Heavy-Duty Automotive Aftermarket Market Size, Share, Trends and Forecast by Replacement Parts, Vehicle Type, Service Channel, and Region, 2026-2034

Global Heavy-Duty Automotive Aftermarket Market Size, Share, Trends & Forecast (2026-2034)

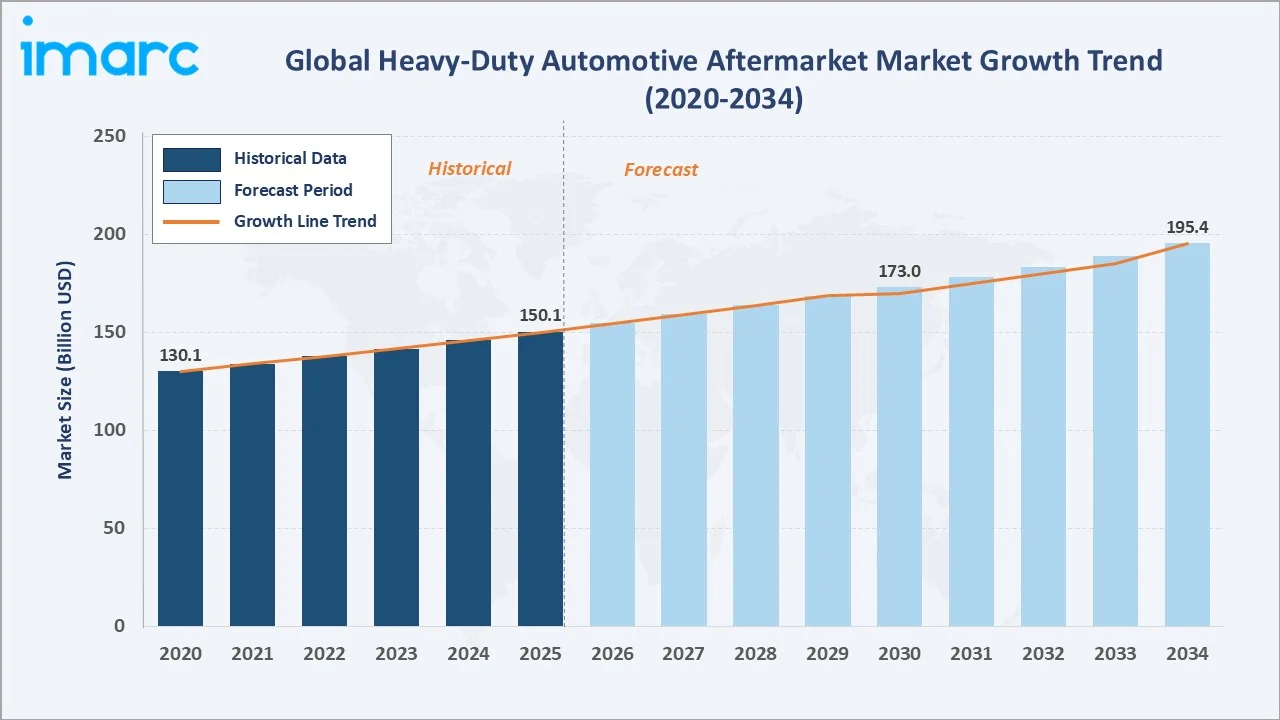

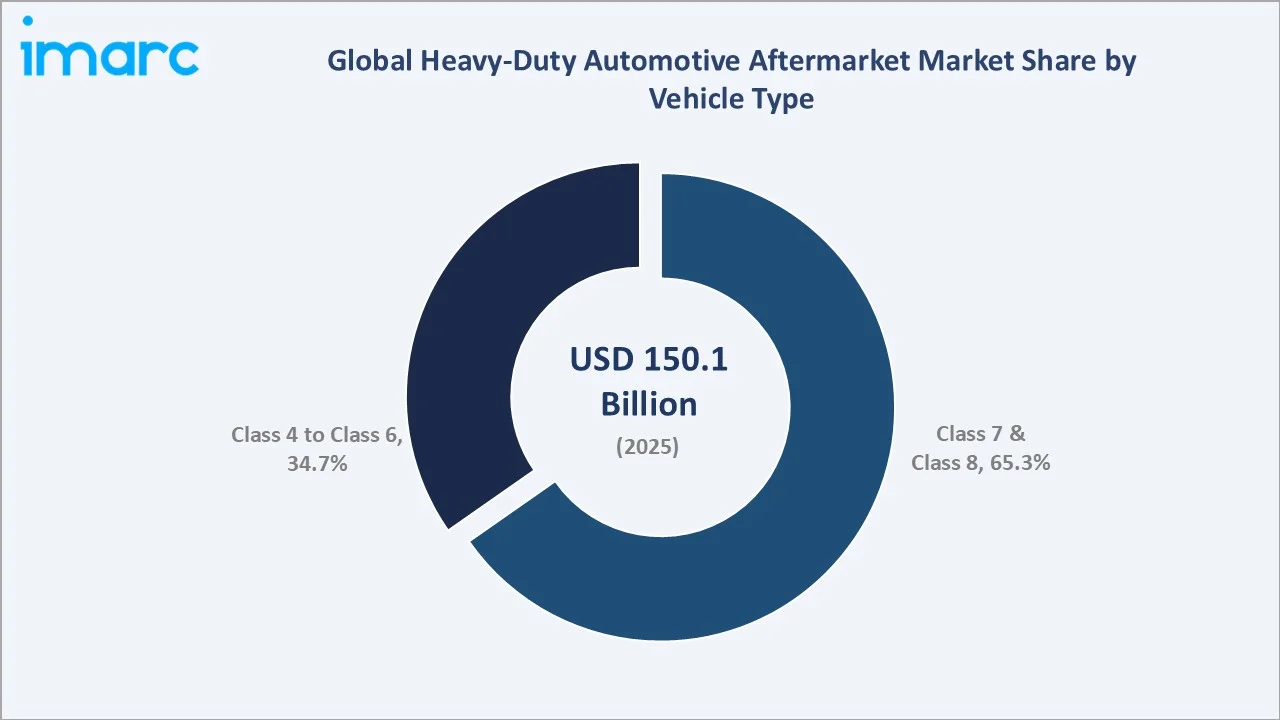

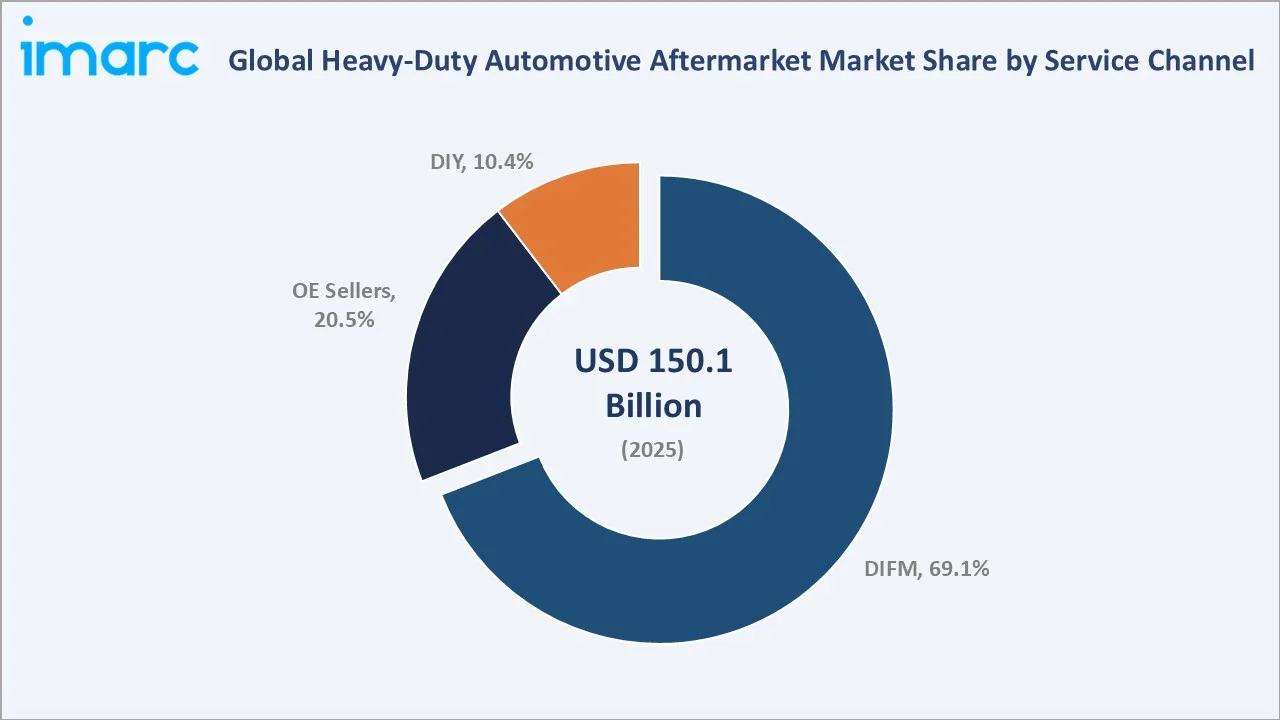

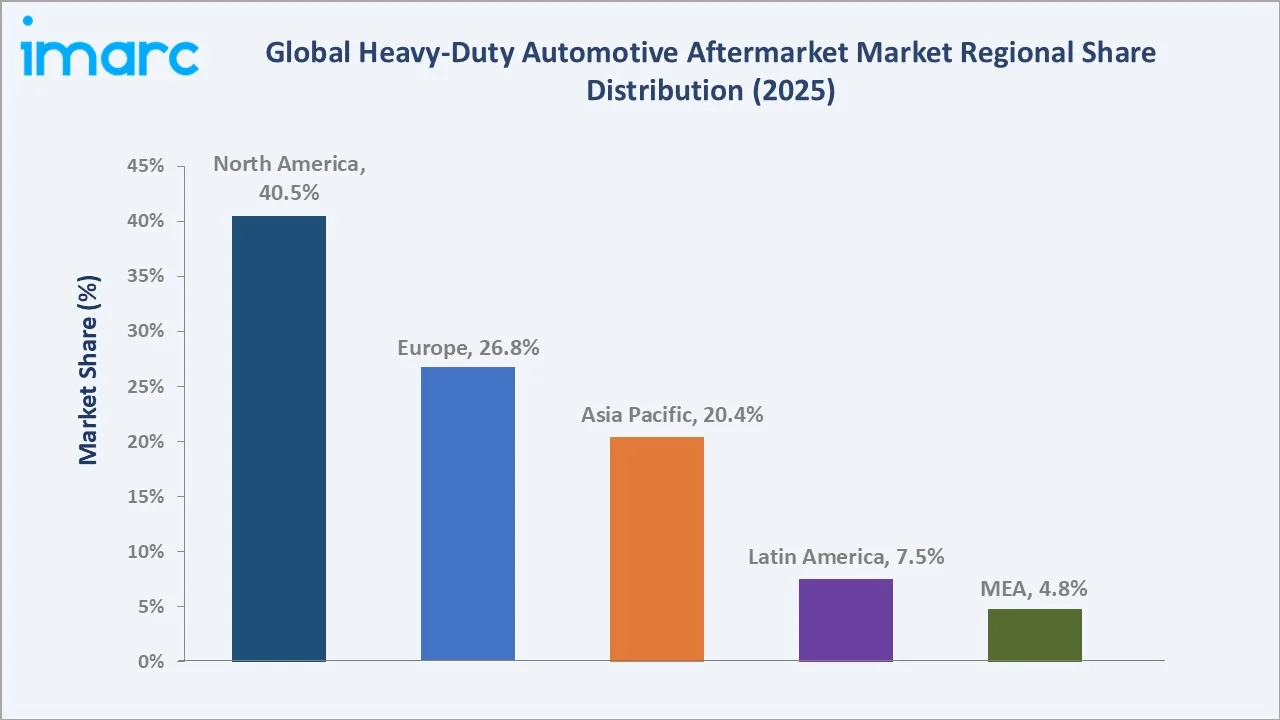

The global heavy-duty automotive aftermarket market size was valued at USD 150.1 Billion in 2025 and is projected to reach USD 195.4 Billion by 2034, exhibiting a CAGR of 2.89% during the forecast period 2026-2034. Growing reliance on aging commercial vehicle fleets, rising freight and logistics activity globally, and the rapid adoption of telematics and predictive maintenance tools are driving the heavy-duty automotive aftermarket market growth. Class 7 and Class 8 vehicles lead the vehicle type segment at 65.3% in 2025, while the DIFM (Do-It-For-Me) channel dominates service delivery at 69.1%. North America accounts for 40.5% of global revenue in 2025, the world's largest regional market.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 150.1 Billion |

|

Forecast Market Size (2034) |

USD 195.4 Billion |

|

CAGR (2026-2034) |

2.89% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North America (40.5% share, 2025) |

|

Fastest Growing Region |

Asia Pacific |

|

Leading Vehicle Segment |

Class 7 & Class 8 (65.3%, 2025) |

|

Leading Service Channel |

DIFM (69.1%, 2025) |

The global heavy-duty automotive aftermarket market growth trajectory from 2020 through 2034 shows a consistent historical expansion base against a sustained forecast curve powered by fleet ageing dynamics, e-commerce-driven parts accessibility, and regulatory compliance requirements across major markets.

