Football Market Size, Share, Trends and Forecast by Type, Size, Distribution Channel, and Region, 2026-2034

Football Market Size, Share, Trends & Forecast (2026-2034)

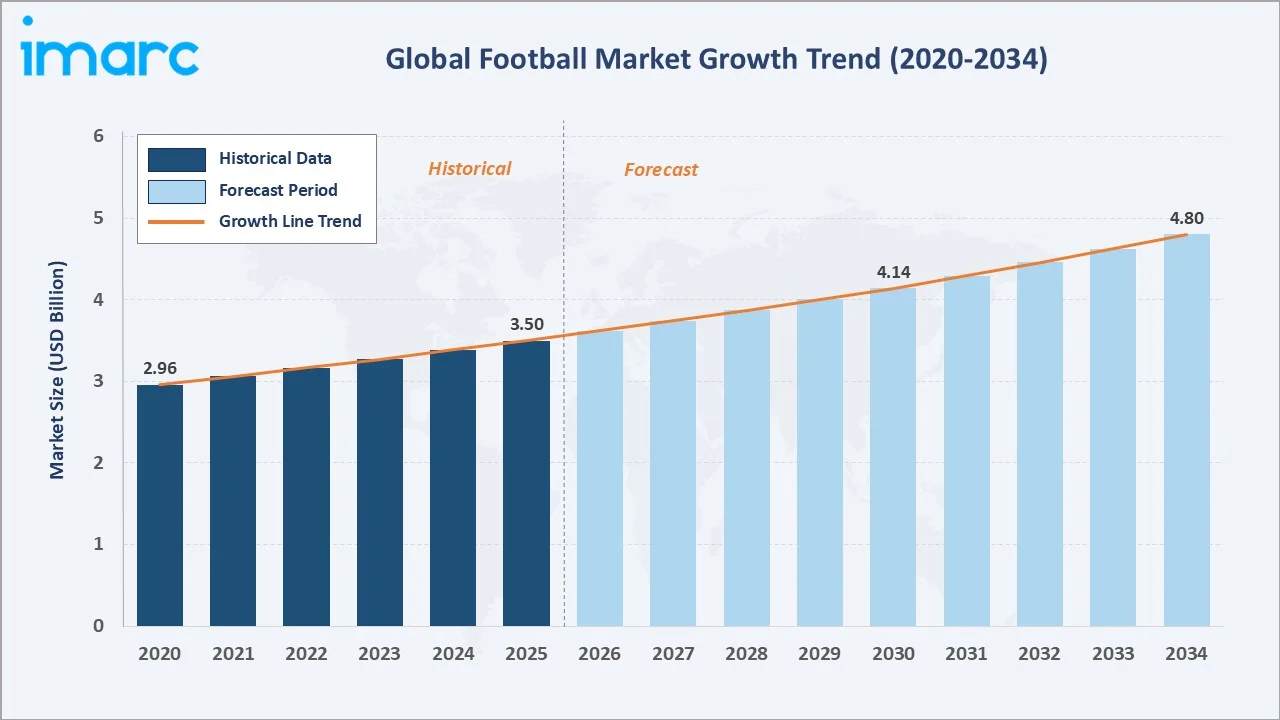

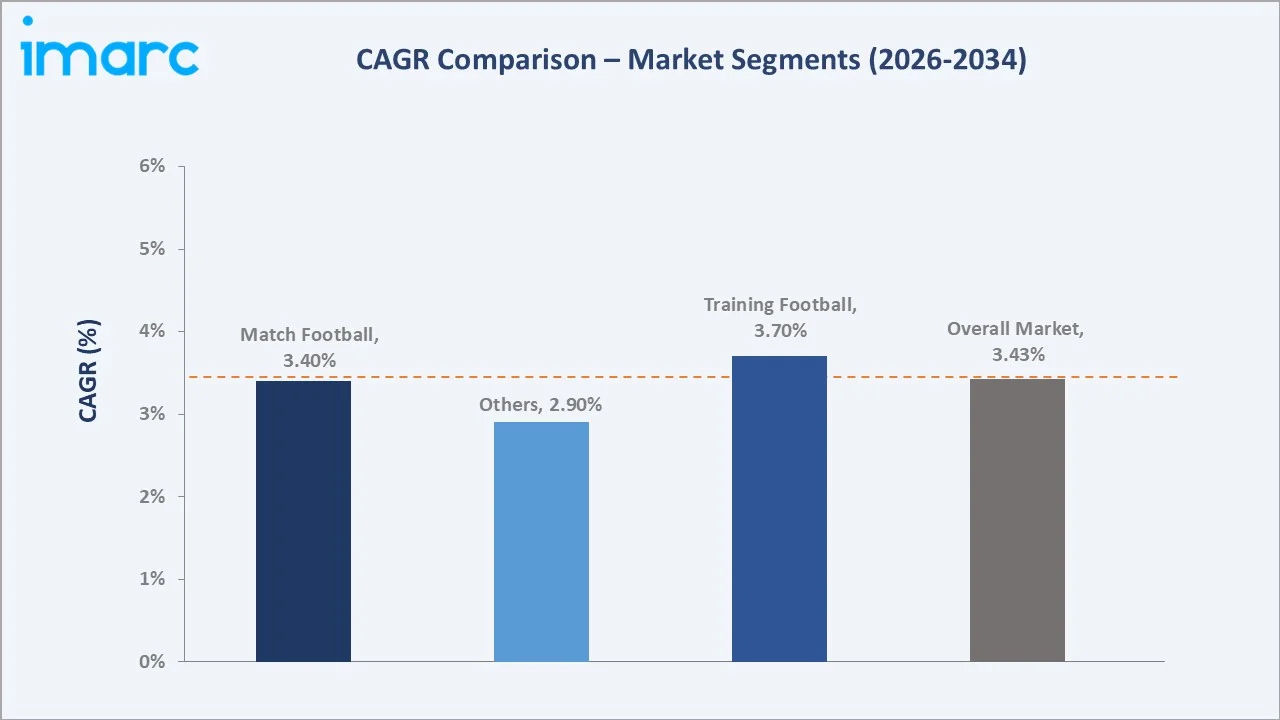

The global football market reached USD 3.50 Billion in 2025 and is projected to reach USD 4.80 Billion by 2034, growing at a CAGR of 3.43% during 2026-2034. Rising global football participation, proliferation of international tournaments, growing sponsorship and partnership ecosystems, expansion of e-sports and digital gaming platforms, and the increasing adoption of online retail channels are the primary growth catalysts.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 3.50 Billion |

|

Forecast Market Size (2034) |

USD 4.80 Billion |

|

CAGR (2026-2034) |

3.43% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

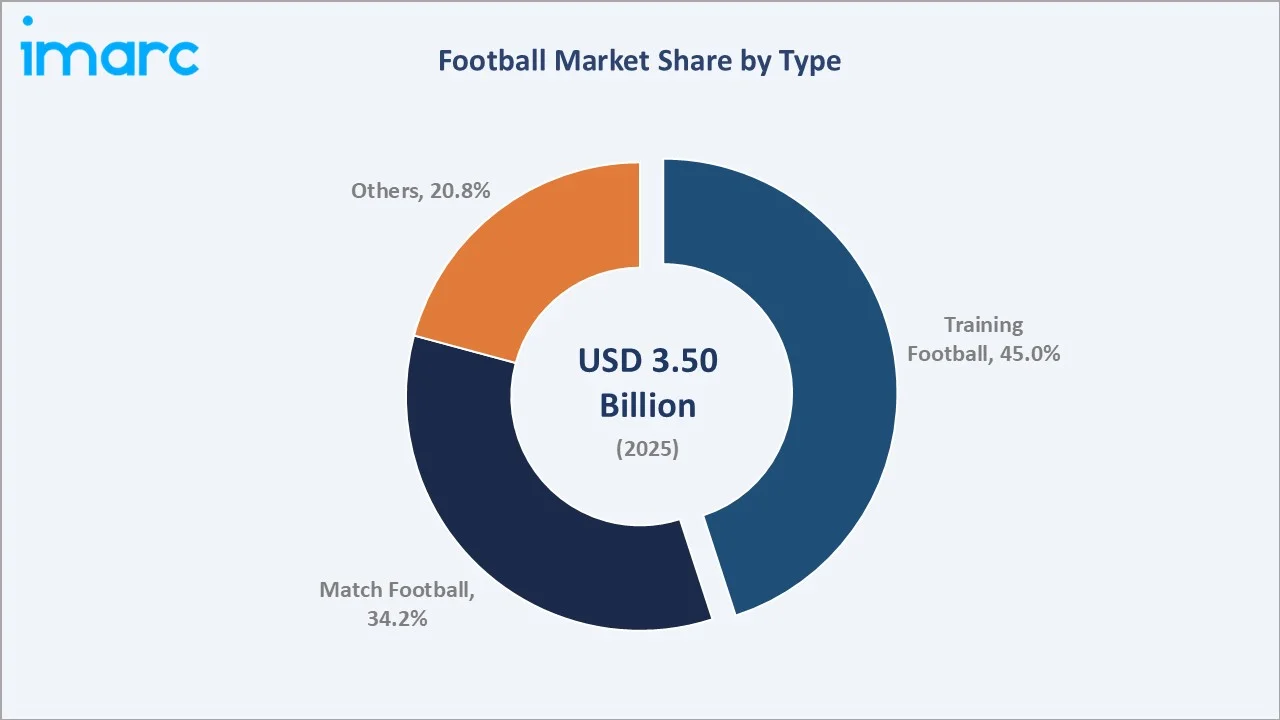

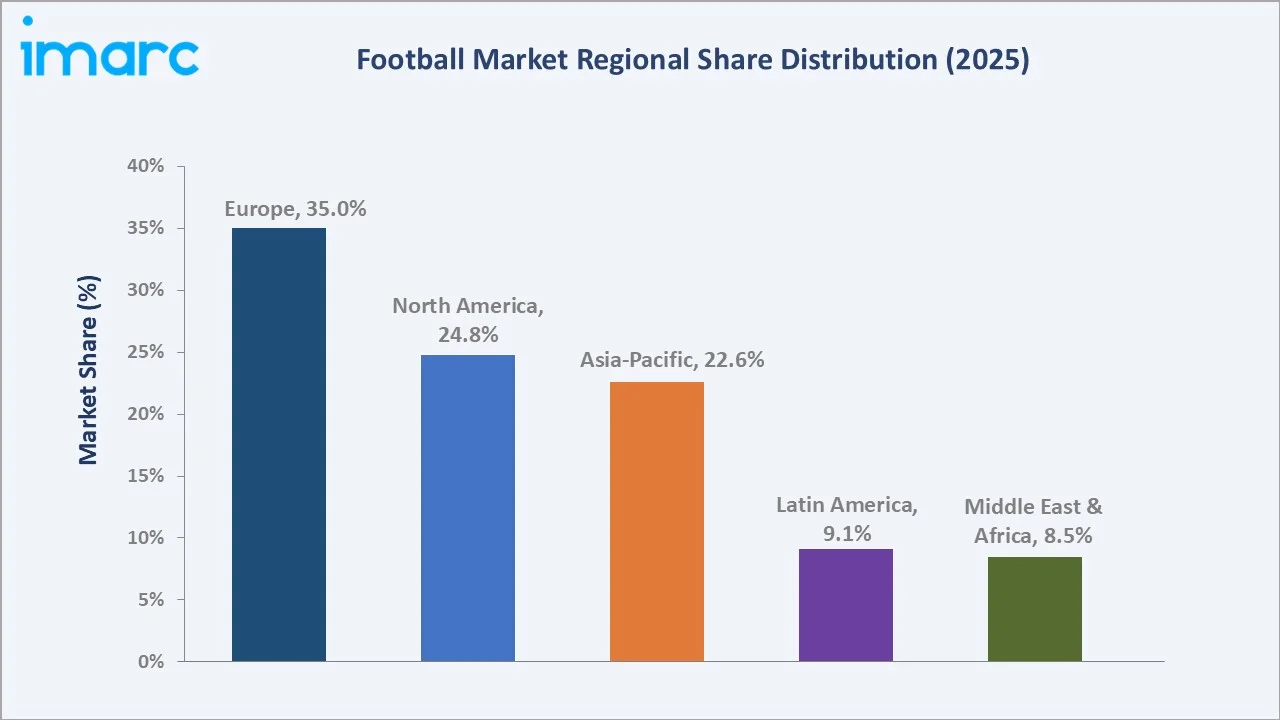

Europe leads regionally with a 35.0% share in 2025, driven by its deep-rooted football culture and the presence of elite leagues including the English Premier League, La Liga, Serie A, and Bundesliga. Training football commands the dominant type segment at 45.0%, while offline distribution channels retain the largest distribution share at 70.0% despite rapid online channel growth.

To get more information on this market, Request Sample

The market grew from USD 2.96 Billion in 2020 to USD 3.50 Billion in 2025, reflecting a historical CAGR of approximately 3.43%. The forecast period 2026–2034 projects sustained growth anchored by the FIFA World Cup North America 2026, expanding grassroots football programs globally, and accelerating digital retail penetration across all geographies.

Executive Summary

The global football market is experiencing steady, sustained growth underpinned by rising global football participation, the proliferation of international tournaments, and deepening brand investment in sponsorships and digital engagement. The market reached USD 3.50 Billion in 2025 and is forecast to reach USD 4.80 Billion by 2034 at a CAGR of 3.43%.

Training football dominates the product type segment with a 45.0% share in 2025, reflecting the large base of amateur, recreational, and academy-level players globally who require durable, cost-effective training balls. Offline distribution channels retain a 70.0% share, supported by sports specialty stores and national retail chains, though online channels growing at approximately 5.2% CAGR are rapidly gaining share.

Key players including adidas AG, NIKE, Inc., PUMA SE, SELECT Sport International, and molten Corporation are competing through product innovation, sustainability initiatives, FIFA/UEFA licensing agreements, and expanding digital retail presence to capture growing demand across both professional and grassroots segments.

Key Market Insights

|

Insight |

Data |

|

Largest Type Segment |

Training Football – 45.0% share (2025) |

|

Fastest Growing Type |

Training Football – ~3.7% CAGR (2026-2034) |

|

Largest Distribution Channel |

Offline – 70.0% share (2025) |

|

Fastest Growing Channel |

Online – ~5.2% CAGR (2026-2034) |

|

Leading Region |

Europe – 35.0% share (2025) |

|

Top Companies |

adidas AG, NIKE, Inc., PUMA SE, SELECT Sport International, and molten Corporation |

Key Analytical Observations Supporting the Above Data:

- Training football at 45.0% (2025) reflects the dominant role of non-professional players in total football ball demand. With FIFA’s Big Count survey estimating over 265 million total registered players globally and hundreds of millions of recreational participants, the training segment underpins consistent baseline demand regardless of professional tournament cycles.

