Golf Equipment Market Size, Share, Trends and Forecast by Type, Distribution Channel, and Region, 2026-2034

Golf Equipment Market Size, Share, Trends & Forecast (2026-2034)

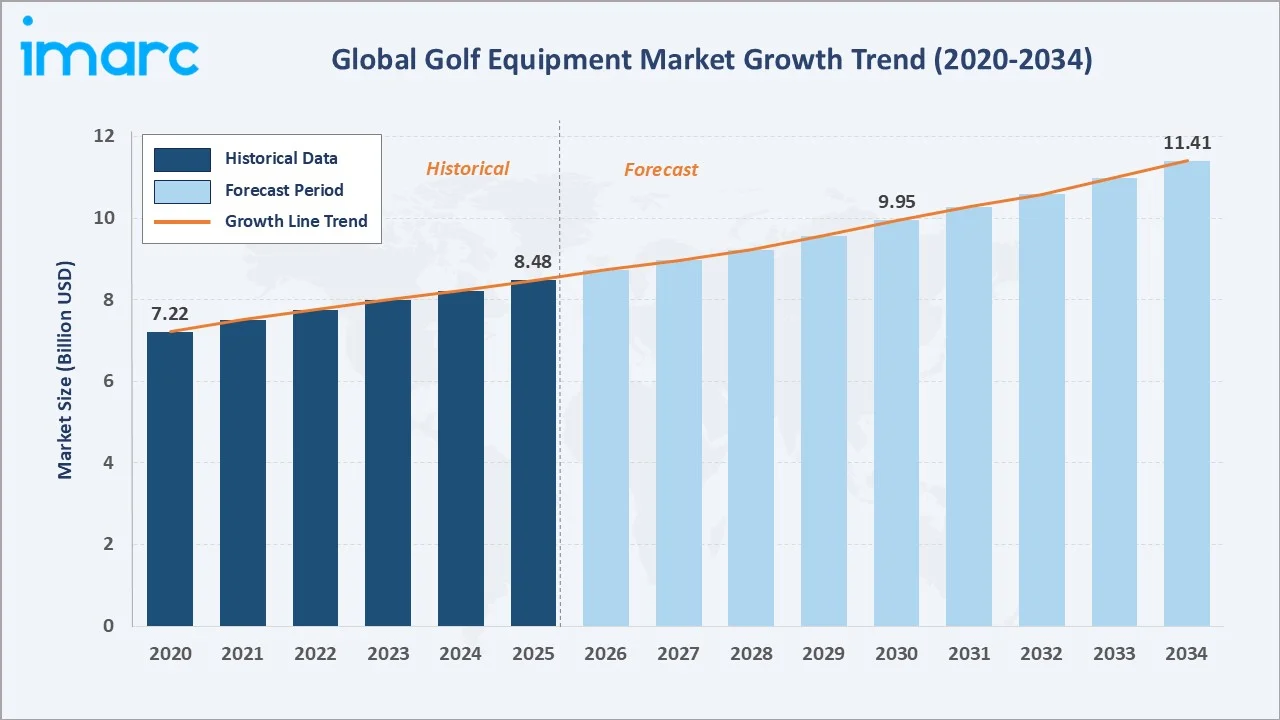

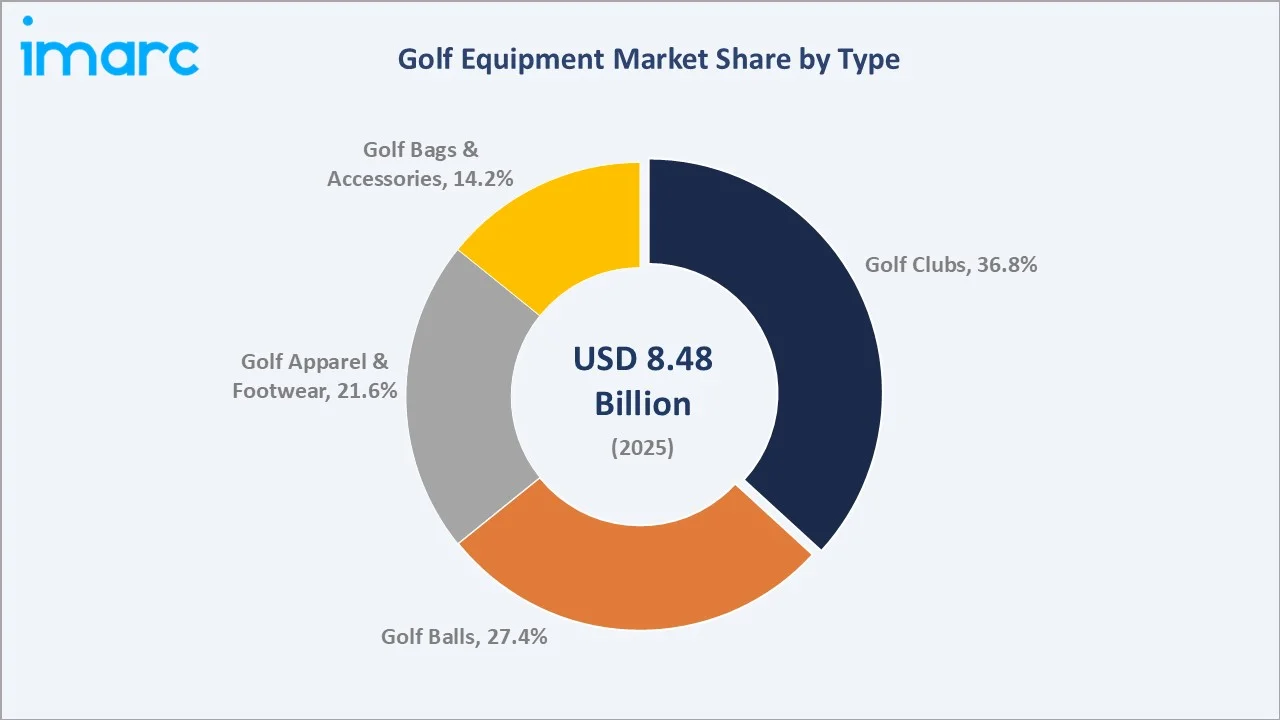

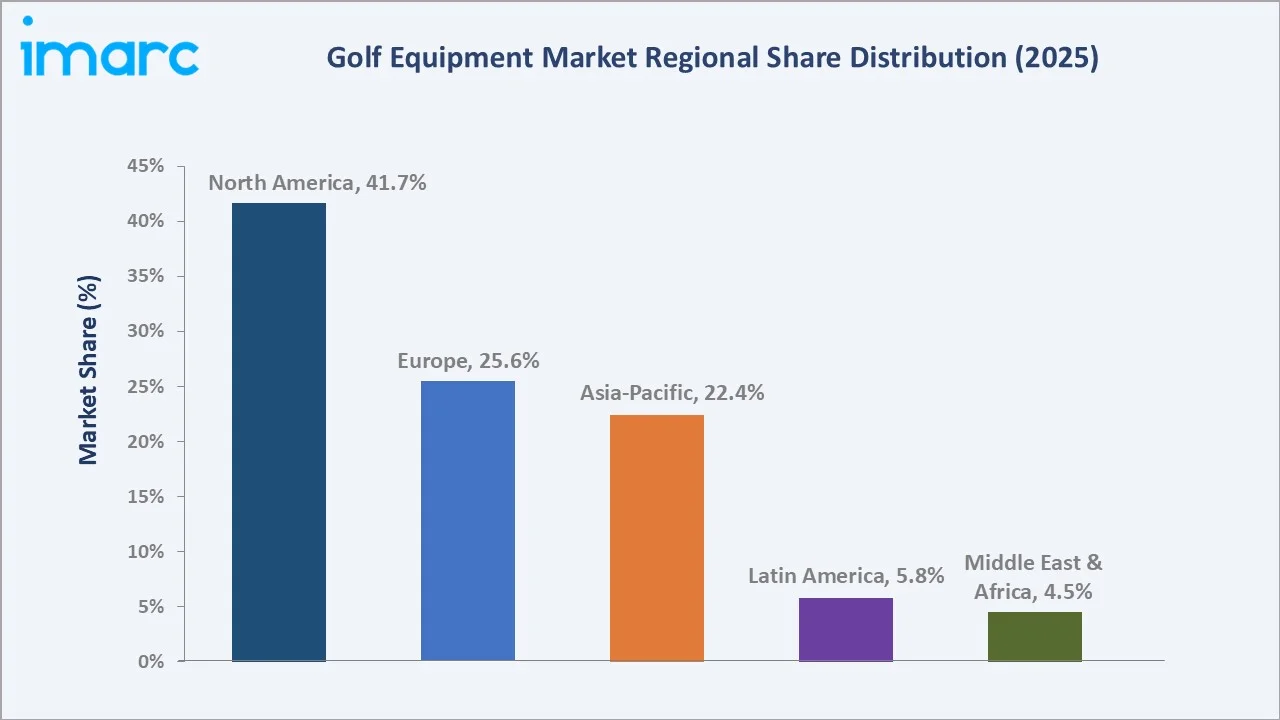

The global golf equipment market reached USD 8.48 Billion in 2025 and is projected to reach USD 11.41 Billion by 2034, growing at a CAGR of 3.26% during 2026-2034. The market is driven by rising popularity of golf as a recreational and professional sport, growing millennial participation, and continuous technological innovation in equipment design. Golf clubs dominate at 36.8%. Specialty stores lead distribution at 34.9%. North America commands 41.7% of the global market share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 8.48 Billion |

|

Forecast Market Size (2034) |

USD 11.41 Billion |

|

CAGR (2026-2034) |

3.26% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Type |

Golf Clubs (36.8%, 2025) |

|

Dominant Distribution Channel |

Specialty Stores (34.9%, 2025) |

|

Leading Region |

North America (41.7%, 2025) |

The global golf equipment market expanded from USD 7.22 Billion in 2020 to USD 8.48 Billion in 2025, anchored at USD 9.95 Billion in 2030, and forecast to reach USD 11.41 Billion by 2034. Rising disposable incomes, government investment in golf infrastructure, and growing e-commerce availability sustained above-trend market growth through 2022-2025.

To get more information on this market, Request Sample

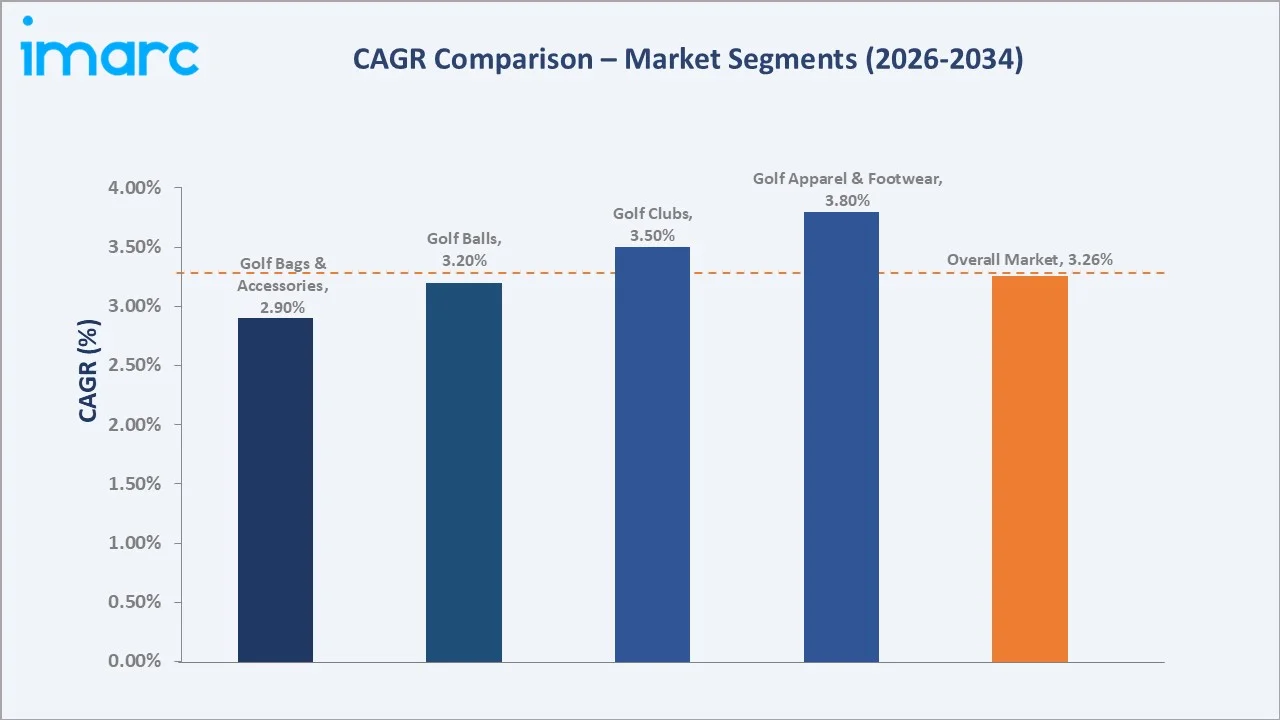

Golf apparel and footwear grows fastest at ~3.8% CAGR as consumers seek performance-enhancing and fashion-forward products. Golf clubs grow at ~3.5% CAGR through premium upgrades and custom fitting services that sustain consistent replacement cycles across consumer segments.

Executive Summary

The global golf equipment market reached USD 8.48 Billion in 2025, representing one of the most dynamic leisure-sports consumer segments globally. The market encompasses golf clubs, balls, apparel, footwear, and accessories used by amateur and professional golfers across all distribution channels.

Golf clubs at 36.8% dominate through their essential role in play and the consistent upgrade cycle driven by innovation. Specialty stores at 34.9% lead through expert fitting and personalized service. North America, at 41.7%, leads through dense golf infrastructure and high consumer spending power.

Key Market Insights

|

Insight |

Data |

|

Dominant Type |

Golf Clubs – 36.8% share (2025) |

|

Dominant Channel |

Specialty Stores – 34.9% market share (2025) |

|

Leading Region |

North America – 41.7% market share |

|

Market Opportunity |

Smart golf equipment; indoor simulators; sustainable materials; AI fitting technology; women's & youth golf |

Key Analytical Observations Supporting the Above Data:

- Golf Clubs at 36.8%: Golf clubs dominate due to continuous innovation in titanium, carbon fiber, and AI-modeled clubfaces driving frequent upgrade cycles. Custom fitting and personalization sustain premium pricing. Drivers and irons command above-average spending across recreational and professional segments.

- Specialty Stores at 34.9%: Specialty stores lead because they offer professional club fitting, expert advice, and hands-on testing. These services differentiate physical retail from online channels and support higher average transaction values and stronger customer retention across all consumer tiers.

- North America at 41.7%: North America dominates due to highest per-capita golf participation globally, the most golf courses worldwide, and strong consumer spending on premium equipment. US PGA Tour media visibility drives continuous equipment demand at all consumer levels.

Golf Equipment Market Overview

The global golf equipment market encompasses the design, manufacturing, marketing, and sale of all equipment and accessories used in playing golf. The market includes premium clubs for professionals, starter sets for beginners, performance golf balls, technical apparel, footwear, and accessories serving amateur and professional golfers globally.

.webp)

Macroeconomic factors include rising global disposable incomes, expanding middle-class populations in Asia-Pacific and Latin America, growing sports participation, and increased interest in golf as a health and wellness activity. Government investment in golf infrastructure, growing media coverage of professional golf, and the expanding global tournament calendar further accelerate market development.

Market Dynamics

.webp)

To evaluate market opportunities, Request Sample

Market Drivers

- Growing Popularity of Golf as a Recreational Sport: The rising global interest in golf as a leisure, social, and wellness activity is increasing equipment demand across all skill levels. Governments and private investors are expanding golf course infrastructure to broaden accessibility. Growing popularity of golf tourism and corporate networking through golf is expanding the active player base, driving sustained equipment procurement growth across regions.

- Rising Disposable Income and Millennial Participation: Higher consumer spending power and growing participation among millennials and Generation Z are reshaping the market. Younger consumers invest in premium performance clubs, branded apparel, and tech-integrated wearable accessories. This demographic shift creates new demand for personalized, technology-driven golf products that sustain above-baseline unit volume and premium pricing across all distribution channels.

- Technological Advancements in Equipment Design: Continuous innovation in materials science and computational design is elevating equipment performance and sustaining upgrade demand. Manufacturers incorporating aerospace-grade titanium, high-modulus carbon fiber, and AI-generated clubface geometries create measurable performance improvements. These advancements motivate equipment replacement even among casual players, sustaining above-baseline unit volume and premium pricing throughout the product lifecycle.

- Expansion of Golf Infrastructure and Tournament Visibility: Growth in the number of professional tour events and international golf tournaments is increasing sport exposure and stimulating equipment demand. Rising television and streaming viewership of major championships inspires recreational players to invest in performance equipment. Government investments in sport tourism and golf infrastructure across Asia and the Middle East are creating significant new market growth opportunities globally.

Market Restraints

- High Cost of Premium Golf Equipment: Significant upfront investment required for quality golf equipment limits penetration among price-sensitive and beginning golfers. Premium driver and custom iron set combinations can require thousands of USD, creating participation barriers that slow market expansion in cost-conscious consumer segments across developing and emerging markets worldwide.

- Intense Market Competition Among Established Brands: Fierce competition among globally recognized brands creates sustained pricing pressure and compressed operating margins. Leading manufacturers constantly invest in R&D, athlete endorsements, and marketing differentiation. This competitive intensity increases market participation costs and makes it difficult for smaller regional players to achieve meaningful market scale or distribution channel penetration.

- Seasonal and Weather Dependency Limiting Year-Round Demand: Golf participation and equipment purchasing are heavily influenced by seasonal weather patterns in major temperate-climate markets. Harsh winters in key markets including Canada, northern Europe, and the northern United States create pronounced demand seasonality, reducing purchase frequency and complicating inventory planning for both manufacturers and specialty retailers throughout the distribution chain.

Market Opportunities

- Indoor Golf Simulator Market Expansion: The rapid growth of indoor golf simulator facilities is creating year-round demand for equipment independent of weather conditions. Proliferating simulator venues across Asia-Pacific and North America expand the addressable market by converting non-traditional venues into points of equipment consumption and new golfer acquisition, bypassing the seasonal limitations of outdoor golf markets.

- Sustainable and Eco-Friendly Equipment Development: Growing consumer environmental consciousness is creating demand for golf equipment manufactured using sustainable materials and responsible production. Brands that effectively communicate sustainability credentials and offer eco-positioned product lines are differentiated in the premium segment and positioned to capture the expanding environmentally motivated consumer cohort across key global markets.

Market Challenges

- Counterfeit Products Threatening Brand Integrity and Revenue: Proliferation of counterfeit golf equipment through online marketplaces and informal trade channels threatens revenue and brand reputation for established manufacturers. Counterfeit clubs and balls sold at heavily discounted prices undermine brand equity, create consumer quality concerns, and divert significant revenue from authentic product sales, requiring ongoing investment in brand protection programs.

- Supply Chain Complexity and Raw Material Price Volatility: Golf equipment manufacturing relies on specialized materials including titanium, carbon fiber composites, and precision-engineered rubber compounds. Global supply chain disruptions, raw material cost volatility driven by geopolitical tensions, and logistics bottlenecks create production cost uncertainty that challenges manufacturers in maintaining stable product pricing and consistent inventory availability.

Emerging Market Trends

1. AI-Powered Club Fitting and Performance Analytics Transforming Equipment Selection

AI-powered launch monitors and swing analysis platforms are transforming club selection by analyzing ball trajectory, spin rate, and impact data to deliver precise fitting recommendations. Integration of AI analytics in professional fitting studios and online D2C configurators is reducing barriers to custom-fitted equipment and expanding the premium equipment market.

2. Smart Wearables and Connected Golf Technology Driving Ecosystem Engagement

Smart golf wearables including GPS watches, rangefinders, and performance-tracking gloves are delivering real-time shot tracking, course mapping, and swing metrics. Integration with mobile applications creates ecosystem lock-in for equipment brands. Connected golf technology is generating new recurring revenue streams through hardware, software subscriptions, and data services beyond the initial equipment sale.

3. E-Commerce and Direct-to-Consumer Sales Reshaping Distribution Channel Dynamics

Rapid growth of online golf equipment sales is restructuring distribution channel economics. E-commerce platforms enable brands to offer personalized configurations, virtual fitting tools, and AI-powered recommendations directly to consumers. D2C digital channels reduce retail dependence, improve margin capture, and build proprietary consumer data assets that support long-term engagement and repurchase.

4. Women's and Youth Golf Equipment Creating New Market Expansion Vectors

Growing participation of women and youth in golf is creating significant product development opportunities. Leading brands are designing lightweight club sets, stylish performance apparel, and affordable starter kits for these high-growth segments. Strategic focus on demographic diversification is expanding the total addressable market beyond its historically narrow core and building long-term consumer relationships with new participants.

Industry Value Chain Analysis

The golf equipment value chain integrates raw material sourcing, component manufacturing, branded equipment assembly, quality assurance testing, distribution, and end-consumer engagement. Each stage contributes distinct value and involves specialized participants with differentiated capabilities.

|

Stage |

Key Participants |

|

Raw Material Sourcing |

Titanium and steel producers, carbon fiber suppliers, rubber and polymer manufacturers, grip material and adhesive producers |

|

Component Manufacturing |

Shaft manufacturers, clubhead foundries, grip and cover material producers, precision engineering specialists, packaging suppliers |

|

Equipment Assembly & Branding |

OEM equipment manufacturers, branded companies (Callaway, TaylorMade, Acushnet), co-brand and white-label production facilities |

|

Quality Control & Compliance |

R&D testing laboratories, launch monitor validation, USGA and R&A regulatory compliance bodies, performance certification agencies |

|

Distribution & Retail |

Specialty golf stores, sporting goods chains, on-course pro shops, online D2C platforms, department stores, golf resort retail |

|

End Consumer |

Amateur golfers, professional players, golf clubs and resorts, corporate buyers, golf academies and training facilities |

The equipment assembly and branding stage is the most commercially differentiated phase, where brand equity, R&D investment, and proprietary technology create significant entry barriers. The distribution stage is undergoing rapid transformation as digital and direct-to-consumer channels gain market share from traditional multi-brand specialty retailers.

Technology Landscape in the Golf Equipment Industry

Advanced Materials Technology

Aerospace-grade titanium, high-modulus carbon fiber, multi-material construction, and variable-thickness face engineering are enabling lighter, stronger, and more forgiving club designs. These material innovations allow manufacturers to reposition weight strategically throughout club heads, optimizing launch conditions and improving off-center hit performance for golfers across all ability levels and price points.

AI-Modeled Clubface Design

AI-driven generative design tools enable manufacturers to optimize clubface geometries and internal weight distributions beyond conventional design capabilities. Computational design approaches analyze millions of performance scenarios to identify face architectures that maximize ball speed consistency across the entire clubface. AI-modeled designs are becoming core competitive differentiators in the premium driver and iron market globally.

Smart Sensor and IoT Integration

Integration of smart sensors into clubs, gloves, and balls enables real-time performance data collection during play and practice. IoT-connected products capture swing speed, impact location, ball flight metrics, and course position data transmitted to mobile applications for analysis. Connected products create ongoing consumer engagement and open subscription-based data service revenue models for manufacturers.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Golf Clubs |

36.8% |

2025 |

|

Distribution Channel |

Specialty Stores |

34.9% |

2025 |

|

Region |

North America |

41.7% |

2025 |

By Type

Golf clubs lead at 36.8% (2025). The golf club segment encompasses drivers, fairway woods, hybrids, irons, wedges, and putters used by golfers at all skill levels. Continuous innovation in shaft technology, clubhead materials, and AI-modeled face design sustains consistent upgrade and replacement demand cycles across the consumer base globally.

To access detailed market analysis, Request Sample

Golf balls at 27.4% represent the highest-frequency consumable purchase in the market, with active golfers replacing balls multiple times per season. Golf apparel and footwear at 21.6% grows fastest through lifestyle crossover positioning. Golf bags and accessories at 14.2% provide stable recurring revenue through natural replacement cycles.

By Distribution Channel

Specialty stores lead at 34.9% (2025). The specialty store segment delivers professional fitting services, product expertise, and personalized experience. This channel commands premium pricing and sustains above-average customer lifetime values through repeat engagement and expert-guided purchasing decisions that online and mass-market channels cannot fully replicate.

.webp)

Sporting goods chains at 24.3% provide broad consumer reach. Online stores at 19.8% are the fastest-growing channel through AI-powered fitting tools. On-course shops at 13.1% benefit from impulse purchasing. Others at 7.9% include department stores and discount retailers.

Regional Market Insights

|

Region |

Share (2025) |

Key Golf Equipment Market Drivers & Characteristics |

|

North America |

41.7% |

Driven by highest per-capita golf participation globally, mature course infrastructure, high consumer spending on premium equipment, and growing adoption of AI-powered fitting technology. |

|

Europe |

25.6% |

Supported by strong golf culture in UK, Germany, and Sweden, growing recreational participation, investment in premium equipment, and rising adoption of indoor simulation facilities. |

|

Asia-Pacific |

22.4% |

Driven by expanding golf culture in Japan, South Korea, China, and Australia, rising disposable incomes, government support for golf as a professional and recreational sport. |

|

Latin America |

5.8% |

Supported by growing golf tourism in Mexico and Brazil, increasing club memberships among rising middle-class consumers, and golf as a premium lifestyle activity. |

|

Middle East & Africa |

4.5% |

Driven by luxury golf resort development in UAE and Saudi Arabia, expanding expatriate communities, and government sport tourism investment across GCC nations. |

North America's 41.7% market leadership is anchored by the United States, which hosts the world's largest number of golf courses and the highest absolute number of active golfers globally. The US professional golf circuit drives continuous media exposure that stimulates equipment demand at all consumer levels.

Asia-Pacific's 22.4% encompasses Japan's deep-rooted golf culture and South Korea's rapidly growing premium equipment market. The Middle East and Africa, at 4.5%, is emerging as a high-growth region driven by luxury resort development and sports tourism investment in GCC nations.

Competitive Landscape

The global golf equipment market competitive landscape encompasses major branded equipment companies, specialty manufacturers, performance apparel brands, and diversified sporting goods conglomerates. Competition is driven by technology differentiation, athlete endorsements, custom fitting capability, and distribution channel depth.

|

Company Name |

Key Products |

Market Position |

Core Strength |

|

Callaway Golf Company |

Paradym Drivers, Chrome Soft Balls |

Market Leader |

Leads through AI-modeled clubface technology and Jailbreak Architecture driving ball speed. Premium ball franchise via Chrome Soft. Strong professional tour endorsement portfolio. |

|

TaylorMade Golf Co. |

Stealth Drivers, TP5 Golf Balls, P-Series Irons |

Market Leader |

Leads through carbon fiber driver innovation and multi-material construction. TP5 franchise competes at premium ball tier. Strong PGA Tour endorsement with major champions globally. |

|

PING |

Drivers, i230 Irons, Glide Wedges |

Established Player |

Differentiated through custom fitting heritage, proprietary shaft and head technology, and family-owned independence enabling long-term R&D investment without short-term earnings pressure. |

|

Adidas AG |

CodeChaos Golf Shoes, Ultimate365 Apparel |

Established Player |

Leverages global sportswear brand equity and broad retail distribution network to offer premium golf apparel and footwear across multiple price tiers in key global markets. |

|

Bridgestone Corporation |

Tour B X Golf Balls, Bridgestone Clubs |

Established Player |

Competes through proprietary ball technology developed from tire manufacturing expertise. Tiger Woods endorsement validates Tour B performance franchise at the premium tier globally. |

Premium brand concentration in the golf equipment market is increasing as leading manufacturers acquire complementary brands to build comprehensive golf lifestyle portfolios. Consolidation reflects consumer preference for integrated equipment ecosystems delivering consistent performance and service from a single trusted brand relationship.

Key Company Profiles

Callaway Golf Company

Callaway Golf Company is one of the world's largest designers and manufacturers of premium golf clubs, golf balls, and accessories. The company markets products under the Callaway and Odyssey brands globally, with strong presence across professional and recreational market segments.

- Key Products: Paradym AI Smoke Drivers, Chrome Soft Golf Balls, Apex Irons, Odyssey Putters.

- Recent Developments: In January 2026, Callaway unveiled its new Quantum family of Drivers, Fairway Woods, Irons, and Hybrids, featuring advanced AI-driven technologies designed to improve speed, forgiveness, and overall performance for golfers across skill levels.

- Strategic Focus: Focused on AI-driven equipment design innovation, premium ball technology, and global brand building through professional tour endorsements and growth of direct-to-consumer digital commerce capabilities.

TaylorMade Golf Co.

TaylorMade Golf Co. is a leading manufacturer of golf drivers, irons, golf balls, and accessories. The company is the industry pioneer of carbon fiber driver construction and multi-material club design that established global performance benchmarks for premium golf equipment.

- Key Products: Stealth 2 Drivers, P-Series Irons, TP5 and TP5x Golf Balls, Spider Putters.

- Recent Developments: In June 2026, TaylorMade Golf introduced the Spider ZT Max putter lineup, expanding its acclaimed Spider franchise with three high-MOI configurations designed to deliver enhanced stability, forgiveness, and consistency for golfers of all skill levels.

- Strategic Focus: Centered on advancing carbon fiber material applications, deepening premium golf ball market penetration through the TP5 franchise, and strengthening global D2C capabilities through personalized equipment configuration platforms and digital consumer engagement.

Market Concentration Analysis

The global golf equipment market is moderately concentrated at the premium club and ball segment tier, where Callaway, TaylorMade, and PING collectively account for premium equipment revenue. The mid-range and mass-market segments are significantly more fragmented with numerous regional manufacturers.

Consolidation is increasing in the golf lifestyle segment as manufacturers acquire complementary apparel and accessory brands. Market concentration at the technology platform level is growing as brands invest in proprietary AI fitting systems and connected equipment ecosystems that create consumer switching costs and long-term relationships.

Investment & Growth Opportunities

Highest Growth Segments

Golf apparel and footwear (~3.8% CAGR), indoor golf simulator accessories (~12-15% CAGR from small base), AI-powered fitting platform technology (~15% CAGR), women's golf equipment (~5% CAGR), and youth golf starter sets (~6% CAGR) represent the highest-growth investment segments in the golf equipment market through 2034.

Emerging Investment Opportunities

Asia-Pacific golf market expansion, particularly across India, Southeast Asia, and China's growing premium recreational segment, represents the largest near-term market opportunity. Equipment brands and specialty retailers establishing distribution networks and fitting capabilities in these markets are positioned for above-market revenue growth as middle-class golf participation accelerates.

Investment Themes

- AI-powered golf fitting platform for D2C recurring revenue: AI club fitting platforms use swing data, ball flight metrics, and biomechanics to recommend personalized equipment configurations. Brands investing in proprietary AI fitting technology create consumer switching costs, build direct relationships supporting premium pricing, and generate recurring accessory revenue throughout the customer lifecycle beyond initial equipment purchase.

- Indoor golf entertainment venue equipment supply partnerships: Rapid global expansion of TopGolf-style indoor venues and simulator bars creates institutional equipment supply opportunities. Brands supplying premium clubs, balls, and branded accessories to commercial indoor golf operators benefit from high-volume sales and brand exposure to millennial consumers who subsequently purchase personal equipment for home and outdoor use.

Future Market Outlook (2026-2034)

The global golf equipment market is projected to grow from USD 8.48 Billion in 2025 to USD 11.41 Billion by 2034, delivering a 3.26% CAGR over the forecast period. The market's anchor value of USD 9.95 Billion in 2030 reflects steady, technology-driven demand growth across all equipment categories and geographic markets.

Three structural forces define market growth through 2034. Expanding global middle-class populations across Asia-Pacific and Latin America are creating millions of new golfers annually, widening the addressable market. Technology-driven equipment obsolescence through AI design, smart connectivity, and advanced materials sustains upgrade cycles supporting above-baseline volume and premium pricing. Golf's transformation into a mainstream wellness and lifestyle activity expands equipment spending into adjacent apparel, accessories, and connected technology categories.

Research Methodology

Primary Research

Primary research comprised structured interviews with 50+ industry stakeholders conducted in 2025, including golf equipment brand executives, specialty retail buyers, professional golf association representatives, supply chain managers, and regional market specialists across North America, Europe, and Asia-Pacific.

Secondary Research

Secondary research encompassed golf industry trade publications, national golf federation participation data, company annual reports, sporting goods retail statistics, and e-commerce market data. Over 60 secondary sources were reviewed including PGA of America data, R&A global golf participation reports, and national golf association membership statistics.

Forecasting Models

Market revenue forecasts were developed using a segment bottom-up model incorporating: (i) equipment category component; (ii) distribution channel component; (iii) regional market component. Scenario analysis incorporated three growth scenarios calibrated to macroeconomic conditions and golf participation rate assumptions through 2034.

Golf Equipment Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Types Covered | Golf Clubs, Golf Balls, Golf Bags and Accessories, Golf Apparel and Footwears |

| Distribution Channels Covered | Specialty Stores, Sporting Goods Chain, On-course Shops, Online Stores, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Callaway Golf Company, TaylorMade Golf Co., Acushnet Holdings Corp. (Fila Holdings Corp.), PING, Adidas AG, Bridgestone Corporation, Mizuno Corporation, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the golf equipment market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global golf equipment market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the golf equipment industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Golf Equipment Market Report

The global golf equipment market reached USD 8.48 Billion in 2025. The market is driven by rising global participation, increasing consumer spending on premium equipment, and continuous technological innovation. Growing popularity of golf as a health, wellness, and social activity is supporting sustained long-term demand growth across all major geographic markets.

The market grows at 3.26% CAGR during 2026-2034, reaching USD 11.41 Billion by 2034. Golf apparel and footwear grows fastest at ~3.8% CAGR through lifestyle crossover and performance positioning. Indoor golf simulator accessories represent the highest-growth adjacent equipment segment through the forecast period.

Golf clubs lead at 36.8% through their essential role in every round of play and the consistent upgrade cycle driven by materials and design innovation. Premium drivers, custom-fitted iron sets, and high-performance putters sustain above-average pricing and replacement demand across both recreational and professional golfer segments.

Specialty stores lead at 34.9% through professional fitting services, expert product knowledge, and personalized experience. These advantages differentiate the specialty channel from mass-market and online competitors, supporting higher average transaction values and stronger customer loyalty across the consumer base.

North America leads at 41.7% through the United States' dominant position as the world's largest golf equipment market. Dense golf course infrastructure, high media visibility of professional golf, and strong disposable income sustain North America's market leadership position through the forecast period to 2034.

Leading companies include Callaway Golf Company, TaylorMade Golf Co., Acushnet Holdings Corp. (Fila Holdings Corp.), PING, Adidas AG, Bridgestone Corporation, and Mizuno Corporation, among many others.

The market is projected to reach approximately USD 9.95 Billion by 2030. AI-powered club fitting is expected to achieve mainstream adoption, indoor golf facilities will expand significantly in Asia-Pacific, and women's and youth equipment segments will register above-average growth as demographic diversification broadens the consumer base.

Key growth opportunities include AI-powered fitting platforms, indoor golf entertainment supply partnerships, Asia-Pacific market expansion, sustainable product lines, women's and youth equipment, and smart wearable accessories integrating equipment with digital performance tracking. Brands positioned across multiple growth vectors are best placed to outperform market growth through 2034.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)