Gaskets and Seals Market Size, Share, Trends and Forecast by Product, Material, Application, End-Use, and Region, 2026-2034

Gaskets and Seals Market Size, Share, Trends & Forecast (2026-2034)

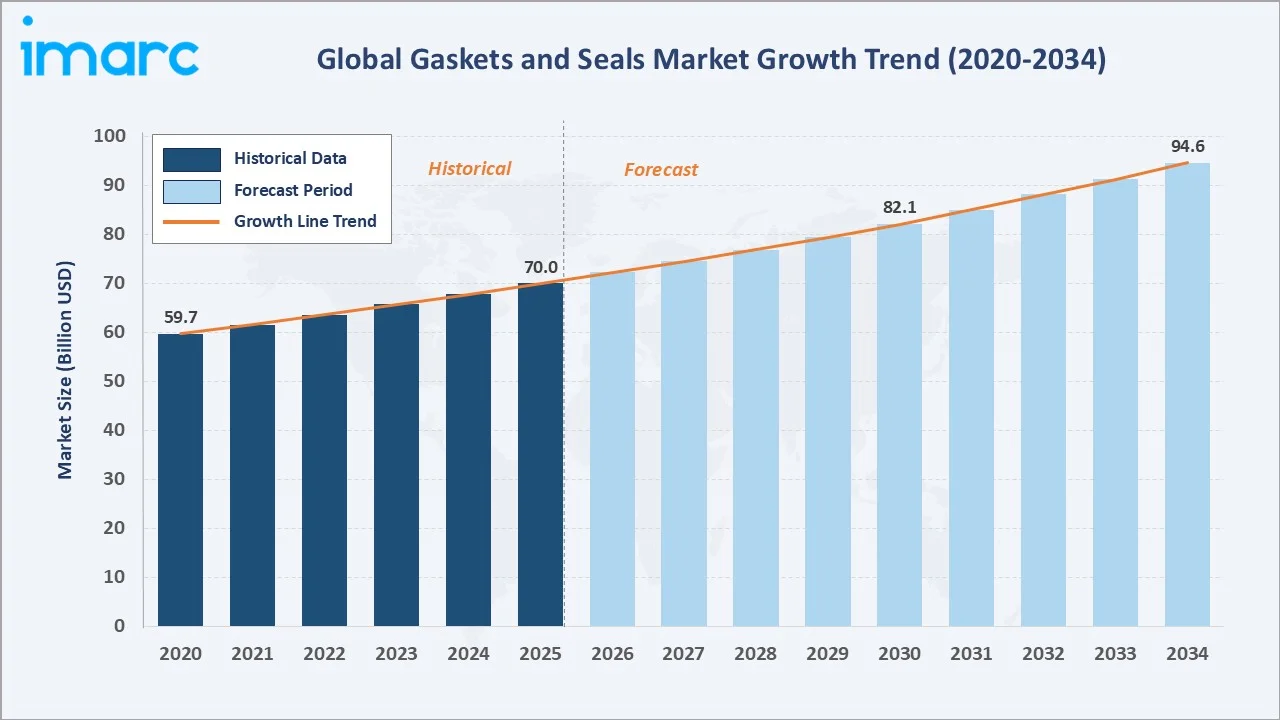

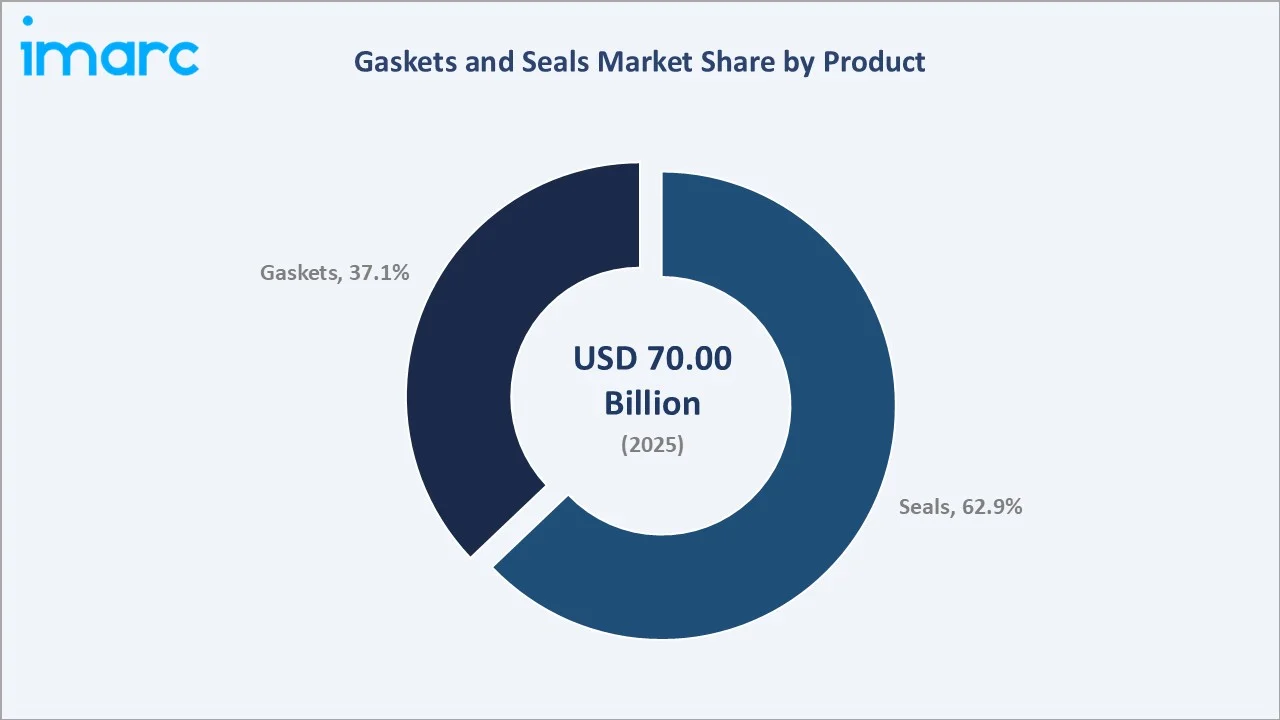

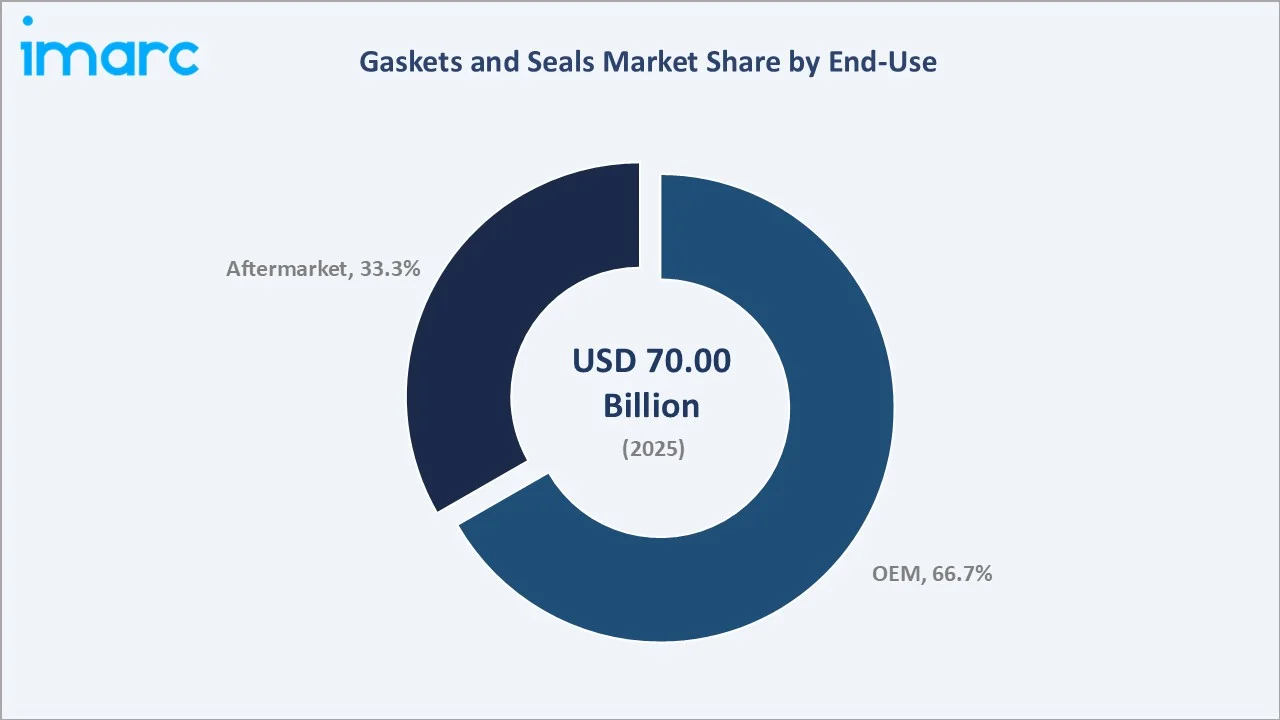

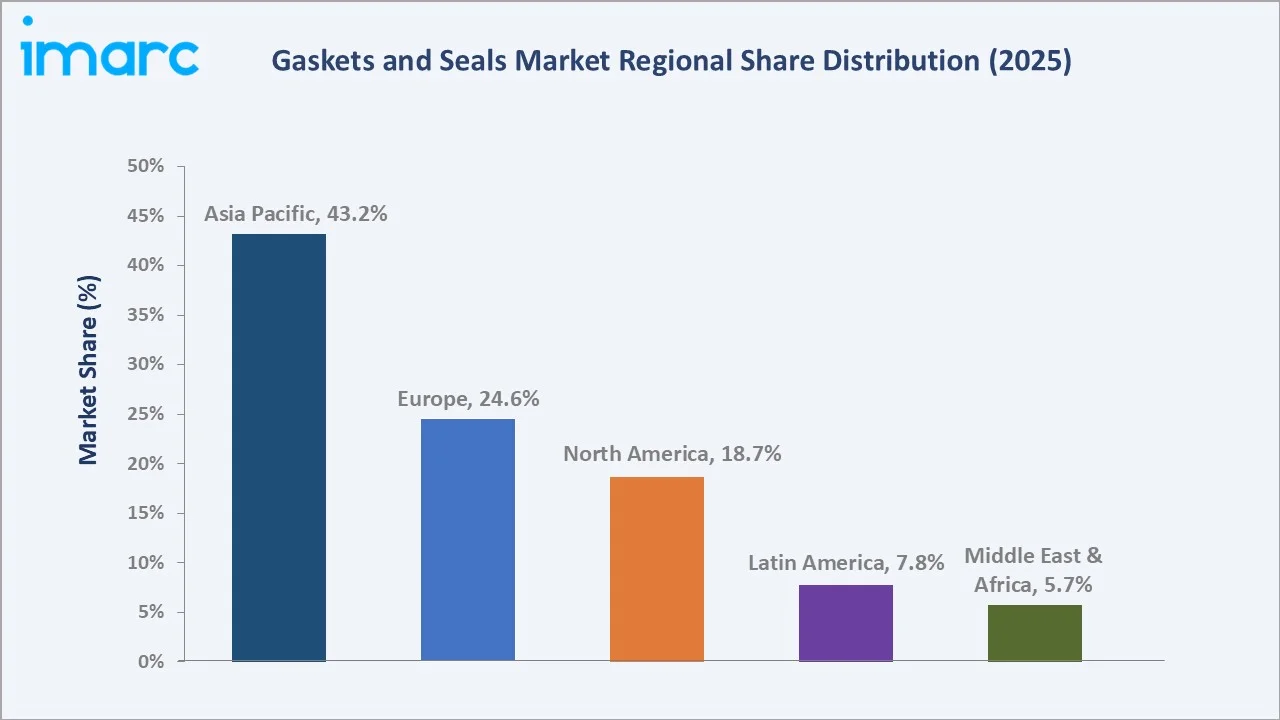

The global gaskets and seals market size was valued at USD 70.0 Billion in 2025 and is projected to reach USD 94.6 Billion by 2034, exhibiting a CAGR of 3.2% during the forecast period 2026-2034. Rising automotive production, including EV platforms, expanding industrial automation, deep aerospace demand, and sustained infrastructure investment are driving the gaskets and seals market growth. Seals lead the product type segment at 62.9% in 2025, while OEM dominates the end-use segment at 66.7%. Asia Pacific accounts for 43.2% of global revenue in 2025, the world's largest regional market for gaskets and seals.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 70.0 Billion |

|

Forecast Market Size (2034) |

USD 94.6 Billion |

|

CAGR (2026-2034) |

3.2% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Asia Pacific (43.2% share, 2025) |

|

Fastest Growing Region |

Asia Pacific (CAGR ~4.1%) |

|

Leading Product |

Seals (62.9%, 2025) |

|

Leading End-Use |

OEM (66.7%, 2025) |

The gaskets and seals market growth trajectory from 2020 through 2034 reflects steady historical expansion supported by automotive recovery, expanding industrial automation, and a forecast curve anchored by EV sealing demand, aerospace orders, and aftermarket replacement cycles.

To get more information on this market, Request Sample

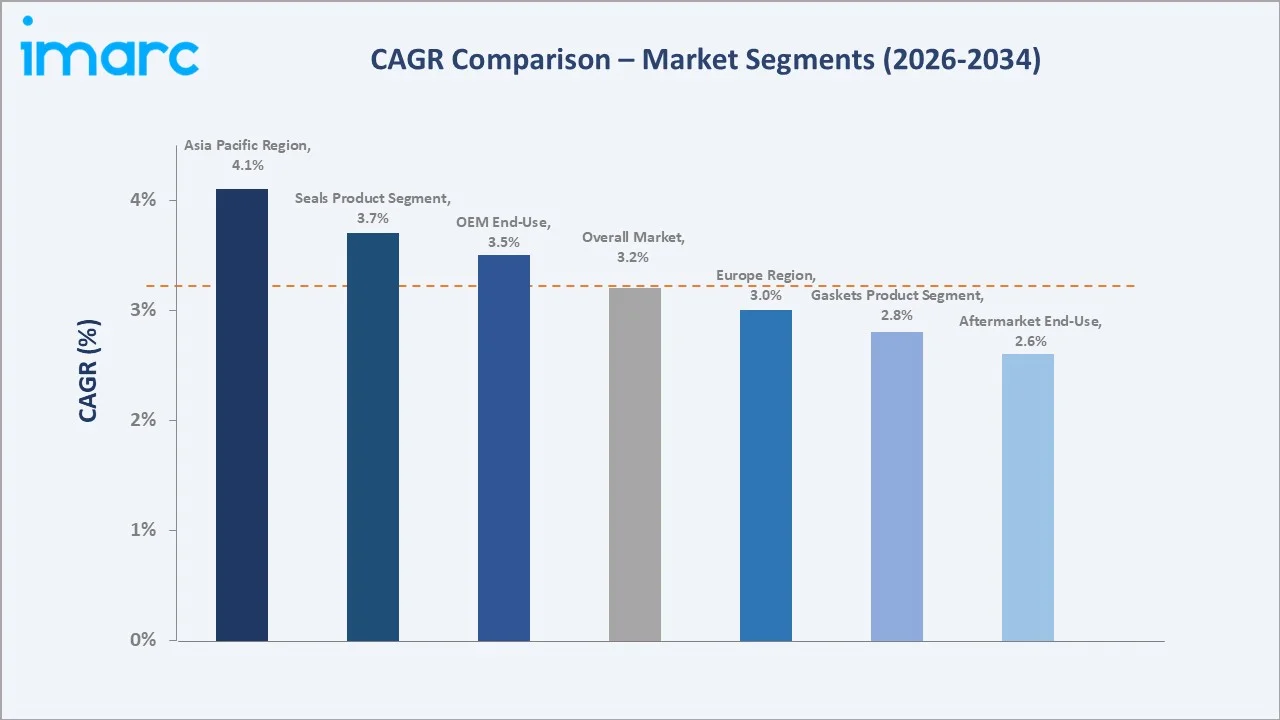

Segment-level CAGR comparison highlights Asia Pacific and the seals product segment as the two fastest-growing sub-segments within the gaskets and seals industry analysis through 2034, supported by EV adoption and automation retrofits.

Executive Summary

The gaskets and seals market is undergoing steady expansion, shaped by the convergence of electrification, industrial automation, and aerospace recovery. Valued at USD 70.0 Billion in 2025, the market is forecast to reach USD 94.6 Billion by 2034 at a CAGR of 3.2%. Global motor vehicle production reached around 93 million units in 2024, while EV car sales topped 17 million units in 2024, each platform requiring discrete sealing components, anchoring structural demand.

Seals command the dominant product type share at 62.9% in 2025, driven by broad applications across rotary shafts, hydraulic systems, and powertrain interfaces in automotive, industrial, and aerospace equipment. Gaskets at 37.1% in 2025 serve static sealing needs, with bio-based and PFAS-free formulations gaining traction.

Asia Pacific dominates with a 43.2% global revenue share in 2025, led by China's vehicle production of 27+ million units and Japan's technology-dense Tier-1 supplier ecosystem. Europe holds 24.6% in 2025 and North America 18.7%, with both regions characterised by premium vehicle penetration and advanced regulatory frameworks covering emissions and chemical compliance.

Key Market Insights

|

Insight |

Data |

|

Largest Product Type |

Seals - 62.9% share (2025) |

|

Largest End-Use |

OEM - 66.7% share (2025) |

|

Leading Region |

Asia Pacific - 43.2% revenue share (2025) |

|

Second Region |

Europe - 24.6% revenue share (2025) |

|

Top Companies |

Freudenberg Group, Parker Hannifin Corp, Trelleborg AB, SKF, Dana Limited, Tenneco Inc., Flowserve Corporation, Smiths Group plc, and ElringKlinger AG. |

Key Analytical Observations Supporting The Above Data:

- Seals' 62.9% dominance in 2025 reflects broad adoption across rotary and hydraulic applications, with EV powertrains requiring 20-30% more seals than ICE platforms per vehicle built.

- OEM share at 66.7% in 2025 reflects first-fit volumes across automotive, industrial machinery, and aerospace, where sealing components are critical for warranty, safety, and quality assurance.

- Asia Pacific's 43.2% global share in 2025 reflects China's role as the world's largest vehicle market at 27 million units produced annually and Japan's Tier-1 elastomer supply ecosystem.

Gaskets and Seals Market Overview

Gaskets and seals are engineered sealing components that prevent fluid, gas, and particulate leakage between mating surfaces in mechanical assemblies. The industry integrates raw material suppliers, compound formulators, precision manufacturers, and OEM/aftermarket distribution into a global supply platform spanning elastomers, fluoropolymers, metals, and composites.

Applications span automotive, industrial machinery, aerospace, oil and gas, chemical processing, food and beverage, and HVAC systems. Each end-use segment specifies distinct performance envelopes covering temperature, pressure, media compatibility, and service life.

Macroeconomic enablers include global vehicle production above 92 million units in 2024, industrial capex recovery, expanding aerospace order books, and sustained infrastructure investment, which together shape annual sealing demand across OEM and aftermarket channels globally.

Market Dynamics

To evaluate market opportunities, Request Sample

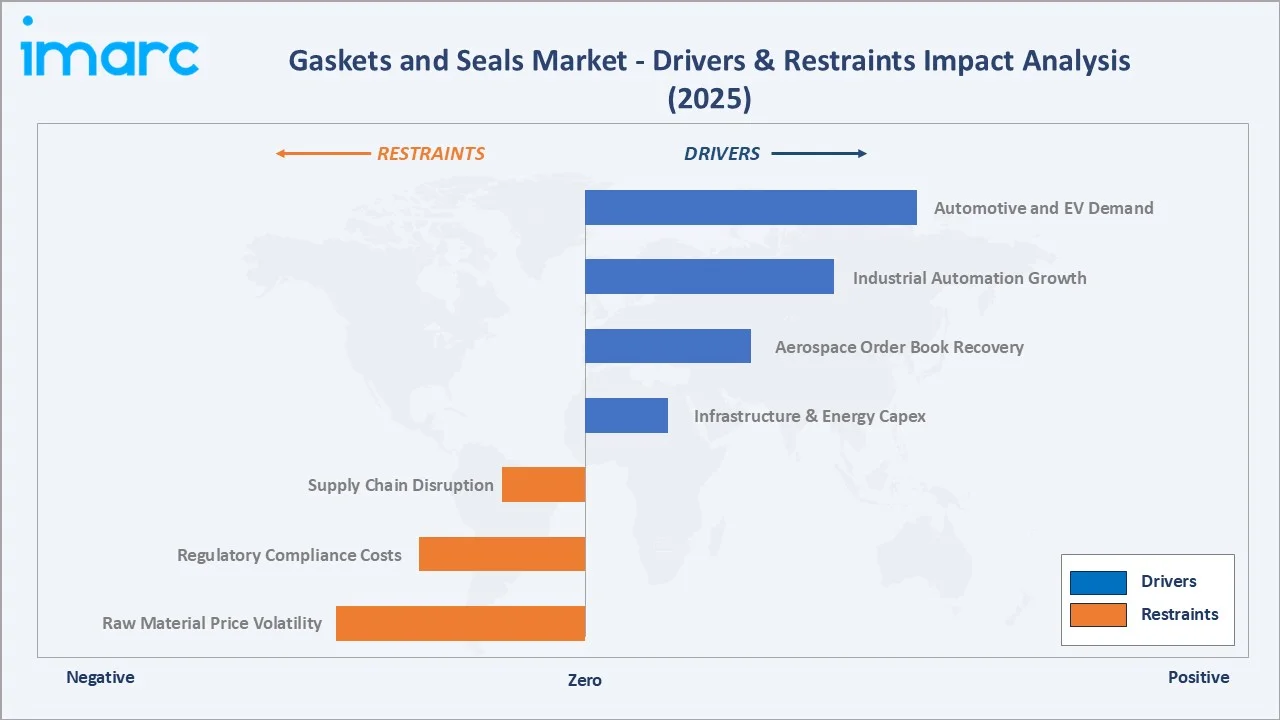

Market Drivers

- Automotive and EV Demand: Global EV sales topped 17 million units in 2024, with each platform requiring a significant number of sealing components, the most powerful structural driver for the gaskets and seals industry.

- Industrial Automation Growth: Industrial robotics installations exceeded 540,000 units globally in 2024, each requiring precision seals in actuators, pneumatics, and hydraulic subsystems.

- Aerospace Order Book Recovery: Boeing and Airbus combined backlog exceeded 13,000 aircraft in 2025, driving long-cycle demand for high-performance sealing solutions in engines and airframes.

- Infrastructure and Energy Capex: Global infrastructure and energy investment exceeded USD 3 trillion in 2024, supporting demand for industrial valves, pumps, and pipeline sealing across energy and water networks.

Market Restraints

- Raw Material Price Volatility: Rubber, fluoropolymer, and metal feedstocks represent a significant share of seal production cost, exposing manufacturer margins to commodity price swings and FX volatility.

- Regulatory Compliance Costs: REACH, RoHS, and emerging PFAS restrictions require reformulation investment, imposing compliance cost burdens on smaller sealing manufacturers.

- Supply Chain Disruption: Concentration in Asia-sourced elastomers and geopolitical friction create structural risks for just-in-time sealing supply across automotive and aerospace OEMs.

Market Opportunities

- EV-Specific Sealing Solutions: Battery packs, e-axles, and thermal management systems require advanced sealing formulations to manage thermal loads, prevent fluid ingress, and ensure long-term durability, positioning EV-focused sealing solutions as a premium and rapidly expanding sub-segment.

- Bio-Based and PFAS-Free Elastomers: Regulatory pressure and OEM sustainability commitments are opening a growth pocket for bio-elastomer and PFAS-alternative seals, particularly in European markets.

- Smart and IoT-Enabled Seals: Smart and IoT-enabled seals are emerging as a niche innovation area, with companies such as Trelleborg developing “cognitive sealing” systems that integrate sensors and analytics to monitor seal performance and enable predictive maintenance in industrial equipment.

Market Challenges

- Product Commoditisation Pressure: Standard gaskets face pricing pressure from low-cost Asian suppliers, squeezing margins and pushing Western producers toward premium and specialty segments.

- Aerospace Qualification Complexity: Multi-year qualification cycles and stringent certification requirements create barriers to new entrants and limit supplier rotation flexibility.

