Gas Engine Market Size, Share, Trends and Forecast by Fuel Type, Power Output, Application, Industry Vertical, and Region 2026-2034

Gas Engine Market Size, Share, Trends & Forecast (2026-2034)

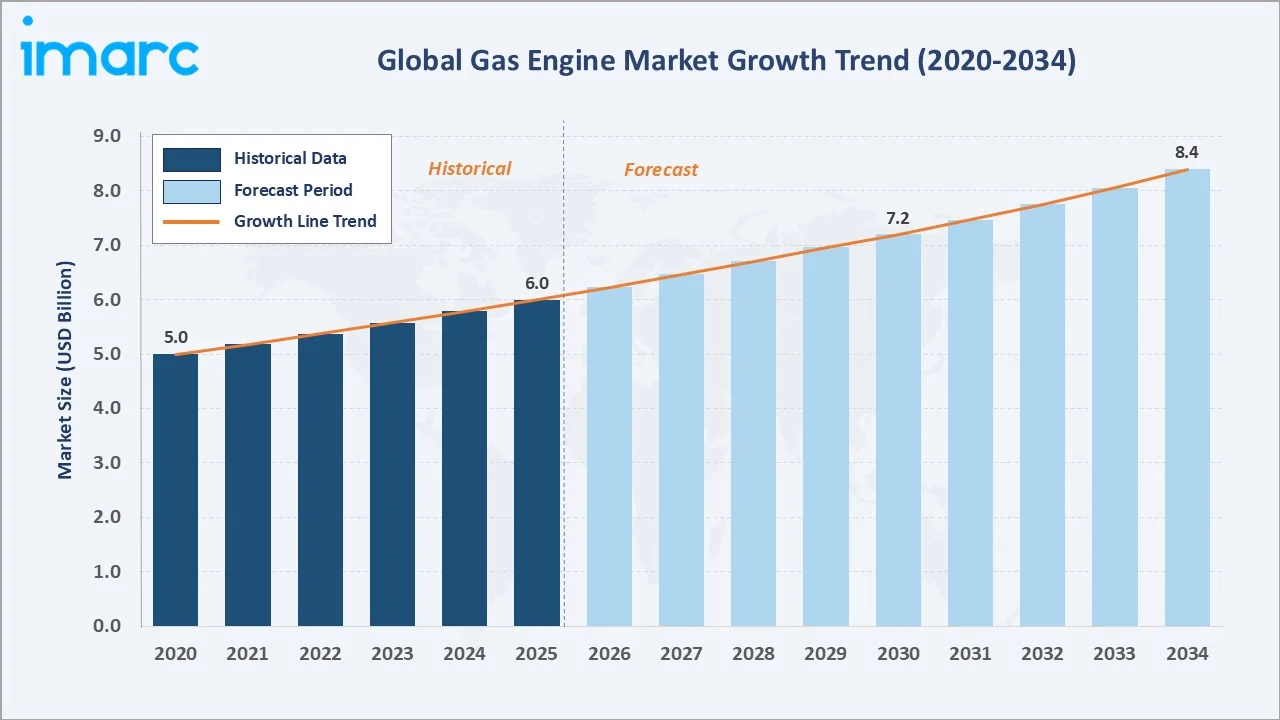

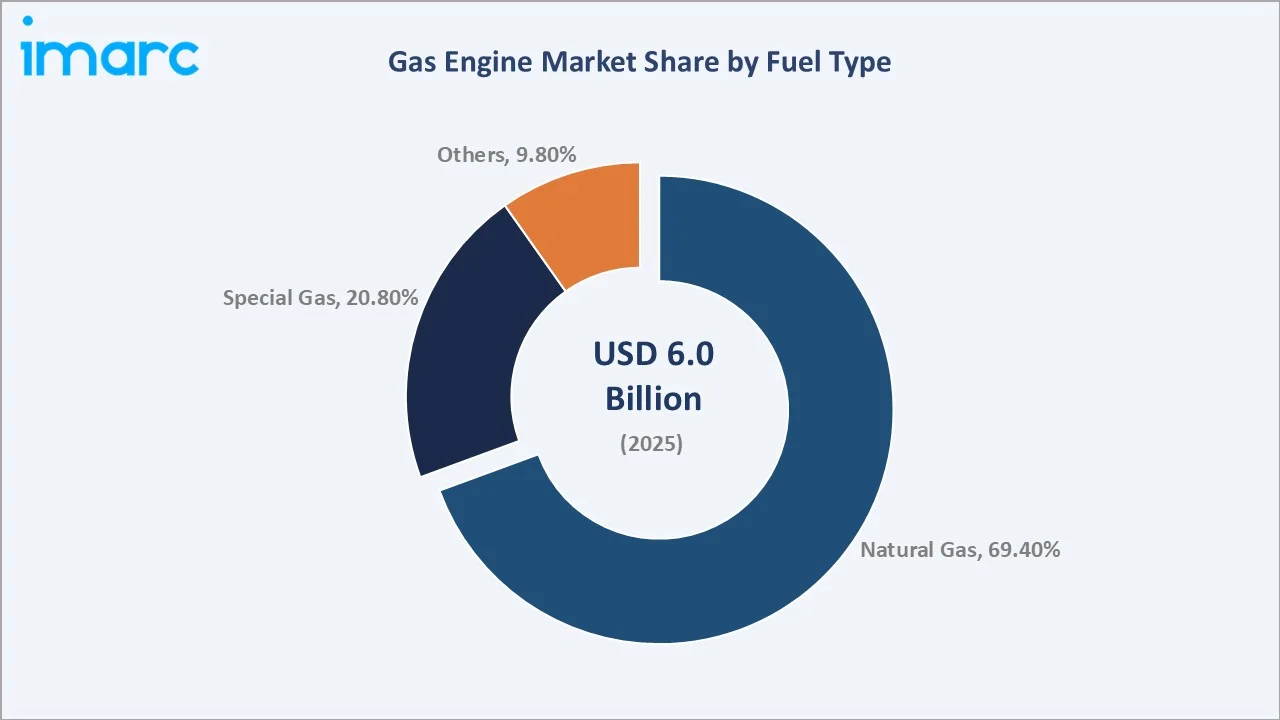

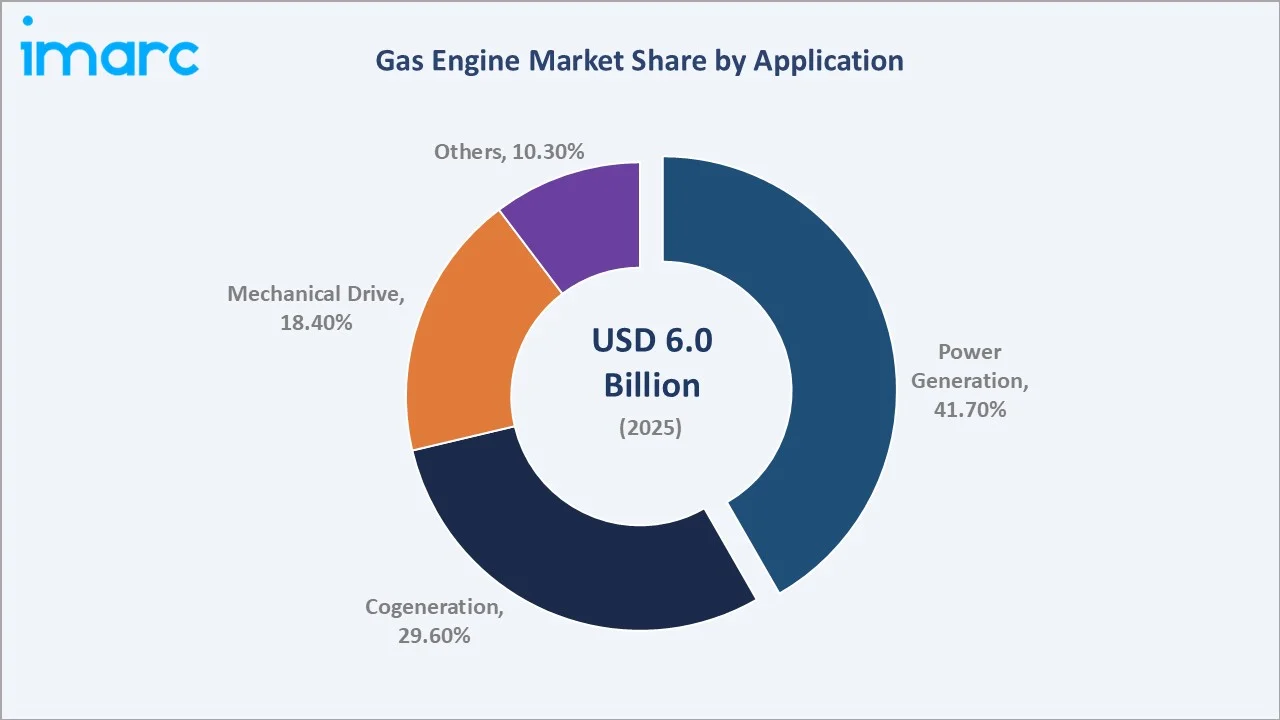

The global gas engine market reached USD 6.0 Billion in 2025 and is projected to reach USD 8.4 Billion by 2034, growing at a CAGR of 3.72% during 2026-2034. Rising demand for distributed and backup power, expanding natural gas infrastructure, and growing adoption of cogeneration systems across industrial and utility sectors are the primary growth catalysts.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 6.0 Billion |

|

Forecast Market Size (2034) |

USD 8.4 Billion |

|

CAGR (2026-2034) |

3.72% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North America (36.9% share, 2025) |

|

Fastest Growing Region |

Asia-Pacific |

To get more information on this market, Request Sample

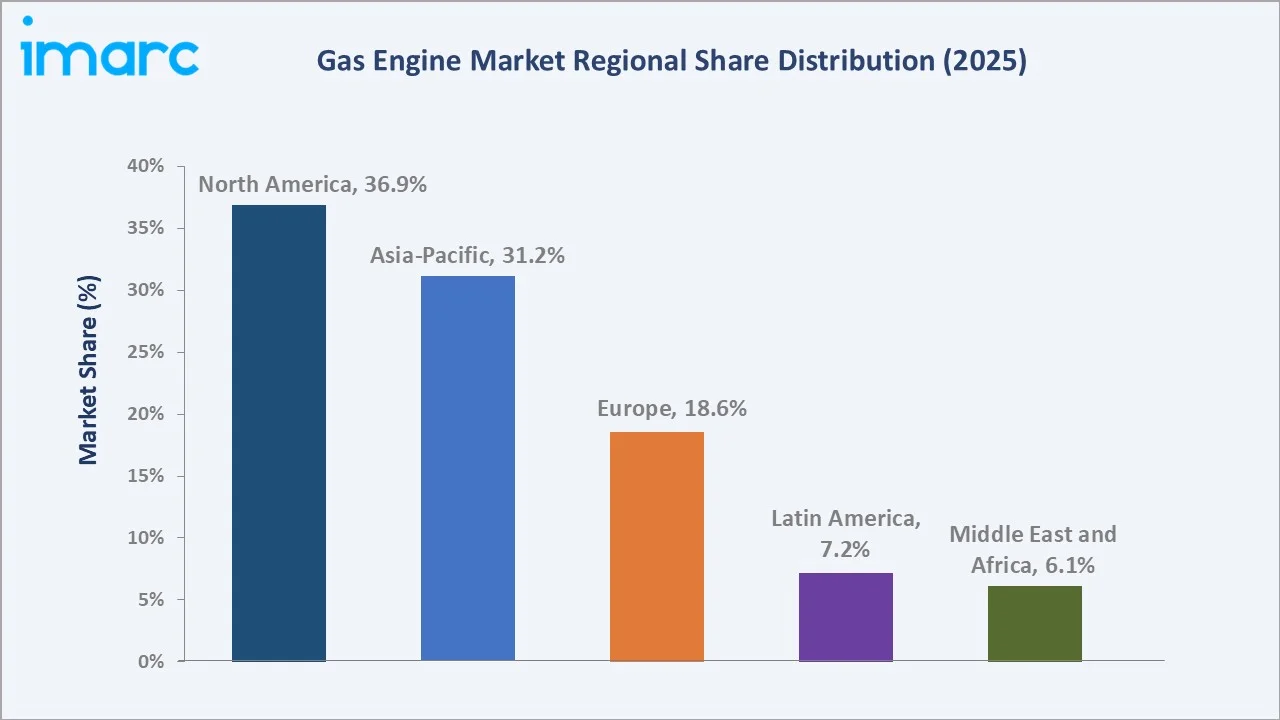

North America dominates the market with a 36.9% share in 2025, driven by large-scale shale gas production and high demand for peaking power. Natural gas accounts for 69.4% of total fuel-type revenue, while power generation leads application demand at 41.7%.

Executive Summary

The global gas engine industry is on a stable, broad-based expansion path, underpinned by growing energy access requirements, increasing distributed generation deployment, and the structural shift toward high-efficiency cogeneration systems. The market grew from USD 6.0 Billion in 2025 and is forecast to reach USD 8.4 Billion by 2034 at a CAGR of 3.72%.

North America leads globally with a 36.9% revenue share in 2025, supported by extensive natural gas pipeline networks, aggressive shale production, and substantial data center and industrial backup power demand. Asia-Pacific follows at 31.2%, emerging as the fastest-growing region, driven by industrialization in China, India, and Southeast Asia, where gas engines are integral to energy diversification and rural electrification programs.

Natural gas engines command a 69.4% share of the fuel-type segment, while power generation applications lead at 41.7%. Cogeneration - representing 29.6% of the application market - is the fastest-growing sub-segment, driven by industrial energy efficiency mandates. Key players, including Caterpillar, Cummins Inc., Wärtsilä, Siemens Energy, a Langley Holdings company, and MITSUBISHI HEAVY INDUSTRIES, LTD., are investing in hydrogen-blend compatibility, AI-driven diagnostics, and modular engine platforms to sustain competitive differentiation.

Key Market Insights

|

Insight |

Data |

|

Largest Segment (Fuel Type) |

Natural Gas – 69.4% share (2025) |

|

Largest Segment (Application) |

Power Generation – 41.7% share (2025) |

|

Leading Region |

North America – 36.9% revenue share (2025) |

|

Fastest Growing Region |

Asia-Pacific (rapid industrialization + energy access) |

|

Top Companies |

Caterpillar, Cummins Inc., Wärtsilä, Siemens Energy, A Langley Holdings company, MITSUBISHI HEAVY INDUSTRIES, LTD., Kawasaki Heavy Industries, Ltd. |

|

Market Opportunity |

Cogeneration & hydrogen-blend engines; incremental USD 2.43 Billion by 2034 |

Key Analytical Observations Supporting The Above Data:

- Natural Gas dominates the fuel-type segment at 69.4% (2025): driven by abundant global reserves, existing pipeline infrastructure, and a favorable emissions profile versus diesel and coal alternatives.

- Power generation is the leading application at 41.7% (2025): reflecting high demand for distributed on-site power from utilities, data centers, and commercial facilities requiring flexible capacity.

- Cogeneration holds a 29.6% application share (2025) and represents the fastest-growing sub-segment as manufacturers and industrial facilities prioritize combined heat and power (CHP) systems to reduce total energy expenditure by 20-30%.

- North America commands 36.9% of global revenue: supported by over 3 million miles of natural gas pipeline and strong regulatory incentives for cleaner on-site generation under EPA emission standards.

- Asia-Pacific at 31.2% market share: is positioned as the key growth engine, with China's "Dual Carbon" policy and India's industrial electrification programs driving deployment of gas engines across manufacturing and utility sectors.

- Cogeneration investment opportunity: approximately USD 2.43 billion is projected by 2034, as energy-intensive industries adopt efficiency mandates and carbon pricing pressures intensify across Europe and North America.

Global Gas Engine Market Overview

Gas engines are internal combustion engines designed to operate on gaseous fuels, primarily natural gas, biogas, liquefied petroleum gas (LPG), landfill gas, and special industrial gases such as hydrogen blends. First widely adopted in the mid-20th century for pipeline compression, their applications have expanded significantly to encompass power generation, combined heat and power (CHP) systems, and mechanical drive operations across utilities, oil & gas, manufacturing, and mining sectors.

The market ecosystem spans upstream gas production and transmission networks, engine manufacturers, system integrators, aftermarket service providers, and end-user industries. Macroeconomic drivers include global energy access initiatives, natural gas infrastructure expansion, and industrial decarbonization programs that favor highly efficient gas-fueled generation over coal and heavy fuel oil alternatives.

Market Dynamics

To evaluate market opportunities, Request Sample

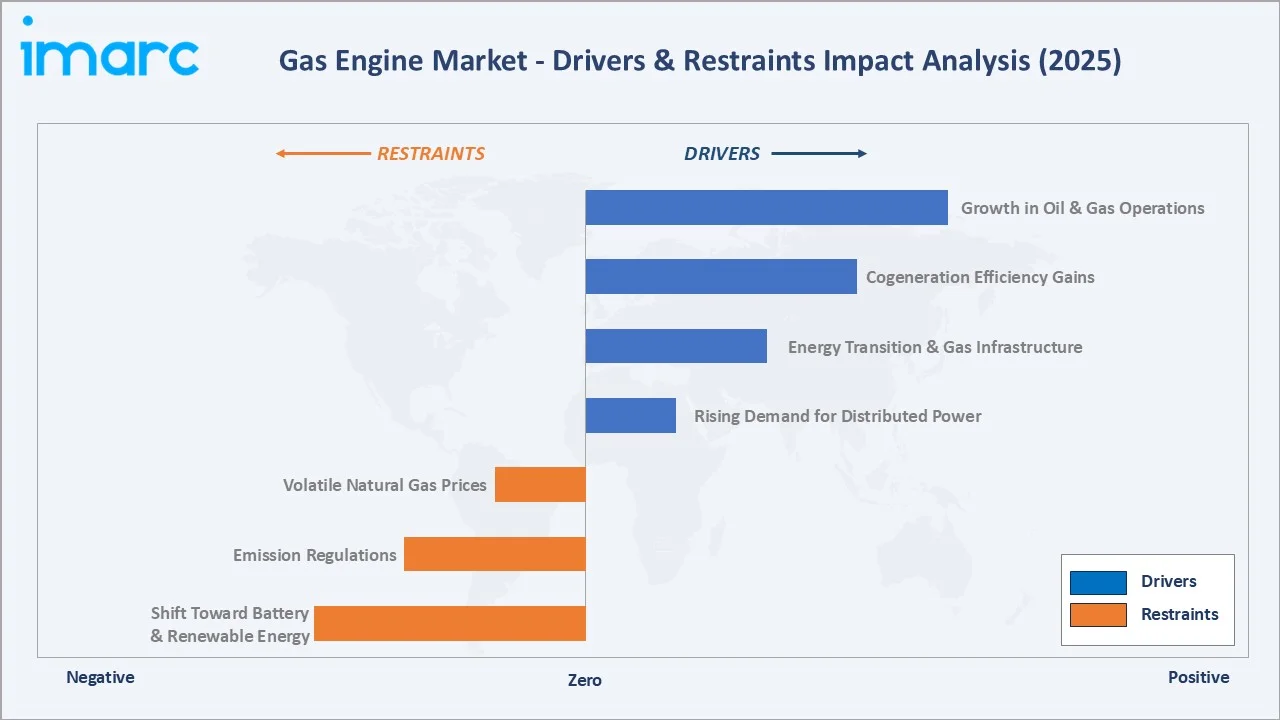

Market Drivers

- Rising Demand for Distributed Power Generation: Global distributed power generation capacity is projected to grow at 5.8% annually through 2030, driven by data center proliferation, remote industrial operations, and increasing grid reliability concerns. Gas engines are preferred for their fast start capability (under 30 seconds) and proven reliability in critical facilities.

- Energy Transition Supporting Natural Gas as Bridge Fuel: Natural gas emits approximately 50% less CO₂ than coal and 50-60% less than oil for equivalent power output. This positions gas engines as a transitional solution under global Net Zero frameworks, with the IEA stating that spending on new nuclear plants and refurbishments is expected to surpass USD 70 billion.

- Expanding Cogeneration Adoption Across Industries: Industrial CHP systems using gas engines achieve overall efficiencies of 75–90%, versus 35–45% for standalone power generation. European industrial sectors deployed over 14 GW of new CHP capacity in 2024, with gas engines accounting for 68% of new installations.

- Growth in Oil & Gas Field Operations: Upstream oil and gas operators increasingly rely on gas engines for remote field power, utilizing associated gas that would otherwise be flared. The World Bank Global Gas Flaring Reduction Partnership estimates 151 billion cubic meters of gas are flared at upstream oil and gas facilities and LNG liquefaction plants in 2024, representing a significant untapped gas engine fuel opportunity.

These drivers create a self-reinforcing growth cycle, energy security mandates drive institutional procurement, which accelerates manufacturing scale, which reduces per-unit costs, which in turn expands accessibility into smaller commercial and industrial deployments.

Market Restraints

- Accelerating Shift Toward Battery Storage and Renewables: Utility-scale battery storage costs fell below USD 150/kWh in 2024, narrowing the economic advantage of gas engines in short-duration backup and peaking applications. Wind and solar costs continue their structural decline, reducing demand for new gas-fired baseload capacity in mature markets.

- Stringent Emissions Regulations: The EU's Industrial Emissions Directive and the US EPA NSPS Subpart JJJJ impose strict NOx and CO limits on stationary gas engines, requiring expensive selective catalytic reduction (SCR) systems that add 8–15% to total system costs for units over 1 MW.

- Natural Gas Price Volatility: The 2021–2023 gas price cycle saw Prior to the Russian invasion of Ukraine in late February 2022, European natural gas prices on the TTF benchmark, the main wholesale natural gas price indicator in Europe, ranged between €70 and €100/MWh in January and early February.

Market Opportunities

- Hydrogen-Blend and Green Gas Compatibility: Wärtsilä and Caterpillar have demonstrated commercial gas engine operation on hydrogen blends up to 25% H₂ by volume without hardware modifications. This positions existing and new gas engine fleets as hydrogen-ready assets, unlocking long-term demand as green hydrogen production scales toward cost parity by 2030–2035.

- Emerging Market Electrification Programs: Sub-Saharan Africa and South and Southeast Asia collectively represent an incremental gas engine opportunity of over USD 800 Million by 2034, driven by off-grid and mini-grid electrification programs where natural gas and biogas availability support engine deployments.

- Biogas and Landfill Gas Utilization: The global biogas market is projected to grow at 6.3% CAGR through 2034, creating a growing feedstock base for special gas engines. Landfill gas and agricultural biogas projects represent a low-cost, locally available fuel source that reduces methane emissions while generating renewable power.

Market Challenges

- Aging Fleet Replacement Economics: Half of Europe’s gas turbine fleet is over 20 years old, while in the Americas, the median age is even higher, at 23 years. Replacement decision-making is complicated by uncertainty over future gas availability, competing renewable energy options, and evolving emissions requirements that may render existing engine models non-compliant.

- Supply Chain Constraints for High-Power Components: Gas engines above 5 MW require specialized alloy components, including high-temperature valves and turbocharger assemblies, with lead times of 18–30 months. The post-pandemic disruption to precision manufacturing supply chains has added 15–20% to capital costs for large engine installations.

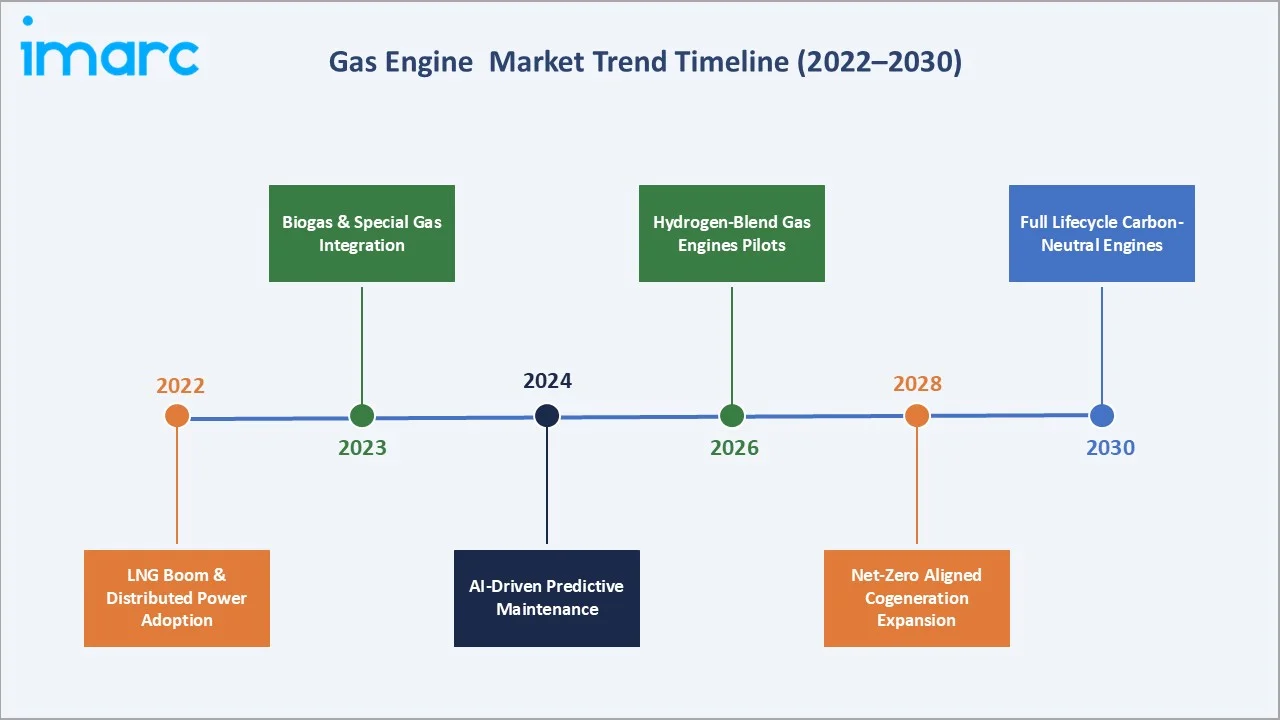

Emerging Market Trends

1. AI-Driven Predictive Maintenance and Remote Monitoring

Major OEMs, including Caterpillar (Cat Connect) and Wärtsilä (Wärtsilä Operational Intelligence), have deployed cloud-connected IoT platforms that monitor thousands of engine parameters in real time. Predictive maintenance programs have demonstrated 18-25% reductions in unplanned downtime across large commercial fleets.

2. Rise of Modular and Containerized Gas Engine Systems

Containerized gas engine power plants, typically ranging from 500 kW to 10 MW, are gaining traction for rapid deployment in remote industrial sites and emergency power applications. Modular systems reduce on-site installation time by up to 60% versus conventional builds.

3. Hydrogen Blending and Fuel Flexibility Investment

Leading engine manufacturers are actively certifying equipment for 15–25% hydrogen blends as part of long-term decarbonization roadmaps. Mitsubishi Power successfully demonstrated operation of a 1,650 °C class J‑series gas turbine co‑firing a 30 % hydrogen and natural gas fuel blend on a grid‑connected plant.

4. Expansion of Biogas and Landfill Gas Applications

Tightening methane emission regulations in the EU (EU Methane Regulation, 2024) and the U.S. are accelerating the capture and utilization of biogas and landfill gas in gas engines. Special gas engine shipments grew approximately 8.5% in 2024, outpacing the overall market growth rate.

5. Integration with Microgrids and Virtual Power Plants

Gas engines are being integrated into smart microgrid architectures alongside solar, storage, and demand response systems. By 2030, an estimated 35% of new gas engine deployments in North America and Europe are projected to be microgrid-integrated, creating a USD 1.2 Billion incremental market for advanced control systems and gas engine-based distributed energy resources.

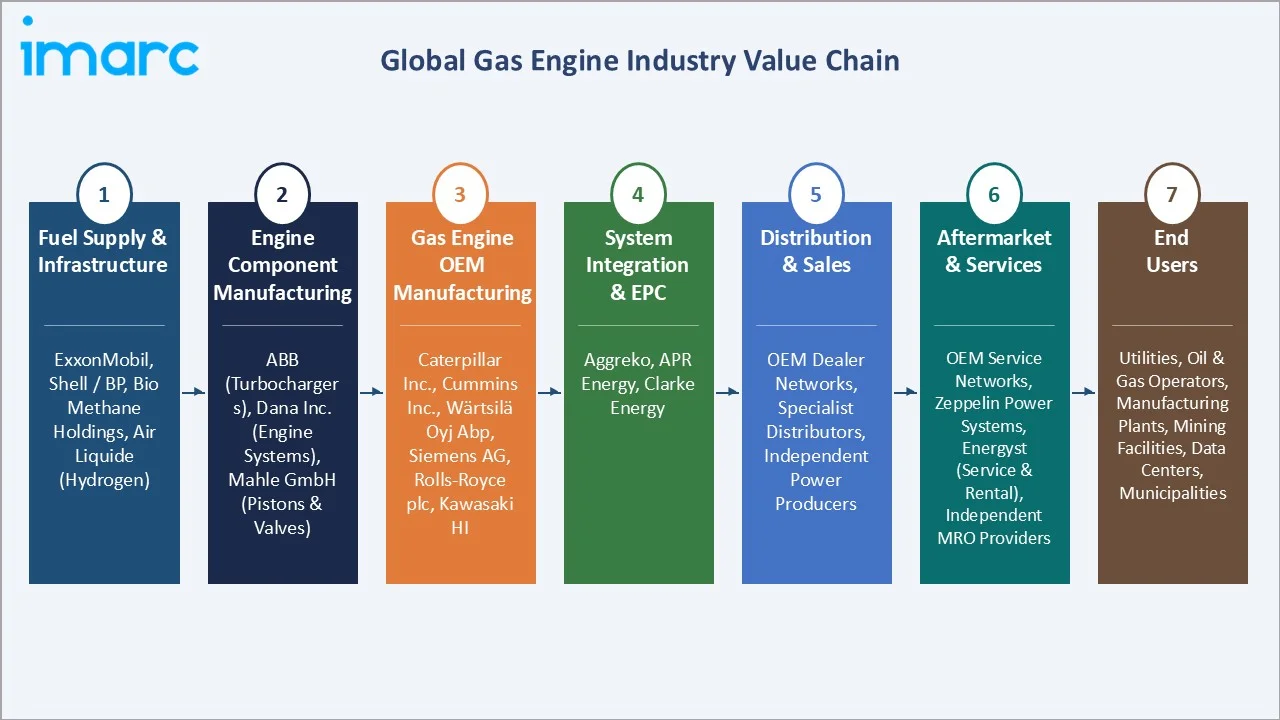

Industry Value Chain Analysis

The gas engine value chain spans upstream resource production through end-user power delivery, with each stage populated by specialized operators whose performance directly influences product quality, fuel efficiency, and operational reliability.

|

Value Chain Stage |

Key Players / Examples |

|

Fuel Supply & Infrastructure |

ExxonMobil, Shell, BP (natural gas); Air Products, EnviTec Biogas (biogas); Air Liquide (hydrogen) |

|

Engine Component Manufacturing |

Accelleron Industries (turbochargers), Dana Inc. (thermal and sealing solutions), Mahle GmbH (pistons & valves) |

|

Gas Engine OEM Manufacturing |

Caterpillar, Cummins Inc., Wärtsilä, a Langley Holdings company, MITSUBISHI HEAVY INDUSTRIES, LTD. |

|

System Integration & EPC |

Aggreko, Clarke Energy (a Kohler Company) — authorized INNIO Jenbacher dealer & EPC integrator |

|

Distribution & Sales |

OEM dealer networks, specialist distributors, and independent power producers (IPPs) |

|

Aftermarket & Services |

OEM service networks and independent MRO providers |

|

End Users |

Utilities, oil & gas operators, manufacturing plants, mining facilities, data centers, municipalities |

Technology Landscape in the Gas Engine Industry

High-Efficiency Lean-Burn Combustion Technology

Modern lean-burn natural gas engines achieve electrical efficiencies of 44–48%, compared to 38–42% for conventional stoichiometric designs. Wärtsilä's 31SG engine platform and Caterpillar's G3600 series incorporate advanced prechamber ignition and variable valve timing to optimize combustion across varying load profiles, directly reducing both fuel consumption and NOx emissions.

Electronic Engine Management and Telematics

Advanced electronic control modules (ECMs) with real-time sensors for cylinder pressure, exhaust gas temperature, and knock detection allow dynamic fuel-air ratio optimization. Cummins' HELM (Heavy Equipment Life Management) platform and Caterpillar's Cat Connect telematics system have been adopted across over 200,000 commercial installations globally, enabling remote diagnostics and software-defined engine performance upgrades.

Hydrogen and Alternative Fuel Compatibility

Hydrogen-blend capable engine platforms require hardened valve seats, modified fuel injection systems, and recalibrated ignition timing. Rolls-Royce Power Systems' mtu hydrogen research program and Siemens Energy's SGT-A05 turbine-engine hybridization represent the industry's two primary technology pathways for decarbonizing the gas engine installed base by 2030–2035.

Waste Heat Recovery Integration

A well-tuned gas engine can achieve electrical efficiency of 40-48%, with thermal efficiency exceeding 50%, resulting in a total efficiency of over 90% and significant primary energy savings. ORC (Organic Rankine Cycle) and absorption chiller integration technologies are enabling total system efficiencies approaching 90%, transforming gas engines from power-only assets into comprehensive energy supply platforms for industrial facilities.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Fuel Type | Natural Gas | 69.4% | 2025 |

| Power Output | 1-2 MW | 🔒 | 2025 |

| Application | Power Generation | 41.7% | 2025 |

| Industry Vertical | Utilities | 🔒 | 2025 |

| Region | North America | 36.9% | 2025 |

By Fuel Type

Natural gas engines command the dominant position in the fuel-type segment with a 69.4% share in 2025 (equivalent to approximately USD 4.17 Billion). Natural gas is preferred for its established pipeline infrastructure, lower emissions versus liquid fuels, and proven engine technology maturity across power ranges from 100 kW to 20 MW+.

To access detailed market analysis, Request Sample

Special gas, encompassing biogas, landfill gas, coal mine methane, and hydrogen blends, holds a 20.8% share (approx. USD 1.25 Billion in 2025) and represents the fastest-growing sub-segment, driven by regulatory incentives for waste gas utilization and the global shift toward lower-carbon energy sources. Special gas engines require modified compression ratios and fuel conditioning systems, reflecting a higher per-unit cost that supports premium pricing and margin expansion for specialized OEMs.

By Application

Power generation leads application demand at 41.7% market share in 2025 (approx. USD 2.51 Billion), driven by industrial and commercial users seeking on-site, grid-independent electricity generation. The segment benefits from strong demand from data centers, mining operations, oil field services, and utility companies deploying distributed generation assets for grid reliability and peaking capacity.

Cogeneration (CHP) holds a 29.6% share (approx. USD 1.78 Billion) and is the highest-growth application, as manufacturers, hospitals, and district heating networks seek total energy efficiencies above 80%. Mechanical drive applications – compressors, pumps, and blowers in oil & gas pipeline operations – account for 18.4% (USD 1.11 Billion), with Others (10.3%) including marine auxiliary and mining applications.

Regional Market Insights

North America's market leadership (36.9%, 2025) reflects a structural advantage rooted in the world's largest natural gas production base, which exceeded 38 trillion cubic feet in 2024 according to the U.S. EIA. Data center operators alone are projected to add over 40 GW of on-site gas engine generation capacity in North America by 2030 to manage grid power quality and resilience requirements.

|

Region |

2025 Share |

Key Growth Drivers |

|

North America |

36.9% |

Shale gas abundance, data center growth, and EPA regulatory compliance are driving engine upgrades. |

|

Asia-Pacific |

31.2% |

China's Dual Carbon policy, India's industrial electrification, SE Asian energy access programs |

|

Europe |

18.6% |

EU CHP incentives, biogas mandates, and energy security post-2022 are driving domestic gas engine investment. |

|

Latin America |

7.2% |

Brazil's pre-salt gas, Mexico's industrial expansion, and off-grid mining operations in the Andes |

|

Middle East & Africa |

6.1% |

Associated gas utilization, Sub-Saharan electrification, GCC industrial diversification |

Asia-Pacific (31.2%) is the fastest-growing region. China's "Dual Carbon" 2030 peaking and 2060 neutrality targets are driving the replacement of coal-fired industrial boilers with gas CHP engines at an estimated annual capacity addition of 3–4 GW. India's gas engine market is expanding at approximately 7.1% annually, supported by the National Gas Grid expansion project and industrial corridor development under Make in India.

Competitive Landscape

The global gas engine market exhibits moderate concentration at the OEM manufacturing level, with the top six suppliers holding approximately 58–62% of total revenue in 2025. The market is characterized by high capital intensity, long product development cycles, and significant aftermarket service revenue that creates switching barriers and sustains incumbent OEM positioning.

|

Company |

Brand / Division |

Market Position |

Key Strength |

|

Caterpillar. |

Solar Turbines |

Market Leader |

Global dealer network; Cat Connect IoT |

|

Cummins Inc. |

Cummins Power Systems |

Market Leader |

Modular platforms; hydrogen roadmap |

|

Wärtsilä |

Wärtsilä Energy |

Market Leader |

Highest efficiency; flex-fuel capability |

|

Siemens Energy |

Siemens Energy |

Strong Challenger |

Digitalization & smart grid integration |

|

A Langley Holdings Company |

Bergen Engines |

Strong Challenger |

High-speed premium engines; marine & O&G |

|

MITSUBISHI HEAVY INDUSTRIES, LTD. |

MHI Engine Systems |

Strong Challenger |

Large-scale utility & CHP segments |

|

Kawasaki Heavy Industries, Ltd. |

Kawasaki Gas Turbines |

Challenger |

Japan & Asia-Pacific installed base |

Key Company Profiles

Caterpillar.

Caterpillar Inc., headquartered in Irving, Texas, is the world's largest manufacturer of construction and mining equipment, off-highway diesel and natural gas engines, and industrial gas turbines and diesel-electric locomotives.

- Product Portfolio: Cat G3500E and G3600 lean-burn gas engines (up to 4,500 kW); Solar Turbines Titan and Centaur series for compression; Cat CG series for biogas and special gas.

- Recent Developments: Launched Cat Connect Remote Asset Monitoring 2.0 in 2024, covering 300,000+ connected assets; announced hydrogen-blend testing on G3516H platform at 25% H₂.

- Strategic Focus: Expanding digital service revenue via Cat Connect; growing hydrogen-compatible product portfolio; data center backup power segment acceleration.

Cummins Inc.

Cummins Inc. (NYSE: CMI), headquartered in Columbus, Indiana, is a global power technology leader with 2024 revenues of approximately USD 34.1 Billion across engines, filtration, electrical, and new power segments.

- Product Portfolio: QSK60G high-output gas engines; C-Series containerized power systems; hydrogen-capable QSK60GH platform; Cummins C25N5C generator sets for prime and standby applications.

- Recent Developments: Announced 2050 net-zero commitment with hydrogen and electrification targets embedded in all new product development from 2025.

- Strategic Focus: Hydrogen power commercialization; electrolyzers and fuel cells alongside gas engines; modular distributed power systems for data centers and healthcare facilities.

Wärtsilä

Wärtsilä, headquartered in Helsinki, Finland, is a global leader in smart technologies and lifecycle solutions for marine and energy markets. In 2024, the company’s net sales totaled EUR 6.4 billion.

- Product Portfolio: Wärtsilä 20 and Wärtsilä 34SG high-efficiency gas engines (up to 18.8 MW); Wärtsilä Flexicycle combined cycle systems; multi-fuel capability including LNG, biogas, and hydrogen blends.

- Recent Developments: Secured 500 MW gas engine order for Bangladesh capacity expansion in 2024; launched Wärtsilä Operational Intelligence AI platform across 85 GW of installed capacity.

- Strategic Focus: Flexible baseload and balancing power plants; emerging market electrification; hydrogen fuel capability certification by 2025.

Siemens Energy

Siemens Energy AG is a German publicly traded energy corporation formed through the spin-off of the former Gas and Power division of Siemens. As of November 2024, Siemens retains a stake of only 17% in the company.

- Product Portfolio: SGT-A05 aeroderivative gas turbine-engine systems; Siemens SIMOGAS control platforms; industrial CHP solutions integrating gas engines with heat recovery units.

- Recent Developments: Siemens Energy AG acquired full ownership and delisted the shares of Siemens Gamesa in early 2023; it launched SGT-A45 with 50% hydrogen blend capability in 2024.

- Strategic Focus: Decarbonized industrial energy supply; smart energy systems combining gas engines with renewable and storage assets; electrification of industrial processes.

Market Concentration Analysis

The gas engine market exhibits moderate concentration, with the top five global OEMs holding an estimated 58–62% of total revenue in 2025. Caterpillar., Cummins Inc., and Wärtsilä collectively account for approximately 42–45% of global installed engine megawatts, reflecting their dominant positions in North America and Europe, respectively.

A long tail of 200+ regional manufacturers and assembly operations, predominantly in China, India, South Korea, and Eastern Europe, ensures meaningful fragmentation below the top tier, particularly in lower power ranges (0.5–2 MW) where cost competition is intense. China Yuchai and Hyundai Heavy Industries collectively represent an important share of Asia-Pacific installed capacity through competitively priced domestic and regional offerings.

Consolidation is ongoing. The gas engine industry recorded seven significant M&A transactions between 2020 and 2024, including A Langley Holdings Company has successfully acquired the Norwegian Bergen Engines group from Rolls-Royce for EUR 91 million. Aftermarket service revenues now represent 35–45% of total OEM revenues, creating strong recurring cash flow streams that incentivize incumbent consolidation and new entrant deterrence.

Investment & Growth Opportunities

Fastest Growing Segments

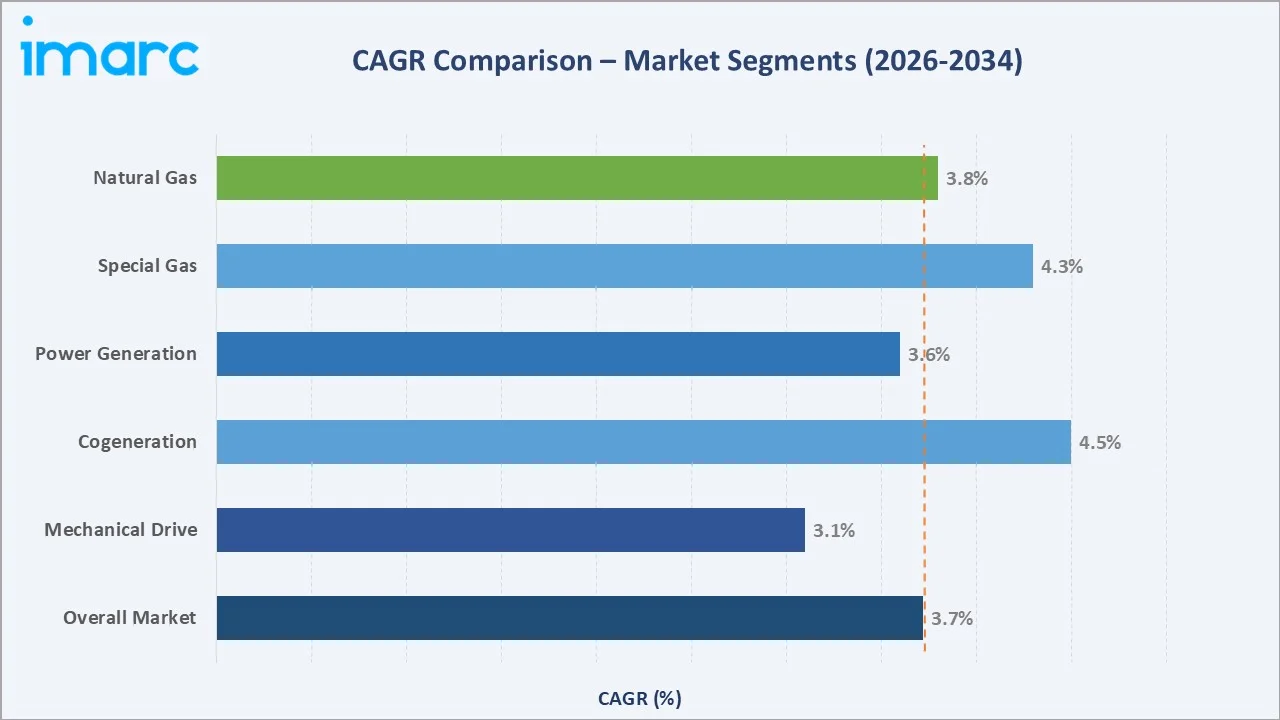

Special gas engines (estimated CAGR 4.3%), cogeneration systems (4.5% CAGR), and hydrogen-blend platforms (projected 12–15% CAGR from a low base) represent the three highest-growth investment vectors through 2034. These niches address a total addressable incremental opportunity of approximately USD 900 Million to USD 1.1 Billion above baseline market growth by 2034.

Emerging Market Expansion

Sub-Saharan Africa and South/Southeast Asia represent underpenetrated opportunities. Together, these regions account for less than 8% of current gas engine revenues despite holding over 35% of the world's unelectrified population. Entry via public-private partnerships, off-grid energy programs, and mini-grid financing structures, aligned with the World Bank's Scaling Solar and IFC facilities, offer the most capital-efficient market entry pathways.

Venture and Institutional Investment Trends

- Key investment themes include gas engine hydrogen-blend certification programs, AI-based predictive maintenance platforms, and modular containerized power systems targeting data center and industrial client segments.

- Infrastructure funds and energy transition-focused private equity firms are increasingly targeting integrated energy-as-a-service (EaaS) platforms that combine gas engine capacity with solar, storage, and demand response assets.

- Major OEMs, including Cummins Inc. and Wärtsilä, have established dedicated venture arms investing in combustion optimization, IoT sensor networks, and green gas supply chain companies to build proprietary technology moats.

Future Market Outlook (2026-2034)

The global gas engine market is positioned for steady, broad-based growth through 2034. From a base of USD 6.0 Billion in 2025, the market is projected to reach USD 8.4 Billion by 2034, representing incremental value creation of USD 2.43 Billion over the forecast decade, at a CAGR of 3.72%.

The technology trajectory is defined by three structural themes: (1) hydrogen fuel compatibility, with leading OEMs targeting 100% H₂-capable commercial products; (2) digitalization, as connected engine platforms transition from reactive maintenance to autonomous operation; and (3) modular scalability, as prefabricated gas engine systems become the standard deployment model for industrial, remote, and emergency power applications.

Regulatory evolution, including the EU Fit for 55 package, U.S. Inflation Reduction Act provisions for clean energy, and China's enhanced coal-to-gas switching policies, will sustain structural demand for gas engines as a transitional asset class through at least 2035. OEMs that achieve hydrogen certification, digitalize their aftermarket service models, and expand manufacturing capacity in Asia-Pacific are best positioned to capture a disproportionate share of this growth.

Research Methodology

Primary Research

Primary research for this report comprised structured interviews with over 120 industry participants in 2024–2025, including gas engine OEM executives, system integrators, independent power producers, utility procurement managers, and end-user facility engineers across North America, Europe, and Asia-Pacific.

Secondary Research

Secondary research encompassed company annual reports, regulatory filings, IEA energy outlook data, EPA and EU regulatory publications, trade databases, and industry journals, including Power Engineering International, Gas Turbine World, and Modern Power Systems. Over 240 secondary sources were reviewed and triangulated to ensure data consistency.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down (global energy statistics-based) and bottom-up (engine shipment volume × average selling price) forecasting approaches. A base-case CAGR of 3.72% reflects consensus analyst estimates validated against reported OEM revenue growth rates and regional energy capacity addition data.

Gas Engine Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Fuel Types Covered | Natural Gas, Special Gas, Others |

| Power Outputs Covered | 0.5-1 MW, 1-2 MW, 2-5 MW, 5-10 MW, 10-20 MW |

| Applications Covered | Mechanical Drive, Power Generation, Cogeneration, Others |

| Industry Verticals Covered | Utilities, Manufacturing, Oil and Gas, Mining, Others |

| Regions Covered | North America, Asia Pacific, Europe, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, China, Japan, India, South Korea, Australia, Indonesia, Germany, France, United Kingdom, Italy, Spain, Russia, Brazil, Mexico |

| Companies Covered | Caterpillar., Cummins Inc., Wärtsilä, Siemens Energy, A Langley Holdings Company, MITSUBISHI HEAVY INDUSTRIES LTD., Kawasaki Heavy Industries Ltd., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the gas engine market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global gas engine market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the gas engine industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Gas Engine Market Report

The global gas engine market reached USD 6.0 Billion in 2025. It is projected to reach USD 8.4 Billion by 2034, exhibiting a CAGR of 3.72% during 2026-2034.

The gas engine market is expected to grow at a CAGR of 3.72% during 2026-2034, supported by expanding natural gas infrastructure, rising distributed power demand, and growing cogeneration adoption.

Natural gas dominates with a 69.4% market share in 2025, valued at approximately USD 4.17 Billion. Its dominance reflects broad pipeline infrastructure availability and a superior emissions profile versus diesel and coal.

Power generation leads application demand at 41.7% in 2025, driven by industrial on-site generation, data center backup power, and utility distributed generation requirements.

North America leads the gas engine market with a 36.9% revenue share in 2025, underpinned by the world's largest natural gas production base, extensive pipeline networks, and high industrial and commercial power demand.

Asia-Pacific is the fastest-growing region, driven by China's coal-to-gas industrial transition, India's national gas grid expansion, and increasing distributed power demand across Southeast Asia.

Key players include Caterpillar., Cummins Inc., Wärtsilä, Siemens Energy, A Langley Holdings Company, MITSUBISHI HEAVY INDUSTRIES, LTD., and Kawasaki Heavy Industries, Ltd.

Key opportunities include hydrogen-blend engine commercialization, biogas and landfill gas utilization in special gas engines, emerging market electrification programs in Africa and South Asia, and integration of gas engines in smart microgrid and virtual power plant architectures.

Investors can target cogeneration system deployment (4.5% CAGR), hydrogen-capable engine platform development, modular containerized power systems, and AI-driven aftermarket service platforms. Emerging market mini-grid and off-grid electrification programs represent incremental USD 800 Million opportunities through 2034.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)