- Offline distribution at 70.0% (2025) reflects the ongoing importance of in-store purchasing for footballs, driven by consumers' preference to physically inspect ball quality, size, and feel before purchase. Sports specialty retailers, general sporting goods chains, and club-affiliated pro shops sustain offline dominance across all major markets.

- Online distribution at 30.0%, growing at ~5.2% CAGR, represents the market's fastest structural shift. Direct-to-consumer e-commerce platforms by Adidas, Nike, and PUMA, alongside sports retail marketplaces, are democratizing access to premium footballs across emerging markets in Asia-Pacific, Latin America, and the Middle East.

- Europe's 35.0% share (2025) reflects the region's unrivalled football culture, club density, and tournament ecosystem. The English Premier League, La Liga, Serie A, Bundesliga, and Ligue 1 collectively generate demand for tens of millions of match and training balls annually, directly supporting European market leadership through 2034.

Football Market Overview

Football encompasses spherical sporting equipment used in association football (soccer), designed for training, recreational, and professional match applications. The global market spans multiple product types including training footballs, match-grade FIFA-certified balls, and specialty segment balls, distributed through offline sports retailers, department stores, and rapidly expanding online platforms. Key ball manufacturers including Adidas, Nike, and PUMA supply official match balls to FIFA, UEFA, and major domestic league competitions, lending their products an aspirational association with elite football events.

The market is shaped by the interplay of professional sports licensing, grassroots participation, and digital retail transformation. FIFA estimates that association football is played by over 265 million total registered players globally, providing a structurally large and growing addressable market. The growing global middle class in Asia-Pacific, Latin America, and Africa is expanding the accessible consumer base for branded footballs beyond traditional European and North American strongholds.

Market Dynamics

To evaluate market opportunities, Request Sample

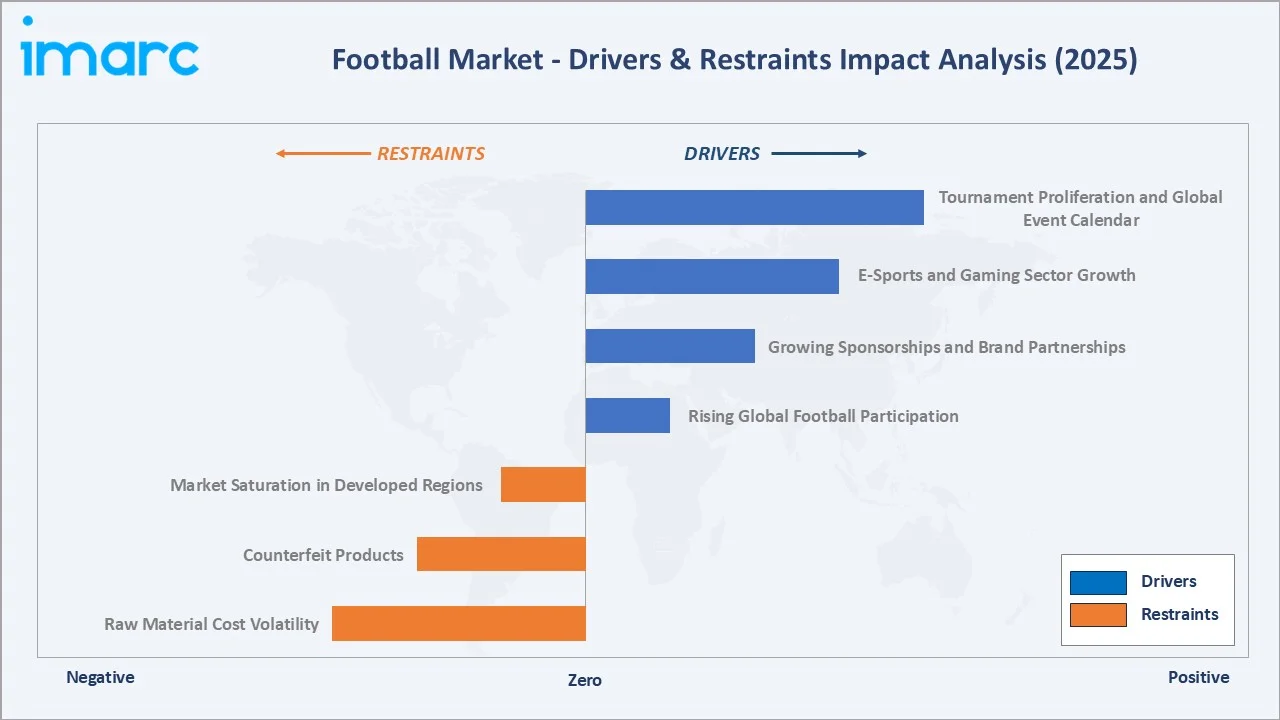

Market Drivers

- Rising Global Football Participation: The global football fan base is estimated at around five billion people, with Latin America, the Middle East, and Africa representing some of the largest concentrations of supporters worldwide. This massive and highly engaged audience continues to drive growth in the football market.

- Growing Sponsorships and Brand Partnerships: Major brands including Adidas, Nike, and PUMA invest billions of dollars annually in football sponsorships. PUMA's March 2022 long-term partnership with Lega Serie A as official technical partner and match ball supplier exemplifies how licensing agreements drive both brand revenue and market visibility, stimulating consumer demand through association with elite competitions.

- E-Sports and Gaming Sector Growth: The expanding FIFA (EA Sports FC) and Football gaming ecosystem creates a powerful digital marketing platform for football brands. In June 2023, One Future Football (1FF) inaugurated a global digital soccer league with 250 CGI players across 12 clubs, reflecting the convergence of digital engagement and physical football product demand.

- Tournament Proliferation and Global Event Calendar: The FIFA World Cup North America 2026, UEFA European Championship, Copa América, and continental confederation tournaments create recurring demand spikes for match and replica balls. Each major FIFA tournament generates tens of millions of ball sales in official match, replica, and training variants, directly supporting market revenue growth.

Market Restraints

- Raw Material Cost Volatility: Premium football balls require synthetic leather (polyurethane), natural rubber latex bladders, polyester/nylon panels, and specialty inks. Fluctuations in petrochemical feedstock prices and natural rubber supply directly impact manufacturing costs, compressing margins for mid-tier manufacturers and limiting price accessibility for consumers in price-sensitive emerging markets.

- Counterfeit Products: The global trade in counterfeit sporting goods represents a significant threat to branded football market revenue. Imitation FIFA-branded and club-branded footballs sold through informal retail channels in Asia, Latin America, and Africa undermine official brand revenue, erode consumer trust in product quality standards, and create safety concerns around sub-standard bladder materials.

- Market Saturation in Developed Regions: Mature markets in Western Europe and North America show moderate growth rates constrained by high existing penetration of branded footballs and slowing population growth. Premium ball replacement cycles are lengthening as product durability improves, limiting volume growth potential in already-developed markets without corresponding share-of-wallet gains.

Market Opportunities

- Emerging Market Penetration: Rapidly growing football participation in India, Indonesia, Nigeria, and Brazil presents significant untapped demand for mid-tier training footballs. India's growing grassroots football infrastructure, led by the All India Football Federation's grassroots program, and Indonesia's football development initiatives collectively represent a multi-hundred-million addressable market for cost-effective training balls through 2034.

- Smart Football Technology Innovation: Adidas's Jabulani and Brazuca innovations and new-generation connected ball technology with embedded sensors tracking spin, speed, and trajectory represent a premium product innovation opportunity. Smart footballs targeting elite academies, coaching analytics programs, and technology-driven training environments create a high-margin product tier that can command significant price premiums above standard training balls.

Market Challenges

- Sustainability and Regulatory Compliance: Growing regulatory and consumer pressure on synthetic materials in sporting goods is compelling manufacturers to invest in bio-based polyurethane, recycled polyester panels, and FSC-certified packaging. Adidas and Nike's sustainability commitments require capital-intensive supply chain transformations, raising production costs and creating compliance complexity across multi-country manufacturing networks in Pakistan, China, and Southeast Asia.

- Supply Chain Concentration Risk: Approximately 70% of global hand-stitched football ball production is concentrated in Sialkot, Pakistan, creating significant single-geography supply chain risk from geopolitical disruption, natural disasters, labor disputes, or regulatory changes. This concentration exposes major brands to supply disruption vulnerability and limits manufacturers' ability to rapidly diversify production across alternative low-cost locations.

Emerging Market Trends

1. FIFA World Cup North America 2026 – Demand Catalyst

The FIFA World Cup North America 2026 generates demand for additional official match balls, training balls, and fan merchandise across three host nations. In October 2025, Adidas unveiled the official match ball for the 2026 FIFA World Cup, named “Trionda,” incorporating advanced connected-ball technology, including a 500Hz motion sensor chip to support VAR decisions and improve in-game accuracy during the tournament.

2. PUMA AI-Powered Football Design

In December 2024, PUMA launched its AI Creator tool powered by DEEPOBJECTS, enabling Manchester City fans to design personalized football kits using generative AI with text prompts, sliders, and creative tools. This AI-driven fan engagement platform represents a new frontier in sports product personalization and brand activation, demonstrating the convergence of artificial intelligence and consumer football products in ways that drive brand loyalty and premium product demand.

3. Public Investment Fund Official Supporter of the 2026 FIFA World Cup

In May 2026, Public Investment Fund was named an official tournament supporter of the 2026 FIFA World Cup as Saudi Arabia accelerated its global football ambitions through increased investments in sports sponsorships, clubs, and international tournaments. The partnership is expected to strengthen Saudi Arabia’s presence in global football ahead of hosting the 2034 FIFA World Cup while boosting commercial growth, fan engagement, and sports tourism opportunities across the football market.

4. Nike to Become Official Match Ball Provider for UEFA Men’s Club Competitions

In April 2026, NIKE, Inc. entered exclusive negotiations with UEFA to become the official match ball supplier for UEFA men’s club competitions from 2027 to 2031, potentially replacing Adidas after a 25-year partnership. The proposed agreement would cover the Champions League, Europa League, and Conference League, strengthening Nike’s visibility and commercial presence across global football.

Industry Value Chain Analysis

The football market value chain encompasses raw material extraction through to final consumer delivery, with geographic concentration in Pakistan (Sialkot manufacturing cluster), China, and Southeast Asia for production, and global distribution networks spanning specialty sports retail, mass market retail, and direct e-commerce channels across all major consuming regions.

|

Stage |

Value-Add Activity |

|

Raw Materials |

Premium synthetic leather, natural rubber latex, and panel material sourcing |

|

Component Mfg. |

Precision panel cutting, bladder curing, multi-layer lining lamination |

|

Ball Assembly & QC |

Hand-stitching or thermally bonded assembly; FIFA quality testing and certification |

|

Brand Marketing |

Official match ball licensing, tournament branding, athlete endorsement, digital marketing |

|

Distribution & Retail |

Multi-channel distribution; direct-to-consumer digital channels; global logistics |

Technology Landscape in the Football Industry

Training Football – Core Market Volume Driver

Training football leads the market at 45.0% share in 2025, encompassing balls used for practice, recreational play, and coaching drills across all skill levels. Major manufacturers including Adidas, Nike, and SELECT have developed entry-to-mid-tier training ball lines targeting the massive global base of amateur clubs, school programs, and individual players, driving consistent volume demand independent of professional tournament cycles.

Match Football – Premium Revenue Driver

Match Football accounts for 34.2% of market share in 2025, representing the premium tier of the global football market. FIFA-certified match balls, including the Adidas Al Rihla (Qatar 2022) and 2026 FIFA World Cup ball Trionda (October 2025), must meet stringent performance specifications for circumference, weight, pressure, and water absorption.

Smart Football and Technology Integration

Smart football technology incorporating embedded electronic sensors, GPS tracking, and Bluetooth connectivity represents an emerging premium tier. KINEXON and SELECT Sport International introduced the SELECT Brillant Super iBall, the first FIFA Quality Pro-approved football with an integrated tracking sensor capable of delivering real-time match data such as shot speed, pass accuracy, and ball trajectory.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Training Football |

45.0% |

2025 |

|

Size |

🔒 |

🔒 |

2025 |

|

Distribution Channel |

Offline |

70.0% |

2025 |

|

Region |

Europe |

35.0% |

2025 |

By Type

Training football dominates the type segment with a 45.0% share in 2025. This segment benefits from the fundamental economics of football participation: for every professional or elite player purchasing high-grade match balls, there are thousands of recreational, school, and amateur players requiring durable training balls that deliver adequate performance at accessible price points.

To access detailed market analysis, Request Sample

Match football at 34.2% reflects the premium segment driven by professional club procurement, national association official ball contracts, and aspirational consumer purchases of FIFA-certified balls associated with iconic tournaments.

By Distribution Channel

Offline distribution channels account for 70.0% of the global football market in 2025, reflecting the importance of in-store product experience for purchasing decisions. Physical retail channels encompass specialist sports retailers, department stores, brand flagship stores, and club-affiliated pro shops.

Online channels at 30.0%, growing at approximately 5.2% CAGR, represent the market's fastest-growing distribution segment. Direct-to-consumer e-commerce platforms by Adidas, Nike, and PUMA, combined with multi-brand sports e-tailers such as Amazon, Zalando, and regional equivalents, are expanding football product accessibility globally.

Regional Market Insights

Europe's market leadership (35.0%, 2025) reflects the region's unrivalled football cultural heritage and institutional infrastructure. The English Premier League, La Liga, Serie A, Bundesliga, and Ligue 1 collectively generate demand for official match balls, training equipment, and fan merchandise on a scale unmatched by any other region globally.

North America at 24.8% is experiencing above-average growth driven by MLS expansion, the FIFA World Cup 2026 co-hosting effect across the US, Canada, and Mexico, and the structural growth of youth soccer participation as the sport gains share from traditional American sports.

|

Region |

Share (2025) |

Key Growth Drivers |

|

Europe |

35.0% |

Premier League, La Liga, Serie A, Bundesliga; UEFA tournament calendar; strong sports retail infrastructure |

|

North America |

24.8% |

MLS expansion; FIFA World Cup 2026 host nation boost; growing youth soccer participation; NBA/NFL cross-sport consumer overlap |

|

Asia-Pacific |

22.6% |

Expanding football academies in China, India, and Southeast Asia; rising middle-class demand for branded footballs |

|

Latin America |

9.1% |

Copa Libertadores and Copa América fan culture; Brazil and Argentina domestic league demand; FIFA grassroots program expansion |

|

Middle East & Africa |

8.5% |

Saudi Pro League global player investment; CAF Africa Cup of Nations; Vision 2030 sport development initiatives in Saudi Arabia |

Asia-Pacific at 22.6% is underpinned by China's football development master plan, India's rapidly expanding grassroots programs, and Southeast Asia's endemic football passion across Indonesia, Thailand, and the Philippines.

Competitive Landscape

The global football market exhibits moderate concentration, with the top five players (adidas AG, NIKE, Inc., PUMA SE, SELECT Sport International, and molten Corporation) collectively holding approximately 55–60% of global market revenue in 2025. Global sports brands Adidas and Nike dominate through official FIFA and UEFA match ball licensing agreements and comprehensive product portfolios spanning professional to entry-level price tiers.

|

Company Name |

Key Brands |

Market Position |

Core Strength |

|

adidas AG |

Adidas |

Market Leader |

Official FIFA World Cup match ball supplier; Al Rihla heritage; sustainable Conext ball line |

|

NIKE, Inc. |

Nike |

Market Leader |

Flight (premier), Magia, Strike (mid-tier), Academy, and Pitch ball lines; DTC digital-first distribution model |

|

PUMA SE |

PUMA |

Strong Challenger |

La Liga, Serie A, and Premier League match ball partner; replica and training portfolio |

|

SELECT Sport International |

SELECT |

Strong Challenger |

FIFA-certified hand-stitched ball expertise; Preferred ball in the Danish, German (via Derbystar), Belgian and Portuguese leagues |

|

molten Corporation |

Molten |

Challenger |

FIFA Quality Pro certified balls; dominant in Asian football federations |

Market consolidation is occurring through global sports brands expanding their football-specific product ranges while specialist ball manufacturers defend technical differentiation in professional and semi-professional market tiers.

Key Company Profiles

adidas AG

adidas AG is one of the world’s largest football-specific sports brands and the official FIFA World Cup match ball supplier. The company's football product portfolio spans professional match balls, training balls, and replica collections used across all levels of the global game, from FIFA finals to grassroots academies.

- Product Portfolio: Official FIFA World Cup match balls (Al Rihla, Brazuca, Jabulani), Conext sustainable training ball series, Tiro Club and Liga entry-level training balls, and specialty futsal and beach soccer ball variants across professional, amateur, and recreational segments.

- Recent Developments: In October 2025, adidas AG introduced the official FIFA World Cup 2026 match ball, TRIONDA, through large-scale launch events in New York, Toronto, and Mexico City. The campaign used hologram displays, fan activations, and cultural celebrations to strengthen global football fan engagement ahead of the 2026 FIFA World Cup.

- Strategic Focus: Maintaining FIFA World Cup official match ball exclusivity; expanding sustainable football product lines using bio-based materials and recycled polyester; DTC digital channel growth targeting premium consumer segments.

NIKE, Inc.

NIKE, Inc. football division encompasses official match ball supply to major domestic leagues and national teams, combined with a comprehensive training and recreational ball portfolio targeting all consumer segments from elite professional to entry-level grassroots.

- Product Portfolio: Flight (premier), Magia, Strike (mid-tier), Academy, and Pitch, along with futsal, beach soccer, and street football specialist variants.

- Recent Developments: In April 2026, NIKE, Inc. entered exclusive negotiations with UEFA to become the official match ball supplier for UEFA men’s club competitions from 2027 to 2031. The proposed deal would cover the Champions League, Europa League, and Conference League, strengthening Nike’s visibility in European football and enhancing its global sports marketing.

- Strategic Focus: DTC digital channel investment targeting millennial and Gen Z football consumers; sustainable product development using recycled polyester and water-based inks.

PUMA SE

PUMA SE is one of the world's leading sports brands with a strong heritage in football product design, club kit supply, and official league ball partnerships. PUMA's football division supplies official match balls to Serie A, national teams, and federation competitions globally.

- Product Portfolio: ORBITA (official Serie A match ball), Prestige and Team categories for training and recreational use, and the PUMA King and Future boot-and-ball integration product lines across professional and amateur football segments.

- Recent Developments: In June 2025, PUMA unveiled its new official Premier League match ball for the 2025/26 season under the “Have a Ball” campaign, marking the beginning of its partnership with the Premier League.

- Strategic Focus: Generative AI and digital consumer engagement platform development; Africa and Middle East football market expansion through national association sponsorships.

Market Concentration Analysis

The global football market exhibits moderate concentration, with the top five players (adidas AG, NIKE, Inc., PUMA SE, SELECT Sport International, and molten Corporation) collectively holding approximately 55–60% of global market revenue in 2025. The market's two-tier structure separates global sports conglomerates competing primarily on brand equity, tournament licensing, and DTC digital channels from technical specialist manufacturers competing on ball quality, federation endorsements, and professional market segment expertise.

Market concentration at the premium tier is high and expected to remain so, given the structural advantage of FIFA and UEFA official ball licensing agreements in driving consumer brand preference. Below the premium tier, a competitive mid-market of specialist manufacturers and regional brands serves price-sensitive amateur and recreational segments.

Investment & Growth Opportunities

Fastest Growing Segments

Online distribution channels (~5.2% CAGR), training football (~3.7% CAGR), and the Asia-Pacific region (~4.5% CAGR) represent the highest-growth investment vectors through 2034. The FIFA World Cup 2026 represents a near-term demand catalyst projected to generate a significant incremental market revenue spike across all product types and distribution channels during the host year, with lasting brand awareness effects sustaining above-trend growth in North America through 2028.

Emerging Market Expansion

Asia-Pacific, growing at approximately 4.5% CAGR, represents the most significant emerging market expansion opportunity through 2034. India's rapidly expanding grassroots football infrastructure, China's continued football development investment despite previous program setbacks, and Southeast Asia's endemic football passion across Indonesia, Thailand, and the Philippines collectively represent a multi-hundred-million addressable market for branded football products at accessible price points.

Venture and Investment Trends

- Global sports brands invested over USD 5 Billion collectively in football sponsorships, club partnerships, and national association agreements in 2024–2025, with FIFA World Cup 2026 activation commitments representing the largest near-term capital deployment cycle in the football market's history.

- Smart football technology investment is accelerating, with connected ball manufacturers attracting venture capital backing to scale embedded sensor and analytics platforms targeting elite academies, coaching programs, and technology-driven training environments at premium USD 200–500+ price points.

Future Market Outlook (2026-2034)

The global football market is positioned for steady, profitable growth through 2034. From USD 3.50 Billion in 2025, the market is projected to reach USD 4.80 Billion by 2034 at a CAGR of 3.43%. The FIFA World Cup North America 2026 represents the most significant near-term demand catalyst, with projected market revenue acceleration during the host year driven by official ball sales, replica purchases, and grassroots program-linked demand across the three host nations.

The 2026–2034 period will be defined by three structural shifts: the continued expansion of grassroots football participation in Asia-Pacific, Africa, and Latin America; the accelerating transition of distribution toward online and direct-to-consumer digital channels, improving margin structures for leading brands; and the increasing integration of technology in football products, creating premium smart ball categories.

Research Methodology

Primary Research

Primary research comprised structured interviews with over 85 industry participants in 2024–2025, including football ball manufacturers, sports retail buyers, national federation procurement officers, football academy directors, consumer insights specialists, and investment analysts covering sports goods equities across Europe, North America, Asia-Pacific, and Latin America.

Secondary Research

Secondary research encompassed adidas AG, Nike Inc., and PUMA SE annual reports; FIFA and UEFA official equipment market publications; Statista global football market data; Business of Sports intelligence reports; and industry publications including SportsPro, Sporting Goods Intelligence, and the World Football Report. Regional football association data from UEFA, AFC, CAF, CONMEBOL, and CONCACAF supplemented global market estimations.

Forecasting Models

Market size estimations used top-down and bottom-up modelling incorporating global registered player population data (FIFA estimates), per-player ball consumption rates by market segment, average selling price trajectories by product type, and distribution channel mix projections. A base-case CAGR of 3.43% reflects consensus sports goods market growth estimates validated against FIFA World Cup 2026 demand projections and leading manufacturer revenue guidance for the 2026–2034 period.

Football Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Training Football, Match Football, Others |

| Sizes Covered | Size 1, Size 2, Size 3, Size 4, Size 5 |

| Distribution Channels Covered | Online, Offline |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | adidas AG, NIKE, Inc., PUMA SE, SELECT Sport International, molten Corporation, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the football market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global football market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the football industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Football Market Report

The global football market reached USD 3.50 Billion in 2025 and is projected to reach USD 4.80 Billion by 2034.

The market is expected to grow at a CAGR of 3.43% during 2026-2034, driven by rising football participation, tournament proliferation, sponsorship growth, and expanding online distribution channels globally.

Training football leads with a 45.0% share in 2025, reflecting the dominant role of amateur, recreational, and academy-level players in total football ball demand across all geographies.

Offline distribution channels dominate with a 70.0% share in 2025, driven by consumers' preference for in-store tactile product evaluation across sports specialty retailers, department stores, and club pro shops.

Europe leads with a 35.0% regional share in 2025, anchored by iconic leagues (Premier League, La Liga, Serie A, Bundesliga) and the region's deeply embedded grassroots football infrastructure and club culture.

Key players include adidas AG, NIKE, Inc., PUMA SE, SELECT Sport International, and molten Corporation, among others.

FIFA World Cup North America 2026 is the single largest near-term demand catalyst, projected to drive significant official ball, replica, and training ball sales uplift across the US, Canada, and Mexico, sustaining above-trend North American market growth through 2028.

Online channels growing at approximately 5.2% CAGR are the market's fastest-growing distribution segment, driven by DTC e-commerce platforms from Adidas, Nike, and PUMA and expanding digital retail penetration across Asia-Pacific and Latin America.

Key challenges include counterfeit product proliferation, raw material cost volatility from polyurethane and latex price fluctuations, supply chain concentration risk in Sialkot manufacturing, and sustainability compliance requirements across manufacturing networks.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)