Germany Logistics Market Size, Share, Trends and Forecast by Model Type, Transportation Mode, End Use, and Region, 2026-2034

Germany Logistics Market Size, Share, Trends & Forecast (2026-2034)

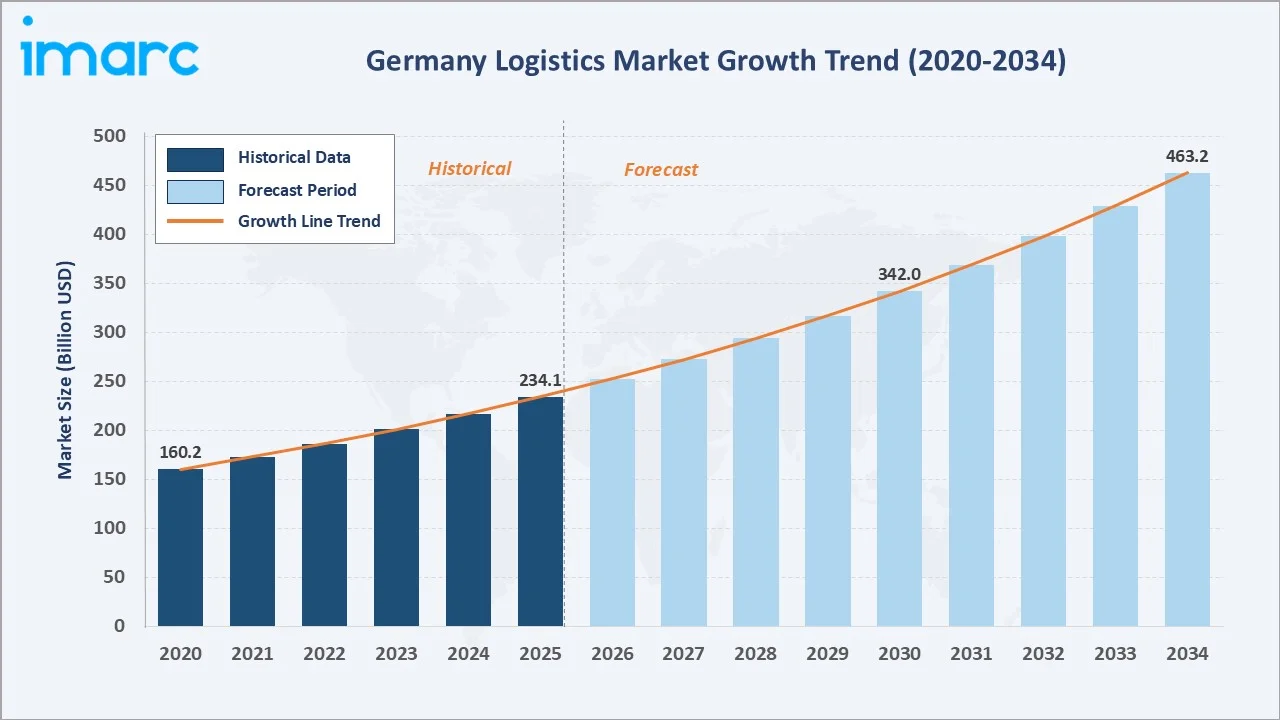

The Germany logistics market reached USD 234.1 Billion in 2025 and is projected to reach USD 463.2 Billion by 2034, growing at a CAGR of 7.88% during 2026-2034. Germany’s status as Europe’s largest economy and premier export nation, the rapid expansion of e-commerce and last-mile delivery networks, and sustained industrial output from automotive, chemicals, and manufacturing sectors are the primary forces driving consistent and robust market growth throughout the forecast period.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 234.1 Billion |

|

Forecast Market Size (2034) |

USD 463.2 Billion |

|

CAGR (2026-2034) |

7.88% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

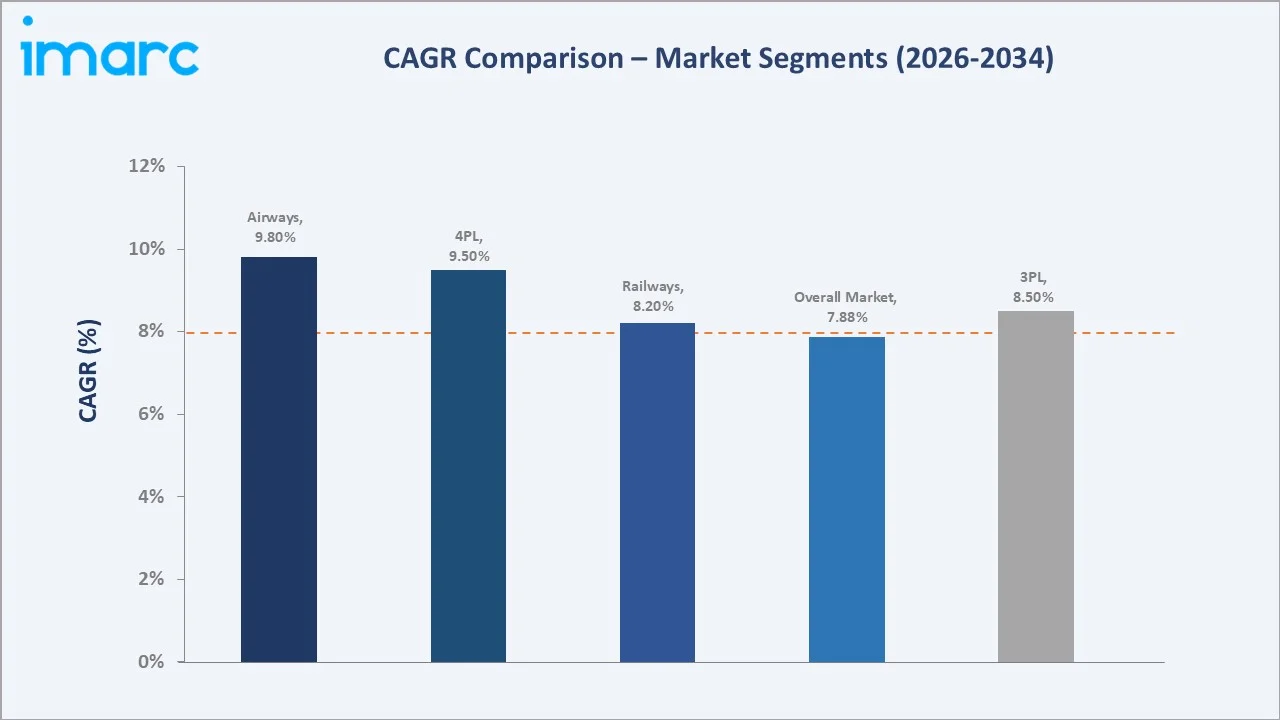

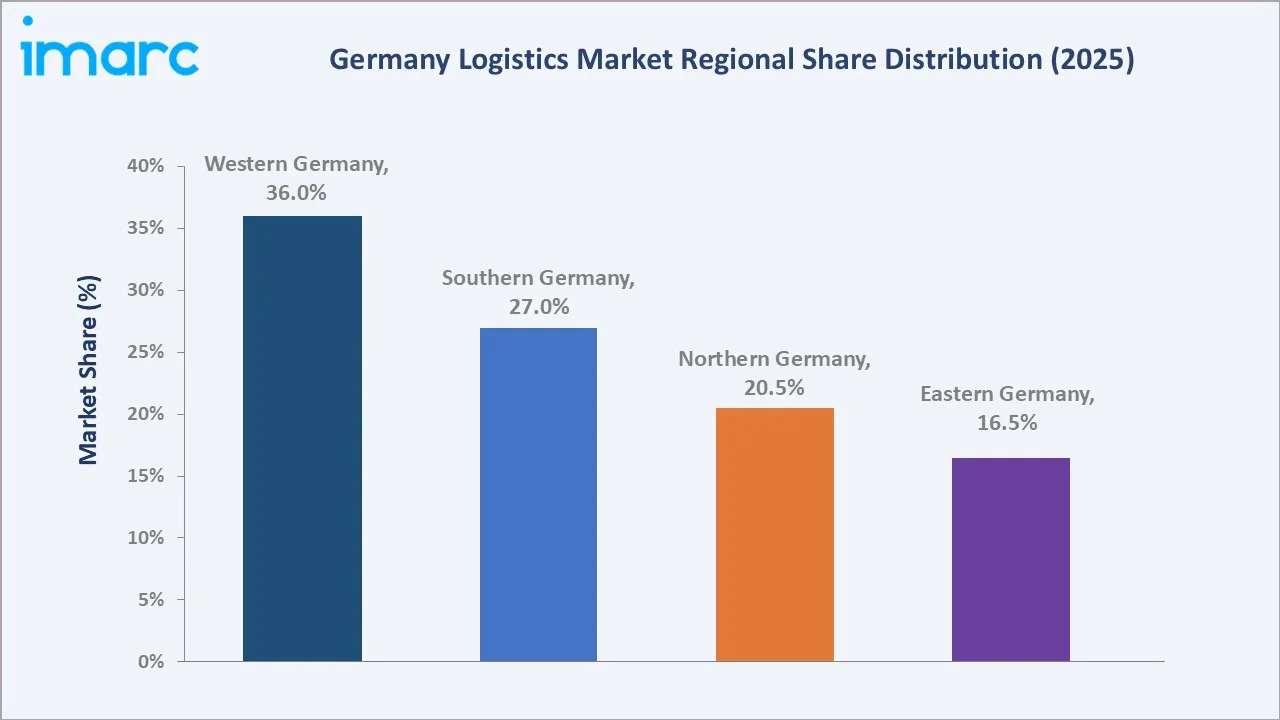

Western Germany leads regionally with a 36.0% market share in 2025, anchored by the Rhine-Ruhr industrial corridor and North Rhine-Westphalia’s dense logistics infrastructure. Third-party logistics (3PL) commands the largest model type share at 46.0%, while roadways dominate transportation mode at 52.5%. 4PL is the fastest-growing model type at ~9.5% CAGR, driven by integrated supply chain outsourcing across Germany’s large manufacturing and retail base.

To get more information on this market, Request Sample

Germany’s logistics market grew from USD 160.2 Billion in 2020 to USD 234.1 Billion in 2025, an increase of USD 73.9 Billion over five years, underpinned by e-commerce volume acceleration, industrial recovery post-COVID, and cross-border trade expansion within the EU single market. The market is forecast to reach USD 463.2 Billion by 2034, reflecting Germany’s structural role as Europe’s central logistics hub, its dense motorway and rail network, and the continued outsourcing of logistics functions to 3PL and 4PL providers by major industrial and retail corporations.

Executive Summary

The Germany logistics market is experiencing accelerated expansion, driven by the convergence of e-commerce growth, Industry 4.0 adoption, intralogistics automation, and Germany’s unrivalled position as the logistical gateway to Central and Eastern Europe. The market stood at USD 234.1 Billion in 2025 and is forecast to reach USD 463.2 Billion by 2034 at a 7.88% CAGR.

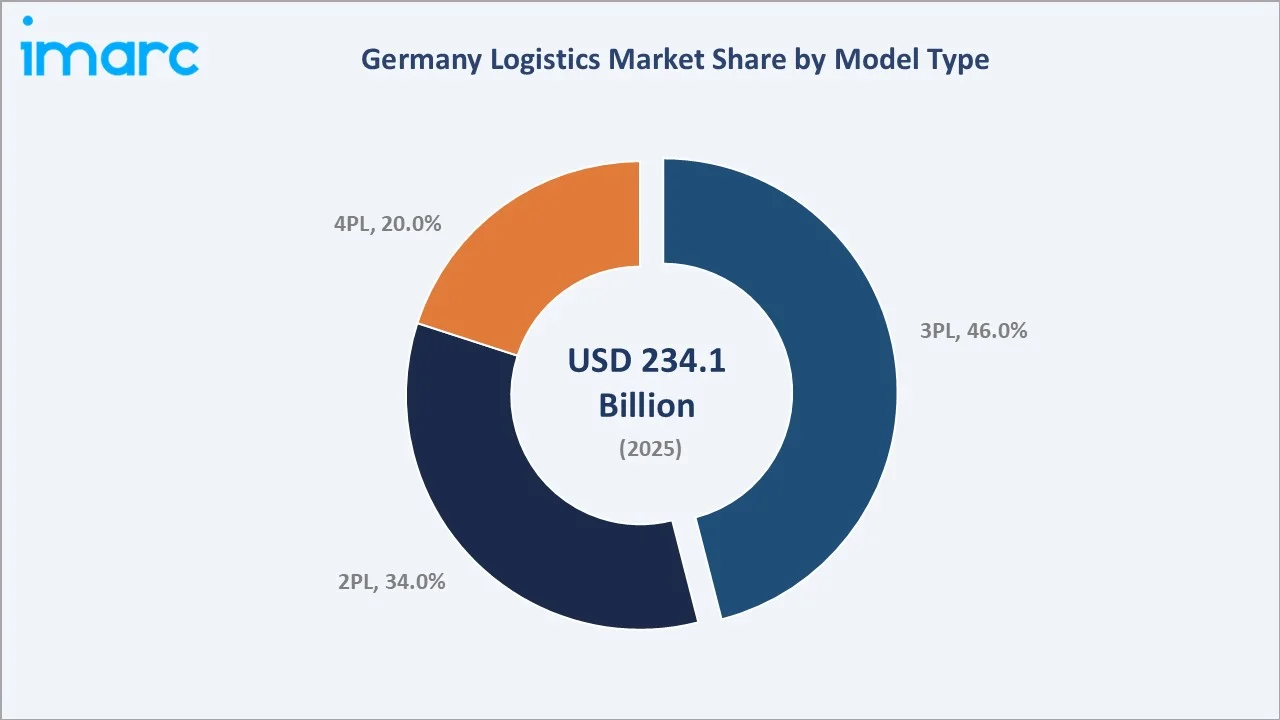

Third-party logistics (3PL) dominates model type with a 46.0% share in 2025, encompassing outsourced warehousing, freight forwarding, order fulfillment, and value-added services for manufacturers, retailers, and e-commerce operators. 2PL at 34.0% serves the large-scale freight transport segment, while 4PL at 20.0% is the fastest-growing model, driven by enterprises seeking fully integrated supply chain management across global networks.

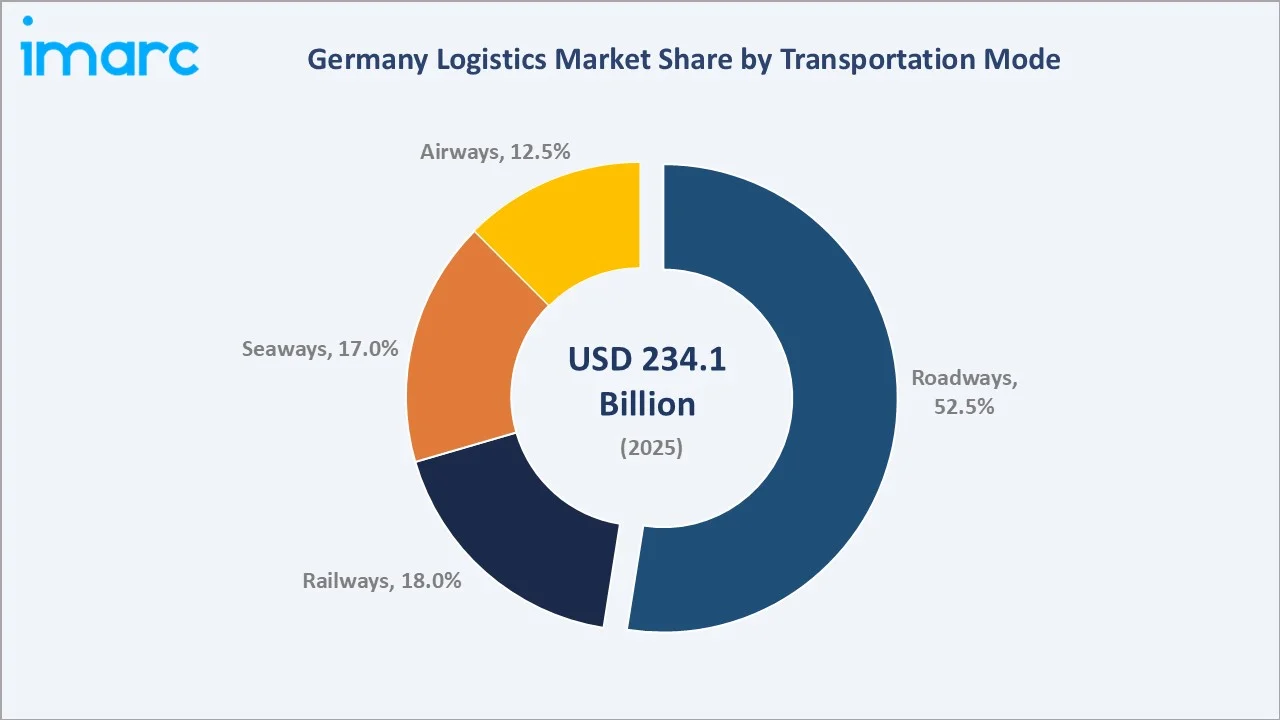

Roadways account for 52.5% of transportation modes, reflecting Germany’s 13,000 km+ motorway network and the critical role of truck freight in domestic and intra-European logistics. Railways at 18.0% benefit from DB Cargo’s extensive network and growing modal shift incentives under Germany’s Bundesverkehrswegeplan 2030. Seaways at 17.0% leverage Hamburg’s and Bremen’s status as Germany’s major ports for intercontinental container trade.

Western Germany leads regionally at 36.0%, driven by the Rhine-Ruhr industrial area, Frankfurt’s logistics hub status, and North Rhine-Westphalia’s concentration of major 3PL operators, including DHL Group and DSV. Southern Germany’s 27.0% share benefits from Bavaria’s automotive manufacturing ecosystem and Munich’s status as a premium air freight hub.

Key Market Insights

|

Insight |

Data |

|

Largest Model Type |

3PL – 46.0% share (2025) |

|

Fastest Growing Model Type |

4PL – ~9.5% CAGR (2026-2034) |

|

Largest Transportation Mode |

Roadways – 52.5% share (2025) |

|

Fastest Growing Transportation Mode |

Airways – ~9.8% CAGR (2026-2034) |

|

Leading Region |

Western Germany – 36.0% share (2025) |

|

Top Companies |

DHL Group, DSV, Kühne Holding AG, RETHMANN SE & Co. KG, Dachser SE |

Key Analytical Observations Supporting The Above Data:

- 3PL at 46.0% (2025) reflects the structural trend of German manufacturers, retailers, and e-commerce operators outsourcing warehousing, fulfilment, and freight management to specialist logistics providers.

- Roadways at 52.5% (2025) underpin Germany’s logistics infrastructure, with the country’s Autobahn network serving as Europe’s primary corridor for truck freight between Western and Eastern Europe.

- 4PL at ~9.5% CAGR is the fastest-growing model type as global manufacturers, including BMW and Volkswagen, increasingly seek single-source supply chain orchestration beyond physical transport and warehousing.

- Western Germany’s 36.0% share reflects the Rhine-Ruhr metropolitan area’s role as Europe’s largest inland port hub, combined with North Rhine-Westphalia’s concentration of 3PL operator headquarters, fulfillment centers, and intermodal terminals that serve both domestic distribution and onward transhipment to Benelux and Scandinavia.

Germany Logistics Market Overview

The Germany logistics market encompasses road freight, rail and air cargo, sea freight forwarding, warehousing and distribution, third-party and fourth-party logistics services, and related value-added supply chain services. Germany is one of the world’s third-largest logistics markets by revenue, underpinned by its position as Europe’s dominant export economy, a centrally located geography enabling access to 500 million EU consumers, and world-class multimodal infrastructure connecting motorways, inland waterways, rail, and international airports.

Germany’s logistics sector is served by over 60,000 companies, ranging from global integrated logistics giants to specialist regional freight operators, customs agents, and last-mile delivery networks. The market is characterized by high capital intensity in warehousing and fleet, increasing digital integration through transport management systems (TMS), warehouse management systems (WMS), and IoT-enabled freight tracking, and a growing skills and driver shortage that is reshaping labor economics across the sector.

Market Dynamics

To evaluate market opportunities, Request Sample

Market Drivers

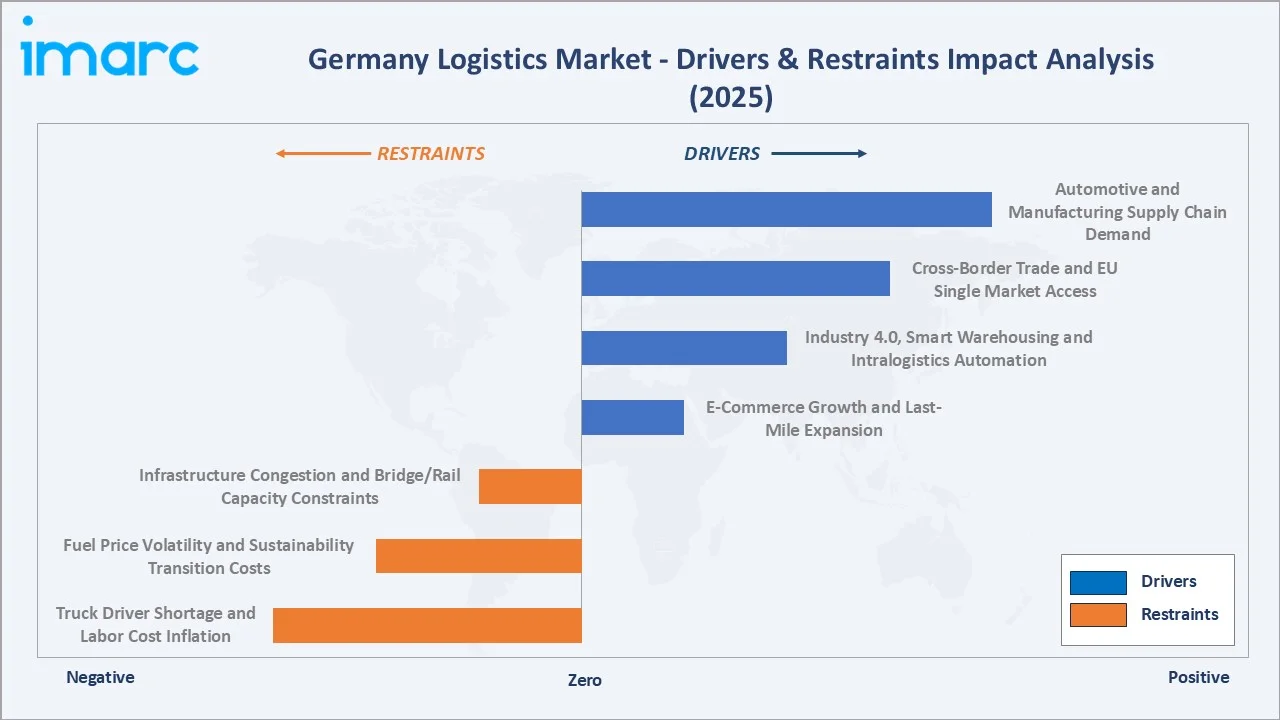

- E-Commerce Growth and Last-Mile Expansion: In 2024, Germany’s e-commerce revenue was estimated at USD 100.6 billion, representing 3.8% growth compared to 2023. The number of e-commerce users in the country is projected to rise from 47.68 million in 2025 to 51.77 million by 2029, driving sustained demand for last-mile parcel delivery, urban micro-fulfilment centers, and returns logistics.

- Industry 4.0, Smart Warehousing and Intralogistics Automation: Germany’s Mittelstand manufacturers and large industrial corporations are investing in automated warehouse systems (AS/RS), autonomous mobile robots (AMRs), and AI-powered inventory management.

- Cross-Border Trade and EU Single Market Access: Germany’s exports totaled EUR 1.56 trillion in 2025, making it the world’s third-largest exporter and anchoring demand for freight forwarding, customs brokerage, and international express delivery services. The EU single market’s elimination of intra-European customs barriers enables seamless cross-border logistics, with Germany serving as the primary gateway for goods entering and exiting the EU’s eastern member states.

- Automotive and Manufacturing Supply Chain Demand: Germany’s automotive sector, which produced 4.1 million passenger cars in 2024, generates complex just-in-time (JIT) and just-in-sequence (JIS) logistics requirements served exclusively by specialist automotive 3PL providers.

Market Restraints

- Truck Driver Shortage and Labor Cost Inflation: Germany faces a structural shortage of approximately 70,000 truck drivers, a deficit projected to grow to 200,000 by 2030. This shortage is compressing freight transport capacity, driving up road haulage rates by 6–10% annually and accelerating investment in driver-assist and autonomous vehicle technologies.

- Fuel Price Volatility and Sustainability Transition Costs: The logistics sector’s exposure to diesel price volatility, combined with Germany’s expanding CO2 toll surcharge on HGVs introduced in December 2023, is materially increasing operational costs. Conversion to LNG, CNG, battery-electric, and hydrogen fuel cell trucks requires capital investments of EUR 200,000–400,000 per vehicle, creating significant fleet transition cost pressure.

- Infrastructure Congestion and Bridge/Rail Capacity Constraints: Germany’s road and rail infrastructure is experiencing capacity constraints. Approximately 4,000 motorway bridges are classified as requiring structural repairs, causing routing disruptions and reducing HGV carrying capacity on key freight corridors.

Market Opportunities

- Green Logistics and Carbon-Neutral Supply Chains: Germany’s Federal Climate Protection Plan mandates a 65% reduction in transport CO2 emissions by 2030. DHL Group’s GoGreen Plus program and Kuehne+Nagel’s Net Zero program are driving corporate demand for verified carbon-neutral logistics services, creating a premium-priced green logistics segment growing at double-digit rates.

- Digital Freight Platforms and AI-Powered Logistics: Digital freight matching platforms and AI-driven route optimization are transforming Germany’s fragmented road freight market, reducing empty truck runs and improving asset utilization.

Market Challenges

- Geopolitical Disruption to Global Supply Chains: Germany’s export-dependent industrial economy is highly exposed to geopolitical supply chain disruptions, including US tariff escalations, Russia-Ukraine war impacts on freight routing through Eastern Europe, and Red Sea shipping diversions increasing container freight rates by 200–300% on Asia-Europe trade lanes.

- Digitalization Gap in SME Logistics Operators: Germany’s logistics sector is characterized by a long tail of SME freight operators. Digital adoption rates in TMS, real-time tracking, and electronic documentation among SME operators remain below 40%, limiting the sector’s overall efficiency and creating integration challenges for major shippers seeking end-to-end digital supply chain visibility.

Emerging Market Trends

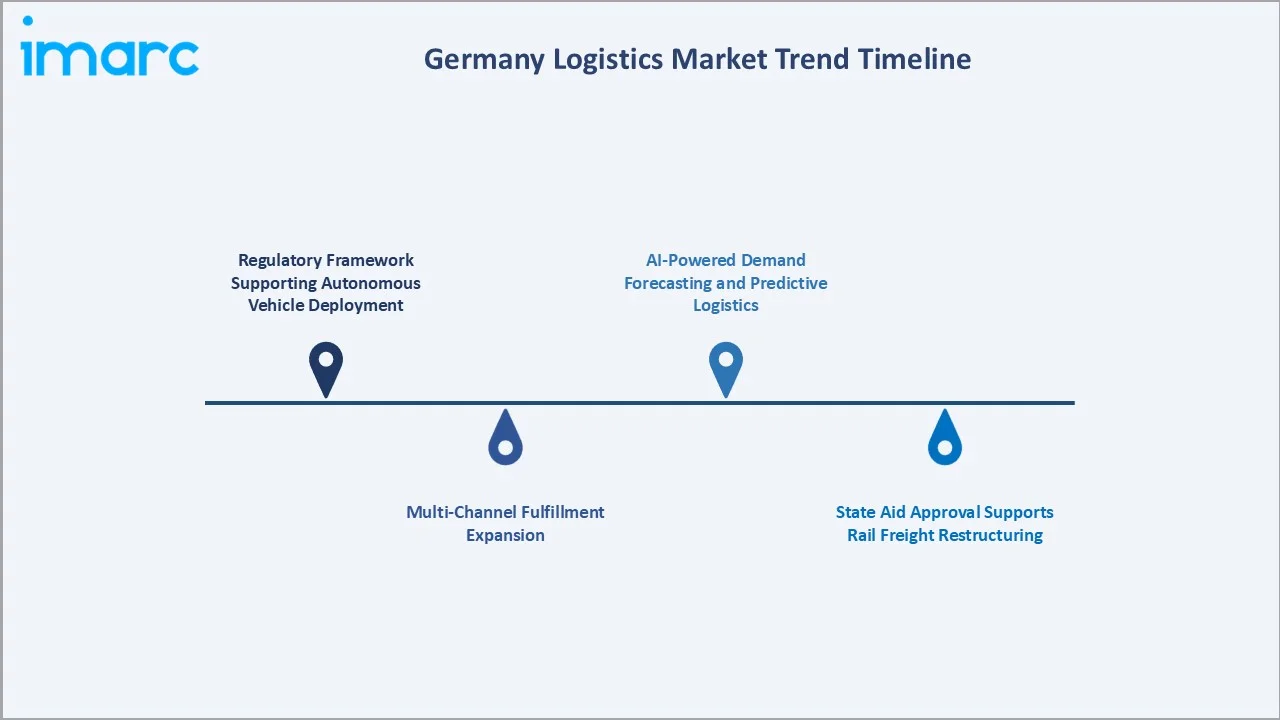

1. Regulatory Framework Supporting Autonomous Vehicle Deployment

Germany’s legal framework permits SAE Level 4 autonomous vehicles to operate on public roads without a driver, but only within pre-approved, defined operating areas and under technical supervision. The framework is based on the 2021 Autonomous Driving Act and the 2022 Autonomous Vehicle Approval and Operation Regulation (AFGBV), setting rules for vehicle approval, operator duties, data recording, and safety oversight.

2. Multi-Channel Fulfillment Expansion

In March 2026, Amazon launched a dedicated German Multi-Channel Fulfillment (MCF) site, enabling brands to use Amazon’s logistics network to fulfill orders from D2C websites, Shopify stores, and other marketplaces across the EU. The service offers Express delivery in 1–2 business days and Standard delivery in 2–3 business days, supported by Amazon fulfillment centers across Germany and other European countries.

3. State Aid Approval Supports Rail Freight Restructuring

In December 2024, the European Commission approved EUR 1.9 billion in German state aid for DB Cargo, concluding that the measure complied with EU State aid rules. The funding is intended to support DB Cargo’s restructuring, improve its long-term viability, and maintain stable rail freight services in Germany and across Europe.

4. AI-Powered Demand Forecasting and Predictive Logistics

AI adoption among German companies reached 36% in 2025, nearly double the previous year’s level. In logistics, companies are using AI for wagon inspection, freight arrival forecasting, robotic warehouse picking, document recognition, volume forecasting, address recognition, and warehouse digital twins. For instance, DB Cargo uses AI-powered image recognition across 13 camera bridges to inspect more than 10,000 freight wagons daily; DHL Group has invested over USD 700 million in AI and uses tools for bid validation and data cleansing.

Industry Value Chain Analysis

Germany’s logistics value chain spans shipper consignment through final consumer delivery across six interconnected stages, each occupied by specialized operators, technology providers, and infrastructure managers. The chain is distinguished by its high degree of vertical integration among major 3PL and 4PL providers, who manage multiple stages simultaneously.

|

Stage |

Key Players / Examples |

|

Shipper / Consignor |

Domestic manufacturers, retailers, wholesalers, exporters, e-commerce operators |

|

Freight Forwarding |

Specialist freight forwarders and logistics brokers managing customs brokerage, trade documentation, and multimodal shipment booking |

|

Transport Operations |

Road haulage operators, rail freight carriers, maritime shipping lines, and air cargo carriers |

|

Warehousing & Fulfilment |

Contract logistics and distribution center operators providing automated and conventional warehousing, pick-and-pack fulfilment, and returns processing |

|

End Consumers & Recipients |

B2B industrial and commercial customers, retail and wholesale distributors, e-commerce end consumers, and reverse logistics management recipients |

Technology Landscape in the Germany Logistics Industry

Transport Management Systems (TMS) and Real-Time Visibility

Germany’s major logistics operators have invested extensively in cloud-based TMS platforms, enabling end-to-end shipment visibility, automated carrier selection, and exception management. SAP Transportation Management, Oracle TMS, and specialist platforms are adopted by over 60% of Germany’s top 100 shippers.

Warehouse Automation and Robotics

Germany is Europe’s largest market for warehouse automation equipment, with installations of automated storage and retrieval systems (AS/RS), autonomous mobile robots (AMRs), and goods-to-person picking systems growing at approximately 18% CAGR. DHL Express’ Leipzig hub, Europe’s largest air express facility, deploys over 2,500 tons of freight every day, with 23,600 flight movements every year.

Digital Freight Platforms and Spot Market Technology

TIMOCOM is a Germany-based FreightTech company offering a digital road freight marketplace that connects over 58,000 verified customers and more than 156,000 users across Germany and other parts of Europe. Its platform supports freight exchange, transport orders, route and cost calculation, vehicle/live shipment tracking, warehousing exchange, tenders, APIs, and AI-supported freight entry to digitalize logistics operations.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Model Type |

3 PL |

46.0% |

2025 |

|

Transportation Mode |

Roadways |

52.5% |

2025 |

|

End Use |

🔒 |

🔒 |

2025 |

|

Region |

Western Germany |

36.0% |

2025 |

By Model Type

3PL dominates with a 46.0% share in 2025. Third-party logistics providers in Germany offer a comprehensive range of outsourced logistics services, including contract warehousing, dedicated transport, freight forwarding, customs brokerage, and value-added supply chain services. 2PL at 34.0% serves the large-scale freight transport segment, comprising asset-based trucking companies, rail freight operators, and shipping lines.

To access detailed market analysis, Request Sample

4PL at 20.0% is the fastest-growing model at ~9.5% CAGR, driven by global manufacturers seeking to fully outsource supply chain design, orchestration, and technology management to single integrated providers capable of managing multi-carrier, multimodal, and cross-border complexity.

By Transportation Mode

Roadways command a 52.5% share in 2025. Germany’s 13,000+ km Autobahn network and dense secondary road system make road freight the primary mode for domestic distribution. Railways at 18.0% are growing steadily as Germany’s rail infrastructure investment reached a record EUR 198 per capita in 2024, marking a 74% increase from 2023, according to lobby group Pro Rail Alliance and consultancy SCI Verkehr.

Seaways at 17.0% leverage Hamburg and Bremen/Bremerhaven for intercontinental container, bulk, and RoRo (roll-on/roll-off) cargo. Airways at 12.5% serve the high-value, time-critical freight segment, with Frankfurt Airport and Leipzig/Halle handling pharmaceutical, automotive parts, and e-commerce express shipments.

Regional Market Insights

Western Germany’s market leadership (36.0%, 2025) reflects North Rhine-Westphalia’s role as Germany’s logistics heartland. The Rhine-Ruhr area, anchored by Europe’s largest inland port at Duisburg, hosts over 1,000 logistics companies. Frankfurt’s intermodal logistics cluster, combining Germany’s busiest airport and the main east-west Autobahn junction, further reinforces Western Germany’s structural logistics advantage.

Southern Germany’s 27.0% share is supported by its strong industrial and manufacturing base, particularly across Bavaria and Baden-Württemberg, where demand for automotive, machinery, electronics, and high-value goods transportation remains high.

|

Region |

Share (2025) |

Key Growth Drivers |

|

Western Germany |

36.0% |

Rhine-Ruhr industrial corridor; Duisburg inland port; DHL Group HQ; Frankfurt air freight hub; dense motorway network to Benelux |

|

Southern Germany |

27.0% |

Automotive OEM supply chains (BMW, Mercedes, Audi/VW); Munich air cargo hub; Stuttgart industrial logistics; Bavaria e-commerce fulfilment expansion |

|

Northern Germany |

20.5% |

Hamburg & Bremen/Bremerhaven seaport gateways; North Sea container transhipment; wind energy component logistics; Hamburg Airport air freight |

|

Eastern Germany |

16.5% |

Growing as a nearshoring hub for Poland/Czech Republic supply chains; Leipzig/Halle air express hub; post-reunification industrial logistics development |

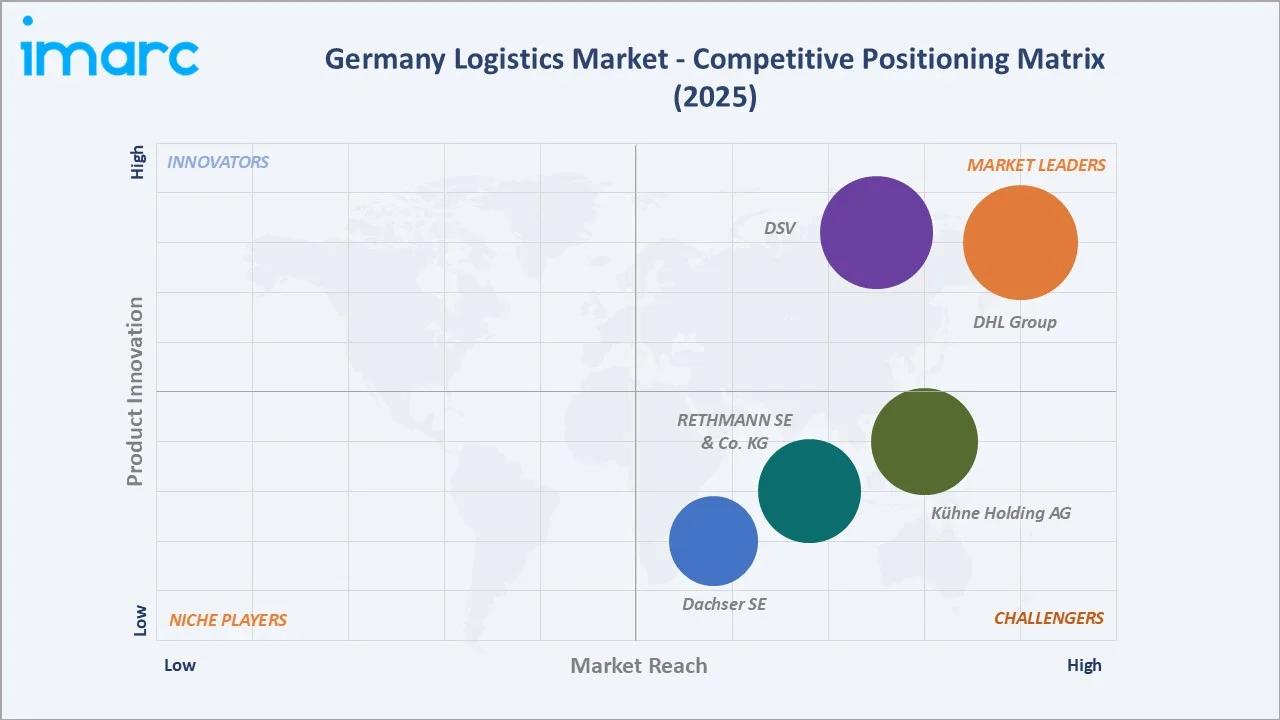

Competitive Landscape

Germany’s logistics market exhibits moderate concentration, with the top five operators collectively controlling an estimated 35–45% of total organized market revenue. The remaining 55–65% is fragmented across thousands of specialist freight operators, regional carriers, customs agents, and digital logistics platforms.

|

Company Name |

Brands/Services |

Market Position |

Core Strength |

|

DHL Group |

DHL Express, DHL e-commerce, DHL Supply Chain, DHL Global Forwarding, Post & Parcel Germany |

Market Leader |

Broadest global footprint; Europe's largest parcel network; Leipzig super-hub; GoGreen sustainability portfolio |

|

DSV |

Digital Services Hub, Transport, Contract Logistics, 4PL/Advanced Logistics Services |

Market Leader |

Overland Europe network; air/ocean forwarding; digital platform |

|

Kühne Holding AG |

Kuehne+Nagel (Transportation & fulfilment, value-added services, supply chain management, and digital services) |

Strong Challenger |

Leading ocean freight forwarder globally; Digital platform; pharmaceutical cold-chain expertise |

|

RETHMANN SE & Co. KG |

Rhenus Logistics (Transport, warehousing, port logistics, commodity logistics, Digital and document solutions) |

Strong Challenger |

Inland waterway & port logistics; Rhine corridor leadership; 3PL warehousing & industrial logistics |

|

Dachser SE |

Dachser |

Challenger |

European palletized groupage network; food logistics expertise; high digital integration |

Competition is driven by network coverage, delivery speed, warehousing capacity, digital freight solutions, sustainability initiatives, and the ability to support cross-border trade across Europe.

Key Company Profiles

DHL Group

DHL Group is one of the world’s largest logistics and express delivery companies, with Germany as its largest domestic market. Through its five divisions, it provides an end-to-end logistics ecosystem covering last-mile parcel delivery, freight forwarding, contract logistics, and express international courier services.

- Service Portfolio: DHL Express time-definite international delivery; DHL e-commerce; DHL Supply Chain contract warehousing and 3PL; DHL Global Forwarding air/ocean freight; DHL Parcel Germany domestic B2C and B2B parcel delivery.

- Recent Developments: In December 2025, DHL deployed the first eight Mercedes-Benz eActros 600 battery-electric trucks from its hylane GmbH partnership, with six stationed in Dorsten and two in Hamburg for parcel-center transport in Germany. DHL also expanded its hylane GmbH order from 30 to 42 electric trucks, with the remaining 34 vehicles expected by the end of Q2 2026.

- Strategic Focus: GoGreen Plus net-zero logistics services; autonomous last-mile delivery technology; AI-powered supply chain resilience platform (Resilience360); expansion of same-day urban delivery in Germany’s 20 largest cities.

DSV

DSV’s subsidiary DB SCHENKER (completed in April 2025) has a dominant position in European overland freight, air, and ocean freight forwarding, and contract logistics.

- Service Portfolio: Digital services hub, transport, contract logistics, and 4PL/advanced logistics services.

- Recent Developments: In February 2025, DB SCHENKER deployed its first 10 fully electric MAN eTGX trucks across ten locations in Germany for low-emission shuttle and line-haul transport. The eTGX offers a range of around 500 km, supports high-volume Megatrailer operations, and further plans to integrate 100 e-trucks to advance logistics decarbonization.

- Strategic Focus: Digital freight transparency and carbon reporting; modal shift from road to rail in collaboration with DB Cargo; autonomous and semi-autonomous truck deployment on German Autobahn corridors; pending integration with DSV’s global logistics network post-acquisition.

Market Concentration Analysis

Germany’s logistics market exhibits moderate concentration in the contract logistics and freight forwarding segments, with the top five operators controlling an estimated 35–45% of organized market revenue. Market consolidation is occurring primarily through digital platform acquisitions and the absorption of specialist regional operators into national 3PL networks.

The market’s long tail of approximately 55,000 small and medium freight operators faces intensifying pressure from platform-based freight matching services, rising driver costs, and fuel transition investment requirements. Consolidation among SME carriers through mergers, fleet-sharing cooperatives, and digital platform integration is expected to accelerate through 2030, reducing the total number of independent freight operators by an estimated 15–20%.

Investment & Growth Opportunities

Fastest Growing Segments

4PL integrated supply chain management (~9.5% CAGR), airways cargo (~9.8% CAGR), cold-chain and pharmaceutical logistics (~10%+ CAGR), and urban last-mile autonomous delivery (~12%+ CAGR from a low base) represent the primary high-growth investment vectors through 2034. Green logistics services (certified carbon-neutral freight) are emerging as a premium-priced category growing at 15%+ CAGR, driven by corporate Scope 3 emission reduction mandates from DAX companies.

Emerging Market Expansion

Eastern Germany’s logistics infrastructure is positioned for above-average growth as BMW and several Chinese EV manufacturers establish manufacturing operations in Saxony and Thuringia, requiring an integrated automotive supply chain logistics. Leipzig/Halle Airport’s expansion as Europe’s third-largest air cargo hub is creating incremental demand for adjacent warehousing, express freight, and customs services estimated at EUR 500+ Million by 2030.

Venture and Institutional Investment Trends

- Germany’s Deutsche Bahn is set to receive higher government investment to modernize its aging rail network, with gross rail infrastructure funding reaching EUR 22 billion in 2025 and EUR 23 billion planned for 2026.

- Germany launched a new public funding program in January 2026 to accelerate the deployment of hydrogen refueling stations and hydrogen-powered N2/N3 trucks for heavy-duty road freight. The scheme supports hydrogen as a complementary zero-emission option to battery-electric trucks, especially for long-haul and high-utilization freight routes.

Future Market Outlook (2026-2034)

Germany’s logistics market is positioned for sustained, high-value expansion through 2034. From a base of USD 234.1 Billion in 2025, the market is projected to reach USD 463.2 Billion by 2034 at a 7.88% CAGR. Western Germany will retain volume leadership through the forecast period, but Eastern Germany’s above-average growth trajectory will increase its regional share from 16.5% to approximately 19% by 2034.

The structural transition from asset-heavy 2PL and 3PL models toward technology-integrated 4PL and platform-based logistics will define the market’s composition by 2034. The green logistics premium segment, encompassing certified carbon-neutral road, rail, and air freight services, is projected to represent 15–18% of total logistics revenues by 2034, creating a structural profitability uplift for operators who successfully decarbonize their service portfolios.

Research Methodology

Primary Research

Primary research comprised structured interviews with over 95 industry participants in 2024–2025, including logistics operators, freight forwarders, e-commerce shippers, automotive OEM supply chain managers, port and airport authorities, and industry association representatives from BVL (Bundesvereinigung Logistik), BGL, and DSLV (Deutscher Speditions- und Logistikverband). Interviews covered market sizing, competitive dynamics, technology adoption trends, and regulatory impact across Germany’s logistics sector.

Secondary Research

Secondary research encompassed annual reports; BVL Logistics Indicator surveys; Bundesministerium für Digitales und Verkehr (BMDV) freight statistics; Destatis transport and logistics sector data; Eurostat modal split statistics; OECD trade and logistics performance index data; and European Commission transport white papers.

Forecasting Models

Market size estimations were derived using top-down GDP and trade-linked logistics intensity modelling combined with bottom-up segment-level revenue analysis by model type, transportation mode, and end-use vertical. A CAGR of 7.88% reflects consensus validated against BVL Logistics Indicator forward projections, Fraunhofer IML scenario modelling, and IMARC’s primary expert panel review.

Germany Logistics Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Model Types Covered | 2 PL, 3 PL, 4 PL |

| Transportation Modes Covered | Roadways, Seaways, Railways, Airways |

| End Uses Covered | Manufacturing, Consumer Goods, Retail, Food and Beverages, IT Hardware, Healthcare, Chemicals, Construction, Automotive, Telecom, Oil and Gas, Others |

| Regions Covered | Western Germany, Southern Germany, Eastern Germany, Northern Germany |

| Companies Covered | DHL Group, DSV, Kühne Holding AG, RETHMANN SE & Co. KG, Dachser SE, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Germany logistics market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Germany logistics market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Germany logistics industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Germany Logistics Market Report

The Germany logistics market reached USD 234.1 Billion in 2025 and is projected to reach USD 463.2 Billion by 2034.

The market is expected to grow at a CAGR of 7.88% during 2026-2034, driven by e-commerce expansion, Industry 4.0 adoption, cross-border trade growth, and the structural outsourcing of logistics to 3PL and 4PL providers.

Western Germany leads with a 36.0% share in 2025, anchored by the Rhine-Ruhr industrial corridor, Duisburg inland port, and the concentration of major logistics operator headquarters in North Rhine-Westphalia.

3PL dominates with a 46.0% share in 2025, driven by the outsourcing of warehousing, freight forwarding, and value-added logistics by Germany’s manufacturers, retailers, and e-commerce operators.

Roadways lead with a 52.5% share in 2025, reflecting Germany’s 13,000 km motorway network and the critical role of truck freight in domestic and intra-European logistics corridors.

Some of the key players in the market include DHL Group, DSV, Kühne Holding AG, RETHMANN SE & Co. KG, and Dachser SE.

4PL is growing at approximately 9.5% CAGR because global manufacturers and retailers increasingly seek fully integrated supply chain management—encompassing design, technology, carrier management, and continuous optimization—beyond the physical transport and warehousing scope of traditional 3PL providers.

Key challenges include a structural truck driver shortage of approximately 70,000 drivers, diesel-to-green fleet transition investment costs, motorway and rail infrastructure congestion, geopolitical supply chain disruptions affecting Germany’s export-dependent economy, and low digital adoption rates among SME freight operators.

Automated logistics real estate, digital freight platforms, pharmaceutical cold-chain logistics, green and carbon-neutral logistics services, urban last-mile autonomous delivery, and Eastern Germany’s emerging manufacturing logistics cluster represent the highest-growth investment opportunities through 2034.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)