant water resources, fertile alluvial soil, and favorable climatic conditions for rice, jute, and tea cultivation. Despite significant agricultural potential, the region is witnessing accelerating growth through expanding irrigation infrastructure, increasing adoption of improved seed varieties, and government-led initiatives promoting crop diversification and farm mechanization across underutilized agricultural lands.

West India contributes substantially to the farming market, driven by diverse agricultural output spanning cotton, groundnut, oilseeds, and horticultural produce across varied terrain. The region benefits from progressive agricultural cooperatives, particularly in dairy and sugar sectors, along with expanding drip irrigation adoption in arid zones. Growing investment in food processing clusters and agri-logistics infrastructure is further strengthening the region's agricultural commercial viability.

Market Dynamics:

Growth Drivers:

Why is the Indian Farming Market Growing?

Government Policy Framework and Agricultural Subsidy Ecosystem

The Indian government's comprehensive agricultural policy framework serves as a foundational growth driver, encompassing direct benefit transfers, crop insurance schemes, subsidized credit facilities, and minimum support price mechanisms that collectively enhance farmer economic viability. As per sources in 2026, the Union Cabinet approved an additional ₹8,000 crore crop insurance premium subsidy under the Pradhan Mantri Fasal Bima Yojana to provide premium relief to around five crore farmers for Kharif 2026. Moreover, central and state government programs focused on soil health management, watershed development, and integrated nutrient management are systematically improving agricultural productivity across diverse agro-climatic zones. The allocation of dedicated budgetary resources toward agricultural research institutions and extension services is accelerating the dissemination of improved farming practices to grassroots-level cultivators nationwide.

Expanding Irrigation Infrastructure and Water Resource Management

The progressive expansion of irrigation coverage across India is fundamentally transforming agricultural productivity by reducing dependence on erratic monsoon patterns and enabling multi-season cropping cycles. Government-led investments in canal networks, micro-irrigation systems, check dams, and groundwater recharge structures are bringing previously rain-fed areas under assured irrigation coverage. In April 2025, the Union Cabinet approved a Rs 1,600 crore sub‑scheme under the Pradhan Mantri Krishi Sinchayee Yojana to modernize irrigation networks and pilot piped irrigation projects benefiting about 80,000 farmers nationwide, reinforcing last‑mile water delivery to farms. The promotion of drip and sprinkler irrigation technologies through dedicated subsidy programs is optimizing water use efficiency while simultaneously improving crop yields and quality, particularly for smallholder farmers in remote agricultural zones.

Rising Domestic Food Demand and Export Market Expansion

India's expanding population base, rapid urbanization, and increasing per capita income levels are generating sustained growth in domestic food demand across cereals, pulses, oilseeds, fruits, vegetables, and dairy products. According to reports, India’s agricultural exports surged with farm shipments worth approximately $4.16 billion in April–May 2025, driven by strong rice, dairy, and fruit/vegetable exports under APEDA’s export facilitation programs. The diversification of dietary patterns among urban consumers toward protein-rich foods and specialty crops is creating new market opportunities for farming communities to cultivate higher-value agricultural products. Simultaneously, India's growing presence in international agricultural commodity markets supported by favorable trade agreements is opening lucrative export channels for diverse agricultural commodities.

Market Restraints:

What Challenges the Indian Farming Market is Facing?

Fragmented Landholding Patterns and Scale Limitations

The prevalence of small and marginal landholdings across India poses a significant constraint on agricultural productivity and mechanization adoption. Fragmented farm sizes limit the economic feasibility of deploying modern equipment and precision agriculture technologies. This structural challenge restricts economies of scale, reduces bargaining power in input procurement and output marketing, and constrains productivity-enhancing infrastructure investments.

Inadequate Cold Chain and Post-Harvest Infrastructure

The insufficient development of cold storage facilities refrigerated transportation networks, and modern warehousing infrastructure across rural India results in substantial post-harvest losses for perishable agricultural commodities. Limited access to appropriate storage and processing facilities forces farmers to sell produce immediately after harvest at unfavorable prices, undermining farmer profitability and restricting the overall value realization potential of the agricultural supply chain.

Climate Variability and Environmental Vulnerability

Increasing frequency of extreme weather events including droughts, floods, unseasonal rainfall, and heat waves poses escalating risks to agricultural production stability across India. The dependence of a significant portion of cultivated areas on monsoon rainfall makes crop yields highly susceptible to shifting precipitation patterns. Soil degradation and declining groundwater tables further compound environmental challenges confronting sustainable agricultural production.

Competitive Landscape:

The Indian farming market is characterized by a highly fragmented and multi-layered competitive structure encompassing government cooperatives, private agribusiness entities, regional input manufacturers, and emerging agritech startups operating across the agricultural value chain. Market participants compete across diverse segments including seeds, fertilizers, crop protection, farm machinery, post-harvest processing, and agricultural distribution networks. The competitive dynamics are shaped by government procurement policies, subsidy allocation frameworks, and regulatory standards that influence market access and pricing strategies. Recent years have witnessed intensifying competition from technology-driven agricultural platforms that are disrupting traditional farming input distribution and output marketing channels. Strategic collaborations between established agricultural companies and digital technology providers are reshaping competitive positioning, while farmer producer organizations are emerging as collective bargaining entities that alter the traditional intermediary-dominated market structure.

Recent Developments:

- In September 2025, Farmway Technologies, founded by Indian entrepreneurs, partnered with the Government of Georgia to invest Rs 870 crore in sustainable agriculture. The initiative includes tokenised ashwagandha cultivation and a 10,000-ton natural oils processing plant, modernizing farming through digital innovation while reinforcing Farmway’s Indian footprint and advancing global agritech adoption.

Indian Farming Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million Metric Tons, Billion INR |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Crop Types Covered | Cereals, Vegetables, Fruits, Plantation Crops, Spices, Pulses, Others |

| Applications Covered | Fresh Consumption, Food Processing, Healthcare, Feed Industry, Textiles, Others |

| Distribution Channels Covered | Self-Consumption, Traditional Retail, Business to Business, Modern Retail, Online |

| Crop Seasonalites Covered | Rabi, Kharif, Zaid |

| Regions Covered | North India, South India, East India, West India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Indian Farming Market Research Report and Industry Forecast Report

The Indian farming market size was valued at INR 32,930.15 Billion in 2025.

The Indian farming market is expected to grow at a compound annual growth rate of 8.28% from 2026-2034 to reach INR 67,406.43 Billion by 2034.

Cereals held the largest Indian farming market share, driven by their foundational role in the Indian dietary framework, large-scale cultivation supported by minimum support price mechanisms, and sustained public distribution system procurement across major grain-producing regions.

Key factors driving the Indian farming market include government agricultural subsidies and policy support, expanding irrigation infrastructure, rising domestic food demand, growing adoption of farm mechanization and digital agriculture technologies.

Major challenges include fragmented landholding patterns limiting mechanization adoption, inadequate cold chain and post-harvest infrastructure causing significant losses, climate variability and environmental vulnerability, and limited access to institutional credit for smallholder farmers.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)