High Purity Alumina Market Size, Share, Trends and Forecast by Purity Level, Production Method, Application, and Region, 2026-2034

High Purity Alumina Market Size, Share, Trends & Forecast (2026-2034)

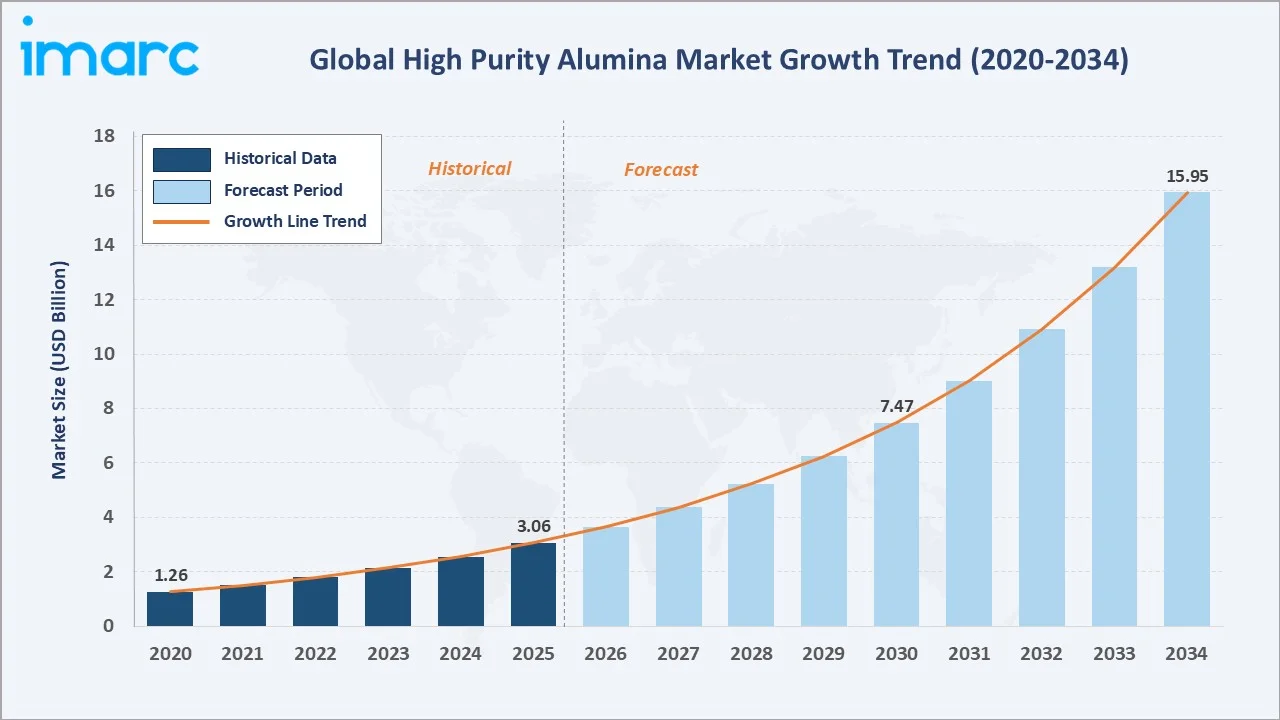

The high purity alumina market was valued at USD 3.06 Billion in 2025 and is projected to reach USD 15.95 Billion by 2034, exhibiting a CAGR of 19.51% during 2026-2034. Rising LED lighting adoption, surging semiconductor fabrication demand, expanding electric vehicle (EV) battery separator applications, and increasing sapphire substrate requirements are the primary drivers shaping the market growth. As per IMARC Group, the global LED lighting market size was valued at USD 97.7 Billion in 2025.

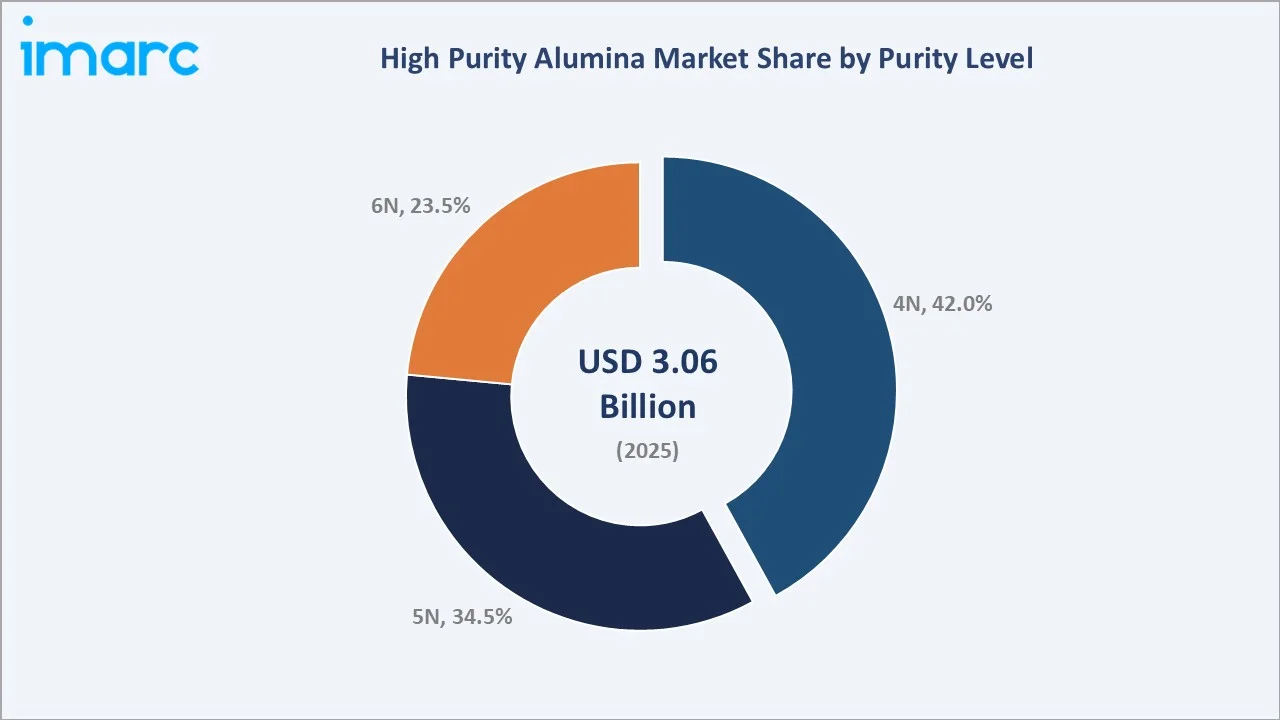

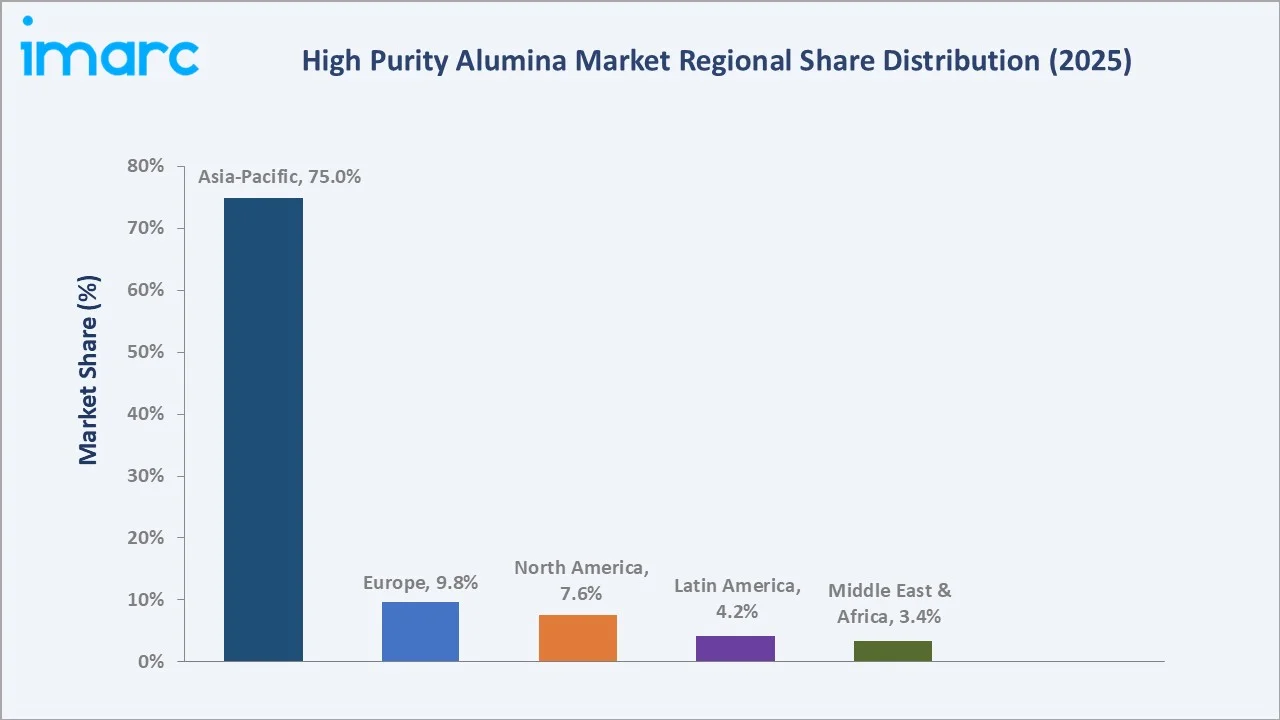

4N leads the purity level segment at 42.0%, LED dominates the application segment at 49.6%, and Asia-Pacific commands 75.0% regional share in 2025.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 3.06 Billion |

|

Forecast Market Size (2034) |

USD 15.95 Billion |

|

CAGR (2026-2034) |

19.51% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Asia-Pacific (75.0%, 2025) |

|

Fastest Growing Region |

North America (7.6%, 2025) |

|

Leading Purity Level |

4N (42.0%, 2025) |

|

Leading Application |

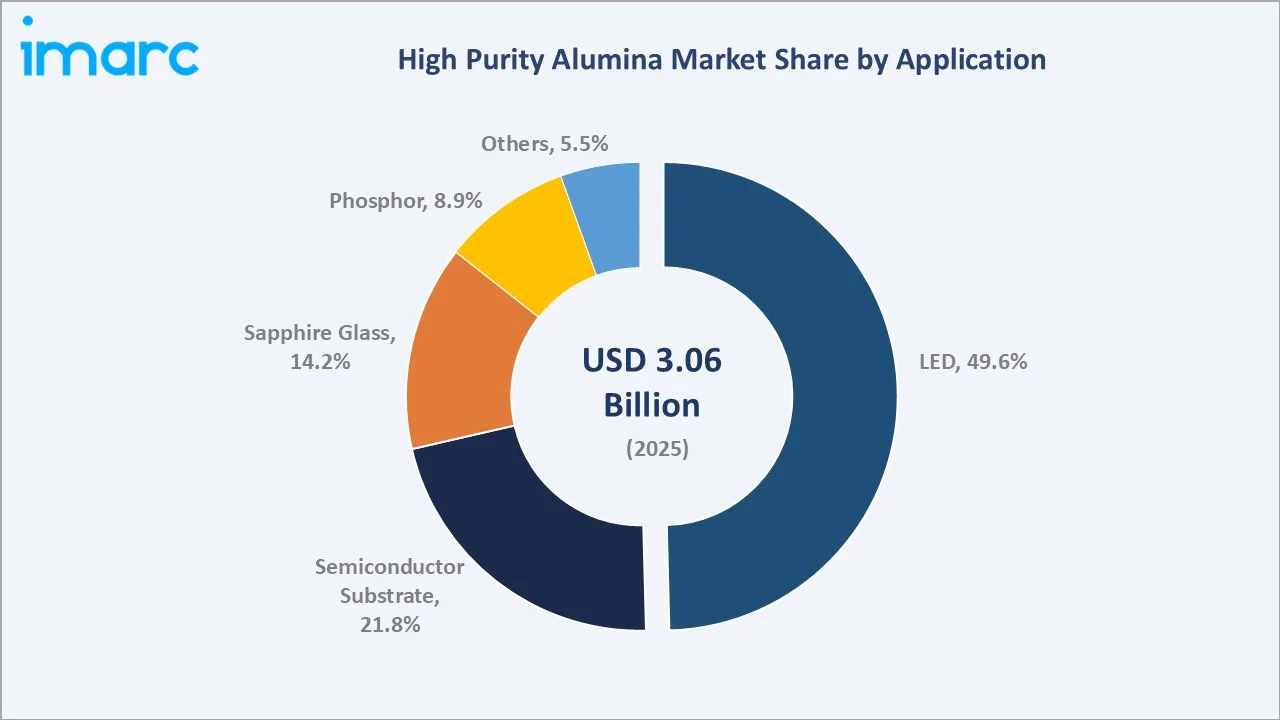

LED (49.6%, 2025) |

The high purity alumina market expanded from USD 1.26 Billion in 2020 to USD 3.06 Billion in 2025, driven by accelerating LED manufacturing, rising semiconductor demand, and growing lithium-ion battery applications. Anchored at USD 7.47 Billion in 2030, the forecast to USD 15.95 Billion by 2034 is supported by expanding EV production and increasing sapphire substrate requirements.

To get more information on this market, Request Sample

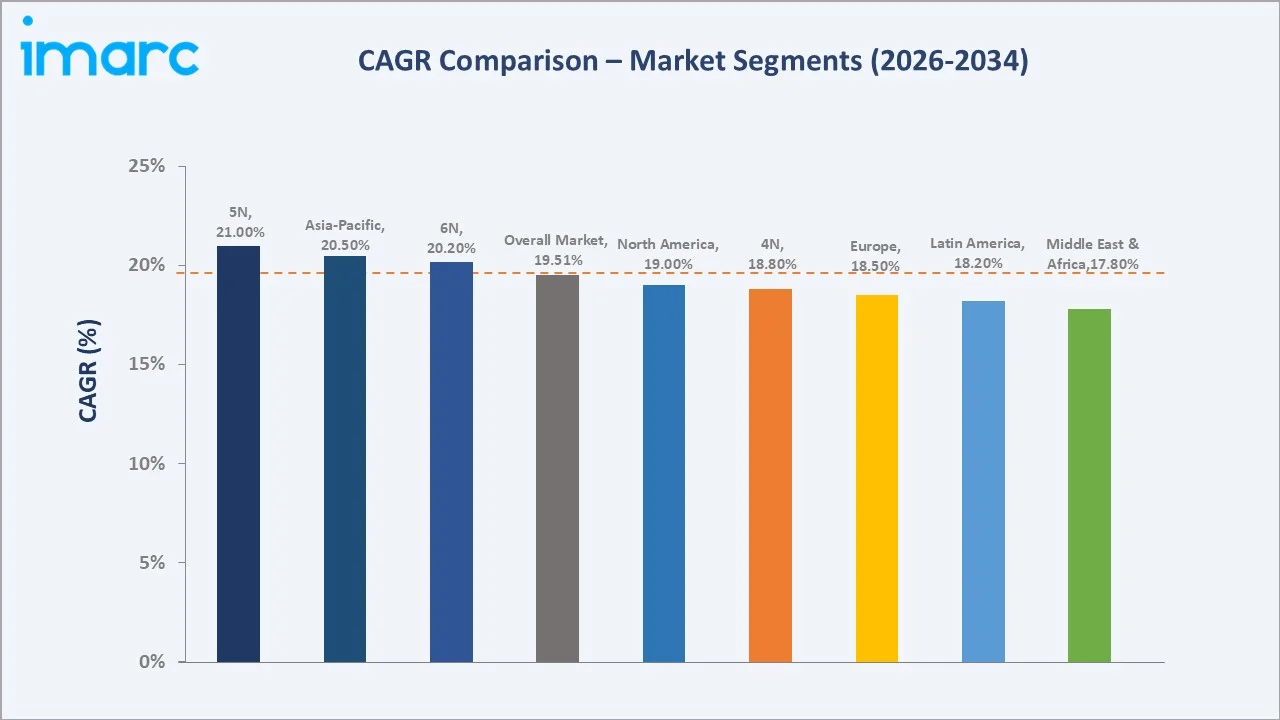

CAGR trajectories across purity level and application sub-segments show 6N and semiconductor substrate expanding faster than the overall 19.51% market CAGR, driven by advanced semiconductor fabrication needs and ultra-high purity requirements for next-generation electronics.

Executive Summary

The high purity alumina market is on a strong growth path from USD 1.26 Billion in 2020 to USD 15.95 Billion by 2034. High purity alumina has evolved from a niche specialty material to a critical enabler across LED lighting, semiconductor fabrication, and EV battery technologies. Falling production costs through advanced purification methods and rising demand for energy-efficient lighting solutions are driving broad-based adoption. Regulatory push toward sustainable manufacturing and clean energy technologies is further accelerating market expansion.

4N dominates the purity level segment at 42.0% in 2025, supported by its widespread use in LED substrates and lithium-ion battery separators. LED commands the application segment at 49.6%, fueled by the global transition from conventional lighting to energy-efficient LED solutions. Asia-Pacific holds 75.0% of the global market, led by China, Japan, and South Korea, driven by established semiconductor manufacturing ecosystems and expanding LED production capacities. In June 2025, Alpha HPA signed a USD 20 Million contract with McCosker Contracting for its Stage 2 high purity alumina plant in Gladstone, Australia, targeting annual output exceeding 10,000 Tons.

Key Market Insights

|

Insight |

Data |

|

Leading Purity Level |

4N - 42.0% share (2025) |

|

Second Purity Level |

5N - 34.5% share (2025) |

|

Leading Application |

LED - 49.6% share (2025) |

|

Second Application |

Semiconductor Substrate - 21.8% share (2025) |

|

Leading Region |

Asia-Pacific - 75.0% share (2025) |

|

Fastest Growing Region |

North America - 7.6% share (2025) |

|

Top Companies |

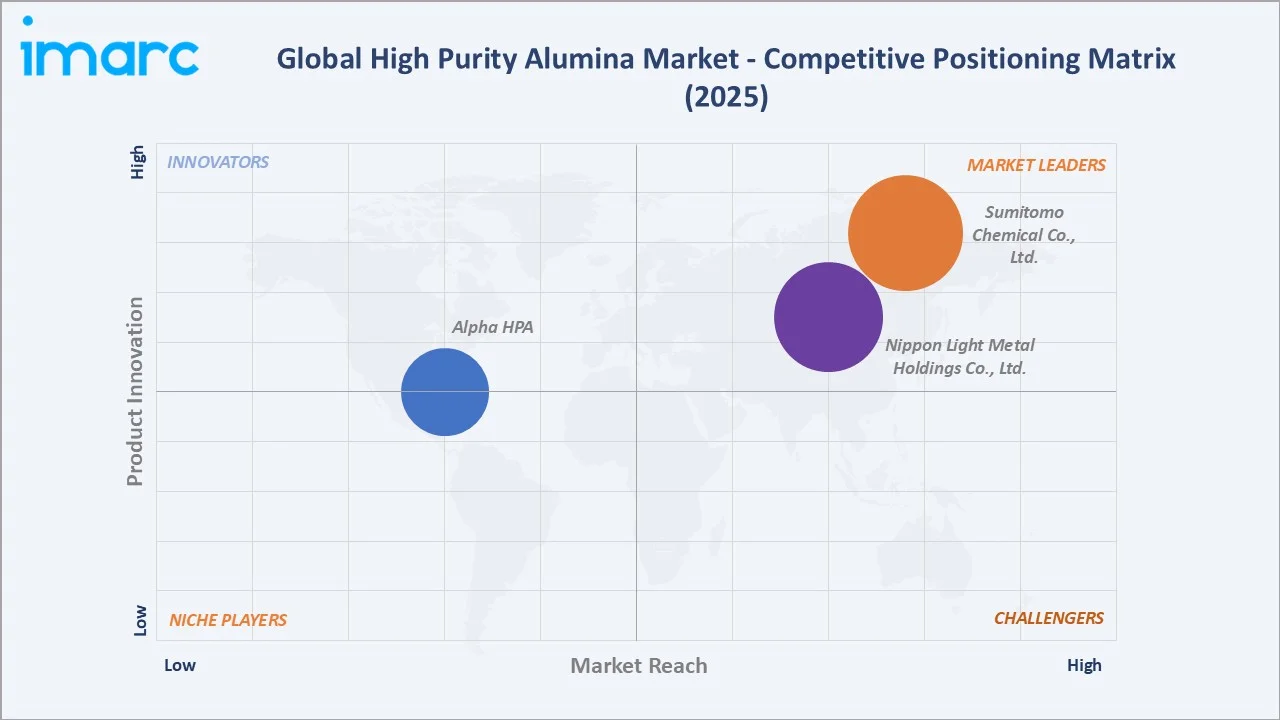

Sumitomo Chemical Co., Ltd., Nippon Light Metal Holdings Co., Ltd., Alpha HPA |

Key Analytical Observations Expanding on the Data Above:

- 4N dominance at 42.0% is driven by its balanced combination of performance and cost-effectiveness, making it the preferred grade for mass-market applications, including LED substrates and lithium-ion battery separator coatings.

- 5N share at 34.5% is sustained by growing demand from semiconductor wafer polishing, advanced ceramic components, and specialty optical applications requiring higher purity specifications.

- LED leadership at 49.6% reflects the global transition to energy-efficient lighting. LED applications consume high purity alumina as a precursor for synthetic sapphire substrates used in chip manufacturing.

- Semiconductor substrate at 21.8% is supported by rising demand for high thermal conductivity and electrically insulating materials used in advanced chip packaging, power electronics, and wafer fabrication processes.

- Asia-Pacific at 75.0% dominates owing to China, Japan, and South Korea hosting large LED manufacturing clusters and semiconductor fabrication facilities. In May 2026, the Indian Union Cabinet, led by Prime Minister Shri Narendra Modi, sanctioned two additional semiconductor initiatives under the India Semiconductor Mission (ISM). Crystal Matrix Limited (CML) plans to create a comprehensive facility for compound semiconductor fabrication and ATMP in Dholera, Gujarat, dedicated to manufacturing Mini/Micro-LED display modules.

High Purity Alumina Market Overview

High purity alumina is an advanced non-metallurgical alumina product with a purity level of at least 99.99%. It serves as a critical precursor material for synthetic sapphire substrates used in LED manufacturing, semiconductor wafer processing, and optical component production.

The global ecosystem integrates bauxite miners, aluminum hydroxide suppliers, high purity alumina refiners using hydrolysis or acid-leaching processes, quality testing laboratories, specialty chemical distributors, and end use manufacturers across the LED, semiconductor, battery, and sapphire glass industries.

Market Dynamics

To evaluate market opportunities, Request Sample

Market Drivers

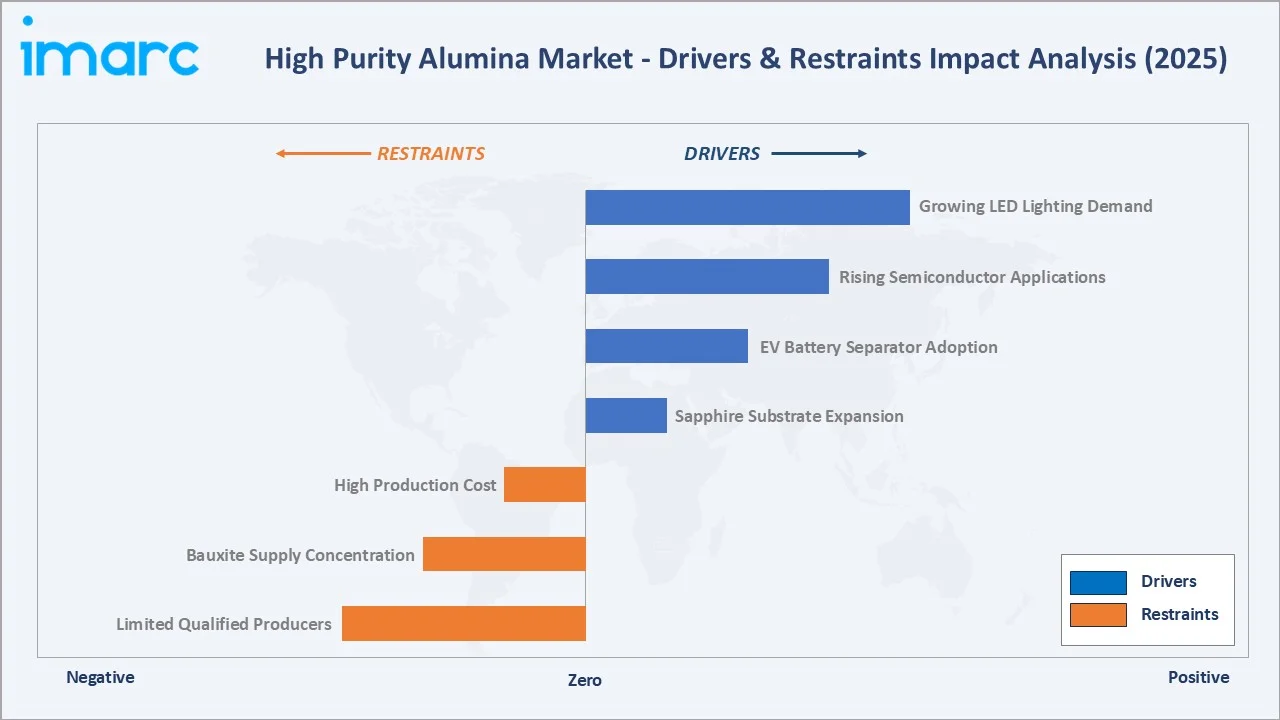

- Growing LED Lighting Demand: The global shift from incandescent and fluorescent lighting to energy-efficient LED solutions is the primary consumption driver for high purity alumina. It serves as the essential precursor for synthetic sapphire substrates used in LED chip manufacturing.

- Rising Semiconductor Applications: Expanding semiconductor fabrication worldwide is increasing demand for 5N and 6N grade high purity alumina used in wafer polishing slurries, plasma-resistant chamber components, and insulating substrates.

- EV Battery Separator Adoption: Lithium-ion batteries used in EVs require high purity alumina-coated separators for thermal runaway prevention. As per IEA, global EV sales surpassed 17 Million units in 2024, directly supporting high purity alumina consumption growth.

- Sapphire Substrate Expansion: Growing demand for scratch-resistant sapphire glass in smartphones, wearable devices, and optical instruments is sustaining strong high purity alumina consumption across consumer electronics.

Market Restraints

- High Production Cost: Manufacturing high purity alumina at 4N-6N grades requires energy-intensive purification processes. Production costs remain significantly higher than standard alumina, limiting adoption in price-sensitive applications and constraining market penetration in emerging economies.

- Bauxite Supply Concentration: Global bauxite reserves are concentrated in a limited number of countries, creating supply chain vulnerability for high purity alumina manufacturers. Geopolitical disruptions and export restrictions in key producing nations pose ongoing risks to feedstock availability and pricing stability.

- Limited Number of Qualified Producers: The market is served by a small number of established producers with proprietary purification technologies. New entrants face multi-year qualification cycles with end users, stringent quality certification requirements, and high capital expenditure barriers that slow supply diversification.

Market Opportunities

- Sustainable Production Technologies: Emerging processes using kaolin clay feedstock and solvent extraction methods are helping reduce the environmental footprint of alumina production. These cleaner technologies are attracting growing interest from clean-energy and advanced materials investors.

- Solid-State Battery Development: The advancement of solid-state battery technologies is expected to create new demand for ultra-high purity alumina as a critical electrolyte and separator material in next-generation energy storage systems.

Market Challenges

- Red Mud Environmental Concerns: Traditional alumina extraction processes generate significant volumes of red mud waste, creating environmental and disposal challenges. Tightening regulations around industrial waste management are increasing compliance costs and limiting capacity expansion in some regions.

- Technology Scalability Barriers: Scaling 5N and 6N production from laboratory to commercial volumes remains technically complex. Maintaining ultra-high purity levels at industrial-scale throughput requires advanced processing technologies and substantial capital investment.

Emerging Market Trends

1. Transition to Hydrochloric Acid Leaching and Solvent Extraction

Traditional hydrolysis methods are increasingly being supplemented by hydrochloric acid leaching and proprietary solvent extraction technologies. These newer processes enable higher yields, lower energy consumption, and reduced waste generation, improving both cost efficiency and environmental compliance across high purity alumina production.

2. Rising Demand for 5N and 6N Ultra-High Purity Grades

Advanced semiconductor fabrication, plasma etching components, and next-generation display technologies are driving a shift toward higher purity grades. Demand for 5N and 6N alumina is expanding, reflecting increasingly stringent purity specifications across high-technology applications.

3. Integration With EV Battery Supply Chain

High purity alumina-coated battery separators have become standard in lithium-ion batteries for EVs, ensuring thermal stability and safety performance. This integration is further strengthening demand for ultra-high purity grades in next-generation battery chemistries.

4. Expansion of Sustainable and Low-Carbon High Purity Alumina Production

Producers are investing in renewable energy-powered facilities, closed-loop chemical recycling, and alternative feedstock sources to minimize environmental impact. These efforts are also helping manufacturers meet tightening ESG and carbon-neutrality requirements across global supply chains.

Industry Value Chain Analysis

The high purity alumina value chain spans six stages from raw material extraction through end use applications. Purification and refining capture the highest value-add, while distribution relationships and quality certification generate downstream competitive advantages in this technology-driven market.

|

Stage |

Key Players / Examples |

|

Raw Material Supply |

Suppliers of bauxite, aluminum hydroxide, kaolin clay, and other alumina precursor materials supporting feedstock production |

|

Purification & Refining |

Facilities operating hydrolysis, hydrochloric acid leaching, and solvent extraction processes to achieve 4N-6N purity levels |

|

High Purity Alumina Manufacturing |

Producers converting refined alumina into powder, tablet, and granular forms tailored to specific application requirements |

|

Quality Control & Certification |

Testing laboratories and standards organizations ensuring purity verification, particle size analysis, and ISO compliance |

|

Distribution & Supply |

Industrial distributors, specialty chemical suppliers, and direct supply agreements connecting manufacturers with end users |

|

End Use Applications |

LED manufacturers, semiconductor fabricators, battery producers, sapphire glass makers, and phosphor producers |

Vertically integrated players with in-house hydrolysis or proprietary solvent extraction technologies achieve stronger cost efficiency and more consistent purity levels compared to manufacturers dependent on externally sourced feedstock.

Technology Landscape in the High Purity Alumina Industry

Purification Process Innovation

Hydrolysis of aluminum alkoxide remains the dominant production method. Hydrochloric acid leaching is gaining traction as an alternative process, offering lower energy consumption and improved compatibility with diverse feedstock sources. Solvent extraction represents the newest commercial technology, enabling near-zero waste production at competitive cost.

Materials and Grade Development

Manufacturers are advancing nano-scale high purity alumina powders with extremely fine primary particle sizes, enabling improved performance in chemical mechanical planarization slurries and LED nanophosphor applications. Alpha-phase and gamma-phase alumina variants are being engineered for specific downstream applications, with bespoke particle sizing and surface area specifications becoming standard.

Sustainable Manufacturing

Green production methods incorporating renewable energy, closed-loop reagent recycling, and alternative feedstocks are emerging as competitive differentiators. Facilities powered by renewable electricity and adopting low-emission processes are setting new benchmarks for environmental performance in the industry.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Purity Level |

4N |

42.0% |

2025 |

|

Production Method |

🔒 |

🔒 |

2025 |

|

Application |

LED |

49.6% |

2025 |

|

Region |

Asia-Pacific |

75.0% |

2025 |

By Purity Level

4N commands a 42.0% majority share in 2025, driven by its balanced performance-to-cost profile that makes it the preferred grade for LED sapphire substrates, lithium-ion battery separator coatings, and standard ceramic applications. This segment benefits from established manufacturing processes and broad industrial acceptance.

To access detailed market analysis, Request Sample

5N at 34.5% in 2025 serves semiconductor wafer polishing, advanced optical components, and specialty electronics requiring higher purity specifications. Demand for this grade is also increasing as chip manufacturing and precision electronics continue to shift toward more advanced process nodes.

By Application

LED commands a 49.6% share in 2025, reflecting the global transition to energy-efficient lighting and the essential role of high purity alumina as a synthetic sapphire substrate precursor. The growing penetration of LED technology across residential, commercial, and industrial settings continues to sustain dominant demand for high purity alumina.

Semiconductor substrate at 21.8% is the second-largest application, driven by expanding global fabrication capacity. Its use is further supported by rising demand for high-performance chips in computing, telecommunications, and consumer electronics.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Asia-Pacific |

75.0% |

Established LED and semiconductor manufacturing ecosystems, expanding EV battery production, and strong government support for advanced materials |

|

Europe |

9.8% |

Stringent environmental regulations, growing focus on sustainability, and investment in clean-technology manufacturing processes |

|

North America |

7.6% |

Rising semiconductor fabrication capacity, expanding EV adoption, and increasing investment in domestic critical mineral processing |

|

Latin America |

4.2% |

Growing electronics manufacturing, expanding industrial applications, and increasing demand for advanced materials across emerging economies |

|

Middle East & Africa |

3.4% |

Rising industrialization, growing electronics assembly operations, and increasing investment in clean energy technologies |

Asia-Pacific at 75.0% in 2025 leads the global market, driven by China, Japan, and South Korea hosting large LED manufacturing clusters, semiconductor fabrication facilities, and lithium-ion battery production lines. Established supply chains and strong government support for advanced electronics manufacturing are further reinforcing regional dominance.

North America at 7.6% represents strong growth potential through 2034. Rising domestic semiconductor manufacturing investment, expanding EV battery production, and increasing government focus on critical mineral supply chain resilience are accelerating regional demand.

Competitive Landscape

The high purity alumina market is moderately concentrated, with established Japanese and European manufacturers leading production capacity while emerging Australian and Chinese producers are scaling through proprietary technologies. Process innovation, purity consistency, and long-term supply agreements form the key competitive moats.

|

Company Name |

Brand / Key Product |

Position |

Strategic Focus |

|

Sumitomo Chemical Co., Ltd. |

AKP-50; ELA Series |

Leader |

Proprietary hydrolysis process; broad product portfolio; strong global distribution |

|

Nippon Light Metal Holdings Co., Ltd. |

High Purity Alumina Powder AHP200D |

Leader |

Refined purification process; LED and semiconductor focus; Japan-based manufacturing |

|

Alpha HPA |

Ultra AAP; Ultra GAP |

Emerging |

Proprietary solvent extraction technology; low-carbon production |

Key players include Sumitomo Chemical Co., Ltd., Nippon Light Metal Holdings Co., Ltd., and Alpha HPA, among others.

Key Company Profiles

Sumitomo Chemical Co., Ltd.

Sumitomo Chemical Co., Ltd. is a leading producer of high purity alumina, leveraging its proprietary hydrolysis of aluminum alkoxide method to manufacture high purity alumina products for LED, semiconductor, and battery applications across multiple continents.

- Product Portfolio: AKP-50 high purity alumina powder for ceramic substrates and sapphire applications; ELA Series low alpha radiation fine spherical alumina for advanced semiconductor packaging.

- Recent Developments: In May 2026, Sumitomo Chemical Co., Ltd. launched the ELA Series of low alpha radiation, high purity fine spherical alumina products, targeting advanced semiconductor packaging applications requiring minimal radiation interference and enhanced heat dissipation.

- Strategic Focus: Proprietary hydrolysis process; broad product portfolio; strong global distribution.

Nippon Light Metal Holdings Co., Ltd.

Nippon Light Metal Holdings Co., Ltd. is a leading Japanese manufacturer of high purity alumina, producing specialized high purity alumina products through refined purification processes for LED, semiconductor, and consumer electronics applications.

- Product Portfolio: High Purity Alumina Powder AHP200D (micrometer-order grain size via spray granulation); high purity aluminum hydroxide for sapphire and electronic material applications.

- Recent Developments: The company has been focusing on improving purification efficiency and strengthening its production capabilities for high purity alumina used in advanced electronic applications. It is also expanding its product development efforts to better serve growing demand from LED, semiconductor, and sapphire substrate markets.

- Strategic Focus: Refined purification process; LED and semiconductor focus; Japan-based manufacturing.

Market Concentration Analysis

The high purity alumina market is moderately concentrated, with the top companies (Sumitomo Chemical Co., Ltd., Nippon Light Metal Holdings Co., Ltd., and Alpha HPA) estimated to hold approximately 50-60% of global production capacity share in 2025.

Barriers to entry include proprietary purification technology development, multi-year quality certification processes, high capital requirements for commercial-scale facilities, and the technical expertise needed to achieve consistent 4N-6N purity levels. These factors favor established producers with deep process knowledge and vertically integrated operations.

Consolidation is accelerating through strategic partnerships, capacity expansion investments, and technology licensing agreements. Scale advantages in production, feedstock sourcing, and quality assurance are further reinforcing the competitive position of leading manufacturers.

Investment & Growth Opportunities

Fastest-Growing Segments

6N at 23.5% is expanding faster than the overall 19.51% market CAGR through 2034, driven by advanced semiconductor fabrication and ultra-high purity requirements. Semiconductor substrate at 21.8% is the fastest-growing application as global chip manufacturing capacity scales upward.

Emerging Markets

North America at 7.6% represents the highest relative growth opportunity as the United States invests in domestic semiconductor manufacturing and critical mineral processing. India, Vietnam, and Southeast Asian economies are attracting high purity alumina demand through expanding electronics manufacturing and growing LED adoption.

Venture & Investment Trends

Investment activity is concentrated in sustainable production technologies, 5N-6N capacity expansion in Australia and North America, EV battery separator coating applications, and solid-state battery research. Government-backed critical mineral initiatives in Australia, the United States, and the European Union are providing additional capital and policy support for high purity alumina industry growth.

Future Market Outlook (2026-2034)

The high purity alumina market is forecast to expand from USD 3.06 Billion in 2025 to USD 15.95 Billion by 2034 at a CAGR of 19.51%, adding roughly USD 12.89 Billion in incremental market value over the forecast period.

Four forces will shape the market through 2034: LED lighting penetration deepening globally; semiconductor fabrication capacity doubling in key regions; EV battery production requiring high purity alumina-coated separators at scale; and solid-state battery commercialization creating new ultra-high purity demand.

By 2034, high purity alumina will be embedded across the entire advanced electronics value chain. Sustainable production methods using solvent extraction and renewable energy will become the manufacturing standard, with 5N and 6N grades collectively capturing a growing share of total market revenue.

Research Methodology

Primary Research

Primary research included interviews with senior production managers at leading high purity alumina manufacturers, LED and semiconductor industry executives, battery separator specialists, and raw material procurement professionals, validating market sizing, regional demand patterns, purity-grade splits, and application-mix evolution.

Secondary Research

Secondary sources included USGS Mineral Commodity Summaries, industry white papers on LED and semiconductor trends, corporate annual reports, investor presentations, press releases from listed manufacturers, and patent filings related to high purity alumina purification technologies.

Forecasting Models

Market forecasts used top-down and bottom-up models combining LED production volumes, semiconductor fabrication capacity additions, EV battery production forecasts, high purity alumina consumption intensity per application, and regional production capacity pipelines.

High Purity Alumina Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Purity Levels Covered | 4N, 5N, 6N |

| Production Methods Covered | Hydrolysis of Aluminium Alkoxide, Hydrochloric Acid Leaching, Others |

| Applications Covered | LED, Semiconductor Substrate, Phosphor, Sapphire Glass, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Sumitomo Chemical Co., Ltd., Nippon Light Metal Holdings Co., Ltd., Alpha HPA, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the high purity alumina market from 2020-2034.

- The high purity alumina market research report provides the latest information on the market drivers, challenges, and opportunities in the global market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the high purity alumina industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the High Purity Alumina Market Report

The global market was valued at USD 3.06 Billion in 2025, driven by LED lighting demand, semiconductor applications, and battery separator adoption.

The market is projected to grow at 19.51% CAGR from 2026 to 2034, reaching USD 15.95 Billion, supported by expanding electronics manufacturing.

4N leads at 42.0% in 2025, driven by LED substrate and battery separator demand. 6N at 23.5% is the fastest-growing purity segment.

LED dominates at 49.6% in 2025, driven by the global shift to energy-efficient lighting. Semiconductor substrate at 21.8% is the second largest.

Asia-Pacific commands 75.0% in 2025, led by China, Japan, and South Korea. North America at 7.6% represents strong growth potential through 2034.

Leading players include Sumitomo Chemical Co., Ltd., Nippon Light Metal Holdings Co., Ltd., and Alpha HPA.

High purity alumina-coated separators in lithium-ion batteries prevent thermal runaway and improve safety. Rising global EV production directly increases high purity alumina consumption.

Key methods include hydrolysis of aluminum alkoxide, hydrochloric acid leaching, and solvent extraction. Hydrolysis remains the dominant commercial process.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade