GCC Construction Waste Management Market Size, Share, Trends and Forecast by Disposal Method, Service, Material, and Country, 2026-2034

GCC Construction Waste Management Market Size, Share, Trends & Forecast (2026-2034)

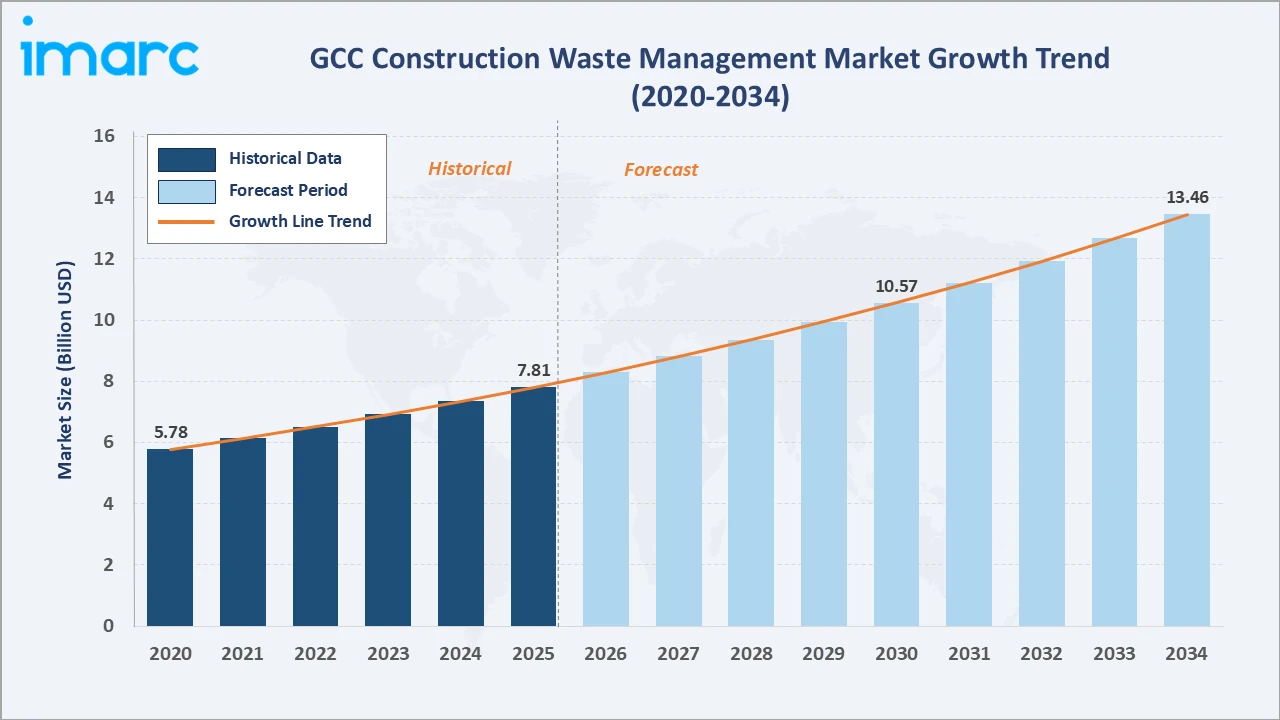

The GCC construction waste management market reached USD 7.81 Billion in 2025 and is projected to reach USD 13.46 Billion by 2034, growing at a CAGR of 6.23% during 2026-2034. Rapid expansion of construction activities under Vision 2030, rising environmental consciousness, development of smart cities, launch of advanced waste management technologies, and growing public-private partnerships are the primary growth catalysts.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 7.81 Billion |

|

Forecast Market Size (2034) |

USD 13.46 Billion |

|

CAGR (2026-2034) |

6.23% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

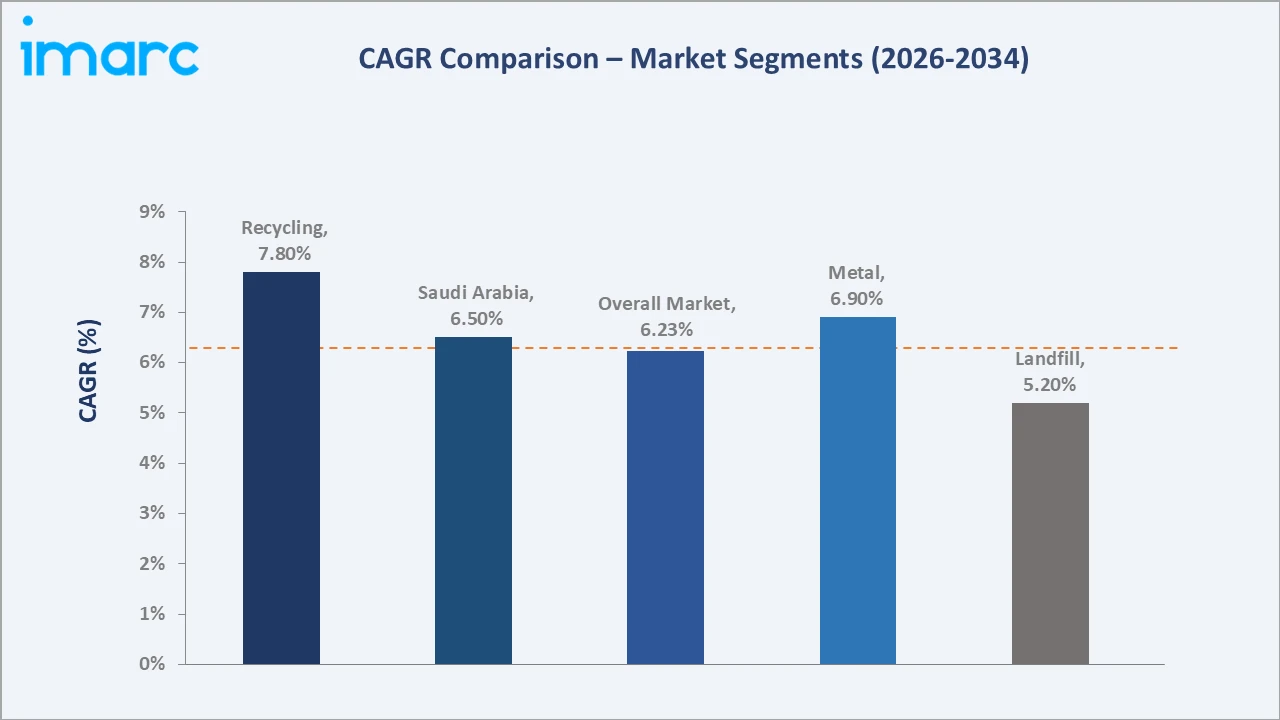

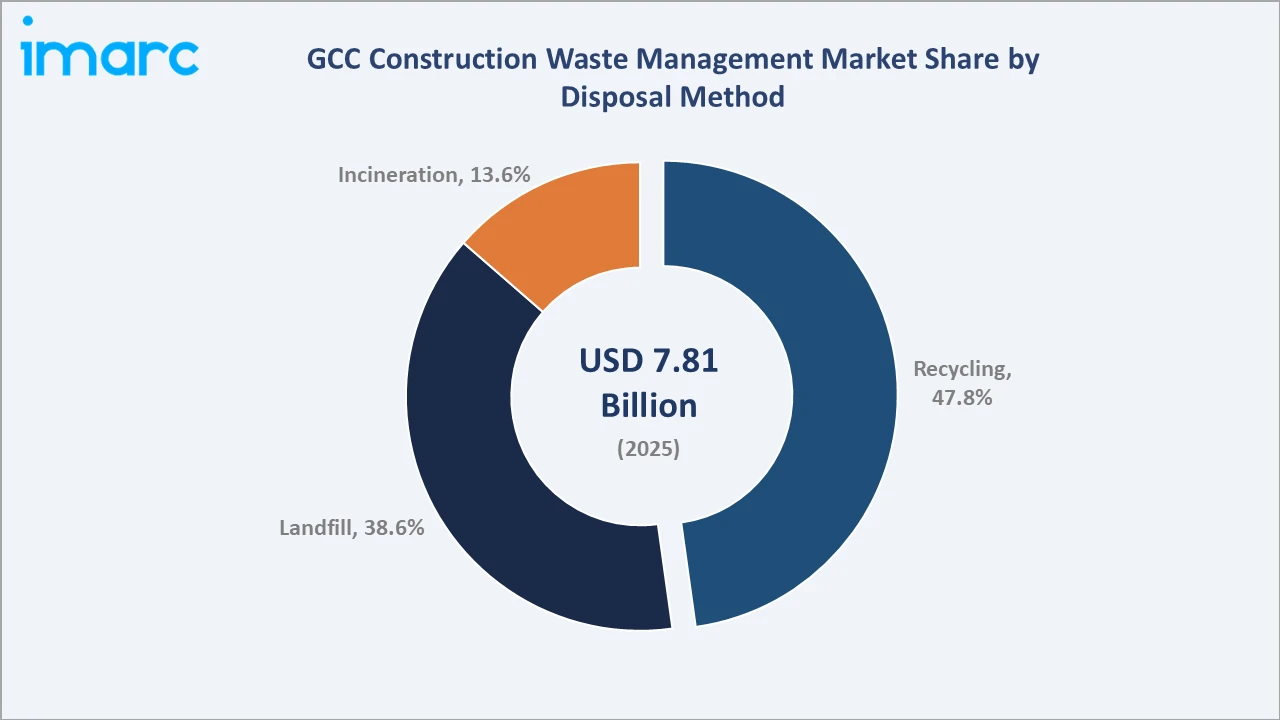

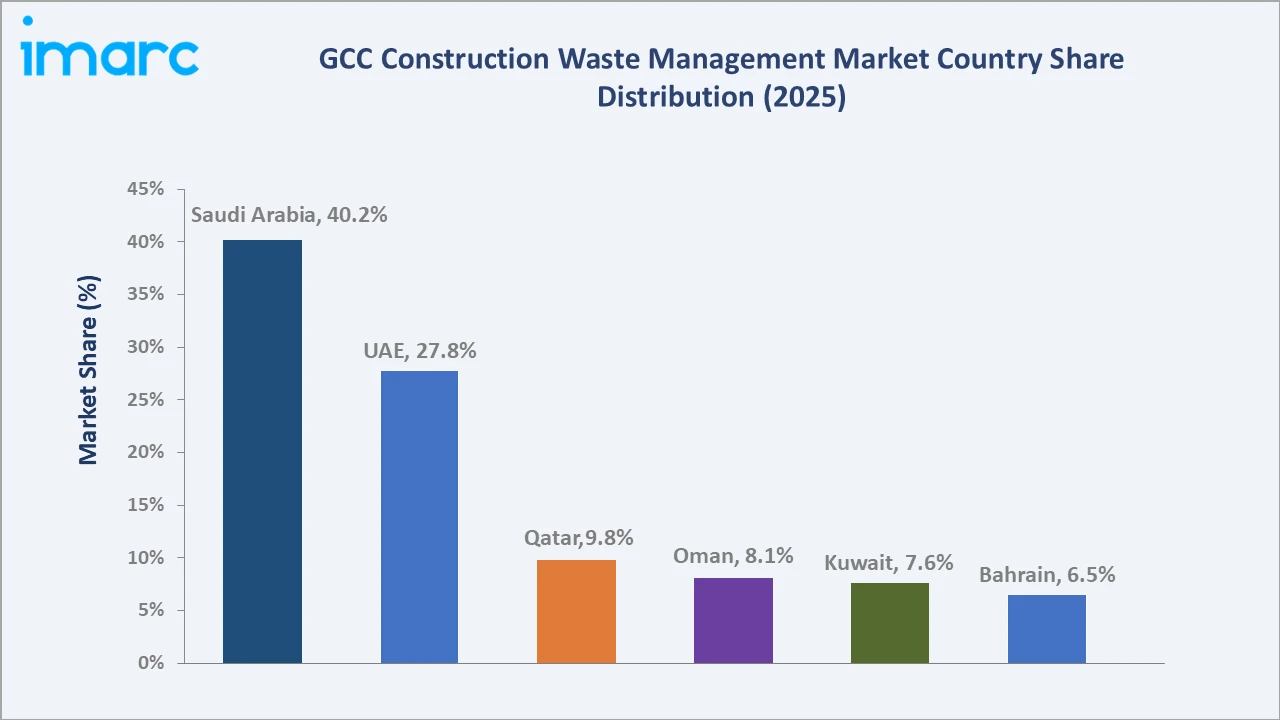

Saudi Arabia leads regionally, holding a 40.2% market share in 2025, driven by Vision 2030 mega-projects including NEOM, the Red Sea Project, and Qiddiya. Recycling dominates the disposal method segment at 47.8%, while metal constitutes the largest materials segment at a 24.8% share in 2025.

To get more information on this market, Request Sample

The GCC's construction waste management market is underpinned by three structural forces: the region's massive infrastructure buildout under national vision programs, increasingly stringent environmental regulation mandating certified waste disposal, and the financial viability of recycling driven by rising raw material costs.

Executive Summary

The GCC construction waste management market is experiencing accelerated expansion, driven by the convergence of unprecedented infrastructure investment, government-enforced sustainability mandates, and technological advancement in waste processing. The market was valued at USD 7.81 Billion in 2025 and is forecast to reach USD 13.46 Billion by 2034, growing at a CAGR of 6.23%.

This growth trajectory is anchored by the GCC mega-project pipeline valued at over USD 2 trillion through 2035, generating substantial volumes of concrete, metal, plastic, and mixed construction waste requiring certified management.

Recycling-based disposal commands the largest share at 47.8% in 2025, encompassing material recovery operations for metals, concrete aggregates, plastics, and glass. Landfill disposal accounts for 38.6%, though regulatory tightening across Saudi Arabia, UAE, and Qatar is progressively reducing this share as recycling capacity expands.

Saudi Arabia leads regionally at 40.2%, anchored by Vision 2030's mega-project pipeline and the Kingdom's National Waste Management Center's regulatory framework. UAE follows at 27.8%, driven by UAE Net Zero 2050 targets and Dubai's zero-landfill ambitions. Leading players collectively dominate the market through integrated waste management platforms.

Key Market Insights

|

Insight |

Data |

|

Largest Disposal Method |

Recycling – 47.8% share (2025) |

|

Fastest Growing Disposal Method |

Recycling – ~7.8% CAGR (2026-2034) |

|

Largest Materials |

Metal – 24.8% share (2025) |

|

Leading Country |

Saudi Arabia – 40.2% share (2025) |

|

Top Companies |

Averda, Veolia Environnement SA, Imdaad LLC, Beeah Group |

Key Analytical Observations Supporting The Above Data:

- Recycling accounts for 47.8% of GCC construction waste disposal in 2025. This dominance reflects the region's progressive regulatory framework, with Saudi Arabia, UAE, and Qatar all having introduced mandatory recycling targets for construction and demolition waste as part of their national environmental strategies.

- Metal's 24.8% share is the highest across all materials in 2025, underpinned by the GCC's steel-intensive construction methodology involving structural steel frames, rebar, and metal cladding. Metal's high residual value makes it the most economically attractive recyclate, commanding consistent demand from regional steel mills and scrap metal processors.

- Saudi Arabia's 40.2% regional share (2025) reflects the Kingdom's status as the GCC's largest construction market, with ongoing mega-projects including NEOM (USD 500+ Billion), the Red Sea Project, and Diriyah Gate generating tens of millions of tons of construction waste annually requiring certified management.

- UAE's 27.8% share (2025) is driven by Dubai's and Abu Dhabi's advanced regulatory frameworks, including Dubai's zero-waste-to-landfill policy and Abu Dhabi's Estidama sustainability rating system, both of which mandate progressive waste diversion in construction projects.

GCC Construction Waste Management Market Overview

Construction waste management encompasses the planning, collection, transportation, sorting, processing, recycling, and compliant disposal of waste materials generated during construction, renovation, and demolition activities. In the GCC context, the market spans a comprehensive value chain serving residential and commercial construction, large-scale infrastructure projects (highways, airports, seaports), and mega-development initiatives under national vision programs.

Macroeconomic drivers include the GCC construction market, which is projected to grow at 4.70% from 2026 to 2034, and government mandates under Saudi Arabia's Vision 2030, UAE's Net Zero 2050, and Qatar's National Environment and Climate Change Strategy (NECCS). Tipping fee structures in the UAE and Saudi Arabia, landfill diversion targets, and green building rating systems (LEED, Estidama, Green Mark) are compelling contractors to upgrade from ad-hoc waste disposal to certified management systems that provide digital compliance certificates required for project completion and green building ratings.

Market Dynamics

To evaluate market opportunities, Request Sample

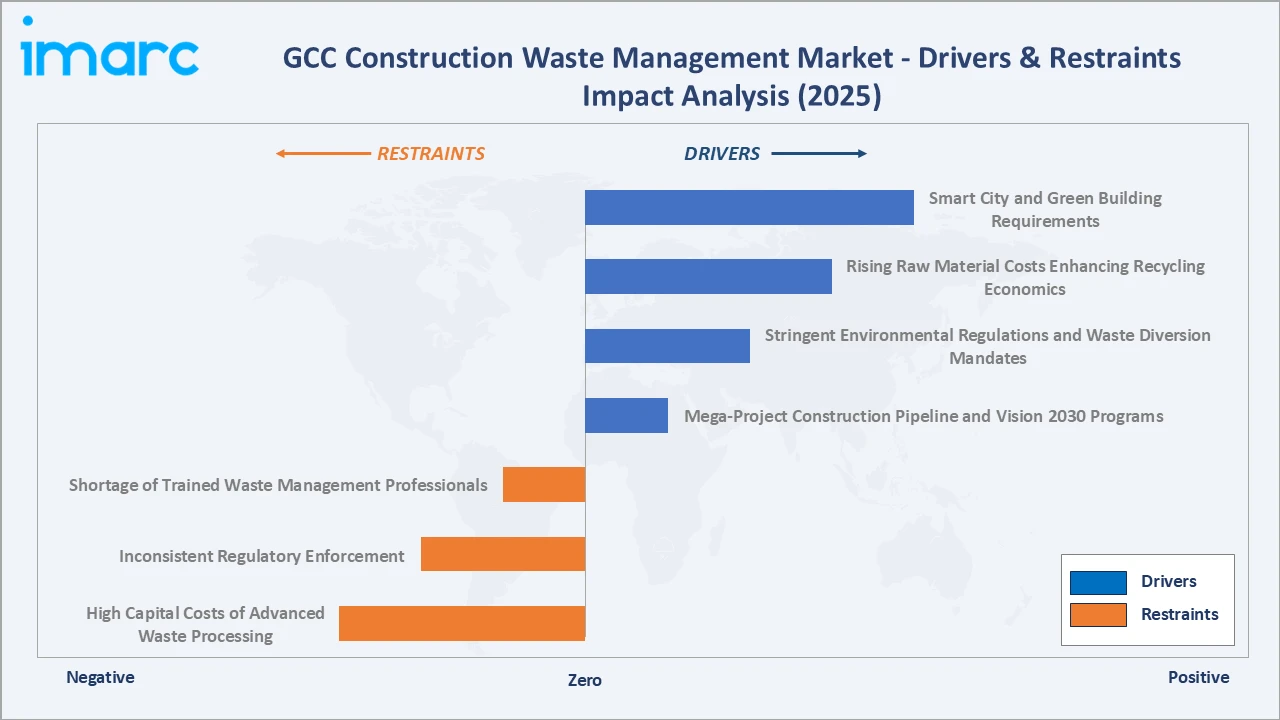

Market Drivers

- Mega-Project Construction Pipeline and Vision 2030 Programs: Saudi Arabia's Vision 2030 has mobilized the world's largest single-nation infrastructure pipeline, with projects including NEOM's The Line, Qiddiya Entertainment City, and the Red Sea Project. Each billion dollars of construction activity generates approximately 50,000–80,000 tons of construction waste, directly translating to waste management service demand growth across collection, sorting, and recycling functions.

- Stringent Environmental Regulations and Waste Diversion Mandates: UAE's Zero Waste to Landfill policy, Qatar's NECCS construction waste targets, and Saudi Arabia's National Waste Management Center's framework all impose mandatory waste management plans on construction projects. Non-compliance attracts financial penalties and project permit revocations, compelling contractors of all sizes to engage certified waste management operators.

- Rising Raw Material Costs Enhancing Recycling Economics: GCC steel import prices, aggregate costs, and plastics feedstock prices have increased 25–40% over 2020–2025, dramatically improving the commercial viability of construction waste recycling. Recycled concrete aggregate (RCA) at 60–70% of virgin aggregate cost and scrap metal at commodity market rates create profitable recycling operations that partially offset collection and processing costs for waste management operators.

- Smart City and Green Building Requirements: GCC governments' commitment to smart city developments mandates embedded sustainability frameworks including zero-landfill construction waste targets. LEED and Estidama certification prerequisites for government-contracted projects require Material Recovery Plans (MRPs), driving systematic waste management adoption across the contractor base.

Market Restraints

- High Capital Costs of Advanced Waste Processing: Construction and commissioning of compliant material recovery facilities (MRFs) with sorting, crushing, baling, and hazardous waste segregation capabilities requires capital investment of USD 15–50 Million per facility. This cost barrier limits new market entry and constrains capacity expansion, particularly in smaller GCC markets including Bahrain and Kuwait.

- Inconsistent Regulatory Enforcement: While UAE and Qatar maintain sophisticated enforcement regimes with electronic waste tracking systems and certified contractor databases, enforcement rigor varies significantly across the region. Inconsistent enforcement enables non-compliant operators to underprice certified waste management providers, creating adverse competitive dynamics that compress margins for compliant operators.

- Shortage of Trained Waste Management Professionals: Advanced waste sorting operations, hazardous material handling, and digital compliance system management require specialized technical expertise that remains in limited supply across the GCC. Expatriate workforce dependency and high staff turnover compound this challenge for operators managing quality-certified facilities.

Market Opportunities

- Advanced Recycling Technology Adoption: Near-infrared (NIR) sorting systems, AI-powered waste identification platforms, and automated concrete crushing lines capable of producing specification-grade RCA represent transformative opportunities for GCC market operators. UAE operators, including Beeah Group, have already piloted AI sorting at their Sharjah facilities, achieving material recovery rates of 90%+, creating a replicable model for regional scale-up.

- Circular Economy Integration with Construction Supply Chains: Direct integration of waste management operators with construction material manufacturers to supply recycled aggregates, reprocessed metals, and recovered plastics as certified secondary raw materials creates circular economy revenue streams with significantly higher value-capture than traditional tip-fee-only models.

Market Challenges

- Contamination and Mixed Waste Streams: GCC construction sites typically generate heavily mixed waste streams including co-mingled concrete, metals, wood, plastics, hazardous materials, and chemical-contaminated materials. Effective sorting and decontamination requires costly manual and automated segregation, and contamination rates consistently above 20% reduce the commercial value of recyclate streams.

- Land Availability for Waste Processing Facilities: High land costs and limited industrial zoning availability in core GCC urban markets including Dubai, Abu Dhabi, and Riyadh constrain the siting of waste processing facilities near construction activity centers, increasing transportation costs and reducing operational margins for waste management operators.

Emerging Market Trends

1. AI-Powered Waste Sorting and Digital Waste Tracking

BEEAH launched a Commercial & Industrial recycling facility in Sharjah using robotics and AI to automatically detect, identify, and separate mixed waste. The facility can process about 156,000 tons per year, supporting Sharjah’s zero-waste-to-landfill ambitions and improving material recovery. UAE's Dubai Municipality simultaneously launched a blockchain-based construction waste tracking system requiring all registered contractors to digitally log waste volumes, disposal routes, and recycling certificates, creating a transparent accountability chain from generation to final disposal.

2. Circular Economy Platforms and Material Exchange Markets

Saudi Arabia's NEOM project established a closed-loop construction material exchange platform, connecting demolition contractors with construction projects requiring secondary aggregates, enabling peer-to-peer material reuse within the mega-project ecosystem. This model is anticipated to reduce external waste management demand for low-value materials while creating cost savings of 15–25% on aggregate procurement versus virgin material sourcing.

3. Waste-to-Energy Integration

Qatar and UAE are progressively integrating construction waste-to-energy (WtE) facilities into national waste management infrastructure. Qatar's Domestic Solid Waste Management Center (DSWMC) at Mesaieed processes non-recyclable construction waste streams, while Dubai's Warsan WtE plant handles residual construction waste not suitable for material recovery, diverting it from raw landfill disposal.

4. Modular and Mobile Processing Units

Mobile concrete crushers, portable shredders, and containerized sorting units are gaining adoption across GCC construction sites, enabling on-site material recovery for large-scale projects. These modular units reduce transportation costs by 30–40% and allow material recovery to occur adjacent to demolition activities, improving recyclate quality by minimizing contamination during transit.

Industry Value Chain Analysis

The GCC construction waste management value chain spans waste generation at construction sites through end-user application of recovered materials, with each stage occupied by specialized contractors, processors, and regulators whose performance directly influences compliance outcomes, material recovery rates, and circular economy value-capture.

|

Stage |

Key Players / Examples |

|

Waste Generation |

Construction contractors, demolition firms, project developers, MEP sub-contractors |

|

Collection & Transport |

Licensed waste hauliers, logistics contractors, fleet operators with GPS-tracked vehicles, regulatory waste manifest systems |

|

Sorting & Segregation |

Material recovery facility (MRF) operators, on-site waste supervisors, NIR sorting technology providers |

|

Processing & Treatment |

Concrete crushing and aggregate production facilities, metal scrap dealers, plastic recycling processors |

|

Recycling & Reuse |

Secondary aggregate suppliers, scrap metal traders and mills, recycled plastic compounders |

|

End Users & Operators |

Construction developers, petrochemical firms, government and regulatory authorities |

Technology Landscape in the GCC Construction Waste Management Industry

Material Recovery Facilities (MRFs) and Automated Sorting

Material Recovery Facilities represent the technological backbone of GCC construction waste management, incorporating conveyor belt systems, trommel screens, magnetic separators for metal recovery, eddy current separators for non-ferrous metals, and near-infrared (NIR) optical sorters for plastics and paper. Leading MRF operators in the GCC, including Beeah Group’s Sharjah facility and Averda's operations in Saudi Arabia, operate at throughput capacities of 500–2,000 tons per day, processing mixed construction and demolition waste into segregated commodity streams.

Concrete Crushing and Aggregate Recovery

Concrete crusher technology converts demolition concrete into recycled concrete aggregate (RCA) at grading specifications suitable for road base, sub-base fill, and non-structural concrete applications. In the GCC, NEOM and large infrastructure projects have adopted on-site mobile crushing units from manufacturers, enabling recovery of 70–80% of concrete demolition waste as usable RCA, significantly reducing virgin quarried aggregate demand.

Waste-to-Energy Technologies

Engineered landfill gas (LFG) capture systems, rotary kiln incineration, and refuse-derived fuel (RDF) pelletizing technologies are progressively deployed across GCC waste management infrastructure. Qatar's DSWMC and UAE's Sharjah and Dubai WtE facilities operate mass-burn grate incineration technology with energy recovery, converting approximately 1,700–2,500 kcal/kg of mixed construction waste into electrical energy.

Digital Waste Tracking and Compliance Platforms

Saudi Arabia's National Waste Management Center has deployed a national electronic waste tracking system requiring licensed haulers to register every waste transfer from construction sites to approved facilities via GPS-verified manifests. Dubai Municipality's equivalent digital platform integrates with contractor licensing databases, enabling real-time monitoring of construction waste diversion rates across active project sites.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Disposal Method |

Recycling |

47.8% |

2025 |

|

Materials |

Metal |

24.8% |

2025 |

|

Service |

🔒 |

🔒 |

2025 |

|

Country |

Saudi Arabia |

40.2% |

2025 |

By Disposal Method

The disposal method segment is analyzed across recycling (47.8%), landfill (38.6%), and incineration (13.6%). Recycling leads as the preferred disposal method, reflecting the GCC's proactive regulatory posture and the strong economic returns from recovering metals, concrete aggregates, and plastics from construction waste streams.

To access detailed market analysis, Request Sample

The recycling segment is driven by mandatory diversion targets across Saudi Arabia, UAE, and Qatar, and strong commodity market demand for recovered metals and aggregates. The landfill segment remains significant but is structurally declining as regulatory frameworks impose progressive diversion mandates. Incineration addresses combustible non-recyclable and hazardous waste streams at WtE facilities in the UAE and Qatar.

By Materials

The materials composition segment is led by metal (24.8%), followed by plastic (19.6%), paper and paperboard (17.4%), glass (13.5%), and food and organic (10.7%). Metal commands the largest share due to the GCC's steel-intensive construction methodology and the high commodity market value of recovered scrap steel and aluminum.

Plastic encompasses PVC piping, electrical conduit, insulation boards, and packaging from construction material deliveries. Paper and paperboard includes gypsum board core paper, packaging, and temporary formwork liners, a straightforward recycling stream with established demand from regional mills.

Regional Market Insights

Saudi Arabia's market leadership at 40.2% in 2025 reflects the Kingdom's status as the GCC's construction powerhouse, with Vision 2030 having mobilized the world's most concentrated single-nation infrastructure pipeline. UAE follows at 27.8%, underpinned by advanced regulatory frameworks and sustainability commitments.

Qatar represents 9.8% of regional market share, with post-FIFA World Cup 2022 construction legacy creating a substantial waste management requirement as temporary facilities are demolished and repurposed.

|

Country |

Share (2025) |

Key Growth Drivers |

|

Saudi Arabia |

40.2% |

Vision 2030 mega-projects; NEOM; National Waste Management Center framework; mandatory waste management plans across all major construction projects |

|

UAE |

27.8% |

Net Zero 2050; Dubai zero-landfill policy; Estidama green building certification |

|

Qatar |

9.8% |

Post-FIFA 2022 legacy infrastructure; NECCS waste diversion targets; Ashghal mandatory waste management plans for all public contracts |

|

Oman |

8.1% |

Oman Vision 2040 infrastructure; tourism resort development along the coastline; Muscat urban expansion programs |

|

Kuwait |

7.6% |

Kuwait 2035 New Kuwait Vision; large-scale public infrastructure programs; residential development initiatives |

|

Bahrain |

6.5% |

Bahrain Economic Vision 2030; urban regeneration; Northern City development; Bahrain International Airport expansion |

Competitive Landscape

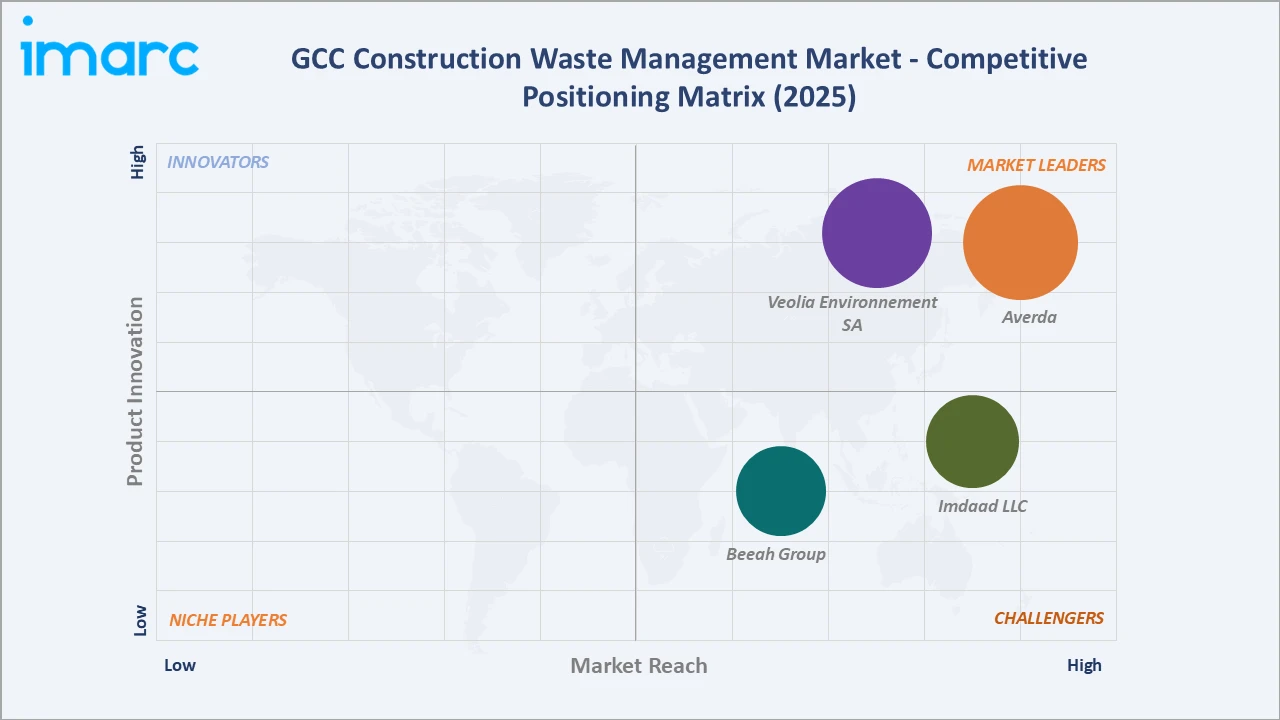

The GCC construction waste management market exhibits moderate concentration, with the leading five operators collectively holding approximately 45–55% of market revenue in 2025. Global environmental services firms compete alongside regional specialists and GCC-headquartered entities that have built substantial local operational platforms.

|

Company Name |

Solution |

Market Position |

Core Strength |

|

Averda |

Construction Waste Removal |

Market Leader |

Integrated waste management across GCC contracts; digital waste tracking platform; largest regional MRF network |

|

Veolia Environnement SA |

Waste Collection and Sorting, Waste to Energy, Recovering Materials from Waste, Industrial Waste Management, Treatment and Recovery of Hazardous and Special Waste |

Market Leader |

Global environmental services scale; advanced MRF operations; water-energy-waste integration; Saudi Arabia concessions |

|

Imdaad LLC |

Waste Management Services |

Strong Challenger |

UAE-focused integrated FM and waste services; established community operations |

|

Beeah Group |

Waste Collection & City Cleaning, Waste Recycling & Processing |

Challenger |

AI-powered MRF achieving high diversion rate; Sharjah government strategic partner; technology-led differentiation |

Global environmental services firms dominate large-scale mega-project contracts through established supply chains, comprehensive service portfolios, and internationally certified environmental management systems.

Key Company Profiles

Averda

Averda is the GCC's leading integrated waste management operator, with operations spanning collection, recycling, materials recovery, and landfill management across Saudi Arabia, UAE, Qatar, Kuwait, Oman, and Bahrain.

- Product/Service Portfolio: Construction waste collection and transport, material recovery facility (MRF) operations, hazardous waste management, landfill management, recycling services, and environmental compliance consulting.

- Strategic Focus: MRF capacity expansion across GCC; digital waste manifesting and compliance platform growth; circular economy material supply partnerships with construction material manufacturers; expansion into emerging GCC markets including Kuwait and Oman.

Veolia Environnement SA

Veolia Environnement SA is a global leader in environmental services providing water, waste, and energy management solutions. Veolia operates across Saudi Arabia, UAE, and Qatar through long-term municipal and industrial waste management concessions.

- Product/Service Portfolio: Construction and demolition waste collection, material recovery and recycling, industrial hazardous waste treatment, WtE operations, and integrated environmental consulting services.

- Recent Developments: In February 2026, Veolia Environnement SA reported record 2025 revenue of EUR 44.4 billion, while its Africa–Middle East business generated EUR 1.83 billion, supported by strong energy services growth in the Middle East (including the GCC).

- Strategic Focus: Saudi Arabia market expansion through Vision 2030 concession pipeline; WtE facility development; circular economy materials recovery platform; water-waste-energy integration bundling for large-scale urban developments.

Market Concentration Analysis

The GCC construction waste management market exhibits moderate concentration, with the top five operators holding approximately 45–55% of total revenue in 2025. Below the top tier, a competitive mid-market of 20–30 specialized contractors and regional integrators serves construction project-specific and geographic niche segments with tailored collection and processing solutions.

Market consolidation is occurring primarily through two dynamics: global environmental services firms expanding GCC footprint through government concession bids, and regional operators investing in technology differentiation to defend margins against commoditized collection-only competitors. The Saudi Arabia market, currently the least consolidated of the six GCC member states in waste management concession structure, represents the largest near-term consolidation opportunity as NWMC regulatory maturity drives out non-compliant operators.

Investment & Growth Opportunities

Fastest Growing Segments

Advanced recycling infrastructure (~7.8% CAGR), AI-powered sorting and digital compliance platforms (~12%+ CAGR), Saudi Arabia regional market services (~7.2% CAGR), and circular economy material exchange platforms (~9%+ CAGR) represent the highest-growth investment vectors through 2034. Together, these sub-categories address a combined addressable market exceeding USD 5 Billion by 2030 within the GCC construction waste management ecosystem.

Emerging Market Expansion

Saudi Arabia's secondary cities collectively represent an incremental USD 2+ Billion construction waste management opportunity beyond Riyadh by 2034, as geographic diversification of Vision 2030 project execution accelerates.

Entry strategies for waste management operators targeting these emerging zones include early-stage concession bidding with Saudi Vision 2030 project developers, co-location of MRF capacity adjacent to mega-project construction camps, and partnership with Saudi-based construction contractors who carry government preferences for local waste management solutions.

Venture and Institutional Investment Trends

- GCC construction CAPEX pipelines exceeding USD 2 trillion through 2035 directly translate to construction waste generation requiring certified management, creating highly visible long-term demand that is attracting institutional capital into waste management infrastructure and concession platforms.

- Government-backed circular economy initiatives in the UAE (Circular Economy Policy 2021–2031) and Saudi Arabia (National Circular Economy Strategy 2021) are creating policy tailwinds for investment in secondary materials recovery businesses, including aggregate recycling plants, scrap metal processing facilities, and construction plastic compounding operations.

- Waste-as-a-Service models are emerging as capital-efficient growth models that reduce developer CAPEX barriers to certified waste management adoption, potentially commanding 20–30% revenue premiums over traditional collection-only service contracts.

Future Market Outlook (2026-2034)

The GCC construction waste management market is positioned for sustained growth through 2034. From a base of USD 7.81 Billion in 2025, the market is projected to reach USD 13.46 Billion by 2034, representing total incremental value creation of USD 5.65 Billion at a CAGR of 6.23%. This growth is underpinned by the multi-year GCC construction pipeline and the region's irreversible trajectory toward mandatory compliance with waste diversion targets embedded in national vision programs.

The technology transition from manual sorting and unregulated disposal to AI-powered material recovery and certified circular economy integration will define the market's composition by 2034. Recycling's share is projected to grow from 47.8% in 2025 to approximately 58–62% by 2034, as Saudi Arabia's NWMC 70% diversion target and UAE's zero-landfill ambition take full regulatory effect.

Research Methodology

Primary Research

Primary research comprised structured interviews with over 90 industry participants in 2024–2025, including construction contractors, waste management operators, recycling facility managers, environmental consultants, and regulatory authority representatives across Saudi Arabia, UAE, Qatar, Kuwait, Oman, and Bahrain.

Secondary Research

Secondary research encompassed national waste management strategy documents, GCC government infrastructure program disclosures, Saudi Arabia NWMC regulatory publications, UAE Municipality waste management guidelines, Qatar Ashghal environmental standards, GCC trade data for waste processing equipment imports and exports, operator annual sustainability reports, and industry publications covering Middle East waste management sector developments.

Forecasting Models

Market size estimations were derived using top-down and bottom-up forecasting, incorporating GCC construction output projections (USD value per country), waste intensity coefficients (tons per USD Million of construction output), management service fee rates per ton by service tier, and recycling rate trajectory models validated against regulatory diversion targets.

GCC Construction Waste Management Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Disposal Methods Covered | Landfill, Incineration, Recycling |

| Services Covered | Collection Service, Collection and transportation, Storage and Handling, Sorting, Disposable Service, Landfills, Recycling, Compositing and Anaerobic Digestion |

| Materials Covered | Paper and Paperboard, Plastic, Metal, Glass, Food, Others |

| Countries Covered | Saudi Arabia, the UAE, Qatar, Bahrain, Kuwait, Oman |

| Companies Covered | Averda, Veolia Environnement SA, Imdaad LLC, Beeah Group, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the GCC construction waste management market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the GCC construction waste management market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the GCC construction waste management industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the GCC Construction Waste Management Market Report

The GCC construction waste management market reached USD 7.81 Billion in 2025 and is projected to reach USD 13.46 Billion by 2034.

The market is expected to grow at a CAGR of 6.23% during 2026-2034, driven by mega-project construction activity, environmental regulatory tightening, and advancing recycling technology adoption across all six GCC member states.

Saudi Arabia leads with a 40.2% market share in 2025, anchored by Vision 2030's unprecedented infrastructure pipeline and the Kingdom's National Waste Management Center's regulatory framework mandating certified waste management plans for all major construction projects.

Recycling dominates with a 47.8% share in 2025, driven by GCC regulatory diversion mandates, the economic viability of metals recovery at commodity market rates, and growing demand for recycled concrete aggregate.

Metal holds the largest materials segment share at 24.8%, driven by the GCC's steel-intensive construction methodology and the high commodity value of recovered scrap steel and aluminum that makes metal collection and processing commercially self-sustaining without tip-fee subsidy.

Some of the key players include Averda, Veolia Environnement SA, Imdaad LLC, and Beeah Group.

Key drivers include Vision 2030 mega-project construction pipelines generating tens of millions of tons of waste annually, stringent waste diversion mandates across Saudi Arabia, and smart city development programs requiring embedded sustainability frameworks and zero-landfill construction waste targets.

Key challenges include high capital costs of advanced waste processing facilities, inconsistent regulatory enforcement across GCC member states, waste stream contamination reducing recyclate quality and commercial value, and limited industrial land availability for processing facility siting in core urban markets.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)