Gas Detection Equipment Market Size, Share, Trends and Forecast by Technology, Detection Type, End Use Industry, and Region, 2026-2034

Global Gas Detection Equipment Market Size, Share, Trends & Forecast (2026-2034)

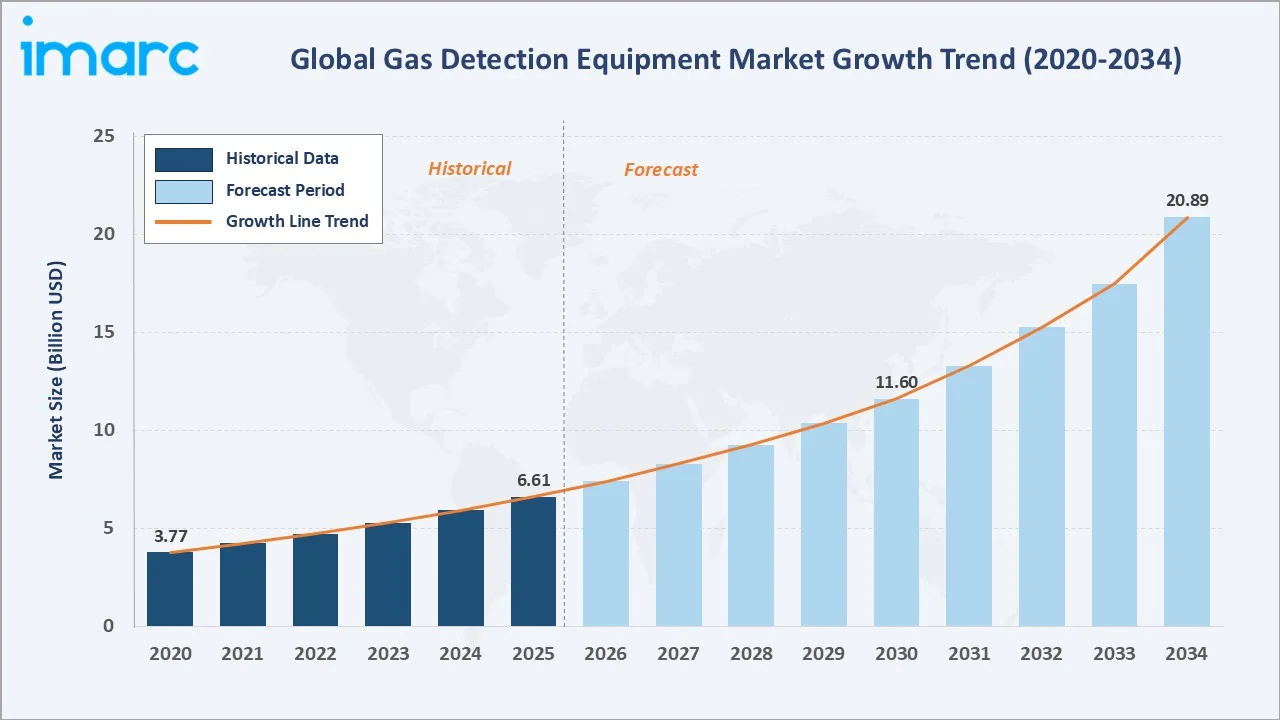

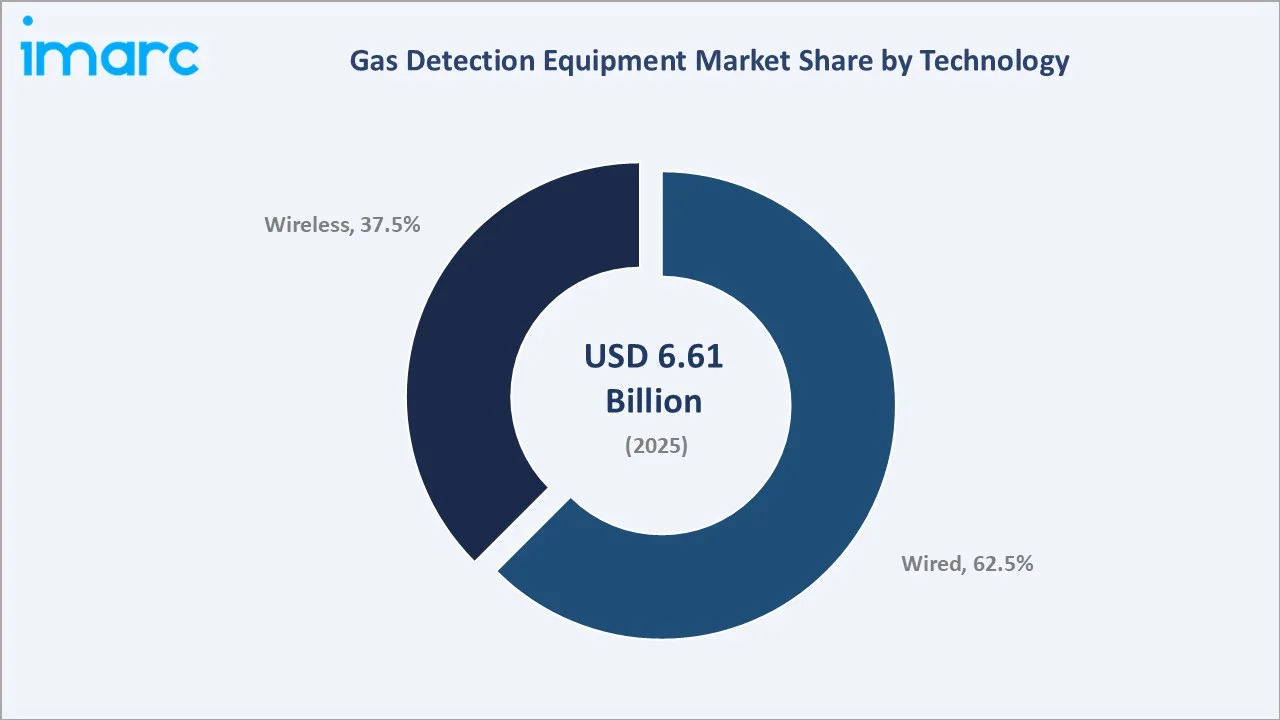

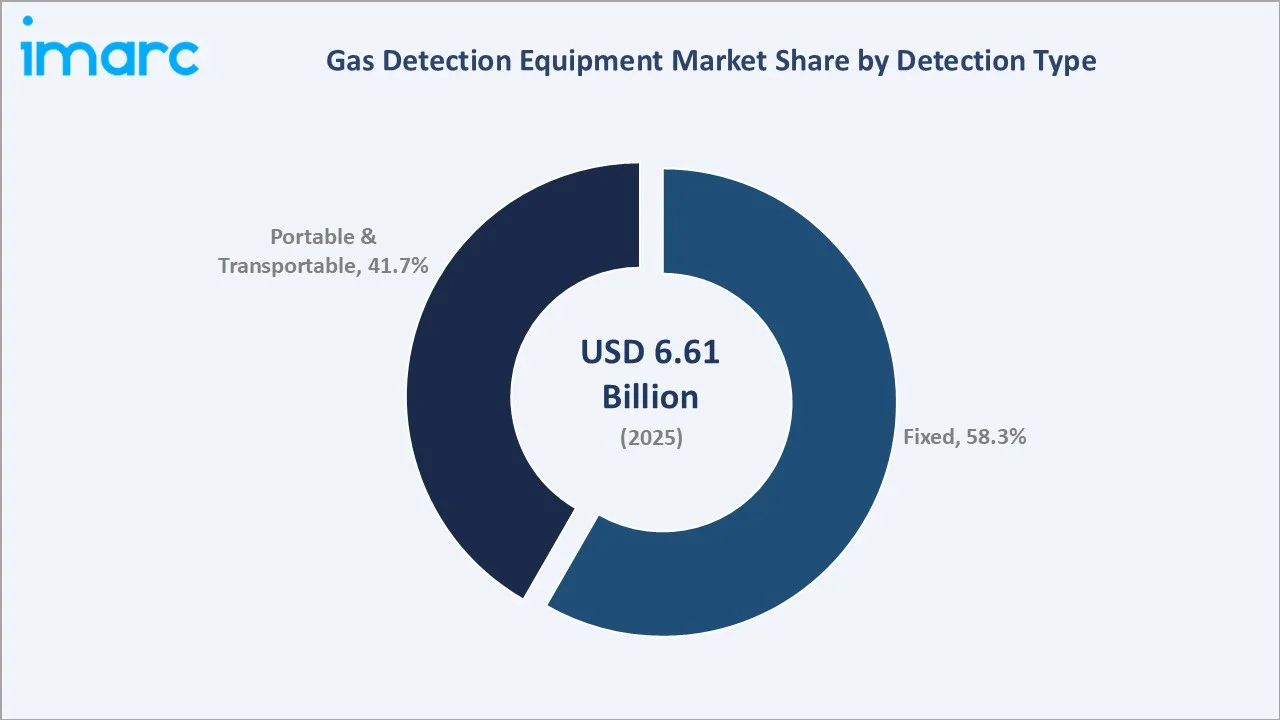

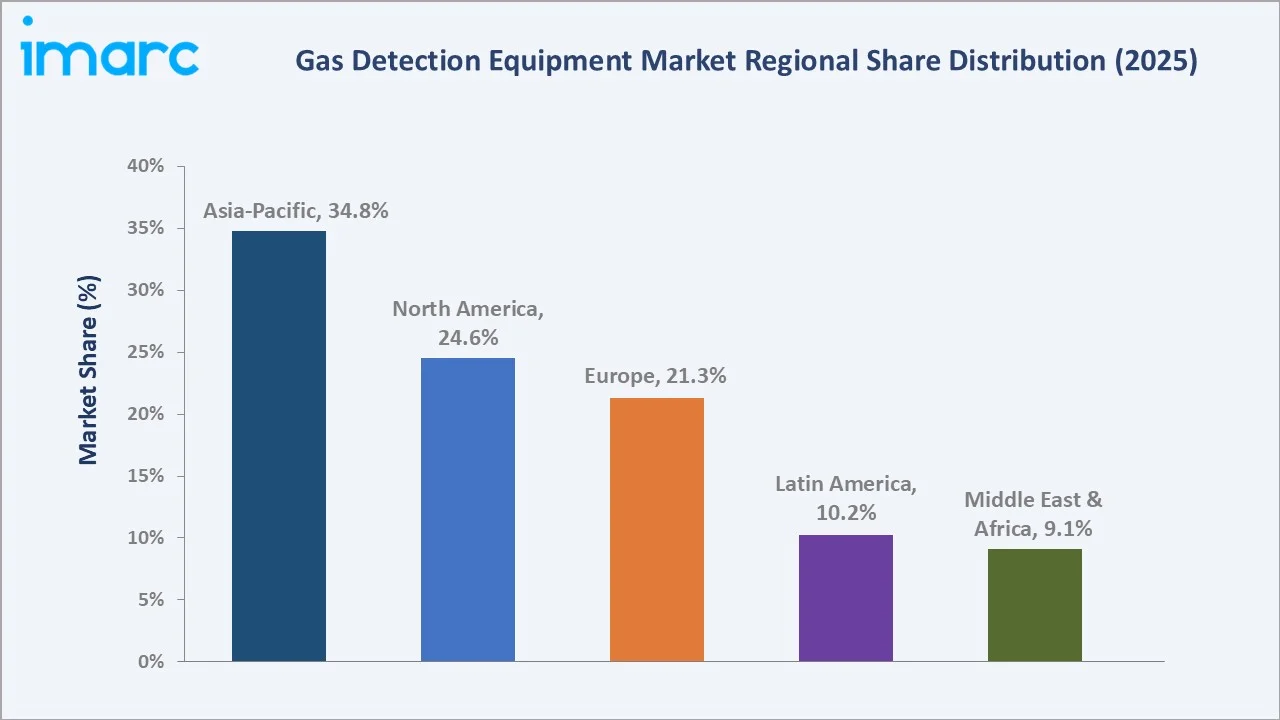

The global gas detection equipment market size was valued at USD 6.61 Billion in 2025 and is projected to reach USD 20.89 Billion by 2034, at a CAGR of 11.90% during 2026-2034. Rising occupational safety regulations, expanding oil and gas capex, accelerating adoption of wireless and IoT-enabled sensors, and growing industrial automation are collectively driving gas detection equipment market growth. Wired technology dominates with a 62.5% share in 2025, while Fixed detectors account for 58.3% of the global market. Asia-Pacific leads regional demand with a 34.8% share in 2025, supported by rapid industrialization across China, India, and Southeast Asia.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 6.61 Billion |

|

Forecast Market Size (2034) |

USD 20.89 Billion |

|

CAGR (2026-2034) |

11.90% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Asia-Pacific (34.8% share, 2025) |

|

Fastest Growing Region |

Asia-Pacific |

|

Leading Technology |

Wired (62.5%, 2025) |

|

Leading Detection Type |

Fixed (58.3%, 2025) |

The chart shows gas detection equipment market growth from 2020–2034, with historical momentum driven by post-pandemic safety investment and forecast expansion supported by Asia-Pacific industrialization and hydrogen-economy build-out.

To get more information on this market, Request Sample

CAGR analysis identifies wireless technology and portable detectors as the fastest-growing segments, with Asia-Pacific leading regional growth through 2034.

Executive Summary

The global gas detection equipment market is being reshaped by tightening industrial safety regulations, expanding energy-sector capex, and the convergence of wireless sensing with IoT platforms. Valued at USD 6.61 Billion in 2025, the market is projected to reach USD 20.89 Billion by 2034 at an 11.90% CAGR. Hazardous-gas exposure across oil and gas, chemicals, mining, and utilities remains the central demand driver.

Wired systems lead with a 62.5% share in 2025, supported by reliability requirements in fixed industrial assets. Fixed detectors hold 58.3% of the market, while portable units are gaining traction in confined-space entry, emergency response, and mobile operations. Key trends include IoT-connected detectors, multi-gas handheld devices, hydrogen-specific sensors, and AI-driven predictive alerts replacing reactive alarm logic.

Asia-Pacific commands a 34.8% share in 2025, anchored by China, India, and Southeast Asia's industrial build-out. North America holds 24.6%, supported by shale operations, LNG expansion, and OSHA enforcement. Europe accounts for 21.3%, driven by ATEX compliance across chemical clusters and accelerating hydrogen-hub investment.

Key Market Insights

|

Insight |

Data |

|

Largest Technology Segment |

Wired – 62.5% share (2025) |

|

Second Technology Segment |

Wireless – 37.5% share (2025) |

|

Leading Detection Type |

Fixed – 58.3% share (2025) |

|

Leading Region |

Asia-Pacific – 34.8% revenue share (2025) |

|

Second Region |

North America – 24.6% revenue share (2025) |

|

Top Companies |

Honeywell International Inc., MSA, Drägerwerk AG & Co. KGaA, Teledyne, Gas and Flame Detection, Industrial Scientific, Thermo Fisher Scientific Inc. |

Key Analytical Observations Supporting the Above Data:

- Wired technology's 62.5% dominance in 2025 reflects its reliability advantage in permanent installations where uninterrupted power, hardwired signal paths, and hazardous-area Zone 0/Zone 1 certification are non-negotiable.

- Wireless detection at 37.5% in 2025 is the fastest-growing technology, expanding at an estimated 14.1% CAGR through 2034 as IoT platforms, LoRaWAN networks, and battery improvements mature.

- Fixed detectors at 58.3% serve large refineries, petrochemical sites, LNG terminals, and utility plants where continuous zone coverage and SCADA integration are mandatory operational requirements.

- Asia-Pacific's 34.8% lead reflects accelerated industrial investment across China and India, where new chemical parks, refineries, and mining expansions demand large-scale detection installations.

- Oil and gas remains a leading end-use vertical, driven by increased investment in fugitive-emission monitoring and stricter methane regulations, though specific market share estimates are not consistently disclosed.

Global Gas Detection Equipment Market Overview

Gas detection equipment comprises sensors, alarms, and monitoring systems that identify the presence of toxic, combustible, or oxygen-deficient atmospheres in industrial and commercial settings. The ecosystem includes sensor suppliers, electronic component makers, OEM manufacturers, system integrators, IoT platform providers, and certification frameworks such as ATEX, IECEx, and UL for use in hazardous environments.

Applications span oil and gas platforms, petrochemical facilities, water treatment plants, mining sites, power generation, and laboratory environments. Macroeconomic tailwinds include rising clean-energy and hydrogen infrastructure capex, post-pandemic focus on occupational health, tighter air-quality standards, and rapid adoption of connected sensor networks for real-time risk monitoring across distributed operations.

