Green Data Center Market Size, Share, Trends and Forecast by Component, Data Center Type, Industry Vertical, and Region, 2026-2034

Global Green Data Center Market Size, Share, Trends & Forecast (2026-2034)

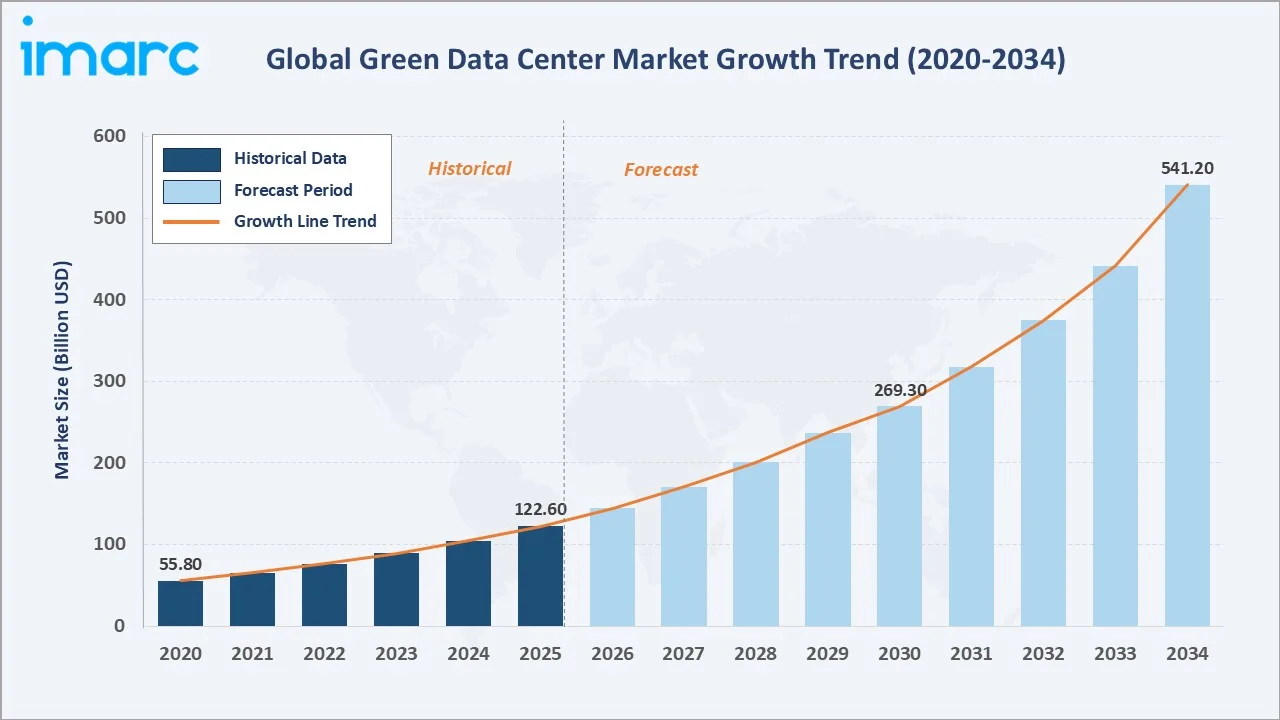

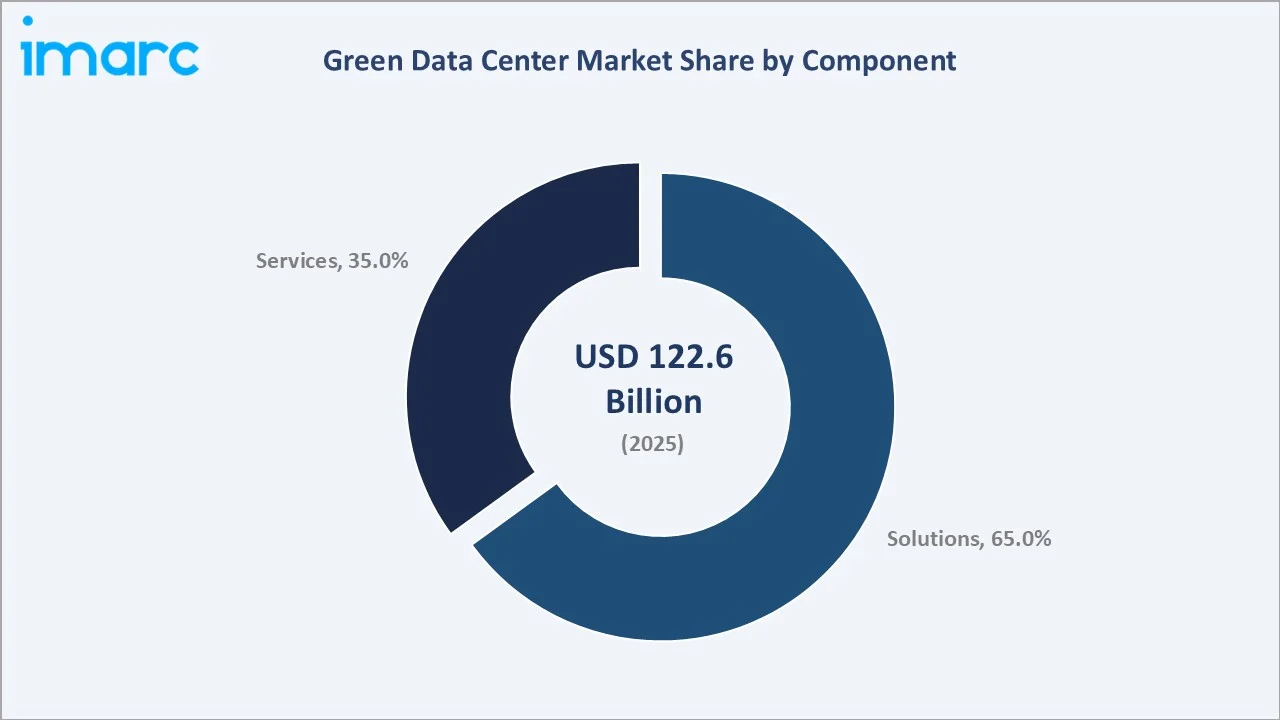

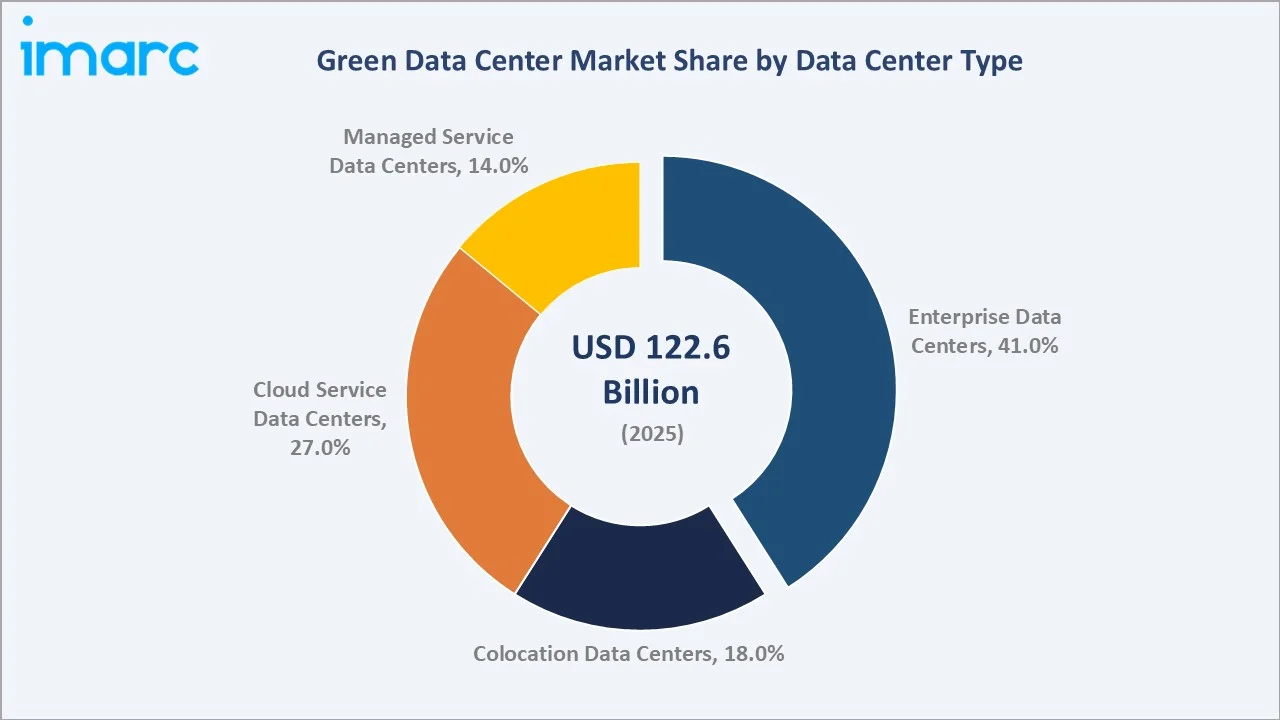

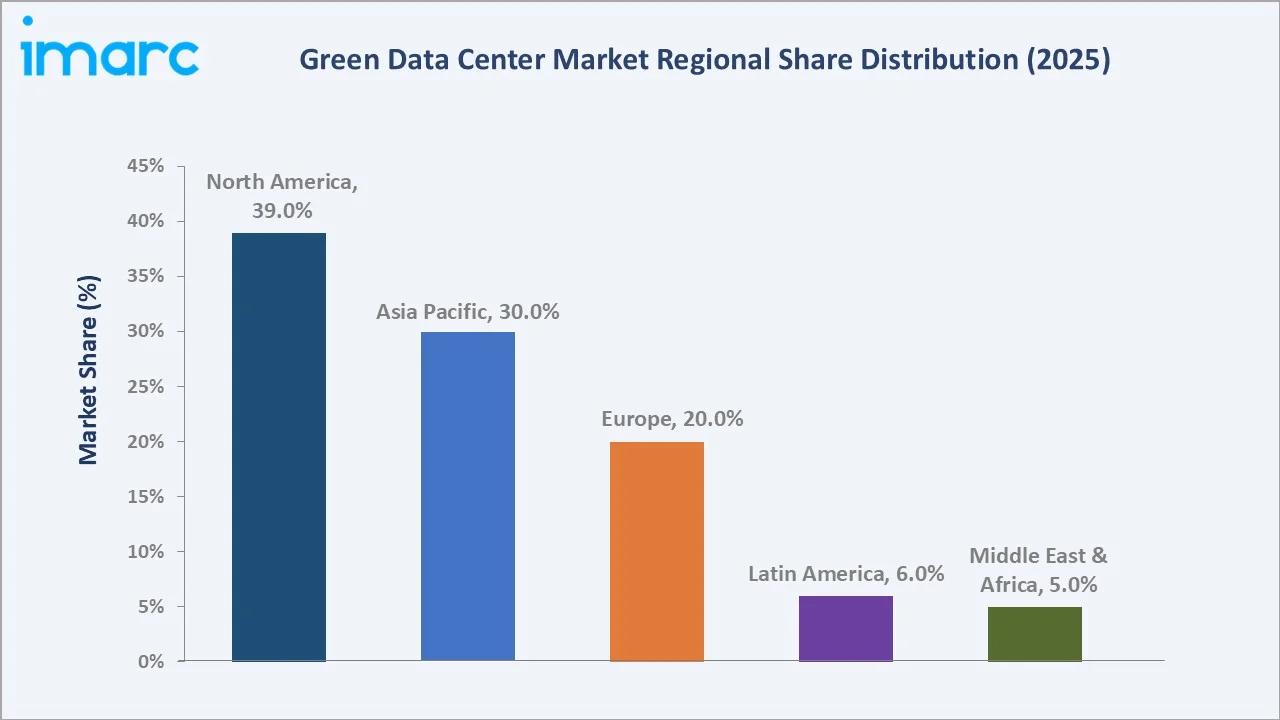

The global green data center market size was valued at USD 122.6 Billion in 2025 and is projected to reach USD 541.2 Billion by 2034, at a CAGR of 17.04% during 2026-2034. Rapid expansion of cloud computing, rising enterprise IT infrastructure investments, and intensifying corporate sustainability mandates are collectively driving green data center market growth. The Solutions segment dominates with a 65.0% share in 2025, while Enterprise Data Centers lead by type with a 41.0% share. North America commands regional leadership with a 39.0% revenue share in 2025.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 122.6 Billion |

|

Forecast Market Size (2034) |

USD 541.2 Billion |

|

CAGR (2026-2034) |

17.04% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North America (39.0% share, 2025) |

|

Fastest Growing Region |

Asia Pacific |

|

Leading Component |

Solutions (65.0%, 2025) |

|

Leading Data Center Type |

Enterprise Data Centers (41.0%, 2025) |

The chart below illustrates green data center market growth from 2020 to 2034, with cloud adoption driving the historical trajectory and sustainability-driven modernization supporting the forecast.

To get more information on this market, Request Sample

CAGR analysis identifies Solutions and Enterprise Data Centers as the largest-contributing segments in the global green data center market, with cloud service centers representing the fastest-growing type through 2034.

Executive Summary

The global green data center market is rapidly transforming due to rising digital demand, stricter carbon regulations, and growing net-zero commitments. Valued at USD 122.6 billion in 2025, the market is projected to reach USD 541.2 billion by 2034, expanding at a CAGR of 17.04%. The transition toward energy-efficient infrastructure is accelerating, led by hyperscale and cloud-native companies deploying at scale.

The Solutions segment leads with 65.0% in 2025, driven by hardware upgrades and renewable integration needs. Enterprise Data Centers dominate at 41.0%, while Cloud Service Data Centers hold 27.0%, reflecting demand from both on-premises and hyperscale cloud operators. Key trends include liquid cooling adoption, AI-driven energy management, and on-site renewable energy integration.

North America leads global demand with a 39.0% share in 2025, driven by hyperscale investments in the United States. Asia Pacific accounts for 30.0% and is the fastest-growing region, supported by rapid digitalization across India, China, and Southeast Asia. Europe holds 20.0%, backed by EU sustainability mandates and strong energy-efficiency regulations.

Key Market Insights

|

Insight |

Data |

|

Largest Component Segment |

Solutions – 65.0% share (2025) |

|

Second Component Segment |

Services – 35.0% share (2025) |

|

Leading Data Center Type |

Enterprise Data Centers – 41.0% (2025) |

|

Leading Region |

North America – 39.0% revenue share (2025) |

|

Fastest Growing Region |

Asia Pacific – 30.0% share (2025) |

|

Top Companies |

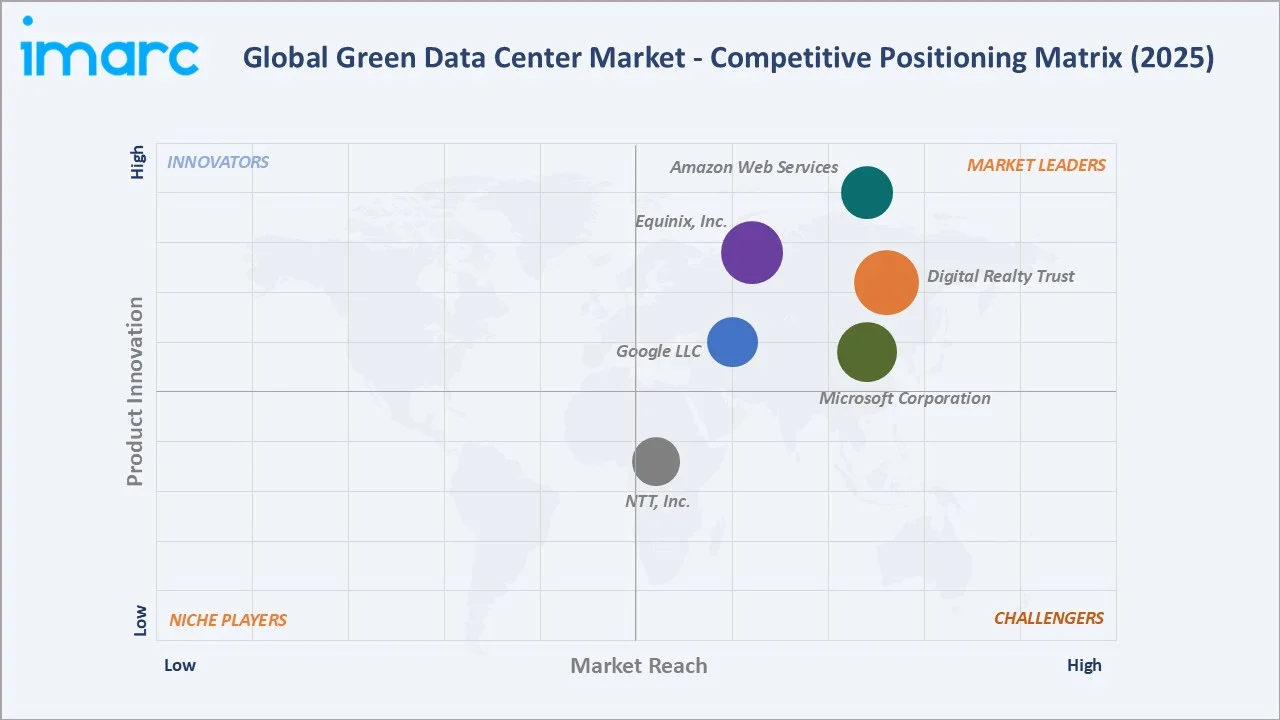

Equinix, Digital Realty, Google, Microsoft, Amazon |

|

Market Opportunity |

AI workload infrastructure and liquid cooling for next-gen GPU clusters |

Key Analytical Observations Supporting The Above Data:

- Solutions 65.0% dominance in 2025 reflects the high capital intensity of green infrastructure upgrades, with hardware such as energy-efficient servers, UPS systems, and advanced cooling units accounting for most spending in new deployments and retrofits.

- Services 35.0% share in 2025 reflects growing demand for sustainability consulting, green certification advisory, and monitoring-as-a-service, especially among mid-market firms lacking in-house green IT expertise.

- Enterprise Data Centers 41.0% market dominance in 2025 reflects organizations’ preference for private infrastructure control, data sovereignty compliance, and upgrading legacy on-premises facilities with energy-efficient systems.

- Cloud Service Data Centers at 27.0% in 2025 reflect the rapid expansion of hyperscale operators like Amazon, Microsoft, and Google collectively committed over $200 billion in new data center capacity in 2025.

- North America's 39.0% share in 2025 is driven by U.S. hyperscale investments, with Virginia, Texas, and Georgia leading as key global data centre hubs.

- Asia Pacific is the fastest-growing region, driven by India’s data center market valued at USD 10 billion in 2025 and projected to exceed USD 22 billion by 2030 alongside China’s push for energy-efficient digital infrastructure.

Global Green Data Center Market Overview

Green data centers are energy-efficient IT facilities designed or retrofitted to reduce environmental impact using renewable power and advanced cooling. The ecosystem includes hardware and software providers, energy suppliers, colocation operators, and service firms, supporting applications across cloud, AI/ML, enterprise IT, financial services, and telecom infrastructure.

Macroeconomic drivers include rising energy costs—data centers used 1.5% of global electricity in 2024 —and stricter carbon regulations across the EU, U.S., and APAC. Corporate net-zero goals and hyperscaler investments are accelerating adoption, with green PUE targets below 1.2 becoming standard in new large-scale deployments.

Market Dynamics

To evaluate market opportunities, Request Sample

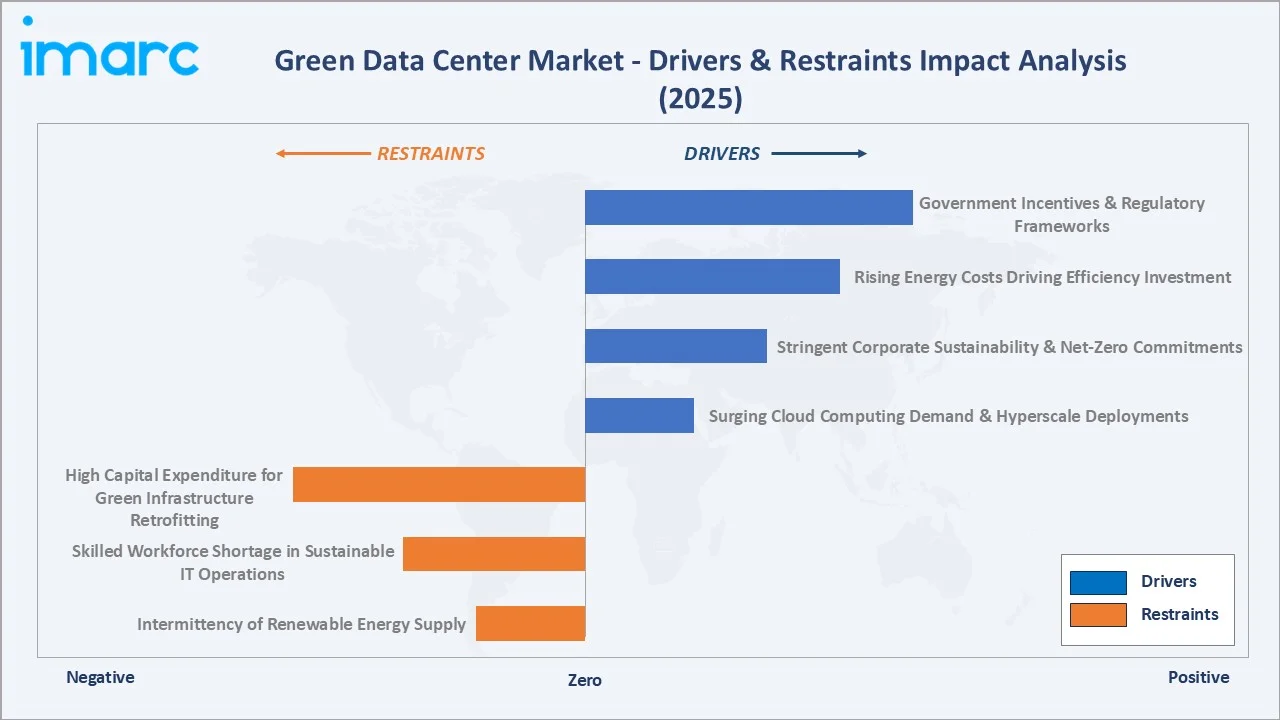

Market Drivers

- Surging Cloud Computing Demand and Hyperscale Deployments: Global cloud services revenue exceeded USD 600 billion in 2023, fueling strong demand for efficient data centers. Hyperscalers like Amazon Web Services, Microsoft Azure, and Google Cloud continue investing heavily in new capacity with sustainability-focused designs.

- Stringent Corporate Sustainability and Net-Zero Commitments: Over 5,000 companies had committed to the Science Based Targets initiative (SBTi) by 2024, driving Scope 2 emission reductions. Data centers account for ~1–1.5% of global electricity use, increasing pressure for greener operations.

- Rising Energy Costs Driving Efficiency Investment: Electricity prices rose significantly across key markets during 2021–2023, strengthening the business case for energy-efficient infrastructure. Improving PUE toward best-in-class levels (1.2 to 1.6 industry average) significantly reduces energy overhead and operating costs in large-scale data centers.

- Government Incentives and Regulatory Frameworks: The Inflation Reduction Act allocates USD 369 billion toward clean energy, supporting sustainable data centers. Similar policies under the EU Green Deal and India’s data center initiatives are accelerating green infrastructure adoption.

Rising IT outsourcing and AI-driven high-density computing are pushing organizations to replace legacy facilities with modern green data centers, while cost efficiency, regulatory compliance, and ESG goals continue to reinforce demand globally.

Market Restraints

- High Capital Expenditure for Green Infrastructure Retrofitting: Retrofitting conventional data centers into green facilities involves substantial upfront costs driven by cooling upgrades, renewable integration, and redesign. Industry sources such as Uptime Institute and International Energy Agency indicate costs are significantly higher than traditional builds, discouraging small and mid-sized operators from rapid transition.

- Skilled Workforce Shortage in Sustainable IT Operations: The data center sector faces a notable talent gap in areas like energy optimization, advanced cooling, and sustainability integration. Uptime Institute estimates a global shortage of skilled professionals, which is slowing deployment of efficient and green infrastructure.

- Intermittency of Renewable Energy Supply: On-site solar and wind energy generation face output variability challenges, particularly for 24/7 data center operations requiring continuous power availability. Battery energy storage systems (BESS) add cost and complexity to renewable integration projects.

Market Opportunities

- AI and High-Performance Computing Infrastructure Demand: AI infrastructure demand is rapidly expanding, with high-density GPU clusters increasing power and cooling needs. International Data Corporation highlights strong AI server growth, driving adoption of efficient cooling and green data center technologies.

- Emerging Market Data Center Expansion in Asia Pacific and Middle East: Emerging markets such as India, United Arab Emirates, and Saudi Arabia are witnessing strong data center investments supported by policy initiatives and digital growth, creating significant opportunities for green infrastructure development.

- Modular and Edge Data Center Green Deployment: Modular and prefabricated data centers enable faster deployment and improved energy efficiency. Growth of edge computing, 5G networks, and industrial IoT is accelerating demand for scalable, energy-efficient green data center solutions.

Market Challenges

- Water Usage and Cooling Environmental Trade-Offs: Evaporative cooling systems used in large-scale data centers consume millions of gallons of water annually. Microsoft's data centers used approximately 1.7 billion gallons of water in 2022, highlighting water scarcity tensions in drought-prone regions.

- Complexity of Multi-Vendor Green Certification Standards: Multiple certification systems such as LEED, BREEAM, and ISO 50001 increase compliance complexity and costs across regions with varying regulatory requirements.

- Grid Infrastructure Limitations in Emerging Markets: In regions like Southeast Asia and Africa, limited grid reliability and renewable availability constrain data centers’ ability to achieve fully green operations and meet sustainability targets.

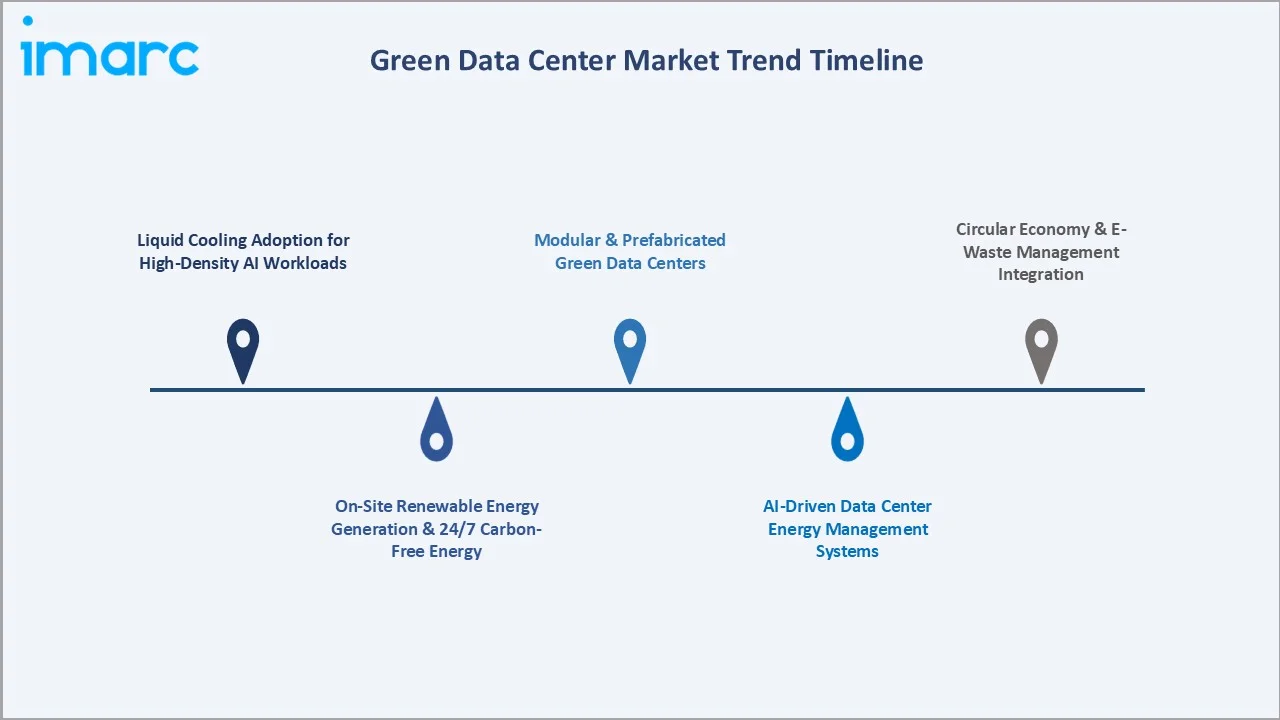

Emerging Market Trends

1. Liquid Cooling Adoption for High-Density AI Workloads

Liquid cooling (DLC, immersion) is rapidly scaling for AI workloads, enabling higher rack densities and improved efficiency. Uptime Institute notes it supports advanced thermal performance versus air cooling, with adoption rising across hyperscale and enterprise operators.

2. On-Site Renewable Energy Generation and 24/7 Carbon-Free Energy

Companies like Google, Microsoft, and Amazon are advancing 24/7 carbon-free energy goals. Google reported ~64% hourly CFE matching in 2023, driving renewable PPAs, storage, and on-site clean energy investments globally.

3. AI-Driven Data Center Energy Management Systems

AI-based energy optimization is improving efficiency across operations. Google DeepMind demonstrated ~40% cooling energy reduction using machine learning, highlighting strong potential for AI-driven sustainability solutions in data centers.

4. Modular and Prefabricated Green Data Centers

Prefabricated modular data centers are gaining traction for faster deployment and energy efficiency. Industry insights from Uptime Institute indicate modular builds can significantly reduce deployment timelines while integrating efficient cooling and power systems.

5. Circular Economy and E-Waste Management Integration

Circular IT practices are expanding, including reuse and recycling of hardware. Microsoft reports its Circular Centers enable reuse and diversion of servers from landfill, aligning with stricter ESG and sustainability regulations globally.

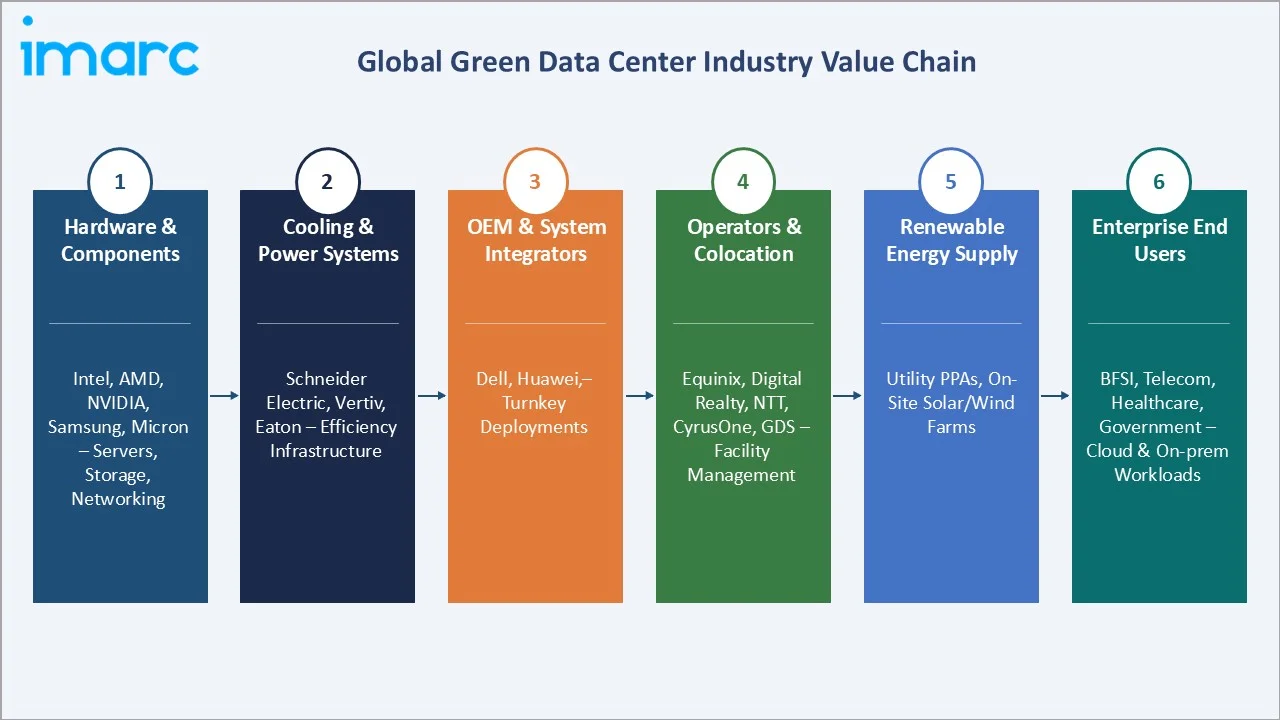

Industry Value Chain Analysis

The green data center value chain encompasses six interconnected stages, from raw materials to end-user consumption. Each stage involves unique technological requirements, sustainability considerations, and competitive dynamics that collectively define the market structure.

|

Stage |

Key Players / Examples |

|

Hardware & Components |

Intel, AMD, NVIDIA, Samsung, Micron |

|

Cooling & Power Systems |

Schneider Electric, Vertiv, Eaton, Siemens, ABB |

|

Green Data Center OEMs & Integrators |

Dell EMC, IBM, Huawei, Fujitsu, Hitachi, Cisco |

|

Operators & Colocation Providers |

Equinix, Digital Realty, NTT, CyrusOne, GDS |

|

Renewable Energy Supply |

Utility PPAs, on-site solar, wind farms, battery storage |

|

Enterprise End Users |

BFSI, telecom, healthcare, government |

Tier-1 hyperscale operators hold the highest value position by controlling infrastructure, software platforms, and direct renewable power sourcing. Their scale enables proprietary hardware design, custom cooling systems, and preferential renewable energy contracts inaccessible to smaller colocation operators.

Technology Landscape in the Green Data Center Industry

Advanced Cooling Technologies

Liquid cooling is gaining traction for AI/HPC workloads, enabling higher efficiency than air cooling. Uptime Institute highlights its role in managing high-density chips and improving energy performance in next-generation facilities.

Renewable Energy Integration

Data centers increasingly adopt renewable energy via PPAs, on-site generation, and storage. International Energy Agency notes strong growth in renewable procurement, supported by energy management tools optimizing carbon intensity and grid usage.

AI-Powered Energy Management Systems

AI-driven building management systems optimize cooling and power usage in real time. Solutions from Schneider Electric and others improve efficiency, with studies showing measurable energy savings versus traditional rule-based systems.

Software-Defined Infrastructure and Automation

Software-defined data centers and hyperconverged infrastructure improve resource utilization and reduce hardware demand. Platforms like VMware and Nutanix enable automation and higher efficiency, lowering overall energy consumption in enterprise environments.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Component | Solutions | 65.0% | 2025 |

| Data Center Type | Enterprise Data Centers | 41.0% | 2025 |

| Industry Vertical | Telecom and IT | 🔒 | 2025 |

| Region | North America | 39.0% | 2025 |

By Component

The Solutions segment captures 65.0% of the green data center market in 2025, driven by hardware upgrades and energy-efficient deployments. Power systems lead demand, while server modernization toward ARM and custom silicon is increasing across hyperscale operators.

To evaluate market opportunities, Request Sample

Services account for 35.0% in 2025, covering green certification, energy management, sustainability reporting, and infrastructure support. Growth is driven by mid-market firms outsourcing green data center strategy and operations to specialized providers due to limited in-house expertise.

By Data Center Type

Enterprise Data Centers hold the largest share at 41.0% in 2025, driven by investments from large enterprises upgrading legacy infrastructure to energy-efficient facilities. Regulatory requirements such as GDPR, HIPAA, and data sovereignty rules continue to favor private data center deployments over fully cloud-based models.

Cloud Service Data Centers represent 27.0% of the market in 2025, underpinned by major hyperscaler expansion programs. AWS, Azure, and Google Cloud continue to invest tens of billions annually in data center expansion, driven by AI and cloud demand, with multiple large-scale projects announced globally in 2024. Colocation Data Centers hold 18.0%, growing due to enterprise hybrid IT adoption, while Managed Service Data Centers account for the remaining 14.0%.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

Major Companies |

|

North America |

39.0% |

Hyperscale investment, IRA green incentives, cloud-native expansion, AI infrastructure |

AWS, Microsoft, Google, Equinix, Digital Realty |

|

Asia Pacific |

30.0% |

India digitalization, China data center policy, ASEAN cloud growth, 5G expansion |

Alibaba Cloud, Tata Communications, NTT, Telstra |

|

Europe |

20.0% |

EU Green Deal, energy efficiency regulations, RE100 memberships, GDPR compliance |

Equinix, Iron Mountain, OVHcloud, Deutsche Telekom |

|

Latin America |

6.0% |

Brazil cloud adoption, financial sector digitalization, regional hyperscaler buildout |

Ascenty, Equinix, Lumen, Claro |

|

Middle East & Africa |

5.0% |

Saudi Vision 2030, UAE Smart Nation, sovereign cloud initiatives, oil sector digitalization |

G42, Khazna Data Centers, Equinix |

North America commands a 39.0% global revenue share in 2025, driven by strong investment in green data center infrastructure. The United States leads globally, with Northern Virginia—the world’s largest data center market—exceeding 4,000 MW of operational capacity, with increasing focus on renewable energy integration. The Inflation Reduction Act further accelerates clean energy adoption across new and existing facilities.

Asia Pacific holds a 30.0% share in 2025, and is the fastest-growing region, driven by strong investments in sustainable data center infrastructure across India and China, along with Singapore’s regulated expansion. Europe, at 20.0%, is supported by strict energy efficiency regulations such as the Energy Efficiency Directive, which mandates energy performance reporting and efficiency improvements for data centers above 500 kW.

Competitive Landscape

|

Company Name |

Key Brand / Platform |

Market Position |

Core Strength |

|

Equinix, Inc. |

Equinix IBX® / xScale® |

Leader |

Global colocation, interconnection, green energy sourcing |

|

Digital Realty Trust |

Digital Realty / PlatformDIGITAL® |

Leader |

Hyperscale colocation, sustainability-first design |

|

Amazon Web Services, Inc. |

AWS |

Leader |

Public cloud, renewable energy procurement, custom silicon |

|

Microsoft Corporation |

Azure / Microsoft Datacenters |

Leader |

Carbon-negative commitments, AI infrastructure, liquid cooling |

|

Google LLC |

Google Cloud |

Leader |

24/7 CFE leadership, DeepMind AI cooling, global PPA scale |

|

NTT, Inc. |

NTT Global Data Centers |

Challenger |

Asia Pacific leadership, green certifications, carrier-neutral |

The green data center market is driven by hyperscale cloud operators and colocation providers. Equinix, Inc., with 260+ data centers across 33 countries and over USD 8 billion revenue (2023), is a leading colocation player, while hyperscalers collectively guide over USD 300 billion in annual capex (2025), with strong focus on energy-efficient data center development.

Key Company Profiles

Equinix, Inc.

Equinix, headquartered in Redwood City, is a leading global digital infrastructure company operating 260+ data centers across 30+ countries. It generated about USD 8.7 billion revenue in 2024, serving enterprises, cloud providers, and networks via its interconnection-focused platform.

- Product & Service Portfolio: Equinix offers IBX colocation data centers, xScale hyperscale facilities, Equinix Fabric interconnection, Network Edge virtual networking, and Equinix Metal bare-metal infrastructure services enabling secure, scalable digital ecosystems globally.

- Recent Developments: In 2025, Equinix, Inc. announced multiple agreements to deploy advanced nuclear energy and fuel cell technologies, securing over 1 GW of clean power capacity to support sustainable, AI-ready data center operations globally. In 2024, Equinix, Inc. signed a 151 MW renewable energy PPA in Australia (Golden Plains Wind Farm) to accelerate its transition toward 100% clean energy operations.

- Strategic Focus: Equinix focuses on scaling sustainable digital infrastructure through renewable energy procurement, energy-efficient operations, hyperscale expansion (xScale), and interconnection-driven ecosystems to support AI, cloud, and global enterprise workloads.

Digital Realty Trust, Inc.

Digital Realty, headquartered in Austin, Texas, is a leading global data center REIT operating 300+ facilities across 55+ metropolitan areas. The company reported approximately USD 5.5 billion revenue in 2023, delivering scalable, interconnected infrastructure through its PlatformDIGITAL ecosystem worldwide.

- Product & Service Portfolio: Digital Realty provides hyperscale and colocation data centers, powered shell solutions, and interconnection services via ServiceFabric under PlatformDIGITAL, enabling hybrid IT deployments across global campuses.

- Recent Developments: In 2024, Digital Realty Trust, Inc. and Blackstone announced a USD 7 billion joint venture to develop hyperscale data center campuses, with transactions expected to close in phases during 2024. In 2025FY, Digital Realty Trust, Inc. strengthened its clean energy strategy, achieving 100% renewable energy coverage across its European portfolio and North American colocation operations, while reaching 75% renewable electricity globally.

- Strategic Focus: Digital Realty focuses on scaling sustainable hyperscale campuses through renewable energy sourcing, PlatformDIGITAL ecosystem expansion, and global interconnection capabilities to support hybrid cloud, AI, and enterprise workloads.

Microsoft Corporation

Microsoft, headquartered in Redmond, operates one of the world’s largest cloud platforms, Azure, spanning 60+ regions globally. The company generated over USD 137.5 billion in Intelligent Cloud revenue in FY2024, driven by AI infrastructure expansion and hyperscale data center investments.

- Product & Service Portfolio: Microsoft offers Azure public cloud, Azure Stack hybrid solutions, hyperscale data center infrastructure, and sustainability tools such as the Microsoft Cloud for Sustainability and Emissions Impact Dashboard for carbon tracking.

- Recent Developments: In 2025, Microsoft Corporation accelerated global AI-ready data center expansion, committing approximately USD 80 billion in FY2025 toward hyperscale infrastructure, including advanced cooling technologies to support high-density AI workloads. In 2026, Microsoft Corporation expanded its renewable energy strategy, achieving 100% renewable electricity matching for operations by 2025, while continuing to scale carbon-free energy procurement toward its 2030 goals.

- Strategic Focus: Microsoft focuses on scaling AI-driven cloud infrastructure with renewable energy, 24/7 carbon-free power, and advanced cooling technologies to achieve carbon-negative, water-positive, and zero-waste data center operations globally.

Market Concentration Analysis

The global green data center market exhibits a moderately concentrated structure at the hyperscale tier, with the top five operators – AWS, Microsoft Azure, Google Cloud, Equinix, and Digital Realty – accounting for approximately 35–40% of global revenue in 2025. Their combined data center investment programs represent a multi-hundred-billion-dollar pipeline, reinforcing their dominant market positions through 2034.

Market fragmentation is high across colocation, managed services, and regional operators, with numerous players serving enterprise and government clients globally. However, rising green certification standards and capital intensity are increasing entry barriers, especially for smaller data centre operators.

Consolidation is accelerating, highlighted by Digital Realty’s USD 3.5 billion Teraco acquisition and Equinix’s xScale expansion strategy. Rising ESG requirements, renewable energy scale advantages, and AI-driven demand are pushing smaller regional operators toward consolidation or acquisition.

Investment & Growth Opportunities

Fastest-Growing Segments

AI-driven infrastructure is among the fastest-growing themes in green data centers, as generative AI workloads require high-density GPU clusters and advanced cooling (including liquid cooling) with greater energy efficiency. NVIDIA reported data center revenue of over USD 47 billion in FY2024, reflecting strong AI-led demand for energy-intensive infrastructure.

The Cloud Service Data Centers at 27.0% in 2025 continue to expand as hyperscalers scale investments globally. New facilities increasingly integrate renewable energy sourcing, efficient cooling, and low-PUE designs as standard requirements, supporting sustained demand for green technologies.

Emerging Market Expansion

Asia Pacific is the fastest-growing region, driven by strong digital adoption and hyperscaler expansion. India is expected to significantly expand its data center capacity by 2027, supported by rising internet usage and large-scale investments from global cloud players.

The Middle East is emerging as a key growth hub, led by initiatives such as NEOM under Saudi Vision 2030 and AI-focused infrastructure in Abu Dhabi. High solar energy availability supports renewable-powered data center development.

Venture & Strategic Investment Trends

Investment in green data center technologies is accelerating, particularly in liquid cooling, energy optimization, and circular infrastructure solutions. Companies such as Submer, LiquidStack, and Green Revolution Cooling have secured significant funding in recent years, reflecting growing demand for efficient cooling solutions in high-density environments.

Future Market Outlook (2026-2034)

The global green data center market is projected to reach USD 541.2 billion by 2034, from USD 122.6 billion in 2025, advancing at a CAGR of 17.04%. Growth will be driven by AI infrastructure expansion, renewable energy integration maturation, and mandatory green compliance frameworks adopted across major economies. The transition from optional sustainability to regulatory mandate – evidenced by EU EED requirements effective in 2024 – is creating structural, non-cyclical demand.

Technological shifts such as liquid immersion cooling, on-site renewable energy integration, and AI-driven data center management are expected to significantly improve efficiency and sustainability. Industry benchmarks show average Power Usage Effectiveness (PUE) levels around ~1.5 globally, while leading hyperscale operators are already achieving near 1.1 or lower in advanced facilities; further reductions will depend on cooling and power innovations rather than a fixed universal target.

Industry transformation will converge around three key themes: AI-native infrastructure design requiring purpose-built thermal and power systems; energy sovereignty through on-site renewable generation and storage; and circular economy adoption mandated by EU WEEE regulations and corporate ESG reporting requirements. Operators investing early in liquid cooling, renewable procurement, and AI-driven operations will hold the strongest competitive positioning through 2034.

Research Methodology

Primary Research

IMARC Group's primary research involves direct engagements with data center operators, technology providers, energy consultants, and enterprise IT decision-makers. Structured interviews and surveys were conducted across North America, Europe, Asia Pacific, and the Middle East to capture market sizing insights, technology adoption trends, and competitive intelligence supporting this report.

Secondary Research

Secondary research drew on publicly available sources including company annual reports (Equinix, Digital Realty, AWS, Microsoft, Google), regulatory filings, government infrastructure policy documents, industry association publications (Uptime Institute, Green Grid, Data Centre Alliance), and third-party market databases. Market data was triangulated across multiple independent sources to ensure accuracy.

Forecasting Models

IMARC's proprietary bottom-up and top-down forecasting models were applied to generate the 2026–2034 market projections. The bottom-up approach aggregates segment-level demand across component, data center type, and regional dimensions, cross-validated against top-down macroeconomic and industry-level growth drivers. Sensitivity analysis was conducted to test forecast robustness under varying technology adoption and regulatory scenarios.

Green Data Center Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Components Covered |

|

| Data Center Types Covered | Colocation Data Centers, Managed Service Data Centers, Cloud Service Data Centers, Enterprise Data Centers |

| Industry Verticals Covered | Healthcare, BFSI, Government, Telecom and IT, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Equinix, Inc., Digital Realty Trust, Amazon Web Services, Inc., Microsoft Corporation, Google LLC, and NTT, Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the green data center market from 2020-2034.

- The green data center market research report provides the latest information on the market drivers, challenges, and opportunities in the global market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the green data center industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Green Data Center Market Report

The global green data center market was valued at USD 122.6 Billion in 2025. It is projected to reach USD 541.2 Billion by 2034, growing at a CAGR of 17.04% during 2026-2034.

The green data center market is projected to grow at a CAGR of 17.04% from 2026 to 2034, driven by cloud expansion, AI infrastructure demand, and corporate sustainability mandates.

North America leads with a 39.0% market share in 2025, anchored by U.S. hyperscale cloud investments. Asia Pacific is the fastest-growing region, driven by India, China, and Southeast Asia digitalization.

The Solutions segment dominates with a 65.0% share in 2025, driven by energy-efficient hardware investments including power systems, servers, and advanced cooling infrastructure at hyperscale and enterprise facilities.

Enterprise Data Centers hold the largest share at 41.0% in 2025, driven by large organizations replacing legacy on-premise infrastructure with modern, energy-efficient facilities while maintaining data sovereignty compliance.

Key drivers include surging cloud and AI computing demand, corporate net-zero commitments, rising energy costs, government incentives like the U.S. IRA, and mandatory energy efficiency regulations across the EU and Asia Pacific.

Leading companies include Equinix, Inc., Digital Realty Trust, Amazon Web Services, Inc., Microsoft Corporation, Google LLC, and NTT, Inc., collectively representing the largest revenue share globally.

Key technologies include liquid cooling systems, AI-powered energy management, on-site renewable energy generation, modular prefabricated designs, and software-defined infrastructure improving hardware utilization significantly.

Major challenges include high capital expenditure for retrofits, skilled workforce shortages, renewable energy intermittency, water usage from evaporative cooling, and complexity of multi-standard green certification across geographies.

High-opportunity areas include AI infrastructure liquid cooling, Asia Pacific emerging market expansion, modular edge data centers, renewable energy storage integration, and circular economy hardware management platforms.

By 2034, the market will reach USD 541.2 Billion, dominated by AI-native liquid-cooled facilities, 100% renewable-powered operations, autonomous AI-managed infrastructure, and circular economy hardware programs across all major regions.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade