France Diabetes Market Size, Share, Trends and Forecast by Segment and Distribution Channel, 2026-2034

France Diabetes Market Size, Share, Trends & Forecast (2026-2034)

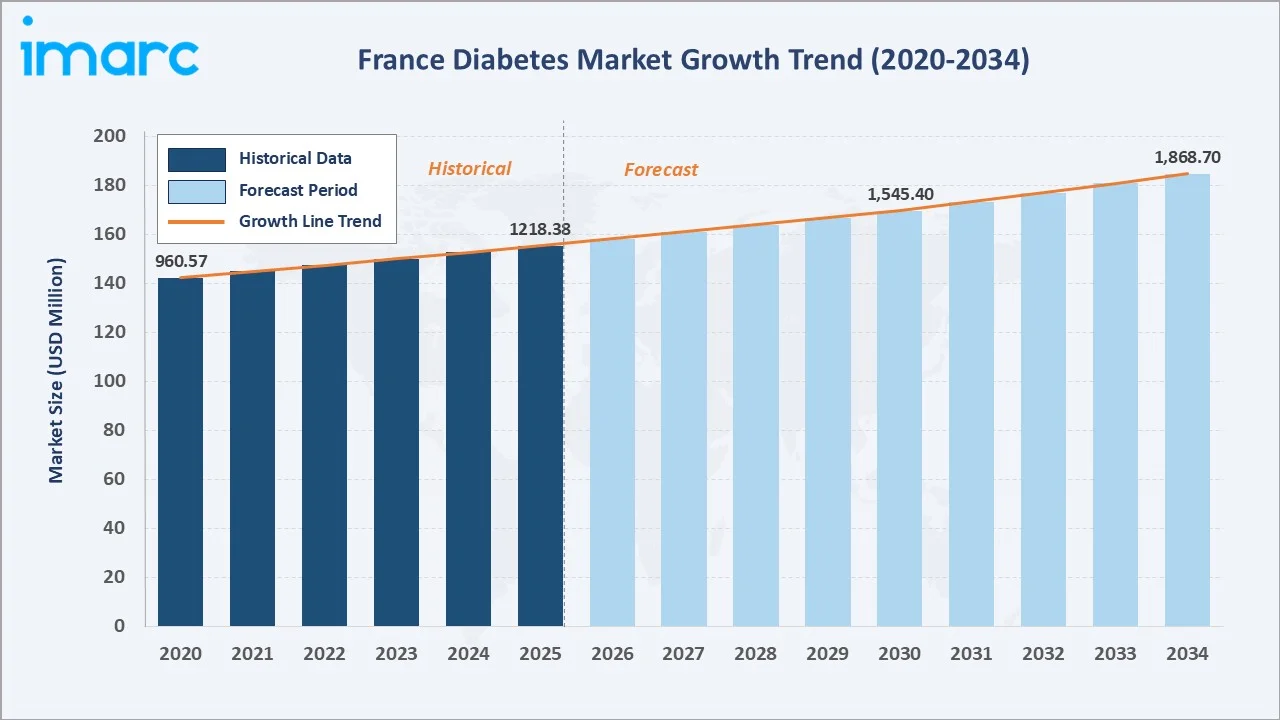

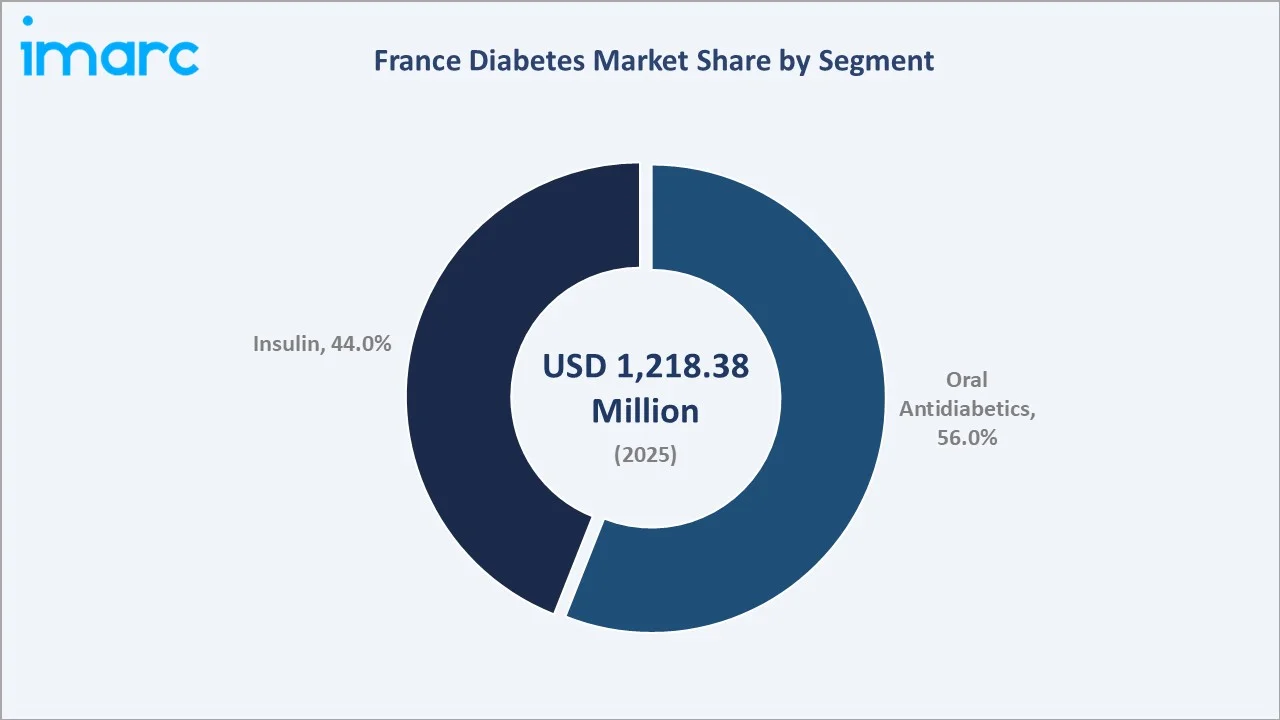

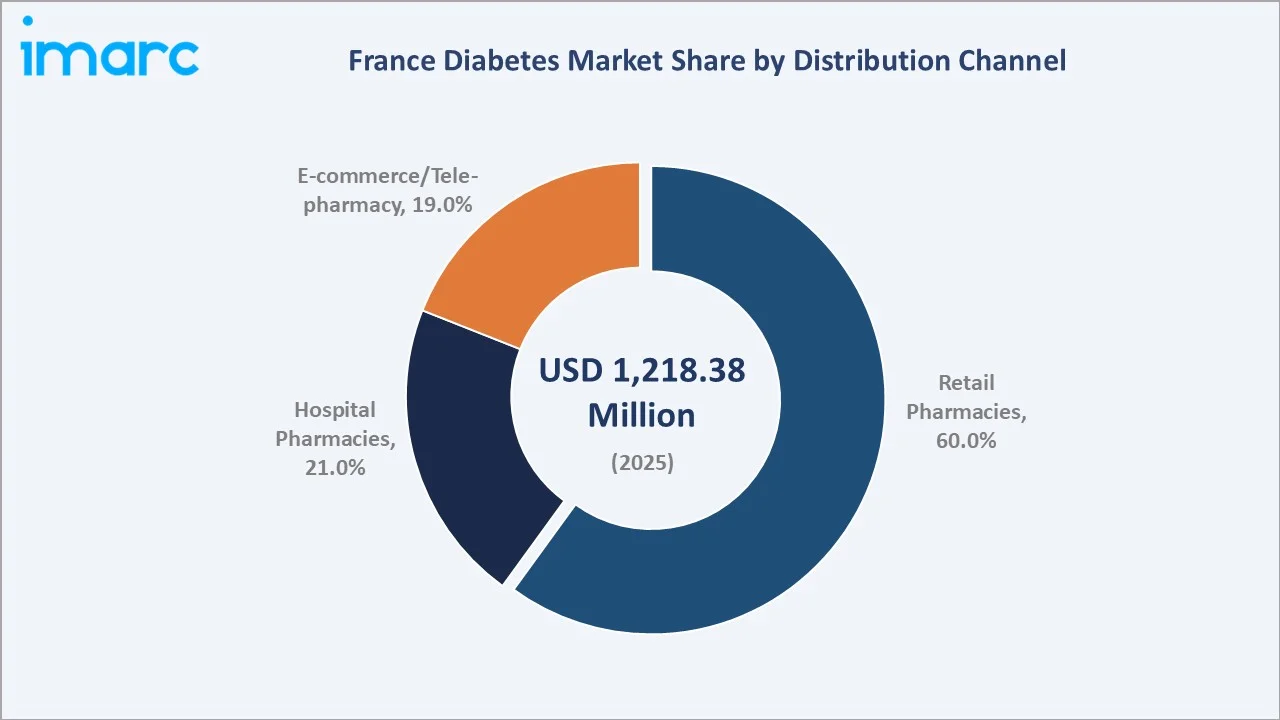

The France diabetes market was valued at USD 1,218.38 Million in 2025 and is projected to reach USD 1,868.70 Million by 2034, expanding at a CAGR of 4.87% during 2026-2034. Growth is driven by rising diabetes prevalence, with 4.1 million adults with diabetes in 2024 from France's ageing population and obesity epidemic, premium SGLT-2 inhibitor and GLP-1 RA adoption driving oral antidiabetic average selling price uplift, universal reimbursement enabling full patient access, and digital health and tele-pharmacy channel expansion. Oral antidiabetics lead at 56.0% and retail pharmacies dominate at 60.0%.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 1,218.38 Million |

|

Forecast Market Size (2034) |

USD 1,868.70 Million |

|

CAGR (2026-2034) |

4.87% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

The France diabetes market expanded from USD 960.57 Million in 2020 to USD 1,218.38 Million in 2025. Anchored at USD 1,545.40 Million in 2030, the forecast projects to USD 1,868.70 Million by 2034.

To get more information on this market, Request Sample

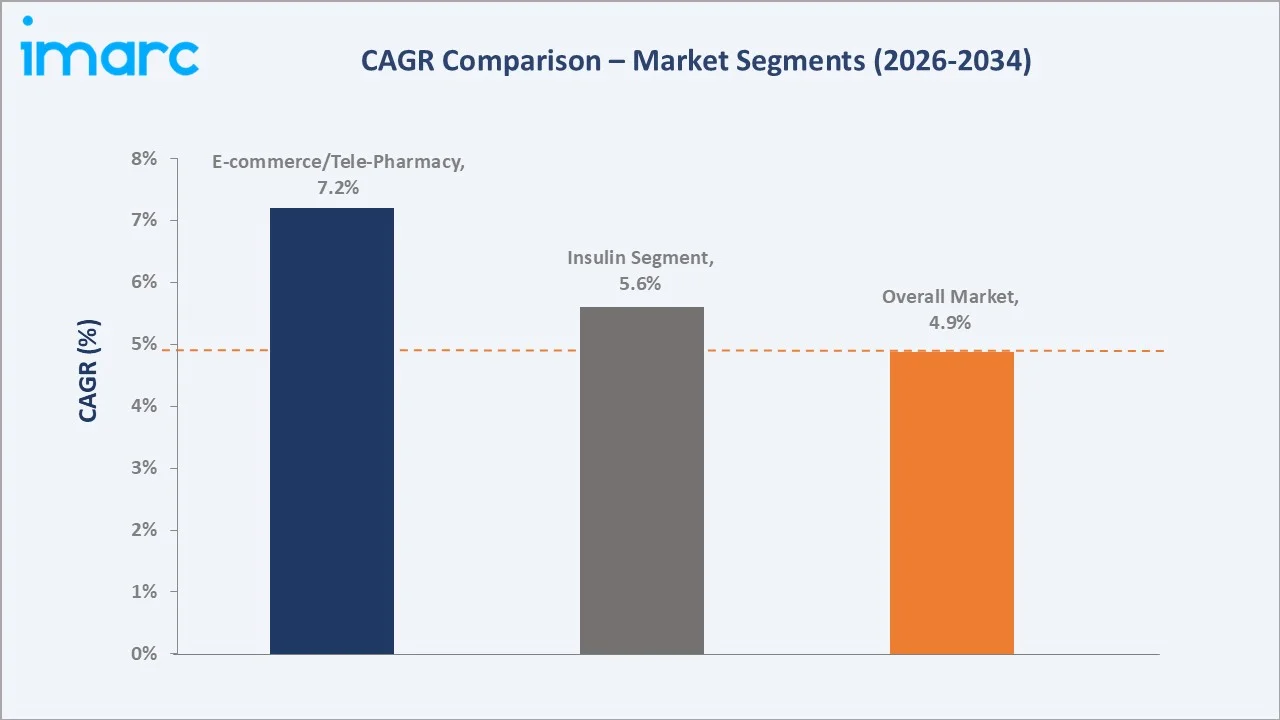

The CAGR across key segments with E-commerce/tele-pharmacy at ~7.2% CAGR grow fastest by distribution channel, and the insulin segment is growing at a 5.6% CAGR.

Executive Summary

The France diabetes market grew from USD 960.57 Million in 2020 to USD 1,218.38 Million in 2025, sustained by diabetes prevalence growth, premium drug class transitions, and universal reimbursement that ensures full cost coverage for France's over 4.1 million diabetic patients. France's diabetes market structural distinction lies in its universal coverage model: reimbursement for all diabetes drugs, devices, and monitoring consumables. This universal access framework creates France's most commercially accessible major European diabetes market, where new drug reimbursement decisions determine market access rather than patient affordability. By 2034, the market will reach USD 1,868.70 Million, driven by oral GLP-1 mainstream adoption, biosimilar insulin market maturation, and tele-pharmacy expansion.

Oral antidiabetics lead at 56.0%, encompassing metformin generics, DPP-4 inhibitors (sitagliptin, linagliptin, alogliptin), SGLT-2 inhibitors (empagliflozin Jardiance, dapagliflozin Farxiga, canagliflozin Invokana), and oral GLP-1 RA (semaglutide Rybelsus). Retail pharmacies dominate at 60.0%, while E-Commerce/Tele-Pharmacy at 19.0% is the fastest-growing channel at approximately 7.2% CAGR.

Key Market Insights

|

Insight |

Data |

|

Dominant Segment |

Oral Antidiabetics - 56.0% revenue share (2025) |

|

Leading Distribution Channel |

Retail Pharmacies - 60.0% revenue share (2025) |

Key Analytical Observations:

- Oral antidiabetics at 56.0% driven by premium SGLT-2/GLP-1 prescription growth: France's oral antidiabetic market majority reflects the structural average selling price premium of next-generation oral agents over generic metformin. A study by the NIH found that between 2013 and 2022, the percentage of patients buying at least one antidiabetic drug per month in France grew from 3.07% to 4.12%. Biguanides remained the top-selling antidiabetic drug, followed by sulfonylureas and insulin.

- Retail pharmacies at 60.0% sustained by ALD 8 prescription dispensing model: France's retail pharmacy channel dominance reflects the ALD 8 dispensing model requiring all diabetes prescriptions to be filled through ANSM-licensed pharmacies.

France Diabetes Market Overview

France's diabetes market encompasses antidiabetic pharmaceuticals (oral agents and injectable insulins and GLP-1 RAs), glucose monitoring devices (SMBG and CGM), insulin delivery systems (pens, pumps), and digital diabetes management platforms. The market serves approximately 4.1 million adult patients with known diabetes (2024). France's diabetes prevalence in the adult population reflects a decade-long upward trend driven by population ageing, obesity prevalence, and improving T2D diagnosis rates.

France's healthcare regulatory architecture fundamentally shapes the diabetes market: ANSM grants marketing authorisation through EMA's centralised procedure. This regulatory-driven market structure means price negotiation is the critical success factor for France diabetes market entry, rather than direct-to-patient marketing approaches used in out-of-pocket markets.

Market Dynamics

To evaluate market opportunities, Request Sample

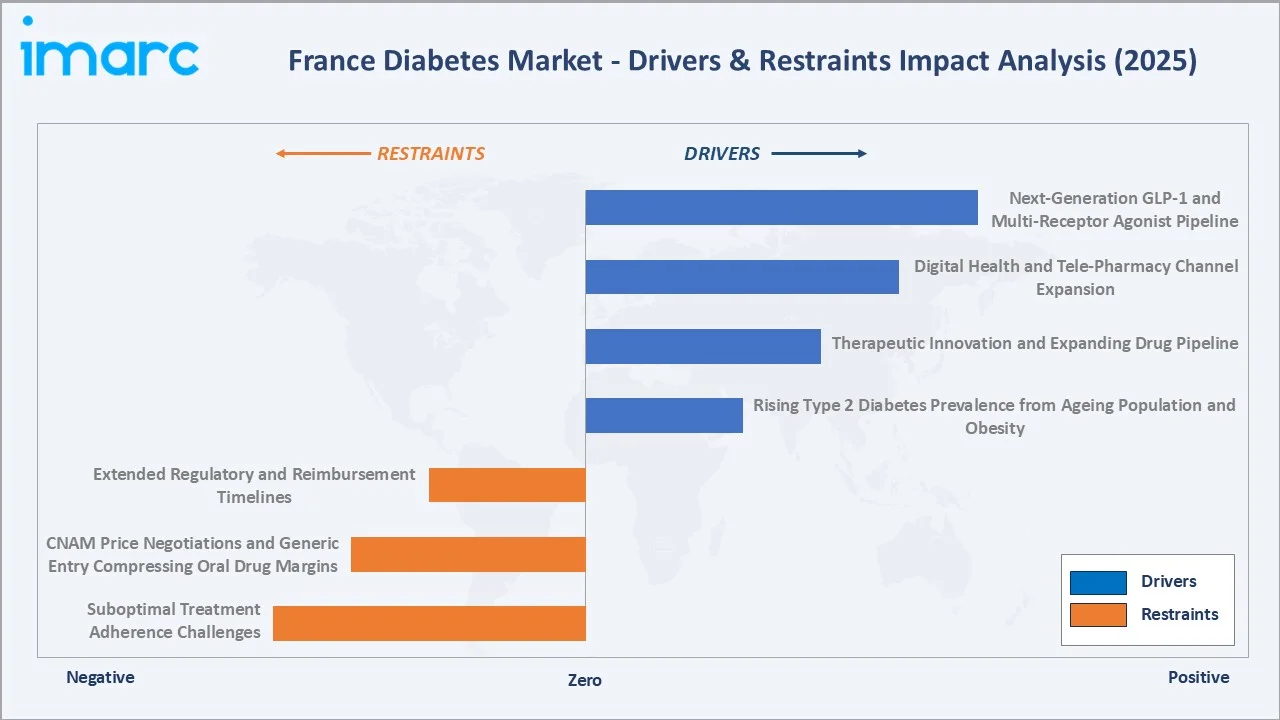

Market Drivers

- Rising Type 2 Diabetes Prevalence from Ageing Population and Obesity: France's T2D prevalence is 4.6% in the general population, with rates increasing substantially with age, rising the demand for the diabetes market in the region.

- Therapeutic Innovation and Expanding Drug Pipeline: The French diabetes market benefits from a robust pipeline of novel treatments. The rapid adoption of GLP-1 receptor agonists, SGLT-2 inhibitors, and dual-action incretin-based therapies such as tirzepatide (Mounjaro) is fundamentally altering the treatment paradigm, offering superior glycemic control alongside cardiovascular and renal protective benefits.

- Digital Health and Tele-Pharmacy Channel Expansion: In June 2024, Insulet Corporation launched Omnipod 5 Automated Insulin Delivery System (Omnipod 5) with Dexcom G6 compatibility. This rising digital health expansion further driving the growth of the market.

Market Restraints

- CNAM Price Negotiations and Generic Entry Compressing Oral Drug Margins: France's CEPS price negotiation framework imposes mandatory annual price reviews with automatic reduction triggers for drugs exceeding CNAM health technology assessment-adjusted volume thresholds.

- Suboptimal Treatment Adherence Challenges: Despite high-quality therapy options, patient adherence remains a persistent challenge. Gastrointestinal side effects associated with metformin and GLP-1 agonists, insulin injection burden, needle phobia, and treatment fatigue contribute to suboptimal medication compliance, limiting real-world effectiveness and the full potential demand realization of antidiabetic pharmaceutical products.

Market Opportunities

- Next-Generation GLP-1 and Multi-Receptor Agonist Pipeline: The development of once-weekly, once-monthly injectable formulations and oral GLP-1 receptor agonists presents a substantial expansion opportunity in France. Improved patient convenience profiles, reduced injection frequency, and combination with weight management indications broaden addressable patient segments beyond current GLP-1 prescribing, tapping into the large population with obesity-associated type 2 diabetes.

- GLP-1 RA for Obesity: Wegovy Market Entry and T2D Prevention: Wegovy launched in France in October 2024 will determine France's first pharmacological obesity treatment reimbursement, potentially adding high annual cardiometabolic drug market revenue.

Market Challenges

- Extended Regulatory and Reimbursement Timelines: The gap between EMA marketing authorization and French national reimbursement approval through the Haute Autorité de Santé (HAS) evaluation and CEPS pricing negotiation processes averages 12–18 months, delaying patient access to innovative therapies and creating revenue lag for pharmaceutical companies compared to markets with expedited health technology assessment pathways.

