Food Emulsifiers Market Size, Share, Trends and Forecast by Type, Application, Source, and Region, 2026-2034

Global Food Emulsifiers Market Size, Share, Trends & Forecast (2026-2034)

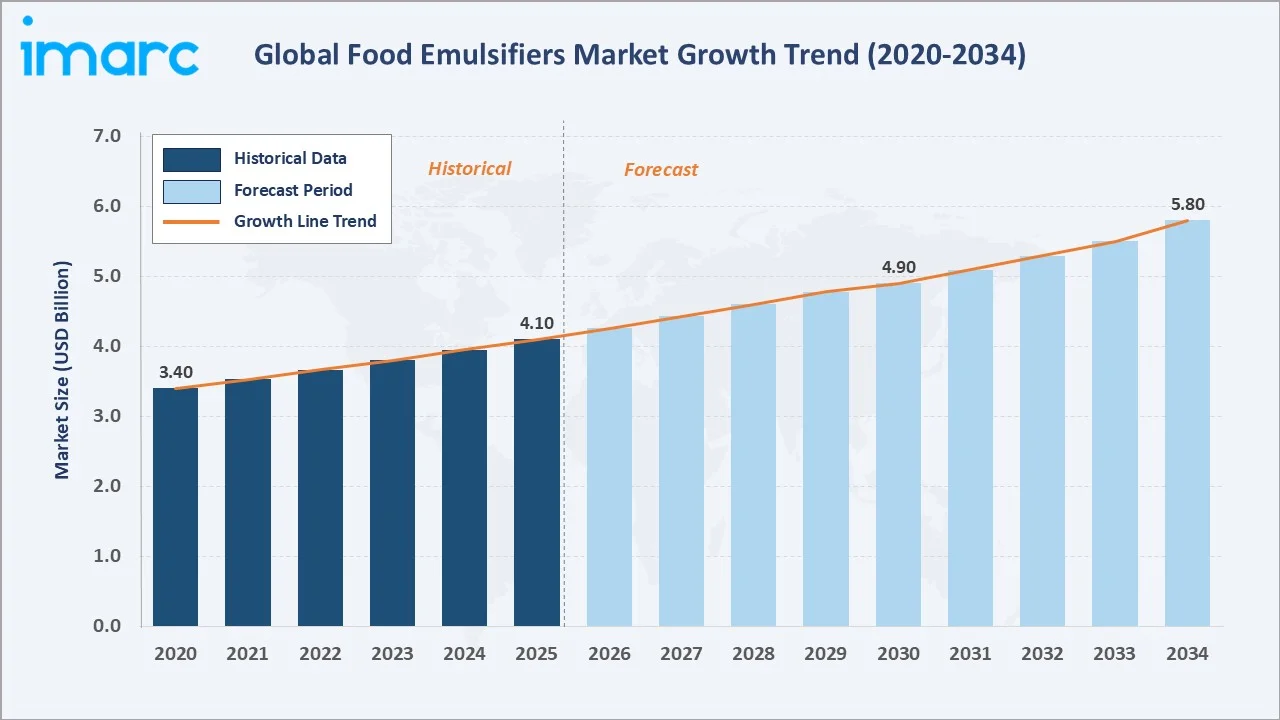

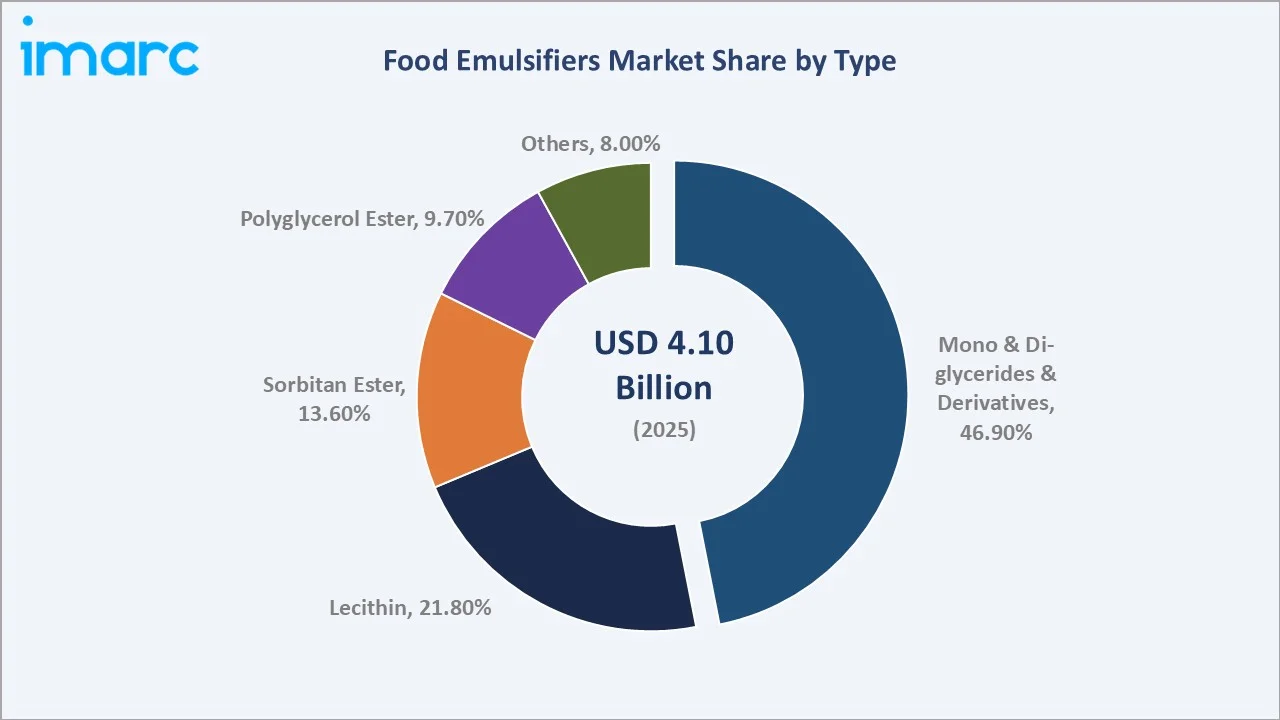

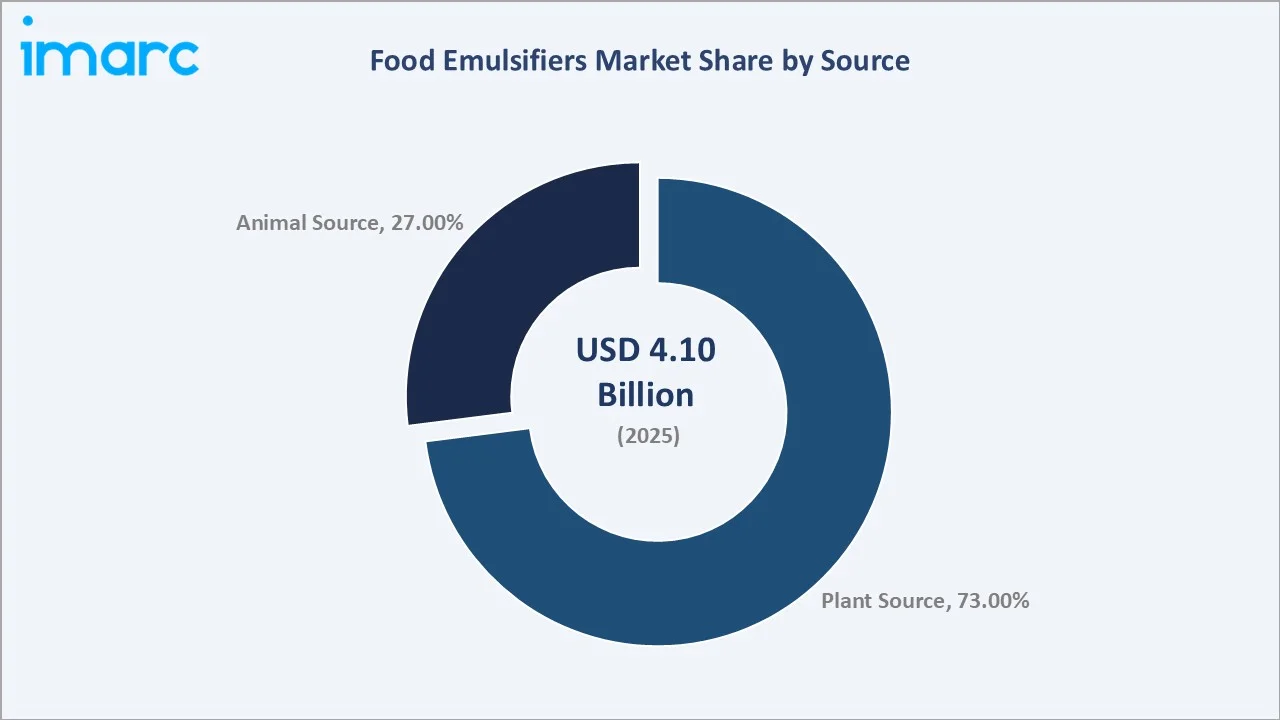

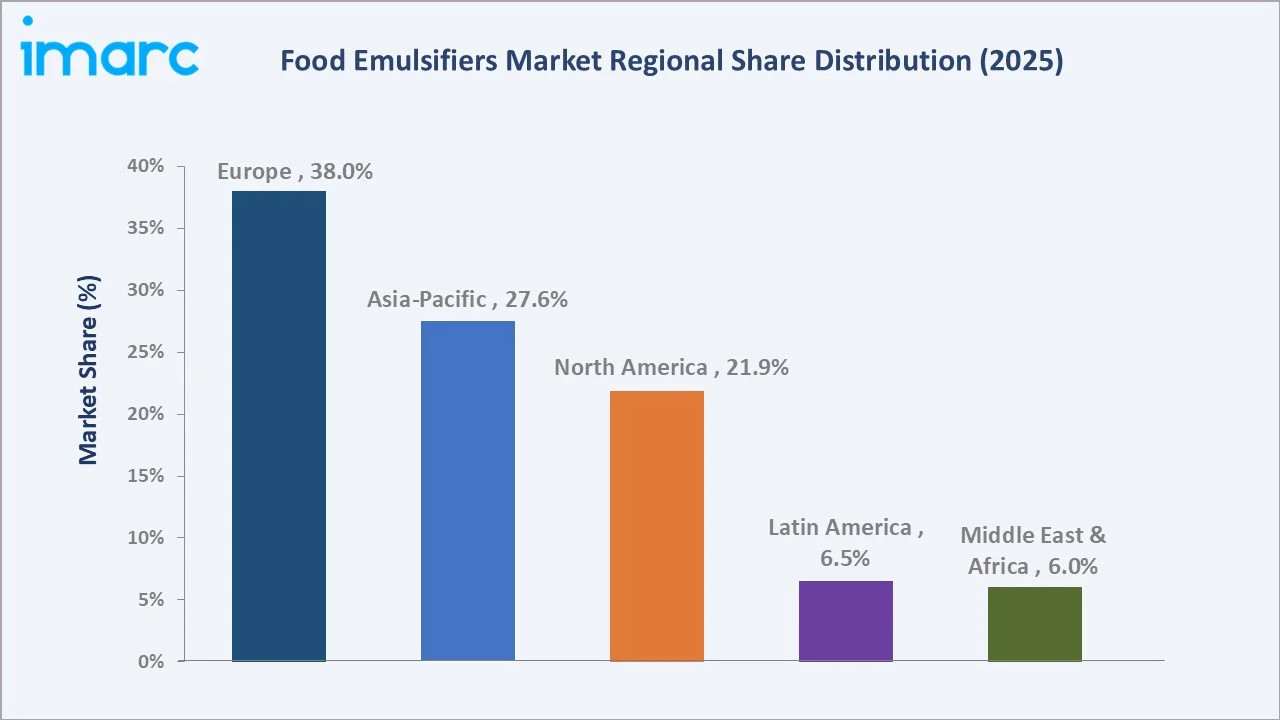

The global food emulsifiers market size reached USD 4.1 Billion in 2025 and is projected to reach USD 5.8 Billion by 2034, at a CAGR of 3.84% during 2026-2034. Escalating demand for processed and convenience foods, surging clean label and plant-based ingredient preferences, and regulatory frameworks mandating safer emulsifier formulations are the primary growth catalysts. According to a Cambridge University article, emulsifiers are found in 51.7% of foods within ultra-processed food (UPF) categories, with lecithin, diphosphates, and mono- and diglycerides of fatty acids being the most commonly used. Mono and di-glycerides lead the type segment at 46.9%, plant-sourced emulsifiers dominate at 73.0%, and Europe holds the largest regional share at 38.0% in 2025, underpinned by its mature food processing industry and stringent quality standards.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 4.1 Billion |

|

Forecast Market Size (2034) |

USD 5.8 Billion |

|

CAGR (2026-2034) |

3.84% |

|

Base ear |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Europe (38.0%, 2025) |

|

Fastest Growing Region |

Asia-Pacific (~4.6% CAGR, 2026-2034) |

|

Leading Type |

Mono & Di-glycerides & Derivatives (46.9%, 2025) |

|

Leading Source |

Plant Source (73.0%, 2025) |

The food emulsifiers market from 2020 through 2034, grew from USD 3.4 Billion in 2020 to USD 4.1 Billion in 2025, anchored at USD 4.9 Billion in 2030 before reaching USD 5.8 Billion by 2034, driven by processed food expansion and clean-label reformulation trends.

To get more information on this market, Request Sample

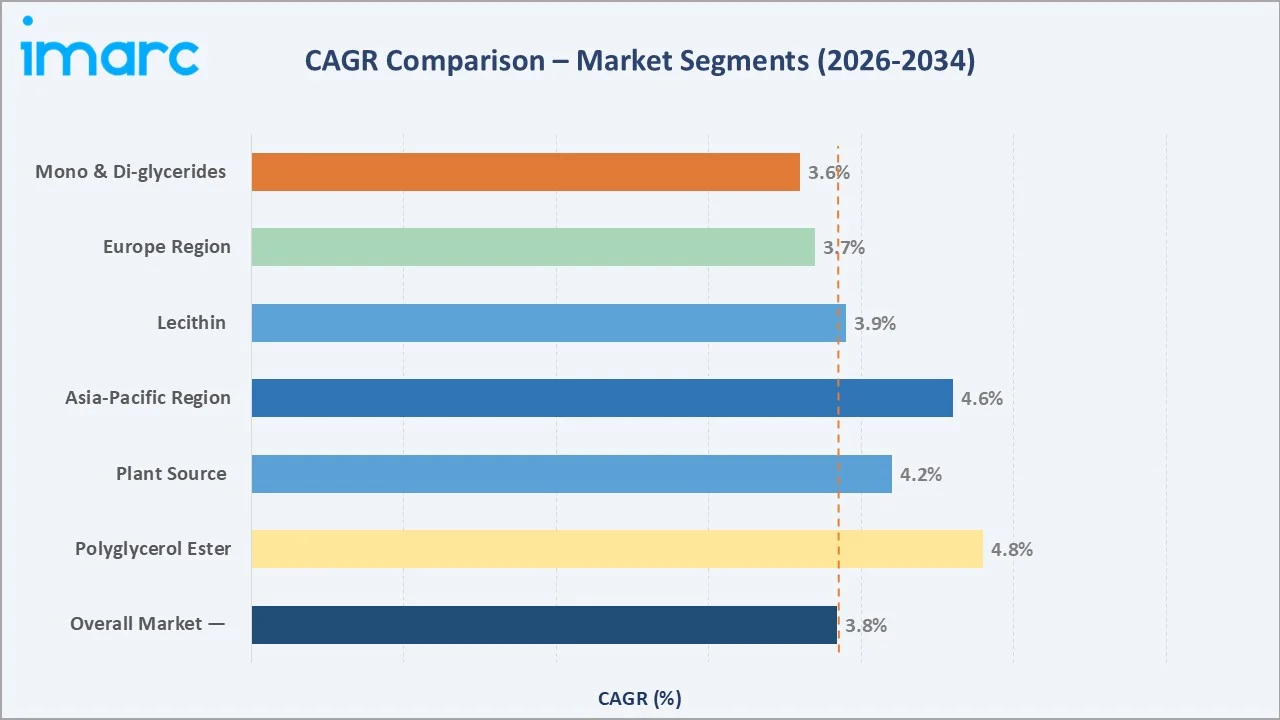

The CAGR across key segments, polyglycerol esters lead at ~4.8% CAGR and Asia-Pacific at ~4.6%, both outpacing the overall 3.84% rate. These reflect growing demand for clean-label polyglycerol-based emulsifiers and rapid food processing expansion across China, India, and Southeast Asia through 2034.

Executive Summary

The global food emulsifiers market is expanding at a 3.84% CAGR from USD 4.1 Billion in 2025 to USD 5.8 Billion by 2034. Food emulsifiers are specialty additives that stabilize mixtures of oil and water in food products, enhancing texture, shelf life, and consistency across applications including bakery, confectionery, dairy, meat products, and convenience foods. They function as surfactants, reducing interfacial tension between immiscible phases to create stable emulsions that are critical to product quality and consumer appeal.

Mono and di-glycerides and their derivatives command the largest type share at 46.9% in 2025, valued for their cost-effectiveness, multifunctionality across fat-in-water and water-in-fat emulsion systems, and compatibility with a wide range of food matrices. Plant-sourced emulsifiers dominate at 73.0% in 2025, driven by the global clean label trend and the exponential growth of plant-based food products.

Europe leads regionally at 38.0% in 2025, anchored by its mature food processing industry, EU Regulations harmonizing food additive standards across 27 member states, and strong consumer preference for natural and certified-organic emulsifiers. Asia-Pacific at 27.6% is growing fastest, driven by China’s and India’s expanding processed food sectors.

Key Market Insights

|

Insight |

Data / Finding |

|

Largest Type |

Mono & Di-glycerides – 46.9% 2025 |

|

Leading Source |

Plant Source – 73.0% 2025 |

|

Leading Region |

Europe – 38.0% 2025 |

|

Fastest Region |

Asia-Pacific – ~4.6% CAGR |

Key Analytical Observations Supporting the Above Data:

- Mono and di-glycerides at 46.9% in 2025 are the workhorse emulsifier type of the global food industry. They improve dough handling, volume, and freshness retention in baked goods by maintaining moisture and regulating fat crystallization.

- Plant-sourced emulsifiers at 73.0% in 2025 reflect the structural alignment of the food ingredients industry with consumer clean label demand and sustainability commitments. In September 2025, Louis Dreyfus acquired BASF’s Food and Health Performance Ingredients Business, which produced plant-based emulsifiers, underscoring the strategic value attributed to plant-based emulsifier assets.

- Europe’s 38.0% regional dominance reflects the continent’s food processing industry depth and regulatory sophistication. EU Regulation No. 1333/2008 creates a positive-list framework; only explicitly approved additives may be used, which drives premium, safety-certified emulsifier demand.

- Asia-Pacific at 27.6% 2025, growing at ~4.6% CAGR, benefits from the simultaneous expansion of modern food processing across China, India, Southeast Asia, and Japan. Palsgaard’s manufacturing facility in Malaysia, with 20,000 MT annual capacity specifically to serve Asian food manufacturers.

Global Food Emulsifiers Market Overview

Food emulsifiers are surface-active molecules with hydrophilic (water-loving) and lipophilic (fat-loving) molecular regions that enable the formation and stabilization of emulsions, mixtures of oil and water phases, in food products. Primary types include mono and di-glycerides (esters of glycerol with fatty acids), lecithin (natural phospholipid from soy, sunflower, or rapeseed), sorbitan esters, polyglycerol esters, and specialty emulsifiers including acetylated monoglycerides and diacetyl tartaric acid esters.

Applications span bakery products, confectionery, dairy and frozen desserts, meat products, beverages, and convenience foods. The ecosystem connects oilseed processors and fat refiners, emulsifier manufacturers, specialty chemical distributors, food ingredient formulators, and food and beverage manufacturers as end-users.

Market Dynamics

To evaluate market opportunities, Request Sample

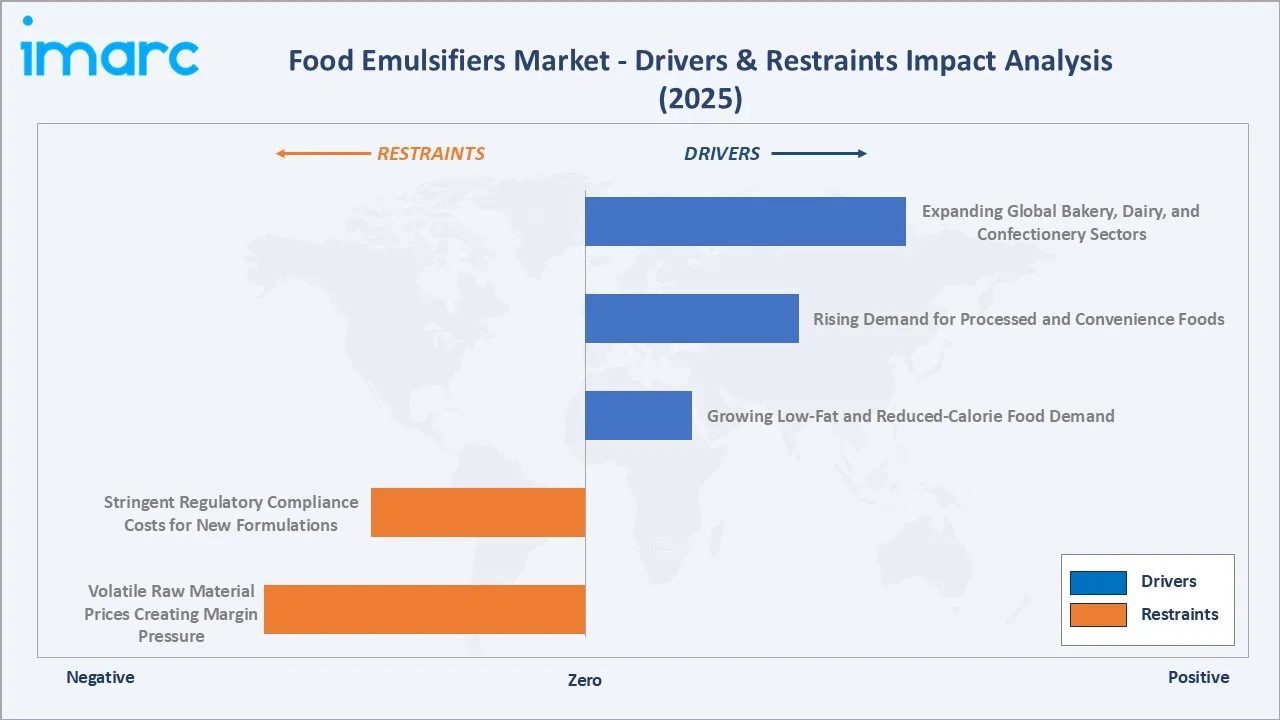

Market Drivers

- Rising Demand for Processed and Convenience Foods: India’s Gen Z, expected to constitute 30% of the Indian workforce by 2030, represents a growing processed food consumer demographic driving demand for snack foods, baked goods, and convenience meals that use mono and di-glycerides and lecithin as quality-stabilizing additives.

- Expanding Global Bakery, Dairy, and Confectionery Sectors: Lecithin in chocolate prevents fat bloom; DATEM in bread improves dough conditioning and loaf volume; polyglycerol polyricinoleate (PGPR) in chocolate reduces viscosity at lower fat content. These technically critical emulsifier functions, where performance cannot be compromised without product quality failure, create inelastic demand that sustains emulsifier procurement through commodity price cycles.

- Growing Low-Fat and Reduced-Calorie Food Demand: Health-conscious consumers driving demand for reduced-fat variants of traditionally high-fat products, low-fat ice cream, reduced-fat margarine, and light mayonnaise are creating premium emulsifier opportunities.

Market Restraints

- Volatile Raw Material Prices Creating Margin Pressure: The Soya Lecithin Price Index rose by 0.89% quarter-over-quarter in the Netherlands . These input cost fluctuations create margin compression for emulsifier manufacturers while complicating long-term pricing commitments to food manufacturer customers.

- Stringent Regulatory Compliance Costs for New Formulations: EU Regulation 1333/2008 requires comprehensive safety evaluation and EFSA opinion before any new emulsifier can receive EU market authorization, a process requiring years and high investment.

Market Opportunities

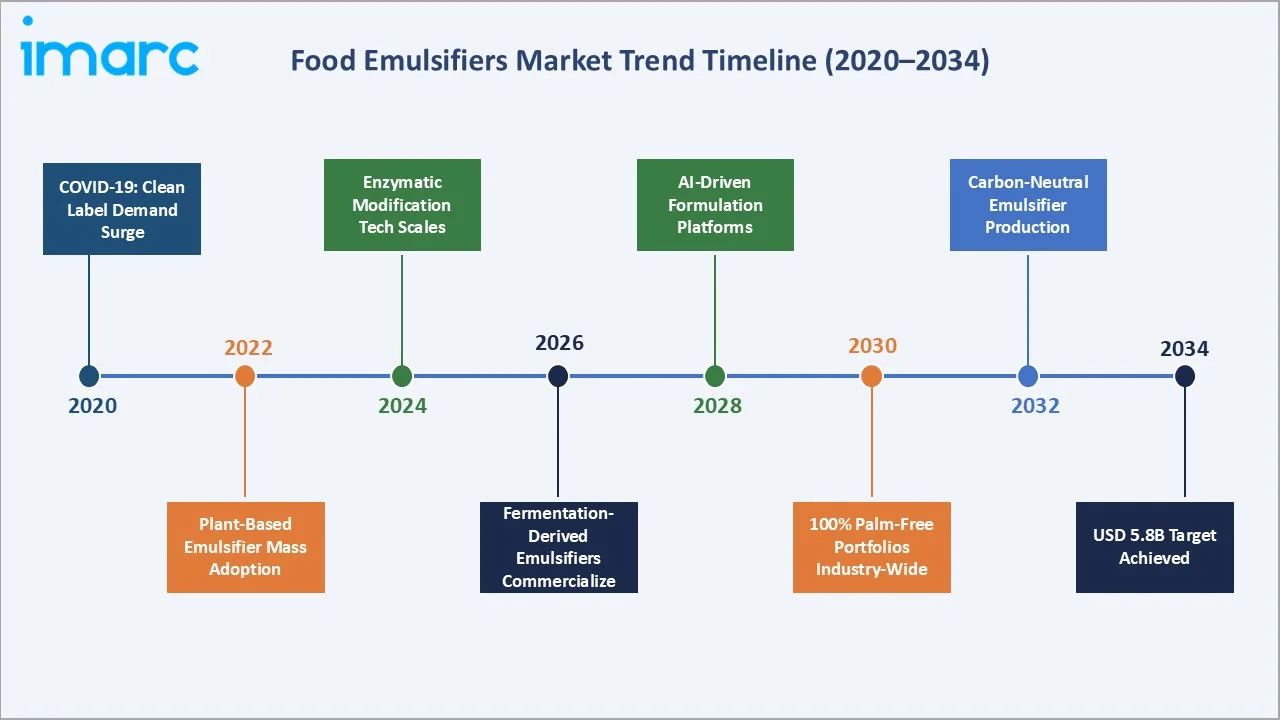

- Fermentation-Derived and Novel Emulsifiers Opening Premium Segments: Yeast-derived phospholipids, microbial glycolipids, and enzyme-modified natural emulsifiers represent an addressable premium niche within the broader food emulsifiers market. Cosaic’s fermentation-derived emulsifier, replacing dairy or synthetic plant-based alternatives with a single multi-functional ingredien, represents the commercial validation of this trend.

- Asia-Pacific’s Rapidly Expanding Processed Food Industry: India’s food processing industry growth, China’s processed food market, and ASEAN’s combined food manufacturing expansion create the world’s largest single growth opportunity for food emulsifier manufacturers.

Market Challenges

- Palm-Derived Emulsifier Sustainability Transition: Palm oil, which serves as their primary feedstock, is the most widely produced vegetable oil globally, representing about 42% of the top four vegetable oils worldwide in 2024, face intensifying NGO pressure, EU deforestation regulation, and consumer boycotts.

- Infant Formula Emulsifier Regulatory Complexity: Infant formula represents the highest-regulatory-scrutiny application for food emulsifiers, with EFSA, FDA, and China’s SAMR each maintaining distinct positive lists of approved emulsifiers at specified maximum use levels.

Emerging Market Trends

1. Plant-Based and Non-GMO Emulsifiers Displacing Synthetic Alternatives

The clean label megatrend is driving systematic reformulation away from DATEM, SSL, CSL, and polysorbates toward sunflower lecithin, enzyme-modified lecithin, and plant-based mono-glycerides.

2. Palm-Free Emulsifier Portfolios Becoming a Competitive Differentiator

EU Regulation 2023/1115 on Deforestation-Free Products requires operators to demonstrate that palm-derived products, including emulsifiers, are not associated with deforestation. In 2017, Palsgaard A/S developed Palsgaard SA 6615, the world’s first palm-free, powdered emulsifier for industrial cakes, establishing a competitive benchmark.

3. AI-Driven Formulation Platforms Accelerating Emulsifier Development

Artificial intelligence-powered food formulation platforms are reducing emulsifier formulation development cycles by predicting emulsifier performance,in complex multi-ingredient matrices.

4. Functional and Nutritional Emulsifiers Bridging Ingredient and Health Categories

Emulsifiers with additional health functionality, phospholipids supporting cognitive health, structured lipid emulsifiers improving fat-soluble vitamin bioavailability, and fiber-based emulsifying systems delivering prebiotic benefits are creating a premium ‘functional emulsifier’ segment.

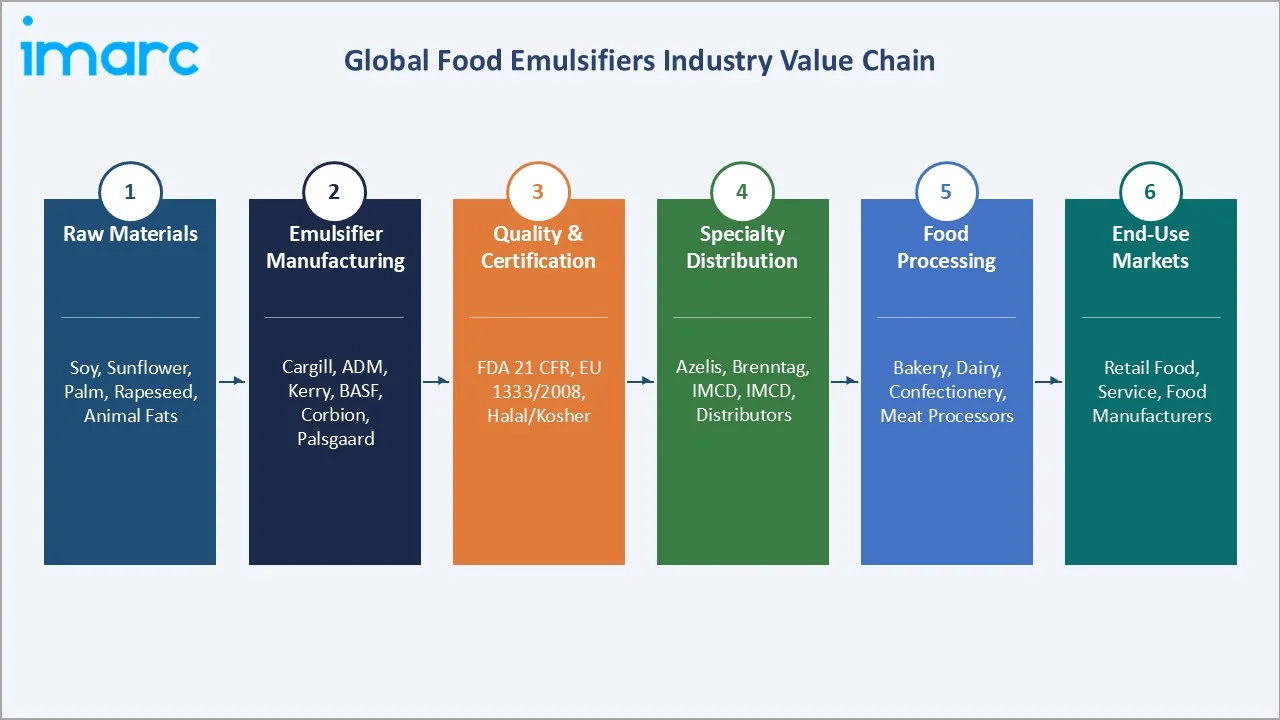

Industry Value Chain Analysis

The food emulsifiers value chain generates highest margin at the specialty manufacturing and formulation customization stages, where manufacturers like Palsgaard achieve EBITDA margins of 18–25% on specialized emulsifier blends at the commodity mono-glyceride production level.

|

Stage |

Key Players & Examples |

|

Raw Materials |

Soy/sunflower/rapeseed processors, palm oil refiners, animal fat renderers, oilseed crushers for lecithin feedstock |

|

Emulsifier Manufacturing |

Cargill, ADM, Louis Dreyfus, Kerry Group, Palsgaard A/S |

|

Quality & Certification |

EU EFSA opinion compliance, FDA GRAS notification, Halal certification (IFANCA, MUI), Kosher certification (OU), non-GMO Project Verification, organic certification (USDA NOP, EU 2018/848) |

|

Food Processing Applications |

Bakery (bread, cakes, pastries), confectionery (chocolate, candies), dairy (ice cream, margarine), meat products, convenience foods, plant-based food manufacturers |

|

End-Use Markets |

Retail packaged foods, foodservice chains, institutional catering, infant formula manufacturers, dietary supplement producers |

Specialty distribution represents 25–30% of total emulsifier supply chain value-add, as distributors provide technical formulation support, small-batch sampling, and local regulatory compliance expertise that emulsifier manufacturers cannot economically deliver direct to mid-sized food processors.

Technology Landscape in the Food Emulsifiers Industry

Enzymatic Modification Technology

Enzymatic interesterification and phospholipase-catalyzed hydrolysis are enabling the production of modified lecithins and structured lipid emulsifiers with precisely controlled HLB values and functional properties.

Precision Fermentation for Novel Emulsifier Production

Microbial biosynthesis using engineered yeast (Saccharomyces cerevisiae) and bacteria (Bacillus subtilis) strains is enabling production of sophorolipids, rhamnolipids, mannosylerythritol lipids (MELs), and phospholipid mixtures with tailored emulsification properties. Cosaic’s yeast fermentation platform produces a multi-functional ingredient replacing conventional emulsifiers.

Nano-Emulsification and Encapsulation Technologies

High-pressure homogenization, ultrasonication, and microfluidization technologies are enabling the production of nano-emulsions with significantly improved stability, bioavailability, and sensory properties versus conventional emulsions. Nano-emulsified curcumin, omega-3 fatty acids, and fat-soluble vitamins using lecithin and polyglycerol esters as emulsifiers, achieve 4–8x higher bioavailability versus standard emulsification, creating premium functional food applications.

Digital Formulation and AI-Assisted Development

Machine learning models trained on large food formulation databases are predicting optimal emulsifier type, concentration, and combination for specific food texture and stability objectives, reducing trial-and-error formulation cycles. Humanize AI can aid optimize the emulsification procedure, leading to more efficient and consistent results in food production .

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Mono and di-glycerides and their Derivatives |

46.9% |

2025 |

|

Application |

Dairy and Frozen Desserts |

🔒 |

2025 |

|

Source |

Plant Source |

73.0% |

2025 |

|

Region |

Europe |

38% |

2025 |

By Type

Mono and di-glycerides and their derivatives command 46.9% in 2025, driven by their broad compatibility across the full range of food emulsion applications. In bakery, the largest single application, DATEM (diacetyl tartaric acid esters of mono-glycerides) and SSL (sodium stearoyl lactylate) are essential dough conditioners that improve bread volume, crumb softness, and anti-staling performance. In confectionery, acetylated monoglycerides provide aeration and foam stabilization in cream-filled products. Their cost advantage over lecithin sustains their dominant position despite clean label pressure driving some reformulation.

To access detailed market analysis, Request Sample

Lecithin at 21.8% (2025) is the clean label champion of the emulsifier market, as food manufacturers reformulate for natural ingredient declarations. Polyglycerol esters at 9.7% growing fastest and serve the low-fat dairy and plant-based fat replacement segments. Sorbitan esters at 13.6% are critical emulsifiers in confectionery, as PGPR (polyglycerol polyricinoleate, E476) reduces chocolate viscosity compared to cocoa butter alone, enabling chocolate manufacturers to reduce cocoa butter usage and lower formulation costs.

By Source

Plant-sourced emulsifiers at 73.0% in 2025 reflect the food industry’s structural alignment with the clean label, vegan, and sustainability megatrends. Soy lecithin, sunflower lecithin, rapeseed-derived mono-glycerides, and plant-based polyglycerol esters from plant-based fatty acids collectively serve the 73.0% plant-source market share.

Animal-sourced emulsifiers at 27.0% (2025), primarily egg yolk lecithin, dairy phospholipids, and animal fat-derived mono-glycerides, maintain critical roles in specific high-value applications. Egg yolk lecithin’s superior phosphatidylcholine content makes it the preferred emulsifier in infant formula. Dairy-derived phospholipids from whey protein concentrate processing serve functional food applications where their specific biological activity, supporting gut health and cognitive function, creates functional food claim opportunities not achievable with plant alternatives.

Regional Market Insights

|

Region |

Share (2025) |

Key Drivers & Data |

|

Europe |

38.0% |

EU Regulation 1333/2008, clean label preference, Palsgaard/Corbion/BASF HQ; Farm to Fork Strategy |

|

Asia-Pacific |

27.6% |

India processed foods growth, Palsgaard Malaysia 20,000 MT factory, China processed food market, Japan functional food innovation |

|

North America |

21.9% |

GRAS framework flexibility, sunflower lecithin non-GMO demand, clean label trend, ADM/Cargill HQ |

|

Latin America |

6.5% |

Brazil food processing expansion, Mexico bakery growth, Argentina oilseed-to-lecithin supply chain, soy lecithin export hub to global markets |

|

Middle East & Africa |

6.0% |

Halal-certified emulsifier demand, UAE/Saudi Arabia food processing investment, Africa packaged food market, mono-glyceride import growth |

Europe’s 38.0% regional dominance in 2025 reflects the continent’s position as the global center of food ingredient quality standards and clean label innovation. EU Regulation 1333/2008’s harmonized positive list creates consistent demand for approved, safety-evaluated emulsifiers across 27 member states with a combined food processing market. European food manufacturers are the world’s most active clean label reformulators, driving premium emulsifier innovation at rates 3–5 years ahead of North American and Asia-Pacific markets.

Asia-Pacific, at 27.6% in 2025, is the market’s most dynamic growth region. Azelis’ 2024 distribution agreement with BASF for emulsifier supply in China, covering bakery, beverage, and nutrition channels, demonstrates multinational emulsifier companies’ strategic prioritization of China market penetration. North America (21.9%) benefits from the US’s flexible GRAS (Generally Recognized as Safe) framework that enables faster introduction of novel emulsifiers versus the EU’s positive list system, creating an innovation sandbox that generates commercial insights later applied to regulated European markets.

Competitive Landscape

The global food emulsifiers market is moderately concentrated. The top 5 players collectively account for an estimated 50–55% of total global market revenue in 2025.

|

Company Name |

Key Brand / Products |

Market Position |

Core Strength |

|

Archer-Daniels-Midland Company |

Stabrium |

Leader |

Vertically integrated oilseed processing, broad lecithin & mono-glyceride portfolio, AI formulation tools |

|

Louis Dreyfus |

LAMEGIN |

Leader |

Polyglycerol ester leadership, plant-based specialty emulsifiers, acquired by Louis Dreyfus in September 2025 |

|

Cargill Incorporated |

LECIPRIME, TOPCITHIN, EMULFLUID, EMULPUR, and LECIGRAN |

Leader |

Sunflower lecithin non-GMO expansion, clean label portfolio, vertically integrated soy/sunflower supply |

|

Croda International Plc |

CRILL |

Leader |

Sorbitan ester and polyglycerol ester specialty, pharmaceutical-grade crossover, Europe & Asia strength |

|

Ingredion Incorporated |

NOVATION, HI-CAP |

Challenger |

Clean-label starch-based emulsifying systems, encapsulation expertise |

|

Kerry Group plc |

Myverol, Admul, Myvatex, Puremul |

Challenger |

Functional ingredient crossover, emulsifier-nutrition blends, European clean label leadership |

|

Palsgaard A/S |

Palsgaard PGPR, Palsgaard SA, Emulpals |

Emerging |

Carbon-neutral certified; palm-free portfolio, sustainability leader |

Apart from top 5 players, the remaining share is distributed among regional specialists, oilseed processors with integrated lecithin operations, and specialty emulsifier companies serving niche application segments.

Key Company Profiles

Archer-Daniels-Midland Company (ADM)

Archer-Daniels-Midland Company is headquartered in Chicago, Illinois. ADM is one of the world’s largest agricultural processors, with food emulsifiers produced through its Nutrition segment encompassing human nutrition, animal nutrition, and specialty ingredients.

- Product Portfolio: ADM’s food emulsifier portfolio includes soy lecithin, sunflower lecithin, mono and di-glycerides, diacetyl tartaric acid esters (DATEM), and specialty emulsifier blends for bakery, confectionery, dairy, and plant-based food applications.

- Recent Developments: ADM completed portfolio restructuring of its Food and BioProducts Divisions in June 2024 .

- Strategic Focus: ADM’s emulsifier strategy leverages vertical integration from oilseed crushing to finished lecithin to deliver cost competitiveness in commodity lecithin while investing in value-added specialty grades, non-GMO, organic, enzymatically modified that command 25–40% price premiums and generate higher margins.

Louis Dreyfus

Louis Dreyfus is headquartered in Netherlands and acquired BASF SE’s Food and Health Performance Ingredients Business, including its food emulsifier portfolio, in September 2025.

- Product Portfolio: Louis Dreyfus’s food emulsifier business, which included whipping agents, food emulsifiers, and fat powder grades.

- Recent Developments: In September 2025, BASF and Louis Dreyfus Company (LDC) successfully completed the sale of BASF’s Food and Health Performance Ingredients Business.

- Strategic Focus: Louis Dreyfus’ acquisition of BASF’s food ingredients business reflects a strategic move to climb the value chain from agricultural commodity trading into specialty food ingredient manufacturing, where EBITDA margins of 18–25% significantly exceed commodity trading margins of 1–3%.

Cargill Incorporated

Cargill Incorporated is headquartered in Minnetonka, Minnesota. Cargill’s food emulsifier operations are housed within its Food Solutions segment, which provides texturizing and functional ingredient solutions to food manufacturers globally.

- Product Portfolio: Cargill’s food emulsifier portfolio includes soy lecithin, sunflower lecithin, LECIPRIME, TOPCITHIN, EMULFLUID, EMULPUR, and LECIGRAN.

- Recent Developments: In November 2024, Cargill successfully launched its new lecithin production process at its Antwerp facility with the delivery of seven custom-designed stainless steel tanks by Gpi Tanks .

- Strategic Focus: Cargill’s emulsifier strategy centers on leveraging its global oilseed supply chain advantages to maintain cost leadership in commodity lecithin while investing in clean label and functional specialty emulsifier categories that deliver 20–35% price premiums.

Palsgaard A/S

Palsgaard A/S, headquartered in Juelsminde, Denmark, is one of the world’s leading specialty emulsifier and stabilizer companies. Palsgaard specializes exclusively in food emulsifiers and stabilizer systems, unlike diversified chemical companies with emulsifier businesses as a small division.

- Product Portfolio: The company offers various food emulsifiers under Palsgaard PGPR, Palsgaard SA, Emulpals

- Recent Developments: In October 2025, Palsgaard expanded production of its Emulpals powdered cake emulsifiers to Brazil .

- Strategic Focus: Palsgaard’s strategy uniquely positions the company as the ‘most sustainable emulsifier company’, leveraging its 2018 carbon-neutral certification, palm-free product portfolio, and renewable energy-powered Danish manufacturing to command a 15–25% sustainability premium in European and North American markets where food manufacturer procurement teams face increasing ESG scrutiny on ingredient sourcing decisions.

Market Concentration Analysis

The global food emulsifiers market exhibits moderate concentration, with the top 5 players accounting for approximately 50–55% of total global revenue in 2025. The market bifurcates between vertically integrated agricultural commodity processors with emulsifier businesses embedded within larger ingredient portfolios, specialty chemical companies with dedicated emulsifier divisions, and pure-play specialist emulsifier manufacturers.

Consolidation activity has been significant: Louis Dreyfus’ acquisition of BASF’s food ingredients business represents the most significant recent market consolidation; Palsgaard’s Malaysia factory expansion demonstrates organic growth consolidation in Asia-Pacific.

Investment & Growth Opportunities

Fastest-Growing Segments

Polyglycerol esters at ~4.8% CAGR represent the highest-growth type segment, driven by increasing use in low-fat dairy emulsions and plant-based fat replacement applications where PGE’s superior HLB range flexibility enables formulation of reduced-fat products with maintained texture quality. Asia-Pacific at ~4.6% CAGR is the highest-volume growth regional opportunity. Palsgaard’s 20,000 MT Malaysia factory and Azelis’ China distribution agreement demonstrate that leading specialty emulsifier companies are actively investing to establish Asia-Pacific positions before local competitors achieve scale.

Emerging Markets

India’s food processing industry growth represents the most underpenetrated high-growth market for specialty food emulsifiers. India’s Food Safety and Standards Authority (FSSAI)’s alignment with Codex Alimentarius standards, progressively adopting internationally approved emulsifiers including polyglycerol esters and acetylated monoglycerides, is removing regulatory barriers to specialty emulsifier adoption.

Venture and Investment Trends

Fermentation-derived emulsifier startups are attracting accelerating investor interest. Strategic corporate venture capital is actively seeking minority stakes in clean-label emulsifier technology startups to track next-generation technologies before acquisition opportunities emerge. Companies that successfully scale fermentation-derived emulsifier production to 1,000+ metric ton commercial volumes between 2026 and 2030 will command 10–14x revenue acquisition multiples from strategic buyers seeking clean label technology assets.

Future Market Outlook (2026-2034)

The global food emulsifiers market is positioned for steady, structurally supported growth through 2034, anchored by the inelastic demand nature of emulsifiers as mandatory functional ingredients in processed food manufacturing. From USD 4.1 Billion in 2025, the market is forecast to reach USD 4.9 Billion by 2030 and USD 5.8 Billion by 2034, representing USD 1.7 Billion in absolute incremental market value over the nine-year forecast horizon at a consistent 3.84% CAGR.

Technological disruptions expected between 2026 and 2034 include the commercial scaling of fermentation-derived emulsifiers, biosurfactants and precision fermentation phospholipids, which promise to deliver clean label performance equivalent to or superior to conventional emulsifiers at competitive cost structures by 2030–2032.

The next decade will witness a bifurcation of the food emulsifiers market into two structurally distinct tiers: a commodity tier and a premium specialty tier. Companies that fail to establish credible positions in the premium specialty tier, either through organic product innovation or strategic acquisition of clean label emulsifier assets, face progressive margin erosion in the commodity tier as Chinese and Southeast Asian low-cost producers scale production capacity through 2034.

Research Methodology

Primary Research

Primary research encompassed over 55 structured interviews in 2024–2025 with food emulsifiers market participants including emulsifier R&D directors, food technologists at multinational bakery, confectionery, and dairy manufacturer, procurement managers at European food manufacturers transitioning to clean label emulsifier specifications, specialty food ingredient distributors, and regulatory affairs specialists familiar with EU Regulation 1333/2008 and FDA GRAS food additive frameworks.

Secondary Research

Key secondary sources include EU Regulation No. 1333/2008 and EFSA opinions on food additives, FDA 21 CFR food additive monographs, Cargill corporate data, Palsgaard carbon-neutral certification documentation, and trade publications including Food Ingredients International, Prepared Foods, and Nutraceuticals World.

Forecasting Models

IMARC’s Bottom-Up and Top-Down estimation models were applied. Bottom-Up aggregates emulsifier demand by type category (mono-glycerides, lecithin, sorbitan esters, polyglycerol esters) across application markets (bakery, confectionery, dairy, meat) in each regional market. Top-Down validates against global processed food market growth projections, EU food additive production volume statistics, and US food ingredient market benchmarks.

Food Emulsifiers Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Mono and di-glycerides and their Derivatives, Lecithin, Sorbitan Ester, Polyglycerol Ester, Others |

| Applications Covered | Confectionery Products, Bakery Products, Dairy and Frozen Desserts, Meat Products, Others |

| Sources Covered | Plant Source, Animal Source |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Archer-Daniels-Midland Company,Louis Dreyfus, Cargill Incorporated, Croda International Plc, Ingredion Incorporated, Kerry Group plc, Palsgaard A/S., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the food emulsifiers market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global food emulsifiers market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the food emulsifiers industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Food Emulsifiers Market Report

The global food emulsifiers market reached USD 4.1 Billion in 2025, growing from USD 3.4 Billion in 2020. Growth is driven by rising processed food demand, clean label trends, and plant-based food expansion globally.

The market is projected to reach USD 5.8 Billion by 2034 at a CAGR of 3.84%, passing through USD 4.9 Billion in 2030. Clean label reformulation, plant-based food growth, and Asia-Pacific processed food expansion are key drivers.

Mono and di-glycerides and their derivatives lead with 46.9% in 2025. They are used in bakery, dairy, and confectionery for dough conditioning, texture stability, and shelf-life extension due to cost-effectiveness and multifunctionality.

Plant-sourced emulsifiers dominate at 73.0% in 2025. Soy and sunflower lecithin, rapeseed mono-glycerides, and plant-based polyglycerol esters are preferred due to clean label demand and vegan certification requirements globally.

Europe leads at 38.0% in 2025, anchored by EU Regulation 1333/2008, consumer clean label preference, and Europe chocolate market growth

Asia-Pacific at 27.6% 2025 is fastest-growing at ~4.6% CAGR. India processed foods growth, Palsgaard opened a 20,000 MT Malaysia factory, Azelis secured BASF emulsifier distribution in China in 2024.

Key players include Archer-Daniels-Midland Company, Louis Dreyfus, Cargill Incorporated, Croda International Plc, Ingredion Incorporated, Kerry Group plc, and Palsgaard A/S.

Key drivers include rising processed food demand, European consumer clean label preference, global plant-based food market growth, expanding bakery market, and Asia-Pacific food processing growth.

Lecithin is a natural phospholipid from soy or sunflower, preferred for clean label applications at 21.8% share. Mono-glycerides are synthetic fatty acid esters at 46.9% share, valued for lower cost and broader functionality in bakery and dairy.

Clean label drives reformulation from synthetic DATEM and SSL toward sunflower lecithin and palm-free alternatives.

Key challenges include soy/sunflower/palm feedstock price volatility, EU regulatory compliance costs of EUR 5-10M per new emulsifier approval, consumer perception issues with E-numbers, and EU Deforestation Regulation driving palm-free reformulation requirements.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)