Flow Meter Market Size, Share, Trends and Forecast by Product Type, Application, and Region, 2026-2034

Flow Meter Market Size and Share:

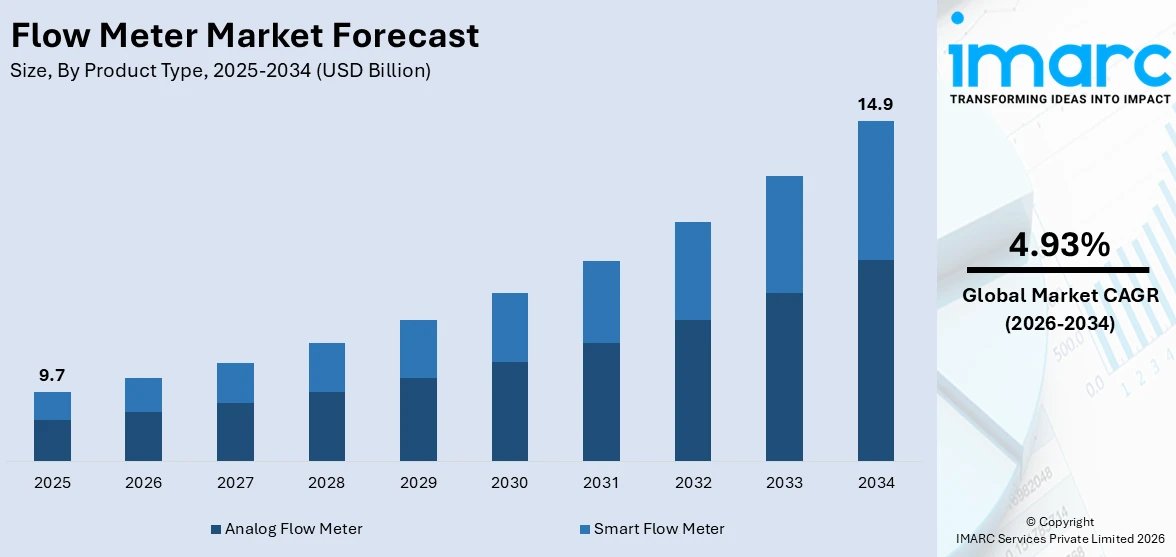

The global flow meter market size was valued at USD 9.7 Billion in 2025. Looking forward, IMARC Group estimates the market to reach USD 14.9 Billion by 2034, exhibiting a CAGR of 4.93% during 2026-2034. Asia Pacific currently dominates the market, holding a significant market share of over 46.8% in 2025. The growing need for wastewater management systems, the rising implementation of stringent safety norms in the oil and gas industry, increasing infrastructure building activities, and automation in the manufacturing sector represent some of the factors that are propelling the market. These factors are significantly contributing to the expansion of the flow meter market share, as industries increasingly rely on accurate flow measurement for efficient operations and regulatory compliance.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025 |

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 9.7 Billion |

| Market Forecast in 2034 | USD 14.9 Billion |

| Market Growth Rate (2026-2034) |

4.93%

|

The global flow meter market is driven by increasing demand across industries such as oil and gas, water and wastewater, and chemicals. Rising investments in infrastructure development and industrial automation are fueling the adoption of advanced flow measurement technologies. Along with this, the growing emphasis on energy efficiency and regulatory compliance also encourages the use of precision flow meters for monitoring and optimizing resource usage. Technological advancements, such as the integration of IoT and smart sensors, further enhance the functionality and accuracy of flow meters, enhancing their adoption. Additionally, the expansion of emerging economies and growing focus on sustainable practices are creating new opportunities, as industries seek to reduce operational costs and environmental impact through improved flow measurement solutions. For instance, on 4th March 2024, Yokogawa Electric Corporation announced the signing of an agreement to acquire Adept Fluidyne Pvt. Ltd., one of India's largest domestic manufacturers of magnetic flowmeters. This acquisition will give Yokogawa an Indian manufacturing base for its lineup of high-performance magnetic flowmeters and will provide access to Adept's product lineup, thereby allowing for more timely delivery of a broad portfolio of flowmeter products for the growing Indian market.

To get more information on this market Request Sample

The United States stands out as a key regional market, majorly driven by the increasing adoption of smart metering technologies across sectors such as utilities, pharmaceuticals, and food and beverage. The growing focus on modernizing aging infrastructure, particularly in water and wastewater management, is significantly enhancing demand. Stringent environmental regulations promoting the use of efficient flow measurement systems are also playing a pivotal role. The rapid growth of the shale gas industry, coupled with advancements in liquid natural gas (LNG) operations, fuels the adoption of flow meters in the energy sector. Furthermore, government incentives for renewable energy projects and smart grid development are driving innovation and deployment of flow meters, supporting accurate measurement, energy conservation, and process optimization in critical industries.

Flow Meter Market Trends:

Growing Demand for Accurate Measurement in Water and Wastewater Management

The market is largely propelled by the growing need for precise flow measurement solutions in water and wastewater management systems. With the rise of urbanization and increasing municipal water consumption, both utilities and industries need accurate monitoring of water usage, detection of leaks, and management of treatment processes. For instance, India's urban population is projected to surge to 35-37% in Census 2024, reflecting a swiftly urbanizing nation, as per SBI Research. Flow meters enable precise billing, resource management, and compliance with regulations, making them vital for effective water distribution systems. In wastewater treatment facilities, they assist in monitoring influent and effluent flow rates, chemical dosing, and process enhancement. The increasing focus on water conservation, updating infrastructure, and smart metering projects is driving the market growth. Government entities and regulatory organizations are progressively mandating the implementation of advanced metering technologies to enhance transparency and efficiency in water systems.

Expansion of Oil, Gas, and Petrochemical Industries

The flow meter market is propelled by the steady growth of the oil, gas, and petrochemical industries that depend on precise flow measurement for production, refining, and distribution processes. As per the IMARC Group, the global petrochemicals market size reached USD 645.7 Billion in 2024. Flow meters help monitor crude oil extraction, pipeline transportation, gas distribution, chemical blending, and refinery operations to ensure safety, efficiency, and regulatory compliance. With increasing exploration of new oil and gas reserves, enhanced pipeline infrastructure, and rising global demand for petroleum products, advanced flow measurement solutions are required to maintain process integrity. Digital and ultrasonic flow meters are gaining prominence due to their non-intrusive measurement capability and suitability for harsh environments.

Industrial Automation and Adoption of Smart Monitoring Systems

Industrial automation and integration of smart monitoring systems are key drivers of the market expansion. Modern manufacturing facilities are seeking automated process control, real-time data analytics, and digital tracking of fluid movement to enhance productivity and reduce operational inefficiencies. Smart flow meters equipped with sensors, wireless connectivity, and embedded diagnostics offer predictive maintenance, remote monitoring, and seamless integration with the Internet of Things (IoT) platforms. These advanced solutions support efficiency improvements in process industries, such as chemical, pharmaceutical, and power generation. As Industry 4.0 and smart factory initiatives are expanding, companies are adopting digital flow measurement tools for optimizing production lines, reducing wastage, and maintaining consistent product quality. In October 2025, OMRON opened an automation center in Bengaluru to enhance smart manufacturing in India. Backed by the government's Make in India and Industry 4.0 efforts, the Center showcased effective automation solutions for manufacturing issues and fostered collaboration with machine builders and system integrators to refine India's manufacturing strengths.

Flow Meter Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global flow meter market, along with forecast at the global, regional, and country levels from 2026-2034. The market has been categorized based on product type, application, and region.

Analysis by Product Type:

- Analog Flow Meter

- Smart Flow Meter

Analog flow meter leads the market driven by its cost-effectiveness, ease of use, and low maintenance requirements. Its robust design makes it suitable for environments with harsh conditions, adding to its demand in industrial sectors including oil and gas. Despite the rise in digital technology, analog meters remain popular due to their compatibility with legacy systems. Durability and reliability also contribute to its sustained market presence. In addition, certain kinds do not require power might be important in severe or remote settings.

Analysis by Application:

Access the comprehensive market breakdown Request Sample

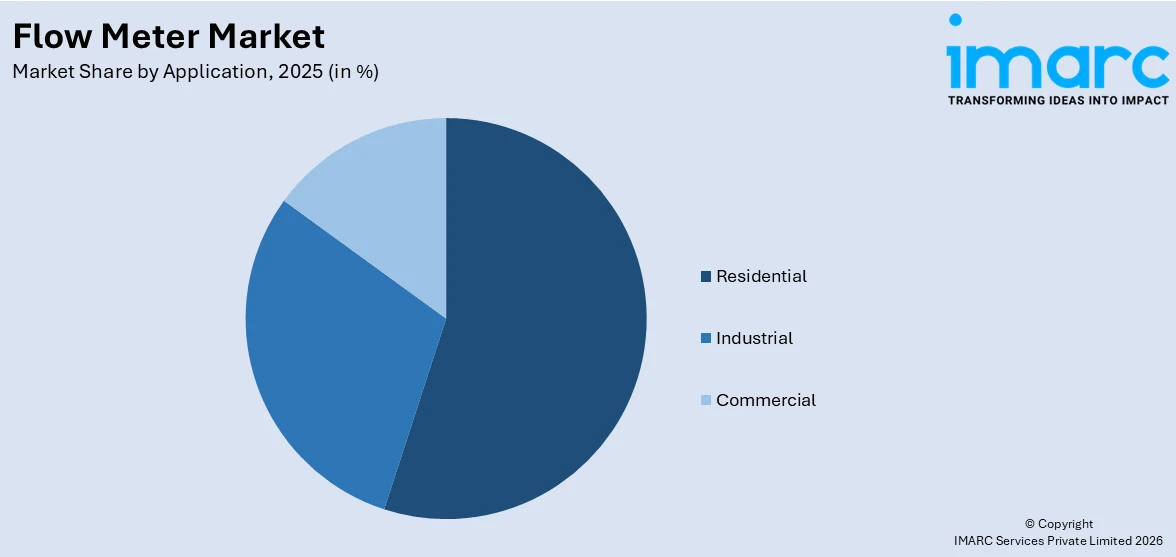

- Residential

- Industrial

- Commercial

Residential leads the market as in the residential sector, flow meters are predominantly driven by water conservation efforts and utility cost management. Based on the data provided by the US Department of Housing, in February 2024, privately-owned housing starts surged to a seasonally adjusted annual rate of 1,521,000, marking a 10.7% increase from the revised January estimate of 1,374,000. Single-family housing starts also saw significant growth, rising by 11.6% from the revised January figure to reach a rate of 1,129,000. Meanwhile, the rate for units in buildings with five units or more stood at 377,000. Demand for high-quality potable water requires accurate metering systems for equitable distribution. Smart metering solutions are increasingly being adopted for real-time leak detection and waste management. Environmental consciousness and sustainability goals among residents also contribute to market growth. Advancements in smart home technologies are integrating flow metering solutions to offer optimized resource management.

Regional Analysis:

To get more information on the regional analysis of this market Request Sample

- North America

- Europe

- Asia Pacific

- Middle East and Africa

- Latin America

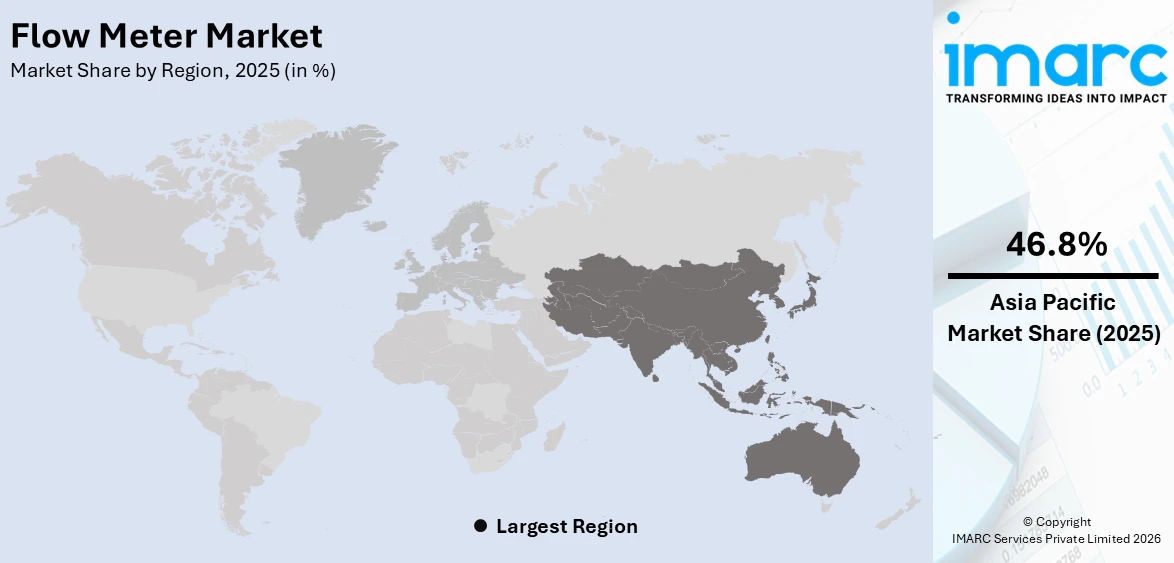

In 2025, Asia Pacific accounted for the largest flow meter market share of over 46.8%. The Asia Pacific region is a burgeoning market for flow meters, driven by rapid industrialization, increasing population, and urbanization. A joint report released by four United Nations agencies states that the rapid urbanization in Asia is projected to concentrate approximately 55% of the region's vast population in urban centers by 2030. Countries such as China and India have become global manufacturing hubs, thereby elevating the demand for industrial flow metering solutions. Investments in infrastructure projects, particularly in water treatment and distribution, are fueling the market. The flow meter market outlook report anticipates growth opportunities, driven by the increasing infrastructure development initiatives in the region.

The region is also witnessing considerable growth in technological adoption, which is contributing to the growth in demand for smart flow meters. Environmental regulations are becoming stringent, compelling businesses and utilities to adopt more accurate and reliable flow metering systems. Policies promoting smart cities in various countries across the region are pushing the integration of smart flow metering solutions in both residential and commercial applications. Furthermore, the growing awareness among end-users regarding the benefits of advanced metering solutions is offering a favorable flow meter market outlook.

Key Regional Takeaways:

North America Flow Meter Market Analysis

The North America flow meter market is driven by increasing investments in smart infrastructure, industrial automation, and the modernization of legacy fluid measurement systems across industries, such as oil and gas, chemical, power generation, and water and wastewater utilities. The growing focus on operational efficiency, leak detection, and accurate flow measurement to reduce product losses and improve process control is boosting the adoption of advanced flow technologies such as ultrasonic, Coriolis, and magnetic flow meters. Stringent regulatory frameworks related to emissions, water conservation, and energy efficiency are encouraging industries to upgrade to precision-based and digital flow metering solutions with remote monitoring and IoT integration. The broadening of shale gas production, pipeline network upgrades, and refinery expansions are also stimulating the market growth, as flow meters are essential for custody transfer, process measurement, and safety monitoring. In March 2025, Enbridge, a Canadian midstream firm, intended to invest USD 2.5 Billion in its natural gas and liquids systems, with USD 2 Billion designated for its Mainline network by 2028. Increased spending on smart water metering to address aging water infrastructure, non-revenue water challenges, and sustainability goals is further driving the demand. The region is also witnessing rising adoption of wireless and battery-operated flow meters, cloud-based analytics, and predictive maintenance features to reduce downtime and optimize asset performance.

United States Flow Meter Market Analysis

The United States holds 80.20% of the market share in North America. The market is driven by strong industrial growth, continuous technological innovations, and high regulatory emphasis on process accuracy, safety, and resource efficiency across major sectors, such as oil and gas, chemical, power, pharmaceutical, water management, and manufacturing. The country’s extensive pipeline network, shale gas activities, and refinery infrastructure are creating consistent demand for flow meters used in custody transfer, flow monitoring, and compliance reporting. Increasing focus on digital transformation and smart manufacturing is encouraging industries to shift towards advanced flow metering technologies capable of real-time data analytics, IoT connectivity, and automated calibration. As per the IMARC Group, the United States smart manufacturing market size is projected to exhibit a growth rate (CAGR) of 11.43% during 2025-2033. Government initiatives related to water conservation, wastewater treatment modernization, and reduction of non-revenue water are also boosting the adoption of smart water flow meters and intelligent metering systems in utilities. In sectors, such as pharmaceutical and biotechnology, the need for high-precision, hygienic, and contamination-free flow measurement is promoting the uptake of Coriolis and ultrasonic flow meters. The rise of renewable energy projects, district heating and cooling systems, and environmental monitoring requirements is adding further momentum.

Europe Flow Meter Market Analysis

The Europe flow meter market is driven by stringent regulatory norms related to environmental protection, energy efficiency, emissions reduction, and water resource management, which are encouraging industries to adopt highly accurate and compliant flow measurement solutions. The growth in renewable energy, hydrogen economy development, and industrial automation is creating the demand for smart and technologically advanced flow meters integrated with IoT and remote diagnostics. As per industry reports, in the UK, renewable energy sources, such as wind, solar, and hydro, accounted for around 35.6% of the overall electricity produced in 2024. Upgrades to aging water supply networks and the need to reduce leakage and non-revenue water are fueling the adoption of ultrasonic and electromagnetic flow meters in municipal utilities. Strong manufacturing, automotive, pharmaceutical, chemical, and food processing industries are further contributing to the demand for precise flow monitoring to ensure product quality, safety, and process control. Additionally, Europe’s focus on circular economy practices, decarbonization, and Industry 4.0 initiatives is accelerating the transition from conventional mechanical meters to digital, energy-efficient, and low-maintenance flow metering systems.

Asia-Pacific Flow Meter Market Analysis

The Asia-Pacific flow meter market is primarily driven by rapid industrialization, infrastructure development, and rising investments in water and wastewater treatment facilities across emerging economies. In September 2025, the Chief Minister of Delhi, Rekha Gupta declared that Union Home Minister Amit Shah would launch Asia’s largest Sewage Treatment Plant (STP) in Okhla. The projects worth INR 4500 Crore for Yamuna revival, encompassing 46 schemes for STPs, sewer systems, and water reservoirs, were to be unveiled. The growing demand from the oil and gas, chemicals, power generation, and manufacturing industries is supporting increased adoption of advanced flow measurement solutions for process optimization and resource conservation. Urbanization and government initiatives to upgrade water distribution networks are boosting the need for smart water metering.

Latin America Flow Meter Market Analysis

The Latin America flow meter market is driven by rising adoption of Industry 4.0 and increasing investments in oil and gas exploration, pipeline upgrades, and refining capacity expansion, particularly in Brazil and Mexico. As per the IMARC Group, the Mexico Industry 4.0 market size reached USD 2,470.50 Million in 2024. The growing focus on improving water supply management, reducing leakage, and modernizing municipal utilities is supporting the adoption of smart flow meters. Industrial growth in chemicals, food processing, and mining is also contributing to the demand for accurate and reliable flow measurement. Additionally, governments’ encouragement for energy efficiency, sustainability, and compliance with environmental standards is motivating industries to replace outdated meters with digital and automated solutions.

Middle East and Africa Flow Meter Market Analysis

The Middle East and Africa flow meter market is driven by strong demand from the oil and gas sector, where accurate flow measurement is essential for production monitoring, custody transfer, and safety compliance. Investments in water desalination, wastewater treatment, and smart water infrastructure are also promoting the adoption of advanced metering technologies. In August 2025, the Sharjah Electricity, Water, and Gas Authority (SEWA) undertook a range of strategic infrastructure initiatives worth AED 4 Billion (over USD 1 Billion) to improve water security and guarantee a sustainable supply throughout Sharjah and the Central Region. The core of the project was the Al Hamriyah Independent Water Desalination Plant, designed to generate as much as 90 Million gallons of drinkable water each day. Industrial diversification, the expansion of petrochemical and power generation projects, and digitalization of process industries are further supporting the market growth. Additionally, the heightened focus on efficient resource management and sustainability is encouraging the shift from conventional to smart and automated flow meter systems.

Competitive Landscape:

Key players in the market are actively focusing on research and development to create advanced and more accurate measurement systems. By investing in technological innovations, these dominant firms are working towards expanding their product portfolios. They are also establishing strategic partnerships to enter new markets and reach a broader customer base. As part of their growth strategy, they are consistently involved in mergers and acquisitions, which allow them to integrate advanced technologies and expand their operational capabilities. Moreover, these companies are prioritizing customer education to drive the adoption of flow meters in industries such as oil and gas, chemicals, and water treatment. They are also participating in global trade shows and industrial expos to showcase their latest offerings. To maintain a competitive edge, market leaders are continually analysing market trends and customer preferences.

The report has provided a comprehensive analysis of the competitive landscape in the market. Detailed profiles of all major companies have also been provided. Some of the key players in the market include:

- ABB Ltd.

- Azbil Corporation

- Bronkhorst

- Christian Bürkert GmbH & Co. KG

- Dwyer Instruments, LLC

- Emerson Electric Co.

- Endress+Hauser Group

- Hitachi High-Tech Corporation

- Honeywell International Inc.

- Keyence Corporation

- Krohne Messtechnik GMBH

- Sick AG

- Siemens AG

- Yokogawa Electric Corporation

Recent Developments:

- October 2025: Malema™, a division of PSG and Dover and a prominent supplier of flow meter solutions for industrial and semiconductor uses, revealed the worldwide launch of the new Malema M-3100 Series Clamp-On Ultrasonic Flow Meter. Designed for accurate fluid velocity assessment in liquid-filled closed pipes, the M-3100 Series was an efficient, non-invasive ultrasonic transit-time flow measurement system, ideal for the most demanding semiconductor applications.

- July 2025: Yokogawa India Limited (YIL), a company specializing in industrial automation and process control, achieved a notable milestone with the initial delivery of its cutting-edge AXG magnetic flowmeters in Maharashtra. The occasion represented the firm’s growing dedication to India’s industrial advancement and the ‘Make in India’ initiative.

- January 2025: Allengra introduced a new hydrogen flow meter aimed at measuring hydrogen and its mixtures. The ultrasonic sensor delivered mass flow, volume information, and gas composition, along with extra sensors for temperature, humidity, and pressure. This flow meter will be employed in Formula 1 vehicles beginning in the 2026 season, aiding the transition to sustainable fuel.

Flow Meter Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Analog Flow Meter, Smart Flow Meter |

| Applications Covered | Residential, Industrial, Commercial |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Companies Covered | ABB Ltd., Azbil Corporation, Bronkhorst, Christian Bürkert GmbH & Co. KG, Dwyer Instruments, LLC, Emerson Electric Co., Endress+Hauser Group, Hitachi High-Tech Corporation, Honeywell International Inc., Keyence Corporation, Krohne Messtechnik GMBH, Sick AG, Siemens AG, Yokogawa Electric Corporation, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the flow meter market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global flow meter market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyse the level of competition within the flow meter industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Flow Meter Market Report

A flow meter is a device used to measure the flow rate or quantity of fluid including liquid or gas, moving through a pipeline. It ensures precise monitoring and control of fluid dynamics in various industrial, residential, and commercial applications.

The global flow meter market was valued at USD 9.7 Billion in 2025.

IMARC estimates the global flow meter market to exhibit a CAGR of 4.93% during 2026-2034.

The market is driven by increasing demand across sectors such as oil and gas, water and wastewater, and chemicals, along with technological advancements such as IoT integration, industrial automation, regulatory compliance, and growing infrastructure development initiatives.

In 2024, analog flow meters represented the largest segment by product type, driven by their cost-effectiveness, durability, and compatibility with legacy systems.

The residential sector leads the market by application due to growing water conservation efforts, utility cost management, and integration of smart metering technologies.

On a regional level, the market has been classified into North America, Asia Pacific, Europe, Latin America, and the Middle East and Africa, with Asia Pacific currently dominating the market.

Some of the major players in the global flow meter market include ABB Ltd., Azbil Corporation, Bronkhorst, Christian Bürkert GmbH & Co. KG, Dwyer Instruments, LLC, Emerson Electric Co., Endress+Hauser Group, Hitachi High-Tech Corporation, Honeywell International Inc., Keyence Corporation, Krohne Messtechnik GMBH, Sick AG, Siemens AG, and Yokogawa Electric Corporation, among others.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)