Heating Equipment Market Size, Share, Trends and Forecast by Product, Application, and Region, 2026-2034

Heating Equipment Market Size and Share:

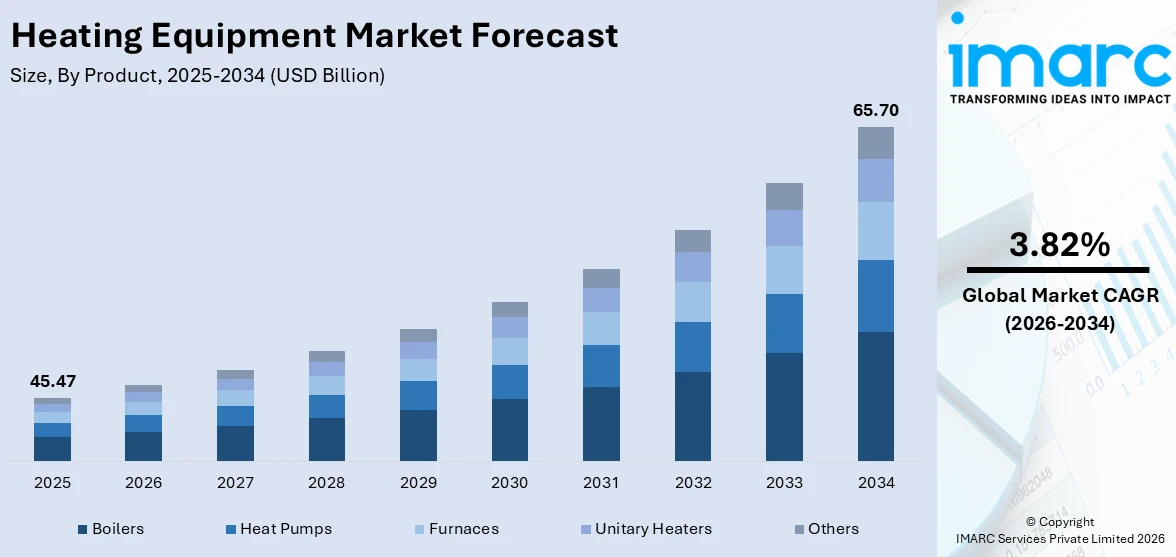

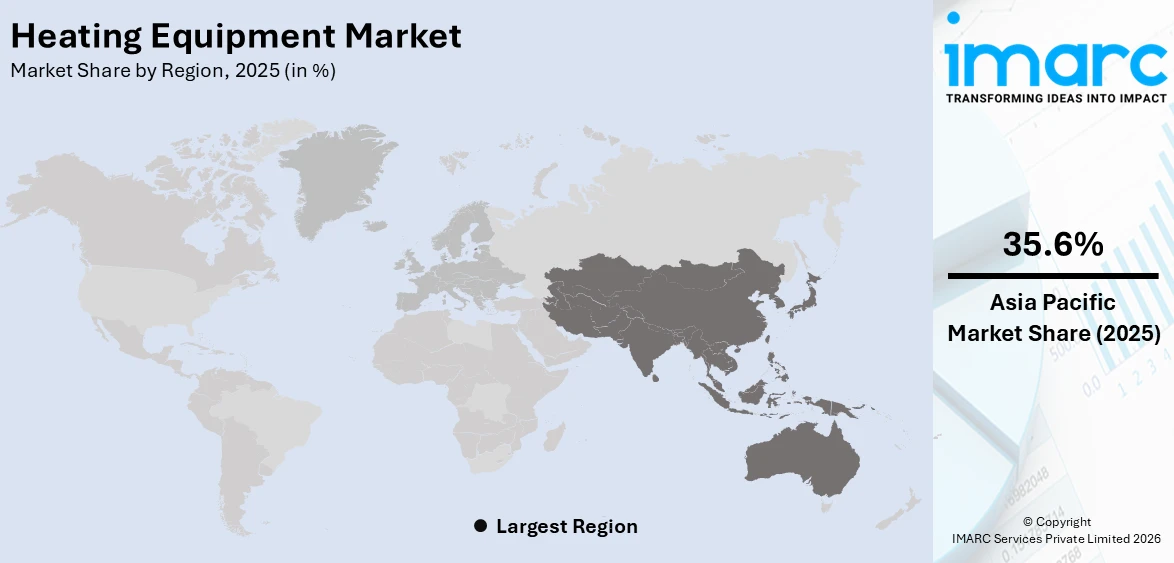

The global heating equipment market size was valued at USD 45.47 Billion in 2025. Looking forward, IMARC Group estimates the market to reach USD 65.70 Billion by 2034, exhibiting a CAGR of 3.82% from 2026-2034. Asia-Pacific currently dominates the market, holding a market share of 35.6% in 2025. The region commands a leading position due to its extensive industrial base, large-scale residential and commercial construction activity, strong government-backed clean heating initiatives, and high demand for energy-efficient systems across both emerging and developed economies, collectively reinforcing the region’s commanding heating equipment market share.

