GCC Telemedicine Market Size, Share, Trends and Forecast by Component, Communication Technology, Hosting Type, Application, End User, and Country, 2026-2034

GCC Telemedicine Market Size, Share, Trends & Forecast (2026-2034)

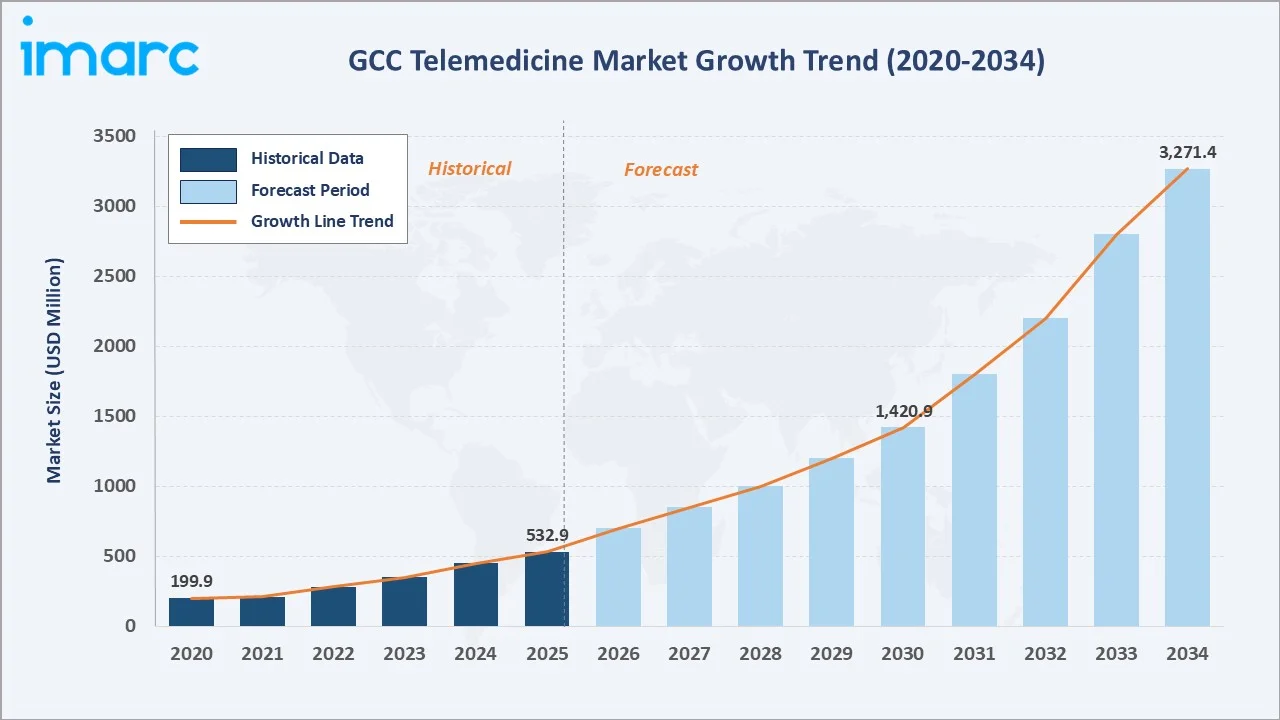

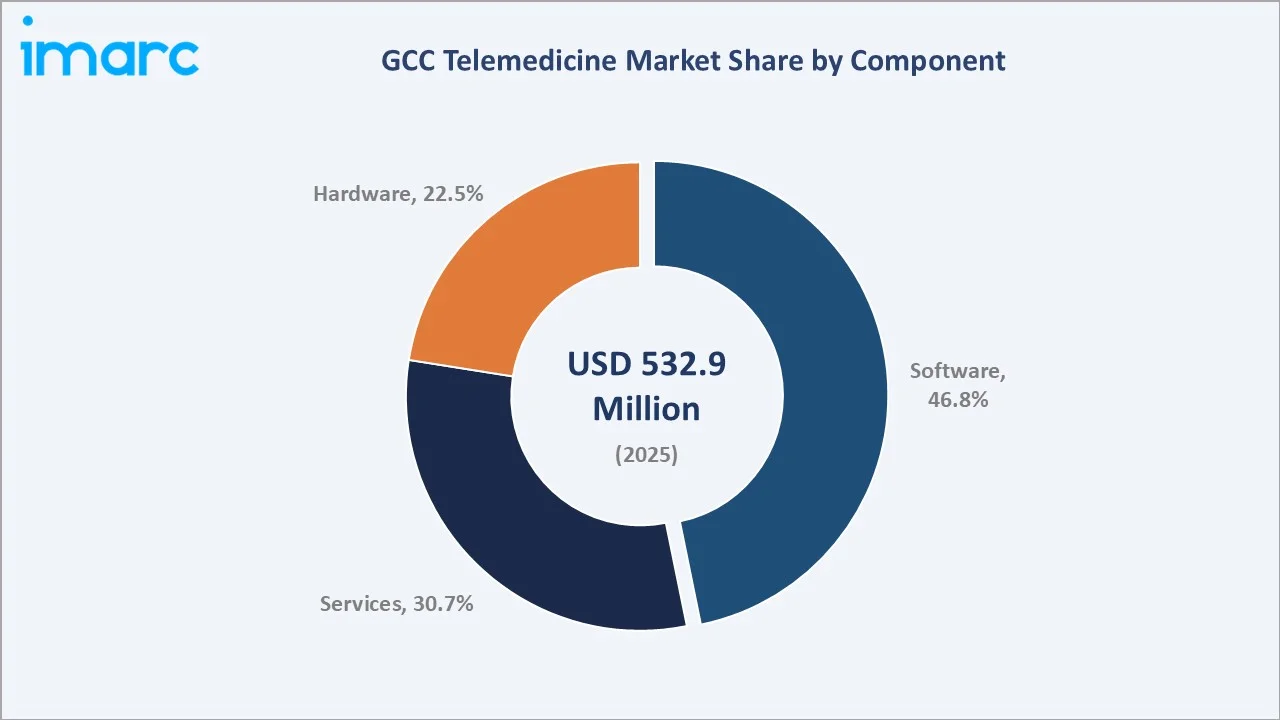

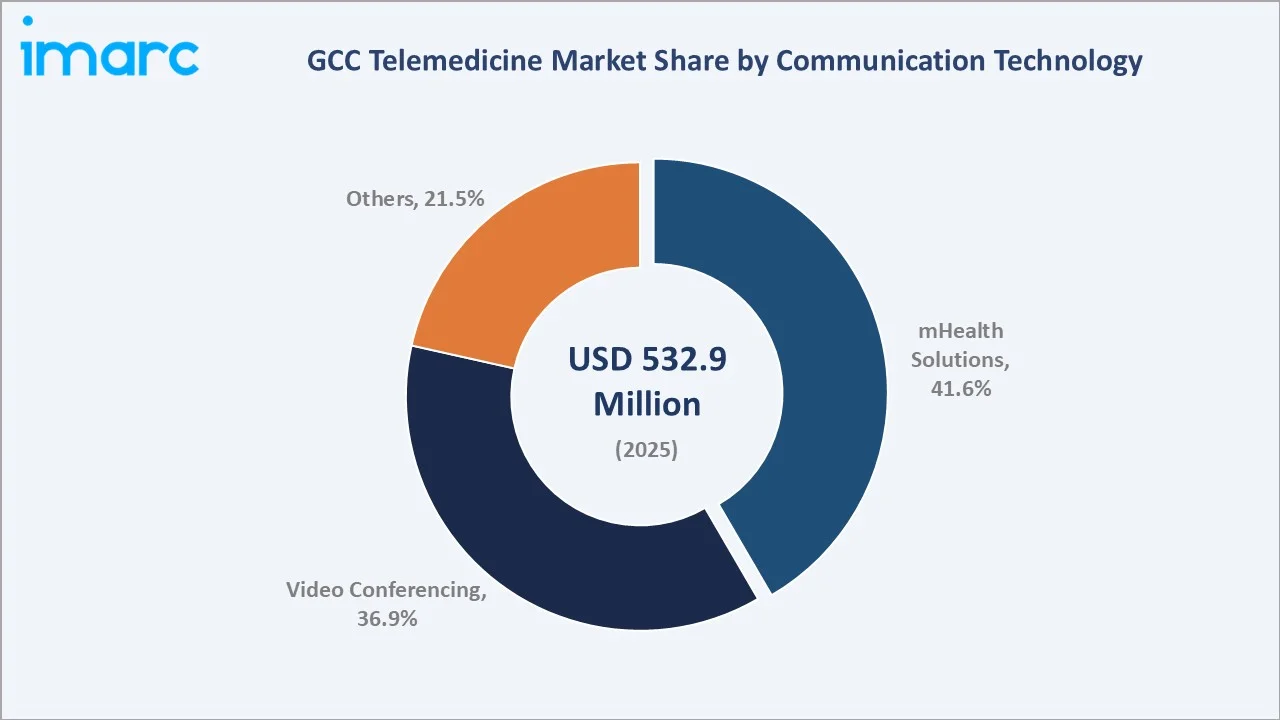

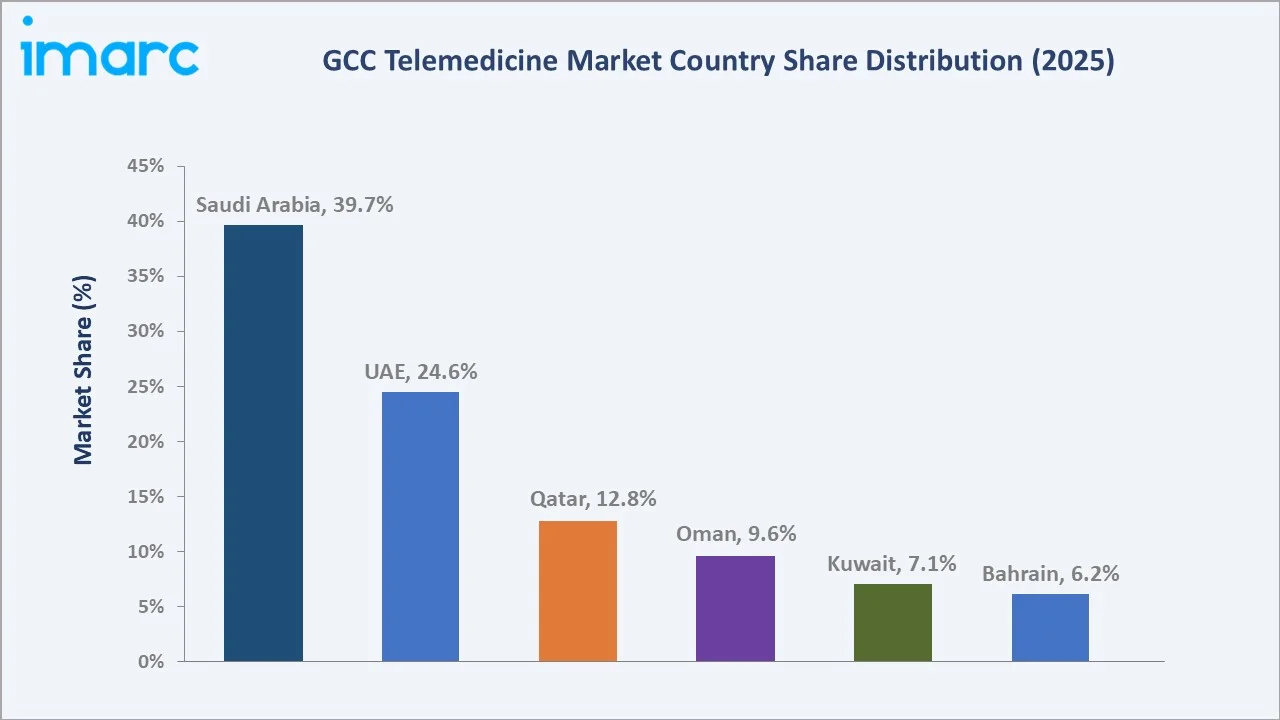

The GCC telemedicine market reached USD 532.9 Million in 2025 and is projected to reach USD 3,271.4 Million by 2034, growing at a CAGR of 21.67% during 2026-2034. GCC telemedicine market growth is driven by strong government digital health initiatives (Vision 2030 programs), rising chronic disease burden, and expanding healthcare access in remote areas. The General Authority for Statistics published its 2024 Health Status Statistics, indicating that 18.95% of individuals aged 15 and above lived with at least one chronic condition in Saudi Arabia, the most prevalent diseases include diabetes (9.1%), hypertension (7.9%), high cholesterol (3.6%), cardiovascular diseases (1.5%), and cancer (0.6%). Software leads at 46.8% component share; mHealth solutions dominate communication technology at 41.6%. Saudi Arabia commands 39.7% of the regional market.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 532.9 Million |

|

Forecast Market Size (2034) |

USD 3,271.4 Million |

|

CAGR (2026-2034) |

21.67% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Country |

Saudi Arabia (39.7%, 2025) |

|

Largest Component |

Software (46.8%, 2025) |

|

Leading Communication Technology |

mHealth Solutions (41.6%, 2025) |

The market expanded from USD 199.9 Million in 2020 to USD 532.9 Million in 2025, anchored at USD 1,420.9 Million in 2030, and forecast to reach USD 3,271.4 Million by 2034. Post-COVID telemedicine normalization, national digital health strategies across all six GCC nations, and government healthcare digitalization investment created a compounding growth cycle, fundamentally transforming the region's healthcare delivery architecture.

To get more information on this market, Request Sample

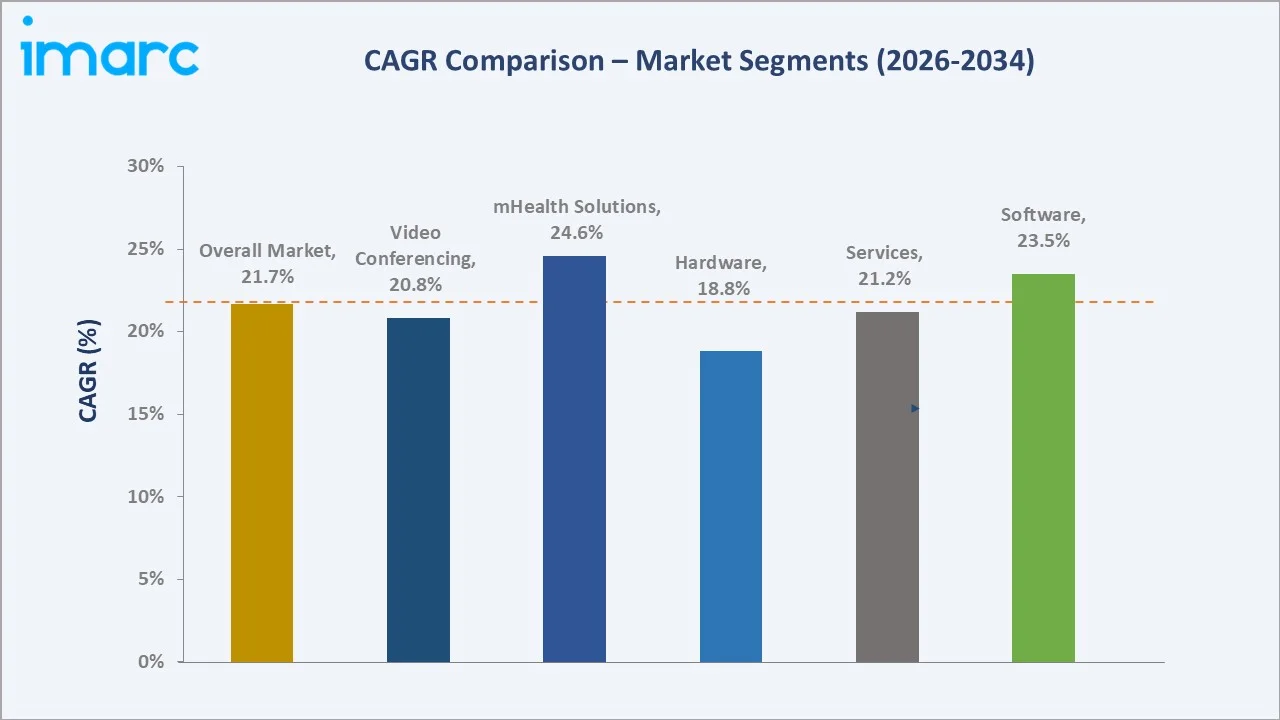

mHealth Solutions grow fastest at ~24.6% CAGR (2026-2034), driven by GCC smartphone penetration, enabling scalable mobile health application adoption. Software components grow at ~23.5% CAGR, reflecting the rapid shift toward cloud-based, AI-integrated telemedicine platform revenues. Hardware grows slowest at ~18.8% CAGR as software-defined telemedicine reduces dedicated hardware dependency.

Executive Summary

The GCC telemedicine market reached USD 532.9 Million in 2025, representing one of the world's fastest-growing regional digital health markets. All six GCC nations, Saudi Arabia, UAE, Qatar, Oman, Kuwait, and Bahrain, have embedded telemedicine within their national digital transformation agendas, creating government-mandated demand expansion that supplements organic private sector growth. Saudi Arabia's Vision 2030 and the UAE's telemedicine framework are the most catalytic policy environments in the region. The market is projected to reach USD 3,271.4 Million by 2034 at 21.67% CAGR, driven by AI integration in diagnostic platforms, 5G-enabled real-time monitoring, chronic disease management at scale for GCC's chronic disease patients, and sustained government procurement.

Software commands 46.8% market share (2025), anchored by clinical telemedicine platforms, AI diagnostic tools, and EHR-integrated teleconsultation systems. mHealth solutions lead communication technology at 41.6%, leveraging world-class GCC mobile infrastructure for scalable digital health access. Saudi Arabia retains 39.7% leadership, UAE at 24.6% serves as the GCC's digital health innovation hub with digital health companies.

Key Market Insights

|

Insight |

Data |

|

Largest Component |

Software - 46.8% share (2025) |

|

Leading Communication Technology |

mHealth Solutions - 41.6% share (2025) |

|

Dominant Country |

Saudi Arabia - 39.7% market share (2025) |

Key Analytical Observations Supporting the Above Data:

- Software at 46.8% (2025), driven by AI diagnostic and cloud platform demand: GCC hospitals are deploying cloud telemedicine software integrating electronic health records with AI-powered diagnostic tools.

- mHealth solutions at 41.6%: Saudi Arabia's Sehhaty government app, with over 24 million active registered users driving the segment growth. These government-funded mHealth platforms are creating the patient-facing infrastructure on which commercial platforms build.

- Saudi Arabia at 39.7% driven by Vision 2030 healthcare investment: The Saudi Arabia government allocated over $1.5 billion for healthcare IT and digital transformation programs. The government's commitment to connecting primary health centers through telemedicine by 2030 creates institutional demand unmatched anywhere in the region.

GCC Telemedicine Market Overview

The GCC telemedicine market encompasses remote delivery of medical services via digital platforms across six member states. It integrates software platforms, video conferencing systems, mHealth applications, remote patient monitoring devices, and telehealth services, connecting patients with providers without requiring physical visits. Applications span teleconsultation, teleradiology, telecardiology, teleneurology, telepsychiatry, and tele-dermatology, serving GCC citizens.

The market operates under health ministry regulatory frameworks in each GCC nation, providing the most developed telemedicine licensing structures. Macroeconomic drivers include GCC population with high smartphone penetration, 5G deployment across Saudi Arabia and UAE, chronic disease prevalence, and government digitalization investments across Vision 2030 and equivalent national strategies through 2034.

Market Dynamics

To evaluate market opportunities, Request Sample

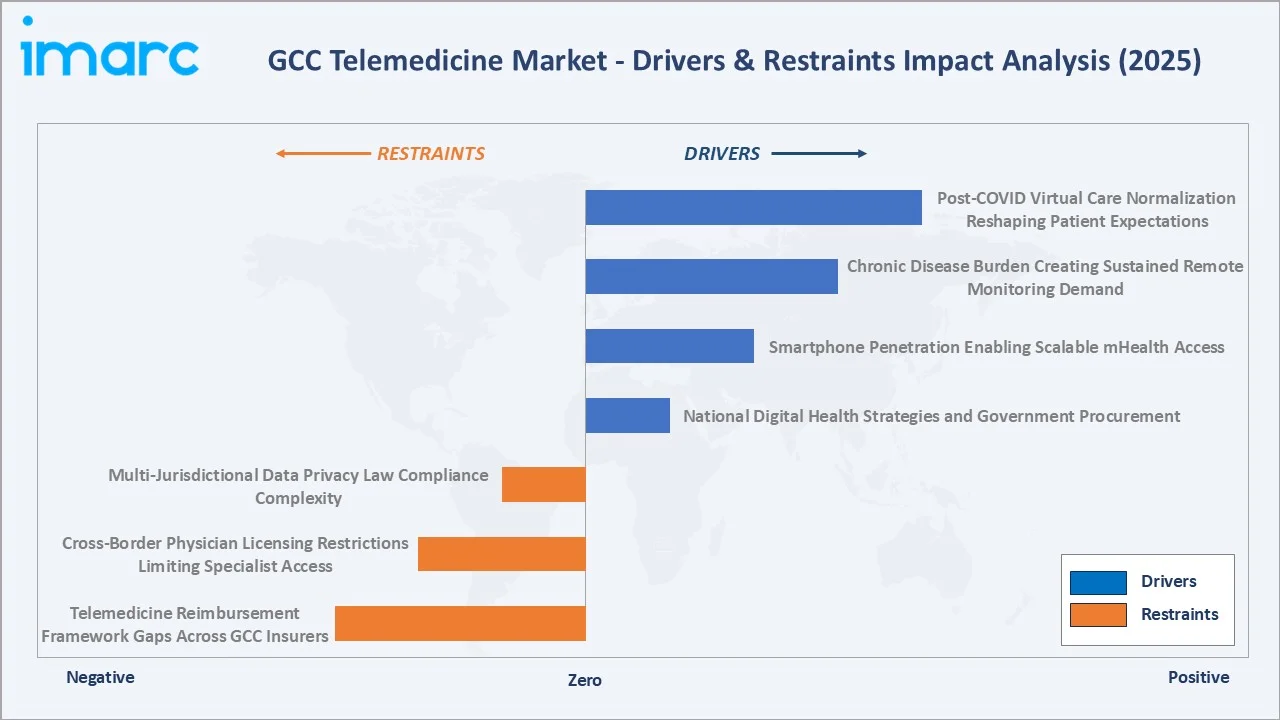

Market Drivers

- National Digital Health Strategies and Government Procurement: Under Vision 2030, the Saudi Arabian Government plans to invest over $65 billion to develop the country’s healthcare infrastructure, with telemedicine as a core delivery mechanism. These government-funded rollouts create structural demand floors independent of private sector adoption cycles, with institutional contracts representing the largest single-deal telemedicine revenues in the GCC.

- Smartphone Penetration Enabling Scalable mHealth Access: GCC's smartphone penetration, combined with 5G network leadership and internet penetration, creates ideal conditions for mHealth platform scaling. The GCC is forecast to have 62 million 5G mobile subscriptions by the end of 2026.

- Chronic Disease Burden Creating Sustained Remote Monitoring Demand: GCC's chronic disease prevalence is among the world's highest. These conditions require continuous monitoring and frequent follow-up, which telemedicine platforms serve at a lower cost per encounter versus in-person hospital visits, creating compelling healthcare system economics driving institutional adoption.

- Post-COVID Virtual Care Normalization Permanently Reshaping Patient Expectations: COVID-19 forced GCC health systems to deploy telemedicine at scale within weeks of pandemic onset. This emergency deployment permanently normalized patient expectations for virtual care access, reducing the consumer adoption barrier that had constrained pre-pandemic telemedicine growth.

Market Restraints

- Multi-Jurisdictional Data Privacy Law Compliance Complexity: GCC patients' health data is subject to distinct national cybersecurity frameworks. Cross-border telemedicine services face multi-jurisdictional data sovereignty compliance, increasing platform development costs and limiting cross-border service scalability.

- Cross-Border Physician Licensing Restrictions Limiting Specialist Access: GCC telemedicine regulations require physicians to hold valid medical licenses in the patient's country, not only in the physician's practice location. This constraint limits cross-GCC specialist telemedicine networks and restricts international physician participation, creating a shortage in specialist teleconsultation capacity for less common specialties.

- Telemedicine Reimbursement Framework Gaps Across GCC Insurers: Despite regulatory progress, comprehensive telemedicine reimbursement frameworks remain incomplete.

Market Opportunities

- AI-Powered Diagnostic Integration Transforming Teleconsultation Accuracy: AI diagnostic tools are increasing teleconsultation diagnostic accuracy to that of in-person examination. The AI research generates GCC-specific clinical AI models trained on local patient demographics, addressing disease pattern accuracy gaps that occur when using Western-trained AI models for GCC populations.

- 5G-Enabled Real-Time Remote Monitoring Scaling Chronic Disease Management: The GCC is forecast to have 62 million 5G mobile subscriptions by the end of 2026. This GCC's 5G networks enable sub-1ms latency remote patient monitoring at 100+ Mbps data speeds, making real-time RPM for GCC chronic disease patients clinically viable.

Market Challenges

- Legacy HIS Integration Complexity Extending Deployment Timelines: GCC public hospitals operate diverse hospital information systems. Integrating telemedicine platforms with these legacy systems requires much time for large hospital deployments versus greenfield facilities, slowing national telemedicine program rollout timelines and creating multi-year revenue recognition delays for platform providers.

- Digital Health Literacy Gaps in Elderly and Rural Populations: GCC's elderly population and rural communities in Saudi Arabia, Oman, and Kuwait's rural areas face digital literacy barriers.

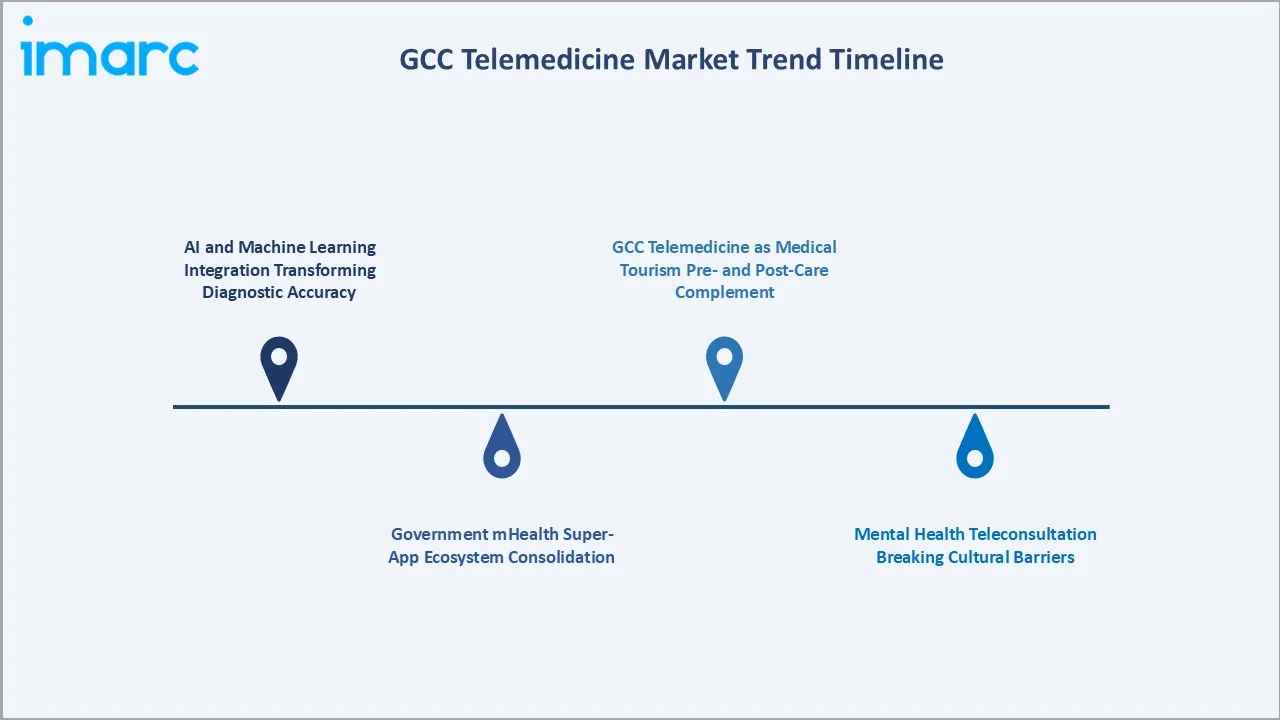

Emerging Market Trends

1. AI and Machine Learning Integration Transforming Diagnostic Accuracy

AI diagnostic tools are transforming GCC telemedicine from reactive video consultations to proactive AI-assisted diagnostic encounters. Saudi Arabian universities are generating GCC-specific clinical AI models trained on local patient demographics and disease patterns, with Saudi teleradiology interpretations expected to use AI assistance.

2. Government mHealth Super-App Ecosystem Consolidation

GCC governments are investing in comprehensive mHealth super-app platforms integrating teleconsultation, pharmacy delivery, chronic disease monitoring, vaccination records, and mental health support. These government platforms are consolidating previously fragmented digital health touchpoints into single patient engagement ecosystems.

3. Mental Health Teleconsultation Breaking Cultural Barriers

Mental health services represent the fastest-growing telemedicine application in the GCC. The anonymity of digital platforms significantly reduces social stigma barriers to mental health care access.

4. GCC Telemedicine as Medical Tourism Pre- and Post-Care Complement

GCC telemedicine is extending the region's medical tourism value proposition, enabling pre-visit virtual consultations and post-treatment remote monitoring for international patients. Dubai's Health Tourism Authority reported 691,000 medical tourists in 2023, with telemedicine pre-consultations increasing.

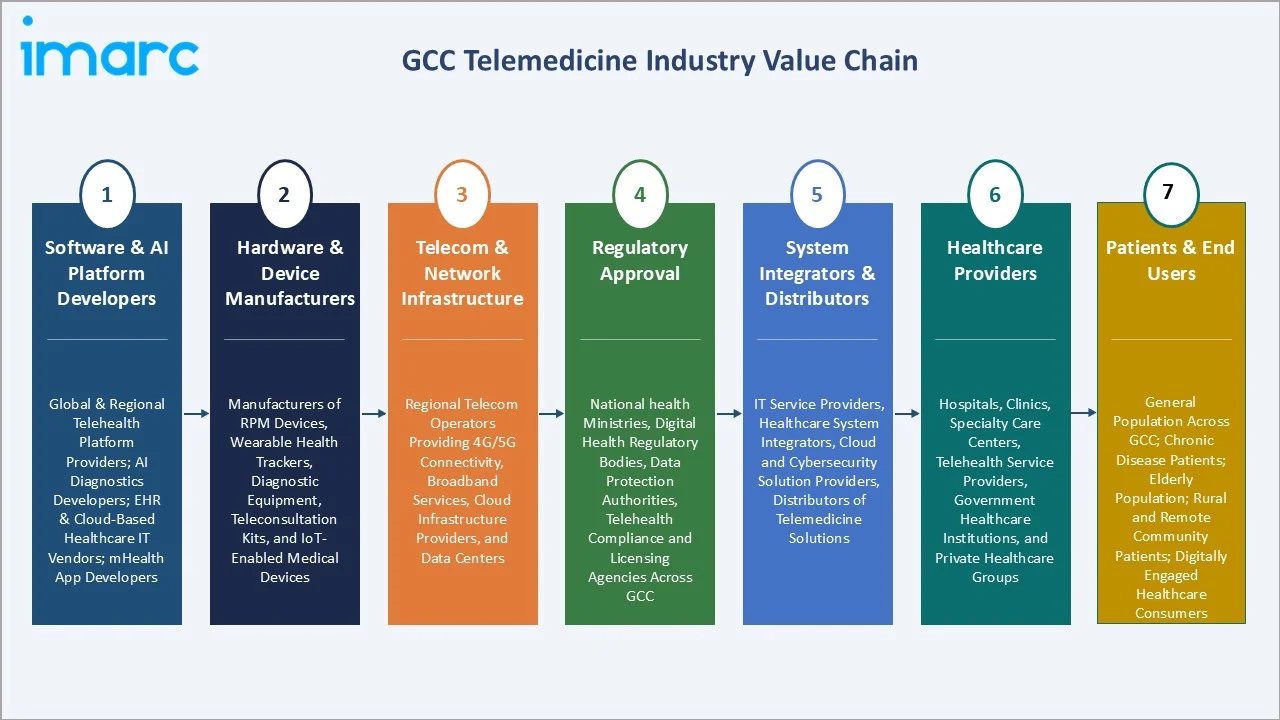

Industry Value Chain Analysis

The GCC telemedicine value chain integrates global software and hardware providers through telecommunications infrastructure, regulatory approval, system integration, and healthcare provider deployment, serving GCC citizens across six nations. Software platform providers capture 60-75% gross margins on SaaS subscriptions; telecom operators earn 30-40% on connectivity infrastructure; healthcare providers earn per-consultation fees supplementing traditional revenues.

|

Stage |

Key Participants |

|

Software & AI Platform Developers |

Global and regional telehealth platform providers; AI-driven diagnostics and remote monitoring solution developers; electronic health record (EHR) and cloud-based healthcare IT vendors; mobile health (mHealth) app developers |

|

Hardware & Device Manufacturers |

Manufacturers of remote patient monitoring (RPM) devices, wearable health trackers, diagnostic equipment, teleconsultation kits, and IoT-enabled medical devices |

|

Telecom & Network Infrastructure |

Regional telecom operators providing 4G/5G connectivity, broadband services, cloud infrastructure providers, and data centers supporting telemedicine platforms |

|

Regulatory Approval |

National health ministries, digital health regulatory bodies, data protection authorities, telehealth compliance and licensing agencies across GCC countries |

|

System Integrators & Distributors |

IT service providers, healthcare system integrators, cloud and cybersecurity solution providers, distributors of telemedicine hardware and software solutions |

|

Healthcare Providers |

Hospitals, clinics, specialty care centers, telehealth service providers, government healthcare institutions, and private healthcare groups |

|

Patients & End Users |

General population across GCC; chronic disease patients; elderly population; rural and remote community patients; digitally engaged healthcare consumers |

Government procurement dominates the GCC institutional market, representing the largest single telemedicine platform procurement entities, with individual national contracts. System integrators earn 15-25% margins on large hospital deployment projects. The emergence of direct-to-consumer mHealth app revenues, through app store subscriptions and per-consultation micro-payments, is creating a parallel consumer revenue stream alongside institutional B2B contracts.

Technology Landscape in the GCC Telemedicine Industry

AI-Powered Diagnostic and Clinical Decision Support

AI diagnostic tools are the GCC telemedicine market's highest-growth technology investment area. In June 2025, Alphaiota and PMcardio partnered to bring the first AI-powered heart attack diagnostic solution to the Kingdom of Saudi Arabia.

5G and Cloud Infrastructure for Real-Time Remote Monitoring

5G deployment across GCC is forecast to have 62 million 5G mobile subscriptions by the end of 2026, enabling sub-1ms latency remote patient monitoring at 100+ Mbps. Cloud-native architectures reduce telemedicine platform deployment time from 18 months to 3-6 months for new GCC health system contracts.

mHealth Platform and Wearable Device Integration

GCC mHealth platforms are integrating consumer wearable device data into clinical telemedicine workflows. Smart glucometer integration with GCC diabetes management platforms enables remote endocrinologist monitoring of glucose patterns without in-person clinic visits.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Component | Software | 46.8% | 2025 |

| Communication Technology | mHealth Solutions | 41.6% | 2025 |

| Hosting Type | Cloud-Based and Web-Based | 🔒 | 2025 |

| Application | Tele-Dermatology | 🔒 | 2025 |

| End User | Patients | 🔒 | 2025 |

| Country | Saudi Arabia | 39.7% | 2025 |

By Component

Software leads at 46.8% market share (2025). GCC telemedicine software encompasses clinical management platforms, AI diagnostic tools, EHR-integrated telemedicine modules, and government patient engagement apps. The software segment grows at ~23.5% CAGR (2026-2034), driven by cloud SaaS model adoption, reducing upfront capital requirements and enabling rapid national platform deployments by GCC health ministries.

To access detailed market analysis, Request Sample

Services at 30.7% encompass teleconsultation fees, remote patient monitoring subscriptions, teleradiology reading services, tele-ICU management, and telemedicine implementation services. Hardware at 22.5% covers telemedicine carts, diagnostic peripherals, and remote patient monitoring devices.

By Communication Technology

mHealth solutions lead at 41.6% market share (2025). GCC's exceptional smartphone penetration has made mobile health applications the primary telemedicine patient access channel. Government-funded platforms serve registered users, creating patient-facing infrastructure at a scale impossible in private-sector-only markets. mHealth grows at ~24.6% CAGR, the fastest segment, through 2034 as AI-integrated health apps mature beyond appointment booking to diagnostic support.

Video conferencing at 36.9% underpins specialist teleconsultation, tele-ICU, and hospital-to-hospital telemedicine networks requiring clinical-grade video interaction. Others at 21.5%, including RPM, store-and-forward teleradiology, and asynchronous messaging, represent teleradiology image submission and text-based chronic disease management programs.

Regional Market Insights

|

Country |

Share (2025) |

Key Growth Drivers & Characteristics |

|

Saudi Arabia |

39.7% |

Large population base, strong government healthcare investments, national digital health transformation programs, and high chronic disease prevalence |

|

UAE |

24.6% |

Advanced digital healthcare infrastructure, high internet and smartphone penetration, strong private healthcare sector, and growing adoption of AI-driven healthcare solutions |

|

Qatar |

12.8% |

Expansion of virtual consultation services, high healthcare spending per capita, and strong telecom infrastructure enabling telehealth delivery |

|

Oman |

9.6% |

Improving rural healthcare access, expansion of telemedicine programs, and increasing tele connectivity in remote regions |

|

Kuwait |

7.1% |

Digital transformation strategies in healthcare, increasing adoption of remote patient monitoring, and growing demand for virtual consultations |

|

Bahrain |

6.2% |

Supportive telemedicine regulations, expansion of private healthcare providers, and increasing demand for digital health services among the urban population |

Saudi Arabia's 39.7% dominance reflects the combination of the GCC's largest population, highest healthcare investment, and most comprehensive national telemedicine program. The UAE's 24.6% share reflects the most advanced GCC digital health regulatory environment, creating a regional innovation ecosystem attracting global platform providers to establish GCC headquarters.

Qatar's 12.8% is anchored by healthcare legacy infrastructure. Oman and Kuwait each represent high-growth, smaller markets investing in national telemedicine programs and digital transformation strategy frameworks.

Competitive Landscape

The GCC telemedicine market is moderately concentrated among global platform leaders at the enterprise level and highly fragmented in the specialty and consumer application layers. Teladoc Health, Philips, and Cisco Systems collectively hold an estimated 35-42% of GCC enterprise telemedicine platform revenues (2025). Government procurement contracts represent the largest individual deal values.

|

Company Name |

Platform / Product Line |

Market Position |

Core Strength |

|

Teladoc Health Inc. |

Prism |

Market Leader |

Teladoc Health connects patients and care providers for medical care, mental health, chronic condition management and more. |

|

Koninklijke Philips N.V. |

eCareManager |

Market Leader |

As a leader in telehealth with 20+ years of expertise, Philips provides flexible, scalable, configurable solutions to meet the needs. |

|

Cisco Systems Inc. |

Webex for Healthcare |

Strong Challenger |

Secure hospital network infrastructure; Webex Health HIPAA-compliant video |

|

American Well Corporation |

Amwell Converge Platform, The Amwell Platform |

Established Player |

Amwell offers many different telehealth services to address all of the health concerns. |

Competitive differentiation is increasingly driven by localization capabilities, integration with national health information exchanges, and MOH regulatory certification. Companies with established GCC regional operations, Saudi and UAE data center presence, and Arabic clinical AI models are building sustainable competitive moats that late-entering global platforms face significant barriers to replicate within the 2026-2034 forecast horizon.

Key Company Profiles

Teladoc Health Inc.

Teladoc Health is one of the world's largest virtual care companies and the leading global telemedicine platform with comprehensive GCC enterprise contracts.

- Product Portfolio: Teladoc Health Platform

- Recent Developments: In January 2026, Teladoc Health launched new enhancements to its 24/7 Care service.

- Strategic Focus: Whole-person virtual care integration combining physical and mental health with chronic condition management.

Koninklijke Philips N.V.

Koninklijke Philips N.V. is one of the GCC's leading providers of clinical-grade remote monitoring and tele-ICU solutions.

- Product Portfolio: eCare Manager.

- Recent Developments: In February 2026, Philips unveiled a suite of AI-powered innovations at the World Health Expo (WHX) Dubai 2026 to meet the region's accelerating demand for smarter, faster and more sustainable care.

- Strategic Focus: Clinical-grade telehealth for hospital-to-home care transitions in chronic disease management.

Cisco Systems Inc.

Cisco Systems provides the secure network infrastructure and enterprise clinical video conferencing platforms upon which GCC hospital telemedicine networks operate.

- Product Portfolio: Cisco Webex for Healthcare.

- Recent Developments: In April 2020, Medcare Hospitals & Medical Centres, a leading UAE healthcare provider, collaborated with Cisco Systems to introduce telehealth technology enabling patients to access advanced video-based consultations via laptops and mobile devices, allowing convenient access to high-quality healthcare services from any location.

- Strategic Focus: Secure healthcare network infrastructure as GCC telemedicine backbone.

Market Concentration Analysis

The GCC telemedicine market exhibits moderate concentration at the enterprise platform level and significant fragmentation in specialty and consumer application layers. Teladoc Health, Philips, and Cisco Systems collectively hold approximately 35-42% of GCC enterprise telemedicine platform revenues (2025), with large government hospital system contracts representing disproportionate single-deal revenue concentrations.

The specialty telemedicine layer is more fragmented, with global leaders competing with regional specialists and digital health companies. mHealth application markets are highly fragmented, with health apps active in GCC app stores, though government platforms increasingly consolidate patient engagement into single super-app ecosystems that reduce the addressable market for competing private consumer health apps.

Investment & Growth Opportunities

Fastest Growing Segments

mHealth solutions (~24.6% CAGR), software components (~23.5% CAGR), AI diagnostic platforms (~28-32% CAGR sub-segment), mental health teleconsultation (~28-32% CAGR), and chronic disease remote patient monitoring (~25% CAGR) represent the GCC's highest-growth investment vectors through 2034. AI-powered clinical decision support, enabling teleconsultation with diagnostic accuracy comparable to in-person care, is the single highest-value investment theme.

Emerging Market Opportunities

GCC's rural and underserved populations represent systematically underserved telemedicine markets. The Saudi MOH's target of connecting primary health centers creates a government procurement opportunity for rural telemedicine infrastructure providers. Bahrain's highly internet-connected population offers a high-density test market for advanced telemedicine applications before GCC-wide scaling at lower market entry risk.

Investment Themes

- Arabic clinical AI development: International AI diagnostic tools trained on Western patient datasets require clinical validation on GCC-specific populations. Investment in Arabic-language clinical NLP models and GCC-specific disease pattern AI creates defensible IP with immediate government procurement applications, where local clinical AI validation is increasingly a tender requirement.

- Tele-mental health platforms for culturally adapted care: GCC's mental health telemedicine market grows at 28-32% CAGR from a low base, with cultural anonymity preferences driving stronger digital adoption than in-person care. Arabic-language mental health platforms aligned with Islamic wellness frameworks represent a differentiated opportunity not served by Western mental health platforms entering without cultural localization.

Future Market Outlook (2026-2034)

The GCC telemedicine market is projected to grow from USD 532.9 Million in 2025 to USD 3,271.4 Million by 2034, delivering a 21.67% CAGR. This trajectory reflects one of the world's most favorable combinations of government-funded demand creation, world-class 5G digital infrastructure, high chronic disease burden requiring continuous monitoring, and ambitious national digital health transformation agendas across all six GCC member states. The market's anchor value of USD 1,420.9 Million in 2030 represents completion of Vision 2030's first digital health implementation phase.

Three structural forces define GCC telemedicine's growth trajectory with exceptional certainty: government procurement providing structural demand stability; AI integration transforming telemedicine from scheduling convenience into diagnostic-quality care delivery, expanding addressable use cases from routine consultations to complex specialist encounters; and 5G enabling real-time remote monitoring at scale for GCC's chronic disease patients, where telemedicine's economic advantage over in-person care is most pronounced.

Research Methodology

Primary Research

Primary research comprised structured interviews with 80+ industry stakeholders (2025), including Chief Digital Officers from King Abdulaziz Medical City, Cleveland Clinic Abu Dhabi, and Hamad Medical Corporation; Saudi MOH Digital Health Division and UAE MOHAP telemedicine regulatory specialists; GCC regional sales directors from Teladoc Health, Philips, and Cisco Systems; health insurance company digital health heads; and telemedicine startup founders from GCC-based digital health companies.

Secondary Research

Secondary research encompassed Saudi MOH National Telemedicine Program reports 2024, UAE MOHAP Digital Health Strategy 2021-2025 progress reports, Qatar National Health Strategy 2024-2030 documentation, GCC Health Ministers' Council digital health initiative publications, WHO EMRO digital health country assessments, HIMSS Middle East 2024 proceedings, ITU GCC digital infrastructure statistics, GSMA GCC 5G deployment reports 2025, and company press releases for all major telemedicine providers. Over 160 secondary sources were reviewed.

Forecasting Models

Market revenue forecasts used bottom-up healthcare facility count x telemedicine penetration x annual platform revenue per facility models for institutional segments, combined with per-capita digital health spending x smartphone penetration x adoption rate models for consumer mHealth segments. Key inputs include GCC population projections, Vision 2030 healthcare investment disbursement schedules, 5G rollout timelines, chronic disease prevalence, and historic telemedicine adoption acceleration from the 2020-2025 COVID normalization period.

GCC Telemedicine Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Components Covered | Software, Hardware, Services |

| Communication Technologies Covered | Video Conferencing, mHealth Solutions, Others |

| Hosting Types Covered | Cloud-Based and Web-Based, On-Premises |

| Applications Covered | Teleconsultation and Telementoring, Medical Education and Training, Teleradiology, Telecardiology, Teleneurology, Telepsychiatry, Tele-Dermatology, Others |

| End Users Covered | Providers, Patients, Payers, Others |

| Countries Covered | Saudi Arabia, UAE, Qatar, Oman, Kuwait, Bahrain |

| Companies Covered | Teladoc Health Inc., Koninklijke Philips N.V., Cisco Systems Inc., American Well Corporation, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the GCC Telemedicine Market Report

The GCC telemedicine market reached USD 532.9 Million in 2025, covering software platforms, hardware devices, and services across Saudi Arabia, UAE, Qatar, Oman, Kuwait, and Bahrain, serving citizens.

The GCC telemedicine market is projected to grow at 21.67% CAGR during 2026-2034, reaching USD 3,271.4 Million by 2034, driven by Vision 2030 investment, AI integration, 5G infrastructure, and chronic disease remote monitoring expansion.

Software leads at 46.8% (2025), driven by cloud telemedicine platforms, AI diagnostic tools, and EHR-integrated teleconsultation modules across GCC hospital networks and government health applications.

mHealth Solutions lead at 41.6% (2025), leveraging GCC smartphone penetration and government mHealth platforms delivering scalable mobile digital health access.

Saudi Arabia leads with 39.7% market share (2025), driven by Vision 2030's healthcare investment and the Sehhaty national telemedicine platform.

Leading companies include Teladoc Health Inc., Koninklijke Philips N.V., Cisco Systems Inc., and American Well Corporation, among others.

The GCC telemedicine market is projected to reach USD 1,420.9 Million by 2030, with AI-powered diagnostics becoming standard across all major hospital telemedicine networks.

AI transforms GCC telemedicine through radiology diagnostic AI, symptom triage chatbots, and predictive RPM analytics for chronic disease management, increasing diagnostic accuracy to near in-person levels.

Key applications include teleconsultation, teleradiology, telecardiology, telepsychiatry, tele-dermatology, and remote patient monitoring. Mental health teleconsultation is the fastest-growing application at 28-32% CAGR, driven by cultural anonymity preferences reducing traditional stigma barriers.

GCC telemedicine growth is driven by strong government digital health investments and strategies, along with high smartphone penetration and expanding 5G connectivity, enabling scalable virtual care. Additionally, rising chronic disease prevalence and post-COVID normalization of remote consultations are accelerating sustained adoption.

Key constraints include multi-jurisdictional data privacy compliance, cross-border physician licensing restrictions, legacy hospital HIS integration requiring 18-24 months, and inconsistent telemedicine reimbursement frameworks across GCC insurers.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)