GCC Pet Food Market Size, Share, Trends and Forecast by Pet Type, Product Type, Ingredient Type, Distribution Channel, and Region, 2026-2034

GCC Pet Food Market Size and Share:

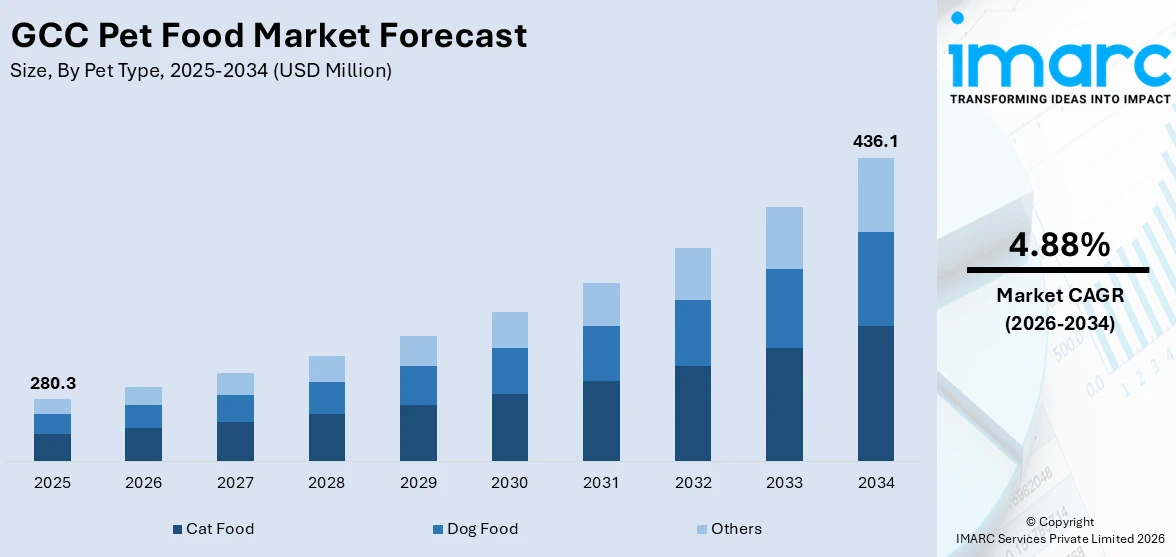

The GCC pet food market size was valued at USD 280.3 Million in 2025. Looking forward, IMARC Group estimates the market to reach USD 436.1 Million by 2034, exhibiting a CAGR of 4.88% during 2026-2034. UAE dominated the market in 2025 due to rising pet ownership, increased disposable income, and growing awareness of pet health. Expanding urban lifestyles, premiumization trends, and a surge in e-commerce and pet specialty stores for high-quality, nutritious pet food products across the country are also some of the key factors contributing to the GCC pet food market share.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

|

Market Size in 2025

|

USD 280.3 Million |

|

Market Forecast in 2034

|

USD 436.1 Million |

| Market Growth Rate 2026-2034 | 4.88% |

The market is growing due to rising pet ownership, especially in urban households where nuclear families and single professionals increasingly adopt pets for companionship. Changing social attitudes and greater acceptance of pets, particularly cats and small dog breeds, are encouraging demand for packaged nutrition. There’s also growing awareness of pet health and wellness, leading to a preference for specialized products such as breed-specific, age-specific, and functional foods. The expansion of modern retail channels and online pet stores makes a wider variety of products accessible across the region. Additionally, rising disposable incomes and a strong expatriate presence supporting premiumization, with consumers seeking higher-quality and imported options, are other factors driving the GCC pet food market growth. Regulatory improvements in pet food standards and growing veterinary infrastructure are also reinforcing consumer trust and market development across the GCC.

To get more information on this market Request Sample

Health-focused offerings are gaining ground in the Gulf pet care space, with new brands emphasizing complete, age-specific diets for cats and dogs. Products highlighting quality ingredients, palatability, and scientific formulation are resonating with informed consumers, reflecting a shift toward nutrition-driven choices and greater expectations from international pet food entrants. For instance, in April 2025, Pet Coin made its debut in the UAE market, offering nutritious options for cats and dogs of all ages. Founded by pet lovers and nutrition experts, the brand aimed to align Turkish quality with UAE pet owners’ expectations. It introduced a full range of flavorful and health-focused recipes, marking a significant entry into the region’s pet industry.

GCC Pet Food Market Trends:

Growing Pet Companionship Influencing Market Dynamics

A noticeable rise in pet companionship across Saudi Arabia is reshaping purchasing patterns in the pet food sector throughout the GCC. With more households embracing cats and dogs as part of the family, demand for specialized nutrition and premium pet care products is gaining momentum. This shift is encouraging retailers and producers to broaden their offerings, focusing on health, taste, and convenience. The increasing emotional bond between owners and their pets is also driving a preference for high-quality, tailored diets. As the role of pets evolves beyond basic companionship, the market is responding with a wider range of products and services that reflect the changing expectations and lifestyles of pet owners in the region. For instance, in 2025, pet ownership in Saudi Arabia has grown significantly, with the combined cat and dog population increasing from 0.8 Million to 2.4 Million in recent years.

Widening Global Footprint in Specialty Pet Nutrition

Based on the GCC pet food market outlook, premium pet food brands are expanding into Gulf markets with a tailored product approach, focusing on species-specific and lifestyle-specific offerings. The entry of international players into Qatar reflects rising interest in high-quality feline nutrition. Exclusive launches of cat food align with the country's strong demand in this segment. Meanwhile, broader product availability targeting diverse pet profiles, such as small breeds and active dogs, signals a maturing market ready for specialized SKUs. Distribution through local pet stores further highlights a shift toward curated retail partnerships and indicates growing acceptance of premium international labels within the region. For example, in March 2025, Kormotech Group of Companies expanded its international presence by entering the Nigerian and Qatari markets, bringing its reach to 46 countries. In Qatar, the company exclusively offered cat food, while in Nigeria, there was demand for cat food, small-breed dog food, and food for active dogs. Club4Paws products were initially distributed through local pet stores in both countries.

Higher Household Spending Power Boosting Pet Care Demand

The GCC pet food market forecast indicates that the rising disposable incomes across the Kingdom are influencing spending patterns in the pet food sector throughout the GCC. With households now enjoying greater financial flexibility, there is a growing shift toward premium pet nutrition and wellness products. Consumers are increasingly willing to invest in quality offerings that support the health, longevity, and overall well-being of their pets. This enhanced spending capacity is also expanding interest in specialized diets, organic ingredients, and functional food varieties. Retailers are responding by enhancing product assortments and introducing upscale options to meet evolving preferences. As pet ownership grows and affluence increases, the regional market is seeing stronger demand for value-added products that align with modern lifestyles and heightened care standards. For instance, in 2023, the average household's monthly disposable income reached SAR 11,839 across the Kingdom.

GCC Pet Food Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the GCC pet food market, along with forecasts at the regional and country levels from 2026-2034. The market has been categorized based on pet type, product type, ingredient type, and distribution channel.

Analysis by Pet Type:

- Dog Food

- Cat Food

- Others

Cat food stood as the largest segment in 2025 due to the substantial prevalence of cat ownership across the GCC, where felines are often favored as household companions. This preference translates directly into a higher volume demand for cat food compared to other pet types. Furthermore, the escalating trend of pet humanization within the region sees owners increasingly regarding their cats as integral family members, leading to a greater inclination to invest in premium, nutritionally rich food options. This focus on the specific dietary requirements of cats, including their need for high protein and essential nutrients, further fuels the demand for specialized cat food formulations, solidifying its position as the dominant force driving growth and revenue within the GCC pet food market.

Analysis by Product Type:

- Dry Food

- Wet and Canned Food

- Snacks and Treats

Dry food led the market in 2025 since consumers in the region increasingly prefer dry food options due to their longer shelf life, convenience in storage and feeding, and lower cost compared to wet food. Dry food also supports better dental health in pets, making it a practical choice for everyday feeding. Urbanization and the rising trend of pet humanization have led to higher spending on pet care, further boosting demand for premium dry food formulations tailored to pet age, breed, and health conditions. With busy lifestyles and an expanding retail presence, especially in supermarkets and online platforms, dry food continues to gain strong traction across the GCC countries.

Analysis by Ingredient Type:

- Animal Derivatives

- Plant Derivatives

- Cereal Derivatives

- Others

Animal derivatives led the market in 2025. These ingredients, such as meat meals, bone meals, and poultry by-products, are rich in proteins and essential nutrients, making them highly suitable for meeting the dietary needs of pets. Local manufacturers and global brands are incorporating high-quality animal derivatives to enhance flavor, digestibility, and nutritional value. With increasing awareness about pet health and a shift toward protein-rich diets, consumers are showing greater preference for pet food that closely mimics natural animal-based nutrition. Additionally, the use of animal derivatives supports cost-effective formulation without compromising quality, making them an attractive option across both premium and value product categories in the region.

Analysis by Distribution Channel:

Access the comprehensive market breakdown Request Sample

- Supermarkets and Hypermarkets

- Convenience Stores

- Online Stores

- Others

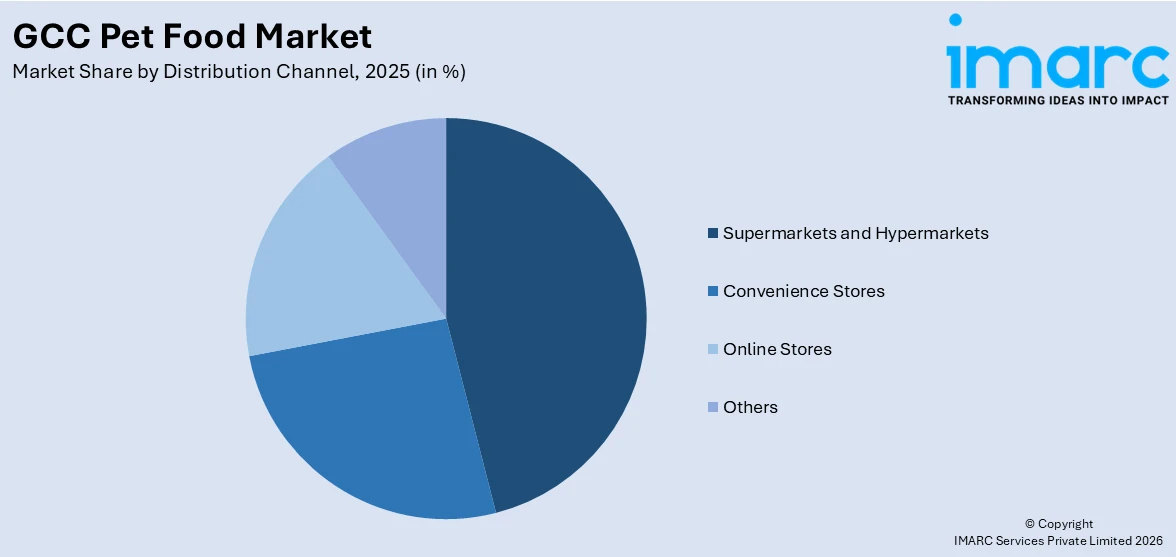

Supermarkets and hypermarkets are supporting the GCC pet food market by offering extensive product variety, competitive pricing, and access to both global and regional brands. Their organized layouts, dedicated pet aisles, and regular promotional campaigns attract a large base of pet owners, especially in urban areas. The availability of premium, specialty, and bulk-packaged pet food options further strengthens their role in market expansion. Convenience stores contribute by catering to on-the-go and routine purchases through their widespread presence, extended operating hours, and quick service. They play a crucial role in last-minute buying decisions and serve as accessible points for everyday pet food needs, particularly in residential neighborhoods, making them a vital distribution channel in the GCC region.

Regional Analysis:

- UAE

- Saudi Arabia

- Kuwait

- Qatar

- Oman

- Bahrain

In 2025, the UAE accounted for the largest market share, driven by rising pet ownership, increasing disposable incomes, and a growing preference for premium pet care products. Urbanization and a strong expatriate population have fostered a culture of pet companionship, especially in cities like Dubai and Abu Dhabi. The country’s well-developed retail infrastructure, including supermarkets, pet specialty stores, and e-commerce platforms, ensures wide product availability and brand visibility. Government regulations supporting pet welfare and growing awareness of pet nutrition are further encouraging demand. The UAE also serves as a regional hub for international pet food brands entering the GCC, making it a focal point for innovation and market expansion.

Competitive Landscape:

The GCC pet food market is experiencing notable growth, driven by several recent developments. Manufacturers are introducing premium and organic products to meet the rising demand for high-quality pet nutrition. Strategic partnerships between pet food companies and veterinary clinics are enhancing product offerings and customer education initiatives. Investments in research and development are leading to innovative formulations tailored to specific pet health needs. E-commerce platforms are expanding, providing consumers with convenient access to a variety of pet food products. Government initiatives promoting pet welfare are also contributing to market expansion. Among these trends, the introduction of new product variants and flavors stands out as a common practice, reflecting the industry's response to evolving consumer preferences.

The report provides a comprehensive analysis of the competitive landscape in the GCC pet food market with detailed profiles of all major companies, including:

- Nestlé Purina

- Mars, Incorporated

- Hill’s Pet Nutrition, Inc.

- General Mills Inc.

- WellPet LLC.

- The J.M. Smucker Company

- Schell & Kampeter, Inc.

- Heristo AG

Latest News and Developments:

- April 2025: Zabeel Feed launched its new pet food brand, Zabeel Pets, at Pet World Arabia 2025. The brand debuted with ready-to-eat pet meals, smart pet tech, and luxury accessories, marking Zabeel's expansion beyond equine nutrition. Held from April 19–20 in Dubai, the event featured over 160 exhibitors and underscored the MENA region's growing USD 7.3 Billion pet market.

- April 2025: Muntajat, rebranded to mark its 20th anniversary, reflecting its commitment to innovation and leadership. It had evolved from its origins as Pet Products Trading Company (PPTCO) into a global force in pet care distribution. The company had reinforced its industry position through strategic partnerships, loyalty programs, and a visionary new identity.

GCC Pet Food Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Pet Types Covered | Dog Food, Cat Food, Others |

| Product Types Covered | Dry Food, Wet and Canned Food, Snacks and Treats |

| Ingredient Types Covered | Animal Derivatives, Plant Derivatives, Cereal Derivatives, Others |

| Distribution Channels Covered | Supermarkets and Hypermarkets, Convenience Stores, Online Stores, Others |

| Countries Covered | UAE, Saudi Arabia, Kuwait, Qatar, Oman, Bahrain |

| Companies Covered | Nestlé Purina, Mars, Incorporated, Hill’s Pet Nutrition, Inc., General Mills Inc., WellPet LLC., The J.M. Smucker Company, Schell & Kampeter, Inc., Heristo AG, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the GCC pet food market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the GCC pet food market.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the GCC pet food industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the GCC Pet Food Market Report

The pet food market in the GCC was valued at USD 280.3 Million in 2025.

The GCC pet food market is projected to exhibit a CAGR of 4.88% during 2026-2034, reaching a value of USD 436.1 Million by 2034.

Key factors driving the GCC pet food market include rising pet humanization, growing awareness of pet nutrition, urbanization, and increasing disposable incomes. Expansion of retail and e-commerce platforms, demand for premium and organic pet food, and supportive government regulations on pet care further contribute to the market’s steady growth.

The UAE accounted for the largest share of the market in 2025. High pet ownership rates, rising disposable incomes, premiumization trends, growing awareness of pet health, strong retail infrastructure, and increasing adoption of Western lifestyles have driven the UAE’s dominance in the GCC pet food market.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)