Fire Sprinklers Market Size, Share, Trends and Forecast by Product Type, Service, Component, Application, Technology, and Region, 2026-2034

Global Fire Sprinklers Market Size, Share, Trends & Forecast (2026-2034)

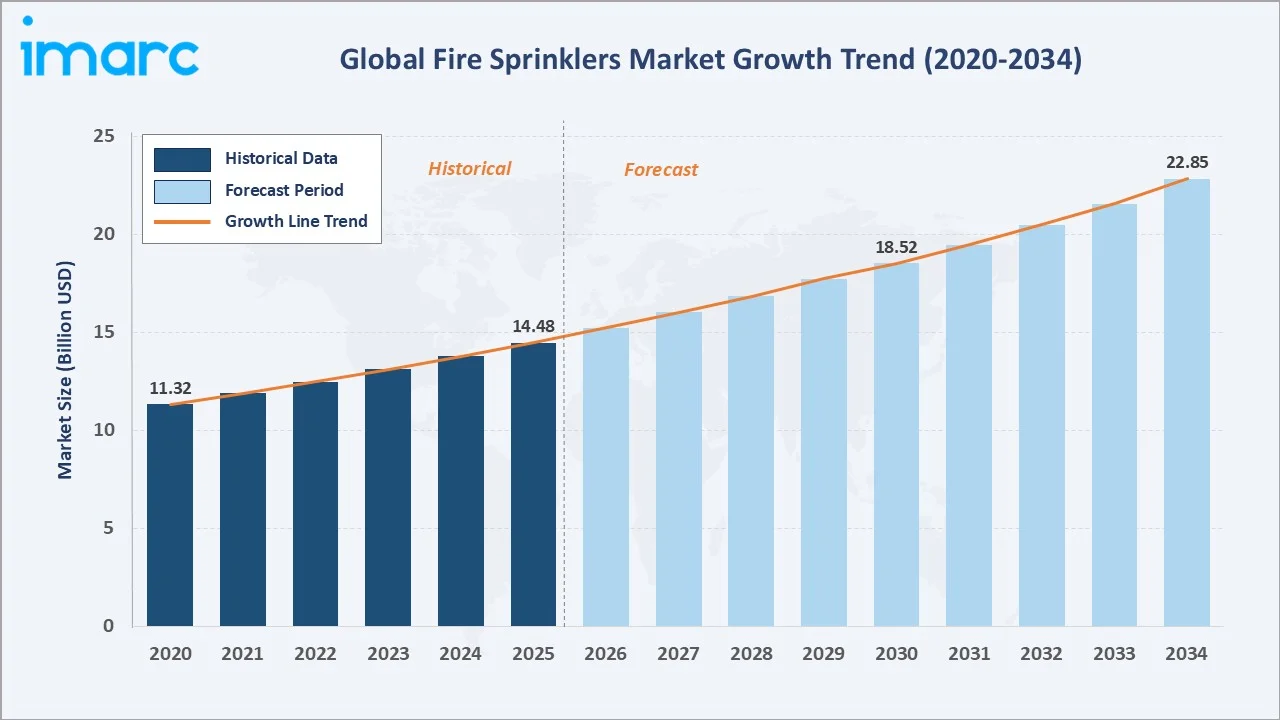

The global fire sprinklers market size reached USD 14.48 Billion in 2025 and is projected to reach USD 22.85 Billion by 2034, exhibiting a CAGR of 5.04% during 2026-2034. Stringent fire safety codes accelerated commercial and data center construction, and IoT-enabled smart fire protection adoption are the primary forces driving market expansion.

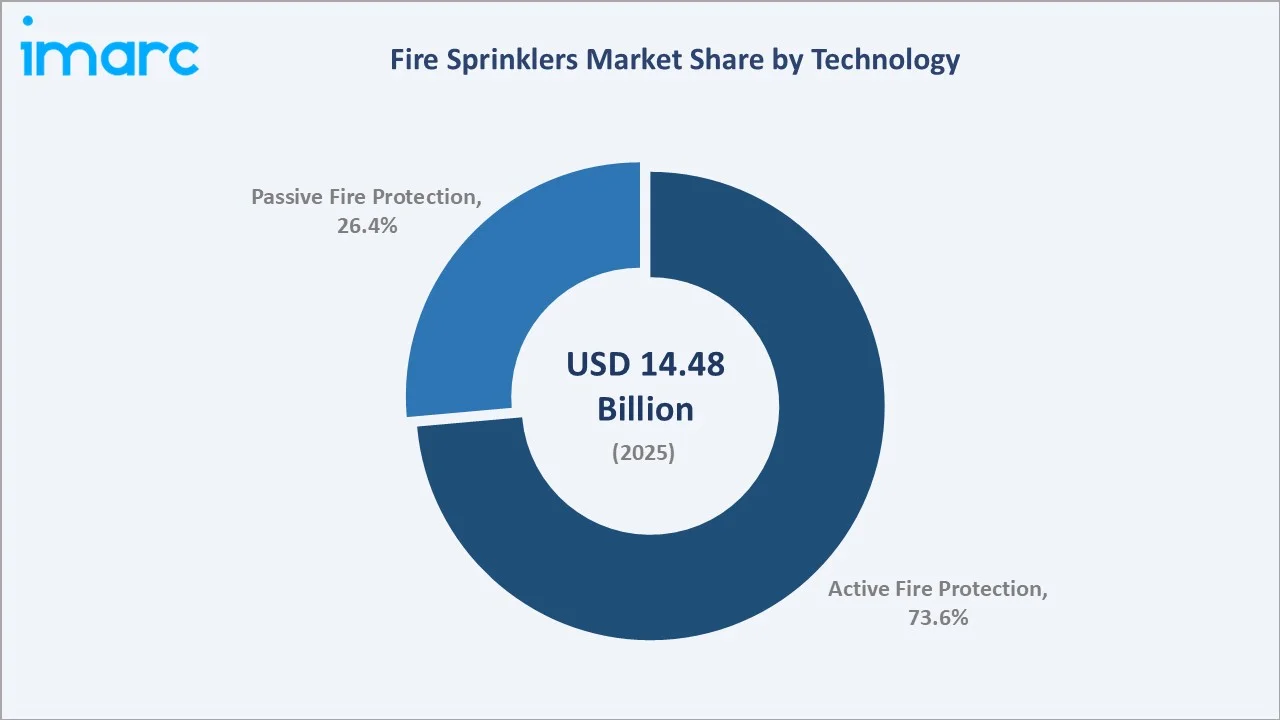

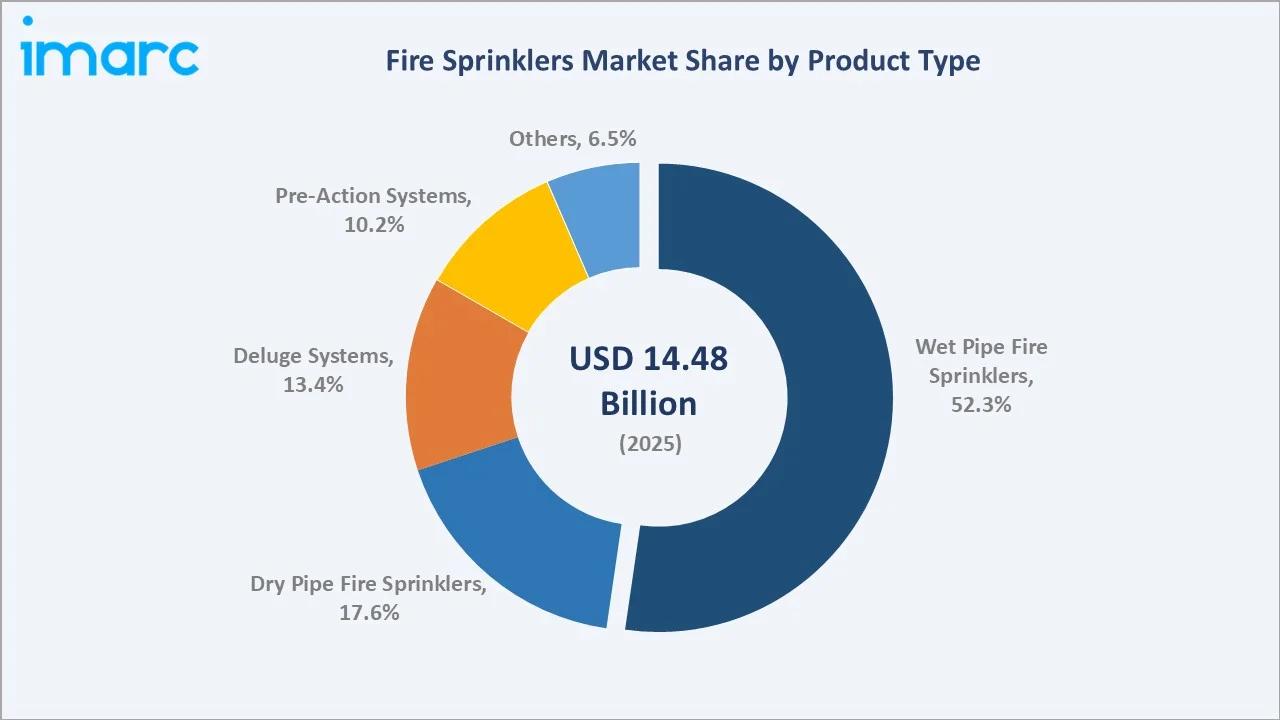

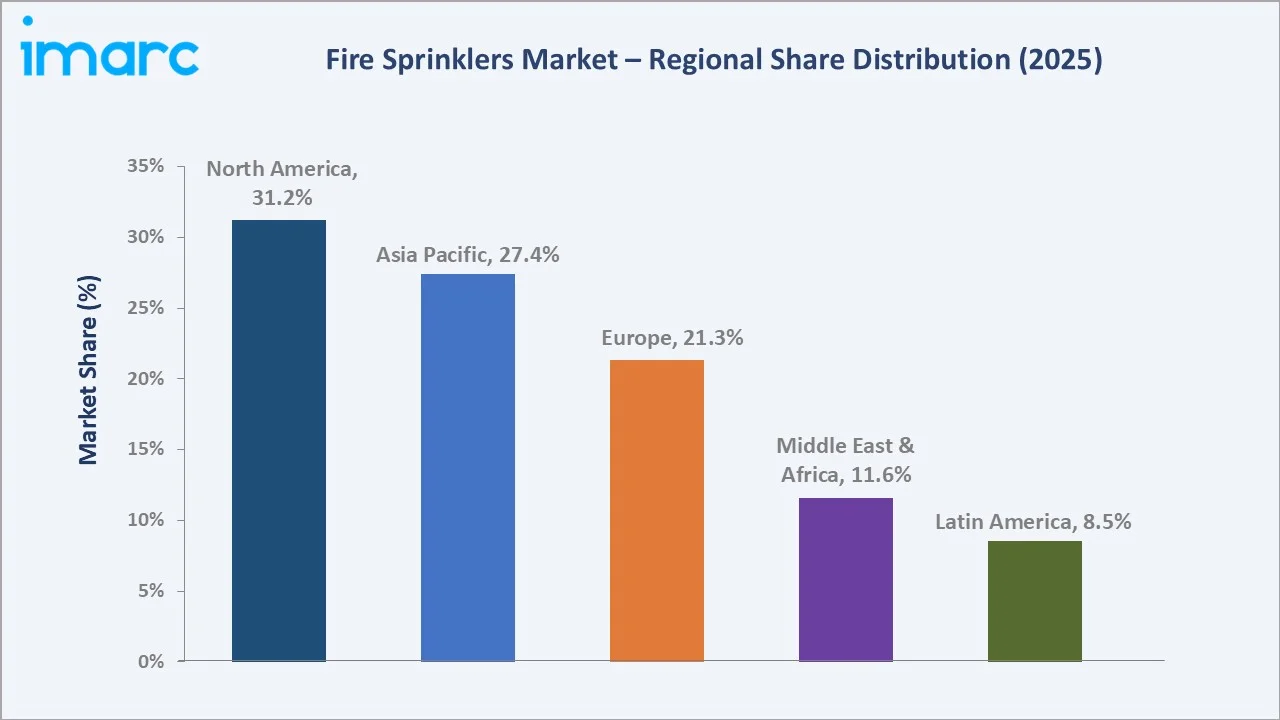

Active fire protection dominates at 73.6% in 2025, while wet pipe fire sprinklers lead the product mix at 52.3%. North America commands a dominant 31.2% regional share in 2025, reflecting stringent NFPA enforcement and mature retrofit demand.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 14.48 Billion |

|

Forecast Market Size (2034) |

USD 22.85 Billion |

|

CAGR (2026-2034) |

5.04% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North America (31.2% share, 2025) |

|

Second Largest Region |

Asia Pacific (27.4% share, 2025) |

|

Leading Technology |

Active Fire Protection (73.6%, 2025) |

|

Leading Product Type |

Wet Pipe Fire Sprinklers (52.3%, 2025) |

The global fire sprinklers market growth trajectory from 2020 through 2034, with the historical expansion to USD 14.48 Billion in 2025, reflects consistent regulation-driven demand, while the forecast to USD 22.85 Billion captures accelerating smart building adoption, commercial construction, and retrofit-led procurement through 2034.

To get more information on this market, Request Sample

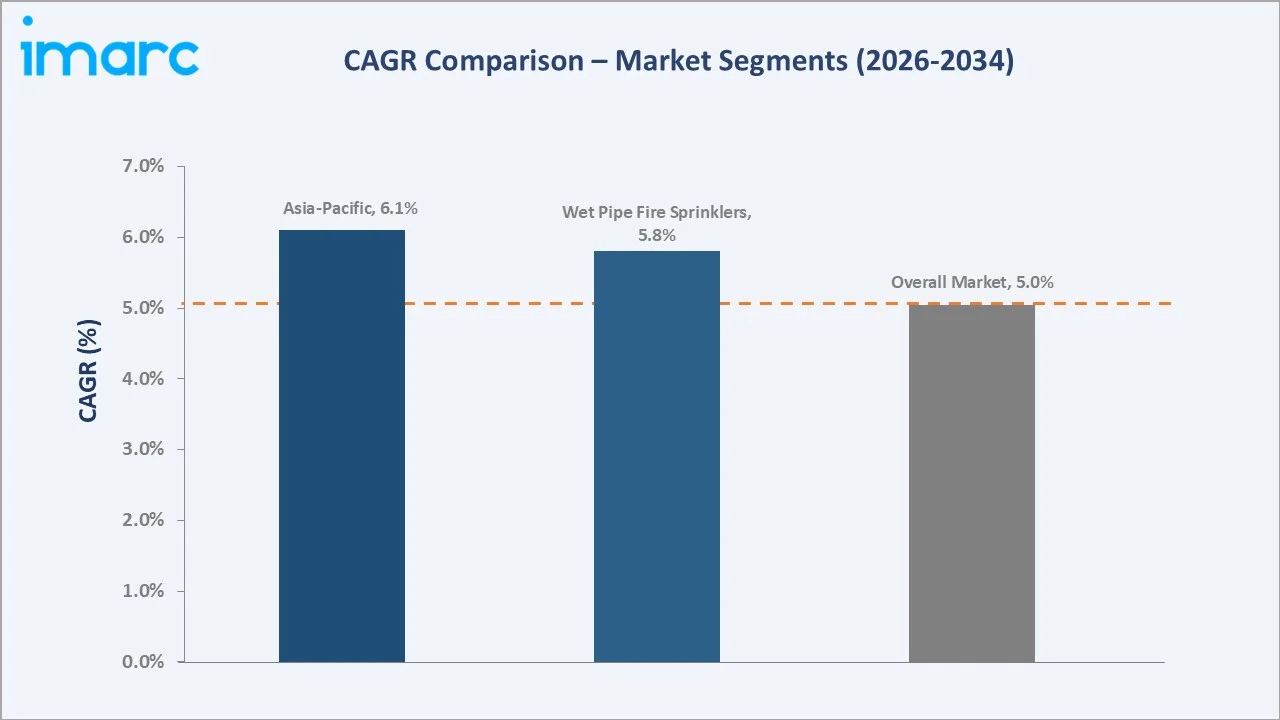

The CAGR trajectories across key product type, technology, and regional sub-segments, with Asia Pacific at ~6.1% CAGR and wet pipe fire sprinklers at ~5.8% CAGR, are the fastest-growing categories within the global fire sprinklers industry analysis through 2034.

Executive Summary

The global fire sprinklers market is on a sustained growth trajectory from USD 14.48 Billion in 2025 to USD 22.85 Billion by 2034. Fire sprinklers, an essential life-safety component deployed across commercial, residential, and industrial facilities, benefit from the non-discretionary, regulation-driven nature of their demand.

Active fire protection dominates the technology split at 73.6% in 2025, owing to its code-mandated status across most commercial building classes and its proven efficacy in suppressing fires before brigade arrival. Passive fire protection (26.4%) complements this layer through compartmentation and fire-rated assemblies.

Wet pipe fire sprinklers lead the product mix at 52.3% in 2025, reflecting their cost-efficiency and reliability in heated buildings. Dry pipe (17.6%), deluge (13.4%), pre-action (10.2%), and other systems (6.5%) address specialised cold, high-hazard, and mission-critical applications respectively across diverse end-use settings.

Key Market Insights

|

Insight |

Data |

|

Leading Technology |

Active Fire Protection - 73.6% share (2025) |

|

Leading Product Type |

Wet Pipe Fire Sprinklers - 52.3% share (2025) |

|

Leading Region |

North America - 31.2% share (2025) |

|

Second Largest Region |

Asia Pacific - 27.4% share (2025) |

|

Top Companies |

Honeywell International Inc., Johnson Controls, APi Group, Bosch Sicherheitssysteme GmbH, Hochiki Corporation, Siemens |

Key Analytical Observations Expanding on the Above Data:

- Active fire protection, with 73.6% in 2025, dominates because codes mandate sprinklers, pumps, and detection as the primary life-safety layer across commercial, healthcare, hospitality, and high-rise residential segments globally.

- Wet pipe fire sprinklers, with 52.3% in 2025, lead the product segment as the simplest, most cost-effective configuration. Continuously pressurised water enables immediate discharge, making wet pipe the default NFPA 13 specification for heated commercial and residential buildings.

- North America commands 31.2% in 2025 reflecting its deeply codified fire-safety regime. NFPA 13 and NFPA 25 mandates, state-level retrofit rules, and insurance-linked requirements generate the world’s largest sprinkler procurement and services market.

- Asia Pacific, with 27.4% in 2025, benefits from accelerating high-rise construction across China, India, Southeast Asia, and Japan alongside strengthening fire codes, translating into the fastest regional CAGR through 2034.

Global Fire Sprinklers Market Overview

Fire sprinklers are automatic water-based suppression systems installed in buildings to detect and control fires, comprising sprinkler heads, piping networks, valves, pumps, and alarm components. Systems are configured as wet pipe, dry pipe, deluge, or pre-action depending on occupancy hazard, ambient conditions, and specification codes.

The global ecosystem integrates component manufacturers, system integrators, engineering firms, regional distributors, licensed installation contractors, and diverse end-use segments spanning commercial real estate, hospitality, healthcare, data centers, warehousing, and industrial manufacturing.

Market Dynamics

To evaluate market opportunities, Request Sample

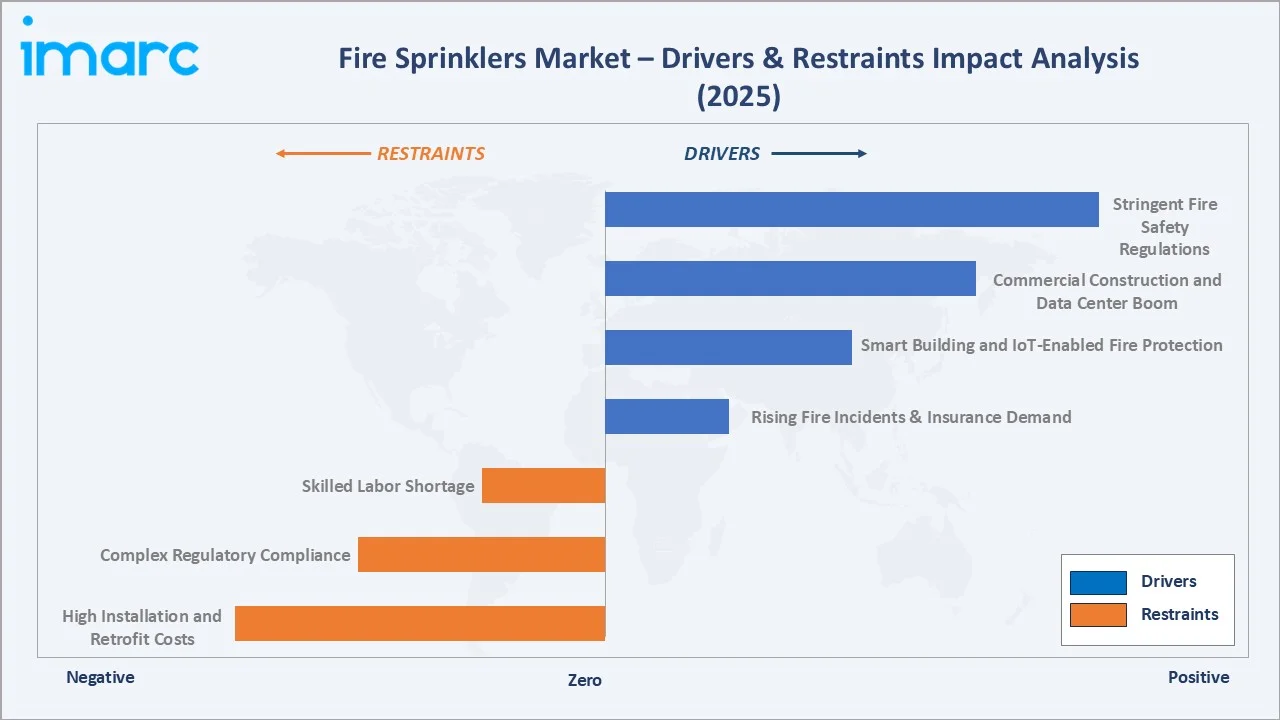

Market Drivers

- Stringent Fire Safety Regulations: NFPA 13 and NFPA 25 in North America, EN 12845 in Europe, and strengthening national codes in Asia Pacific are mandating sprinkler installation across a broadening range of occupancies, including residential high-rises, care facilities, and warehouses, driving continuous new-build and retrofit procurement globally.

- Commercial Construction and Data Center Boom: Nearly 100 GW of new data centers between 2026 and 2030 and sustained commercial real estate construction are generating dense sprinkler specification per square foot, particularly pre-action and clean-agent hybrid systems for mission-critical rooms with high-value IT equipment assets.

- Smart Building and IoT-Enabled Fire Protection: IoT-connected sprinkler monitoring, cloud-based inspection logging, and predictive maintenance analytics are becoming standard specifications in new commercial developments, creating premium price points and recurring software-and-services revenue streams for leading system integrators worldwide.

Market Restraints

- High Installation and Retrofit Costs: Sprinkler retrofits in existing multi-story residential and historic commercial buildings carry significant costs due to concealed piping, structural modifications, and disruption to occupants. Budget constraints in emerging markets delay voluntary upgrades despite evident fire-loss reduction benefits.

- Complex Regulatory Compliance: Divergent national codes, frequent revisions, and jurisdiction-specific amendments require extensive engineering adaptation. Multinational owners must navigate NFPA, EN, BS, GB, and JIS standards simultaneously, increasing design cost and lengthening project timelines for globally active contractors.

Market Opportunities

- Data Center and Hyperscale Facility Expansion: AI computing infrastructure is driving a doubling of global data center capacity by 2030, each facility requiring dense pre-action sprinkler zones, VESDA integration, and bespoke hazard-specific designs, generating elevated revenue per installed square foot relative to conventional commercial projects globally.

- Green and Smart Building Retrofits: LEED, BREEAM, and WELL certification schemes reward advanced fire-safety integration, while aging commercial stock across Europe and North America requires sprinkler modernization. Duplex systems combining low-flow heads and digital monitoring are creating premium upgrade opportunities for well-capitalized suppliers.

Market Challenges

- Skilled Labor Shortage: Licensed sprinkler fitters and NICET-certified designers are in short supply across North America and Europe. Aging workforce demographics and lengthy apprenticeship cycles are constraining installation capacity precisely when retrofit demand and new construction are accelerating in tandem across most major markets.

- Water Damage and Liability Concerns: Perceived risk of accidental discharge, pipe leakage, and freeze damage in dry and pre-action systems continues to shape owner specifications in data-center and heritage assets, increasing adoption of hybrid and clean-agent solutions and complicating standard wet-pipe sprinkler market penetration.

Emerging Market Trends

1. IoT-Enabled Smart Sprinkler Systems Transforming Fire Protection

IoT integration across fire sprinkler networks is enabling continuous pressure monitoring, leak detection, remote inspection, and cloud-based compliance reporting. Platforms reduce false alarms, shorten inspection cycles by 30-40%, and generate recurring services revenue for integrators while improving building-level safety outcomes for insurers, facility managers, and regulatory authorities alike.

2. Early Suppression Fast Response (ESFR) Technology in Warehouses

ESFR sprinkler adoption is accelerating in high-piled warehousing, fulfilment centers, and cold storage facilities, where rapid activation and high-volume discharge can suppress rather than merely control fires. The technology is replacing traditional in-rack sprinklers in many configurations, reducing design complexity and total installation cost.

3. Eco-Friendly and Water-Efficient Sprinkler Designs

Sustainability pressures are driving specification of low-flow sprinkler heads, recycled-content piping, and water-conservation design approaches. Manufacturers are introducing heads that maintain NFPA compliance while reducing discharge volumes, aligning fire protection with broader building decarbonization and water stewardship goals increasingly required by green certification frameworks.

4. AI-Based Predictive Maintenance and Digital Twin Integration

AI-enabled analytics applied to sprinkler inspection and hydraulic data are enabling predictive maintenance scheduling, reducing unplanned failures, and supporting digital twin models of building fire-safety systems. Integration with building information modeling and facility management platforms is becoming a key differentiator for tier-one integrators serving institutional clients.

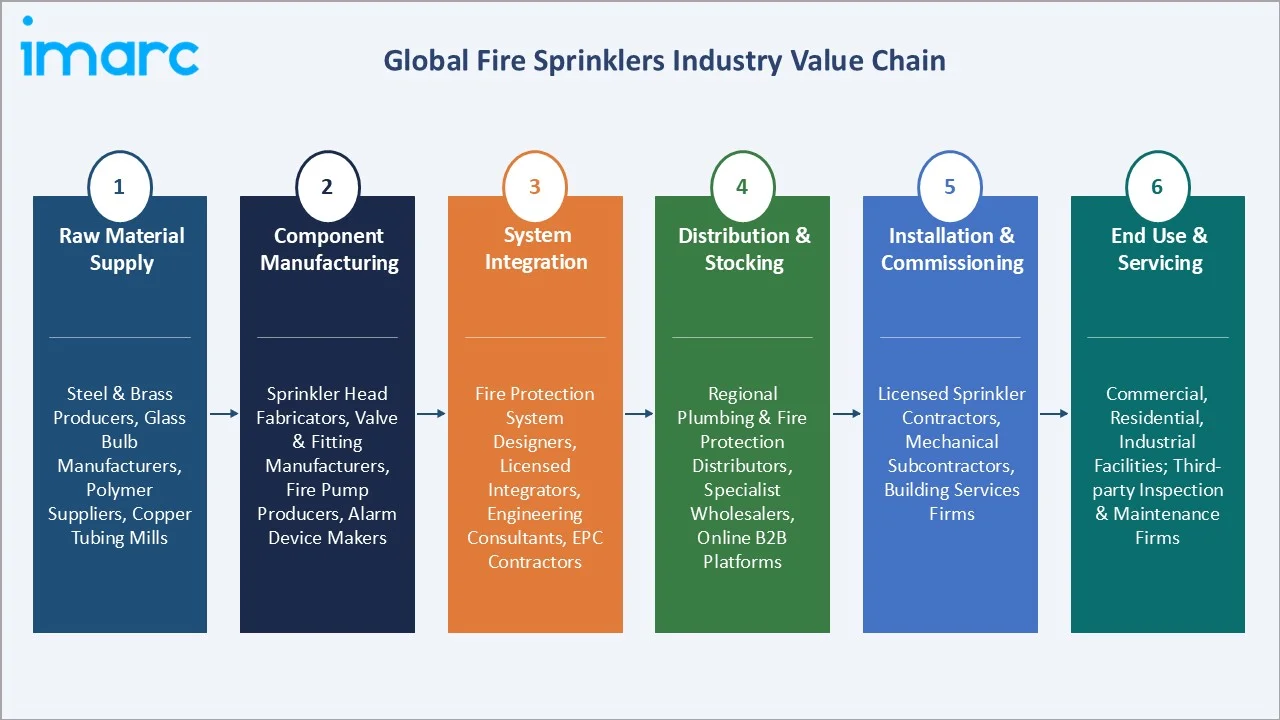

Industry Value Chain Analysis

The fire sprinklers value chain spans six stages from raw material input through end-use servicing. System integration, installation, and inspection services capture the highest value-add margins, while component manufacturing is increasingly commoditised. Long-cycle servicing contracts generate predictable recurring revenue for well-positioned regional and multinational firms.

|

Stage |

Key Players / Examples |

|

Raw Material Supply |

Steel and brass producers, glass bulb manufacturers, polymer suppliers, copper tubing mills |

|

Component Manufacturing |

Sprinkler head fabricators, valve and fitting manufacturers, fire pump producers, alarm device makers |

|

System Integration |

Fire protection system designers, licensed integrators, engineering consultants, EPC contractors |

|

Distribution & Stocking |

Regional plumbing and fire protection distributors, specialist wholesalers, online B2B platforms |

|

Installation & Commissioning |

Licensed sprinkler contractors, mechanical subcontractors, building services firms |

|

End Use & Servicing |

Commercial, Residential, Industrial facilities; third-party inspection and maintenance firms |

Integrated players combining manufacturing, engineering design, and installation services, such as Johnson Controls and APi Group, capture multi-stage margins and benefit from cross-sell of inspection and servicing revenue. Vertical integration is a meaningful competitive advantage in large commercial and industrial project segments where buyers consolidate suppliers.

Technology Landscape in the Fire Sprinklers Industry

Sprinkler Head Technology: Quick Response and ESFR

Quick response (QR) and ESFR sprinkler heads, activating within seconds of ceiling-level temperature rise, are progressively replacing standard response heads in most new specifications. QR heads improve life-safety outcomes in residential and assembly occupancies, while ESFR heads target high-hazard storage environments with large-droplet, high-momentum water delivery patterns.

Piping Materials: CPVC, Steel, and Hybrid Systems

CPVC piping is gaining share in light-hazard residential and commercial applications owing to its corrosion resistance, ease of installation, and lower labor costs. Black steel and galvanized steel remain dominant in ordinary and extra-hazard classifications, while stainless steel is specified for corrosive environments and seismic zones.

Digital Design and BIM Object Libraries

Fire sprinkler manufacturers are investing in BIM-compatible product libraries for Autodesk Revit, Hydratec, and AutoSPRINK platforms. Parametric sprinkler families enable automated hydraulic calculations, clash detection with HVAC and structural elements, and streamlined coordination with fire alarm and security subsystems across complex multi-trade projects.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

| Product Type | Wet Pipe Fire Sprinklers | 52.3% |

2025 |

| Service |

🔒 |

🔒 |

2025 |

| Component | Stop Valve |

🔒 |

2025 |

| Application | Commercial Applications | 58.7% |

2025 |

| Technology | Active Fire Protection | 73.6% |

2025 |

|

Region |

North America | 31.2% |

2025 |

By Technology

Active fire protection commands a 73.6% majority share in 2025 owing to its code-mandated role as the primary life-safety barrier in commercial, high-rise residential, healthcare, hospitality, and industrial occupancies. Sprinklers, pumps, detection, and alarms collectively constitute the active layer specified across virtually every regulated new-build project globally.

To access detailed market analysis, Request Sample

Passive fire protection at 26.4% in 2025 complements active systems through fire-rated walls, floors, doors, intumescent coatings, and compartmentation. Although capturing a smaller share, passive solutions are growing steadily as building codes increasingly require layered fire-safety strategies combining suppression with containment to protect occupants and limit property loss.

By Product Type

Wet pipe fire sprinklers dominate the product type segment at 52.3% in 2025, representing the default specification for heated buildings across commercial, residential, and light-industrial occupancies. Continuously charged piping, simple design, and lowest-cost maintenance profile make wet pipe the first-choice configuration under NFPA 13 and equivalent standards.

Dry pipe fire sprinklers, with 17.6% in 2025, serve unheated spaces such as parking garages, freezer warehouses, and attics, where frozen water would compromise wet systems. Deluge systems (13.4%) are specified for high-hazard applications including aircraft hangars and chemical storage, using open heads and simultaneous discharge across protected zones.

Pre-action systems, with 10.2% in 2025, protect water-sensitive environments such as data centers, museums, and archives where accidental discharge is unacceptable. They require dual activation through both detection and sprinkler operation. Other specialized systems (6.5%) include foam-water, antifreeze, and combined sprinkler-standpipe configurations serving niche industrial and marine applications globally.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

North America |

31.2% |

Strict NFPA codes; commercial construction; data center boom; retrofit mandates |

|

Asia Pacific |

27.4% |

Rapid urbanization; China and India high-rise construction; industrial facility expansion |

|

Europe |

21.3% |

EN 12845 enforcement; green building retrofits; aging infrastructure upgrades |

|

Middle East & Africa |

11.6% |

GCC Vision 2030 mega-projects; NEOM construction; hospitality sector growth |

|

Latin America |

8.5% |

Brazil commercial construction; Mexico industrial parks; rising fire safety regulations |

North America’s 31.2% market dominance in 2025 is driven by the world’s most codified fire-safety regime. NFPA 13 and NFPA 25 compliance, state-level high-rise retrofit mandates in cities such as New York and Chicago, and insurance-driven specification requirements collectively sustain the largest sprinkler procurement and inspection-services market globally.

Asia Pacific, with 27.4% in 2025, is experiencing the fastest regional growth. China’s high-rise residential stock, India’s commercial real-estate expansion, ASEAN industrial park development, and Japan’s seismic-retrofit activity collectively anchor demand. Strengthening national fire codes and rising insurance penetration are accelerating sprinkler specification across previously under-served segments regionally.

Competitive Landscape

The global fire sprinklers market is moderately consolidated, with a small group of global leaders serving multinational customers across broad product and service portfolios, while regional specialists hold strong local positions. Competitive intensity is rising as IoT and services revenue reshape differentiation beyond traditional hardware pricing dynamics.

|

Company Name |

Key Products |

Market Position |

Global Strategic Focus |

|

Honeywell International Inc. |

Sprinkler monitoring devices, control panels, smart fire protection systems |

Leader |

Global; IoT-enabled solutions; smart buildings |

|

Johnson Controls |

Tyco Sprinklers, wet and dry pipe systems, deluge valves |

Leader |

Global; broadest product range; retrofit services |

|

APi Group |

Installation, inspection, and service of sprinkler systems |

Leader |

North America; largest services platform |

|

Bosch Sicherheitssysteme GmbH |

Fire detection, control panels, integrated sprinkler solutions |

Challenger |

Europe and APAC; technology-led integration |

|

Hochiki Corporation |

Detection devices, alarm valves |

Challenger |

Global component specialist |

|

Siemens |

Cerberus fire protection, sprinkler control systems |

Leader |

Global; smart building and digital integration |

Key players include Honeywell International Inc., Johnson Controls, APi Group, Bosch Sicherheitssysteme GmbH, Hochiki Corporation, Siemens, and others.

Key Company Profiles

Honeywell International Inc.

Honeywell International is a leading global provider of fire protection, detection, and building automation solutions. Its fire portfolio spans sprinkler heads, control panels, and IoT-enabled smart protection platforms, leveraging the company’s broader building technologies ecosystem to deliver integrated life-safety outcomes.

- Product Portfolio: Sprinkler heads, control panels, smart fire protection and detection platforms.

- Recent Developments: In October 2025, Honeywell introduced its NOTIFIER INSPIRE system in Canada, a next-generation fire and life safety solution designed to simplify installation, improve maintenance efficiency, and support regulatory compliance.

- Strategic Focus: Honeywell’s strategy emphasizes IoT-enabled smart fire protection, cross-selling across its building technologies portfolio, and capturing recurring software and services revenue from digital monitoring and predictive maintenance contracts with large commercial and institutional customers globally.

Johnson Controls

Johnson Controls, through its Tyco Fire Protection Products brand, is among the world’s largest fire protection companies, offering the broadest sprinkler product range covering wet pipe, dry pipe, deluge, and pre-action configurations alongside inspection and servicing capabilities.

- Product Portfolio: Tyco Fire sprinklers, control valves, deluge systems, and full-scope inspection and servicing.

- Recent Developments: In June 2025, Johnson Controls relaunched its Connected Sprinkler service, introducing an upgraded digital solution designed to enhance fire safety and maintenance efficiency across buildings. The service provides facility managers with real-time insights into sprinkler system performance by monitoring key indicators such as temperature, pressure, and water presence.

- Strategic Focus: Johnson Controls focuses on maintaining global leadership through the broadest sprinkler and fire-suppression product range, deep retrofit and servicing footprint, and digital platforms that create switching costs and recurring revenue in large commercial building portfolios worldwide.

APi Group Inc.

APi Group Inc. is one of the largest fire protection and life-safety services platform in North America. The company operates a decentralized model of regional contractor brands delivering installation, inspection, and maintenance across commercial, industrial, and institutional client bases in the United States and Canada.

- Product Portfolio: Sprinkler installation, inspection, testing, and maintenance services across all product types.

- Recent Developments: In April 2026, APi Group Corporation entered into an agreement to acquire Onyx-Fire Protection Services, a Canada-based provider of fire and life safety solutions, from funds managed by Blackstone. The acquisition is aimed at strengthening APi’s presence in the North American safety services market and expanding its capabilities in inspection, service, and monitoring offerings.

- Strategic Focus: APi Group focuses on scaling its services-led platform through acquisition, integrating digital inspection tools, and capturing share of the long-cycle recurring inspection-and-maintenance revenue pool as sprinkler-equipped building stock continues expanding across North America.

Market Concentration Analysis

The global fire sprinklers market is moderately consolidated, with the top five players collectively accounting for an estimated 35-45% of global revenue. North America and Europe exhibit higher consolidation, while Asia Pacific and Latin America remain fragmented, served primarily by domestic manufacturers addressing local code and pricing requirements.

Investment & Growth Opportunities

Fastest-Growing Segments

Wet pipe fire sprinklers at ~5.8% CAGR through 2034 remain the highest-absolute-growth product segment, driven by commercial construction and residential retrofit mandates. Pre-action systems are growing fastest on a relative basis, fuelled by data center construction demanding double-interlock suppression in mission-critical environments globally.

Emerging Markets

Asia Pacific at ~6.1% CAGR is the fastest-growing region through 2034. Middle East and Africa at ~5.5% CAGR is accelerating via GCC Vision 2030 mega-projects and strengthening regional fire codes, generating large-scale procurement from under-penetrated commercial and industrial building stock across the region.

Venture & Investment Trends

Private equity interest in fire protection services platforms remains strong. Smart sprinkler IoT startups, predictive maintenance analytics, and digital inspection platforms are attracting capital, reflecting the shift toward software-enabled recurring revenue that commands higher valuation multiples than traditional hardware product businesses.

Future Market Outlook (2026-2034)

The global fire sprinklers market is forecast to expand from USD 14.48 Billion in 2025 to USD 22.85 Billion by 2034 at a CAGR of 5.04%. Three forces will shape the landscape: IoT and AI-enabled smart sprinkler ecosystems, data center construction driving elevated specification density, and strengthening emerging-market codes expanding the addressable installed base.

Research Methodology

Primary Research

Primary research encompassed over 40 structured interviews with fire sprinklers stakeholders including senior commercial managers, fire protection engineers, NFPA-certified designers, and insurance loss-control specialists, validating market sizing, segment shares, and digital adoption timelines.

Secondary Research

Key secondary sources include NFPA codes, FM Global reports, EN 12845 documentation, company annual reports, National Fire Sprinkler Association and European Fire Sprinkler Network publications, and trade journals covering fire protection engineering globally.

Forecasting Models

Market size estimations were derived using combined top-down and bottom-up models incorporating construction spending, GDP growth, urbanization trends, and historical penetration data. Scenario analysis (base, optimistic, conservative) was conducted to account for macroeconomic and regulatory uncertainty.

Fire Sprinklers Market Report Scope

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Wet Pipe Fire Sprinklers, Dry Pipe Fire Sprinklers, Deluge Systems, Pre-Action Systems, Others |

| Services Covered | Engineering Services, Installation, Design Maintenance, Inspection, Managed Services, Others |

| Components Covered | Stop Valve, Alarm Valve, Fire Sprinkler Head, Alarm Test Valve, Motorized Alarm Bell |

| Applications Covered | Commercial Applications, Residential Applications, Industrial Applications |

| Technologies Covered | Active Fire Protection, Passive Fire Protection |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Companies Covered | Honeywell International Inc., Johnson Controls, APi Group, Bosch Sicherheitssysteme GmbH, Hochiki Corporation, Siemens, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the fire sprinklers market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global fire sprinklers market.

- The study maps the leading, as well as the fastest-growing, regional markets.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the fire sprinklers industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Fire Sprinklers Market Report

The global fire sprinklers market reached USD 14.48 Billion in 2025, reflecting consistent demand driven by stringent building fire-safety codes, accelerating commercial construction, and growing specification of IoT-enabled active suppression systems across commercial, residential, and industrial buildings globally.

The market is projected to reach USD 22.85 Billion by 2034, growing at a CAGR of 5.04% during 2026-2034, driven by Asia Pacific urbanization, North America retrofit mandates, smart building adoption, and data center and warehouse construction generating sustained sprinkler specification globally.

Active fire protection leads with a 73.6% technology share in 2025, valued for its code-mandated role as the primary life-safety suppression barrier, serving the vast majority of commercial, high-rise residential, healthcare, hospitality, and industrial building classifications globally.

Wet pipe fire sprinklers lead at 52.3% in 2025, representing the most cost-effective and reliable suppression configuration for heated buildings. Continuously pressurized water piping, simple maintenance requirements, and broad NFPA 13 specifications make wet pipe the default product type across most commercial and residential occupancies.

North America commands a dominant 31.2% market share in 2025, driven by the world’s most codified fire-safety regime including NFPA 13 and NFPA 25 enforcement, state-level high-rise retrofit mandates, insurance-driven sprinkler requirements, and a large installed base generating inspection and servicing revenue cycles.

Wet pipe fire sprinklers are the highest-absolute-growth product segment at ~5.8% CAGR through 2034, driven by sustained commercial construction and residential retrofit mandates. Pre-action systems are the fastest growing on a relative basis, fueled by data center and mission-critical facility expansion requiring double-interlock suppression protection.

Leading companies include Honeywell International Inc., Johnson Controls, APi Group, Bosch Sicherheitssysteme GmbH, Hochiki Corporation, Siemens, and others.

Key applications include commercial office and retail buildings, high-rise residential towers, hospitals and care facilities, hospitality venues, data centers and server rooms, warehouses and fulfilment centers, manufacturing and industrial plants, and transportation infrastructure, each demanding tailored suppression configurations based on hazard classification and occupancy.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)