Market Dynamics

To evaluate market opportunities, Request Sample

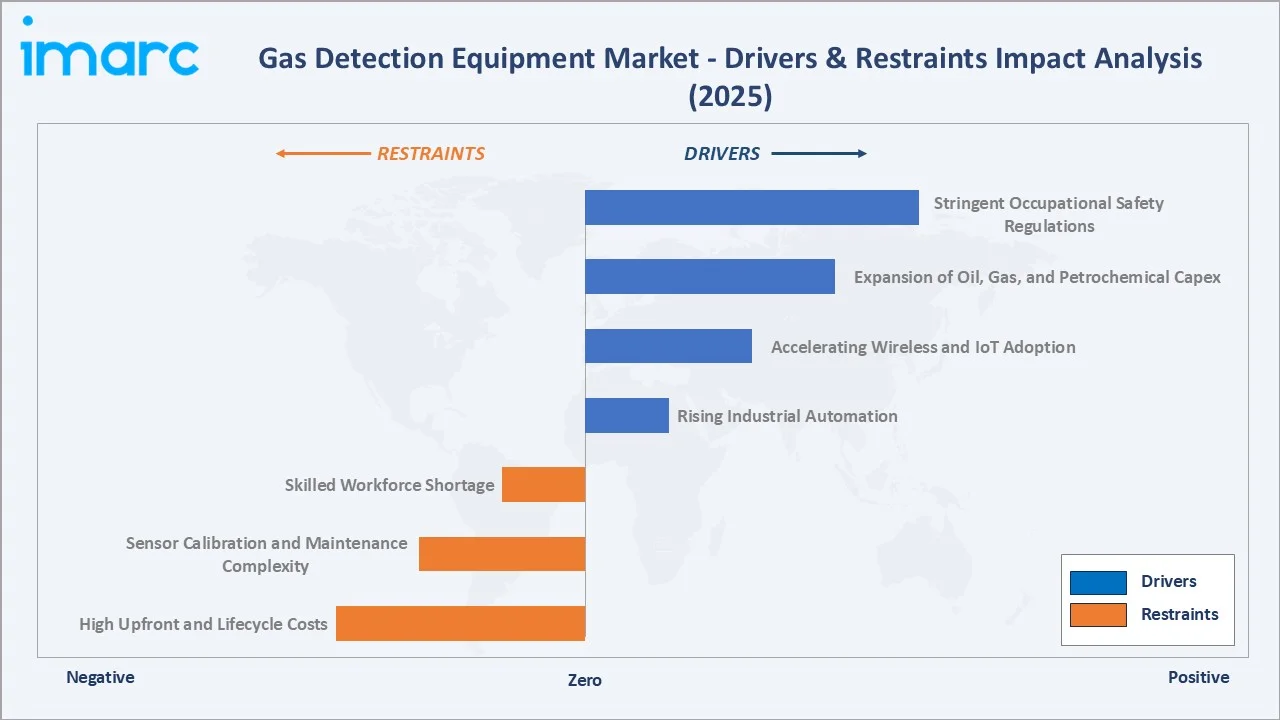

Market Drivers

- Stringent Occupational Safety Regulations: Regulatory bodies such as OSHA, ATEX, and IECEx mandate gas monitoring in hazardous workplaces. Carbon monoxide incidents remain a major risk, driving compliance-based adoption of gas detection systems.

- Expansion of Oil, Gas, and Petrochemical Capex: Rising investments in upstream exploration, LNG infrastructure, and petrochemicals across regions like the U.S., Middle East, and China are increasing demand for gas detection systems. Global oil and gas capital expenditure has shown steady growth, supporting wider deployment of safety equipment.

- Accelerating Wireless and IoT Adoption: Wireless gas detection with IoT connectivity enables real-time monitoring, remote diagnostics, and predictive maintenance, reducing unplanned downtime and improving safety response times across large industrial estates.

- Rising Industrial Automation: Growing adoption of industrial automation integrates gas detection with SCADA and DCS platforms, enabling centralized monitoring and analytics. This increases system value, enhances safety compliance, and drives demand for advanced, connected detection solutions.

Market Restraints

- High Upfront and Lifecycle Costs: Fixed detection systems with hazardous-area certification, redundant wiring, and calibration infrastructure carry significant installation costs, limiting adoption among small and mid-sized industrial operators in emerging markets.

- Sensor Calibration and Maintenance Complexity: Electrochemical and catalytic bead sensors require frequent calibration and periodic replacement, creating operating-expense headwinds and specialized technician requirements that constrain adoption in cost-sensitive verticals.

- Skilled Workforce Shortage: Installation, calibration, and compliance verification require trained safety engineers. Shortages across North America, Europe, and Asia are extending project timelines and slowing deployment at peak industrial-capex phases.

Market Opportunities

- Hydrogen Economy and Clean Energy Build-Out: Growth in hydrogen production, storage, and transport is creating demand for advanced leak detection systems. Large-scale global investments in clean hydrogen projects are expanding opportunities for specialized gas detection technologies.

- Emerging Market Industrialization: Rapid industrial expansion in countries such as India, Indonesia, Vietnam, and Saudi Arabia is increasing demand for gas detection across refining, petrochemical, and mining sectors, creating strong growth opportunities in developing economies.

- Smart City and Environmental Monitoring: Urban air-quality networks, indoor air-quality regulations, and building-level gas monitoring are opening new non-industrial revenue streams for miniaturized, consumer-grade, and semi-portable detectors.

Market Challenges

- Supply Chain Dependency on Sensor Components: Global semiconductor shortages and disruptions in sensor supply chains during 2021–2023 increased lead times and component costs for gas detectors, exposing manufacturers to procurement risks and production delays.

- Fragmented Regional Certification Requirements: Compliance with standards such as ATEX, IECEx, CSA Group, and UL requires multiple certifications, increasing testing costs, design complexity, and time-to-market for global manufacturers.

- Commoditization Pressure in Portable Devices: Low-cost Chinese and regional manufacturers are intensifying price competition in portable single-gas detectors, compressing margins for mid-tier global vendors and accelerating consolidation.

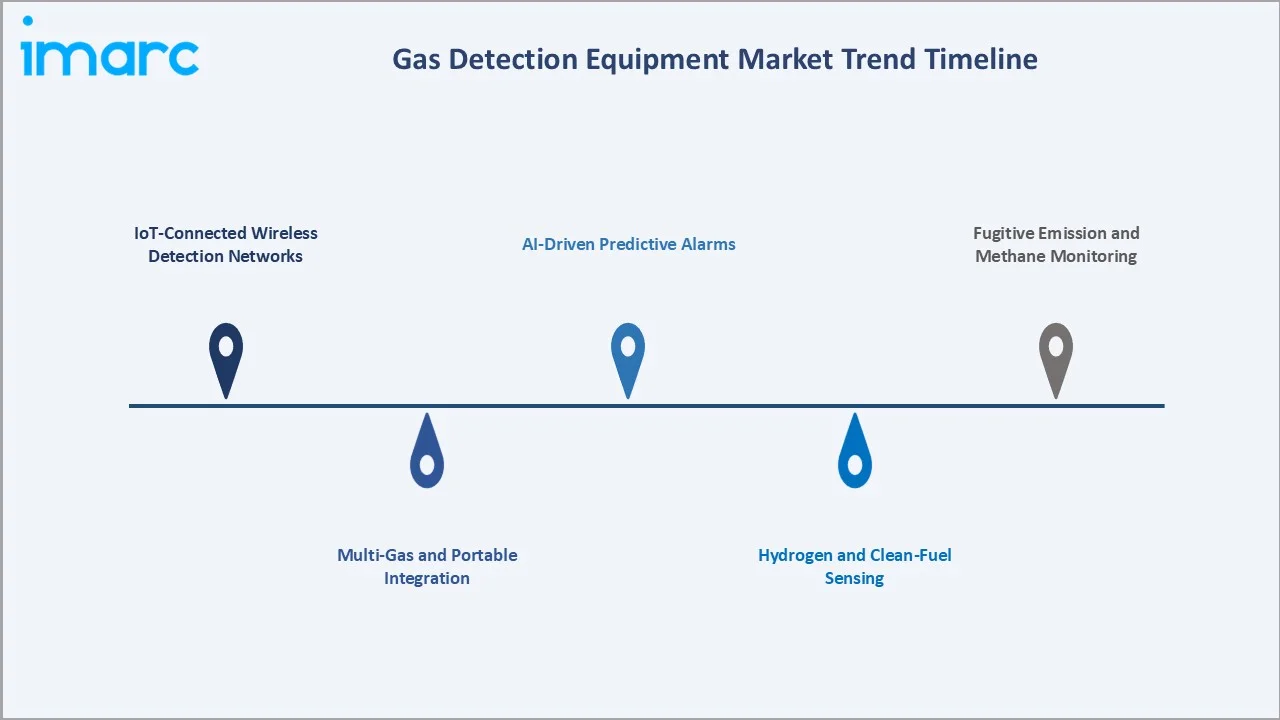

Emerging Market Trends

1. IoT-Connected Wireless Detection Networks

Wireless gas detection integrated with cloud platforms enables real-time monitoring, predictive maintenance, and centralized safety management. Companies like Honeywell, Dräger, and Industrial Scientific are expanding connected worker solutions.

2. Multi-Gas and Portable Integration

Portable multi-gas detectors measuring LEL, oxygen, carbon monoxide, hydrogen sulfide, and VOCs are increasingly standard for confined-space safety, improving worker mobility and ensuring compliance across industrial and hazardous environments.

3. Hydrogen and Clean-Fuel Sensing

Dedicated hydrogen sensors with ppm-level sensitivity are gaining traction as green-hydrogen hubs come online in the EU, U.S., and Middle East, opening a new product category adjacent to traditional hydrocarbon detection.

4. AI-Driven Predictive Alarms

AI and machine-learning technologies are being integrated into gas detection systems to improve alarm accuracy, detect leak patterns, and enable predictive maintenance, enhancing safety and operational efficiency in industrial facilities.

5. Fugitive Emission and Methane Monitoring

Stricter methane and VOC regulations, including standards from the U.S. Environmental Protection Agency, are driving adoption of continuous emission monitoring systems across oil and gas, landfill, and petrochemical industries.

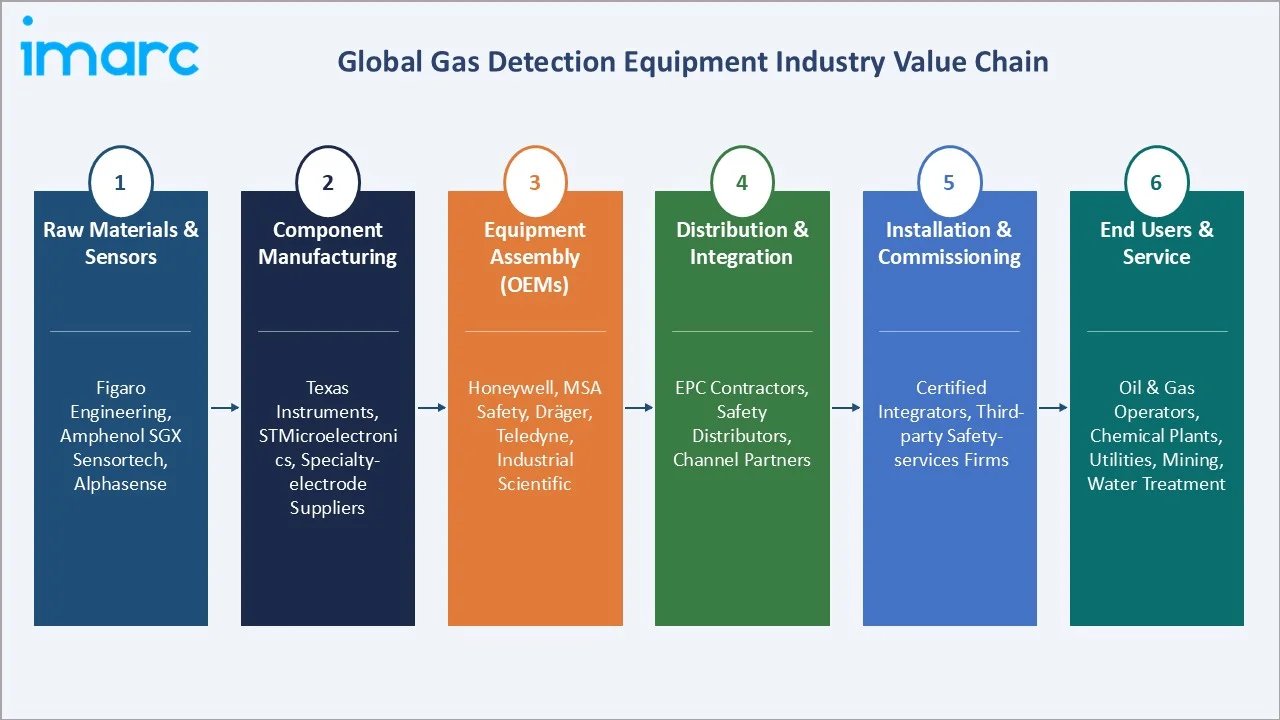

Industry Value Chain Analysis

The gas detection equipment value chain covers six stages, from raw sensor materials to end-consumer service, each involving distinct competitive dynamics, margin structures, and technological complexities.

|

Stage |

Key Players / Examples |

|

Raw Materials & Sensors |

Figaro Engineering, Amphenol SGX Sensortech, Alphasense |

|

Component Manufacturing |

Texas Instruments, STMicroelectronics, specialty-electrode suppliers |

|

Equipment Assembly (OEMs) |

Honeywell, MSA Safety, Dräger, Teledyne, Industrial Scientific |

|

Distribution & Integration |

EPC contractors, safety distributors, channel partners |

|

Installation & Commissioning |

Certified integrators, third-party safety-services firms |

|

End Users & Service |

Oil & gas operators, chemical plants, utilities, mining, water treatment |

Tier-1 OEMs like Honeywell and MSA Safety capture the most value by integrating sensors, electronics, and software. Their scale supports in-house sensor R&D, certification depth, and global service networks unmatched by smaller competitors.

Technology Landscape in the Gas Detection Equipment Industry

Sensor Technologies

Electrochemical, catalytic bead, infrared, semiconductor, and photoionization sensors dominate gas detection. Infrared and laser-based technologies are increasingly used for methane and CO₂ monitoring, particularly in industrial and oil and gas applications.

Wireless Connectivity and IoT Integration

LoRaWAN, Wi-Fi, cellular, and mesh-network protocols now support real-time detector communication. Cloud dashboards from Honeywell Connected Plant, MSA +X Cellular, and Industrial Scientific iNet enable fleet-wide asset visibility and safety analytics.

Multi-Gas and Miniaturization

Advances in MEMS and nanomaterials enable compact multi-gas detectors with improved battery life. Modern portable devices can detect multiple gases simultaneously, enhancing efficiency and replacing single-gas monitoring instruments in industrial safety applications.

Automation and Predictive Analytics

Gas detection systems are increasingly integrated with industrial automation platforms like SCADA and DCS. Advanced analytics and AI improve alarm management, enable predictive maintenance, and enhance safety monitoring across large industrial facilities.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

| Technology | Wired | 62.5% |

2025 |

| Detection Type | Fixed | 58.3% |

2025 |

| End Use Industry | Oil and Gas |

🔒 |

2025 |

| Region | Asia-Pacific | 34.8% |

2025 |

By Technology

Wired detection equipment holds a 62.5% share in 2025, supported by its unmatched reliability in permanent installations, hardwired power and signal paths, and suitability for hazardous-area zone 0 and zone 1 environments. Large refineries, chemical complexes, and offshore platforms anchor demand for wired networks.

To access detailed market analysis, Request Sample

Wireless systems, with a 37.5% share in 2025, are the fastest-growing technology at an estimated 14.1% forecast CAGR through 2034. Ease of retrofit, mobile worker monitoring, and IoT-enabled fleet visibility are accelerating adoption across brownfield operators adding coverage without rewiring assets.

By Detection Type

Fixed detectors captured a 58.3% share in 2025, reflecting deployment across refineries, LNG terminals, semiconductor fabs, and water-treatment facilities where continuous zone coverage is mandatory. Fixed systems support central alarm panels, SCADA integration, and high-reliability hazardous-area classifications.

Portable and transportable detectors, holding 41.7% in 2025, represent the fastest-growing detection type at an estimated 13.2% CAGR, driven by confined-space entry, emergency response, and mobile maintenance workflows. Multi-gas portables with docking-station calibration are replacing single-gas units across safety fleets.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Asia-Pacific |

34.8% |

Industrial expansion across China, India, Indonesia; rising safety enforcement; regional OEM growth |

|

North America |

24.6% |

Shale and LNG investment, OSHA compliance, EPA methane-rule enforcement, high replacement rates |

|

Europe |

21.3% |

ATEX mandates, chemical cluster density in Germany, Benelux, France; hydrogen-hub investment |

|

Latin America |

10.2% |

Brazil pre-salt offshore, Mexico petrochemical expansion, Argentina shale growth |

|

Middle East & Africa |

9.1% |

Saudi Aramco and ADNOC capex, Qatar LNG expansion, African mining and oilfield growth |

Asia-Pacific commands a 34.8% global share in 2025, supported by China’s extensive refining capacity, India’s expanding petrochemical sector, and advanced electronics manufacturing in Japan and South Korea. Strengthening industrial safety regulations, including China’s Work Safety Law and India’s Factories Act, are accelerating adoption and replacement of gas detection equipment.

North America, at 24.6% in 2025, benefits from a large installed base of gas detectors in oil and gas operations, supported by stringent methane-emission regulations enforced by the U.S. Environmental Protection Agency. Europe’s 21.3% share reflects strong ATEX and IECEx compliance across major chemical hubs, while the EU’s hydrogen strategy is fostering demand for advanced and specialized gas detection technologies.

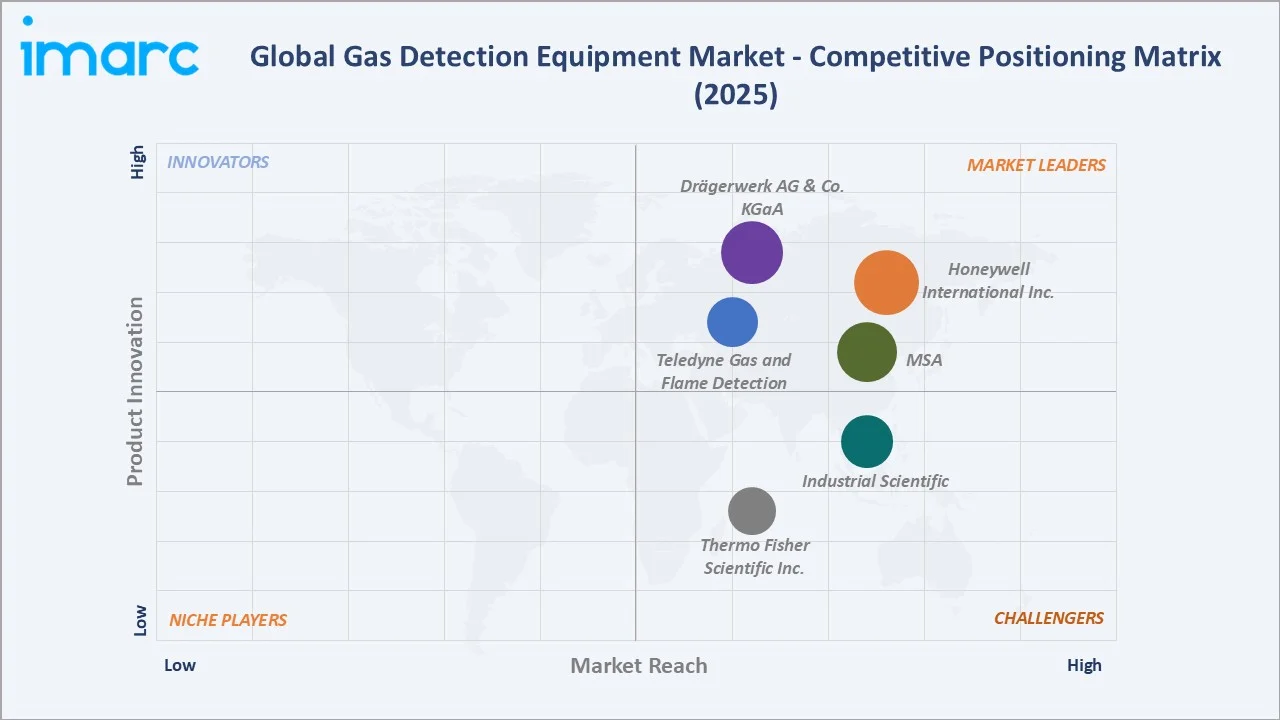

Competitive Landscape

|

Company Name |

Key Brand / Product Line |

Market Position |

Core Strength |

|

Honeywell International Inc. |

Honeywell BW / Searchline Excel |

Leader |

Broadest portfolio, global scale, Connected Plant IoT platform |

|

MSA |

ALTAIR/ General Monitors |

Leader |

Fixed & portable leadership, oil & gas, mining focus |

|

Drägerwerk AG & Co. KGaA |

Dräger Polytron / X-am |

Leader |

Premium European brand, medical-industrial crossover |

|

Teledyne Gas and Flame Detection |

Teledyne Oldham Simtronics |

Leader |

Industrial process safety, fixed detection systems |

|

Industrial Scientific |

Ventis / iNet |

Challenger |

Portable gas detection, cloud fleet management |

|

Thermo Fisher Scientific Inc. |

410iQ Carbon Dioxide Analyzer, TVA2020 Toxic Vapor Analyzer |

Challenger |

Laboratory and environmental monitoring |

The gas detection equipment market is led by a small number of global operators alongside fragmented regional specialists. Honeywell International reported USD 38.5 Billion in total 2024 revenue, with its Safety and Productivity Solutions segment including gas detection driving strong double-digit growth in the product category.

Key Company Profiles

Honeywell International Inc.

Honeywell, headquartered in Charlotte, North Carolina, operates in over 70 countries with approximately 120,000 employees. The company reported USD 38.5 Billion in revenue in FY2024, with its gas detection portfolio sitting within the Safety and Productivity Solutions segment.

- Product & Service Portfolio: BW Solo / BW Clip portable detectors, Searchline Excel open-path infrared detectors, Sensepoint fixed detectors, Touchpoint controllers, and Connected Plant IoT platform.

- Recent Developments: In May 2024, Honeywell International Inc. announced a partnership with Weatherford International plc to deliver an integrated emissions management solution for the oil & gas sector. The collaboration combines Honeywell’s emissions monitoring technologies with Weatherford’s CygNet SCADA platform, enabling near real-time tracking, reporting, and reduction of methane and other hazardous gas emissions, along with advanced analytics for regulatory compliance and operational optimization.

- Strategic Focus: Honeywell is advancing connected detection ecosystems, methane-emissions management, hydrogen-sensing capabilities, and integration with industrial automation platforms.

MSA

MSA, headquartered in Cranberry Township, Pennsylvania, is a global provider of advanced safety equipment and solutions. With around 5,000 employees and operations in over 40 countries, it reported approximately USD 1.8 billion revenue in 2024, led by gas and flame detection systems.

- Product & Service Portfolio: MSA offers portable gas detectors under the ALTAIR brand, fixed gas and flame detection systems via General Monitors, cloud-connected safety platforms like Sentry io, and refrigerant monitoring solutions such as Chillgard.

- Recent Developments: In May 2025, MSA Safety Incorporated highlighted advancements in its fixed gas and flame detection portfolio, emphasizing next-generation ultrasonic gas leak detection technologies with enhanced acoustic sensing and digital connectivity for improved integration with industrial safety systems.

- Strategic Focus: MSA prioritizes expansion into oil and gas, fire service, and utilities markets, with investment in connected monitoring, cellular-enabled portable devices, and emerging-market penetration.

Drägerwerk AG & Co. KGaA

Dräger, headquartered in Lübeck, Germany, operates in over 190 countries with approximately 16,000 employees. The company reported EUR 3.48 billion in revenue in 2025, with gas detection a cornerstone of its industrial safety division.

- Product & Service Portfolio: Dräger’s portfolio includes Polytron fixed gas detectors, X-am portable multi-gas detectors, Pac single-gas monitors, Regard control systems, and specialized gas detection solutions for firefighting, mining, and confined-space safety applications.

- Recent Developments: In March 2024, Drägerwerk AG & Co. KGaA expanded its portable gas detection portfolio, emphasizing enhanced X-am series capabilities with improved sensor performance, Bluetooth-enabled connectivity, and integration with cloud-based Gas Detection Connect for real-time monitoring and fleet management.

- Strategic Focus: Dräger emphasizes industrial safety, medical-technology integration, emergency-response applications, and equipment reliability in extreme and hazardous environments.

Market Concentration Analysis

The global gas detection equipment market is moderately concentrated at the top, with Honeywell, MSA Safety, and Dräger collectively accounting for an estimated 35–40% of 2025 revenue. These three operators lead both fixed and portable categories, benefiting from certification breadth, global service networks, and integrated software platforms.

The remaining market is fragmented among regional specialists, niche technology providers, and cost-competitive Asian manufacturers. Companies such as Hanwei Electronics Group, Trolex Ltd., and Sensidyne LP are well positioned in segments like industrial safety, mining, and air monitoring rather than holding broad global leadership.

Consolidation activity is accelerating, with recent transactions including Fortive's ongoing integration of Industrial Scientific and ENVEA's 2024 acquisition of Asia Pacific Air Quality Group. Continued M&A is expected as large players build IoT platforms and expand into adjacent hydrogen and environmental-monitoring segments.

Investment & Growth Opportunities

Fastest-Growing Segments

Wireless gas detection is the fastest-growing segment at an estimated 14.1% CAGR through 2034, driven by IoT integration, battery improvements, and mesh-network scalability. Portable and transportable detectors follow at approximately 13.2% CAGR, led by confined-space safety and mobile workforce applications.

Emerging Markets

India, Indonesia, Vietnam, and Saudi Arabia represent the highest-return geographic opportunities. India's refining capacity targets 450 million tons per year by 2030, and Saudi Arabia's Vision 2030 petrochemical expansion is creating multi-billion-dollar greenfield detector demand.

Venture and Strategic Investment Trends

Venture funding into industrial IoT, hydrogen-sensor startups, and AI-enabled emission-monitoring platforms is accelerating. Corporate venture activity from Honeywell Ventures, Fortive Ventures, and MSA Innovation Labs is shaping the next wave of connected, analytics-driven detection products.

Future Market Outlook (2026-2034)

The global gas detection equipment market forecast projects sustained expansion from USD 6.61 Billion in 2025 to USD 20.89 Billion by 2034, at a CAGR of 11.90% – adding more than USD 14 Billion in value over the forecast period. Growth will be led by emerging-market industrialization, hydrogen economy development, and widespread adoption of IoT-connected detection platforms.

Three transformational shifts will reshape the industry through 2034. First, wireless and IoT-connected detection will become the default for new installations, supported by falling battery costs and mature mesh networks. Second, AI-driven alarm management will displace reactive alarm logic, reducing false alarms and enabling predictive maintenance. Third, hydrogen and low-carbon fuel sensing will emerge as a standalone high-growth category paralleling traditional hydrocarbon detection.

By 2034, gas detection is expected to evolve from standalone safety instrumentation into integrated risk-intelligence platforms combining sensing, analytics, and response orchestration. Operators investing in connected ecosystems, multi-gas capability, and hydrogen-specific technologies are best positioned to capture disproportionate value across industrial and emerging clean-energy verticals.

Research Methodology

Primary Research

Structured interviews and surveys conducted in 2024–2025 with senior safety engineers at Fortune 500 oil, gas, and chemical operators, procurement directors at petrochemical companies, channel distributors, certified safety integrators, and technical leaders at OEM manufacturers informed demand-side perspectives.

Secondary Research

Sources include company annual reports (Honeywell International Inc., MSA, Drägerwerk AG & Co. KGaA, Teledyne, Gas and Flame Detection, Industrial Scientific, Thermo Fisher Scientific Inc.), regulatory publications (OSHA, ATEX, IECEx, EU EPA, U.S. EPA), trade associations (International Society of Automation, ASSE), and industry journals including Occupational Health & Safety and Process Safety Progress.

Forecasting Models

Market sizing uses a combined top-down and bottom-up approach, triangulated against end-user capex data, industrial output, workforce safety statistics, and historical detector replacement cycles. Scenario analysis models reflect base, optimistic, and conservative macroeconomic and regulatory assumptions.

Gas Detection Equipment Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Technologies Covered | Wired, Wireless |

| Detection Types Covered | Fixed, Portable and Transportable |

| End Use Industries Covered | Oil and Gas, Chemicals and Petrochemicals, Water and Wastewater, Metal and Mining, Utilities, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Honeywell International Inc., MSA, Drägerwerk AG & Co. KGaA, Teledyne Gas and Flame Detection, Industrial Scientific, Thermo Fisher Scientific Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the gas detection equipment market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global gas detection equipment market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the gas detection equipment industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Gas Detection Equipment Market Report

The global gas detection equipment market was valued at USD 6.61 Billion in 2025, driven by industrial safety mandates, oil and gas capex, and accelerating wireless detector adoption across hazardous workplaces.

The market is projected to reach USD 20.89 Billion by 2034, growing at a CAGR of 11.90% during 2026-2034, powered by Asia-Pacific industrialization and hydrogen-economy infrastructure investments.

Wired technology leads with a 62.5% share in 2025, supported by its reliability advantages in permanent installations, hazardous-area certification, and continuous monitoring requirements across large industrial sites.

Fixed detection systems command a 58.3% share in 2025, driven by deployments in refineries, petrochemical plants, LNG terminals, and utilities requiring continuous zone coverage and SCADA integration.

Asia-Pacific leads with a 34.8% share in 2025, anchored by China, India, Japan, and South Korea's industrial expansion, rising safety enforcement, and strong regional OEM manufacturing capacity.

Key drivers include stringent safety regulations, oil and gas capex expansion, wireless and IoT adoption, multi-gas detector innovation, and rising industrial automation across chemicals, mining, and utilities.

Asia-Pacific is the fastest-growing region through 2034, driven by Chinese and Indian refining growth, Southeast Asian petrochemical expansion, and increasing enforcement of worker safety standards regionally.

Leading companies include Honeywell International Inc., MSA, Drägerwerk AG & Co. KGaA, Teledyne, Gas and Flame Detection, Industrial Scientific, and Thermo Fisher Scientific Inc. among others.

Wireless detection holds a 37.5% share in 2025 and is the fastest-growing technology at approximately 14.1% CAGR, driven by IoT integration, easier retrofit, and remote monitoring capabilities.

Portable detector growth is driven by confined-space entry protocols, emergency-response applications, mobile maintenance workflows, and the shift to multi-gas handheld units with docking-station calibration.

IoT sensors, AI-driven analytics, multi-gas capability, and wireless mesh networks are reducing false alarms, enabling predictive maintenance, and expanding value per detector across industrial sites globally.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)