Faucet Market Size, Share, Trends and Forecast by Type, Application, Technology, Material, Distribution Channel, End User, and Region 2026-2034

Global Faucet Market Size, Share, Trends & Forecast (2026-2034)

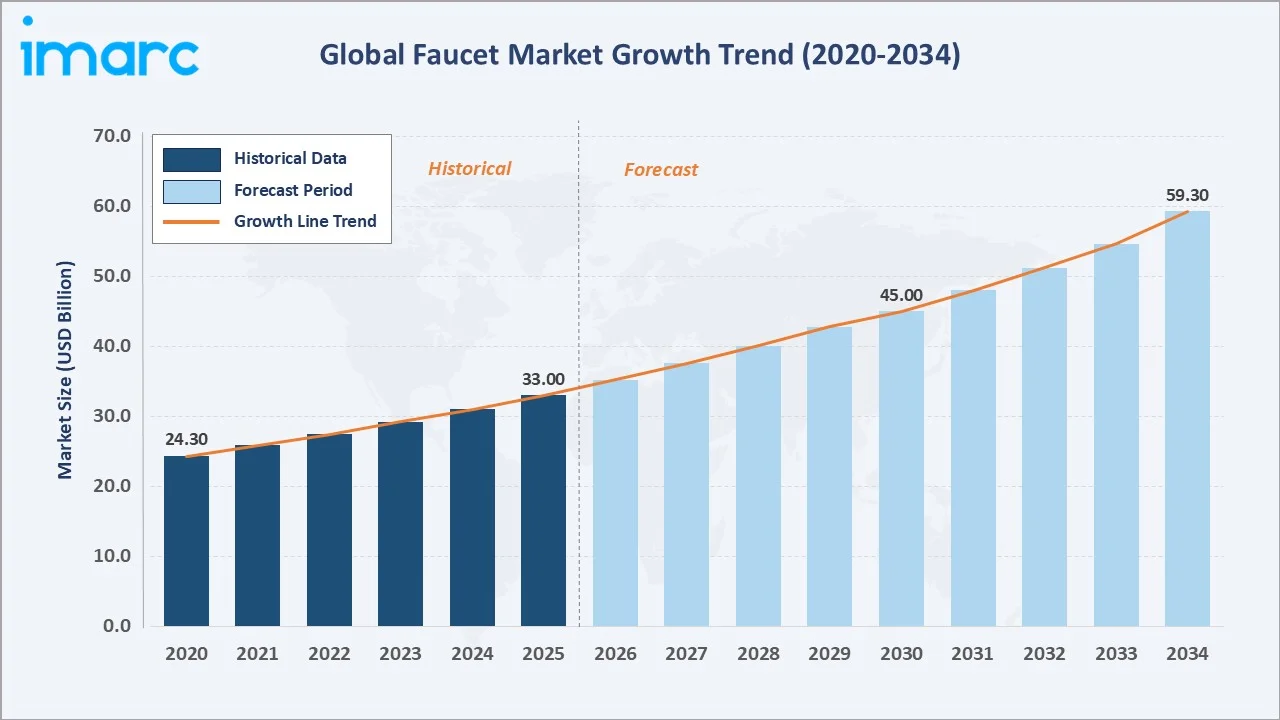

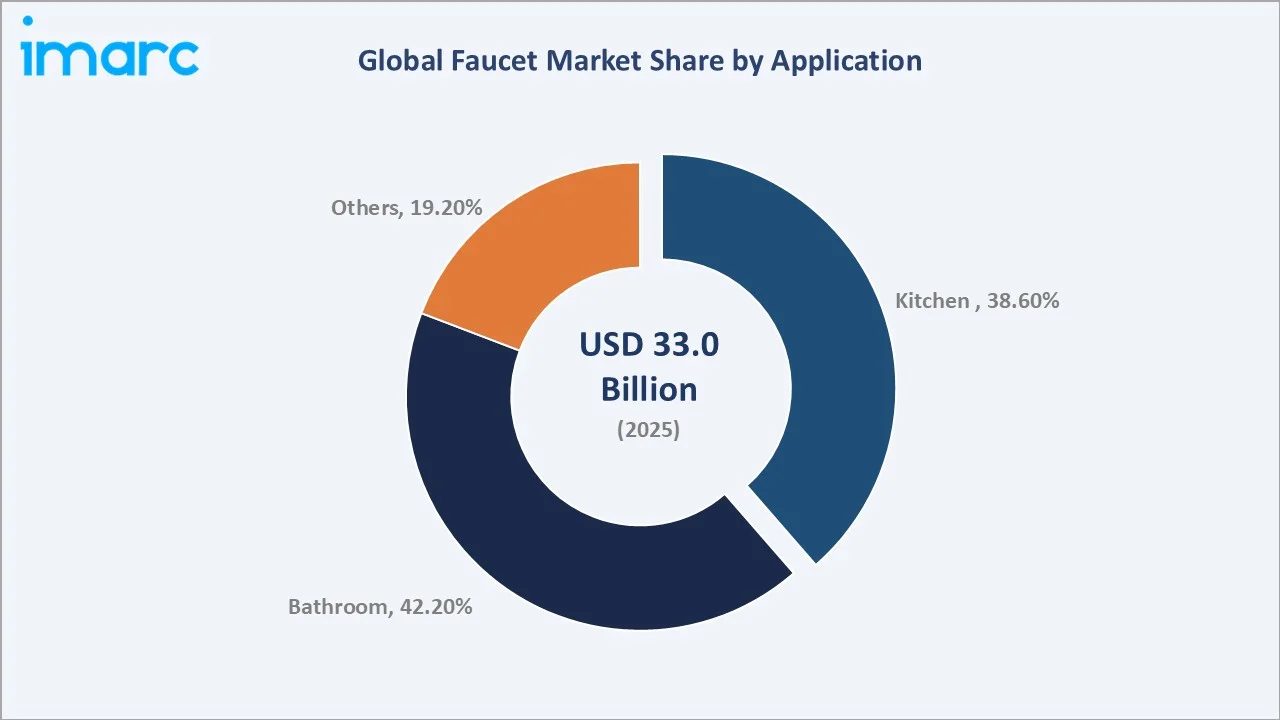

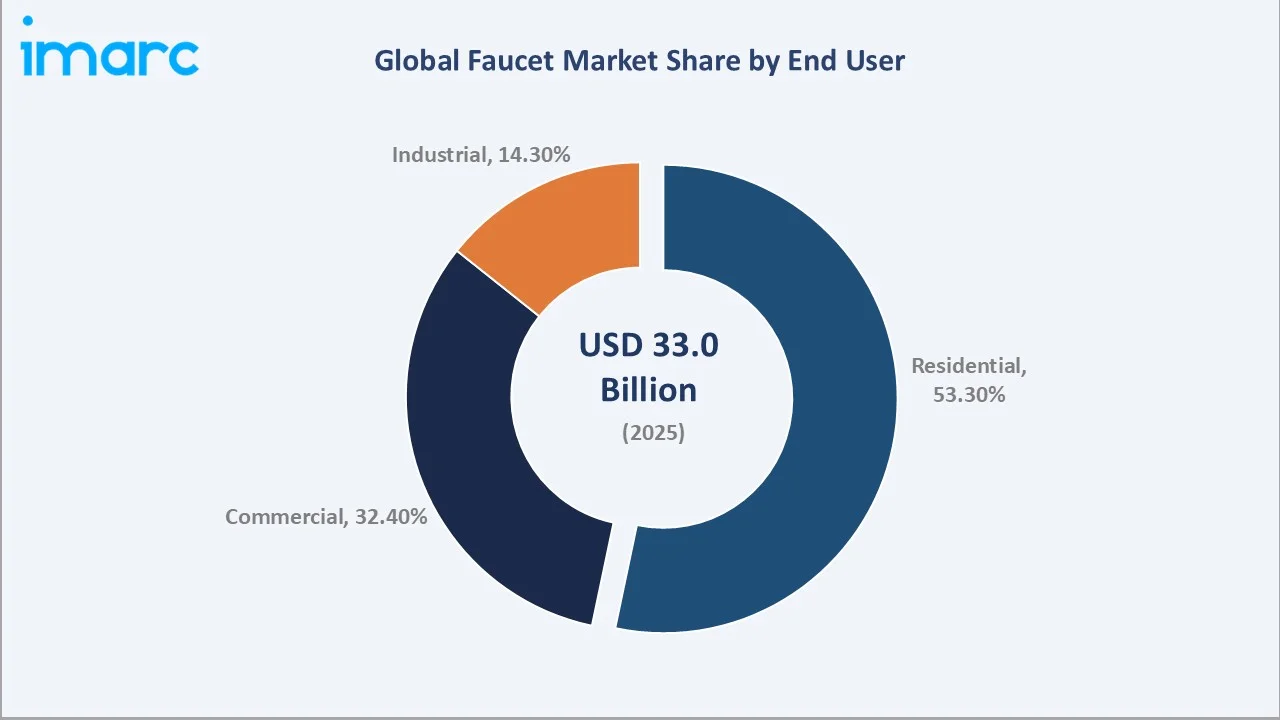

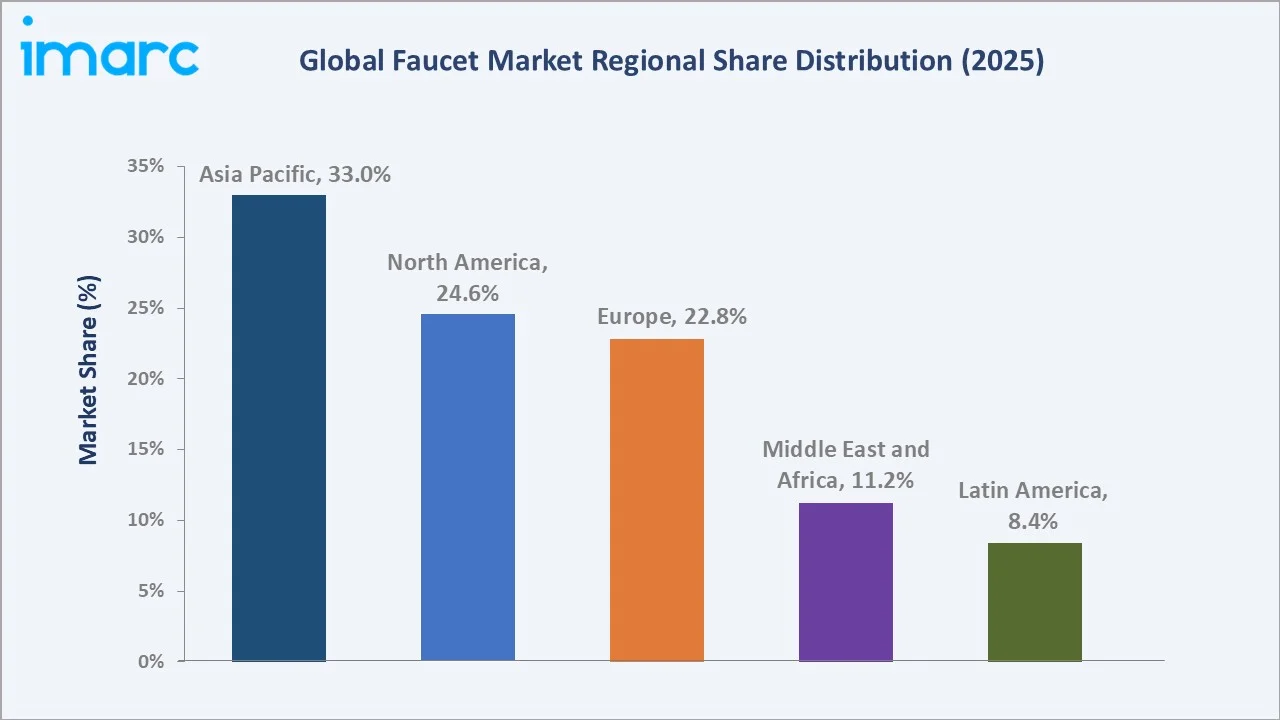

The global faucet market size was valued at USD 33.0 Billion in 2025 and is projected to reach USD 59.3 Billion by 2034, exhibiting a CAGR of 6.37% during the forecast period 2026-2034. Rapid urbanization, rising residential and commercial construction, growing demand for water-efficient plumbing fixtures, and accelerating smart-home integration are driving the faucet market growth. Bathroom applications lead at 42.2% share in 2025, while residential end users account for 53.3% of global demand. Asia Pacific dominates with 33.0% of global revenue in 2025.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 33.0 Billion |

|

Forecast Market Size (2034) |

USD 59.3 Billion |

|

CAGR (2026-2034) |

6.37% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Asia Pacific (33.0% share, 2025) |

|

Fastest Growing Region |

Asia Pacific (CAGR ~7.4%) |

|

Leading Application |

Bathroom (42.2%, 2025) |

|

Leading End User |

Residential (53.3%, 2025) |

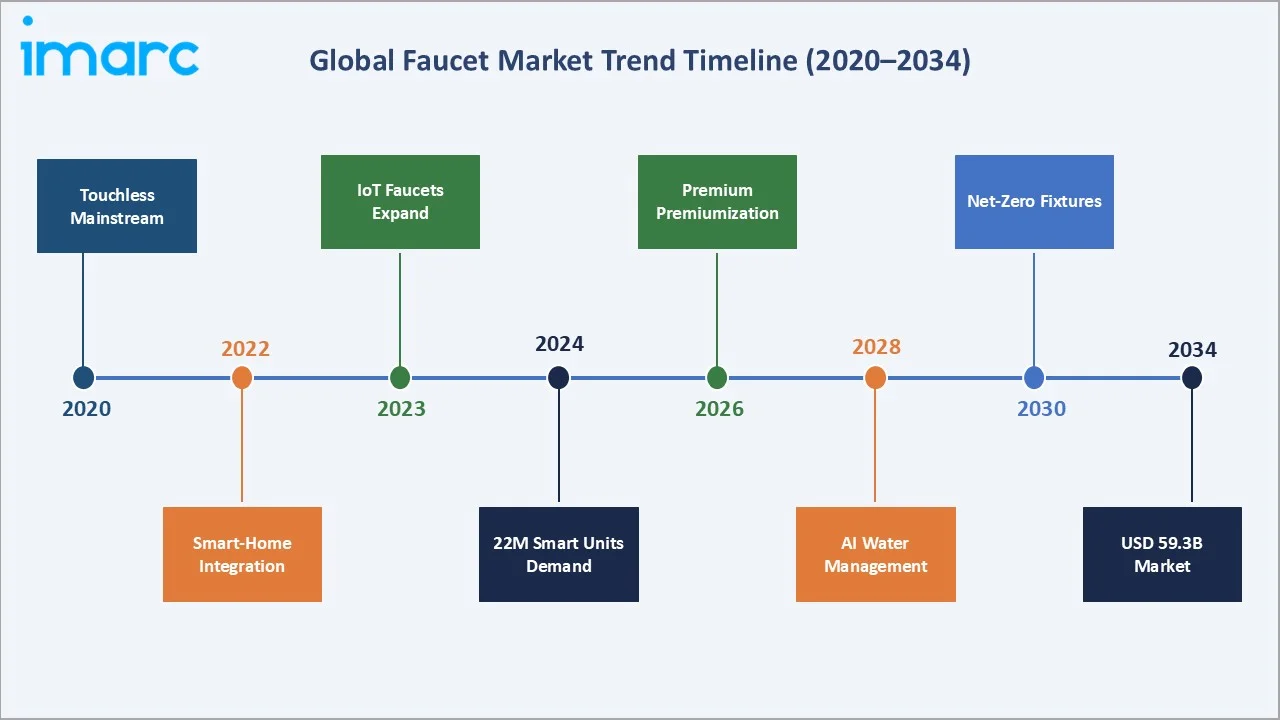

The global faucet market growth trajectory from 2020 through 2034, contrasting historical expansion against a sustained forecast curve powered by urbanization, renovation expenditure, and smart-home technology adoption across residential and commercial segments.

To get more information on this market, Request Sample

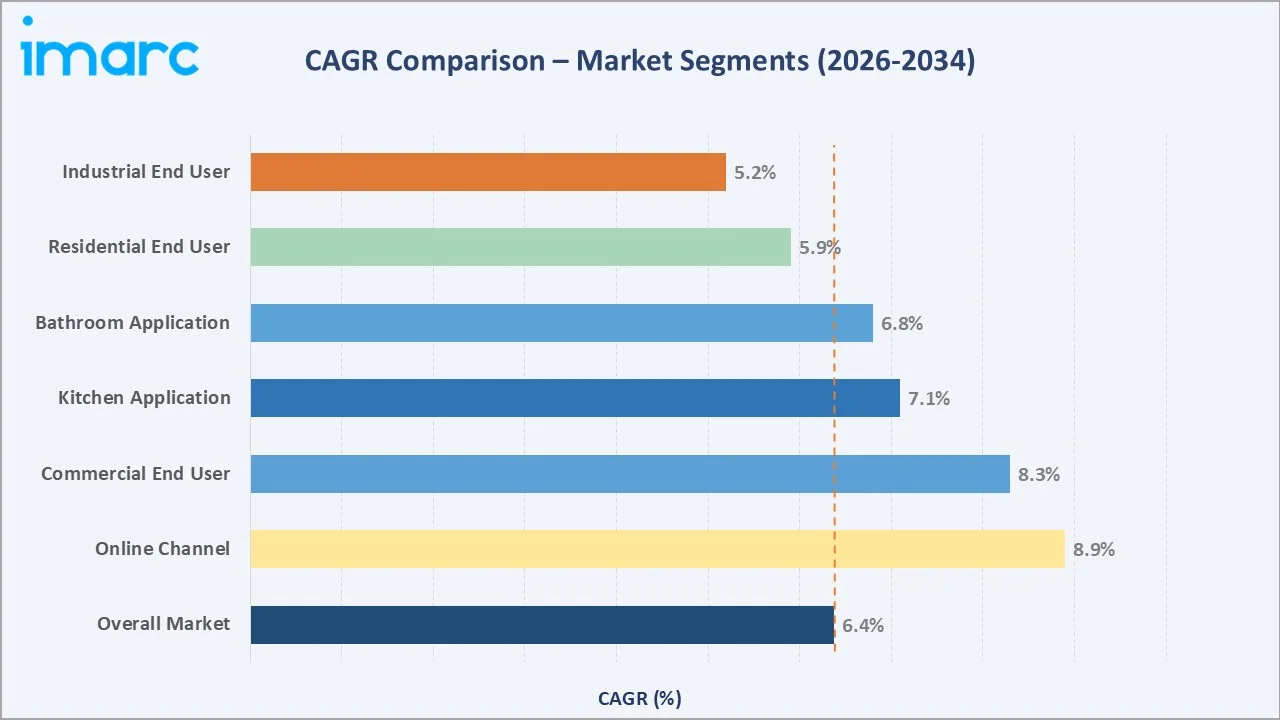

Segment-level CAGR comparisons highlighting online channel adoption and commercial end-user expansion as the fastest-growing sub-categories within the global faucet market forecast through 2034.

Executive Summary

The global faucet market is undergoing a significant transformation. It is driven by urbanization, sustainability regulation, and smart-home technology adoption. Valued at USD 33.0 Billion in 2025, the market is forecast to reach USD 59.3 Billion by 2034 at a CAGR of 6.37%.

Bathroom command 42.2% share in 2025, driven by premium renovation and hospitality expansion. Kitchen segment is propelled by pull-down configurations and commercial kitchen buildouts. Residential represent 53.3% of global demand, while the commercial segment is the fastest-growing end user category at an estimated CAGR of 8.3% through 2030.

Asia Pacific leads with 33.0% global revenue share in 2025. North America holds 24.6% and Europe 22.8%. The faucet market outlook remains positive as premiumization, sustainability design, and touchless adoption converge across all major markets.

Key Market Insights

|

Insight |

Data |

|

Largest Application |

Bathroom – 42.2% share (2025) |

|

Second Application |

Kitchen – 38.6% share (2025) |

|

Largest End User |

Residential – 53.3% share (2025) |

|

Fastest Growing End User |

Commercial – ~8.3% CAGR (2025-2030) |

|

Leading Region |

Asia Pacific – 33.0% revenue share (2025) |

|

Top Companies |

Kohler, Fortune, Delta, LIXIL, TOTO, Hansgrohe |

|

Smart Faucet Demand |

22 million units (2025) |

Key Analytical Observations Supporting the Above Data:

- Bathroom's 42.2% dominance in 2025 reflects premium renovation activity and rapid luxury hotel room inventory expansion across Asia Pacific and the Middle East.

- Kitchen faucets' 38.6% share is driven by pull-down and pull-out configurations in residential renovations and commercial kitchen buildouts, along with demand for filtration-integrated designs.

- Residential end users' 53.3% majority is underpinned by new housing completions globally. The U.S. Census Bureau recorded 724,000 single-family housing sales in early 2024, a 5.1% year-over-year increase.

- Asia Pacific's 33.0% global dominance reflects China's role as the world's largest residential construction market and India's government-backed housing programs targeting 20 million affordable urban homes.

- Smart and sensor-based faucet demand reached 22 million units in 2025, driven by hygiene awareness, smart-home ecosystems, and EPA WaterSense and Dubai Green Building Regulation programs (March 2025).

Global Faucet Market Overview

Faucets are essential plumbing fixtures designed to control water flow and temperature across residential, commercial, and industrial applications. The global market includes a broad portfolio of products such as single- and dual-handle mixers, touchless sensor-based faucets, ceramic disc systems, and ball-valve configurations. These products are manufactured using materials like brass, stainless steel, zinc alloys, and engineered polymers, catering to diverse use cases ranging from kitchens and bathrooms to laboratories, industrial facilities, and outdoor installations.

The industry operates at the convergence of construction demand, evolving design preferences, regulatory frameworks, and smart-home integration. Growth is supported by macroeconomic drivers such as infrastructure development in emerging markets, rising disposable incomes fuelling premiumization, and increasingly stringent regulations mandating water efficiency and lead-free compliance. At the same time, the market is undergoing a structural shift toward connected, sustainable, and technology-enabled solutions, which are redefining product innovation and procurement strategies on a global scale.

Market Dynamics

To evaluate market opportunities, Request Sample

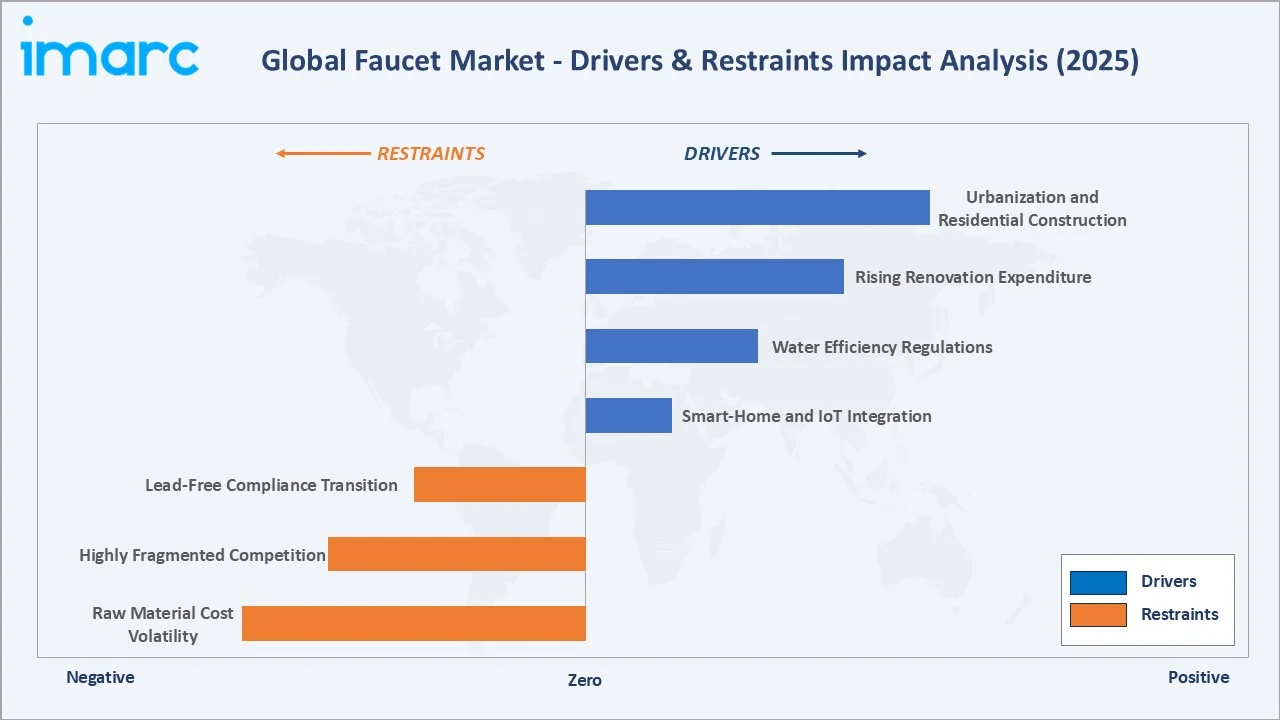

Market Drivers

- Urbanization and Residential Construction: Global housing demand remains a primary growth lever for the faucet market. Government-backed housing initiatives in high-growth regions such as India, China, and the Middle East are driving large-scale procurement of entry-level and mid-range faucet solutions, particularly in affordable housing segments.

- Rising Renovation Expenditure: According to the Harvard Joint Center for Housing Studies, U.S. home improvement and repair spending reached approximately USD 485 billion in 2024. Replacement demand driven by renovation cycles continues to be a critical volume driver, with a clear shift toward premium, design-led, and smart-enabled faucet systems in developed markets.

- Water Efficiency Regulations: Regulatory frameworks are structurally shaping product specifications and demand. Programs such as EPA WaterSense, EU Ecodesign Regulation, and WELS Scheme mandate water-saving and compliance standards, accelerating the adoption of certified fixtures. In June 2025, Water Europe introduced a water resilience strategy, further reinforcing water stewardship targets within European building infrastructure.

- Smart-Home and IoT Integration: The rapid expansion of smart-home ecosystems is accelerating the integration of connected technologies across household infrastructure. This trend is extending to plumbing, with touchless, sensor-based, and app-enabled faucets moving beyond niche luxury into broader adoption. Rising demand for convenience, hygiene, and water efficiency—especially in urban and higher-income segments—is driving this shift toward mainstream use.

Market Restraints

- Raw Material Cost Volatility: Copper, nickel, and zinc commodity swings directly inflate production costs.

- Highly Fragmented Competition: Numerous regional manufacturers in China and India intensify price competition and limit premium pricing power for global brands targeting cost-sensitive residential markets in emerging economies.

Market Opportunities

- IoT-Enabled Smart Faucet Systems: Government-led retrofit initiatives and evolving green building regulations in key global cities such as New York and Dubai are accelerating the adoption of energy- and water-efficient building systems. These frameworks increasingly mandate the integration of advanced, digitally controlled infrastructure across commercial and hospitality assets. As a result, institutional procurement is shifting toward smart plumbing fixtures, including sensor-based and connected faucet systems, as part of broader building modernization and sustainability compliance efforts.

- Hospitality and Mega-Project Pipelines: GCC nations' infrastructure projects valued at USD 3.7 trillion, including Saudi Arabia's NEOM and the Red Sea Project, are generating multi-year bulk orders for premium specification-grade fixtures.

Market Challenges

- Lead-Free Compliance Transition: Evolving lead-free mandates in California (AB 1953), Canada (NSF 61 Amendment), and EU markets force manufacturers to reformulate alloys, creating material transition costs that disproportionately affect smaller regional producers.

- Distribution Channel Fragmentation: Serving both trade plumbing channels and direct-to-consumer online retail requires differentiated packaging, pricing, and fulfilment capabilities that strain operational resources for manufacturers lacking digital commerce infrastructure.

Emerging Market Trends

1. Accelerating Touchless and Sensor-Based Faucet Adoption

Heightened hygiene standards are accelerating the adoption of touchless faucets, making them a default in high-traffic commercial settings such as healthcare, hospitality, and public infrastructure. Sensor-based technologies are the fastest-growing segment, driven by regulatory focus on hygiene, water efficiency, and user convenience.

2. Smart-Home and IoT Ecosystem Integration

The expansion of smart-home ecosystems is driving increased demand for connected plumbing solutions, including faucets with app-based water monitoring and temperature control features. This trend reflects a broader shift toward integrated home management systems, where connectivity, efficiency, and user convenience are key decision factors. As a result, faucets are evolving from purely functional fixtures into digitally enabled products that support sustainability, personalization, and lifestyle-oriented use cases within modern residential environments.

3. Water Conservation and Sustainability-Led Design

Lead-free stainless steel is gaining traction due to stricter regulations and its durability, safety, and premium positioning, with growth expected to outpace the broader market. Simultaneously, water-efficient features such as low-flow aerators and pressure-compensating systems are becoming standard in mid- to premium-tier faucets, driven by tightening regulations across North America, Europe, and Australia.

4. Premiumization and Design Differentiation

Premium finishes like matte black, brushed gold, and PVD command strong price premiums, driven by consumer demand for aesthetics and durability. Touchless operation and LED temperature indicators are increasingly featured in high-end tiers, transforming faucets from functional fixtures into design-led, lifestyle-oriented elements in kitchens and bathrooms.

5. E-Commerce Channel Expansion

Online faucet sales are projected to grow at a CAGR of 8.8–8.9% through 2030, outpacing offline channels. Home improvement apps, virtual product visualization, and direct-to-consumer platforms are bypassing traditional plumbing distributors, with North America and the Asia Pacific leading in online adoption.

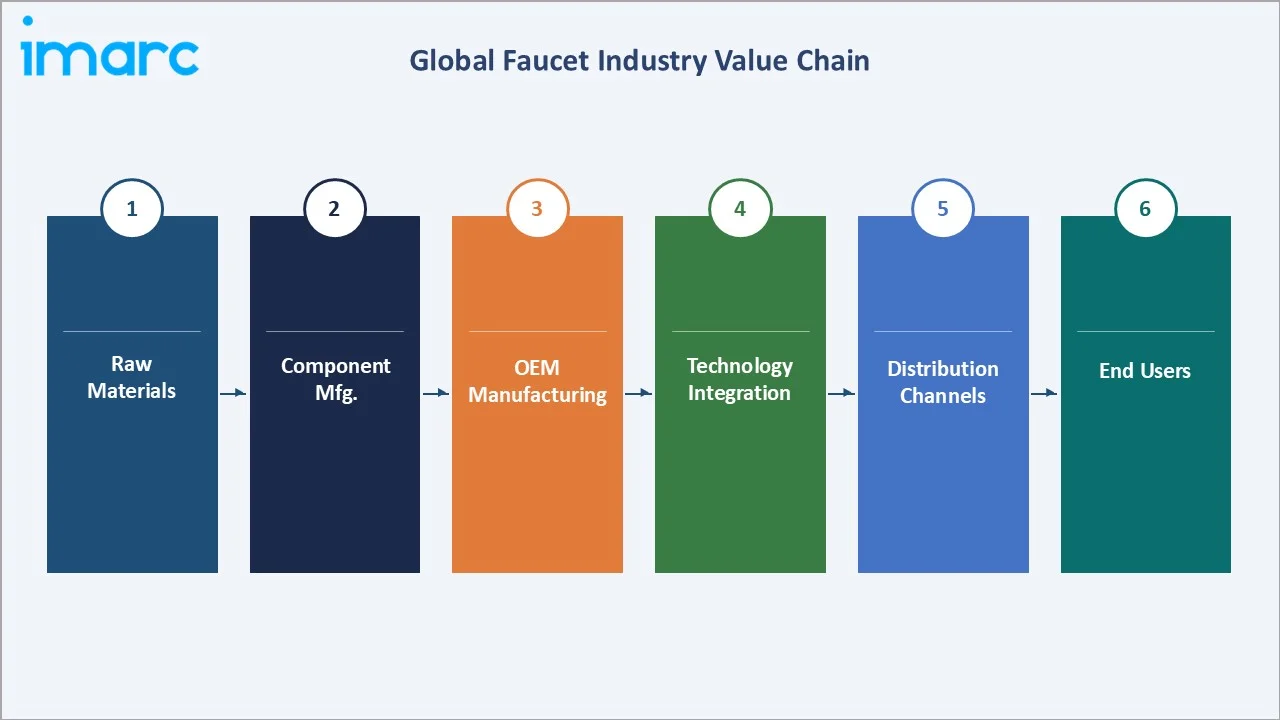

Industry Value Chain Analysis

The global faucet industry value chain spans six integrated stages from raw material supply through end-consumer installation. Each stage presents distinct competitive dynamics, margin profiles, and technology investment requirements relevant to the overall faucet market analysis.

|

Value Chain Stage |

Key Participants / Description |

|

Raw Materials |

Copper, zinc, nickel, lead-free brass alloys, stainless steel, engineering plastics (ABS, POM), ceramic discs |

|

Component Manufacturing |

Cartridge assemblies, ceramic disc valves, aerators, mixing chambers, and seals – produced by Tier-2/Tier-3 suppliers in China, Germany, and India |

|

OEM Manufacturing |

Kohler, LIXIL, Fortune, Delta, TOTO, Hansgrohe, Roca – full product assembly, PVD/chrome finishing, and international certification |

|

Technology Integration |

Infrared/proximity sensor modules, IoT connectivity chips (Wi-Fi/Bluetooth), voice-control systems, and LED temperature indicators |

|

Distribution Channels |

Specialty plumbing & sanitaryware stores (56.7% share), home improvement retail, online platforms (~8.9% CAGR), plumbing contractors |

|

End Users |

Residential homeowners, commercial property developers, hospitality operators, healthcare institutions, and industrial facilities |

OEMs hold the highest strategic value by integrating components, advanced materials, and technology into turnkey solutions. Meanwhile, e-commerce and direct-to-consumer channels are reshaping distribution, letting manufacturers bypass intermediaries, strengthen brand connections, and capture higher margins.

Technology Landscape in the Faucet Industry

Sensor and Touchless Technology

Infrared and proximity sensors continue to dominate touchless faucet technology, particularly in commercial and high-traffic environments. At the same time, capacitive touch and voice-enabled interfaces are gaining traction, reflecting the broader shift toward interactive and connected user experiences. Manufacturers are increasingly consolidating digital platforms and integrating IoT capabilities to enhance functionality, streamline device management, and improve overall consumer experience within smart-home ecosystems.

Ceramic Disc and Cartridge Innovation

Ceramic disc valve technology is gaining widespread adoption due to its superior durability, near drip-free performance, and longer service life compared to traditional washer-based systems. Cartridge-based mechanisms dominate the market, supported by ease of operation and compatibility with modern plumbing systems. Single-lever cartridge designs are increasingly preferred across residential and commercial applications, offering precise temperature control and enhanced user convenience.

Smart Connectivity and IoT Integration

Wi-Fi- and Bluetooth-enabled faucets are transitioning from niche luxury offerings to mainstream smart-home accessories. Integration with leading ecosystems such as Amazon Alexa, Google Home, and Apple HomeKit is expanding, enabling features such as voice control, usage monitoring, and personalized settings. Leading manufacturers are increasingly embedding connectivity into their product portfolios, reflecting a broader shift toward deeper integration of plumbing fixtures within the smart-home ecosystem.

Sustainable Materials Innovation

Physical vapour deposition (PVD) technology is enabling durable, uniform, and cost-efficient premium finishes such as matte black and brushed gold. Stainless steel demand is increasing, supported by lead-free compliance requirements and its durability advantages, with growth expected to outpace the broader market. At the same time, manufacturers are incorporating water-efficient technologies—including aerators, pressure-compensating cartridges, and laminar-flow designs—to meet increasingly stringent flow-rate regulations across key markets.

Market Segmentation Analysis

IMARC Group provides an analysis of the key trends in each segment of the global faucet market, along with forecasts at the global, regional, and country levels from 2026 to 2034. The market has been categorized based on application and end user.

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

One Hand Mixer |

🔒 |

2025 |

|

Application |

Bathroom |

42.2% |

2025 |

|

Technology |

Cartridge |

🔒 |

2025 |

|

Materials |

Metal |

🔒 |

2025 |

| Distribution Channel | Offline | 83.3% | 2025 |

| End User | Residential | 53.3% | 2025 |

|

Region |

Asia Pacific |

33.0% |

2025 |

By Application

Bathroom leads the global faucet market application with a 42.2% share in 2025. Demand is driven by residential renovation activity and the rapid expansion of luxury hotel room inventory. The global bathroom faucet sub-segment was valued at approximately USD 13.79 Billion in 2024 and is projected to grow at 7.6% CAGR through 2030. Sensor-activated and wall-mounted designs are gaining traction across premium residential and hospitality segments. Healthcare and commercial washrooms sustain volume demand with specification-grade touchless models.

To access detailed market analysis, Request Sample

Kitchen faucets account for 38.6% of global application demand. Pull-down and pull-out configurations dominate new residential installations. The commercial kitchen sector, encompassing restaurants, institutional catering, and food processing, creates substantial demand for high-flow, durable models. Consumer preference for filtered water delivery and instant-hot capabilities is expanding average selling prices. The Others segment (19.2%) includes laundry, outdoor, laboratory, and industrial utility faucets.

By End User

Residential is the dominant end user segment at 53.3% of global revenue in 2025. U.S. single-family housing sales reached 724,000 units in early 2024, a 5.1% year-over-year increase per the U.S. Census Bureau. Government-backed housing initiatives in India, China, and the Middle East generate volume demand for affordable and mid-range faucets. Premium residential consumers in North America and Europe are driving smart and designer faucet growth.

Commercial users represent 32.4% of global demand and are the fastest-growing segment, expanding at an estimated CAGR of 8.3% from 2025 to 2030. Hospitality pipeline expansion across GCC, Southeast Asia, and Latin America drives demand. Healthcare institutions are specifying touchless faucets as a standard infection-control measure. Industrial users (14.3%) serve manufacturing, processing, and laboratory facilities with specification-grade flow-control fixtures.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Asia Pacific |

33.0% |

China housing pipeline, India PMAY scheme, ASEAN urbanization, Smart Cities Mission |

|

North America |

24.6% |

U.S. renovation expenditure, EPA WaterSense mandates, smart-home adoption, commercial retrofits |

|

Europe |

22.8% |

EU Ecodesign Regulation, luxury hospitality expansion, lead-free mandates, Water Europe strategy 2025 |

|

Middle East & Africa |

11.2% |

GCC mega-projects (NEOM, Red Sea), Dubai Green Building Regulation, Africa affordable housing |

|

Latin America |

8.4% |

Brazil/Colombia residential construction, growing middle-class upgrades, hospitality sector expansion |

Asia Pacific commands 33.0% global revenue share in 2025. China is the single most important national market, combining massive residential construction with rapidly premiumizing consumers. India’s Pradhan Mantri Awas Yojana (Urban) targets the development of over 11 million affordable urban homes, creating a large and structured procurement pipeline for building materials and fixtures. This government-led housing initiative is a key demand driver for cost-efficient, standardized faucet solutions across the affordable housing segment. Asia Pacific is also forecast to be the fastest-growing region, advancing at approximately 7.4% CAGR through 2034.

North America holds 24.6% of global revenue, anchored by U.S. renovation spending reaching USD 485 Billion in 2024. The U.S. is the world's largest smart faucet market. EPA WaterSense programmes incentivize low-flow certified fixtures. Water-efficiency mandates at the federal and state levels are standardizing compliance targets and accelerating replacement cycles for non-compliant fixtures.

Europe holds 22.8%, characterized by high design expectations, robust sustainability legislation, and renovation activity in France, Germany, and the UK. In June 2025, Water Europe launched a water resilience strategy reinforcing the EU's building water-stewardship targets. The Middle East and Africa represent 11.2%, driven by GCC mega-projects. Dubai's Green Building Regulation expansion in March 2025 is boosting the specification of water-efficient fixtures. Latin America accounts for 8.4%, led by Brazil, Colombia, and Argentina, through residential construction and a growing urban middle class.

Competitive Landscape

|

Company Name |

Key Platform / Brand |

Market Position |

Core Strength |

|

Kohler Co. |

Kohler, Kallista, Sterling |

Leader |

Design leadership, smart faucets, global distribution |

|

Fortune Brands Innovations |

Moen, ROHL, Riobel |

Leader |

Motionsense touchless tech, North America dominance |

|

Delta Faucet (Masco) |

Delta, Brizo, Peerless |

Leader |

Touch2O, VoiceIQ, broad residential/commercial range |

|

LIXIL Corporation |

American Standard, GROHE |

Leader |

Global scale, water efficiency, Asia Pacific reach |

|

TOTO Ltd. |

TOTO, Neorest |

Leader |

Hygiene innovation, Japan/Asia Pacific premium |

|

Hansgrohe SE |

Hansgrohe, Axor |

Challenger |

German engineering, sustainable design, European premium |

|

Roca Sanitario |

Roca, Laufen |

Challenger |

Southern Europe/Latin America strength, eco innovation |

|

Jaquar Group |

Jaquar, Artize |

Emerging |

India and South Asia leadership, premium positioning |

The global faucet market's competitive landscape is moderately fragmented, with global powerhouses competing alongside regional specialists and high-volume Asian manufacturers. Leading players compete on product innovation, IoT integration, distribution reach, certification compliance, and sustainability credentials. Strategic acquisitions are a key tool - Fortune Brands Innovations acquired SpringWell Water Filtration Systems in February 2024 to extend its whole-home water ecosystem capabilities.

Key Company Profiles

Kohler Co.

Kohler Co. is the global leader in kitchen and bath design, headquartered in Kohler, Wisconsin, USA. Founded in 1873, it operates across plumbing, power, and hospitality sectors with a presence in over 50 countries.

- Product & Platform Portfolio: Kohler's faucet portfolio spans the Kohler, Kallista, Sterling, and Artifacts product lines, covering smart faucets, touchless designs, pull-down kitchen models, and luxury bath collections.

- Recent Developments: In January 2021, Kohler Co. expanded its smart home portfolio at CES with a focus on wellness, launching the Stillness Bath, Innate Intelligent Toilet, touchless faucet collection, and Phyn-powered whole-home water monitoring systems (DIY and Pro with automatic shut-off).

- Strategic Focus: Kohler's strategy centers on smart-home ecosystem integration, design-led premiumization, and expansion in high-growth emerging markets, particularly in India and Southeast Asia, where luxury residential and hospitality construction is accelerating.

Fortune Brands Innovations

Fortune Brands Innovations, headquartered in Deerfield, Illinois, is a leading provider of home, security, and building products, serving residential and commercial markets globally.

- Product & Platform Portfolio: Its portfolio includes Moen and House of Rohl faucets, Therma‑Tru and Larson doors, Fiberon outdoor living products, and security solutions from Master Lock, Yale, August, and SentrySafe.

- Recent Developments: In October 2022, Fortune Brands Innovations’ flagship brand Moen, is highlighting new research revealing that inexpensive, off-brand, foreign-made faucets may pose significant health risks to consumers.

- Strategic Focus: Fortune Brands focuses on innovation, connected home solutions, and category leadership, aiming for global growth and operational excellence.

Delta Faucet Company

Delta Faucet Company, a division of Masco Corporation, is one of the largest and most recognized faucet brands globally. Headquartered in Indianapolis, Indiana, Delta operates across residential and commercial product categories.

- Product & Platform Portfolio: Delta's portfolio includes Touch2O touch-activated faucets, VoiceIQ voice-controlled models, the Brizo luxury brand, and the new ShowerSense Digital Shower system featuring Wi-Fi connectivity and 12 programmable presets.

- Recent Developments: In February 2025, Delta showcased its latest product innovations at the Kitchen and Bath Industry Show (KBIS) in Las Vegas. Also in February 2025, Delta migrated its legacy VoiceIQ platform to the DFC@Home platform, consolidating voice and IoT device management.

- Strategic Focus: Delta's strategy focuses on expanding its Touch2O and VoiceIQ technology ecosystem, growing the Brizo premium brand in international hospitality markets, and leveraging Masco Corporation's distribution scale to maintain leadership across North American retail and trade channels.

Market Concentration Analysis

The global faucet market exhibits moderate fragmentation. The top four players - Kohler, Delta, LIXIL, and TOTO - collectively account for 30-38% of global market revenue in 2025. The remaining market share is distributed across Hansgrohe, Roca, Jaquar, and a large number of regional Chinese and Indian manufacturers.

The market is experiencing a bifurcated dynamic. At the premium OEM tier, consolidation is occurring around brand equity, IoT platform capabilities, and sustainability certification. Simultaneously, the Chinese and Indian domestic markets are generating competitive challengers that are increasingly targeting international export markets with cost-competitive, design-improved products. This dual dynamic is intensifying competition across all price tiers and geographies through 2034.

Investment & Growth Opportunities

Fastest-Growing Segments

Online channel sales are the highest-growth distribution sub-segment at approximately 8.9% CAGR through 2030. Commercial end users are the fastest-growing application tier at 8.3% CAGR. Smart and sensor-activated faucets represent the premium technology growth opportunity, with demand reaching 22 million units in 2025 and continuing to expand as smart-home ecosystems achieve mainstream adoption.

Emerging Market Expansion

India represents the highest-potential emerging market, driven by the PMAY housing scheme targeting 20 million affordable homes and rapid premiumization among urban middle-class consumers. Southeast Asia's hospitality expansion, GCC mega-projects, and Sub-Saharan Africa's urban sanitation infrastructure programs collectively represent significant volume growth opportunities for manufacturers with local distribution capabilities.

Venture and Strategic Investment Trends

Strategic acquisitions are reshaping the competitive landscape. Fortune Brands Innovations acquired SpringWell Water Filtration Systems in February 2024 to extend its whole-home water ecosystem. Investments in IoT connectivity platforms, lead-free material R&D, and AI-powered water management systems are the primary focus areas for venture and corporate capital in the faucet industry through 2034.

Future Market Outlook (2026-2034)

The global faucet market forecast projects steady value expansion from USD 33.0 Billion in 2025 to USD 59.3 Billion by 2034 at a CAGR of 6.37%. Asia Pacific will retain regional leadership while accelerating structurally. North America and Europe will sustain premium value growth through renovation spending and regulatory compliance cycles.

Three key shifts will reshape the faucet market through 2034. Smart-home convergence will embed faucet controls into integrated home systems, making connected fixtures standard in new builds by 2028–2030. Tightening water-scarcity regulations will drive adoption of sub-6 L/min flow standards. Meanwhile, Chinese and Indian manufacturers are expected to reach premium design and quality benchmarks, intensifying global competition across price tiers.

Research Methodology

Primary Research

Primary research encompassed structured interviews conducted in 2024-2025 with faucet industry stakeholders, including product directors at OEM manufacturers, procurement managers at commercial property developers, retail buyers at home improvement chains, and institutional investors in building products. Primary insights validated market sizing, segmentation estimates, and technology adoption timelines.

Secondary Research

Secondary sources include U.S. Census Bureau housing data, EPA WaterSense program reports, Harvard Joint Center for Housing Studies, Water Europe publications, IEA infrastructure data, company annual reports, trade publications including Architectural Digest, Kitchen and Bath Business, and Plumbing & Mechanical Engineer, and regional construction association databases.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating GDP growth rates, urbanization indices, construction activity data, and historical market evolution patterns. Scenario analysis (base, optimistic, and conservative cases) was performed to account for macroeconomic uncertainty.

Faucet Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | One Hand Mixer, Two Hand Mixer, Others |

| Applications Covered | Bathroom, Kitchen, Others |

| Technologies Covered | Cartridge, Compression, Ceramic Disc, Ball |

| Materials Covered | Metal, Plastics |

| Distribution Channels Covered | Online, Offline |

| End Users Covered | Residential, Commercial, Industrial |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Kohler Co., Fortune Brands Innovations, Delta Faucet (Masco), LIXIL Corporation, TOTO Ltd., Hansgrohe SE, Roca Sanitario, Jaquar Group, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the faucet market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global faucet market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the faucet industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Faucet Market Report

The global faucet market was valued at USD 33.0 Billion in 2025, driven by urbanization, residential construction, and growing demand for water-efficient and smart plumbing fixtures globally.

The market is projected to reach USD 59.3 Billion by 2034, growing at a CAGR of 6.37% during 2026-2034, supported by renovation expenditure, IoT integration, and sustainability-led design.

Bathroom applications lead with a 42.2% share in 2025, driven by premium renovation activity, rapid hotel room inventory expansion, and rising consumer preference for spa-like bathroom aesthetics.

The commercial segment is the fastest-growing end user category, expanding at an estimated CAGR of 8.3% through 2030, driven by hospitality infrastructure expansion and healthcare's increasing specification of touchless faucets.

Asia Pacific dominates with a 33.0% share in 2025. China's construction pipeline, India's PMAY housing scheme, and rapid middle-class urbanization across Southeast Asia underpin its leadership.

Key drivers include global urbanization, rising residential and commercial construction, water conservation regulations, EPA WaterSense mandates, EU Ecodesign requirements, smart-home adoption, and renovation expenditure, particularly in the U.S. and Europe.

Major players include Kohler Co., Fortune Brands Innovations, Delta Faucet (Masco), LIXIL Corporation, TOTO Ltd., Hansgrohe SE, Roca Sanitario, and Jaquar Group.

Sensor-based and touchless faucets are the fastest-growing technology segment, advancing at approximately 9.1% CAGR from 2025 to 2030, driven by hygiene requirements, smart-home integration, and water efficiency incentive programs.

Key opportunities include IoT-enabled smart faucet platforms, commercial sector retrofitting, India and Southeast Asia market expansion, sustainable lead-free product lines, and direct-to-consumer online channel development targeting the rapidly growing e-commerce segment.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)