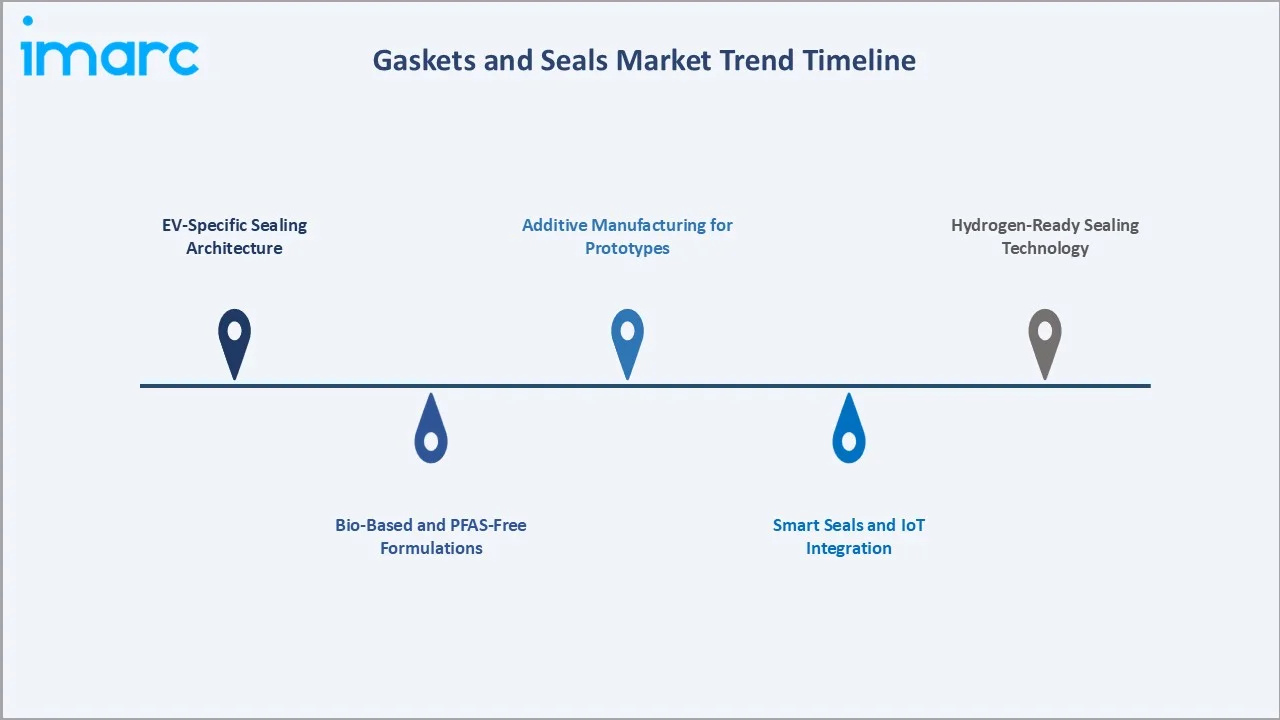

Emerging Market Trends

1. EV-Specific Sealing Architecture

Electric vehicle platforms demand seals that handle high-voltage environments, thermal cycling, and direct-oil cooling. Leading producers launched EV-grade portfolios targeting battery enclosures, e-axle housings, and power electronics modules. In 2025, Trelleborg debuted its CellXPro portfolio of next-generation sealing materials engineered specifically for EV battery cells at The Battery Show Europe.

2. Bio-Based and PFAS-Free Formulations

European REACH pressure and US EPA proposals on PFAS drove rapid reformulation activity during 2024-2025. In 2025, Freudenberg Sealing Technologies introduced an optimised elastomer sealing material for e-mobility applications as an alternative to PFAS-containing thermoplastic and FKM seals, processed by injection molding and meeting increasingly stringent environmental regulations.

3. Smart Seals and IoT Integration

Sensor-integrated seals capable of reporting wear, temperature, and leak detection data moved from pilots to commercial deployment. Industrial users increasingly value the predictive maintenance benefits, as early warning of seal degradation helps schedule repairs during planned shutdowns rather than incurring the cost of emergency outages.

4. Additive Manufacturing for Prototypes

3D-printed elastomer prototypes reduced design-iteration cycles from weeks to days at major OEMs. Full-scale production remains conventional, but rapid prototyping is accelerating new sealing development timelines, enabling faster customisation for EV, aerospace, and specialty industrial applications.

5. Hydrogen-Ready Sealing Technology

Hydrogen mobility and industrial hydrogen networks require seals compatible with small-molecule hydrogen at high pressures. Leading manufacturers announced hydrogen-specific portfolios, positioning for 2030 commercial scale-up.

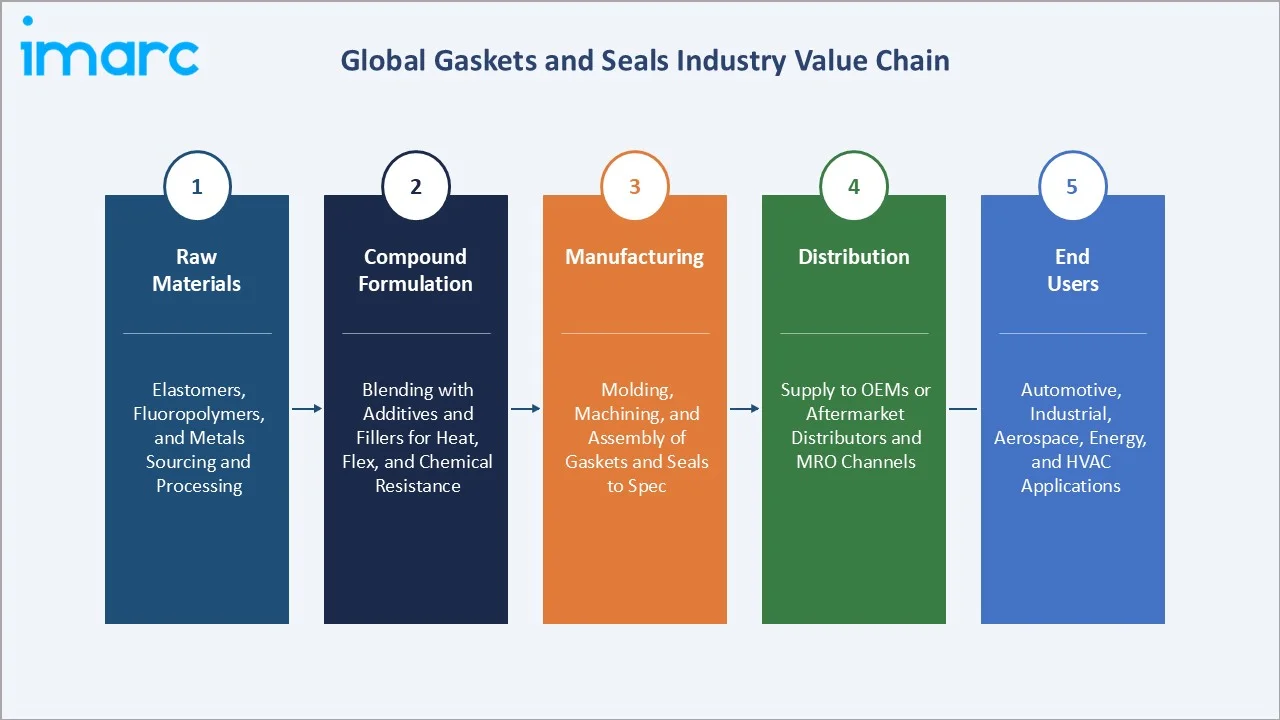

Industry Value Chain Analysis

The gaskets and seals value chain spans five integrated stages from raw material extraction through end-user delivery. Each stage presents distinct margin profiles, with raw materials representing the largest share of costs, followed by significant value addition during manufacturing.

|

Stage |

Key Players / Examples |

|

Raw Materials |

Base inputs such as elastomers, fluoropolymers, and metals are sourced and processed to meet performance requirements. |

|

Compound Formulation |

Materials are blended with additives and fillers to achieve specific properties like heat resistance, flexibility, and chemical stability. |

|

Manufacturing |

Formulated compounds are molded, machined, or assembled into finished gaskets and seals with precise specifications. |

|

Distribution |

Products are supplied to OEMs directly or through aftermarket distributors and MRO channels for industrial use. |

|

End Users |

Final components are utilized across automotive, industrial, aerospace, energy, and HVAC applications. |

Tier-1 sealing manufacturers occupy the highest strategic value position, combining compound R&D, precision manufacturing, and OEM co-engineering into turnkey sealing solutions. This position is under competitive pressure from low-cost Asian producers in standard product categories and from specialty chemical companies expanding downstream into finished sealing components.

Technology Landscape in the Gaskets and Seals Industry

Elastomer and Polymer Innovation

The industry is shifting toward high-performance elastomers, including HNBR, FKM, and FFKM for demanding applications. Bio-based alternatives and PFAS-free fluoroelastomers are gaining commercial traction as regulatory pressure and OEM sustainability commitments drive reformulation activity. In June 2025, Trelleborg presented its Isolast FFKM range with PFAS-free alternatives alongside FlexCoat NG and Seal-Glide surface coatings at the Trelleborg ConneX event, targeting semiconductor and chemical processing applications.

Precision Manufacturing and Automation

Advanced molding, laser-cut gasket production, and automated inspection systems are enabling leading Tier-1 producers to reduce defect rates and improve throughput. In 2025, Freudenberg Sealing Technologies invested in a new seal manufacturing plant in Querétaro, Mexico, an automated central warehouse at its Weinheim facility in Germany, and started construction on a new elastomer mixing plant for automotive and industrial customers.

Smart Connectivity and IoT-Enabled Seals

Sensor-integrated seals reporting real-time wear, temperature, and leak data moved from pilots to commercial deployment, enabling predictive maintenance and reducing unplanned equipment downtime at early adopters. At Drinktec 2025 in Munich, Freudenberg Sealing Technologies unveiled its SmartChange hygienic clamping system alongside new high-performance materials such as 75 HNBR 641, demonstrating the transition of smart, self-diagnosing seals from concept to commercial deployment in food and process industries.

Additive Manufacturing and Digital Simulation

3D-printed elastomer prototypes and finite-element simulation of sealing interfaces reduced development cycles at leading OEMs. Full production remains conventional, but digital design workflows now precede every major sealing launch.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Product | Seals | 62.9% | 2025 |

| Material | Rubber | 47.5% | 2025 |

| Application | Automotive | 29.4% | 2025 |

| End-Use | OEM | 66.7% | 2025 |

| Region | Asia Pacific | 43.2% | 2025 |

By Product

Seals command a 62.9% majority share in 2025, reflecting broad deployment across rotary shafts, hydraulic pistons, and dynamic sealing interfaces in automotive, industrial machinery, aerospace, and oil and gas applications. The segment benefits from structurally higher unit pricing and complexity premium over standard gaskets.

To access detailed market analysis, Request Sample

Gaskets at 37.1% in 2025 serve static sealing requirements across engine covers, flanges, pipelines, and bolted joints. The segment includes metallic, non-metallic, and composite constructions, with expanding demand for bio-based and PFAS-free formulations in Europe and North America.

By End-Use

OEM applications dominate at 66.7% in 2025, driven by first-fit demand across automotive assembly, industrial machinery production, and aerospace manufacturing. OEM channels deliver higher volumes and long-term supply agreements, but compress margins through competitive bidding and annual price-down expectations.

Aftermarket applications at 33.3% in 2025 cover replacement, repair, and MRO requirements across a large global vehicle base and an industrial installed base comprising tens of millions of valves, pumps, and compressors. Aftermarket margins remain structurally higher than OEM supply, supported by recurring demand and stronger pricing power.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Asia Pacific |

43.2% |

China NEV boom, Japan Tier-1 tech, India auto expansion, ASEAN manufacturing |

|

Europe |

24.6% |

VW/BMW/Mercedes EV platforms, EU emissions rules, PFAS reformulation demand |

|

North America |

18.7% |

US OEM onshoring, Tesla and Big Three EV capex, aerospace order book |

|

Latin America |

7.8% |

Brazil and Mexico auto production, growing industrial and agricultural equipment |

|

Middle East & Africa |

5.7% |

GCC oil and gas capex, petrochemical expansion, industrial infrastructure |

Asia Pacific commands a 43.2% global revenue share in 2025, the most dominant regional position. China is the single most important national market, combining the world's largest vehicle production base at 27.5 million units in 2024 with the most adoption of EV platforms that demand advanced sealing solutions. Japan and South Korea add premium Tier-1 supplier depth, while India and ASEAN drive volume growth.

Europe holds 24.6% in 2025, anchored by premium OEMs and leading the global push on EV sealing and PFAS-free formulations. North America (18.7%) benefits from US OEM onshoring and aerospace recovery. Latin America (7.8%) serves regional auto production, while Middle East & Africa (5.7%) is driven by oil and gas capex and industrial infrastructure expansion.

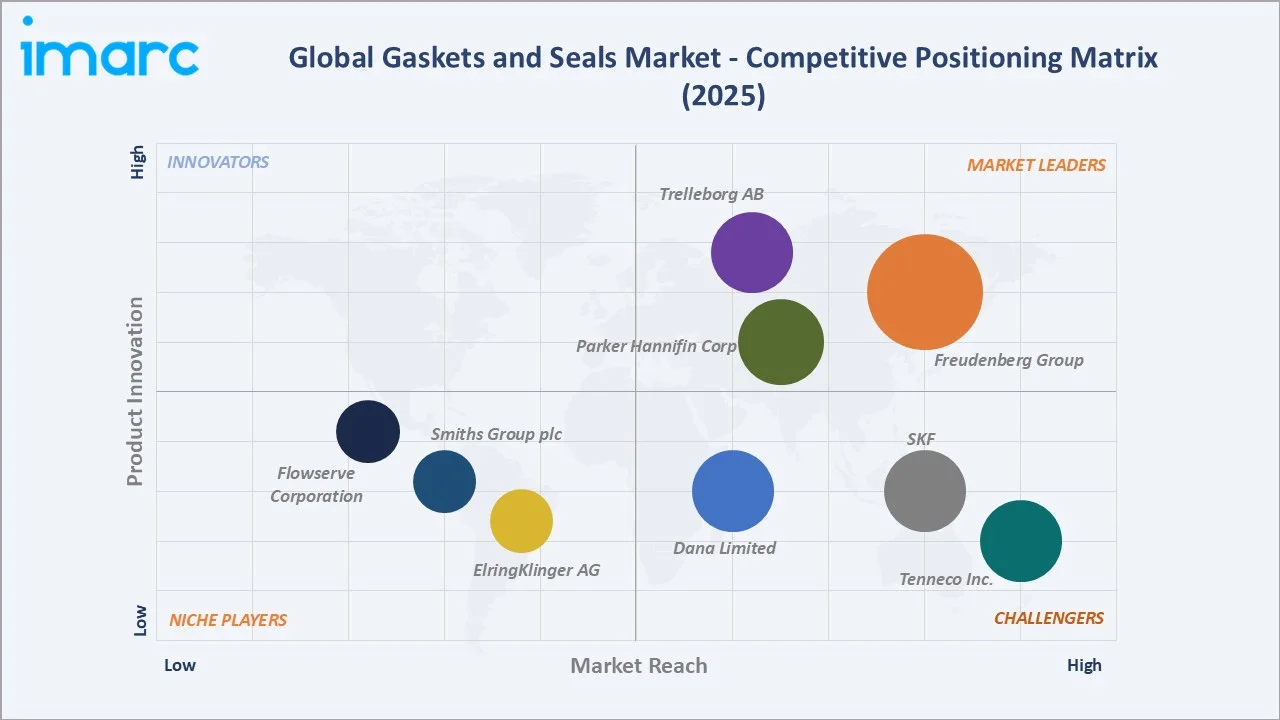

Competitive Landscape

|

Company Name |

Key Brand / Platform |

Market Position |

Core Strength |

|

Freudenberg Group |

Simriz, Merkel |

Leader |

Diversified sealing portfolio, EV solutions, global scale |

|

Parker Hannifin Corp |

Parker O-Seal |

Leader |

Motion and control sealing, aerospace specialty |

|

Trelleborg AB |

Trelleborg Sealing Solutions |

Leader |

Precision polymer sealing, aerospace and industrial |

|

SKF |

SKF Scotseal, Speedi-Sleeve |

Challenger |

Rotary sealing, bearing-integrated solutions |

|

Dana Limited |

Victor Reinz Gaskets |

Challenger |

Engine and driveline sealing, auto OEM supply |

|

Tenneco Inc. |

Goetze |

Challenger |

Automotive aftermarket, engine sealing |

|

Flowserve Corporation |

Flowserve Mechanical Seals |

Emerging |

Pump and valve sealing, oil and gas focus |

|

Smiths Group plc |

John Crane |

Emerging |

Industrial mechanical seals, rotating equipment |

|

ElringKlinger AG |

Elring Oil Seals |

Emerging |

Cylinder-head and specialty automotive sealing |

The gaskets and seals competitive landscape is characterised by a handful of global Tier-1 suppliers commanding substantial OEM relationships across automotive, industrial, and aerospace end-markets, alongside specialty players with deep technology focus in mechanical seals, engine sealing, and sensor-integrated solutions. Market leaders differentiate through material science R&D, OEM co-engineering, and global manufacturing footprints.

Key Company Profiles

Freudenberg Group

Freudenberg is the global leader in sealing technology, operating through Freudenberg Sealing Technologies, with manufacturing in 30+ countries and strong exposure to automotive, industrial, and specialty applications.

- Product & Platform Portfolio: Simrit, Merkel, Eagle Burgmann, EV-grade sealing solutions, bio-elastomer formulations.

- Recent Developments: In 2025, Freudenberg Sealing Technologies introduced a new elastomer sealing material for e-mobility battery cells as a PFAS-free alternative to thermoplastic and FKM seals, and continues to expand its hydrogen sealing portfolio with low-permeability seal materials for electrolyzers and fuel cell applications.

- Strategic Focus: Freudenberg prioritises material science leadership, EV and hydrogen sealing platforms, sustainability through bio-based and PFAS-free formulations, and global manufacturing footprint optimisation across key automotive and industrial clusters.

Parker Hannifin Corp

Parker Hannifin is a global motion and control technologies leader with a broad sealing and fluid management portfolio serving automotive, aerospace, industrial, and specialty markets from over 50 operating divisions.

- Product & Platform Portfolio: Parker O-Seal, Chomerics EMI shielding, PolyPak, aerospace sealing systems.

- Recent Developments: In 2025, Parker Hannifin announced the acquisition of Filtration Group Corporation for USD 9.25 billion, its second-largest transaction ever, significantly expanding its filtration and aftermarket platform serving aerospace, industrial, and sealing-adjacent applications.

- Strategic Focus: Parker targets high-margin specialty sealing in aerospace and hydrogen applications, cross-division technology sharing, digital predictive maintenance services, and selective M&A to strengthen its filtration and fluid management platform.

Trelleborg AB

Trelleborg is a Swedish precision polymer solutions specialist, operating Trelleborg Sealing Solutions with a strong focus on aerospace, industrial, and premium automotive sealing requirements globally.

- Product & Platform Portfolio: Turcon, Zurcon, Orkot, Wills Rings, EV-specific and aerospace high-performance sealing.

- Recent Developments: In 2025, Trelleborg finalised the acquisition of CRC Distribution, a US-based distributor of polymer seals for hydraulics, hydropower, oil and gas, and fluid power applications, followed by the acquisition of Aero-Plastics Inc. to strengthen its aerospace interior solutions portfolio.

- Strategic Focus: Trelleborg focuses on premium sealing technology in aerospace and industrial, sustainability leadership through circular economy initiatives, and geographic expansion via targeted acquisitions, complementing its core polymer engineering capabilities.

Market Concentration Analysis

The gaskets and seals market exhibits moderate concentration, with Freudenberg, Parker Hannifin, Trelleborg, SKF, and Dana collectively accounting for approximately 35-42% of global revenue in 2025. The remainder is distributed across mid-sized specialty players and regional manufacturers serving local OEM and aftermarket demand.

Segment-level concentration varies. Aerospace and specialty industrial sealing display a high concentration, with the top three players holding above 50% share, driven by long qualification cycles and certification barriers. Standard automotive and industrial gaskets are more fragmented, with Asian suppliers expanding volume share on pricing advantage.

Consolidation trends are expected to continue through 2030, driven by material science capex requirements, ESG-linked financing, and OEM preference for globally-scaled partners. Smaller specialty players with unique material or sensor-integration capabilities remain attractive acquisition targets for Tier-1 leaders seeking technology differentiation.

Investment & Growth Opportunities

Fastest-Growing Segments

EV-specific sealing solutions are the highest-growth sub-segment through 2034, driven by battery pack, e-axle, and thermal management demand across accelerating electrification programmes. Asia Pacific is the fastest-growing region, supported by China's NEV production base and India's expanding industrial manufacturing sector.

Emerging Market Expansion

Hydrogen mobility sealing and PFAS-free elastomer reformulation are the emerging premium sub-markets, transitioning from early pilots to mainstream commercial adoption. Smart and sensor-integrated seals represent the highest-potential technology opportunity, offering both product premium pricing and recurring service revenue.

Venture & Private Investment Trends

Notable transactions include Trelleborg's bolt-on acquisitions in engineered coatings, Freudenberg's continued capex in EV and hydrogen sealing, and private equity interest in specialty elastomer compounders. Sensor-integrated seal start-ups are attracting venture capital in the USD 10-50 million range.

Future Market Outlook (2026-2034)

The gaskets and seals market forecast projects steady expansion from USD 70.0 Billion in 2025 to USD 94.6 Billion by 2034 at a CAGR of 3.2%, supported by EV adoption, industrial automation, aerospace recovery, and sustained aftermarket replacement demand across a growing global installed base.

Three technology discontinuities are most likely to reshape the market through 2034. EV-specific sealing will scale from niche to mainstream premium, commanding 15-25% of automotive seal revenue by 2030. PFAS-free and bio-based formulations will reach 30-40% of new launches in regulated markets. Sensor-integrated seals will create a recurring service-revenue layer in industrial applications.

By 2034, the gaskets and seals industry will have transitioned from a largely commoditised product economy to a more differentiated platform play, where material science, digital integration, and sustainability credentials drive competitive advantage. Leaders will be shaped by three strategic archetypes: diversified Tier-1s (Freudenberg, Parker, Trelleborg), specialty mechanical seal experts (Flowserve, John Crane), and regional champions.

Research Methodology

Primary Research

Primary research encompassed over 50 structured interviews conducted in 2024-2025 with sealing industry stakeholders including product managers at Tier-1 suppliers, automotive OEM purchasing leads, aerospace certification officers, industrial MRO specialists, and institutional investors. Primary insights validated market sizing, segmentation, and competitive positioning.

Secondary Research

Secondary sources include IEA Global EV Outlook, OICA vehicle production statistics, Boeing and Airbus order book publications, REACH and EPA regulatory documents, company annual reports, trade publications such as Sealing Technology and Fluid Sealing Association reports, and industry conference proceedings.

Forecasting Models

Market size estimations were derived using a combination of top-down and bottom-up models, incorporating vehicle production, industrial capex, aerospace deliveries, and historical evolution patterns. Scenario analysis (base, optimistic, conservative) was performed to account for commodity volatility and regulatory shifts.

Gaskets and Seals Market Report Coverage

|

Attribute |

Details |

|

Market Size (2025) |

USD 70.0 Billion |

|

Forecast Size (2034) |

USD 94.6 Billion |

|

CAGR (2026-2034) |

3.2% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Segmentation |

By Product (Seals, Gaskets); By End-Use (OEM, Aftermarket) |

|

Regional Analysis |

Asia Pacific, Europe, North America, Latin America, Middle East & Africa |

|

Key Companies |

Freudenberg Group, Parker Hannifin Corp, Trelleborg AB, SKF, Dana Limited, Tenneco Inc., Flowserve Corporation, Smiths Group plc, and ElringKlinger AG. |

|

Report Format |

PDF, Excel |

|

Customisation |

Available on request |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the gaskets and seals market from 2020-2034.

- The gaskets and seals market research report provides the latest information on the market drivers, challenges, and opportunities in the global market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the gaskets and seals industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Gaskets and Seals Market Report

The global gaskets and seals market was valued at USD 70.0 Billion in 2025, driven by automotive production, industrial automation, aerospace demand, and sustained aftermarket replacement cycles globally.

The market is projected to reach USD 94.6 Billion by 2034, growing at a CAGR of 3.2% during 2026-2034, driven by EV sealing demand, industrial automation, and aerospace recovery.

Seals lead with a 62.9% share in 2025, driven by broad deployment across rotary shafts, hydraulic pistons, and dynamic sealing interfaces in automotive, industrial, and aerospace applications.

OEM applications dominate with a 66.7% share in 2025, driven by first-fit demand across automotive assembly, industrial machinery production, and aerospace manufacturing volumes.

Asia Pacific leads with a 43.2% share in 2025, driven by China NEV production, Japan Tier-1 supply ecosystem, India automotive expansion, and ASEAN manufacturing growth momentum.

Key drivers include EV platform sealing demand (17M units in 2024), industrial automation (540K robots installed), aerospace backlog of 14,000 aircraft, and infrastructure capex expansion.

EV-specific sealing solutions are the fastest-growing sub-segment at 8-12% CAGR through 2034, driven by battery pack, e-axle, and thermal management applications in electric vehicles.

Leading companies include Freudenberg Group, Parker Hannifin Corp, Trelleborg AB, SKF, Dana Limited, Tenneco Inc., Flowserve Corporation, Smiths Group plc, and ElringKlinger AG globally.

Electrification drives demand for EV-specific seals in battery packs, e-axles, and thermal systems, with each EV requiring 20-30% more sealing components than comparable ICE vehicles.

PFAS restrictions in Europe and proposed US rules drive reformulation toward bio-based and PFAS-free elastomers, reaching 15-20% of new product launches in premium applications during 2024-2025.

Smart seals integrate sensors for wear, temperature, and leak detection, enabling predictive maintenance with documented savings of USD 2,000-8,000 per avoided unplanned equipment shutdown.

Aftermarket applications account for 33.3% of the market in 2025, covering replacement and MRO demand across a vehicle parc exceeding 1.5 billion units and industrial equipment globally.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade