Heavy Construction Equipment Market Report by Equipment Type (Earthmoving Equipment, Material Handling Equipment, Heavy Construction Vehicles, and Others), End User (Infrastructure, Construction, Mining, Oil and Gas, Manufacturing, and Others), and Region 2026-2034

Heavy Construction Equipment Market Size:

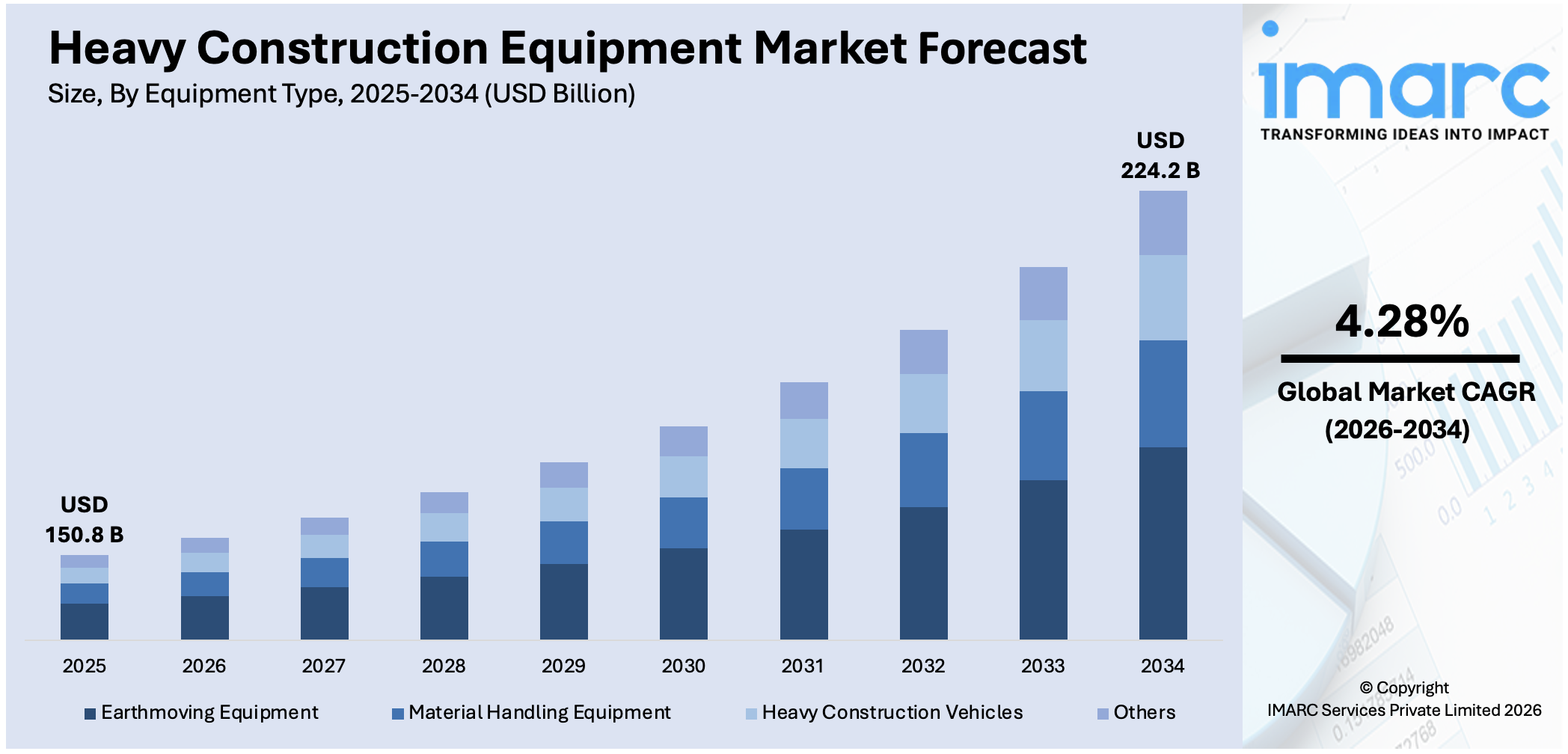

The global heavy construction equipment market size reached USD 150.8 Billion in 2025. Looking forward, IMARC Group expects the market to reach USD 224.2 Billion by 2034, exhibiting a growth rate (CAGR) of 4.28% during 2026-2034. Asia-Pacific currently dominates the heavy construction equipment market globally due to the presence of substantial infrastructure development in nations such as China and India. Infrastructure development projects, technological advancements, government regulations regarding emissions and safety standards, the trend towards rental services, adoption of renewable energy projects, recovery of the construction industry, and expansion of mining activities contribute to market growth.

Market Size & Forecasts:

- Heavy construction equipment market was valued at USD 150.8 Billion in 2025.

- The market is projected to reach USD 224.2 Billion by 2034, at a CAGR of 4.28% from 2026-2034.

Dominant Segments:

- Equipment Type: Earthmoving equipment represents the leading market segment driven by several key factors that shape its dynamics, such as the increasing demand for infrastructure development projects worldwide drives the need for earthmoving equipment.

- Region: Asia Pacific leads the market, driven by the increasing urbanization and infrastructure development projects, which serve as key factors propelling the demand for heavy construction equipment.

Key Players:

- The leading companies in the market include AB Volvo, Caterpillar Inc, CNH Industrial N.V., Deere & Company, HD Hyundai Infracore, Hitachi Construction Machinery Co., Ltd., J C Bamford Excavators Ltd., Komatsu Ltd, Liebherr Group, SANY Group, Terex Corporation, XCMG Group, etc.

Key Drivers of Market Growth:

- Infrastructure Development: Fast-growing urbanization in emerging economies and high investments in global infrastructure projects are driving the demand for heavy construction equipment, especially in developing economies.

