GCC Artificial Intelligence Market Size, Share, Trends and Forecast by Type, Solutions, System, Technology, End Use Industry, and Country 2026-2034

GCC Artificial Intelligence Market Size, Share, Trends & Forecast (2026-2034)

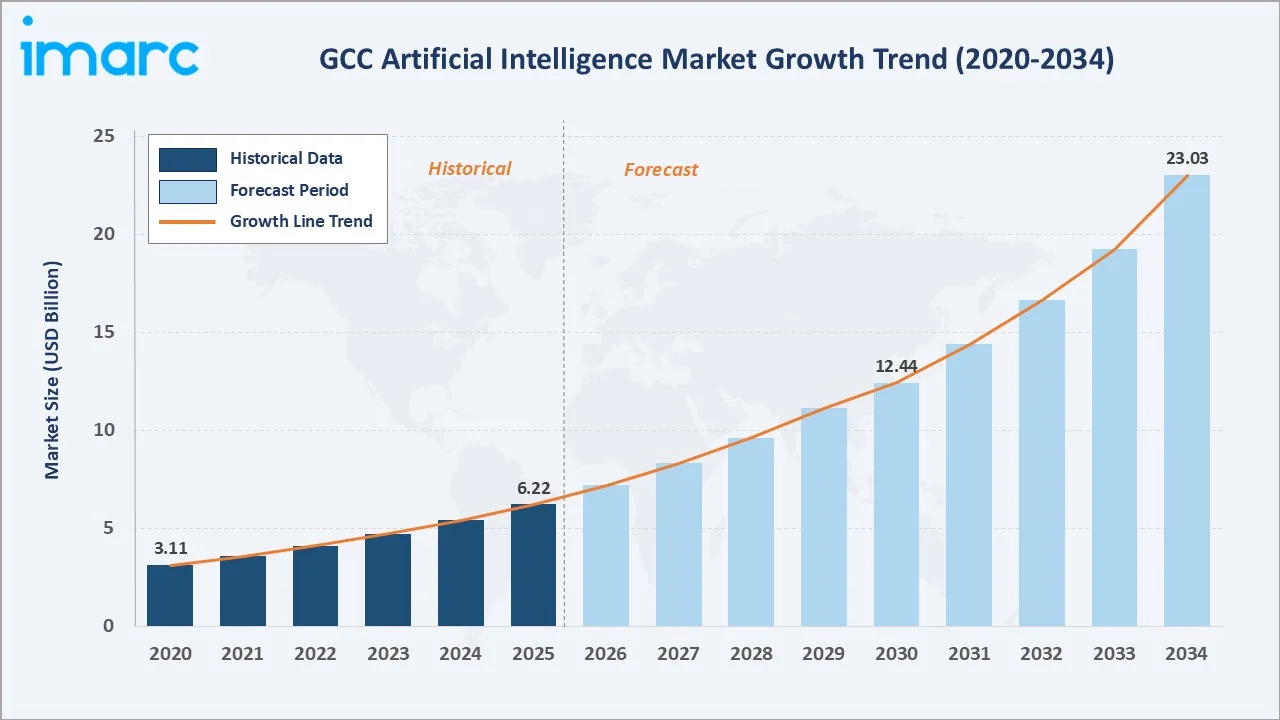

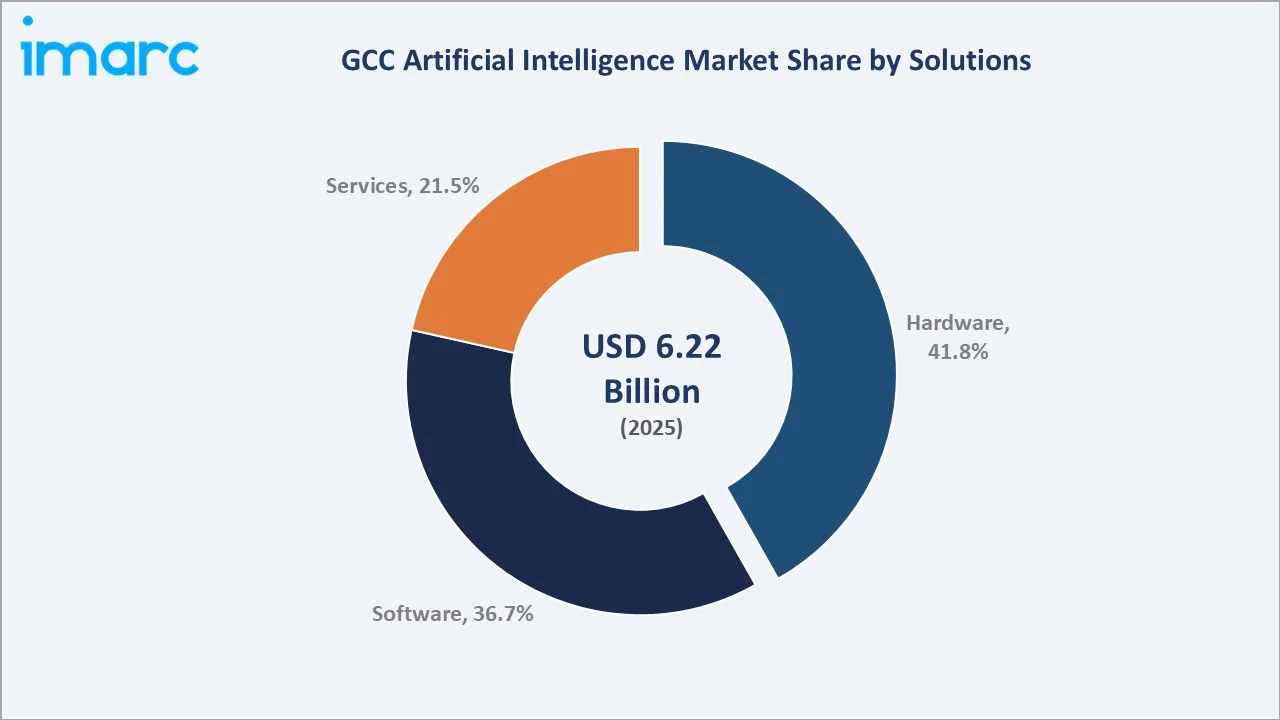

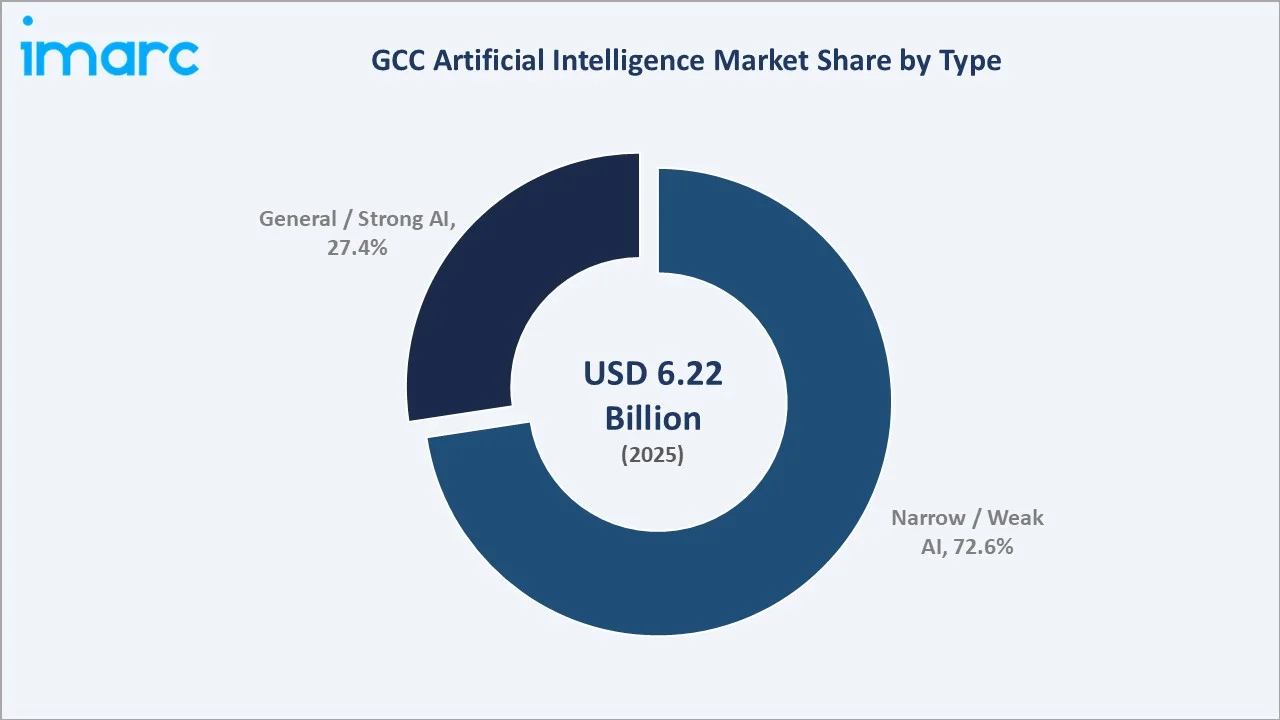

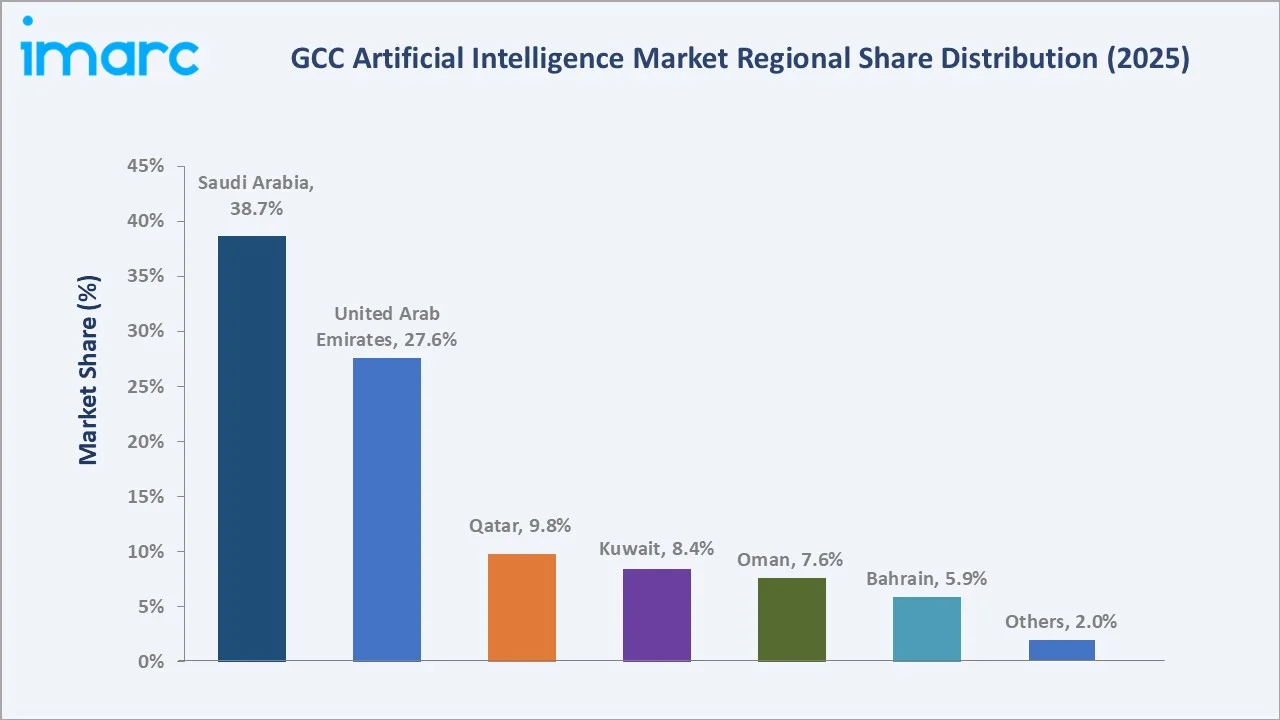

The GCC artificial intelligence market size was valued at USD 6.22 Billion in 2025 and is projected to reach USD 23.03 Billion by 2034, at a CAGR of 14.87% during 2026-2034. Rapid digital transformation initiatives, ambitious national AI strategies, and substantial government investment across Saudi Arabia and the UAE are collectively driving GCC artificial intelligence market growth. Hardware solutions dominate with a 41.8% share in 2025, while Narrow/Weak AI accounts for 72.6% of regional demand. Saudi Arabia leads regional demand with a 38.7% share in 2025.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 6.22 Billion |

|

Forecast Market Size (2034) |

USD 23.03 Billion |

|

CAGR (2026-2034) |

14.87% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Country |

Saudi Arabia (38.7% share, 2025) |

|

Fastest Growing Country |

United Arab Emirates |

|

Leading Solution |

Hardware (41.8%, 2025) |

|

Leading AI Type |

Narrow/Weak AI (72.6%, 2025) |

The chart illustrates GCC AI market growth from 2020–2034, with accelerating national AI strategies and digital investment programs driving both the historical expansion and forward projections.

To get more information on this market, Request Sample

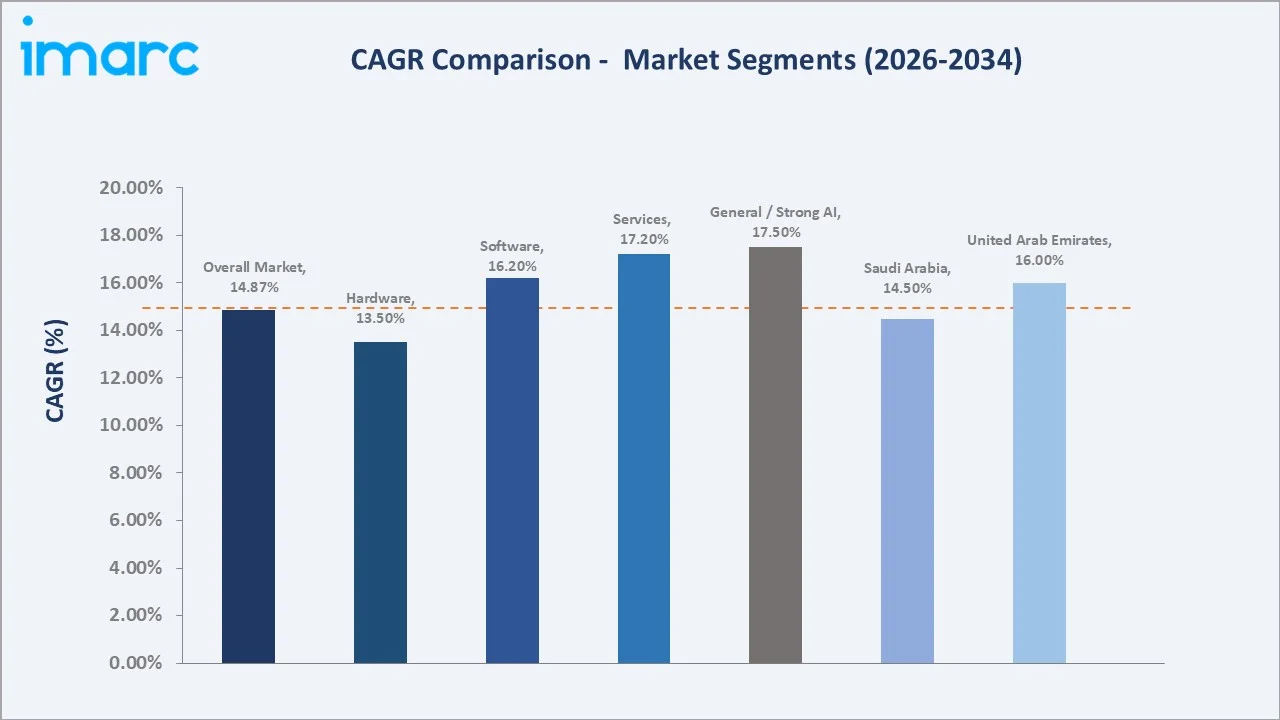

CAGR analysis identifies Hardware and Software solutions as the most structurally impactful segments, with Narrow AI maintaining dominance throughout the GCC artificial intelligence market forecast period through 2034.

Executive Summary

The GCC artificial intelligence market is rapidly expanding, driven by government-led digital initiatives, sovereign AI investments, and rising private sector adoption of automation. Valued at USD 6.22 billion in 2025, the market is forecast to reach USD 23.03 billion by 2034 at a 14.87% CAGR, supported by key policies like Saudi Arabia’s NSDAI and the UAE’s AI Strategy 2031.

Hardware dominates the solutions landscape with a 41.8% share in 2025, driven by investments in AI data centers, GPU clusters, and semiconductor infrastructure. Software holds 36.7% due to rising enterprise AI adoption, while services account for 21.5%, supported by demand for consulting and integration. Key sectors include BFSI, energy, healthcare, smart cities, and retail.

Saudi Arabia leads the market with a 38.7% share in 2025, driven by Vision 2030, NEOM, and SDAIA. The UAE holds 27.6%, supported by Dubai’s AI roadmap and Abu Dhabi’s TII initiatives. Qatar, Kuwait, Oman, and Bahrain together account for 31.7%, each advancing sector-specific AI adoption strategies across key industries.

Key Market Insights

|

Insight |

Data |

|

Largest Solutions Segment |

Hardware – 41.8% share (2025) |

|

Second Solutions Segment |

Software – 36.7% share (2025) |

|

Leading AI Type |

Narrow/Weak AI – 72.6% share (2025) |

|

Leading Country |

Saudi Arabia – 38.7% revenue share (2025) |

|

Second Country |

United Arab Emirates – 27.6% revenue share (2025) |

|

Top Companies |

Microsoft, Google Cloud, IBM, Amazon Web Services, SAP, Huawei |

Key Analytical Observations Supporting the Above Data:

- Hardware leads with a 41.8% share in 2025, driven by strong GCC investments in AI-ready data centers, hyperscale cloud infrastructure, and GPU-based computing to support sovereign AI development goals.

- Software holds a 36.7% share in 2025, driven by enterprise adoption of AI platforms, including NLP, machine learning frameworks, computer vision tools, and automation solutions across BFSI, healthcare, and energy sectors.

- Narrow/Weak AI leads with a 72.6% share, reflecting the region’s focus on task-specific, deployment-ready applications such as predictive analytics, robotic process automation, and computer vision, ahead of broader general AI adoption.

- Saudi Arabia's 38.7% regional dominance in 2025 reflects its status as the GCC's largest AI investment hub, anchored by SDAIA, the National Center for AI (NCAI), and marquee projects including NEOM's AI-integrated urban infrastructure.

- The UAE’s rapid AI growth is driven by Abu Dhabi’s Falcon LLM and G42’s expanding ecosystem, supported by strong national strategies and increasing global investments, positioning the country as a leading global AI hub.

- Hyperscaler investments in the GCC are rising, led by Microsoft’s multi-billion-dollar AI and cloud spending in the UAE, which includes $7.3 billion already deployed since 2023 and another $7.9 billion planned through 2029.

GCC Artificial Intelligence Market Overview

Artificial intelligence includes machine learning, NLP, computer vision, robotics, and decision systems enabling cognitive tasks. In the GCC, AI is used in smart cities, fraud detection, energy optimization, healthcare, and e-government. The ecosystem spans hardware providers, cloud firms, software vendors, integrators, regulators, and state-backed investors.

Macroeconomic diversification across GCC nations is accelerating AI investment beyond hydrocarbons, supported by strong government-led digital strategies. The UAE ranks among global leaders in ICT readiness and digital infrastructure, while a young, digitally active population strengthens AI adoption, creating a favourable environment for sustained market growth.

Market Dynamics

To evaluate market opportunities, Request Sample

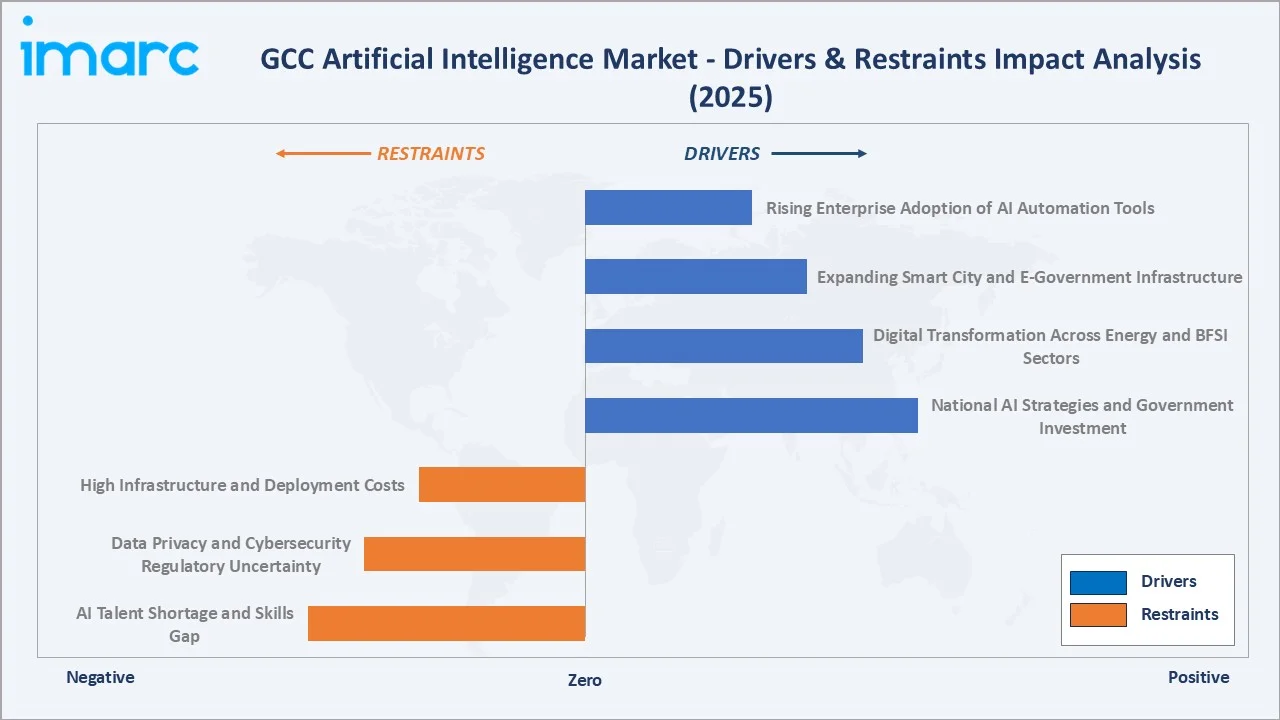

Market Drivers

- National AI Strategies and Government Investment: Saudi Arabia's NSDAI targets SAR 75 billion in AI investment by 2030, Saudi Arabia and the UAE are investing heavily in AI through national strategies (Vision 2030, UAE AI Strategy 2031), positioning AI as a key economic diversification driver in the GCC.

- Digital Transformation Across Energy and BFSI Sectors: GCC energy leaders like Saudi Aramco and ADNOC deploy AI for predictive maintenance, optimization, and analytics, accelerating enterprise AI demand.

- Expanding Smart City and E-Government Infrastructure: Smart city projects including NEOM, Masdar City, and Dubai are embedding AI into urban mobility, energy management, water systems, and public safety. These projects demand integrated AI hardware and software platforms at scale.

- Rising Enterprise Adoption of AI Automation Tools: GCC enterprises in retail, logistics, healthcare, and telecommunications are adopting AI-powered automation, NLP-driven chatbots, and predictive analytics, driving Software and Services segment demand across both multinational and regional organizations.

Market Restraints

- AI Talent Shortage and Skills Gap: GCC countries face shortages of AI and data science talent, with demand exceeding supply, slowing AI adoption despite strong hiring growth in markets like the UAE and Saudi Arabia.

- Data Privacy and Cybersecurity Regulatory Uncertainty: Evolving regulations like Saudi Personal Data Protection Law and UAE Federal Data Protection Law increase compliance complexity, slowing AI adoption in regulated sectors.

- High Infrastructure and Deployment Costs: Building sovereign AI-grade data centers and procuring advanced GPU clusters requires substantial capital expenditure. For SMEs and smaller GCC government entities, cost barriers to AI infrastructure deployment remain a market constraint.

Market Opportunities

- Arabic NLP and Localized AI Model Development: Growing demand for Arabic-language AI models presents opportunities, with initiatives like Technology Innovation Institute (Falcon) and Saudi Data and AI Authority advancing localized NLP solutions.

- AI in Oil and Gas Optimization: AI adoption in GCC oil and gas—led by Saudi Aramco and ADNOC—is expanding across predictive maintenance, reservoir modeling, and operations optimization, offering strong long-term growth potential.

- Healthcare AI and Digital Health Expansion: GCC governments are investing in AI-powered diagnostic imaging, clinical decision support, and remote patient monitoring. Saudi Vision 2030 healthcare commitments include AI-driven hospital management systems, creating significant near-term market expansion opportunities.

Market Challenges

- AI Governance and Ethical Framework Gaps: AI adoption in GCC is advancing faster than regulatory frameworks, with evolving guidelines on ethics, transparency, and accountability creating uncertainty for enterprises, especially in regulated sectors.

- Dependence on International Technology Vendors: The GCC remains heavily reliant on international AI hardware suppliers (NVIDIA, Intel) and hyperscale cloud platforms (AWS, Microsoft Azure, Google Cloud), creating supply chain vulnerability and sovereignty concerns.

- Integration Complexity Across Legacy Systems: Legacy IT systems across GCC enterprises and governments create integration challenges for AI deployment, increasing implementation time, costs, and complexity in sectors using ERP and industrial systems.

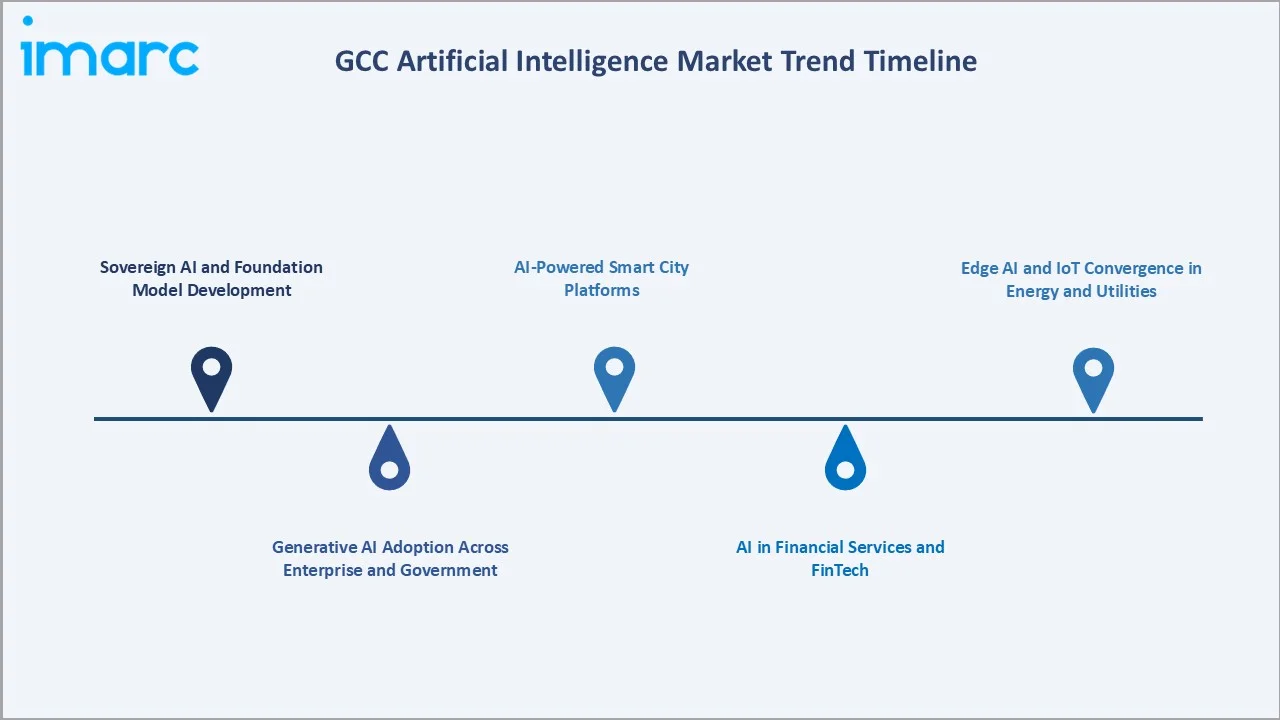

Emerging Market Trends

1. Sovereign AI and Foundation Model Development

GCC countries are advancing sovereign AI through local model development. The UAE’s Falcon LLM by Technology Innovation Institute ranks among leading open-source models, while Saudi and Qatar institutions are expanding national AI research capabilities.

2. Generative AI Adoption Across Enterprise and Government

Generative AI adoption is accelerating across GCC enterprises and governments. McKinsey & Company estimates generative AI could add USD 20–35 billion annually to regional economies, driving demand for AI-enabled software, automation, and productivity solutions.

3. AI-Powered Smart City Platforms

NEOM's AI-integrated urban operating system and Dubai's AI-driven traffic and safety management represent flagship regional smart city AI deployments. These platforms create deep integration between computer vision, IoT sensor networks, and decision-intelligence systems at city scale.

4. AI in Financial Services and FinTech

AI adoption in GCC financial services is rising across fraud detection, credit scoring, and compliance. Saudi Arabia’s fintech ecosystem, supported by Saudi Central Bank (SAMA), continues expanding, with strong regulatory backing for digital and AI-driven banking innovation.

5. Edge AI and IoT Convergence in Energy and Utilities

Deployment of edge AI hardware in oil fields, desalination plants, and power grid monitoring is accelerating across the GCC. Saudi Aramco and DEWA are deploying edge AI sensors capable of real-time anomaly detection and autonomous process control, reducing both downtime and operational costs.

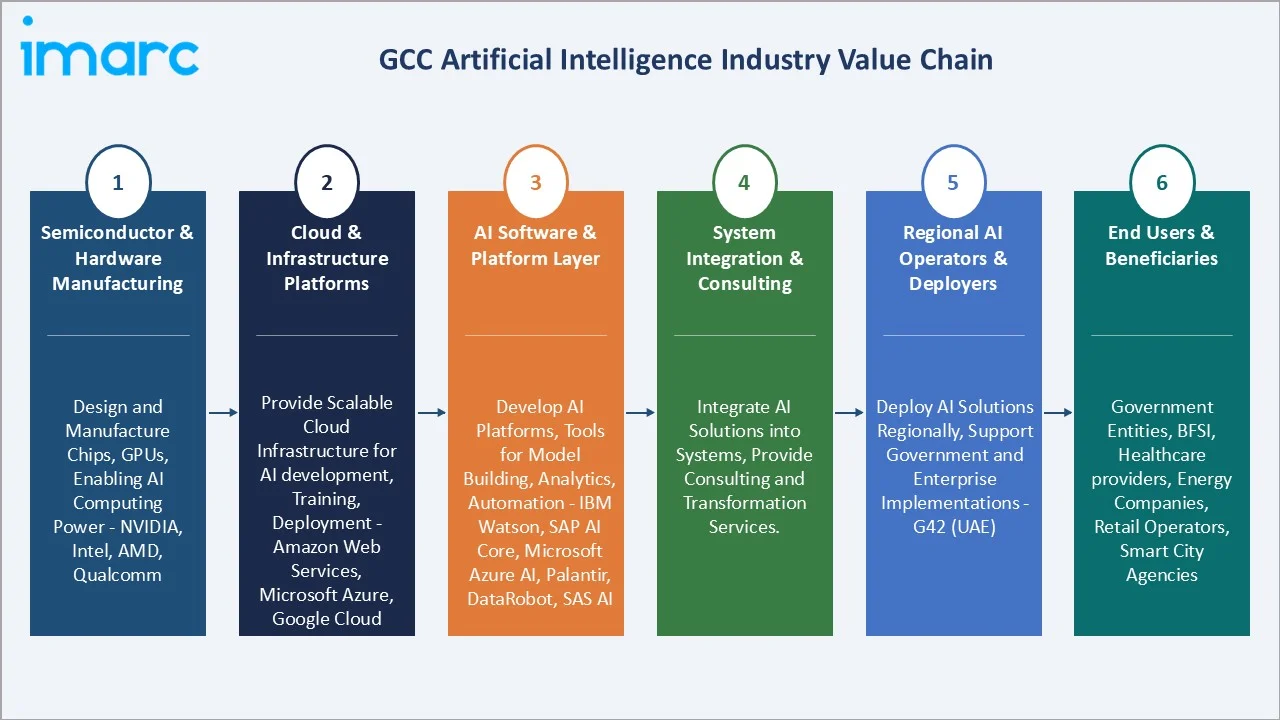

Industry Value Chain Analysis

The GCC AI industry value chain spans six stages, from semiconductor hardware manufacturing to end-user AI application deployment, each characterized by distinct competitive dynamics and margin structures.

|

Stage |

Key Players / Examples |

|

Semiconductor & Hardware Manufacturing |

NVIDIA, Intel, AMD, Qualcomm, Huawei HiSilicon – GPU clusters, AI chips, edge hardware |

|

Cloud & Infrastructure Platforms |

Amazon Web Services, Microsoft Azure, Google Cloud, Alibaba Cloud, Oracle Cloud – hyperscale AI infrastructure |

|

AI Software & Platform Layer |

IBM Watson, SAP AI Core, Microsoft Azure AI, Palantir, DataRobot, SAS AI |

|

System Integration & Consulting |

Accenture, Deloitte, PwC, IBM GBS, Wipro, Infosys – AI deployment and transformation services |

|

Regional AI Operators & Deployers |

G42 (UAE), SDAIA, STCAI, e&, STC, Etisalat – sovereign and enterprise AI projects |

|

End Users & Beneficiaries |

Government entities, BFSI, healthcare providers, energy companies, retail operators, smart city agencies |

Hyperscale cloud and data center providers dominate GCC AI value due to control over compute infrastructure. However, regional players like G42 and Saudi Data and Artificial Intelligence Authority (SDAIA) are emerging as key intermediaries enabling localized, sovereign AI deployment.

Technology Landscape in the GCC AI Industry

Natural Language Processing and Arabic Language AI

NLP is a key growth area in the GCC, driven by rising demand for Arabic-language AI. Initiatives like Technology Innovation Institute’s Falcon LLM (2023) accelerated regional model development, with increasing Arabic AI deployments across government, education, and customer service use cases.

Machine Learning and Predictive Analytics

Machine learning adoption is expanding across GCC industries for predictive analytics and optimization. Saudi Aramco uses AI-driven reservoir modeling to enhance forecasting and efficiency, supporting broader enterprise adoption, though specific ROI figures vary across applications and are not consistently disclosed.

Computer Vision and Smart Surveillance

Computer vision solutions for facial recognition, traffic management, crowd analysis, and industrial inspection are among the most actively deployed AI applications across GCC smart city and security programs. Dubai Police, Abu Dhabi smart city, and NEOM's autonomous surveillance systems are major adopters.

Context-Aware Computing and Autonomous Systems

The GCC is advancing autonomous systems through smart mobility and automation initiatives. NEOM’s autonomous mobility projects and UAE drone programs, supported by regulatory sandboxes, are accelerating AI deployment in logistics, robotics, and financial process automation across the region.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Narrow/Weak Artificial Intelligence |

72.6% |

2025 |

|

Solutions |

Hardware |

41.8% |

2025 |

|

System |

Intelligence Systems |

🔒 |

2025 |

|

Technology |

Machine Learning |

🔒 |

2025 |

|

End Use Industry |

Construction and Manufacturing |

🔒 |

2025 |

|

Country |

Saudi Arabia |

38.7% |

2025 |

By Solutions

Hardware holds a 41.8% share in 2025, driven by expanding data centers, GPU clusters, and AI-optimized servers backed by GCC sovereign investments. Projects like NEOM and Abu Dhabi cloud infrastructure are key demand drivers, with growth aligned to rising compute-intensive AI workloads.

To access detailed market analysis, Request Sample

Software accounts for 36.7% in 2025, driven by enterprise adoption of AI platforms, NLP tools, machine learning, and generative AI, with strong demand from government e-services and defence. Services represent 21.5% in 2025, led by AI consulting, integration, managed services, and AI-as-a-service offerings.

By Type

Narrow/Weak AI commands a 72.6% share in 2025, driven by widespread deployment of task-specific solutions such as chatbots, image recognition, fraud detection, and predictive maintenance across energy, BFSI, and government sectors, reflecting a strong focus on practical, ROI-driven AI adoption.

General/Strong AI accounts for 27.4% in 2025, reflecting strong government-led investment in advanced AI research. Institutions like Technology Innovation Institute and KACST are driving large-scale development of next-generation AI capabilities.

Regional Market Insights

|

Country |

Share (2025) |

Key Growth Drivers |

|

Saudi Arabia |

38.7% |

NSDAI, NEOM, Vision 2030, SDAIA establishment, Aramco AI programs, smart city infrastructure |

|

United Arab Emirates |

27.6% |

UAE AI Strategy 2031, G42, TII Falcon LLM, Dubai Smart City, FinTech AI adoption |

|

Qatar |

9.8% |

QF Research, Qatar National Vision 2030, smart infrastructure, World Cup AI legacy investment |

|

Kuwait |

8.4% |

Kuwait Vision 2035, e-government AI services, BFSI AI adoption, energy optimization programs |

|

Oman |

7.6% |

Digital Oman Strategy, Oman Vision 2040, smart city Muscat, port logistics AI |

|

Bahrain |

5.9% |

Bahrain Economic Vision 2030, FinTech AI hub, cloud-first government policy, TrustedCloud initiative |

|

Others |

2.0% |

Cross-border GCC AI initiatives and spillover deployment from larger markets |

Saudi Arabia commands a 38.7% share of the GCC AI market in 2025, supported by strong sovereign investments, SDAIA’s national AI mandate, and large-scale projects like NEOM. AI initiatives by Saudi Aramco and STC further expand adoption across energy, telecom, and digital infrastructure sectors.

The UAE holds 27.6% in 2025 and is the fastest-growing GCC AI market, driven by strong investments from G42 and Technology Innovation Institute, including globally competitive AI models. Dubai’s AI roadmap is accelerating public sector demand. Qatar accounts for 9.8%, supported by advanced smart infrastructure and Qatar Foundation’s research ecosystem, strengthening innovation capacity.

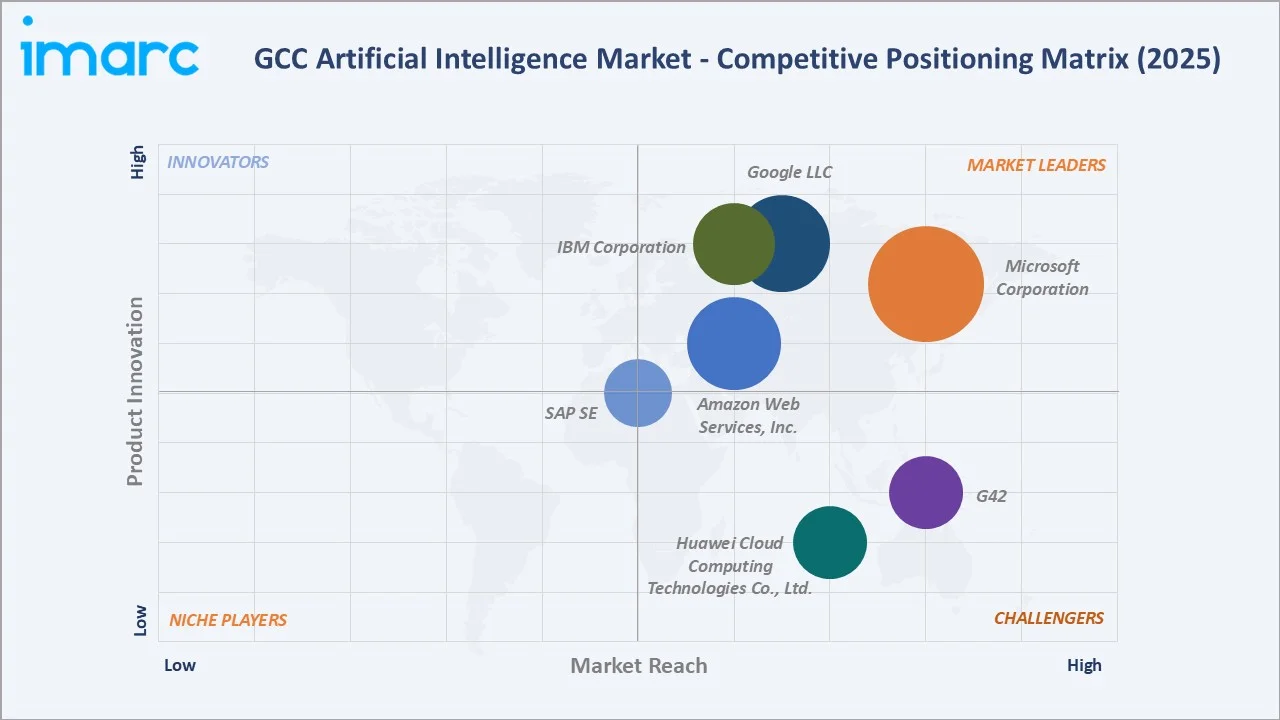

Competitive Landscape

|

Company Name |

Key Brand / Platform |

Market Position |

Core Strength |

|

Microsoft Corporation |

Azure AI / Copilot |

Leader |

Hyperscale cloud AI, enterprise software, GCC data center investment |

|

Google LLC (Alphabet Inc.) |

Google Cloud AI / Gemini |

Leader |

AI research leadership, cloud AI services, NLP and vision APIs |

|

Amazon Web Services, Inc. |

Amazon Bedrock |

Leader |

Cloud infrastructure, ML platform, GCC hyperscale data centers |

|

IBM Corporation |

IBM Watsonx |

Leader |

Enterprise AI, BFSI and government, consulting-led deployment |

|

G42 |

Core42 |

Leader |

UAE sovereign AI, foundation models, hyperscale infrastructure |

|

Huawei Cloud Computing Technologies Co., Ltd. |

Huawei Cloud |

Challenger |

AI hardware, smart city solutions, Huawei Cloud GCC expansion |

|

SAP SE |

SAP BTP AI |

Challenger |

Enterprise AI integration, ERP-embedded AI, manufacturing sector |

The GCC AI market is led by global hyperscalers like Microsoft, AWS, and Google Cloud through strategic government partnerships. G42 acts as a sovereign AI infrastructure leader, supported by major data center projects and global collaborations, strengthening the UAE’s regional AI leadership.

Key Company Profiles

Microsoft Corporation

Microsoft Corporation, headquartered in Redmond, is a global leader in cloud and AI, expanding rapidly in the GCC through Azure infrastructure and partnerships like G42, supporting sovereign AI adoption and enterprise-scale generative AI deployments across government and regulated industries.

- Product & Service Portfolio: Microsoft’s AI portfolio includes Azure AI Services, Azure OpenAI Service, Microsoft Copilot (including GitHub and Microsoft 365 Copilot), Power Platform AI, and enterprise AI tools for vision, speech, language, and generative AI applications.

- Recent Developments: In April 2024, Microsoft announced a $1.5 billion strategic investment in UAE-based AI firm G42, acquiring a minority stake and board representation. The partnership aims to expand Azure-powered AI solutions across the Middle East, Central Asia, and Africa while strengthening global AI infrastructure.

- Strategic Focus: Microsoft focuses on cloud AI infrastructure leadership, enterprise AI platform adoption, and sovereign AI partnerships with GCC governments through Azure Government and national AI strategy alignments.

Google LLC (Alphabet Inc.)

Google LLC, via Google Cloud, is a leading AI and hyperscale cloud provider in the GCC, expanding through Saudi Arabia’s Dammam region and AI hub initiatives, supporting sovereign AI, data localization, and enterprise adoption of Gemini and Vertex AI platforms.

- Product & Service Portfolio: Google Cloud AI, Vertex AI, Gemini (LLM), Google Workspace AI, TensorFlow, and BigQuery ML.

- Recent Developments: In November 2023, Google Cloud officially launched its Dammam (Saudi Arabia) cloud region, delivering high-performance, low-latency cloud and AI services to public and private sector users, while supporting Saudi Arabia’s Vision 2030 digital transformation and AI-driven innovation initiatives.

- Strategic Focus: Google focuses on AI research leadership, open-source model ecosystems, cloud-native AI deployment, and enterprise AI adoption through its GCC channel partner network.

Amazon Web Services, Inc.

Amazon Web Services (AWS) is a leading hyperscale cloud and AI provider in the GCC, operating regional data centers in Bahrain and the UAE, while expanding in Saudi Arabia to support sovereign cloud, low-latency AI workloads, and large-scale enterprise adoption.

- Product & Service Portfolio: AWS offers AI services including Amazon Bedrock, SageMaker, Rekognition, Comprehend, Lex, Polly, Textract, and Transcribe, enabling enterprises in the GCC to build, train, and deploy machine learning and generative AI applications at scale.

- Recent Developments: In November 2025, AWS signed a multi-year strategic collaboration with Zero&One to accelerate cloud and AI adoption across Saudi enterprises, focusing on modernization, migration to AWS cloud, and scaling enterprise AI use cases aligned with Vision 2030.

- Strategic Focus: AWS focuses on expanding sovereign cloud infrastructure in Saudi Arabia and the UAE, enabling multi-model generative AI via Bedrock, and building regional partnerships to scale enterprise AI adoption across government and industry sectors in the GCC.

Market Concentration Analysis

The GCC AI market is moderately concentrated at the platform level, with Microsoft, Amazon Web Services, and Google Cloud contributing around 40–45% of cloud AI revenue in 2025. At the hardware level, NVIDIA dominates AI GPU supply, leading to near-monopolistic concentration in AI compute infrastructure.

Market fragmentation is high at the services layer, with a broad base of AI firms and consultancies across the GCC. Innovation hubs like Hub71 and Saudi-led AI initiatives are accelerating competition in niches such as Arabic NLP, energy AI, and smart logistics.

Consolidation dynamics are emerging through strategic acquisitions and government-mandated technology partnerships. Saudi Aramco's Wa'ed Ventures, Abu Dhabi's ADQ, and Mubadala Investment Company are actively deploying venture capital into AI platform companies, seeking to build sovereign AI value chains that reduce regional dependence on international AI infrastructure providers.

Investment & Growth Opportunities

Fastest-Growing Segments

AI services (consulting, managed AI, AI-as-a-service) are among the fastest-growing segments in the GCC, driven by strong enterprise demand for AI deployment support across banking, healthcare, and government sectors facing talent gaps.

Arabic NLP and localized generative AI solutions represent a high-growth opportunity, supported by government digital mandates and increasing demand for Arabic-language AI applications across public services and consumer platforms.

Emerging Market Opportunities

Healthcare AI is a key opportunity area in the GCC, supported by large-scale healthcare modernization initiatives and growing adoption of AI in diagnostics, clinical decision support, and remote care systems.

Oman and Bahrain present emerging AI opportunities due to ongoing national digital strategies and cloud adoption policies, creating early-stage demand for AI infrastructure and enterprise AI deployment.

Venture & Strategic Investment Trends

AI startup activity in the GCC is increasing, with growing funding momentum and strong backing from sovereign wealth funds such as PIF, ADQ, and Mubadala, alongside international investors.

Future Market Outlook (2026-2034)

The GCC artificial intelligence market is positioned for sustained double-digit expansion through 2034, with the market projected to grow from USD 6.22 billion in 2025 to USD 23.03 billion at a 14.87% CAGR. Saudi Arabia and the UAE will remain the twin growth engines, with combined share expected to hold above 60% through the forecast period. Qatar, Kuwait, and Oman are projected to increase their collective share as national AI programs mature.

Technological disruption will be most pronounced in generative AI adoption, Arabic foundation model proliferation, and autonomous system deployment. GCC governments' proactive regulatory frameworks including the UAE's AI governance guidelines and Saudi Arabia's AI ethics framework are expected to accelerate enterprise AI deployment by providing deployment certainty.

The GCC AI market is set for strong long-term growth, driven by national AI strategies and digital transformation programs. Saudi Arabia and United Arab Emirates are investing heavily across smart cities, energy, and financial services, supporting sustained multi-billion-dollar AI demand through 2030.

Research Methodology

Primary Research

Primary research for the GCC AI market included structured interviews with 120+ industry stakeholders, including AI technology vendors, sovereign AI program directors, enterprise AI deployment leads, GCC government digitalization officials, and academic AI research institutions. Quantitative surveys were conducted across 6 GCC nations to validate segmentation data and growth assumptions.

Secondary Research

Secondary research encompassed analysis of 300+ sources, including GCC government AI strategy documents, annual reports of leading AI vendors, national statistics authority publications, World Bank ICT development data, GSMA Intelligence reports, and AI industry databases including Gartner, IDC, and Forrester.

Forecasting Models

Market forecasts employed a hybrid bottom-up and top-down quantitative model, calibrating GCC-specific AI expenditure drivers including government IT budget allocations, private sector digital transformation investment, and AI talent deployment rates. All forecast values are in USD and represent total addressable market (TAM) estimates across hardware, software, and services segments.

GCC Artificial Intelligence Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Narrow/Weak Artificial Intelligence, General/Strong Artificial Intelligence |

| Solutions Covered | Hardware, Software, Service |

| Systems Covered | Intelligence Systems, Decision Support Processing, Hybrid Systems, Fuzzy Systems |

| Technologies Covered | Natural Language Processing, Machine Learning, Computer Vision, Context-Aware Computing, Others |

| End Use Industries Covered | Banking, Financial Services and Insurance (BFSI), Technology, Media and Telecommunication, Transportation and Logistics, Energy, Mining and Utilities, Retail and Wholesale Trade, Construction and Manufacturing, Education and Healthcare, Others |

| Countries Covered | United Arab Emirates, Saudi Arabia, Oman, Qatar, Kuwait, Bahrain |

| Companies Covered | Microsoft Corporation, Google LLC (Alphabet Inc.), Amazon Web Services, Inc., IBM Corporation, G42, Huawei Cloud Computing Technologies Co., Ltd., SAP SE, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the GCC Artificial Intelligence Market Report

The GCC AI market was valued at USD 6.22 Billion in 2025, driven by national AI strategies, hyperscaler investment, and enterprise digital transformation programs across the six GCC nations.

The GCC AI market is projected to reach USD 23.03 Billion by 2034, growing at a CAGR of 14.87% during 2026-2034, driven by sustained government AI investment and enterprise adoption.

The GCC artificial intelligence market is forecast to grow at 14.87% CAGR from 2026 to 2034, well above the global AI market average, supported by concentrated sovereign AI investment programs.

Saudi Arabia leads the GCC AI market with a 38.7% share in 2025, underpinned by SDAIA, Vision 2030 AI mandates, and Saudi Aramco's large-scale AI deployment programs.

Key drivers include national AI strategies (UAE AI Strategy 2031), smart city investments, energy sector AI adoption, BFSI digitalization, and sovereign AI infrastructure development.

Hardware holds the largest solutions share at 41.8% in 2025, reflecting significant GCC investment in AI data centers, GPU clusters, and AI-optimized computing infrastructure.

Narrow/Weak AI accounts for 72.6% of GCC AI demand in 2025, encompassing task-specific applications including NLP chatbots, predictive analytics, computer vision, and fraud detection systems.

Leading players include Microsoft Corporation, Google LLC, Amazon Web Services, Inc., IBM Corporation, G42, Huawei Cloud Computing Technologies Co., Ltd., and SAP SE. G42 is the dominant sovereign AI operator in the GCC region.

The GCC AI industry is defined by high government investment concentration, sovereign AI development ambitions, Arabic NLP gaps, and increasing hyperscaler competition for regional cloud AI infrastructure contracts.

Key trends include sovereign AI model development (Falcon LLM), generative AI enterprise adoption, edge AI in energy, Arabic NLP, AI-powered smart cities, and healthcare AI platform deployment.

Growth opportunities include AI services, Arabic generative AI tools, healthcare AI platforms, Oman and Bahrain market entry, and AI-integrated energy optimization solutions within GCC oil and gas sectors.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)