Greek Yogurt Market Size, Share, Trends and Forecast by Product Type, Flavor, and Distribution channel, and Region, 2026-2034

Global Greek Yogurt Market Size, Share, Trends & Forecast (2026-2034)

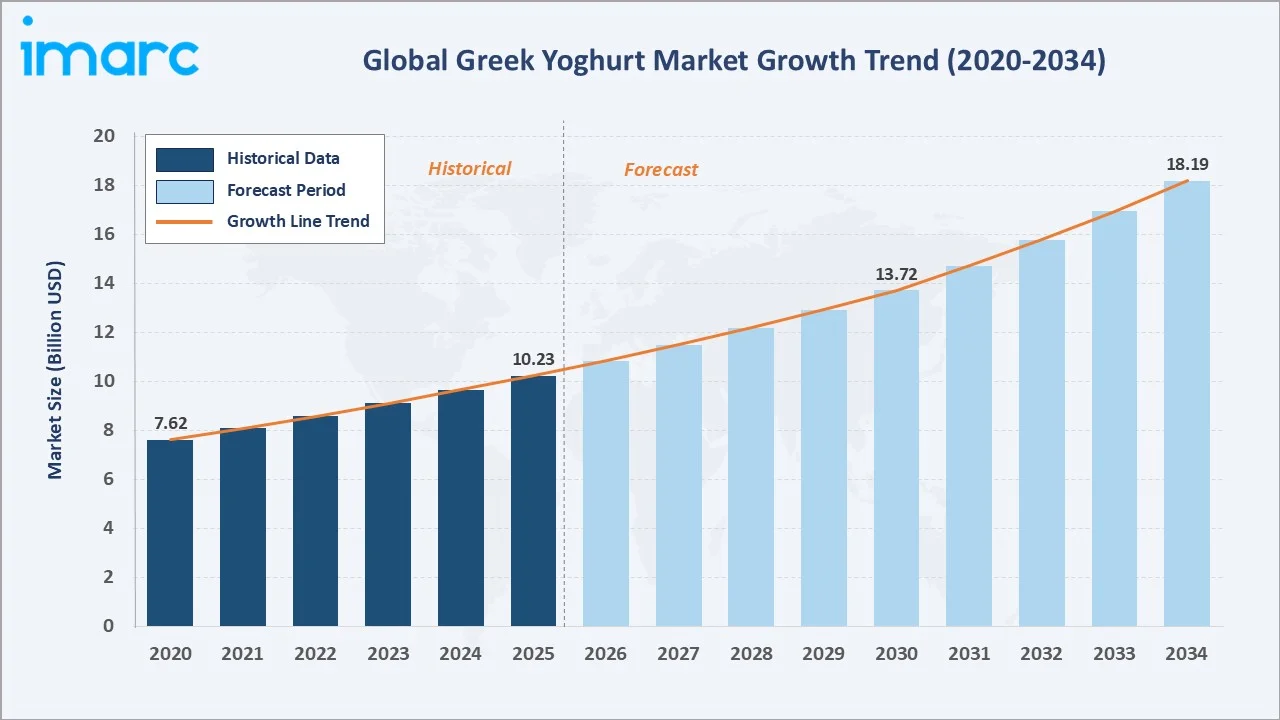

The global Greek yogurt market reached USD 10.23 Billion in 2025 and is projected to hit USD 18.19 Billion by 2034, growing at a CAGR of 6.05% during 2026-2034. Rising consumer demand for high-protein dairy products, increasing health awareness, expanding flavor innovation, and supportive clean-label trends are the key drivers shaping market growth. In October 2024, Chobani LLC launched its High Protein Greek Yogurt cups offering 20 grams of protein per serving, reflecting the category's strong momentum toward protein-forward positioning.

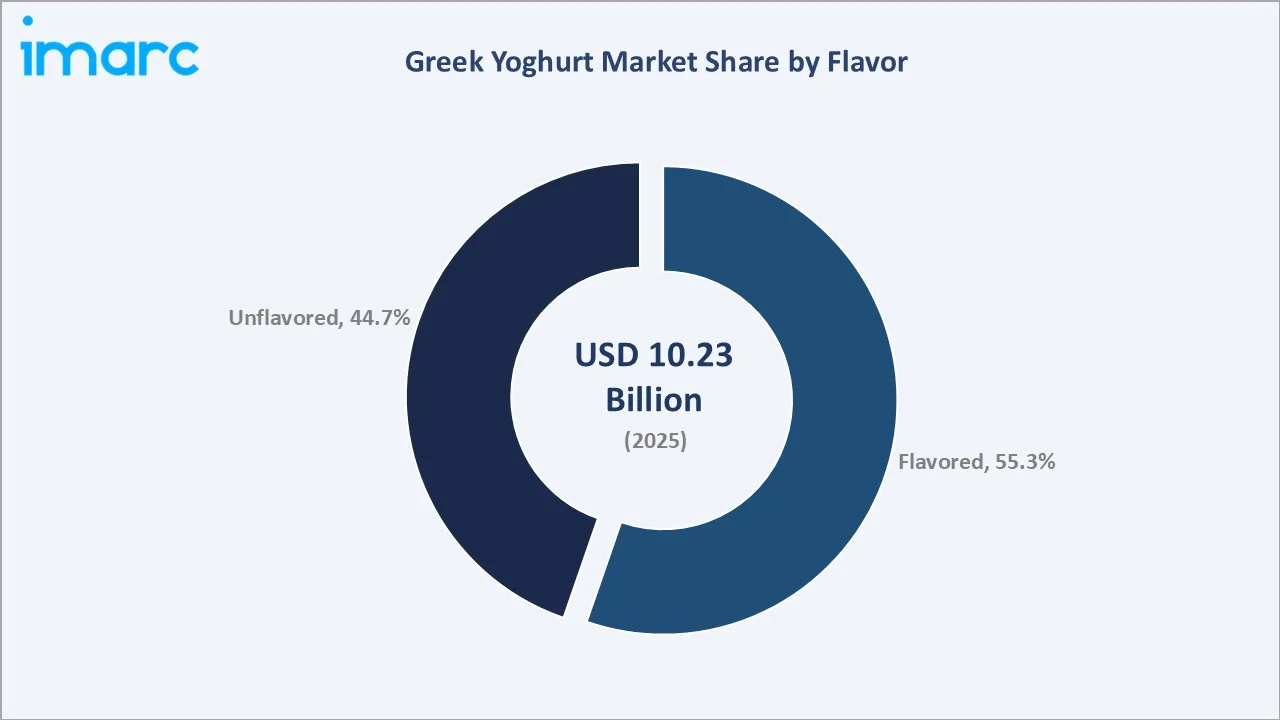

Regular Greek yogurt leads the product type segment at 58.7%, flavored dominates the flavor segment at 55.3%, and North America commands a 36.4% regional share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 10.23 Billion |

|

Forecast Market Size (2034) |

USD 18.19 Billion |

|

CAGR (2026-2034) |

6.05% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North America (36.4%, 2025) |

|

Fastest Growing Region |

Asia-Pacific (18.6%, 2025) |

|

Leading Product Type |

Regular Greek Yogurt (58.7%, 2025) |

|

Leading Flavor Segment |

Flavored (55.3%, 2025) |

The global Greek yogurt market expanded from USD 7.62 Billion in 2020 to USD 10.23 Billion in 2025, supported by growing consumer preference for high-protein snacks, rising awareness around probiotic dairy, and continued product innovation. Anchored at USD 13.72 Billion in 2030, the forecast to USD 18.19 Billion by 2034 is driven by mainstream adoption of functional dairy and expanding distribution in emerging markets.

To get more information on this market, Request Sample

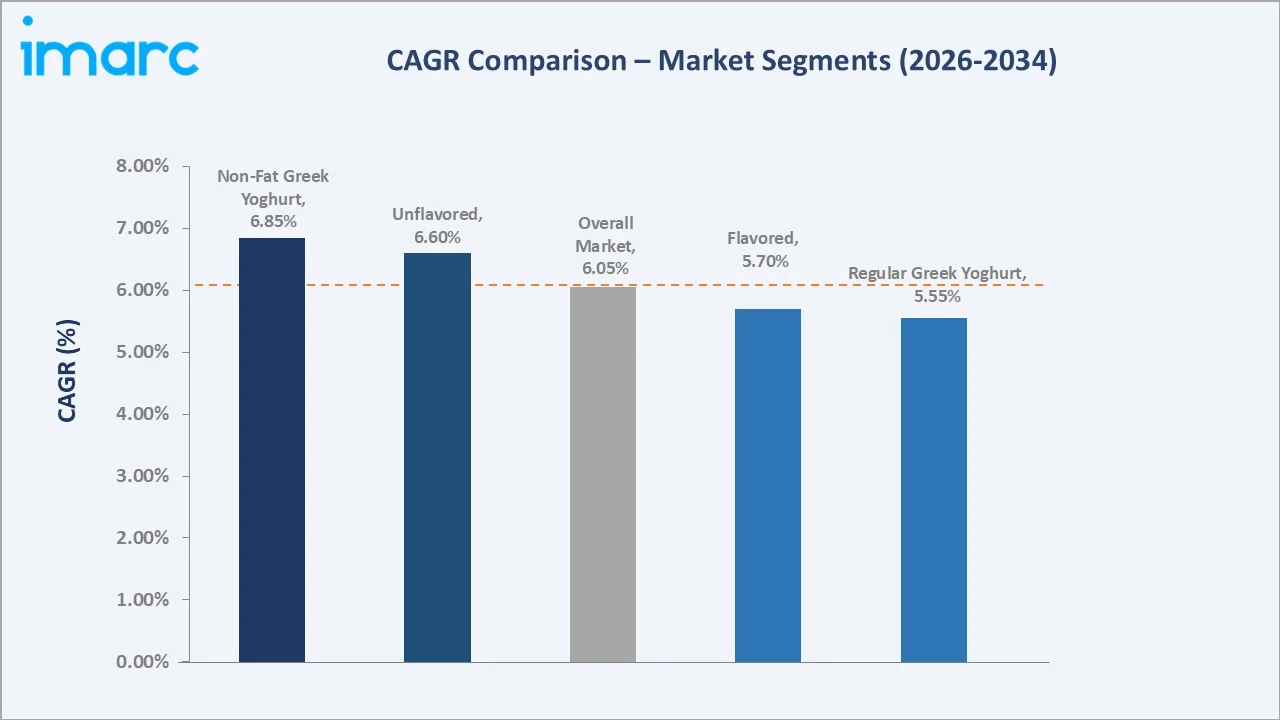

CAGR trajectories across product type and flavor sub-segments indicate that non-fat Greek yogurt and unflavored are gaining faster traction relative to the overall 6.05% market CAGR, fueled by calorie-conscious consumers and growing culinary applications.

Executive Summary

The global Greek yogurt market is on a steady growth trajectory, expanding from USD 7.62 Billion in 2020 to a projected USD 18.19 Billion by 2034. Once viewed as a premium niche, Greek yogurt has transitioned into a mainstream protein-rich dairy staple. Falling barriers to adoption, widening flavor portfolios, and stronger retail placement are reinforcing its place in everyday consumer routines across both developed and emerging markets.

Regular Greek yogurt dominates the product type segment with 58.7% share in 2025, supported by its rich texture, higher protein content, and versatility in culinary applications. Flavored leads the flavor segment at 55.3%, reflecting the growing popularity of fruit-infused and dessert-inspired options among younger consumers. North America holds a 36.4% regional share, anchored by strong brand presence, mature retail infrastructure, and high per-capita consumption. In April 2025, Chobani LLC announced a USD 1.2 Billion investment to build a new dairy processing facility in Rome, New York, signaling robust confidence in sustained consumer demand.

Key Market Insights

|

Insight |

Data |

|

Leading Product Type |

Regular Greek Yogurt - 58.7% revenue share (2025) |

|

Second Product Type |

Non-Fat Greek Yogurt - 41.3% revenue share (2025) |

|

Leading Flavor Segment |

Flavored - 55.3% revenue share (2025) |

|

Second Flavor Segment |

Unflavored - 44.7% revenue share (2025) |

|

Leading Region |

North America - 36.4% revenue share (2025) |

|

Fastest Growing Region |

Asia-Pacific - 18.6% revenue share (2025) |

|

Top Companies |

Chobani LLC, Fage International S.A., Lactalis, Danone, Emmi Group |

Key Analytical Observations Expanding on the Data Dbove:

- Regular Greek yogurt dominance at 58.7% is driven by strong consumer preference for traditional full-fat variants, supported by their rich taste, creamy texture, and versatility across breakfast, snacking, and cooking applications.

- Non-fat Greek yogurt at 41.3% is gaining share through its alignment with weight-management trends, diabetic-friendly positioning, and growing demand for low-calorie high-protein snacks.

- Flavored leadership at 55.3% is supported by fruit, vanilla, and indulgent dessert-inspired variants that drive category excitement, particularly among millennial and Gen Z consumers seeking novelty and premium taste experiences.

- Unflavored at 44.7% continues to attract health-focused consumers due to its clean label, zero added sugar, and versatility in home cooking, smoothies, and meal preparation.

- North America at 36.4% leads the market on the back of high per-capita yogurt consumption, strong brand presence, and well-established retail networks across the United States and Canada, further supported by regulatory recognition of yogurt’s potential role in reducing type 2 diabetes risk. In March 2024, the US FDA announced a qualified health claim stating that regular yogurt intake may reduce the risk of type 2 diabetes, further strengthening the category's health positioning. The FDA regards 2 cups (3 servings) of yogurt weekly as the minimum quantity for this qualified health claim.

- Asia-Pacific at 18.6% represents the fastest-growing region, fueled by rising disposable incomes, rapid urbanization, expanding cold-chain infrastructure, and increasing consumer preference for premium dairy products.

Global Greek Yogurt Market Overview

Greek yogurt is a strained dairy product made by filtering regular yogurt through cheesecloth or specialized membranes to remove excess whey, resulting in a thick, creamy texture with higher protein concentration than traditional yogurt. It typically delivers 15 to 20 grams of protein per serving.

The global ecosystem spans dairy farms, milk processors, bacterial culture suppliers, packaging converters, cold-chain logistics providers, private-label manufacturers, branded food companies, modern-trade retailers, quick-commerce platforms, and foodservice operators, together enabling wide product availability across consumption occasions.

Market Dynamics

To evaluate market opportunities, Request Sample

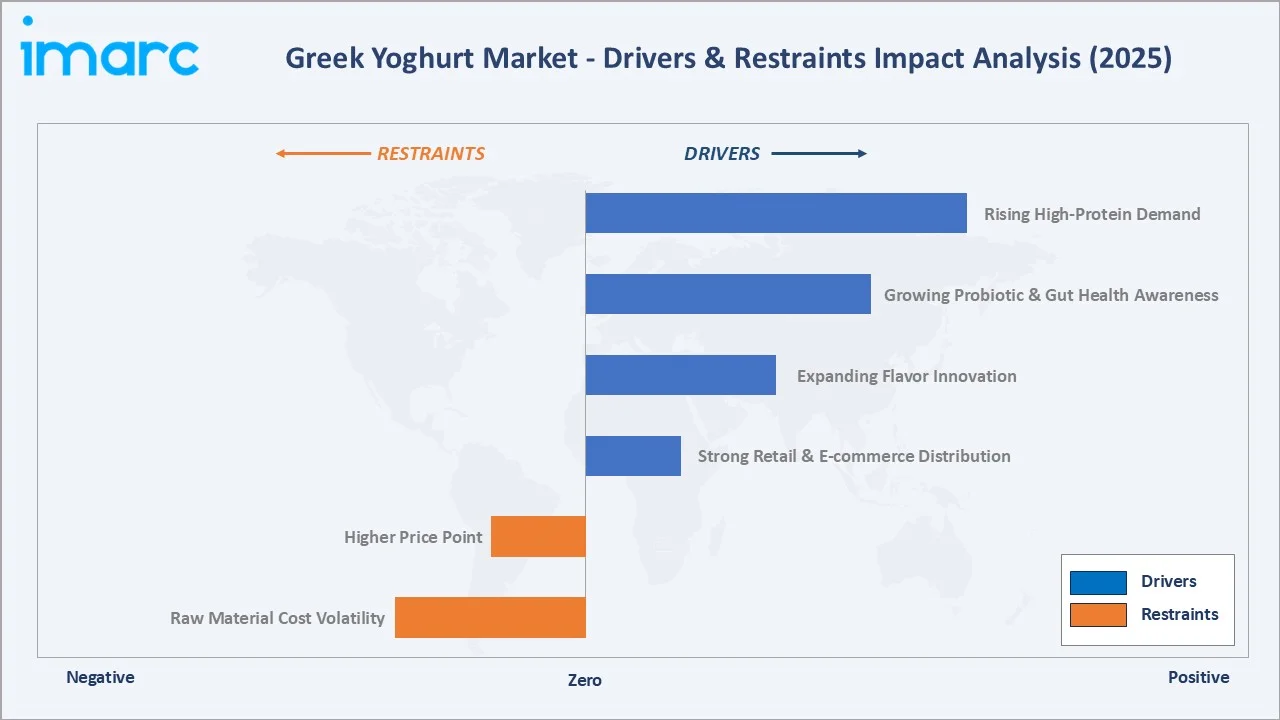

Market Drivers

- Rising Consumer Demand for High-Protein Foods: Health-conscious consumers increasingly seek protein-rich snack options, and Greek yogurt offers roughly double the protein of regular yogurt per serving, positioning it as a preferred functional food choice.

- Growing Awareness of Probiotic and Gut Health Benefits: Heightened consumer focus on digestive wellness and immunity is fueling demand for live culture dairy products. According to the International Diabetes Federation (IDF) Diabetes Atlas (2025), 11.1% of adults aged 20 to 79 globally were living with diabetes, boosting interest in low-sugar, high-protein dairy options such as Greek yogurt.

- Expanding Flavor Innovation and Product Variety: Continuous launches in fruit, exotic, and dessert-inspired flavors are broadening the consumer base and keeping the category relevant across demographics and taste preferences.

- Strong Retail and E-commerce Distribution: Supermarkets, hypermarkets, convenience stores, and online grocery platforms are making Greek yogurt widely accessible, with quick-commerce further accelerating household penetration in urban markets.

Market Restraints

- Higher Price Point Compared to Regular Yogurt: Greek yogurt production requires 3 pounds of milk to yield one cup of finished product through its authentic straining process, as stated by Chobani LLC, which structurally elevates manufacturing costs and limits adoption among price-sensitive consumers in emerging economies.

- Raw Material and Input Cost Volatility: Greek yogurt production requires significantly more milk than conventional yogurt, making the category sensitive to fluctuations in dairy prices, energy costs, and packaging inputs.

- Competition from Plant-Based Alternatives: Rising popularity of almond, coconut, and soy-based yogurt alternatives among vegan and lactose-intolerant consumers is drawing a share of wallet away from traditional dairy Greek yogurt offerings.

Market Opportunities

- Expansion into Emerging Markets: Rising middle-class populations in countries such as India, Brazil, China, and Indonesia, combined with increasing health awareness, offer significant headroom for category expansion.

- Premium and Functional Product Development: Opportunities exist for fortified Greek yogurt enriched with collagen, fiber, vitamins, adaptogens, and enhanced probiotic strains, targeting wellness and fitness-focused consumers.

- Drinkable and Portable Formats: Single-serve drinkable yogurts, squeezable tubes, and on-the-go pouches are emerging as high-growth adjacencies aligned with snacking and convenience-driven lifestyles.

Market Challenges

- Acid Whey Disposal and Sustainability: The Greek yogurt straining process generates large volumes of acid whey byproduct, creating environmental disposal concerns and rising compliance costs for manufacturers.

- Supply Chain and Cold-Chain Requirements: Temperature-sensitive products demand robust refrigerated logistics infrastructure, which remains underdeveloped in several emerging markets and constrains wider distribution.

- Private-Label and Commoditization Pressure: Growing private-label penetration in modern trade and quick-commerce channels is squeezing branded manufacturer margins and intensifying price competition.

Emerging Market Trends

1. Rise of High-Protein Greek Yogurt Variants

Protein-fortified Greek yogurt with 15 to 30 grams of protein per serving is becoming a defining category trend, driven by fitness culture, weight-management diets, and the broader protein-focused consumer mindset. In April 2025, Parag Milk Foods broadened its product range with nutrient-dense, high-protein offerings, addressing the increasing demand for health-oriented nutrition. This strategic investment highlights the company's dedication to innovation and quality, solidifying its status as a top provider of premium dairy nutrition in the rapidly expanding Indian and global markets.

2. Clean-Label and No-Added-Sugar Formulations

Consumer scrutiny of ingredient lists is pushing brands toward clean-label Greek yogurts with no artificial flavors, preservatives, or added sugars. Natural sweeteners, such as monk fruit, stevia, and allulose, are being adopted to retain taste while meeting health-led expectations.

3. Drinkable and Snackable Formats Expansion

Drinkable Greek yogurts, squeezable pouches, and single-serve protein drinks are gaining traction as convenient alternatives to traditional cups. These formats address on-the-go snacking needs and broaden the category's appeal beyond breakfast consumption occasions.

4. Premiumization and Culinary-Inspired Flavors

Brands are moving beyond strawberry and vanilla toward exotic, dessert-inspired, and regionally tailored flavor profiles such as mango hibiscus, matcha, salted caramel, and cheesecake. This premiumization is enabling margin expansion and attracting adventurous millennial and Gen Z consumers.

Industry Value Chain Analysis

The Greek yogurt value chain covers six key stages from raw milk sourcing through end-consumer consumption. Value concentration is highest at the processing, branding, and retail distribution stages, while sourcing reliability and cold-chain efficiency form the backbone of category competitiveness.

|

Stage |

Key Players / Examples |

|

Raw Material Supply |

Dairy farms, co-operatives, and milk processors supplying fresh raw milk and cultures |

|

Processing & Straining |

Dairy processors operating yogurt culturing, straining, and packaging lines |

|

Ingredient & Flavor Sourcing |

Suppliers of fruit preparations, natural flavors, sweeteners, and probiotic cultures |

|

Packaging & Cold Chain |

Packaging converters, refrigerated warehouses, and logistics providers |

|

Distribution & Retail |

Supermarkets, hypermarkets, specialty stores, convenience chains, and online grocery platforms |

|

End Use & Consumer |

Household consumers, foodservice operators, and institutional buyers |

Vertically integrated players with owned dairy supply and proprietary culture libraries enjoy stronger margin control, faster product development, and better continuity of supply compared to players reliant on third-party milk sourcing.

Technology Landscape in the Global Greek Yogurt Industry

Advanced Straining and Filtration Techniques

Membrane filtration and ultra-filtration methods are replacing traditional cloth-bag straining, enabling higher yields, greater protein concentration, and reduced acid whey waste. These improvements are enhancing production efficiency and sustainability for large-scale manufacturers.

Probiotic and Fermentation Innovation

Development of novel probiotic strains and controlled fermentation technologies is enabling brands to deliver targeted gut health, immunity, and digestive wellness benefits. This is strengthening functional positioning and supporting premium pricing in the category.

Sustainable Packaging Solutions

Paper-based cups, bio-resins, and recyclable mono-material formats are gaining adoption as brands respond to consumer and regulatory pressure on plastic use. Lightweight designs and reduced plastic content are becoming standard across leading product lines.

Smart Manufacturing and Digital Quality Control

Automation, Internet of Things (IoT)-enabled process monitoring, and artificial intelligence (AI)-driven quality checks are improving consistency, reducing downtime, and enhancing traceability from farm to shelf. These digital capabilities also support regulatory compliance and brand trust.

Market Segmentation Analysis

The report includes following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product Type |

Regular Greek Yogurt |

58.7% |

2025 |

|

Flavor |

Flavored |

55.3% |

2025 |

|

Distribution Channel |

Hypermarkets and Supermarkets |

43.5% |

2025 |

|

Region |

North America |

36.4% |

2025 |

By Product Type

Regular Greek yogurt commands a 58.7% majority share in 2025, driven by its creamy texture, higher fat content, and broad culinary use across breakfast, snacking, and cooking applications. Consumers favor its indulgent taste profile and nutritional density, particularly in North American and European markets.

To access detailed market analysis, Request Sample

Non-fat Greek yogurt holds a 41.3% share in 2025, supported by its low-calorie profile, high-protein density, and strong appeal among weight-management and fitness-focused consumers. This segment is growing at a faster pace than regular variants, aided by diabetic-friendly positioning and clean-label marketing.

By Flavor

Flavored leads with 55.3% share in 2025, fueled by continuous launches in fruit, vanilla, honey, and dessert-inspired variants. Strawberry, blueberry, and peach are category staples, while emerging adventurous flavors are broadening the consumer base and driving premium price points.

Unflavored accounts for 44.7% in 2025, underpinned by its clean-label appeal, zero added sugar, and wide culinary applications. Plain variants are preferred by health-conscious consumers, athletes, and home cooks using it as a base for smoothies, dips, marinades, and baking.

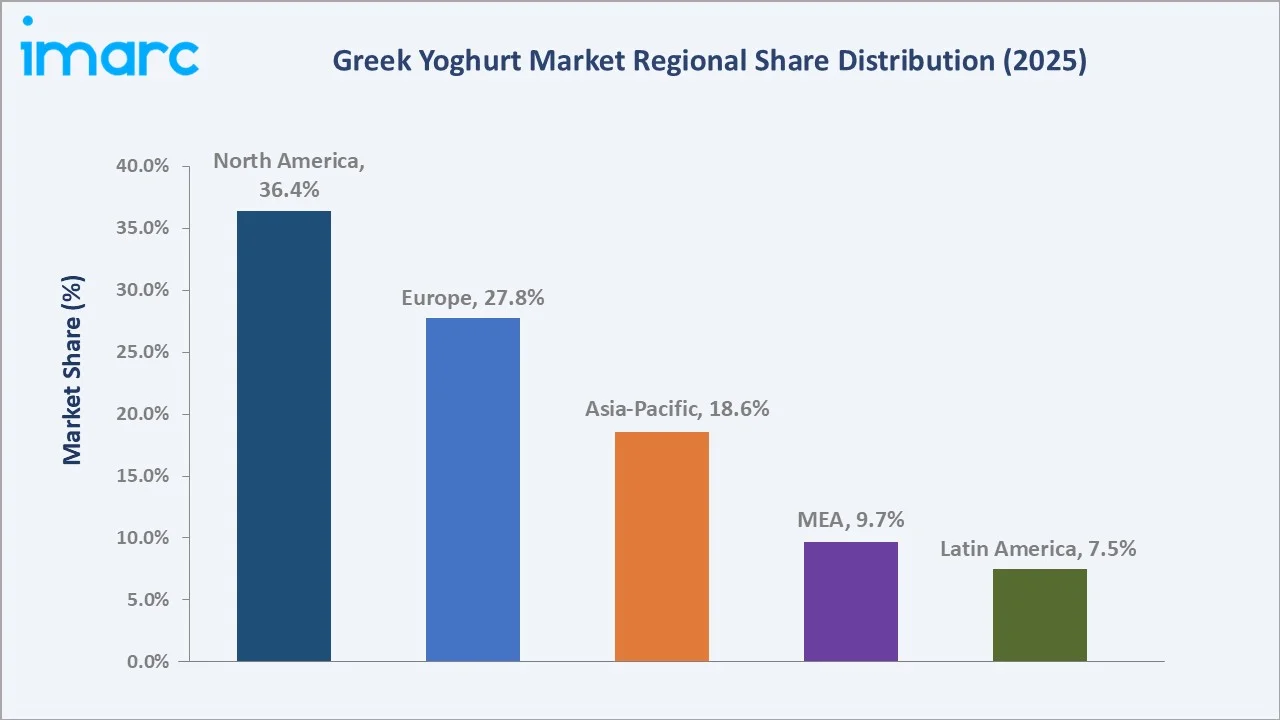

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

North America |

36.4% |

Strong health and wellness trends, established retail networks, and consumer preference for high-protein dairy products |

|

Europe |

27.8% |

Deep-rooted yogurt consumption culture, rising demand for clean-label offerings, and innovation in functional dairy |

|

Asia-Pacific |

18.6% |

Rising disposable incomes, rapid urbanization, growing middle-class population, and expanding modern retail infrastructure |

|

Middle East and Africa |

9.7% |

Traditional dairy consumption habits, growing health awareness, and increasing penetration of packaged branded yogurt |

|

Latin America |

7.5% |

Expanding supermarket penetration, rising interest in functional foods, and growing affordability of premium dairy |

North America at 36.4% in 2025 leads the global market, anchored by strong brand presence, mature retail infrastructure, and high per-capita yogurt consumption in the United States and Canada. The region benefits from active innovation pipelines, widespread cold-chain networks, and entrenched consumer familiarity with Greek yogurt as a mainstream staple.

Asia-Pacific at 18.6% is the highest-growth region through 2034. Rising disposable incomes, urban lifestyle shifts, expanding modern trade, and growing health awareness in China, India, Japan, and Australia are accelerating premium dairy adoption.

Competitive Landscape

The global Greek yogurt market is moderately consolidated, with a handful of leading players dominating brand recognition and shelf space in mature markets, while regional specialists serve niche flavor, format, and price-tier segments. Brand equity, distribution reach, and innovation cadence form the key competitive levers.

|

Company Name |

Brand / Key Product |

Position |

Strategic Focus |

|

Chobani LLC |

Chobani |

Leader |

High-protein innovation; mainstream retail leadership; US manufacturing expansion |

|

Fage International S.A. |

FAGE Total |

Leader |

Authentic Greek heritage; premium positioning; family-owned vertically integrated operations |

|

Lactalis |

Stonyfield Organic, Yoplait |

Leader |

Multi-brand portfolio spanning organic, Greek, and skyr segments; scale-driven consolidation through acquisitions; global dairy manufacturing footprint |

|

Danone |

Oikos |

Challenger |

Strong probiotic positioning; high-protein product range; wide global footprint |

|

Emmi Group |

Emmi Swiss Premium Greek Style Yogurt |

Emerging |

Premium niche specialization over mass-market competition; high-protein and functional dairy positioning |

Key players include Chobani LLC, Fage International S.A., Lactalis, Danone, and Emmi Group, among others.

Key Company Profiles

Chobani LLC

Chobani LLC is a US-based food and beverage company, recognized as America's leading Greek yogurt brand. Founded in 2005 by Hamdi Ulukaya, the company has played a pivotal role in transforming Greek yogurt into a mainstream category across the United States and internationally.

- Product Portfolio: Greek Yogurt cups and tubs, Chobani High Protein line, Chobani Flip, Chobani Less Sugar, drinkable yogurts, oat milk, dairy creamers, and ready-to-drink coffee.

- Recent Developments: In May 2025, Chobani LLC acquired plant-based food maker Daily Harvest, expanding its portfolio into ready-to-make smoothies, bowls, and frozen meals — the company's first entry into the frozen grocery category. In March 2025, the firm also announced a USD 500 Million expansion of its Twin Falls, Idaho facility to boost production capacity by 50%.

- Strategic Focus: Protein-forward product innovation, natural ingredient sourcing, domestic manufacturing expansion, and diversification into adjacent dairy and ready-to-drink beverage categories.

Fage International S.A.

Fage International S.A. is a family-owned international dairy company founded in Athens, Greece in 1926. It is widely recognized as the brand that introduced authentic strained Greek yogurt to global markets through its flagship FAGE Total range.

- Product Portfolio: FAGE Total (full-fat, 2%, 0%) plain strained Greek yogurt, FAGE Total Split Cup with fruit and honey, lactose-free yogurt variants, sour cream, and traditional Greek dairy products including feta cheese.

- Recent Developments: FAGE continues to expand its US footprint through its Johnstown, New York manufacturing facility and has introduced new flavor variants and lactose-free formats aimed at broadening appeal among health-conscious and lactose-sensitive consumers.

- Strategic Focus: Authentic Greek heritage branding, premium quality positioning, vertical integration from milk sourcing to retail, and targeted expansion across North America and Europe through established distribution partnerships.

Lactalis

Lactalis is a leading global dairy corporation with operations spanning milk, cheese, butter, cream, yogurt, and specialty dairy ingredients. As one of the largest players in the worldwide dairy industry, the company maintains a broad multi-brand portfolio across organic, Greek, strained, and high-protein yogurt categories, with a strong presence in both retail and foodservice channels across North America, Europe, and international markets.

- Product Portfolio: Stonyfield Organic Greek Yogurt, Brown Cow cream top yogurt, Green Mountain Creamery Greek yogurt, Yoplait Greek, :ratio high-protein Greek yogurt, Oui French-style yogurt, Go-Gurt kids' yogurt, along with cheese, butter, cream, and specialty dairy brands.

- Recent Developments: In June 2025, Lactalis USA completed the acquisition of General Mills' US yogurt business, adding Yoplait, Go-Gurt, Oui, Mountain High, and :ratio brands along with manufacturing facilities in Murfreesboro, Tennessee and Reed City, Michigan.

- Strategic Focus: Scale-led portfolio consolidation through acquisitions, multi-brand positioning across organic, Greek, protein-forward, and skyr segments, global manufacturing footprint expansion, and strengthening leadership in both branded retail and foodservice yogurt channels.

Market Concentration Analysis

The global Greek yogurt market is moderately consolidated, with the top five players (Chobani LLC, Fage International S.A., Lactalis, Danone, and Emmi Group) estimated to account for a significant share of branded sales in mature markets, such as the United States and Western Europe.

Barriers to entry include brand trust, cold-chain and distribution infrastructure, dairy sourcing scale, proprietary culture libraries, and retail shelf access, all of which favor well-capitalized incumbents with established manufacturing footprints.

Consolidation is expected to accelerate through acquisitions, private-label expansion, and strategic partnerships. Meanwhile, emerging markets remain more fragmented, with regional dairy co-operatives and local brands competing on price, freshness, and culturally adapted flavor profiles.

Investment & Growth Opportunities

Fastest-Growing Segments

Non-fat Greek yogurt and unflavored variants are expanding faster than the overall 6.05% market CAGR through 2034, supported by fitness culture, diabetic-friendly positioning, and the ongoing shift toward low-sugar functional dairy.

Emerging Markets

Asia-Pacific at 18.6% represents the highest-growth region, with China, India, Japan, and Australia leading category expansion. Latin America and the Middle East and Africa offer significant untapped opportunities as retail modernization and cold-chain investments unlock premium dairy adoption.

Venture & Investment Trends

Capital is flowing into high-protein dairy innovation, sustainable packaging, precision fermentation, plant-based Greek-style alternatives, and direct-to-consumer digital brands. Private equity activity is also increasing in regional dairy processors with strong Greek yogurt portfolios and premium positioning.

Future Market Outlook (2026-2034)

The global Greek yogurt market is forecast to expand from USD 10.23 Billion in 2025 to USD 18.19 Billion by 2034 at a CAGR of 6.05%, adding approximately USD 7.96 Billion in incremental market value over the forecast period.

Four forces will shape category evolution through 2034: accelerating high-protein adoption, clean-label and no-added-sugar reformulation, geographic expansion into Asia-Pacific and Latin America, and premiumization through functional ingredients and innovative flavor experiences.

By 2034, Greek yogurt is expected to remain a mainstream dairy staple in developed markets while emerging as a fast-growth premium category across developing economies. Digital retail, quick-commerce, and private-label growth will further redefine category dynamics and consumer access over the decade.

Research Methodology

Primary Research

Primary research included in-depth interviews with dairy processors, brand marketing executives, retail category managers, foodservice operators, and ingredient suppliers, validating market sizing, regional demand patterns, flavor preferences, and product-mix evolution across consumption channels.

Secondary Research

Secondary sources include industry association reports, company annual filings, regulatory databases, trade publications, retail scan data, government statistics, investor presentations, and press releases from listed and private dairy manufacturers operating in the Greek yogurt category.

Forecasting Models

Market forecasts combine top-down and bottom-up modeling approaches, incorporating per-capita consumption trends, retail channel growth, pricing trajectories, product innovation pipelines, and macroeconomic indicators. Scenario analysis addresses raw milk price fluctuations and private-label penetration risks.

Greek Yogurt Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Regular Greek Yogurt, Non-Fat Greek Yogurt |

| Flavors Covered | Flavored, Unflavored |

| Distribution Channels Covered | Hypermarkets and Supermarkets, Specialty Stores, Convenience Stores, Independent Retailers, Online, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Companies Covered | Chobani LLC, Fage International S.A., Lactalis, Danone, Emmi Group, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Greek yogurt market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global Greek yogurt market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Greek yogurt industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Greek Yogurt Market Report

The global Greek yogurt market was valued at USD 10.23 Billion in 2025, supported by rising protein demand, clean-label preferences, and broader flavor innovation.

The market is projected to grow at 6.05% CAGR from 2026 to 2034, reaching USD 18.19 Billion, driven by high-protein adoption and expanding emerging market demand.

Regular Greek yogurt leads at 58.7% in 2025, favored for its creamy texture, higher fat content, and culinary versatility across breakfast, snacking, and cooking.

Flavored dominates at 55.3% in 2025, supported by fruit, vanilla, and dessert-inspired variants that continue to attract younger consumer demographics.

North America commands 36.4% in 2025, anchored by strong brand presence and mature retail. Asia-Pacific at 18.6% is the fastest-growing region through 2034.

Leading players include Chobani LLC, Fage International S.A., Lactalis, Danone, and Emmi Group.

Demand is driven by fitness culture, weight-management diets, and broader consumer interest in functional foods delivering 15 to 20 grams of protein per serving.

Greek yogurt is strained to remove excess whey, resulting in a thicker texture, roughly double the protein, and lower sugar and lactose than conventional yogurt.

Flavor innovation drives premiumization and consumer engagement, with brands launching fruit, exotic, and dessert-inspired variants to broaden appeal and raise margins.

Key challenges include higher production costs, acid whey disposal, cold-chain requirements, price sensitivity in emerging markets, and competition from plant-based alternatives.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)