- Technological Advancements: Automation, telematics, and electric drive machinery are enhancing the productivity, safety, and eco-friendliness of heavy construction equipment, leading to adoption across all construction markets.

- Government Investments: Governments are spending large amounts of money on public infrastructure projects, such as roads, bridges, and smart city initiatives, which indirectly drive the need for heavy construction equipment.

- Increased Construction Activities: Increased demand for residential, commercial, and industrial buildings and large-scale infrastructure works is driving the demand for heavy construction machinery.

- Environmental Regulations: Tighter environmental rules and emission standards are pushing the innovation of cleaner, fuel-efficient equipment, which is promoting a move towards greener options for construction fleets.

Future Outlook:

- Strong Growth Outlook: The heavy construction equipment industry is expected to experience steady growth with growing demand from infrastructure development, urbanization, and technology upgrades in the sector.

- Market Evolution: The market will spread to new regions geographically, with huge growth experienced in developing nations where the development of infrastructure remains a priority.

The market for heavy construction equipment is going through a dynamic evolution, with some notable trends and drivers governing its growth pattern. Safety is a top priority in the construction sector and is promoting the use of more sophisticated heavy equipment with inherent safety features. Facing regulatory demands and the need to safeguard workers, manufacturers are adding features like collision avoidance systems, improved operator visibility, and sophisticated monitoring systems to their equipment. These technologies are minimizing accidents, enhancing worker safety, and optimizing the general efficiency of construction processes. In addition, more stringent regulatory systems are forcing construction firms to adhere to safety and environmental regulations. For instance, safety standards can mandate that the use of equipment with safety sensors or automated shutdown procedures be adopted by operators to minimize accidents. These standards are assisting in spurring demand for safe machines in the industry that can pass regulatory requirements, thus making construction companies fulfil legal requirements while having top-notch safety measures on-site.

To get more information on this market Request Sample

Heavy Construction Equipment Market Trends:

Growing Infrastructure Investments

Governments across the globe are making significant investments in infrastructure, like roads, bridges, and intelligent cities, which is driving the demand for heavy construction machinery. The Government of India aims to build 10,000 km of national highways (NHs) in the fiscal year 2025-26. These investments are driven by long-term strategies to strengthen transport infrastructures. Governments in both developed and emerging regions are placing greater emphasis on developing their infrastructures to accommodate increasing populations and spur economic growth. As these projects continue, they are generating sustained demand for various types of construction equipment, such as cranes, excavators, bulldozers, and graders. Construction firms are reacting to these demands by replacing their fleets with equipment that can address the demands of these mega-projects. Further, these investments are also promoted by the need to implement new, more effective technologies, which are spurring the uptake of advanced and specialized machinery in the heavy construction industry.

Driving Technological Integration

Continuous technological progressions are constantly supporting the market growth. The manufacturers are incorporating automation, telematics, and digital solutions into the machinery to drive productivity and security. These technologies are enabling contractors to streamline operations, track equipment performance in real-time, and enhance maintenance plans, minimizing downtime. With smarter machinery, operators can work more productively, minimizing human faults and maximizing overall output. More electric and hybrid-powered equipment is also finding its way onto job sites, as the world moves toward greater sustainability. The use of artificial intelligence (AI) autonomous driving capabilities, and remote operation technologies is revolutionizing the market, enabling more advanced tasks to be performed with a greater level of accuracy. These technological innovations are encouraging manufacturers to adopt more advanced and newer machinery. In 2025, bauma 2025 highlighted the newest technological advancements in the construction and mining sectors once more. Manufacturers of equipment globally introduced new machines of different types and sizes designed to assist customers in completing their tasks in a productive, efficient, and safe way. The new construction machinery unveiled at bauma 2025 showcases advancements in hydraulics, along with progress in electrification, automation, and digitalization.

Increased Demand for Environmentally Conscious Construction Practices

The construction sector is shifting its focus towards using eco-friendly practices, and that is creating a demand for green heavy construction equipment. Governments and regulations are setting more stringent environmental standards for machinery emissions, which compels manufacturers to innovate and produce equipment that will comply with them. Firms are giving importance to buying energy-efficient machinery, like electric and hybrid construction vehicles, to reduce their carbon footprint and also meet the requirements set by regulations. In response, manufacturers are investing heavily in the development of fuel-efficient and low-emission technologies for heavy construction equipment. The demand for equipment that not only offers enhanced operational performance but also supports environmentally responsible practices is growing steadily. This is supporting the move towards more environment friendly solutions in the industry, encouraging both construction companies and equipment manufacturers to embrace new, more sustainable technology in accordance with international efforts to minimize environmental footprint. IMARC Group predicts that global buildings construction market is projected to attain USD 10.5 Trillion by 2033.

Heavy Construction Equipment Market Growth Drivers:

Increase in Private Sector Investments

Private sector investments are playing an instrumental role in increasing the demand for heavy construction machinery. Large corporations, property developers, and industrial businesses are now investing in massive construction and infrastructure projects. Such investments cut across various sectors of industry, namely residential, commercial, industrial, and energy, all of which involve massive construction activities. While private firms undertake constructing new structures, factories, and infrastructure for accommodating expanding businesses and industries, they are acquiring new and efficient construction machinery. The private sector transition towards adopting cutting-edge machinery, sometimes coupled with advanced technologies such as automation and telematics, is facilitating streamlined operations, cost-cutting, and enhancing project timelines.

Innovation in Rental Schemes and Financing Arrangements

Growing availability of rental configurations and flexible financing structures is empowering more building companies, especially smaller ones, to use high-end heavy construction equipment without the substantial initial outlay. Most building companies are choosing to lease equipment instead of buying, which helps them vary size with respect to project-specific requirements. The rental option offers financial versatility, allowing firms to better control cash flow and minimize capital spending. Also, the leasing and financing facilities provided by original equipment manufacturers and third-party financiers are facilitating the acquisition and utilization of the most recent heavy equipment by construction companies. Such models are attractive particularly for those operating in markets with volatile demand or those engaged in short-duration or specialized work. Increased accessibility of rental and financing options is expanding market reach and driving the market, as more firms embrace the latest machines without the hassle of costly financial outlays.

Enhancing Regulatory Frameworks

With governments globally enacting stricter rules for safety, emissions, and operating standards, demand is growing for higher-end heavy construction equipment. Machinery is also seeing regulatory authorities create standards for machines to ensure increased safety, as well as reduced environmental impact. For example, new emission standards are creating demand for cleaner-burning, more fuel-efficient engines; meanwhile, safety regulations are driving equipment manufacturers to add features that include collision avoidance systems and enhanced operator visibility. These regulations are encouraging construction businesses to update their fleets to meet current standards, driving a demand for newer, more sophisticated equipment. Moreover, as these regulatory systems become more complete, they assist in building a healthier, more sustainable construction industry, promoting long-term investment in heavier, newer construction equipment.

Heavy Construction Equipment Market Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the market, along with forecasts at the global, regional, and country levels for 2026-2034. Our report has categorized the market based on equipment type and end user.

Breakup by Equipment Type:

- Earthmoving Equipment

- Material Handling Equipment

- Heavy Construction Vehicles

- Others

Earthmoving equipment represents the leading market segment

The report has provided a detailed breakup and analysis of the market based on the equipment type. This includes managed earthmoving equipment, material handling equipment, heavy construction vehicles, and others. According to the report, earthmoving equipment represented the largest segment.

The earthmoving equipment segment is driven by several key factors that shape its dynamics, such as the increasing demand for infrastructure development projects worldwide fuels the need for earthmoving equipment. Infrastructure projects, including the construction of roads, bridges, dams, and urban development initiatives, require earthmoving machinery for excavation, grading, and leveling tasks. As countries invest in modernizing their transportation networks and expanding urban areas, the demand for earthmoving equipment continues to rise steadily. Moreover, the growing trend towards mechanization and automation in the construction industry propels the demand for advanced earthmoving equipment. Construction companies are increasingly adopting automated and semi-automated machinery to improve efficiency, productivity, and safety on construction sites. The integration of technologies such as GPS, telematics, and remote monitoring enhances the precision and accuracy of earthmoving operations, driving the adoption of modern equipment solutions. Apart from this, stringent government regulations and environmental standards drive innovation in the earthmoving equipment segment.

Breakup by End User:

Access the comprehensive market breakdown Request Sample

- Infrastructure

- Construction

- Mining

- Oil and Gas

- Manufacturing

- Others

The report has provided a detailed breakup and analysis of the market based on the end-user. This includes infrastructure, construction, mining, oil and gas, manufacturing, and others.

The infrastructure segment is driven by the increasing demand for modernization and expansion of transportation networks, utilities, and urban areas. Governments worldwide are investing heavily in infrastructure projects to stimulate economic growth, enhance connectivity, and address urbanization challenges. This includes the construction of roads, bridges, railways, airports, ports, and utilities such as water supply and sanitation systems. Additionally, the growing emphasis on sustainable infrastructure development, coupled with the need to upgrade aging infrastructure, further fuels the demand for construction activities in this segment.

The construction segment is driven by the increasing demand for residential, commercial, and industrial buildings, fueled by population growth, urbanization, and economic development. Urbanization trends are leading to the construction of new housing developments, office buildings, retail centers, and industrial facilities to accommodate growing populations and meet the needs of businesses. Moreover, infrastructure projects such as roads, bridges, and utilities also contribute to the construction sector's growth.

The mining segment is driven by the increasing demand for minerals, metals, and aggregates for various industries, including construction, manufacturing, and infrastructure development. Growing population and urbanization drive demand for raw materials used in construction, infrastructure, and manufacturing activities. Additionally, industrialization and economic growth in emerging economies lead to increased demand for metals such as steel, copper, and aluminum for manufacturing and infrastructure projects. Technological advancements in mining equipment and processes, including automation, remote sensing, and digitalization, enhance operational efficiency, safety, and productivity in the mining sector.

The oil and gas segment is driven by the increasing global energy demand, industrialization, and urbanization, which require the exploration, extraction, and production of oil and gas resources. Growing population, urbanization, and economic development drive demand for energy to power industries, transportation, and households. Additionally, emerging economies' industrialization drives demand for petrochemicals used in manufacturing various products, further fueling the oil and gas sector's growth.

The manufacturing segment is driven by the increasing demand for manufactured goods, driven by population growth, rising disposable incomes, and urbanization. Manufacturing plays a crucial role in economic development, job creation, and technological innovation. Demand for manufactured goods spans various industries, including automotive, electronics, consumer goods, and machinery. Technological advancements such as automation, robotics, and additive manufacturing are transforming manufacturing processes, making them more efficient, flexible, and cost-effective.

The others segment encompasses various industries and sectors not covered by the specific categories mentioned above, including agriculture, healthcare, retail, and services. The driving factors for this segment vary depending on the industry and its specific characteristics.

Breakup by Region:

- North America

- United States

- Canada

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

Asia Pacific leads the market, accounting for the heavy construction equipment market share

The report has also provided a comprehensive analysis of all the major regional markets, which include North America (the United States and Canada); Europe (Germany, France, the United Kingdom, Italy, Spain, Russia, and others); Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, and others); Latin America (Brazil, Mexico, and others); and the Middle East and Africa. According to the report, Asia Pacific represents the largest regional market for heavy construction equipment.

The Asia Pacific region is driven by the increasing urbanization and infrastructure development projects, which serve as key factors propelling the demand for heavy construction equipment. As countries in the region experience rapid population growth and urban migration, there is a pressing need to accommodate the expanding urban population through the construction of residential buildings, commercial complexes, transportation networks, and utilities. This surge in urbanization creates a significant demand for heavy construction equipment, including excavators, bulldozers, cranes, and concrete mixers, to undertake large-scale construction activities efficiently and effectively. Additionally, infrastructure development initiatives, such as the construction of roads, highways, bridges, airports, and ports, are prioritized by governments to support economic growth, enhance connectivity, and attract investments. Consequently, substantial investments are allocated to infrastructure projects, creating lucrative opportunities for equipment manufacturers and rental companies in the region. Furthermore, the increasing adoption of advanced technologies, such as IoT, telematics, and automation, in construction equipment further drives market growth in the Asia Pacific region. These technologies enable equipment operators to monitor performance, track maintenance needs, and optimize operations in real-time, resulting in improved productivity, safety, and cost-effectiveness.

Competitive Landscape:

In the highly competitive global heavy construction equipment market, key players are strategically focused on several initiatives to maintain and strengthen their market positions. These initiatives include investing significantly in R&D to innovate and introduce advanced technologies in their product portfolios. By incorporating IoT, telematics, automation, and other cutting-edge solutions, manufacturers aim to enhance equipment efficiency, productivity, and safety, meeting the evolving needs and preferences of customers. Furthermore, there is a concerted effort among market players to expand their geographic presence and distribution networks, tapping into emerging markets with high growth potential. Strategic collaborations, partnerships, mergers, and acquisitions are also prevalent strategies employed by key players to broaden their product offerings, diversify their customer base, and gain a competitive edge. Additionally, sustainability has become a key focus area, with manufacturers investing in the development of eco-friendly construction equipment that complies with stringent environmental regulations and addresses growing concerns about carbon emissions and resource depletion.

The report provides a comprehensive analysis of the competitive landscape in the global heavy construction equipment market with detailed profiles of all major companies, including:

- AB Volvo

- Caterpillar Inc

- CNH Industrial N.V.

- Deere & Company

- HD Hyundai Infracore

- Hitachi Construction Machinery Co., Ltd.

- J C Bamford Excavators Ltd.

- Komatsu Ltd

- Liebherr Group

- SANY Group

- Terex Corporation

- XCMG Group

Heavy Construction Equipment Market News:

- June 2025: Volvo Construction Equipment announced that it will start manufacturing crawler excavators and large wheel loaders at its Shippensburg, Pennsylvania, plant as part of a broader global investment to address increasing demand for its heavy equipment. The subsidiary of the Volvo Group intends to invest $261 million to enhance crawler excavator manufacturing at three locations, which include Shippensburg; Changwon, South Korea; and a site in Sweden, as stated in a recent announcement.

- June 2025: To improve service for its North American clientele, Volvo Construction Equipment (Volvo CE) is increasing heavy machinery production at its facility in Shippensburg, Pennsylvania. Volvo CE is increasing production capacity to meet customer needs in South Korea, Sweden, and North America, as part of a broader $261 million strategic investment. This expansion will enable the Shippensburg plant, which currently produces compactors and mid-size wheel loaders, to manufacture excavators and large wheel loaders.

- January 2025: SANY India, a top producer of construction machinery, has opened a modern factory at its expansive 90-acre manufacturing site in Pune. This expansion marks a crucial step in boosting production capacity and local manufacturing in India. Additionally strengthening SANY's dedication to the Indian market and establishing India as a global sourcing center.

- December 2024: Hitachi Construction Machinery Company, Limited announced the creation of Hitachi Construction Machinery Development Center India Private Limited (“Hitachi Construction Machinery Development Center India”), a subsidiary that will focus on the development and design of construction gear in India, established in late December to enhance the product manufacturing capabilities of the Hitachi Construction Machinery Group.

- October 2024: Teleo, a firm developing autonomous technology for heavy construction machinery, reveals at UP.Partners' UP.Summit that it is broadening its strategic emphasis to implement autonomous heavy equipment like wheel loaders, terminal tractors, excavators, and others into additional industries outside of construction. The company has also revealed that it has obtained orders for 34 machines and finalized nine new customer agreements in the logging, port logistics, pulp and paper, munition clearing, and agriculture sectors. Teleo is aiming to expand into various sectors, including airports, waste and recycling, logistics, warehousing, and additional areas. Further orders have been made that broaden Teleo's footprint in the snow removal and construction sectors, encompassing the firm's entry into the Australian market.

Heavy Construction Equipment Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Equipment Types Covered | Earthmoving Equipment, Material Handling Equipment, Heavy Construction Vehicles, Others |

| End-Users Covered | Infrastructure, Construction, Mining, Oil and Gas, Manufacturing, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | AB Volvo, Caterpillar Inc, CNH Industrial N.V., Deere & Company, HD Hyundai Infracore, Hitachi Construction Machinery Co., Ltd., J C Bamford Excavators Ltd., Komatsu Ltd, Liebherr Group, SANY Group, Terex Corporation, XCMG Group, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the heavy construction equipment market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global heavy construction equipment market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the heavy construction equipment industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Heavy Construction Equipment Market Report

The global heavy construction equipment market was valued at USD 150.8 Billion in 2025.

We expect the global heavy construction equipment market to exhibit a CAGR of 4.28% during 2026-2034.

The introduction of driver assistance systems and real-time data tracking to streamline processes and monitor the location, fuel usage, operating hours, maintenance of the machinery, etc., is primarily driving the global heavy construction equipment market.

The sudden outbreak of the COVID-19 pandemic had led to the implementation of stringent lockdown regulations across several nations, resulting in the temporary closure of numerous end-use industries for heavy construction equipment.

Based on the equipment type, the global heavy construction equipment market can be bifurcated into earthmoving equipment, material handling equipment, heavy construction vehicles, and others. Currently, earthmoving equipment exhibits a clear dominance in the market.

On a regional level, the market has been classified into North America, Asia-Pacific, Europe, Latin America, and Middle East and Africa, where Asia-Pacific currently dominates the global market.

Some of the major players in the global heavy construction equipment market include AB Volvo, Caterpillar Inc, CNH Industrial N.V., Deere & Company, HD Hyundai Infracore, Hitachi Construction Machinery Co., Ltd., J C Bamford Excavators Ltd., Komatsu Ltd, Liebherr Group, SANY Group, Terex Corporation, and XCMG Group.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)