To get more information on this market, Request Sample

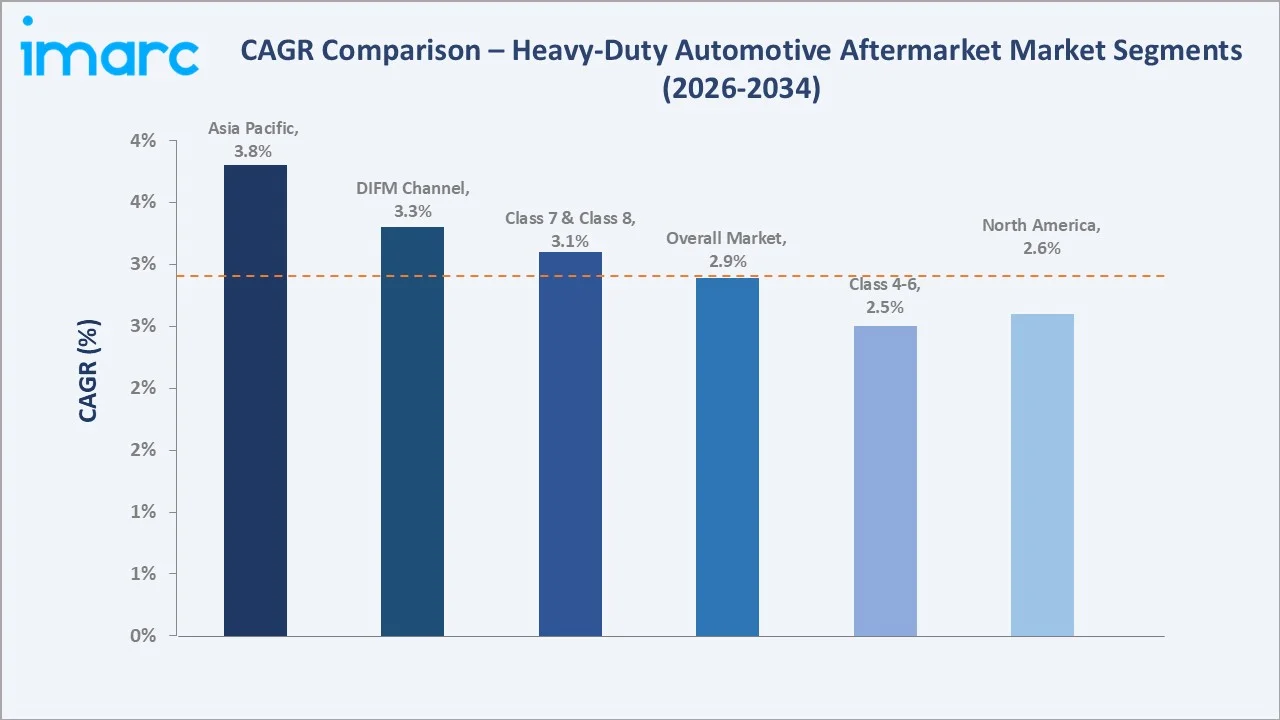

Segment-level CAGR comparisons highlighting Asia Pacific and the DIFM service channel as the fastest-growing sub-categories within the global heavy-duty automotive aftermarket industry analysis through 2034.

Executive Summary

The global heavy-duty automotive aftermarket market is experiencing consistent and broad-based expansion, driven by the structural growth of the global commercial vehicle fleet and the ongoing requirement for regular parts replacement, maintenance, and regulatory compliance upgrades. Valued at USD 150.1 Billion in 2025, the market is forecast to reach USD 195.4 Billion by 2034, exhibiting a CAGR of 2.89%. Fleet operators globally are prioritising vehicle uptime and cost efficiency over new vehicle acquisition, which directly sustains demand for replacement parts, repair services, and component upgrades across all major regions.

Class 7 and Class 8 vehicles command the dominant vehicle type share at 65.3% in 2025, driven by the high annual mileage accumulated by long-haul tractor-trailers and heavy freight trucks that require more frequent parts replacement than lighter commercial vehicles. The DIFM service channel holds a 69.1% share in 2025, reflecting the technical complexity of heavy-duty vehicle maintenance that necessitates professional servicing. Key growth drivers include the aging commercial vehicle fleet – with the average Class 8 truck age exceeding 7 years in the United States in 2024 – rising telematics adoption, and expanding e-commerce platforms that simplify parts procurement for fleet managers. According to the IMARC Group, the United States commercial telematics market is set to attain USD 61.0 Billion by 2033, growing at a CAGR of 12.3% during 2025-2033.

North America leads with a 40.5% regional share in 2025, supported by a vast aging fleet, high per-vehicle mileage from long-haul logistics operations, and a well-developed distribution ecosystem anchored by companies including Genuine Parts Company. Europe holds a 26.8% share, driven by Euro 7 emission compliance mandates and fleet modernisation programmes. Asia Pacific represents 20.4% of the market in 2025 and is the fastest-growing regional market, fuelled by rapid freight growth in China and India and expanding commercial vehicle fleet penetration across Southeast Asia.

Key Market Insights

|

Insight |

Data |

|

Largest Vehicle Segment |

Class 7 & Class 8 – 65.3% share (2025) |

|

Leading Service Channel |

DIFM – 69.1% share (2025) |

|

Leading Region |

North America – 40.5% revenue share (2025) |

|

Second Largest Region |

Europe – 26.8% revenue share (2025) |

|

Top Companies |

Genuine Parts Company, Robert Bosch GmbH, ZF Friedrichshafen AG, Tenneco Inc., Dana Limited, Continental AG and MAHLE Aftermarket GmbH |

Key Analytical Observations Supporting The Above Data:

- Class 7 & Class 8 vehicles' 65.3% dominance in 2025 reflects the substantially higher annual mileage, heavier load cycles, and more frequent component replacement requirements of long-haul tractor-trailers and heavy freight trucks compared to medium-duty Class 4-6 vehicles.

- The DIFM channel's 69.1% share in 2025 underscores the technical specialisation required for heavy-duty vehicle maintenance; the integration of telematics, emission control systems, and electronic diagnostic platforms has made professional servicing indispensable for fleet operators.

- North America's 40.5% global dominance in 2025 stems from a large and aging commercial fleet – with over 3.1 million active Class 8 units in the US alone – combined with high per-vehicle mileage from long-haul logistics and a mature, well-distributed aftermarket supply chain.

Global Heavy-Duty Automotive Aftermarket Market Overview

The heavy-duty automotive aftermarket includes replacement parts, maintenance, and repair services for Class 4–8 commercial vehicles, spanning medium-duty trucks to heavy freight and specialized vehicles. The ecosystem comprises OEM, independent aftermarket (IAM), and remanufactured components, distributed through DIFM service networks, OEM channels, and DIY supply points.

It serves diverse applications, including long-haul freight, last-mile delivery, construction, agriculture, and municipal services. Key product categories—such as tires, batteries, brakes, filters, electronics, and exhaust systems—have distinct replacement cycles and margin profiles that shape competitive dynamics.

Market growth is supported by rising freight activity, aging fleets in developed markets, and expanding vehicle parc in emerging regions, alongside increasing adoption of digital fleet management and predictive maintenance technologies that are making aftermarket demand more structured and recurring.

Market Dynamics

To evaluate market opportunities, Request Sample

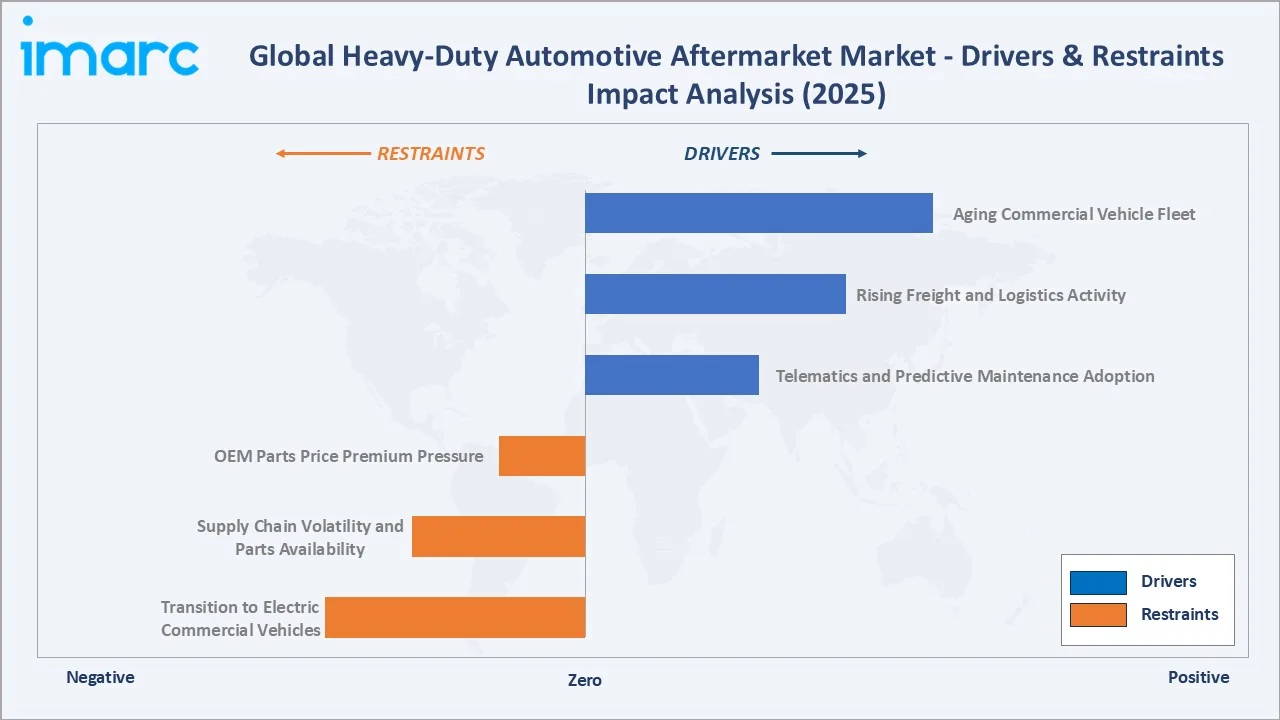

Market Drivers

- Aging Commercial Vehicle Fleet: The steady increase in average fleet age across North America and Europe is a core structural driver of aftermarket demand. Fleet operators are extending vehicle lifecycles to defer capital expenditure, which directly increases maintenance intensity. Older vehicles require more frequent replacement of high-wear components such as brakes, filters, suspension systems, and exhaust assemblies, creating a stable and recurring revenue base for aftermarket participants.

- Rising Freight and Logistics Activity: Growth in freight movement, supported by e-commerce expansion and supply chain regionalization, is increasing annual vehicle utilization. Higher kilometres driven per truck accelerate wear-and-tear cycles, directly translating into increased demand for replacement parts and maintenance services across all major regions.

- Telematics and Predictive Maintenance Adoption: Increasing penetration of connected vehicle technologies is shifting maintenance from reactive to predictive. Real-time diagnostics enable fleet operators to identify component degradation early, leading to planned replacement cycles, reduced downtime, and more consistent aftermarket demand visibility.

- Emission Compliance Requirements: Tightening emission regulations in key markets are driving demand for exhaust aftertreatment systems, including diesel particulate filters and selective catalytic reduction units. Fleet operators are required to upgrade or retrofit older vehicles to remain compliant, adding a regulatory-driven layer of aftermarket demand beyond routine maintenance.

Market Restraints

- Transition to Electric Commercial Vehicles: The gradual adoption of battery-electric trucks presents a structural restraint on the aftermarket. Electric powertrains have significantly fewer moving parts and eliminate the need for several high-value ICE-related components such as engine systems, exhaust assemblies, and multi-speed transmissions, reducing long-term parts demand in these categories.

- Supply Chain Volatility and Parts Availability: The aftermarket ecosystem remains exposed to supply-side disruptions, including fluctuations in raw material costs, component shortages, and logistics constraints. These factors can impact parts availability, increase procurement costs, and compress margins for distributors and service providers.

Market Opportunities

- Remanufacturing and Circular Economy: Remanufactured components are gaining traction as a cost-effective alternative to new parts, offering comparable performance at significantly lower cost. This segment aligns with both cost optimization strategies of fleet operators and broader sustainability objectives, while also benefiting from the large installed base of internal combustion engine vehicles.

- Asia Pacific Fleet Expansion: Rapid growth in commercial vehicle parc across emerging markets such as India and Southeast Asia is creating new aftermarket demand pools. These regions remain relatively underpenetrated in terms of organized distribution networks, providing expansion opportunities for both global and regional aftermarket players.

- Digital Parts Marketplaces: The rise of digital B2B procurement platforms is improving parts accessibility, pricing transparency, and ordering efficiency. Companies investing in e-commerce capabilities, digital catalogs, and integrated logistics are well-positioned to capture share from traditional distribution models.

Market Challenges

- OEM Parts Price Premium Pressure: OEM-branded parts typically carry a pricing premium relative to independent aftermarket alternatives. Under cost pressure, fleet operators often shift toward lower-cost substitutes, creating sustained pricing pressure and margin compression for OEM aftermarket businesses.

- Certified Technician Shortage: The shortage of trained heavy-duty vehicle technicians is a critical bottleneck in the service value chain. Limited service capacity increases turnaround times and restricts the ability of the aftermarket ecosystem to fully capture demand, particularly in high-utilization fleet environments.

Emerging Market Trends

1. Telematics-Driven Predictive Maintenance Transforming Aftermarket Service Demand

Fleet operators are rapidly integrating telematics platforms, IoT-enabled sensors, and AI-driven diagnostics to monitor vehicle health in real time, including engine performance, braking systems, tire condition, and fuel efficiency. This is shifting maintenance from mileage-based to condition-based scheduling, enabling earlier intervention and more frequent replacement of critical wear components while reducing unplanned breakdowns. As a result, aftermarket demand is becoming more predictable, with improved planning visibility for both fleet operators and parts suppliers.

2. E-Commerce Reshaping Heavy-Duty Parts Procurement

The traditional parts distribution model is undergoing structural disruption as digital procurement platforms gain traction. Fleet operators are increasingly sourcing parts online, benefiting from greater price transparency, wider supplier access, and faster delivery timelines. Advanced digital capabilities such as AI-driven parts identification, VIN-based search, and integrated logistics are enabling faster and more efficient procurement, allowing digital-first players to capture share from conventional distributor networks.

3. Remanufacturing and Circular Economy Adoption

Cost pressures and sustainability considerations are accelerating the adoption of remanufactured components across heavy-duty vehicle segments. Products such as engines, transmissions, turbochargers, and alternators offer comparable performance to new parts at materially lower cost while extending component lifecycle and reducing waste. This trend is driving the industrialization of remanufacturing, with both OEMs and independent suppliers expanding capabilities to support a growing installed base of aging vehicles.

4. Emission System Aftermarket Expansion Driven by Regulatory Mandates

Stringent emission standards are creating a distinct and growing aftermarket segment focused on exhaust aftertreatment systems. Components such as diesel particulate filters (DPF), selective catalytic reduction (SCR) systems, exhaust gas recirculation (EGR) units, and related sensors require periodic replacement under intensive operating conditions. This compliance-driven demand is structurally additive to routine maintenance and remains resilient due to the large installed base of diesel vehicles.

5. Electric Commercial Vehicle Aftermarket Beginning to Emerge

The gradual deployment of electric heavy-duty vehicles is giving rise to a new aftermarket category centered on EV-specific services. These include battery diagnostics, thermal management systems, electric drivetrains, high-voltage components, and charging infrastructure maintenance. While still at an early stage, this segment is expected to scale over time as fleet electrification increases, partially offsetting the long-term decline in traditional internal combustion engine-related aftermarket demand.

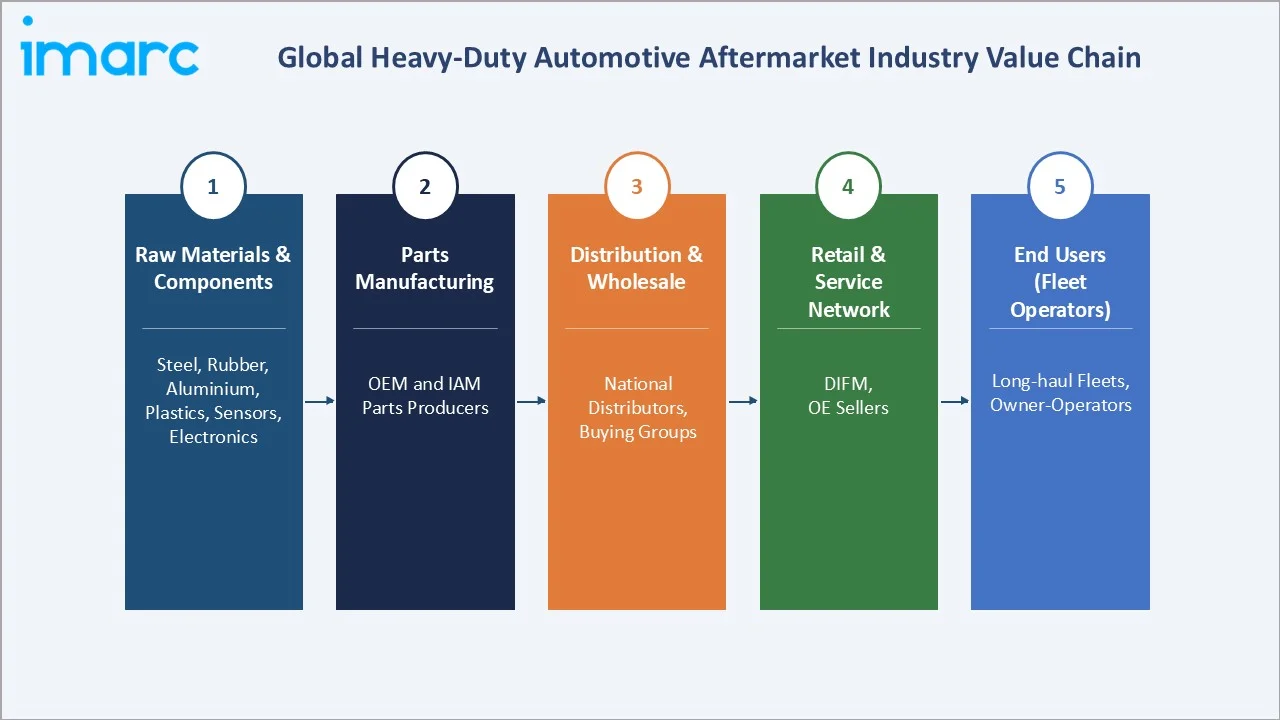

Industry Value Chain Analysis

The heavy-duty automotive aftermarket value chain spans five integrated stages from raw material supply through to end-user fleet operations. Each stage involves specialised participants with distinct competitive dynamics, margin profiles, and strategic investment requirements.

|

Stage |

Key Players / Activities |

|

Raw Materials & Components |

Steel, rubber, aluminium, plastics, sensors, electronics |

|

Parts Manufacturing |

OEM and IAM parts producers |

|

Distribution & Wholesale |

National distributors, buying groups, digital portals |

|

Retail & Service Network |

DIFM workshops, dealerships, fleet service centres |

|

End Users (Fleet Operators) |

Long-haul fleets, owner-operators, leasing firms, municipal fleets |

The distribution and wholesale stage represents the highest concentration of competitive activity, where national parts distributors, buying groups, and digital platforms compete on pricing, availability, speed, and service breadth. Independent aftermarket (IAM) players continue to gain share versus OEM-aligned channels, particularly in high-volume commodity categories including filters, brakes, and standard electrical components. The retail and service network stage is being disrupted by e-commerce platforms that are compressing the traditional distributor-to-shop supply chain.

Technology Landscape in the Heavy-Duty Automotive Aftermarket Industry

Telematics and IoT-Based Diagnostics

Advanced telematics platforms combining GPS tracking, vehicle health monitoring, and IoT-connected sensors are fundamentally changing aftermarket service scheduling. Real-time monitoring of engine parameters, brake wear indicators, tire pressure management systems (TPMS), and exhaust aftertreatment system performance enables fleet managers to schedule parts replacements before failures occur.

Remanufacturing Technology and Circular Economy

Industrial remanufacturing has evolved from basic reconditioning to precision engineering with OEM-grade quality standards. Automated cleaning systems, advanced non-destructive testing (NDT), computer-controlled machining, and ISO/PAS 9001 quality certification are enabling remanufactured components to meet or exceed original performance specifications.

Digital Parts Catalogue and E-Commerce Integration

Modern parts e-commerce platforms integrate AI-powered parts lookup, VIN-based compatibility checking, real-time inventory visibility across multiple distribution centres, and automated procurement workflows. APIs connecting fleet management systems directly to parts procurement portals are enabling fully automated replenishment for predictable wear items. This digital infrastructure is compressing traditional 2-3 day lead times toward same-day or next-day delivery in well-served markets.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Replacement Parts | Tires | 🔒 | 2025 |

| Vehicle Type | Class 7 and Class 8 | 65.3% | 2025 |

| Service Channel | DIFM | 69.1% | 2025 |

| Region | North America | 40.5% | 2025 |

By Vehicle Type

Class 7 and Class 8 vehicles command a 65.3% majority share of the heavy-duty automotive aftermarket in 2025, driven by the substantially higher annual mileage, heavier load cycles, and more complex technical profiles of long-haul tractor-trailers, heavy dump trucks, and specialised freight haulers.

To access detailed market analysis, Request Sample

Class 4 to Class 6 vehicles represent 34.7% of the market in 2025. This segment spans medium-duty delivery trucks, refuse vehicles, utility trucks, and municipal service vehicles across a diverse range of applications. While average annual mileage is lower than Class 8, the breadth of parts categories required – and the growth of last-mile logistics operations driven by e-commerce expansion – is providing a positive counter-cyclical growth dynamic relative to long-haul freight. The Class 4-6 segment is also less exposed to the fleet electrification transition risk, as electric medium-duty vehicles are commercially available earlier and in greater volume than Class 8 electric trucks.

By Service Channel

The DIFM (Do-It-For-Me) channel commands the largest share at 69.1% in 2025, a dominant position that reflects the high technical complexity of modern heavy-duty vehicle maintenance. Fleet managers rely on professional workshops, authorised dealership service centres, and specialised heavy-duty independent repair shops (ISPs) for complex diagnostics, warranty-compliant emission system maintenance, and electronic system repairs. The integration of telematics, emission control systems, advanced braking technologies, and electronic engine management into modern Class 4-8 vehicles has further reinforced the structural dominance of professional service channels.

OE Sellers account for 20.5% of the market in 2025, representing parts sourced directly through OEM dealerships and authorised service networks. This channel commands a pricing premium but provides warranty compliance assurance, access to the latest technical service bulletins, and OEM-certified repair procedures that are required for fleet warranty maintenance contracts. The DIY segment holds 10.4% share, primarily serving owner-operators, small independent haulers, and fleet operations with in-house maintenance teams capable of handling routine servicing tasks such as oil changes, basic filter replacements, and lamp servicing.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

North America |

40.5% |

Aging fleet, high per-vehicle mileage, strong distribution ecosystem, and telematics growth |

|

Europe |

26.8% |

Euro 7 compliance drive, fleet modernisation, strong OEM aftermarket channels |

|

Asia Pacific |

20.4% |

Rapid freight growth in China and India, fleet expansion, and emerging distribution networks |

|

Latin America |

7.5% |

Cost-sensitive fleets, rising e-commerce penetration, and import-dependent supply chains |

|

ME & Africa |

4.8% |

Infrastructure expansion, urbanisation, and growing commercial vehicle adoption |

North America commands a 40.5% global revenue share in 2025, the most dominant regional position in the heavy-duty automotive aftermarket. Europe holds a 26.8% share in 2025, shaped by stringent Euro 7 emission mandates, an aging freight truck fleet, and a high concentration of large fleets operated by pan-European logistics companies. Euro 7 standards are creating a compliance-driven wave of exhaust aftertreatment parts replacements. Germany, France, and the United Kingdom represent the largest national aftermarket sub-markets, with regional suppliers. The European aftermarket is also benefiting from a growing remanufacturing sector as circular economy regulations incentivise component refurbishment over disposal.

Asia Pacific represents 20.4% of the global market in 2025 and is the fastest-growing regional segment. China and India are the principal growth engines. China's heavy-duty truck market is the world's largest by unit volume, with commercial vehicle registrations. India's freight vehicle fleet is growing at 6-7% annually, creating a large and underserved aftermarket opportunity in tires, batteries, brakes, and filters. Distribution infrastructure is developing rapidly, with both domestic players and multinational distributors, including Bosch India and Continental, expanding their aftermarket network presence across Tier-2 and Tier-3 cities.

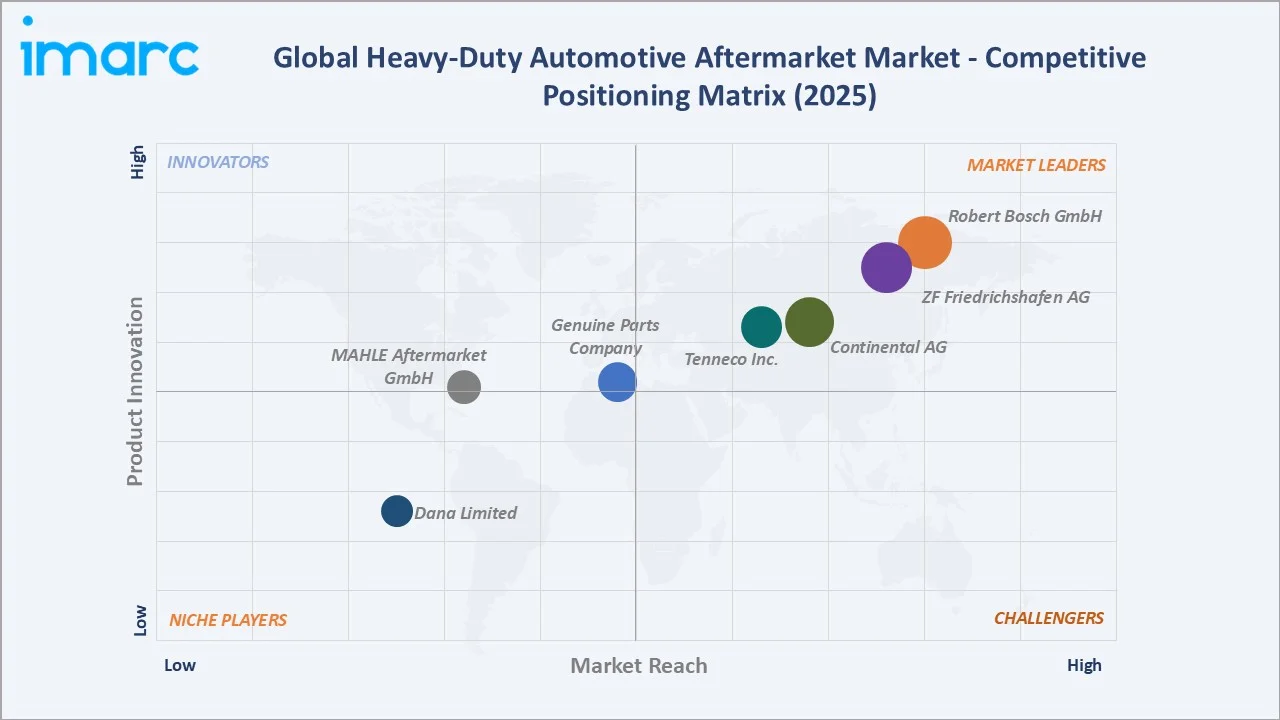

Competitive Landscape

|

Company Name |

Key Brand |

Market Position |

Core Strength |

|

Genuine Parts Company |

NAPA |

Leader |

Broad distribution, global reach, e-commerce expansion |

|

Robert Bosch GmbH |

Bosch Mobility Aftermarket |

Leader |

Filtration, braking, electrical systems, diagnostics |

|

ZF Friedrichshafen AG |

ZF Aftermarket |

Leader |

Driveline, suspension, steering, remanufacturing |

|

Tenneco Inc. |

Monroe |

Challenger |

Ride performance, emission control, DPF/SCR products |

|

Dana Limited |

Spicer |

Emerging |

Drivetrain, sealing, thermal management components |

|

Continental AG |

ContiTech |

Emerging |

Belts, sensors, fluid systems, emission solutions |

|

MAHLE Aftermarket GmbH |

Clevite |

Challenger |

Engine components, filters, gaskets, thermal management, and HD diagnostics |

The heavy-duty automotive aftermarket competitive landscape is characterised by a small number of global multinational distributors and parts manufacturers commanding substantial market positions, alongside regional distributors and specialised component suppliers serving specific parts categories and geographies. The top five players collectively account for approximately 25-30% of global market revenue in 2025, with the remainder held by a diverse ecosystem of regional operators and independent specialists.

Key Company Profiles

Genuine Parts Company

Genuine Parts Company is an automotive parts distributor, operating the NAPA Auto Parts network across more than 6,000 stores in North America and extensive operations in Europe and the Asia Pacific.

- Product Portfolio: Replacement parts for brakes, filters, batteries, belts, hoses, electrical components, and chassis systems across Class 4-8 vehicle ranges, distributed under the NAPA and Motion Industries brands.

- Recent Developments: In February 2026, Genuine Parts Company announced a plan to separate automotive and industrial businesses into two industry-leading public companies.

- Strategic Focus: Genuine Parts Company focuses on expanding fleet penetration through digital commerce, rapid delivery, and targeted pricing programs, while accelerating international growth via acquisitions in Europe and the Asia Pacific.

Robert Bosch GmbH

Robert Bosch is a global leader in heavy-duty aftermarket components, supplying filtration systems, braking components, sensors, diagnostics equipment, and electrical components for Class 4-8 commercial vehicles. Its Bosch Automotive Aftermarket division offers more than 45,000 part numbers for the commercial vehicle sector.

- Product Portfolio: Filtration (oil, fuel, air, cabin air), braking systems, starters and alternators, injectors, spark plugs, sensors, vehicle diagnostics platforms, and emission control components.

- Recent Developments: In January 2024, Qualcomm and Robert Bosch unveiled the automotive industry's first central vehicle computer integrating both infotainment and ADAS functions on a single SoC, demonstrating Bosch's progression toward software-defined vehicle architecture leadership relevant to the connected aftermarket.

- Strategic Focus: Bosch Aftermarket's strategy prioritises OEM-quality assurance, connected diagnostics integration, and digital workshop management tools that link Bosch parts supply directly to fleet maintenance scheduling platforms.

ZF Friedrichshafen AG

ZF Aftermarket supplies driveline, suspension, steering, and braking components to the global heavy-duty aftermarket under multiple branded lines, including TRW, Sachs, and Lemforder. ZF serves both the OEM service channel and the independent aftermarket with a comprehensive commercial vehicle parts portfolio.

- Product Portfolio: Clutches, transmissions, axle components, steering systems, suspension systems, braking components, and driveline parts for Class 4-8 commercial vehicles.

- Recent Developments: In September 2024, ZF Aftermarket presents solutions for a sustainable automotive aftermarket at Automechanika.

- Strategic Focus: ZF Aftermarket is investing in electrification-ready product lines, remanufacturing scale, and digital service tools that provide fleet operators with component health monitoring and planned replacement scheduling.

Market Concentration Analysis

The global heavy-duty automotive aftermarket market exhibits moderate fragmentation at the global level but meaningful concentration within specific product categories and regional markets. The major key players include Genuine Parts Company, Robert Bosch GmbH, ZF Friedrichshafen AG, Tenneco Inc., and Dana Limited.

Independent aftermarket (IAM) channels are steadily gaining share in high-volume, price-sensitive categories, while OEM channels remain dominant in complex, software-integrated, and warranty-linked components where certification and liability matter. Developed markets are consolidating, with scaled players like Genuine Parts Company expanding via acquisitions across North America, Europe, and Asia-Pacific. In contrast, China operates a more fragmented, domestically anchored ecosystem, where local IAM distributors and OEM networks dominate, limiting global consolidation.

Investment & Growth Opportunities

Fastest-Growing Segments

Asia Pacific is the fastest-growing aftermarket region, driven by expanding commercial vehicle parc in China and India. Growth is led by the DIFM (Do-It-For-Me) service channel, which is outpacing DIY and OE seller channels as vehicle electronics and telematics increase servicing complexity. Within parts, emission control components (DPF, SCR, EGR) are among the fastest-growing categories, supported by tightening regulatory norms.

Emerging Market Expansion

India and Southeast Asia are priority expansion markets due to rising fleet sizes and fragmented aftermarket ecosystems. Countries like Vietnam, Indonesia, and Thailand are seeing steady additions to commercial vehicle fleets, creating recurring demand for parts and service. Limited distribution maturity presents early-entry advantages for players investing in local supply chains and brand presence.

Venture and Private Investment Trends

Notable investment activity includes Genuine Parts Company's European distribution acquisitions, ZF's circular economy and remanufacturing capacity investments, and multiple strategic investments in fleet telematics platforms that are increasingly creating closed-loop aftermarket demand generation. Digital parts marketplace start-ups – including Fleetio, PartsTech, and Fullbay – are attracting venture capital investment, reflecting the platform-based disruption opportunity in traditional parts distribution channels.

Future Market Outlook (2026-2034)

The global heavy-duty automotive aftermarket market is projected to deliver consistent compound growth from USD 150.1 Billion in 2025 to USD 195.4 Billion by 2034 at a CAGR of 2.89%, adding approximately USD 45 billion in incremental annual market value across the forecast period. This trajectory is underpinned by structural fleet ageing dynamics in North America and Europe, regulatory compliance requirements creating non-discretionary parts spending, and the digital transformation of fleet management that is increasing the frequency and efficiency of aftermarket service events.

Three structural shifts will reshape the heavy-duty aftermarket through 2034. First, connected vehicle telematics will drive a shift from reactive to predictive maintenance, increasing planned parts replacement cycles. Second, fleet electrification will gradually erode ICE-related demand post-2029 while creating new EV aftermarket segments (battery, motor, high-voltage systems). Third, digital and e-commerce procurement will disrupt distribution, pressuring traditional players and favoring those with integrated digital and logistics capabilities.

By 2034, the aftermarket will be more tech-enabled, digitally transacted, and sustainability-focused, with competitive advantage accruing to players that combine scale, digital platforms, remanufacturing, and multi-powertrain service expertise.

Research Methodology

Primary Research

Primary research included structured interviews with fleet operators, parts distributors, OEM aftermarket leaders, IAM specialists, and industry bodies such as the Heavy Duty Manufacturers Association and Automotive Aftermarket Suppliers Association across major global regions. Insights were used to validate market sizing, segmentation, technology adoption, and competitive positioning.

Secondary Research

Secondary sources include US Federal Motor Carrier Safety Administration (FMCSA) fleet data, Eurostat commercial vehicle registrations, India Ministry of Road Transport and Highways (MoRTH) reports, Heavy Duty Trucking magazine, Commercial Carrier Journal, Transport Topics, IMARC Group commercial telematics market reports, EPA emission regulatory publications, Euro 7 Commission framework documentation, public company annual reports and investor presentations, and industry association publications from ATA, HDMA, CLEPA, and the Aftermarket Auto Parts Alliance.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models. Bottom-up models aggregate demand by vehicle type, parts category, service channel, and region using replacement cycle data, fleet size estimates, and average per-vehicle aftermarket spend. Top-down models incorporate GDP growth rates, freight volume indices, commercial vehicle production data, and historical aftermarket-to-OEM sales ratio evolution. Scenario analysis incorporating fleet electrification acceleration, regulatory tightening intensity, and e-commerce displacement rates was performed to generate base, optimistic, and conservative growth cases.

Heavy-Duty Automotive Aftermarket Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Replacement Parts Covered | Tires, Batteries, Brake Parts, Filters, Body Parts, Lighting and Electronic Components, Wheels, Exhaust Components, Turbochargers, Others |

| Vehicle Types Covered | Class 4 to Class 6, Class 7 and Class 8 |

| Service Channels Covered | DIY, OE Seller, DIFM |

| Regions Covered | North America, Asia-Pacific, Europe, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, China, Japan, India, South Korea, Australia, Indonesia, Germany, France, United Kingdom, Italy, Spain, Russia, Brazil, Mexico |

| Companies Covered | Genuine Parts Company, Robert Bosch GmbH, ZF Friedrichshafen AG, Tenneco Inc., Dana Limited, Continental AG, MAHLE Aftermarket GmbH, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, the heavy-duty automotive aftermarket market forecast, and dynamics of the market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global heavy-duty automotive aftermarket market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the heavy-duty automotive aftermarket industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Heavy-Duty Automotive Aftermarket Market Report

The global heavy-duty automotive aftermarket market was valued at USD 150.1 Billion in 2025.

The market is projected to reach USD 195.4 Billion by 2034, growing at a CAGR of 2.89% during 2026-2034.

Class 7 and Class 8 vehicles lead with a 65.3% share in 2025.

The DIFM (Do-It-For-Me) channel dominates with a 69.1% share in 2025.

North America leads with a 40.5% share in 2025.

Key drivers include aging commercial vehicle fleets (average US Class 8 fleet age above 7 years), rising freight and logistics activity, telematics adoption enabling predictive maintenance, and emission compliance requirements mandating aftertreatment system upgrades.

Asia Pacific is the fastest-growing region at approximately 3.8% CAGR through 2034, fuelled by rapid freight growth in China and India, expanding commercial vehicle fleets, and developing aftermarket distribution networks.

Leading companies include Genuine Parts Company, Robert Bosch GmbH, ZF Friedrichshafen AG, Tenneco Inc., Dana Limited, Continental AG, and MAHLE Aftermarket GmbH.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)