Emerging Market Trends

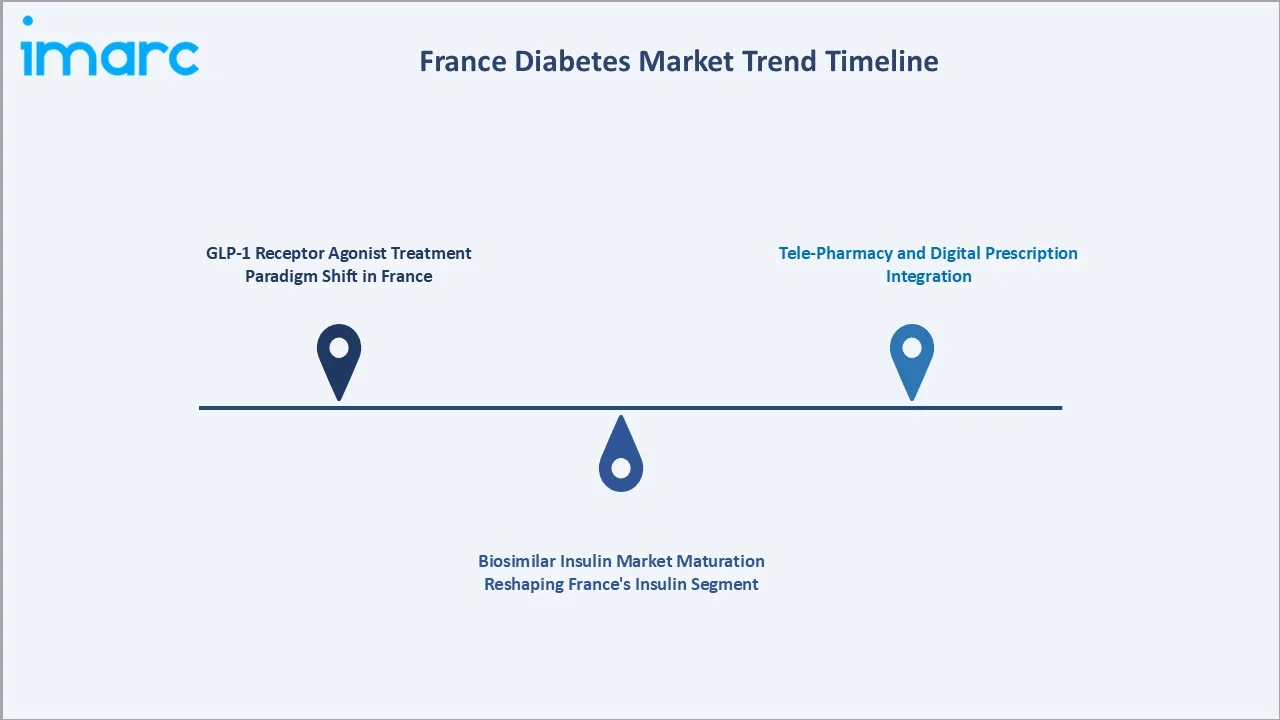

1. GLP-1 Receptor Agonist Treatment Paradigm Shift in France

France's GLP-1 RA market is experiencing its most transformative decade as Ozempic, Rybelsus, and Mounjaro collectively redefine France's T2D treatment algorithm from a glycaemia-first metformin escalation model to a cardiovascular risk and weight-first GLP-1/SGLT-2 combination model.

2. Biosimilar Insulin Market Maturation Reshaping France's Insulin Segment

France's biosimilar insulin market is completing its transition from originator-dominated to biosimilar-majority, collectively capturing price-sensitive prescriptions under CNAM's biosimilar substitution framework.

3. Tele-Pharmacy and Digital Prescription Integration

France's tele-pharmacy channel's 19.0% distribution share reflects three regulatory developments. For chronic disease management where patients require monthly or quarterly prescription renewal, the e-prescription-to-e-pharmacy workflow creates a frictionless reorder model for growth.

Industry Value Chain Analysis

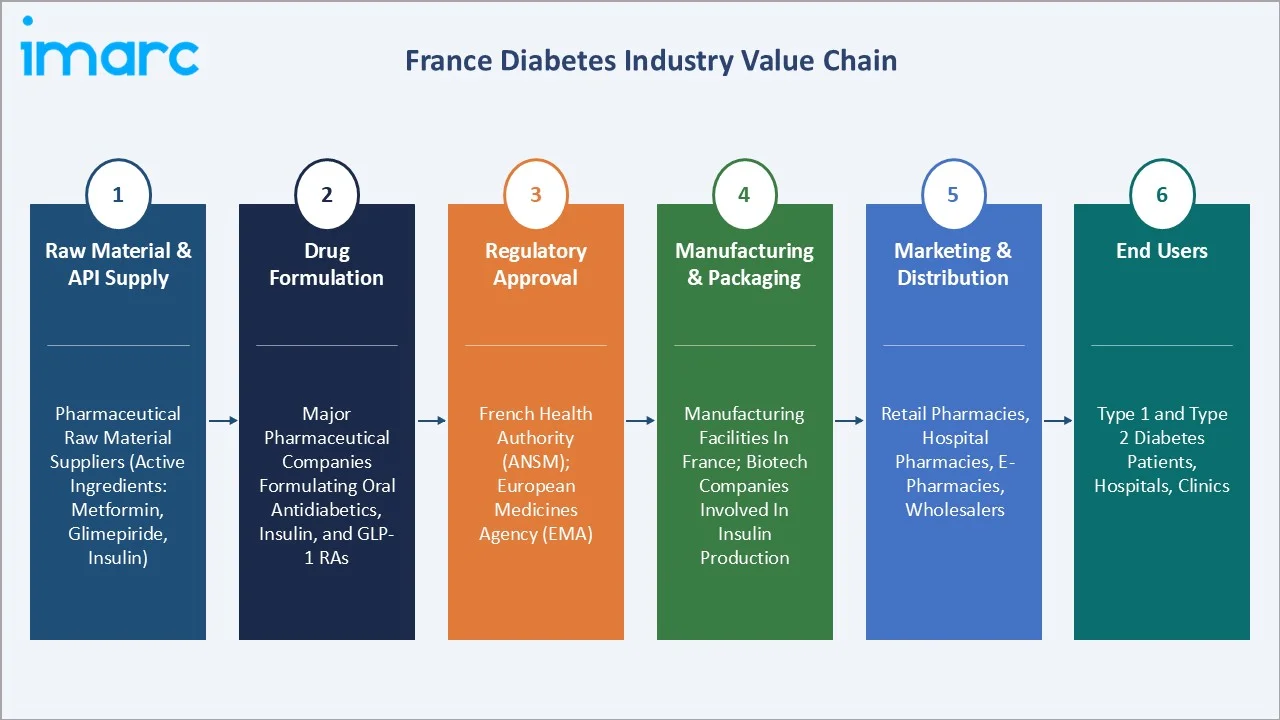

France diabetes value chain integrates raw material and API supply, drug formulation, regulatory approval process, manufacturing and packaging, marketing and distribution, and end-users.

|

Stage |

Key Participants |

|

Raw Material & API Supply |

Pharmaceutical raw material suppliers (e.g., active ingredients like metformin, glimepiride, insulin) |

|

Drug Formulation |

Major pharmaceutical companies formulating oral antidiabetics, insulin, and GLP-1 RAs |

|

Regulatory Approval |

French Health Authority (ANSM); European Medicines Agency (EMA) |

|

Manufacturing & Packaging |

Manufacturing facilities in France, biotech companies involved in insulin production |

|

Marketing & Distribution |

Distribution channels through pharmacies (both retail and hospital), e-pharmacies, wholesalers, etc. |

|

End Users |

Type 1 and Type 2 diabetes patients, hospitals, clinics, etc. |

The France diabetes market value chain raw material suppliers providing essential APIs like insulin, followed by pharmaceutical companies formulating and manufacturing diabetes drugs. These treatments are then approved by regulatory bodies (ANSM, EMA) and distributed to pharmacies, hospitals, and clinics through distributors. End users, including Type 1 and Type 2 diabetes patients, access these medications, often through public healthcare or e-pharmacies.

Technology Landscape in the France Diabetes Industry

Digital Health & Remote Monitoring Platforms

In March 2025, Hedia unveiled the start of a clinical study in France. The study will assess the effectiveness of its digital therapy, DTx Hedia Diabetes Assistant (HDA), in addressing suboptimal glycemic control in individuals with type 1 diabetes. France has rapidly adopted digital diabetes management tools such as connected glucometers, continuous glucose monitors (CGMs), and mobile health apps. Public and private healthcare systems are increasingly using telemedicine and remote monitoring to support patient self‑management and reduce hospital visits.

Advanced Therapeutics and Biologics Innovation

France’s strong biotech ecosystem drives the development of next‑generation insulin analogs, GLP‑1 receptor agonists, and cell‑based therapies. Regulatory and funding support from ANSM and Inserm accelerates clinical research and commercialization of innovative diabetes treatments.

Data Integration & AI‑Driven Decision Support

Healthcare data infrastructure in France is evolving with national initiatives like the Dossier Médical Partagé (DMP), enabling secure patient data sharing across hospitals and clinics. AI and predictive analytics are increasingly applied for risk stratification, personalized treatment plans, and early detection of complications, supported by collaborations between hospitals and tech partners.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Segment | Oral Antidiabetics | 56.0% | 2025 |

| Distribution Channel | Retail Pharmacies | 60.0% | 2025 |

By Segment

Oral antidiabetics dominate the France diabetes market with a 56.0% revenue share in 2025, reflecting their status as the cornerstone of first-line type 2 diabetes management across France. Metformin remains the most prescribed agent, with DPP-4 inhibitors (sitagliptin, vildagliptin), SGLT-2 inhibitors (dapagliflozin, empagliflozin), and sulfonylureas collectively constituting the second-line prescribing portfolio.

To access detailed market analysis, Request Sample

Insulin holds a 44.0% market share, driven by the essential therapeutic requirement for type 1 diabetes patients and advanced type 2 patients requiring insulin intensification. Long-acting insulin analogues (insulin glargine, insulin degludec) represent the premium segment, while biosimilar insulin glargine formulations are progressively capturing volume in cost-sensitive treatment settings. The introduction of once-weekly basal insulin formulations in late clinical development stages is expected to further elevate the insulin segment's appeal by substantially reducing injection burden.

By Distribution Channel

Retail pharmacies lead distribution with a 60.0% share in 2025, underpinned by France's extensive network of community pharmacies that function as primary points of diabetes medication dispensing and patient counseling. Pharmacists under French health law are recognized contributors to chronic disease management, conducting medication reviews, adherence support, and glucose monitoring education, creating a structurally entrenched role in the diabetes care pathway.

Hospital pharmacies account for 21.0% of distribution, serving patients requiring specialist-initiated insulin therapies, newly diagnosed type 1 patients, and complex type 2 cases managed by hospital-based diabetology units. E-Commerce and Tele-Pharmacy represent a fast-growing 19.0% share, driven by the post-COVID acceleration of digital health adoption, the expansion of reimbursed telemedicine consultations, and the convenience premium associated with home delivery of long-term chronic disease medications.

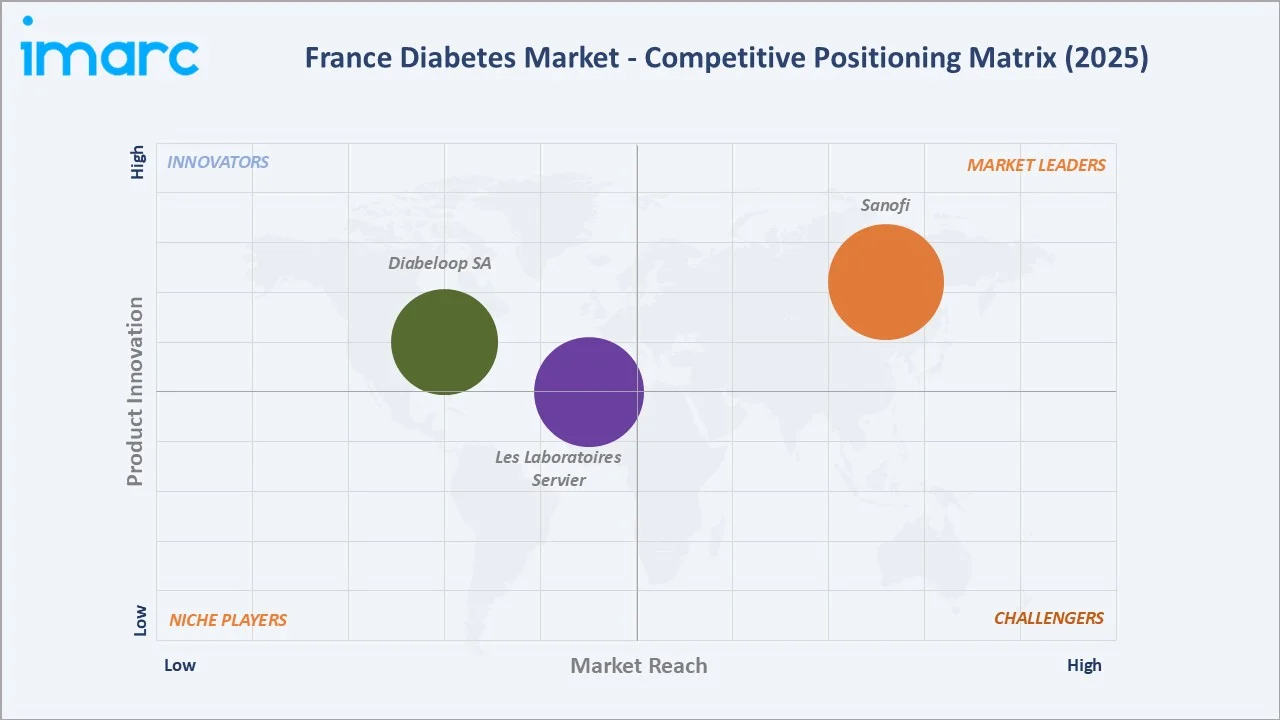

Competitive Landscape

France's diabetes market exhibits a two-tier competitive structure: the pharmaceutical drug tier and the diabetes device and digital health tier. France's diabetes market is highly competitive, dominated by established multinational pharmaceutical companies with diversified antidiabetic portfolios, subject to increasing competitive pressure from biosimilar insulin manufacturers and generic oral antidiabetic producers.

|

Company Name |

Brand / Product Line |

Market Position |

Core Strength |

|

Sanofi |

Toujeo, Lantus, Soliqua, Admelog, Amaryl |

Market Leader |

Sanofi is France largest domestic pharmaceutical company and historical leader of the diabetes market. |

|

Les Laboratoires Servier |

Diamicron |

Established |

France-based pharma with deep domestic prescriber relationships |

|

Diabeloop SA |

DBLG1 |

Established |

As of May 2025, Diabeloop has equipped more than 11,000 patients in Europe with DBLG1, showcasing an algorithm that is both clinically and commercially validated and integrated into four different insulin pumps. |

The top three originators, Sanofi, Les Laboratoires Servier, and Diabeloop, collectively command the majority of branded market revenue. Key competitive strategies encompass novel formulation development, fixed-dose combination products, digital health platform integration, and real-world evidence generation to support reimbursement dossiers.

Key Company Profiles

Sanofi

Sanofi is France's largest pharmaceutical company and the historical market leader in diabetes care, with a comprehensive portfolio spanning long-acting insulins, rapid-acting formulations, and the first disease-modifying type 1 diabetes therapy approved in Europe.

- Product Portfolio: Lantus (insulin glargine originator), Toujeo (high-concentration glargine U300), Admelog, Soliqua, Amaryl.

- Recent Developments: In May 2024, Sanofi announced an investment exceeding €1 billion to expand bioproduction capacity at its sites in Vitry-sur-Seine, Le Trait, and Lyon Gerland. In Lyon Gerland, €10 million will be dedicated to producing Teizeild, a biologic for type 1 diabetes acquired by Sanofi in April 2023.

- Strategic Focus: Toujeo brand loyalty defence through pharmacist education programme targeting France T1D/T2D patients clinically indicated for U300 glargine hypoglycaemia reduction advantage.

Diabeloop SA

Diabeloop is a leading French healthtech company focused on improving diabetes management through innovative digital health solutions. Their flagship product, DBLG1, is an advanced diabetes management system integrating algorithms with insulin pumps to deliver optimal glycemic control.

- Product Portfolio: DBLG1 (Automated Insulin Delivery System).

- Recent Developments: As of May 2025, Diabeloop has equipped more than 11,000 patients in Europe with DBLG1, showcasing an algorithm that is both clinically and commercially validated. DBLG1 has been integrated into four different insulin pumps, further improving the company's market standing in diabetes care.

- Strategic Focus: Focuses on developing cutting-edge diabetes management systems, leveraging AI and machine learning for more personalized and automated care solutions.

Market Concentration Analysis

France's diabetes pharmaceutical market exhibits moderate-to-high concentration among the top three originator manufacturers: Sanofi, Servier, and Diabeloop collectively account for approximately 65–70% of total branded diabetes market revenue in France. However, market concentration dynamics are being disrupted by the progressive entry of biosimilar insulin and generic oral antidiabetic manufacturers, which are capturing volume share in the metformin, sulfonylurea, and insulin glargine segments through mandatory generic substitution policies.

Three structural forces sustain the innovator concentration: GLP-1 receptor agonist and SGLT-2 inhibitor classes remain under patent protection, commanding price premiums unavailable to generic manufacturers; the clinical evidence requirements for new reimbursement applications under HAS assessment favor established companies with clinical trial infrastructure; and France's disease-modifying therapy segment is category-exclusively held by Sanofi, representing a structurally protected revenue stream for the forecast horizon.

Investment & Growth Opportunities

Fastest Growing Segments

- E-Commerce/Tele-Pharmacy channel: Projected to grow at the fastest rate among distribution channels, driven by post-COVID digital health adoption, regulatory enabling of remote prescription fulfillment, and patient convenience preferences for chronic medication home delivery.

- GLP-1 receptor agonist class within oral antidiabetics: Oral semaglutide (Rybelsus) and the developmental oral tirzepatide represent the highest-growth sub-segment within the oral antidiabetic category, targeting the large pool of injection-averse type 2 patients.

Emerging Technology and Policy Opportunities

Diabeloop's DBLG2 system and equivalent platforms represent the convergence of pharmaceutical and digital therapeutic value, supported by France's national digital health strategy. The growing volume of insulin glargine biosimilar demand under France's mandatory substitution framework presents manufacturing scale investment opportunities for cost-competitive producers. France's expanding DTx (Digital Therapeutics) reimbursement framework under the digital health innovation pathway creates first-mover advantages for diabetes management application developers.

Investment Themes

Investment in the France diabetes market is focused on advancing digital health technologies, including AI-driven algorithms and integrated insulin pumps, to enhance glycemic control and patient outcomes. Additionally, there is growing emphasis on expanding biopharmaceutical capabilities, especially in biologics like Tzield for type 1 diabetes, alongside efforts to strengthen production capacities for advanced diabetes treatments.

Future Market Outlook (2026-2034)

The France diabetes market is positioned for its most therapeutically transformative and commercially consequential decade since insulin's discovery. From USD 1,218.38 Million in 2025, the market will reach USD 1,868.70 Million by 2034 at a sustained 4.87% CAGR, a growth rate that is structurally reliable given France's universal reimbursement model and the epidemiological certainty of France's ageing, increasingly obese population generating new T2D diagnoses.

Three transformative forces define the forecast period: the GLP-1 RA treatment paradigm's maturation from specialist-initiated injectable to GP-prescribed oral, the completion of France's CGM transition from SMBG that will peak by 2027-2028 as CGM penetration approaches 90%+ in insulin-treated populations, and the biosimilar insulin market's stabilisation as originator premium positioning for specialty insulins creates a two-tier insulin market between biosimilar commodity and branded specialty.

Research Methodology

Primary Research

Primary research included structured interviews with France diabetes market stakeholders, comprising hospital-based diabetologists and endocrinologists from CHU Paris, Lyon, and Marseille, community pharmacists across urban and rural regions, patient advocacy representatives from Fdration Franaise des Diabtiques, pharmaceutical medical affairs executives, and healthcare economists specializing in French reimbursement policy analysis.

Secondary Research

Secondary research encompassed Assurance Maladie prescription database, Haute Autorité de Santé medical service rating assessments, CEPS pharmaceutical pricing negotiation records, European Medicines Agency product information and CHMP opinions, IMS Health/IQVIA France pharmaceutical sales data, Diabète France epidemiological surveillance reports, INSEE demographic projections, annual reports of listed diabetes pharmaceutical companies, and IMARC's global healthcare intelligence database. Over 100 secondary sources were reviewed.

Forecasting Models

IMARC's Bottom-Up and Top-Down dual estimation methodology was applied. The Bottom-Up approach aggregates France diabetes market demand by segment and distribution channel, weighted by therapy class penetration rates, reimbursement timeline modeling, and generic substitution progression curves. The Top-Down approach validates against France's overall pharmaceutical market, European diabetes market benchmarks, and epidemiological patient population projections.

France Diabetes Market Report Coverage

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Segments Covered | Oral Antidiabetics, Insulin |

| Distribution Channels Covered | E-commerce and Tele-pharmacy, Hospital Pharmacies, Retail Pharmacies |

| Companies Covered | Sanofi, Les Laboratoires Servier, Diabeloop SA, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the France Diabetes Market Report

The France diabetes market was valued at USD 1,218.38 Million in 2025 and is projected to reach USD 1,868.70 Million by 2034.

The France diabetes market is forecast to grow at a CAGR of 4.87% during 2026-2034, driven by Type 2 diabetes prevalence growth, SGLT-2 inhibitor and GLP-1 RA premium adoption, universal reimbursement, and tele-pharmacy channel expansion.

Oral antidiabetics lead with 56.0% revenue share (2025), driven by premium SGLT-2 inhibitor and GLP-1 RA prescription growth and average selling price uplift over generic metformin and DPP-4 inhibitor categories.

Retail pharmacies lead with 60.0% share (2025), sustained by France's dispensing model requiring pharmacy prescription fulfilment, licensed pharmacies, and CNAM's Entretien Pharmaceutique Diabete reimbursed pharmacist consultation programme.

Key companies include Sanofi, Les Laboratoires Servier, and Diabeloop SA, among others.

Key drivers include rising type 2 diabetes prevalence from aging demographics and lifestyle factors, therapeutic innovation in GLP-1 receptor agonists and dual-action incretin therapies, comprehensive ALD reimbursement coverage, and the expansion of digital health and continuous glucose monitoring into standard care pathways.

Key trends include GLP-1 RA paradigm shift, biosimilar insulin market maturation and suboptimal treatment adherence challenges.

Key challenges include CEPS mandatory price negotiation, reducing SGLT-2 and GLP-1 ex-manufacturer margins 15-25% post-reimbursement, biosimilar insulin CNAM substitution, and Ozempic supply shortage restricting eligible patient treatment initiations.

Top opportunities include listed equity in Sanofi, tele-pharmacy platform investment, CGM sensor supply chain, oral GLP-1 RA pipeline investment, and AID system investment in Diabeloop DBLG1 expansion.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade