Germany Diabetes Market Size, Share, Trends and Forecast by Segment and Distribution Channel, 2026-2034

Germany Diabetes Market Size, Share, Trends & Forecast (2026-2034)

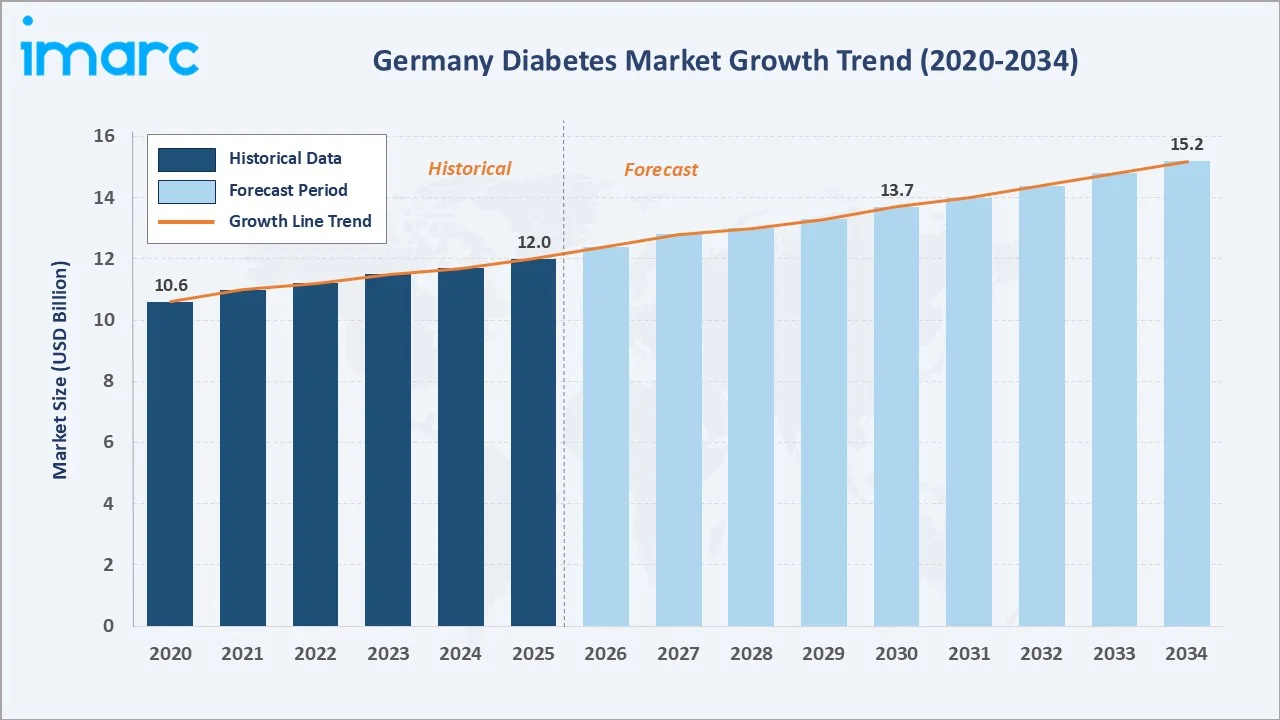

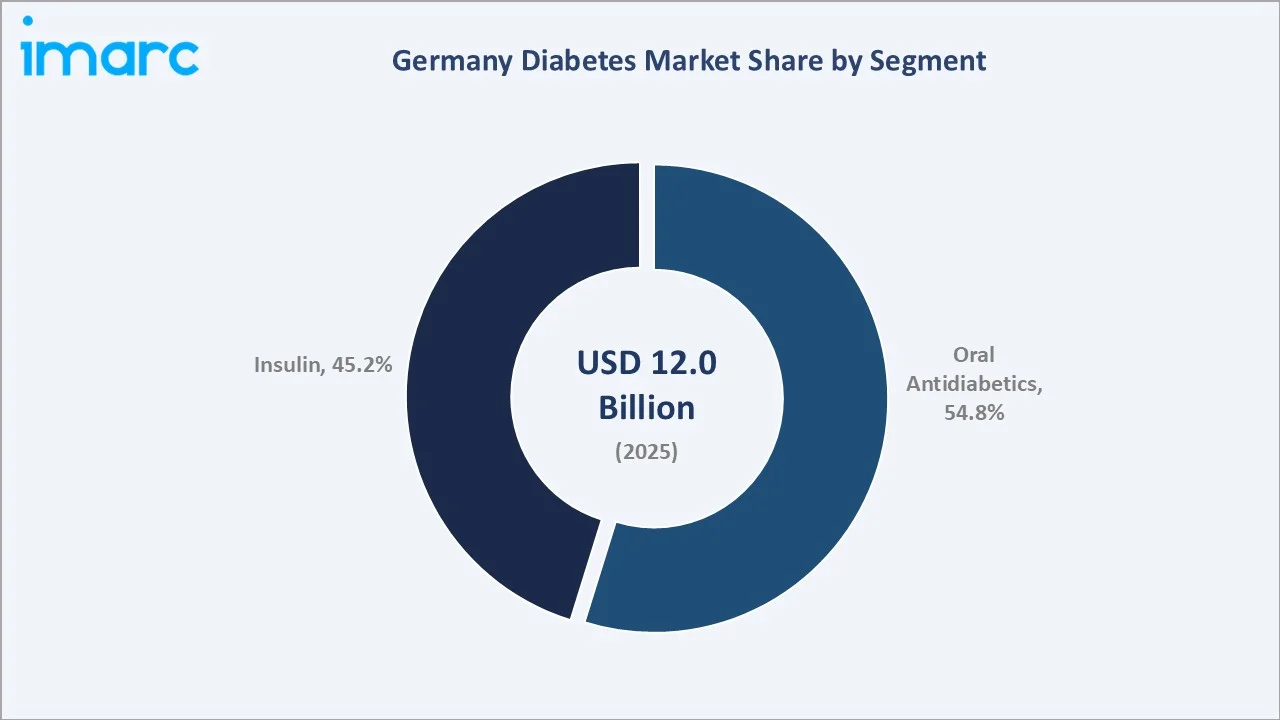

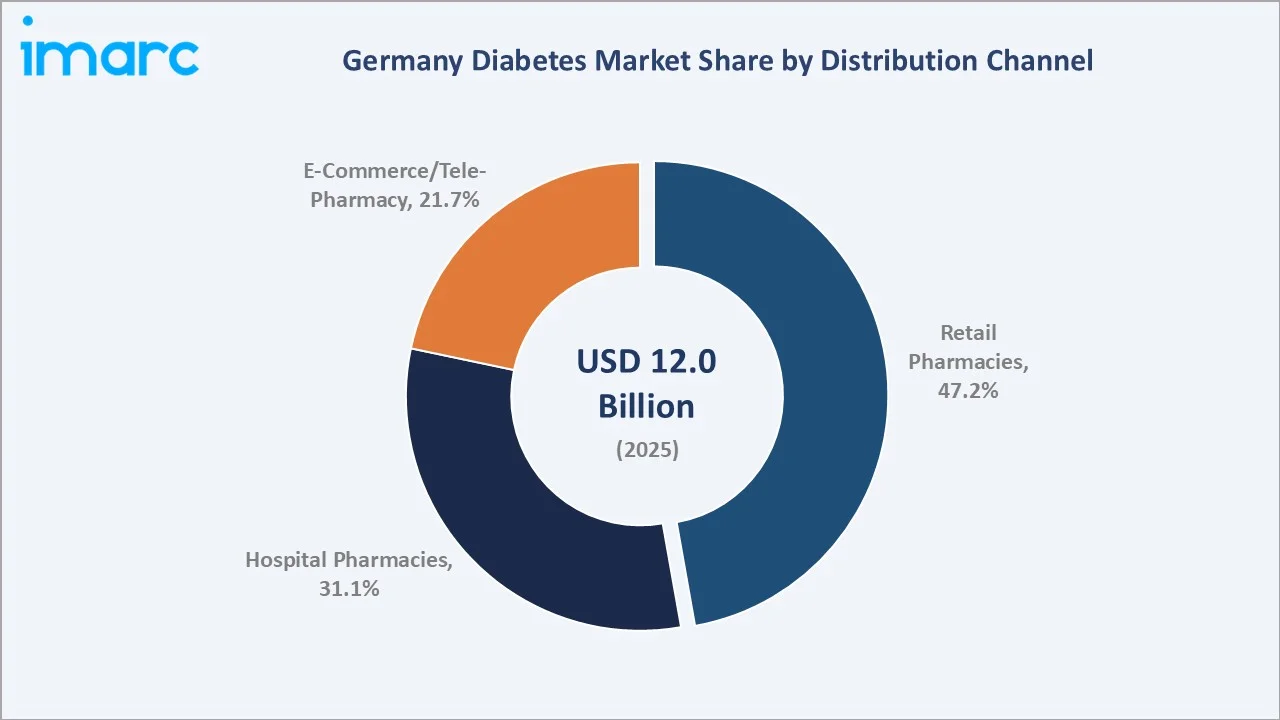

The Germany diabetes market was valued at USD 12.0 Billion in 2025 and is projected to reach USD 15.2 Billion by 2034, expanding at a CAGR of 2.58% during 2026-2034. The number of adults (20–79 years) with diabetes in Germany is 6.5 million in 2024. Growth is driven by the aging population, rising Type-2 diabetes incidence with around 8.9 million in 2023, and Germany's statutory health insurance (GKV) covering over 90% of the population. Oral Antidiabetics lead with 54.8% share in 2025, followed by Insulin at 45.2%, and retail pharmacies lead in the distribution channel with 47.2% share

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 12.0 Billion |

|

Forecast Market Size (2034) |

USD 15.2 Billion |

|

CAGR (2026-2034) |

2.58% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

The Germany diabetes market expanded from an estimated USD 10.6 Billion in 2020 to USD 12.0 Billion in 2025, anchored at USD 13.7 Billion in 2030 and projected to reach USD 15.2 Billion by 2034. The post-2020 growth reflects GLP-1 agonist class uptake, digital health app adoption, and steady GKV reimbursement support.

To get more information on this market, Request Sample

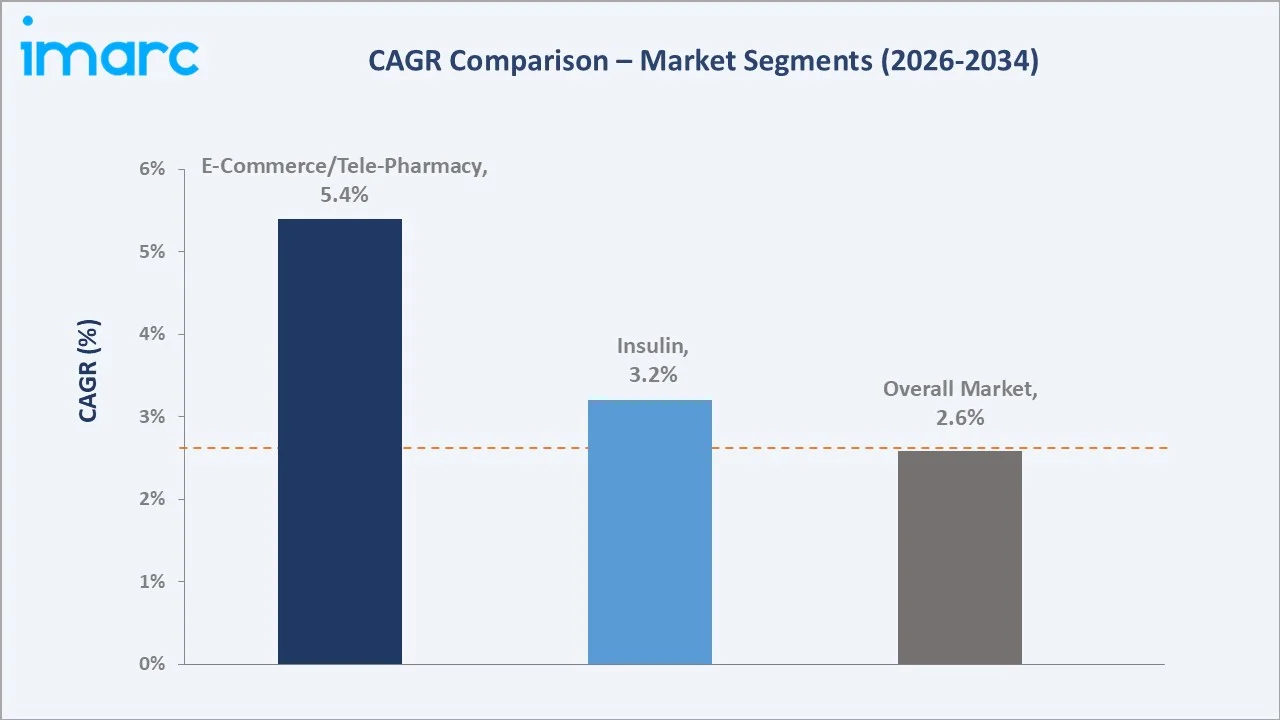

E-Commerce/Tele-Pharmacy grows fastest among distribution channels at ~5.4% CAGR (2026-2034), reflecting the post-pandemic shift to online medication dispensing. Oral Antidiabetics grow faster, driven by wider prescription of newer-generation SGLT-2 inhibitors and DPP-4 inhibitors within the oral segment.

Executive Summary

The Germany diabetes market reached USD 12.0 Billion in 2025, underpinned by 6.5 million recorded diabetes patients in 2024 and one of Europe's most comprehensive statutory reimbursement systems. Germany's GKV covers over 90% of the population, ensuring broad access to both oral antidiabetics and insulin therapies, creating a structurally large, policy-supported revenue base. The market is projected to reach USD 15.2 Billion by 2034 at a 2.58% CAGR, driven by Germany's aging demographics, rising lifestyle-related Type-2 prevalence, GLP-1 agonist class expansion, digital health platform adoption, and continuous glucose monitoring (CGM) device uptake.

Oral Antidiabetics command 54.8% market share in 2025, led by metformin and newer classes including SGLT-2 inhibitors and GLP-1 receptor agonists. Insulin retains 45.2% share, supported by stable Type-1 diabetes prevalence and basal insulin demand from advanced Type-2 cases. Retail pharmacies lead distribution at 47.2% of 2025 revenues, reflecting Germany's licensed pharmacies serving as the primary dispensing channel.

Key Market Insights

|

Insight |

Data |

|

Largest Segment |

Oral Antidiabetics - 54.8% revenue share (2025) |

|

Leading Distribution Channel |

Retail Pharmacies - 47.2% share (2025) |

Key Analytical Observations Supporting the Above Data:

- Oral Antidiabetics at 54.8% share (2025) driven by metformin's first-line status: Germany's Type-2 diabetes prevalence, with around 8.9 million. This rising prevalence strengthens the treatment guidelines positions metformin as universal first-line therapy, creating a structurally high-volume prescription base. Newer SGLT-2 inhibitors and GLP-1 agonists are expanding the premium oral segment.

- Retail Pharmacies at 47.2% anchored by Germany's pharmacy network: Germany has 17,500 pharmacies, which mandates prescription dispensing through licensed pharmacies, ensuring retail pharmacies remain the primary diabetes medication access point with stable, regulated revenue.

Germany Diabetes Market Overview

Germany's diabetes market encompasses all pharmaceutical treatments, monitoring devices, and digital management solutions for patients with Type-1, Type-2, and gestational diabetes. The ecosystem integrates pharmaceutical manufacturers, biotech innovators, regulatory bodies, statutory health insurers, wholesale distributors, and retail/hospital/e-pharmacy dispensing channels serving diabetes patients.

The market is regulated under Germany's AMNOG (The German Reform Act on the Reorganisation Of Market For Medicinal Products) framework, which mandates early benefit assessments for new drugs, setting reimbursement negotiations between manufacturers and insurers. Macroeconomic influences include Germany's aging demographic structure, rising obesity rates, a primary Type-2 risk factor, increasing healthcare expenditure, and post-COVID telehealth adoption.

Market Dynamics

To evaluate market opportunities, Request Sample

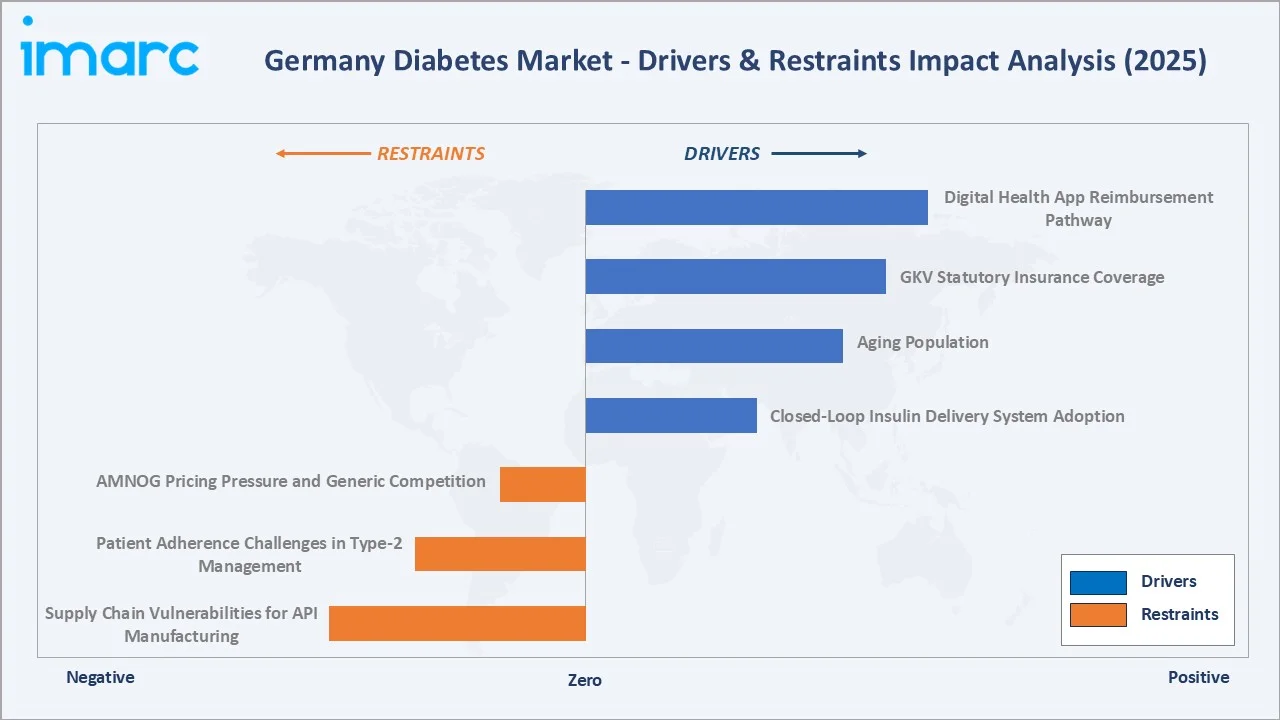

Market Drivers

- Aging Population: Germany’s population age 65 and older is projected to grow by 41% to 24 million by 2050, accounting for nearly one-third of the total population, which has a significantly higher Type-2 diabetes prevalence, driving disproportionate insulin and oral antidiabetic prescription volumes from the geriatric segment.

- GKV Statutory Insurance Coverage: Germany's GKV covers 90% of the German population, with diabetes medications reimbursed under therapeutic necessity classifications. This near-universal coverage eliminates the affordability barrier present in other markets, creating a structurally reliable revenue base for manufacturers.

- Digital Health App Reimbursement Pathway: Germany's digital health app framework is driving the market growth. In July 2025, Diabeloop launched its DBLG1 algorithm with the Dana-i insulin pump from Sooil in Germany.

Market Restraints

- AMNOG Pricing Pressure and Generic Competition: Germany's AMNOG mandatory early benefit assessment restricts pharmaceutical launch pricing for new diabetes drugs unless proven clinical superiority.

- Patient Adherence Challenges in Type-2 Management: Adherence to oral antidiabetic regimens in Germany is estimated to be long-term, driven by side effects, polypharmacy complexity in elderly patients, and lifestyle modification resistance.

Market Opportunities

- GLP-1 Agonist Class Expansion into Cardiovascular and Renal Indications: Semaglutide and dulaglutide have received EMA approval for cardiovascular risk reduction in high-risk Type-2 patients, expanding GKV reimbursement eligibility beyond glycemic control. This dual-indication positioning could add high value to Germany's premium diabetes drug market by 2030.

- Closed-Loop Insulin Delivery System Adoption: In 2019, Medtronic received Germany's statutory health insurance system reimbursement for the MiniMed 670G hybrid closed-loop insulin pump system for people with type 1 diabetes, enabling automated insulin delivery for type 1 patients.

Market Challenges

- Supply Chain Vulnerabilities for API Manufacturing: Germany's oral antidiabetic API supply (including metformin and glipizide) relies heavily on Indian and Chinese API manufacturers. These metformin supply disruptions highlight structural risks in Germany's generic diabetes drug supply chain.

- Reimbursement Delays Under AMNOG for Novel Therapies: The AMNOG early benefit assessment process averages 12-18 months post-launch before reimbursement price negotiation completion, creating a delayed market access window for novel GLP-1, SGLT-2, and closed-loop device therapies versus other European markets.

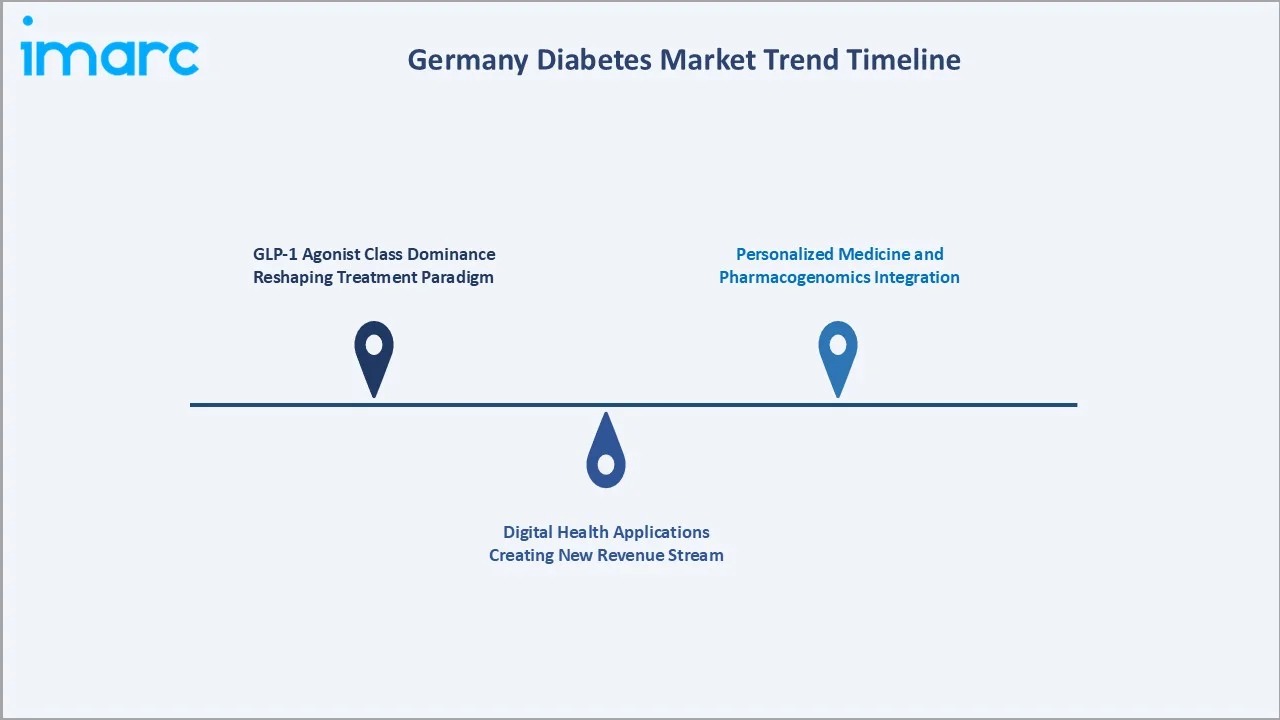

Emerging Market Trends

1. GLP-1 Agonist Class Dominance Reshaping Treatment Paradigm

GLP-1 receptor agonists (semaglutide, dulaglutide, liraglutide) have emerged as Germany's fastest-growing diabetes drug class. By 2030, GLP-1 agonists are projected to exceed insulin revenues within Germany's premium diabetes market.

2. Digital Health Applications Creating New Revenue Stream

Germany's pioneering digital health apps reimbursement framework has created a high annual market for digital diabetes management apps. Apps provide GKV-reimbursed digital therapeutic programs, fundamentally expanding the addressable diabetes market beyond pharmaceuticals into connected health services.

3. Personalized Medicine and Pharmacogenomics Integration

German academic centers are integrating pharmacogenomics into diabetes treatment protocols, identifying patient-specific responses to SGLT-2 inhibitors and metformin variants. This precision medicine approach is expected to influence GKV reimbursement guidelines for personalized therapy selection.

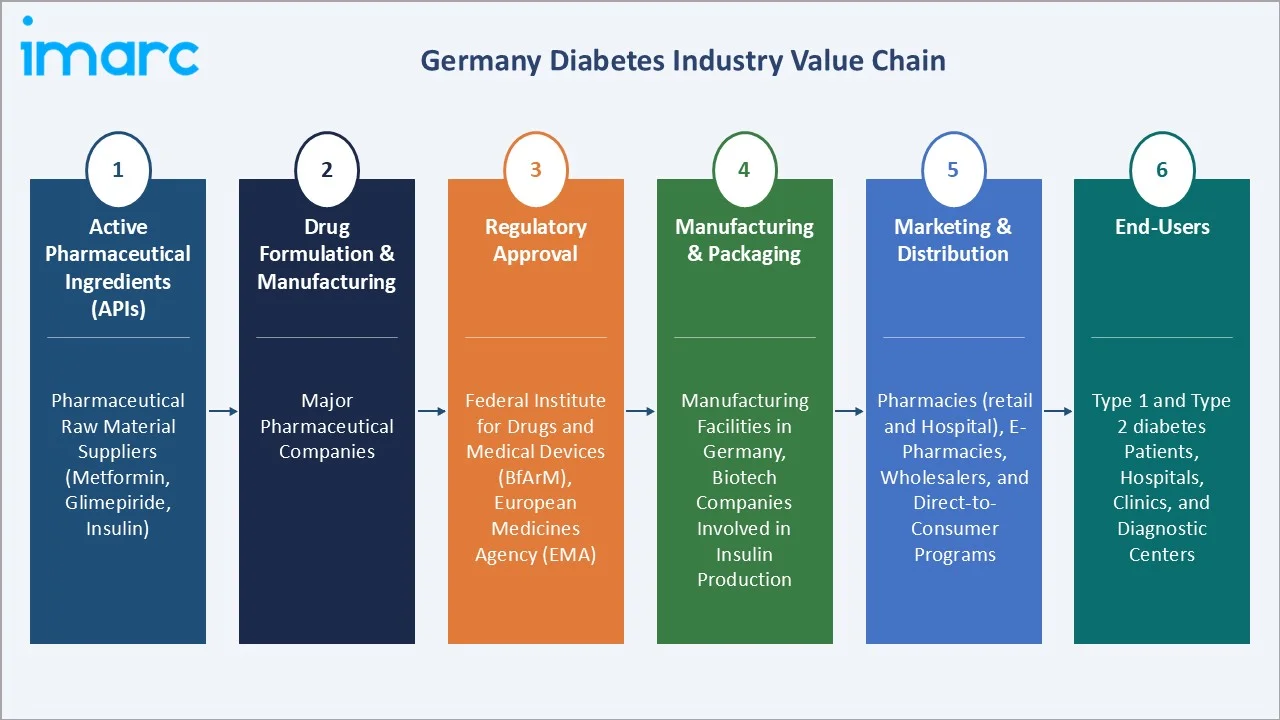

Industry Value Chain Analysis

Germany's diabetes market value chain integrates API manufacturing through pharmaceutical production, regulatory approval, multi-channel distribution, and end-patient dispensing serving over 6.5 million diabetes patients under GKV statutory reimbursement.

|

Stage |

Key Participants |

|

Active Pharmaceutical Ingredients (APIs) |

Pharmaceutical raw material suppliers (active ingredients like metformin, glimepiride, insulin) |

|

Drug Formulation & Manufacturing |

Major pharmaceutical companies |

|

Regulatory Approval |

Federal Institute for Drugs and Medical Devices (BfArM), European Medicines Agency (EMA) |

|

Manufacturing & Packaging |

Manufacturing facilities in Germany, biotech companies involved in insulin production |

|

Marketing & Distribution |

Distribution channels through pharmacies (both retail and hospital), e-pharmacies, wholesalers, and direct-to-consumer programs |

|

End-Users |

Type 1 and Type 2 diabetes patients, hospitals, clinics, and diagnostic centers |

Pharmaceutical manufacturers capture the highest value-added margins at 60-70% gross margins on branded insulin analogs. Wholesale distributors operate on 3-5% margins under regulated German pharmaceutical pricing. Retail pharmacies earn high dispensing fees per prescription under the German Prescription Drug Price Regulation.

Technology Landscape in the Germany Diabetes Industry

Continuous Glucose Monitoring (CGM) Systems

Senseonics Holdings, Inc. announced that its Eversense 365 CE Mark submission, which meets the EU Medical Device Regulation (MDR) requirements, has been approved for commercialization in the European Union (EU). The company plans to launch the Eversense 365 in Germany in 2026. Real-time CGM devices are transforming diabetes monitoring in Germany with factory-calibrated, sensor-based glucose readings every minute.

Digital Health Applications and AI Integration

Germany's approved diabetes apps incorporate machine learning algorithms for insulin dose recommendation, dietary pattern analysis, and HbA1c trajectory prediction. In November 2024, Temedica introduced its innovative digital companion, Dibi, aimed at individuals with Type 2 diabetes. Sponsored by Novo Nordisk Pharma GmbH, Germany, the app provides extensive support throughout all stages of diabetes care, with a special emphasis on assisting insulin-naïve patients who are beginning insulin therapy.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Segment | Oral Antidiabetics | 54.8% | 2025 |

| Distribution Channel | Retail Pharmacies | 47.2% | 2025 |

By Segment

Oral antidiabetics lead at 54.8% market share (2025). Germany's Type-2 diabetes first-line metformin protocol, combined with second-line SGLT-2 inhibitors and GLP-1 agonists, creates a high-volume, premium-shifting oral antidiabetic market. The segment grows as GLP-1 reclassification into the oral drug category expands volume.

To access detailed market analysis, Request Sample

Insulin retains 45.2% share (2025), anchored by Germany's more than 37,000 children and adolescents as well as 340,000 adults (2023) type-1 patients requiring lifelong insulin therapy and advanced Type-2 patients progressing to insulin from oral therapies. Basal insulin analogs constitute the premium insulin franchise. The insulin segment grows as biosimilar insulin entrants apply pricing pressure.

By Distribution Channel

Retail pharmacies lead at 47.2% market share (2025). Germany's licensed retail pharmacies remain the primary diabetes medication dispensing channel, supported by AMPreisV fixed dispensing fees, pharmacist consultation mandates, and geographic accessibility.

Hospital pharmacies hold 31.1% share (2025), serving inpatient diabetes management for hospitalized patients across Germany's hospitals. E-Commerce/Tele-Pharmacy at 21.7% grows fastest at ~5.4% CAGR, driven by diabetes prescriptions under GKV discount frameworks.

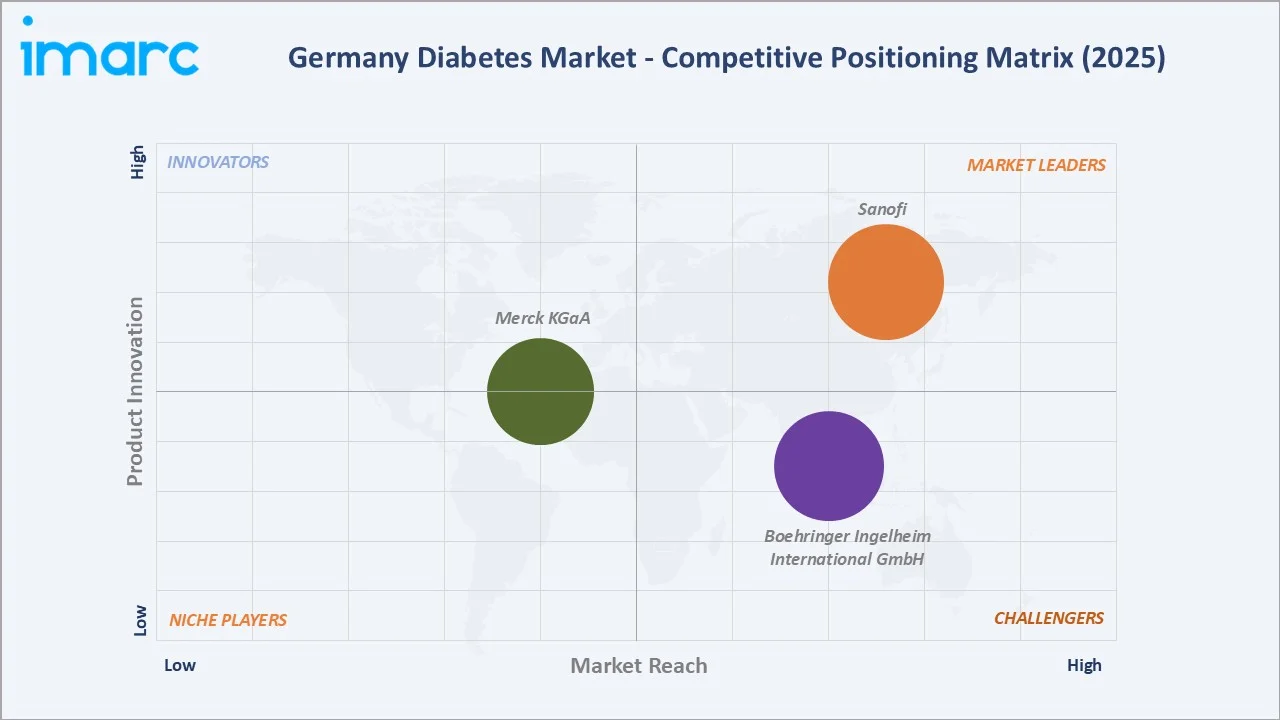

Competitive Landscape

Germany's diabetes market is moderately concentrated at the branded pharmaceutical level and fragmented in the generic oral antidiabetic segment. Boehringer Ingelheim and Merck collectively account for approximately 35-40% of the total Germany diabetes market revenues (2025), driven by their insulin franchise dominance and GLP-1 agonist leadership, respectively.

|

Company Name |

Brand / Product |

Market Position |

Core Strength |

|

Boehringer Ingelheim International GmbH |

Jardiance, Trajenta |

Strong Challenger |

Boehringer Ingelheim GmbH stands out in the Germany diabetes market through its pioneering approach in developing oral diabetes treatments and biologics, transforming how patients manage their condition. |

|

Merck KGaA |

Glucophage |

Established Player |

Metformin franchise through Glucophage remains Germany's high-volume oral antidiabetic brand |

|

Sanofi |

Lantus, Toujeo, Soliqua |

Market Leader |

Sanofi is one of the largest pharmaceutical companies and a historical leader of the diabetes market. |

The competitive landscape is being disrupted by device and digital health entrants, who are collectively capturing 8-10% of total diabetes market revenues by shifting value from traditional pharmaceutical dispensing to connected device ecosystems, a trend accelerating toward 2034.

Key Company Profiles

Boehringer Ingelheim International GmbH

Boehringer Ingelheim, headquartered in Ingelheim am Rhein, Germany, holds a structurally advantaged domestic market position as the leading SGLT-2 inhibitor company in Germany.

- Product Portfolio: Jardiance, Trajenta.

- Recent Developments: In August 2025, Boehringer Ingelheim and Palatin Technologies, Inc., announced a global research collaboration and licensing agreement aiming to develop an innovative therapy for retinal diseases including diabetic retinopathy.

- Strategic Focus: Jardiance multi-indication positioning across diabetes, heart failure, and CKD cardiometabolic continuum; DPP-4 inhibitor Trajenta maintenance in elderly diabetic patients where SGLT-2 tolerability limitations drive DPP-4 persistence.

Merck KGaA

Merck KGaA, headquartered in Darmstadt, Germany, maintains a significant diabetes presence through Glucophage (branded metformin).

- Product Portfolio: Glucophage (metformin).

- Recent Developments: In August 2024, Merck Foundation, the philanthropic arm of Merck KGaA Germany, launched the first diabetes animation movie, "SUGAR FREE JUDE," to raise awareness about diabetes prevention, early detection, and the promotion of a healthy lifestyle, targeting children and youth.

- Strategic Focus: Branded metformin as volume anchor with premium formulation.

Market Concentration Analysis

Germany's diabetes pharmaceutical market exhibits moderate concentration at the branded level. Regional players, Boehringer Ingelheim and Merck, collectively hold approximately 35-40% of total market revenues (2025), driven by insulin franchise dominance. The top 3 companies, Boehringer Ingelheim, Merck, and Sanofi, collectively account for approximately 60-65% of Germany's branded diabetes pharmaceutical revenue in 2025.

The oral antidiabetic segment is significantly fragmented at the generic level. Metformin generics from manufacturers compete on price under GKV substitution mandates, compressing branded Glucophage to premium prescription positioning. SGLT-2 and GLP-1 segments remain branded-oligopolistic with patent protection.

Investment & Growth Opportunities

Fastest Growing Segments

E-Commerce/Tele-Pharmacy channel (~5.4% CAGR, 2026-2034), GLP-1 receptor agonists (~6-8% class CAGR within oral antidiabetics), CGM device segment (~15% CAGR), closed-loop insulin delivery systems (~12% CAGR), and digital diabetes apps (~20% CAGR from 2025 base) represent Germany's highest-growth investment vectors. Premium GLP-1 agonist formulations represent the single highest-value pharmaceutical investment opportunities.

Emerging Market Opportunities

Germany's undiagnosed Type-2 diabetes population represents a systematic screening and diagnosis expansion opportunity. Federal prevention programs targeting HbA1c screening in at-risk populations (obese adults, >45 years) could add high annual diagnosed patient treatment revenues by 2030. Obesity management-adjacent GLP-1 prescriptions represent a German revenue opportunity pending GKV reimbursement negotiation.

Venture and Strategic Investment Themes

- Digital therapeutic development: Germany's digital diabetes market is growing at ~20% CAGR with GKV automatic reimbursement for approved apps, a uniquely attractive regulatory environment versus the US and other European markets.

- Closed-loop insulin delivery: Germany's Type-1 patient base with high disposable income and GKV device reimbursement creates the ideal commercial launch market for next-generation artificial pancreas systems.

Future Market Outlook (2026-2034)

The Germany diabetes market is projected to grow from USD 12.0 Billion in 2025 to USD 15.2 Billion by 2034, at a steady 2.58% CAGR underpinned by Germany's aging demographics, 6.5 million patient base, and structurally supported GKV reimbursement framework. This growth trajectory reflects the convergence of pharmaceutical premiumization, device ecosystem expansion, and digital health adoption across Germany's comprehensive diabetes care continuum.

Three structural forces anchor this growth with high visibility: Germany's demographic aging structure; the GLP-1 agonist class transition from injectable specialty drugs to mainstream Type-2 first-line therapy, compressing treatment timelines; and the CGM-to-closed-loop device transition among Germany's Type-1 patients, creating a parallel device revenue stream alongside the pharmaceutical market.

Research Methodology

Primary Research

Primary research comprised structured interviews with 85+ industry stakeholders in 2025, including German endocrinologists and diabetologists from major centers (Charite Berlin, University Hospital Munich, Heidelberg University Hospital), GKV insurance fund (AOK, Techniker Krankenkasse) formulary and reimbursement executives, pharmaceutical company Germany market access directors, and hospital pharmacy directors across Germany's 1,900+ hospital network.

Secondary Research

Secondary research encompassed German Diabetes Society (DDG) clinical practice guidelines 2024-2025, IDF Diabetes Atlas 2023 Germany country data, Robert Koch Institute (RKI) Diabetes Surveillance Report 2024, BfArM pharmaceutical approval database, GKV-SV pharmaceutical expenditure statistics 2024, AMNOG benefit assessment outcomes database (G-BA), IQVIA Germany pharma market data, and company annual reports. Over 150 secondary sources were reviewed.

Forecasting Models

Market forecasts were developed using bottom-up pharmaceutical prescription volume models validated against GKV expenditure data, with separate modeling for oral antidiabetics, insulin, and device/digital health segments. Key inputs include DDG treatment guideline adoption rates, GLP-1 penetration S-curve modeling by Type-2 patient cohort, AMNOG price negotiation outcome assumptions, CGM penetration curves by diabetes type, and Germany's demographic aging projections from the Federal Statistical Office through 2034.

Germany Diabetes Market Report Coverage

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Segments Covered | Oral Antidiabetics, Insulin |

| Distribution Channels Covered | E-commerce and Tele-pharmacy, Hospital Pharmacies, Retail Pharmacies |

| Companies Covered | Boehringer Ingelheim International GmbH, Merck KGaA, Sanofi, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Germany Diabetes Market Report

The Germany diabetes market was valued at USD 12.0 Billion in 2025, covering oral antidiabetics, insulin therapies, monitoring devices, and digital health solutions for approximately 6.5 million patients.

The Germany diabetes market is projected to grow at a CAGR of 2.58% during 2026-2034, reaching USD 15.2 Billion by 2034, driven by GLP-1 agonist expansion, CGM adoption, and Germany's aging population dynamics.

Oral Antidiabetics lead with 54.8% market share (2025), driven by metformin's first-line protocol status and expanding premium SGLT-2 inhibitor and GLP-1 agonist prescriptions under GKV reimbursement.

Retail pharmacies hold the largest channel share at 47.2% (2025), anchored by Germany's licensed pharmacies dispensing GKV-reimbursed diabetes prescriptions under AMPreisV fixed dispensing fee regulations.

E-Commerce/Tele-Pharmacy grows fastest at ~5.4% CAGR (2026-2034), driven by high diabetes prescriptions under GKV online pharmacy discount frameworks.

Leading companies include Sanofi, Boehringer Ingelheim International GmbH, and Merck KGaA, among others.

Key drivers include 6.5 million+ diabetes patients, Germany's aging population, GKV statutory insurance covering 90%+ population, GLP-1 agonist class growth, and digital health app reimbursement adoption.

AMNOG mandates early benefit assessments for new diabetes drugs, restricting premium launch pricing unless clinical superiority is proven. This compresses novel drug revenue but maintains high generic volume and GKV expenditure predictability.

Insulin holds 45.2% of Germany's diabetes market (2025), anchored by Type-1 patients requiring lifelong therapy and advanced Type-2 patients progressing to insulin. Premium basal analogs dominate the insulin sub-segment.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade