General Aviation Market Size, Share, Trends and Forecast by Product, Application, and Region, 2026-2034

General Aviation Market Size and Share:

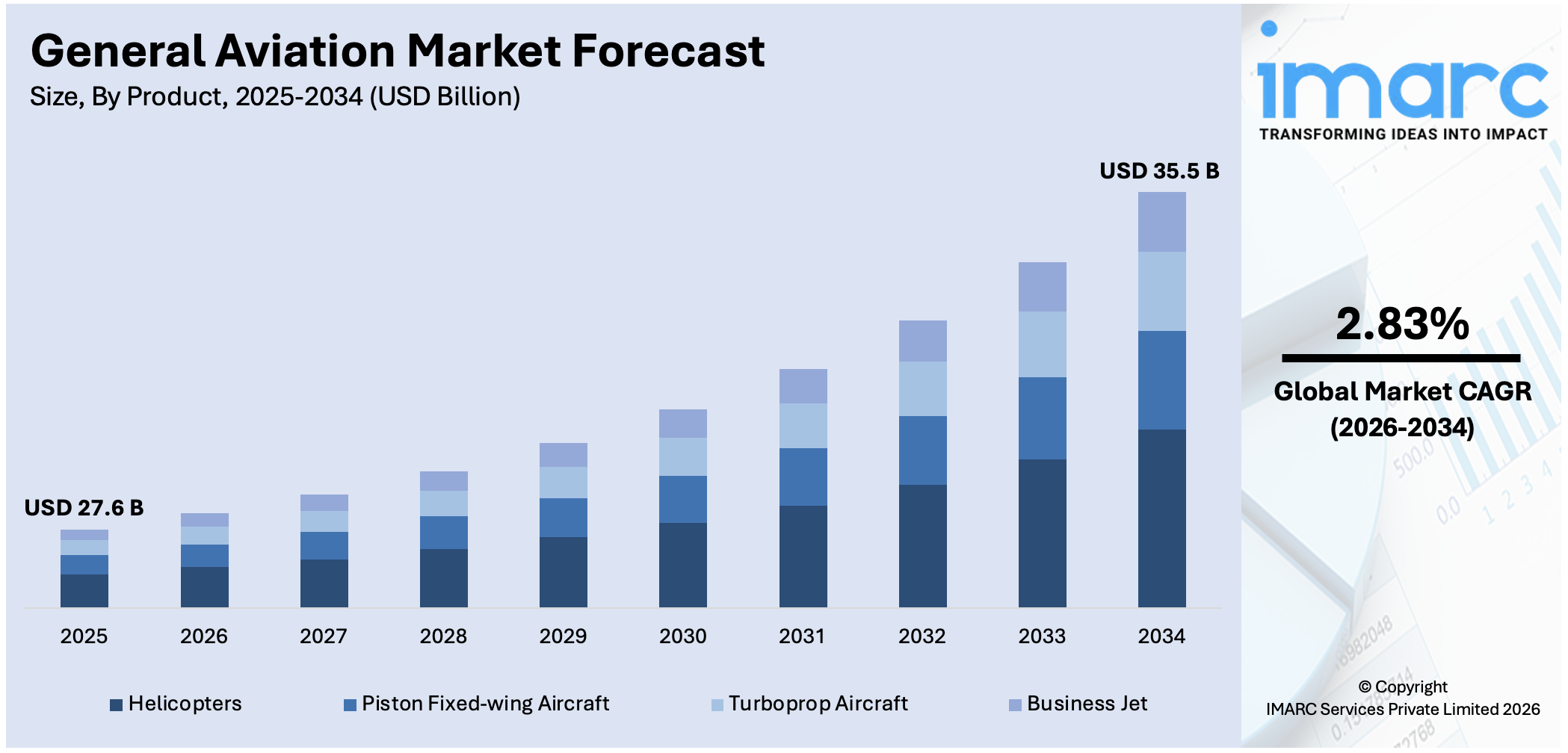

The global general aviation market size was valued at USD 27.6 Billion in 2025. Looking forward, IMARC Group estimates the market to reach USD 35.5 Billion by 2034, exhibiting a CAGR of 2.83% from 2026-2034. North America currently dominates the market. The development of urban air mobility solutions through eVTOL aircraft and autonomous flight technology, ongoing improvements in battery technology that lower operating costs, and significant investments in aviation infrastructure to improve capacity and safety in order to support increasing air traffic are all important factors.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

|

Market Size in 2025

|

USD 27.6 Billion |

|

Market Forecast in 2034

|

USD 35.5 Billion |

| Market Growth Rate (2026-2034) | 2.83% |

The global market is majorly propelled by the rising need for business and private air travel, creating a need for more flexible, time-efficient transportation options. Similarly, continual technological advancements in avionics, propulsion systems, and safety features have greatly improved aircraft performance and reliability. For example, the December 2, 2024, strategic agreement between Honeywell and Bombardier focuses on next-generation aviation technologies such as Honeywell Anthem avionics, enhanced engines, and communications by satellite, valued at USD 17 Billion. Furthermore, increasing disposable incomes, especially in emerging markets, augmenting private aircraft ownership is propelling the general aviation market share. Additionally, the demand for specialized services like air ambulance, search and rescue, and aerial surveillance supports market growth. Furthermore, favorable government incentives for sustainable aviation fuels and the development of urban air mobility solutions are driving innovation and expansion in the sector.

To get more information on this market Request Sample

The United States is a key regional market is influenced by the vast network of airports and airfields, which provide essential infrastructure for both private and commercial operations. In line with this, the growing demand for pilot training and growth in flying clubs and recreational aviation are key contributors to market activity. Furthermore, increased concerns about travel disruptions and flight cancellations are promoting more interest in private air travel. Additionally, supportive government incentives, including tax breaks and grants for aircraft ownership and operations, is further stimulating market expansion. For instance, on January 8, 2025, the Biden-Harris Administration announced over USD 332 Million in grants through the Bipartisan Infrastructure Law to modernize airports in 32 states, supporting general aviation market trends by enhancing safety and efficiency. Moreover, the growing use of drones for commercial purposes, such as surveying and delivery services, is also fueling market growth.

General Aviation Market Trends:

Growing Adoption of Electric Aircraft

Electric aircraft are rapidly gaining momentum as the aviation industry prioritizes environmental sustainability and carbon emission reduction. This transformation is powered by significant advancements in electric propulsion technologies and battery energy density improvements that enable longer flight durations and enhanced performance capabilities. Electric aircraft deliver substantial operational advantages including dramatically lower operating costs compared to traditional fuel-powered alternatives, significantly reduced noise pollution benefiting urban operations, and simplified aircraft systems that make pilot training more accessible and cost-effective. The technology appeals to flight schools, recreational pilots, and urban air mobility operators seeking environmentally responsible solutions. Aircraft manufacturers are investing billions in electric propulsion research and development, with multiple certification programs advancing toward commercial deployment. Regional operators and charter services are evaluating electric aircraft for short-haul routes where battery technology already provides viable range capabilities. The electric aircraft segment is attracting substantial venture capital and government funding as nations pursue decarbonization goals. As battery technologies continue improving and charging infrastructure expands at airports worldwide, electric aircraft adoption will accelerate across general aviation applications, fundamentally transforming the industry's environmental footprint.

Expansion of Urban Air Mobility Solutions

Urban air mobility represents a revolutionary approach to alleviating traffic congestion in densely populated metropolitan areas through innovative air transportation networks. This emerging sector leverages advanced vertical take-off and landing aircraft capable of operating from compact urban locations without traditional runway requirements. The technology is enabled by breakthroughs in autonomous flight systems, electric propulsion eliminating emissions concerns, and smart infrastructure development integrating air taxis into existing transportation networks. Major metropolitan governments are partnering with aerospace companies to establish vertiport infrastructure, air traffic management protocols, and regulatory frameworks supporting urban air mobility operations. The solutions promise dramatically reduced commute times, decreased surface traffic congestion, and enhanced accessibility to urban centers and regional destinations. Companies are developing aircraft specifically designed for urban environments with quiet operations, redundant safety systems, and passenger-friendly cabin designs. Pilot programs in major cities demonstrate technical feasibility and public acceptance. Investment from automotive manufacturers, technology companies, and traditional aerospace firms totals billions of dollars as stakeholders recognize urban air mobility's transformative potential. As certification processes advance and operational frameworks mature, urban air mobility will transition from experimental programs to routine commercial services.

Increased Investment in Aviation Infrastructure Development

Aviation infrastructure investment has emerged as a critical priority for governments and private sector stakeholders recognizing the necessity of supporting expanding air traffic volumes and modernizing aging facilities. This comprehensive investment encompasses airport terminal expansions, runway extensions and rehabilitations, modern hangar construction, and advanced air traffic management system implementations. The infrastructure improvements enhance safety through better lighting, improved navigation aids, and weather monitoring capabilities. Efficiency gains result from reduced congestion, optimized aircraft flows, and decreased ground delays. Capacity enhancements accommodate growing general aviation flight operations particularly in emerging markets experiencing rapid economic development. Emerging nations are constructing dedicated general aviation airports and regional airfields connecting secondary cities and remote areas previously lacking air connectivity. Public-private partnerships are enabling infrastructure projects through shared funding and long-term operating agreements. Advanced technologies including automated air traffic control systems, remote tower operations, and digital aircraft management platforms are being integrated into infrastructure upgrades. The investments create positive multiplier effects across aviation ecosystems including maintenance facilities, flight training centers, and parts distribution networks. This infrastructure development trend positions general aviation for sustained geographic expansion and operational resilience.

General Aviation Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global general aviation market, along with forecast at the global, regional, and country levels from 2026-2034. The market has been categorized based on product and application.

Analysis by Product:

- Helicopters

- Piston Fixed-wing Aircraft

- Turboprop Aircraft

- Business Jet

Helicopter stand as the largest segment in 2025, holding around 53.2% of the market due to their versatility, established infrastructure, and wide range of applications. They are widely employed in commercial, military, search and rescue, and medical emergency services, leading to their big market share. The helicopters also have the added advantage of going to remote regions and performing work in varied environmental conditions, aside from having the relatively lower costs of acquisition and operation compared with fixed-wing aircraft. Moreover, helicopters are necessary for oil and gas, tourism, and transport industries, leading to continued demand and growth for the segment.

Analysis by Application:

Access the comprehensive market breakdown Request Sample

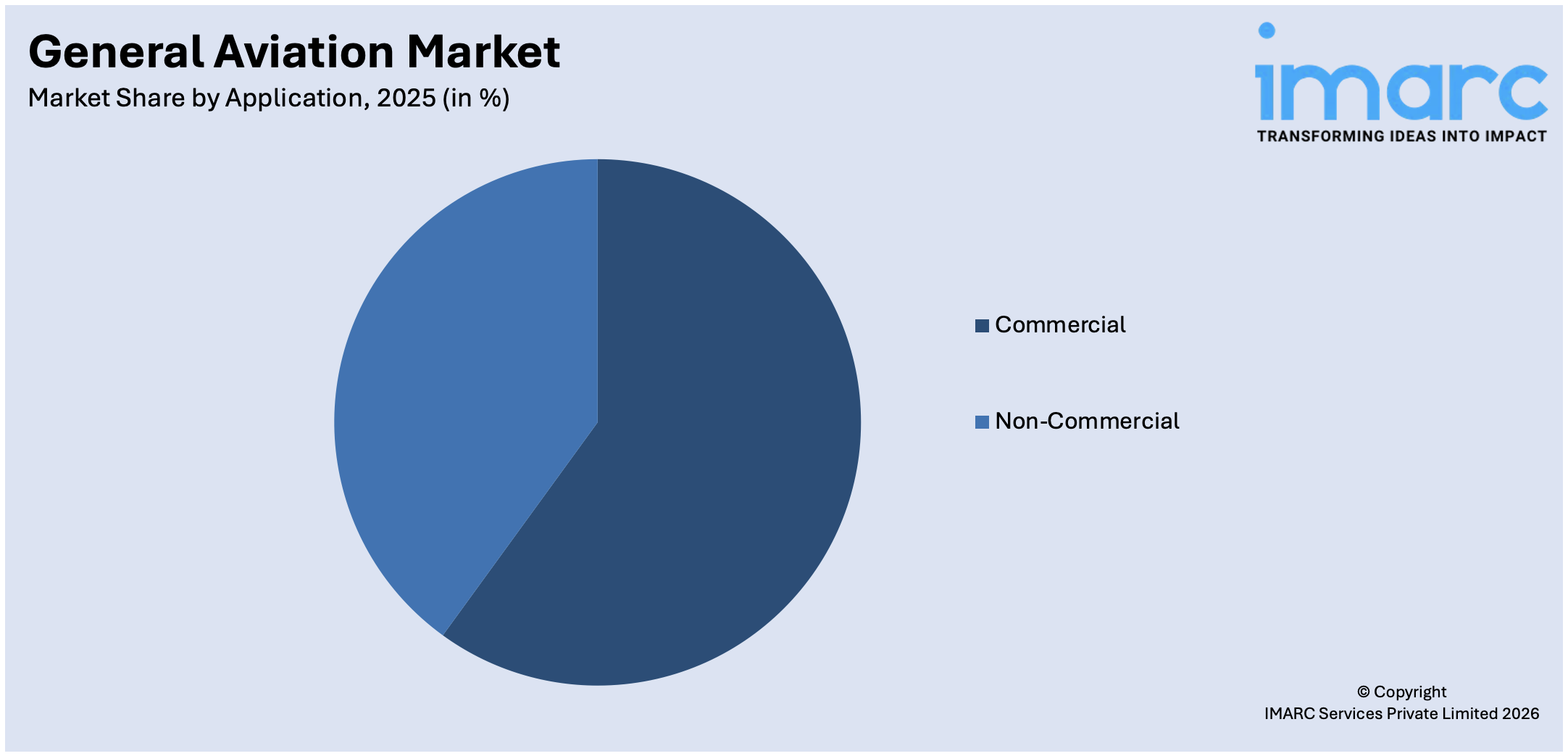

- Commercial

- Non-Commercial

Commercial applications in general aviation play an important role in meeting the diverse needs of businesses and industries. This segment involves air charter services, cargo transport, aerial surveying, and other specialized services like crop dusting and pipeline inspection. This industry is cherished given the flexibility it affords companies, giving them a route to any place without reliance on commercial airlines and their timetables. High-priority delivery, executive transportation, and emergency services require such aircraft where timely delivery matters the most. This is further expanding commercial applications with the rise of air taxis and urban air mobility solutions, particularly with the development of electric and autonomous aircraft technologies.

Non-commercial applications in the market encompass a broad spectrum of activities, including recreational flying, personal transport, flight training, and government or military use. These aircraft are typically owned by individuals, flying clubs, or small private companies for leisure or non-profit purposes. Non-commercial users often rely on general aviation for its cost-effectiveness, autonomy, and accessibility compared to commercial airline travel. Additionally, non-commercial applications serve vital functions in search and rescue operations, law enforcement, and emergency medical services. The growing popularity of private pilot licenses and the rise of hobbyist and amateur aviators also contribute to the expansion of non-commercial aviation activities.

Regional Analysis:

- North America

- United States

- Canada

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

In 2025, North America dominates the market share attributed to its extensive infrastructure, strong economic base, and high demand for private and business aviation. The region benefits from a vast network of airports, advanced aviation technology, and a large community of private pilots and aircraft owners. In addition, the U.S. alone accounts for a significant portion of global general aviation activity driven by a strong culture of aviation and favorable regulations. For instance, Gulfstream, a leading business jet manufacturer which is based in the U.S., highlights the region's influence on the market.

Key Regional Takeaways:

United States General Aviation Market Analysis

The United States maintains its commanding position accounting for a significant majority of the North American market, sustained by a robust economy, extensively developed aviation infrastructure, and deeply embedded cultural affinity for private aviation. Business aviation demand continues accelerating as corporations and entrepreneurs prioritize efficient, flexible transportation enabling enhanced productivity and competitive advantages. The nation's vast network of regional airports, exceeding five thousand facilities, provides unparalleled accessibility to urban centers and remote locations unavailable through commercial airline service. Urban air mobility initiatives are advancing rapidly with multiple cities developing vertiport infrastructure and regulatory frameworks for air taxi operations. Emergency medical services, search and rescue operations, and disaster response capabilities increasingly rely on general aviation assets. Government support through favorable tax policies, infrastructure modernization grants, and streamlined certification processes creates an advantageous business environment. The sustainability movement is driving adoption of electric aircraft technologies, sustainable aviation fuel utilization, and carbon offset programs positioning American operators as environmental leaders. Flight training institutions are expanding capacity to address pilot shortages while incorporating advanced simulation technologies and accelerated training pathways.

Europe General Aviation Market Analysis

European general aviation experiences steady expansion propelled by increasing high-net-worth individual populations seeking private aviation services and time-efficient travel alternatives to commercial airlines. Urbanization trends across the continent amplify demand for air taxis and urban air mobility solutions particularly in congested metropolitan areas where ground transportation faces severe capacity constraints. Business aviation remains robust as corporations leverage private flights for executive transportation, client entertainment, and operational flexibility. Regulatory harmonization initiatives across member states are streamlining operations, standardizing safety protocols, and reducing administrative burdens for operators conducting international flights. Sustainability imperatives drive significant innovation in electric aircraft development, sustainable aviation fuel adoption, and carbon reduction programs aligned with aggressive climate targets. Flight training programs are attracting new generations of aviators through modern curricula, advanced simulation technologies, and career pathway partnerships with commercial airlines. Digital transformation including aircraft management software, predictive maintenance systems, and enhanced air traffic control technologies improves operational efficiency and safety outcomes. Investment in regional airport infrastructure expands accessibility while modernization programs upgrade facilities to accommodate contemporary aircraft requirements.

Asia Pacific General Aviation Market Analysis

The Asia-Pacific region demonstrates exceptional growth potential driven by rapid economic development, expanding corporate sectors, and surging high-net-worth individual populations across major economies. Urbanization proceeding at unprecedented rates creates substantial demand for private aviation services and air taxi solutions addressing severe ground transportation congestion in megacities. Infrastructure development including new regional airports, dedicated general aviation facilities, and modernized air traffic management systems supports sector expansion and operational efficiency. Air cargo demand grows robustly particularly in remote areas and island nations where general aviation provides essential connectivity for commerce and essential services. Regulatory frameworks are evolving to accommodate sector growth with governments implementing certification standards, safety regulations, and operational guidelines. Flight training capacity expansion addresses pilot shortages through new aviation academies, university programs, and international partnerships. Tourism sectors leverage general aviation for destination accessibility, scenic flights, and luxury travel experiences. Government aviation development programs provide financial incentives, infrastructure investments, and policy support recognizing general aviation's economic contributions and connectivity benefits.

Latin America General Aviation Market Analysis

Latin American general aviation fulfills critical transportation needs in remote and underserved regions where geography and sparse populations make commercial airline service economically unviable. Private aviation accessibility expands among business owners, agricultural operators, and executives requiring flexible travel to dispersed operations and markets. Urbanization reaching approximately eighty percent creates concentrated demand for air mobility solutions in major metropolitan areas experiencing severe ground traffic congestion. Tourism growth drives scenic flight operations, remote resort accessibility, and adventure aviation services. Agricultural aviation supports crop management, livestock operations, and forestry monitoring across vast rural areas. Medical evacuation services provide essential healthcare access to remote communities lacking advanced medical facilities. Infrastructure challenges including limited airport facilities and navigation aid coverage constrain operations in some regions. Regulatory environments vary significantly across nations affecting operational consistency and safety standards.

Middle East and Africa General Aviation Market Analysis

The Middle East and North Africa region demonstrates robust general aviation demand driven by substantial high-net-worth individual populations concentrated in Gulf Cooperation Council nations seeking private aviation services. Urbanization exceeding sixty percent creates strong demand for business aviation and private flights particularly in densely populated commercial centers and rapidly developing cities. New airport development and aviation hub establishment, especially across Gulf countries, significantly enhances operational infrastructure supporting international and regional connectivity. Air mobility services including aircraft chartering, fractional ownership programs, and air taxi services experience growing adoption among business travelers and affluent individuals. Oil and gas sector operations rely extensively on helicopter services for offshore platform access and remote facility transportation. Tourism development leverages general aviation for destination accessibility and luxury travel experiences. Political instability and security concerns in certain regions create operational challenges affecting insurance costs and route viability.

Competitive Landscape:

The competitive landscape in the general aviation market has a mix of established giants and emerging innovators. Companies with leadership positions hold the a big share of the production of conventional aircraft, ranging from fixed-wing to helicopters to turboprops. The urban air mobility space is growing on the back of startups emphasized on electric vertical take-off and landing (eVTOL) aircraft. There are also more aggressive competitors in the avionics, flight training, and infrastructure segments. Companies are entering into strategic collaborations, mergers, and acquisitions in a bid to increase their reach in air taxis, cargo, and recreational aviation as demand grows. For example, on July 23, 2024, HIF Global and Airbus signed an MoU to take e-SAF production forward for a net-zero-emission future of the aviation industry. It is also making progress on its commercial-scale e-Fuel facilities in Texas, Uruguay, Australia, and Chile.

The report provides a comprehensive analysis of the competitive landscape in the general aviation market with detailed profiles of all major companies, including:

- Bombardier

- Cirrus Design Corporation D/B/A Cirrus

- Dassault Aviation

- Diamond Aircraft Industries

- Eclipse Aerospace, Inc.

- Embraer

- Gulfstream Aerospace Corporation

- Honda Aircraft Company

- Pilatus Aircraft Ltd

- Piper Aircraft, Inc

- Robinson Helicopter Company

- Textron Aviation Inc.

Latest News and Developments:

- January 2025: GMR Airports Ltd has entered into a Share Purchase Agreement to acquire up to 5,00,000 equity shares and 1,90,00,000 Non-Cumulative Compulsorily Convertible Preference Shares (CCPS) of Bird Delhi General Aviation Services Private Ltd, representing 50% of its paid-up share capital.

- January 2025: The Biden-Harris Administration announced over USD 332 Million in grants through the Bipartisan Infrastructure Law to modernize airports in 32 states. The initiative supports general aviation market trends by enhancing safety, efficiency, and infrastructure across regional and general aviation facilities nationwide.

- October 2025: Gulfstream Aerospace Corp. announced its fleet of corporate, demonstration, and support aircraft has surpassed 3 million nautical miles flown on sustainable aviation fuel blends. The company showcased the G800, G700, G600, and G400 at NBAA-BACE 2025, demonstrating leadership in sustainability innovations and advancing business aviation's environmental goals.

- October 2025: Honda Aircraft Company became the first twin-turbine very light business jet manufacturer to fly the HondaJet on 100% sustainable aviation fuel in October 2025. This achievement demonstrates the viability of sustainable fuel alternatives in light business aviation and reinforces Honda's commitment to environmental stewardship and technological innovation.

General Aviation Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered | Helicopters, Piston Fixed-wing Aircraft, Turboprop Aircraft, Business Jet |

| Applications Covered | Commercial, Non-Commercial |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Bombardier, Cirrus Design Corporation D/B/A Cirrus, Dassault Aviation, Diamond Aircraft Industries, Eclipse Aerospace, Inc., Embraer, Gulfstream Aerospace Corporation, Honda Aircraft Company, Pilatus Aircraft Ltd, Piper Aircraft, Inc, Robinson Helicopter Company, Textron Aviation Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the general aviation market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global general aviation market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the general aviation industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the General Aviation Market Report

The general aviation market was valued at USD 27.6 Billion in 2025.

The general aviation market is projected to exhibit a CAGR of 2.83% during 2026-2034, reaching a value of USD 35.5 Billion by 2034.

Key factors include continuous advancements in battery technology reducing operating costs, growth of urban air mobility solutions through eVTOL aircraft and autonomous flight technology, and substantial investments in aviation infrastructure to enhance capacity and safety, supporting rising air traffic.

North America currently dominates the general aviation market. This dominance is fueled by extensive infrastructure, high demand for private aviation, and a strong culture of aviation in the United States.

Some of the major players in the general aviation market include Bombardier, Cirrus Design Corporation D/B/A Cirrus, Dassault Aviation, Diamond Aircraft Industries, Eclipse Aerospace, Inc., Embraer, Gulfstream Aerospace Corporation, Honda Aircraft Company, Pilatus Aircraft Ltd, Piper Aircraft, Inc, Robinson Helicopter Company, and Textron Aviation Inc., among others.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)