The global heating equipment market is driven by multiple converging factors that are reshaping the demand landscape across residential, commercial, and industrial segments. Growing emphasis on energy efficiency and decarbonization is compelling governments worldwide to introduce stricter building performance standards, which in turn encourage the replacement of outdated, fossil-fuel-based heating systems with advanced low-emission alternatives. The rapid expansion of urban infrastructure in emerging economies across Asia-Pacific and Latin America is creating sustained demand for new heating installations. Furthermore, rising awareness of indoor thermal comfort and air quality among consumers is accelerating adoption of modern, technologically advanced heating solutions. The integration of smart controls, programmable thermostats, and remote monitoring capabilities is also broadening consumer appeal. Additionally, the growing adoption of renewable energy in district heating equipment market growth is enabling municipalities to transition away from centralized fossil fuel systems, while robust investment in hospitality, healthcare, and educational facility construction continues to generate strong institutional demand for heating solutions globally.

The United States has emerged as a major region in the heating equipment market owing to many factors. Stringent federal and state-level energy efficiency mandates are accelerating the transition from conventional gas furnaces to advanced heat pump systems across both new and existing residential and commercial buildings. Extensive retrofit programs supported through the Inflation Reduction Act provide homeowners and building owners with substantial financial incentives to upgrade outdated heating infrastructure, making advanced equipment more accessible. Rising energy costs are also driving consumers to seek high-efficiency systems that deliver lower operating expenses over the long term. Additionally, extreme weather variability across many parts of the country underscores the need for reliable and high-capacity heating solutions. For instance, in September 2025, Valtris Specialty Chemicals and the Transfar Group announced new progress in their ongoing collaboration. Following the April 2024 announcement of Valtris granting an exclusive technology license to Transfar Huayang for phenol-free over-based barium stabilizers, both companies have made steady advancements in introducing this technology to the Asian market.

To get more information on this market Request Sample

Heating Equipment Market Trends:

Rising Adoption of Heat Pump Technology

The widespread shift toward heat pump adoption is among the most significant developments reshaping the global heating equipment landscape. Heat pumps deliver superior energy efficiency by transferring thermal energy from ambient air, ground, or water sources rather than generating heat through combustion, making them far more sustainable than conventional systems. Government-backed incentive programs, particularly across North America and Europe, have substantially reduced the upfront cost burden for residential and commercial users, triggering a surge in installations. The ability of modern cold-climate heat pumps to operate reliably in sub-zero temperatures has expanded the viable geography for adoption beyond historically mild climates. Inverter-driven compressor technology has further enhanced seasonal performance and reduced electricity consumption throughout the heating cycle. In the United States, heat pump sales rose by 15% overall in 2025, with a 30% surge recorded in the second half of the year, according to the International Energy Agency, reflecting accelerating consumer and contractor interest driven by evolving technology standards and growing energy cost pressures for residential and commercial building owners.

Integration of Smart and IoT-Enabled Heating Systems

The integration of Internet of Things connectivity, artificial intelligence, and building automation systems is fundamentally transforming how heating equipment is monitored, controlled, and maintained. Smart thermostats, predictive maintenance sensors, and AI-driven energy optimization algorithms are enabling building operators and homeowners to achieve granular control over heating performance while reducing wasteful energy expenditure. Building automation systems that interface directly with heating equipment now allow real-time diagnostics, remote fault detection, and automated scheduling based on occupancy and weather data. This digitalization trend is strengthening the heating equipment market outlook, as end users increasingly seek intelligent solutions that combine operational convenience with measurable energy savings. Advanced implementations incorporating digital twin technology are enabling facility managers to simulate and optimize heating performance under different operating scenarios, extending equipment lifespan and reducing unplanned downtime. According to a 2025 research publication in the journal Machines, IoT-managed heating systems demonstrated significant reductions in operational energy expenditure versus conventional central heating configurations, validating the commercial and environmental case for smart heating integration across residential and non-residential building categories.

Strengthening of Energy Efficiency Regulations and Green Standards

Evolving regulatory frameworks across major markets are establishing increasingly stringent energy performance requirements for heating systems, compelling manufacturers to accelerate product innovation and investment in next-generation low-emission technologies. The European Union’s revised Energy Performance of Buildings Directive mandates member states to achieve a collective 11.7% reduction in energy consumption by 2030, with heating and cooling systems at the center of these targets. Fossil-fuel-based stand-alone boilers lost subsidy eligibility across EU markets from January 2025, redirecting consumer and contractor preference toward hybrid and fully electric alternatives. The growing body of minimum efficiency standards, carbon pricing mechanisms, and building codes that specify near-zero energy performance is making compliance a central factor in the purchasing and specification process. These dynamics are expected to positively shape the long-term heating equipment market forecast, as regulators continue to tighten standards. In the United Kingdom, the December 2024 Department for Energy Security and Net Zero consultation proposed updated ecodesign and energy labeling legislation for space and combination heaters, aimed at improving efficiency standards, reducing carbon emissions, and lowering consumer energy bills across the residential building stock.

Heating Equipment Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global heating equipment market, along with forecast at the global, regional, and country levels from 2026-2034. The market has been categorized based on product and application.

Analysis by Product:

- Heat Pumps

- Furnaces

- Boilers

- Unitary Heaters

- Others

Boilers holds 35.4% of the market share. Boilers serve as enclosed pressurized vessels that generate hot water or steam for distribution across space heating and process applications in residential, commercial, and industrial settings. Their versatility across diverse fuel types, including natural gas, oil, biomass, and electricity, makes them adaptable to a broad range of building configurations and regional energy contexts. Condensing boilers capture additional heat from exhaust gases, improving energy efficiency compared to conventional systems. As a result, they are increasingly favored for both new heating system installations and the replacement of older boiler units in regulated markets. The integration of IoT connectivity and smart controls has elevated boiler performance further, allowing remote diagnostics, automated load balancing, and real-time efficiency monitoring. Commercial and industrial users continue to specify boilers for large-scale applications such as district heating networks, process heating, and institutional facilities due to their ability to deliver high-capacity, consistent thermal output. Evolving heating equipment market trends reflect a parallel shift toward hydrogen-ready boiler designs as part of broader decarbonization strategies. The global residential boiler market size was valued at USD 8.93 Billion in 2024. Looking forward, IMARC Group estimates the market to reach USD 13.28 Billion by 2033, exhibiting a CAGR of 4.28% during 2025-2033, supported by strict carbon-reduction regulations and increasing demand for high-efficiency condensing units across urban and suburban settings.

Analysis by Application:

Access the comprehensive market breakdown Request Sample

- Residential

- Commercial

- Industrial

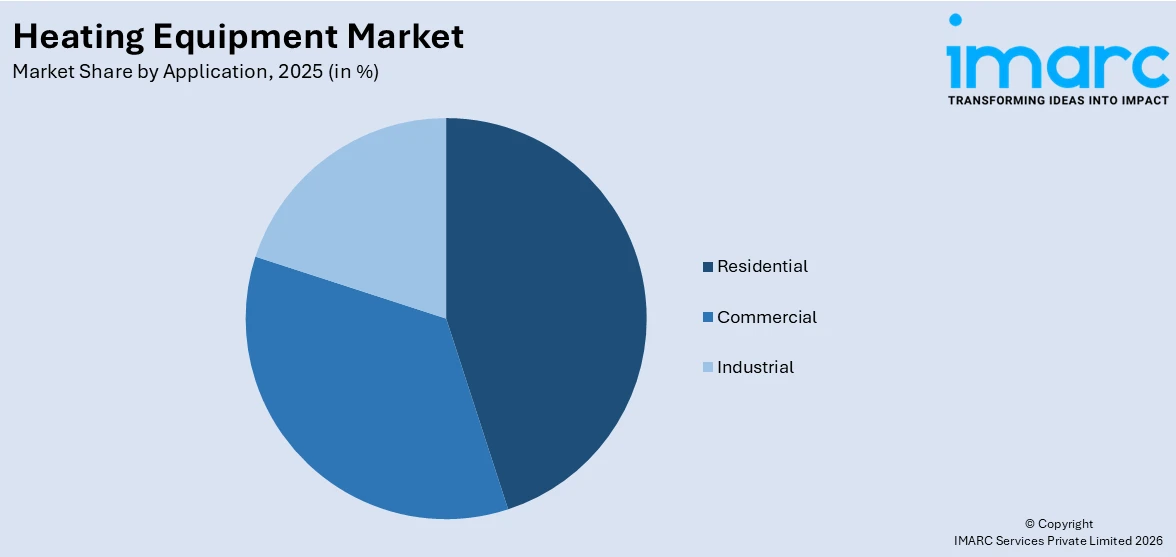

Residential leads the market with a share of 44.8%. The residential segment encompasses all space heating and hot water systems installed in single-family homes, apartments, and multi-family complexes, making it the foundational demand driver across all global regions. Homeowners are consistently the most numerous and price-sensitive end users, and they increasingly prioritize solutions that reduce recurring energy expenditure without sacrificing thermal comfort. Growing urbanization is expanding the pool of residential heating consumers, particularly in Asia-Pacific and Latin America, where rising incomes are enabling households to invest in dedicated heating systems for the first time. The replacement cycle for aging heating equipment in mature markets such as North America and Europe also generates a stable, recurring source of residential demand independent of new construction trends. Government incentive programs such as tax credits, subsidies, and rebates are encouraging homeowners to upgrade residential climate control systems. As a result, heat pumps are gaining popularity due to their ability to provide both heating and cooling, reflecting growing demand for energy-efficient and multifunctional home comfort solutions.

Regional Analysis:

To get more information on the regional analysis of this market Request Sample

- North America

- United States

- Canada

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

Asia-Pacific, accounting for 35.6% of the share, enjoys the leading position in the market. The region’s dominance is underpinned by its expansive industrial base, rapid urbanization in markets such as China, India, Indonesia, and Vietnam, and significant government investment in clean energy and energy-efficient building infrastructure. China’s Clean Heating Plan and dual-carbon strategy have redirected household and district heating investment toward heat pumps and other low-emission systems, generating sustained replacement and new installation demand. Industrial expansion across the region, particularly in chemical processing, food production, and manufacturing, sustains robust demand for high-capacity boiler and furnace installations. Japan’s focus on hydrogen-compatible heat pump systems and South Korea’s extension of green heating incentives in 2024 to cover district heating upgrades and residential heat pumps have further reinforced regional demand. Strong manufacturing competitiveness across major economies keeps system costs attractive for domestic buyers. For instance, in March 2025, Global manufacturer Gulbrandsen, recognized for its expertise in specialty polyethylene waxes and polymers, announced plans to expand its operations by adding new polyethylene wax production capacity and establishing a functional polymers facility at its Dahej, India site.

Key Regional Takeaways:

North America Heating Equipment Market Analysis

North America represents one of the most technologically advanced and policy-driven regional markets for heating equipment globally. A sustained focus on decarbonizing the building stock has placed heat pumps and high-efficiency furnaces at the center of both residential retrofit activity and new commercial construction projects. The Inflation Reduction Act has included some substantial financial incentives that lower the effective cost of installing heat pumps in millions of households and owners of small commercial buildings, triggering a transition away from natural gas and oil heating and cooling. The Greener Homes Initiative in Canada has also given retrofit grant funding for the use of heat pumps and low-NOx gas furnaces, especially in Ontario and British Columbia, where homeowners are replacing old baseboard heaters and oil heaters with new ones. The historical consumer hesitation in the north and in the provinces due to cold climate has been solved through improvements in the performance of cold climate heat pump models in next-generation models, increasing the market that could be addressed significantly. The commercial and institutional buildings are also hastening to move towards the advanced radiant heating and programmable boiler controls to maximize the cost of operation. For instance, in February 2024, the Canadian federal government rolled out new rebates under the Canada Greener Homes Initiative, specifically targeting residential retrofits with energy-efficient heat pumps, driving a measurable surge in upgrade activity across major provinces.

United States Heating Equipment Market Analysis

The United States holds 83.20% of the market share in North America. The US heating equipment market is shaped by a combination of strict regulatory standards, strong consumer preference for technologically advanced systems, and an extensive network of professional installation contractors capable of deploying complex, multi-component heating solutions. The federal government’s commitment to building decarbonization, reinforced through tax credit programs and energy efficiency benchmarks under the Inflation Reduction Act, has spurred unprecedented investment in heat pump and hybrid heating system adoption across both single-family and multi-family residential buildings. Commercial building owners, guided by evolving ASHRAE standards and local building codes, are increasingly specifying low-emission heating solutions for new construction and major renovations. The industrial sector continues to demand high-output steam and hot water boiler systems for process applications, particularly in food processing, chemical manufacturing, and healthcare facilities. For instance, in September 2025, Lennox became the first manufacturer to complete U.S. Department of Energy laboratory validation for a commercial cold climate heat pump rooftop unit in the 15-25 ton category, setting a new benchmark for performance in large commercial heating applications and reinforcing U.S. leadership in heat pump technology advancement.

Europe Heating Equipment Market Analysis

Europe is a mature yet dynamically evolving market for heating equipment, driven by the world’s most ambitious regulatory framework for building energy performance and decarbonization. The EU Energy Performance of Buildings Directive mandates member states to renovate their most energy-inefficient building stock progressively, while removing subsidies for standalone fossil fuel boilers from January 2025. Germany has expanded its BEG subsidy program to cover up to 70% of heat pump installation costs for qualifying residential upgrades, while the United Kingdom is strengthening its Boiler Upgrade Scheme to incentivize heat pump adoption alongside planned restrictions on combustion heating systems. France, Italy, and Spain are implementing building renovation programs aligned with the EU Renovation Wave strategy. The transition from gas and oil boilers to heat pump systems is accelerating across Northern and Western European markets, where installer capacity and consumer awareness are highest. District heating networks are also being expanded and decarbonized across Nordic and Central European countries. In June 2025, the European Commission adopted a support package offering practical guidance to help EU countries implement the revised Energy Performance of Buildings Directive, reinforcing the regulatory pressure that is driving sustained demand for energy-efficient heating systems throughout the continent.

Asia-Pacific Heating Equipment Market Analysis

Asia-Pacific is the world’s largest and fastest-growing regional market for heating equipment, underpinned by robust industrial demand, large-scale urbanization, and expanding government investment in clean and energy-efficient heating infrastructure. China’s coal-to-clean heating transition under its dual-carbon policy framework is generating substantial demand for heat pumps and district heating upgrades across northern provinces. India’s growing manufacturing sector and the construction of new hospitals, educational institutions, and commercial complexes continue to drive boiler and furnace installations. Japan’s expertise in advanced heat pump technology and South Korea’s green heating incentive programs contribute further to regional innovation and market depth. In 2024, the World Bank authorized a USD 300 million loan to support renewable and low-carbon heating in China’s Shaanxi province, aiming to cut emissions and advance carbon neutrality goals, underscoring the scale of public investment flowing into modernized heating infrastructure across the region.

Latin America Heating Equipment Market Analysis

Latin America’s heating equipment market is gaining momentum as rising living standards, expanding urbanization, and growing investment in tourism and hospitality infrastructure fuel demand for modern thermal comfort solutions. High-altitude cities in Colombia, Peru, Argentina, and Chile present particularly strong requirements for residential and commercial heating equipment due to persistently cold climatic conditions. Industrial demand for boilers and furnaces in food processing, chemical manufacturing, and agricultural product handling also supports market activity. Government efforts to improve energy efficiency in public buildings and promote renewable heating technologies are beginning to create a more favorable investment climate. For instance, in January 2025, Argentina’s Ministry of Tourism, Environment, and Sport announced plans to open 70 new hotels across the country, signaling substantial upcoming demand for commercial heating equipment installations.

Middle East and Africa Heating Equipment Market Analysis

The Middle East and Africa heating equipment market is primarily driven by large-scale commercial and industrial construction activity, particularly across GCC nations implementing ambitious infrastructure development agendas. Saudi Arabia’s Vision 2030 program and associated hotel, hospitality, and mixed-use developments are generating significant demand for heating systems in commercial facilities. Industrial heating applications in chemical plants, petroleum processing, and manufacturing support sustained boiler and furnace demand. Improving living standards in sub-Saharan African markets are gradually expanding residential heating equipment penetration. For instance, in 2024, the Middle East’s total energy investment reached USD 175 billion, with clean energy accounting for approximately 15% of the total, according to the World Energy Investment 2024 report, reflecting the growing emphasis on efficient and low-emission heating infrastructure across the region.

Competitive Landscape:

The global heating equipment market is characterized by intense competition among established multinational corporations, regionally dominant players, and a growing cohort of technology-focused entrants. Key participants are investing heavily in research and development (R&D) to develop next-generation heat pump systems, hydrogen-compatible boilers, and IoT-enabled heating controls that comply with tightening efficiency regulations. Strategic acquisitions have reshaped the competitive landscape, with major players expanding their geographic footprint and product breadth. Companies are also competing on smart connectivity, after-sales service quality, and installer network strength. Product differentiation through cold-climate performance, low-GWP refrigerant compatibility, and seamless integration with building automation systems has become a critical competitive dimension. Pricing pressures from lower-cost Asian manufacturers are compelling Western incumbents to pursue operational efficiencies and premium product positioning. Sustainability credentials, including third-party energy efficiency certifications and carbon footprint disclosures, are increasingly influencing procurement decisions in European and North American institutional markets. The report provides a comprehensive analysis of the competitive landscape in the heating equipment market with detailed profiles of all major companies, including:

- Daikin Industries Ltd.

- Emerson Electric Co.

- Honeywell International Inc.

- Johnson Controls

- Lennox International Inc.

- Mitsubishi Electric Corporation

- Panasonic Corporation

- Robert Bosch GmbH

- Schneider Electric SE

- Siemens AG

- The Danfoss Group

Latest News and Developments:

- In January 2026, Daikin Applied Americas and Daikin Comfort Technologies unveiled a range of high-performance HVAC innovations at the AHR Expo in Las Vegas, including the FIT AURORA Cold Climate Residential Heat Pump featuring low-GWP R-32 refrigerant and next-generation VRV systems with cloud-connected HERO Cloud Services. The product launches build on Daikin Applied’s USD 163 million investment in a new 71,000-square-foot research and development (R&D) test lab at its Plymouth, Minnesota headquarters, announced in December 2025, designed to accelerate HVAC innovation for data centers and advanced commercial applications.

- In August 2025, Robert Bosch GmbH completed its USD 8 billion acquisition of the residential and light commercial HVAC business from Johnson Controls, along with 100% of the Johnson Controls-Hitachi Air Conditioning joint venture including Hitachi’s 40% stake. The transaction, the largest in Bosch history, nearly doubled the size of Bosch Home Comfort Group to over 25,000 associates and added manufacturing facilities in Norman, Oklahoma and Wichita, Kansas, significantly strengthening the company’s presence in the Americas and Asia-Pacific heating equipment markets.

Heating Equipment Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered | Heat Pumps, Furnaces, Boilers, Unitary Heaters, Others |

| Applications Covered | Residential, Commercial, Industrial |

| Regions Covered | North America, Asia-Pacific, Europe, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, China, Japan, India, South Korea, Australia, Indonesia, Germany, France, United Kingdom, Italy, Spain, Russia, Brazil, Mexico, Others |

| Companies Covered | Daikin Industries Ltd., Emerson Electric Co., Honeywell International Inc., Johnson Controls, Lennox International Inc., Mitsubishi Electric Corporation, Panasonic Corporation, Robert Bosch GmbH, Schneider Electric SE, Siemens AG, The Danfoss Group, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the heating equipment market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global heating equipment market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter’s Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the heating equipment industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Heating Equipment Market Report

The heating equipment market was valued at USD 45.47 Billion in 2025.

The heating equipment market is projected to exhibit a CAGR of 3.82% during 2026-2034, reaching a value of USD 65.70 Billion by 2034.

The heating equipment market is driven by increasing demand for energy-efficient heating systems amid stricter building energy codes, rapid urbanization expanding residential and commercial construction, government incentive programs promoting low-emission heating technologies, integration of smart controls and IoT-enabled diagnostics, and the transition from fossil-fuel-based systems to advanced heat pump and hybrid heating solutions across global markets.

Asia-Pacific currently dominates the heating equipment market, accounting for a share of 35.6%. The region benefits from extensive industrial demand, rapid urbanization, government-backed clean heating programs, and strong manufacturing competitiveness, all of which support continued investment in residential, commercial, and industrial heating equipment installation and upgrades.

Some of the major players in the heating equipment market include Daikin Industries Ltd., Emerson Electric Co., Honeywell International Inc., Johnson Controls, Lennox International Inc., Mitsubishi Electric Corporation, Panasonic Corporation, Robert Bosch GmbH, Schneider Electric SE, Siemens AG, The Danfoss Group, etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)