Hospital Linen Supply and Management Services Market Size, Share, Trends and Forecast by Product, Material, Service Provider, End Use, and Region, 2026-2034

Hospital Linen Supply and Management Services Market Size, Share, Trends & Forecast (2026-2034)

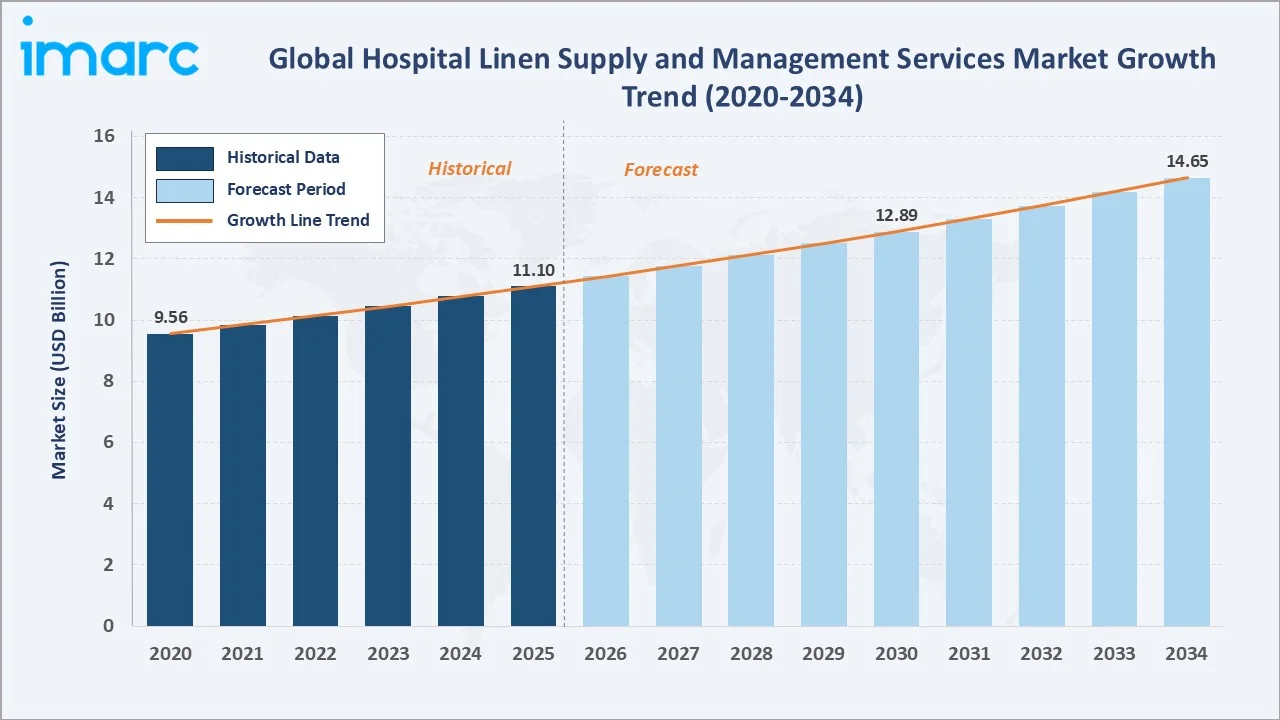

The hospital linen supply and management services market was valued at USD 11.10 Billion in 2025 and is projected to reach USD 14.65 Billion by 2034, exhibiting a CAGR of 3.04% during 2026-2034. Rising hospital admissions, stricter infection-control protocols, and growing outsourcing of healthcare laundry are the primary drivers shaping market expansion. In May 2026, Healthcare Linen Services Group acquired Texas Textile Services, expanding its outsourced hospital laundry network.

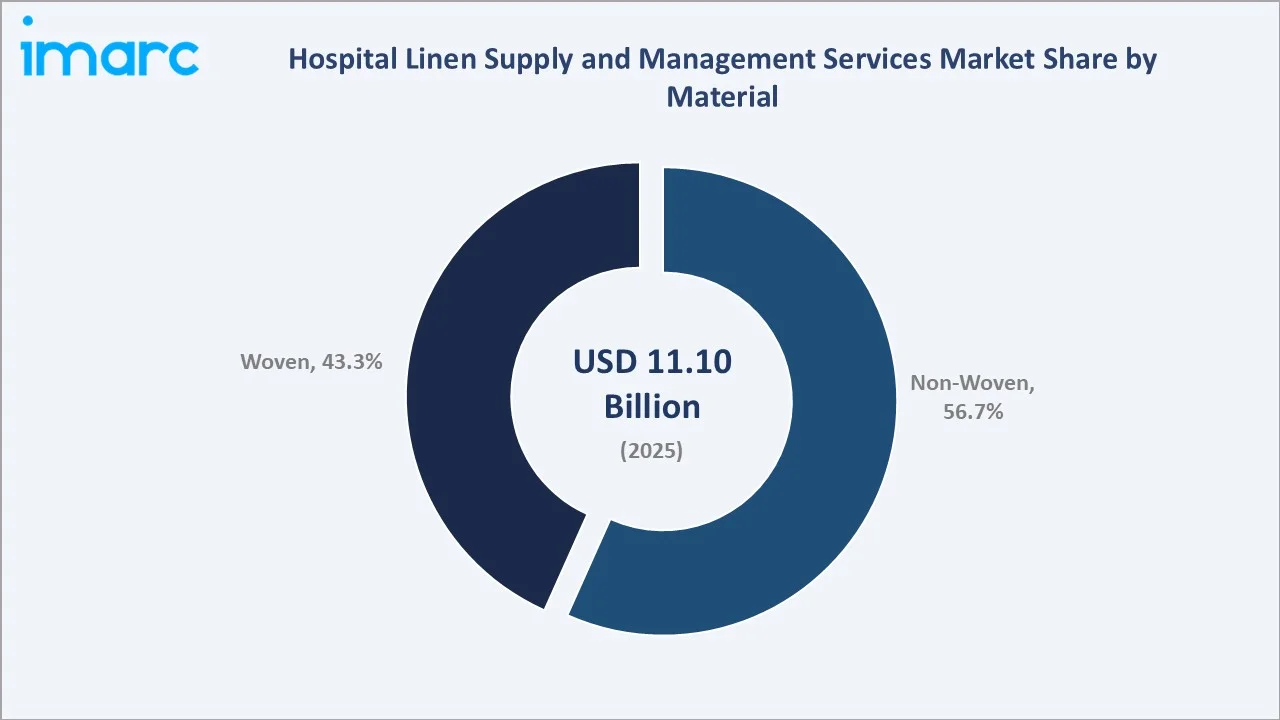

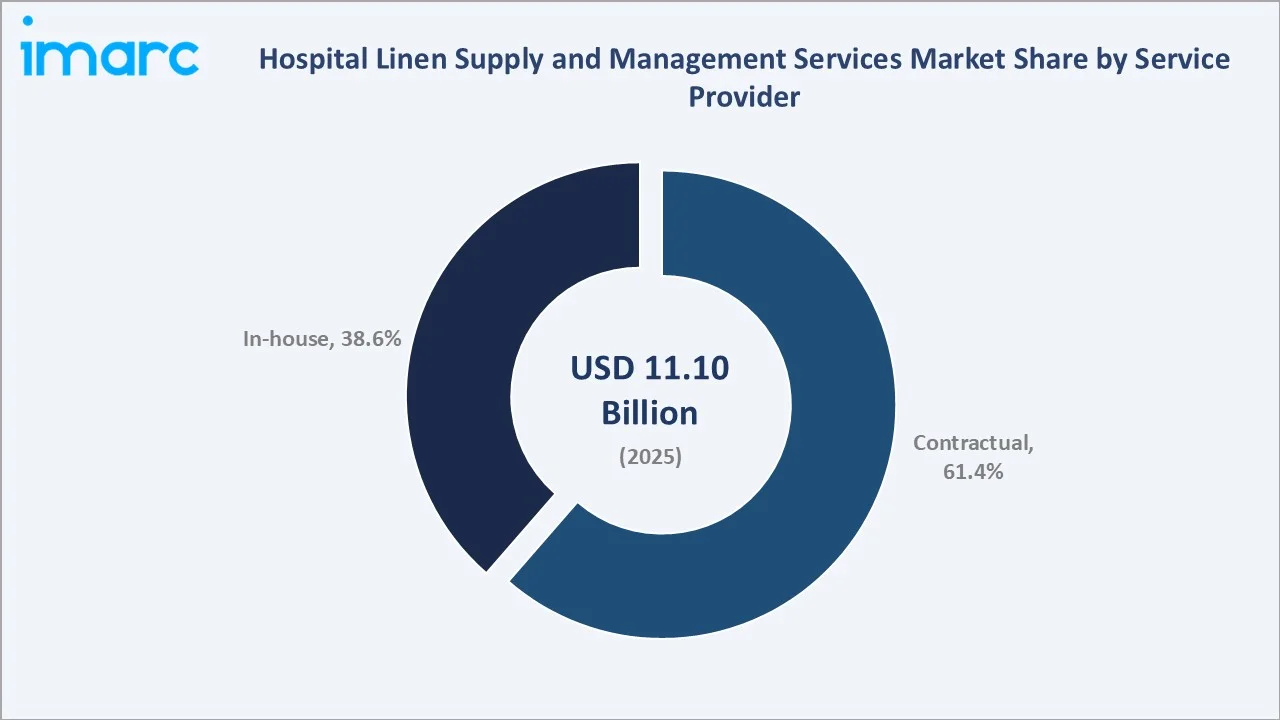

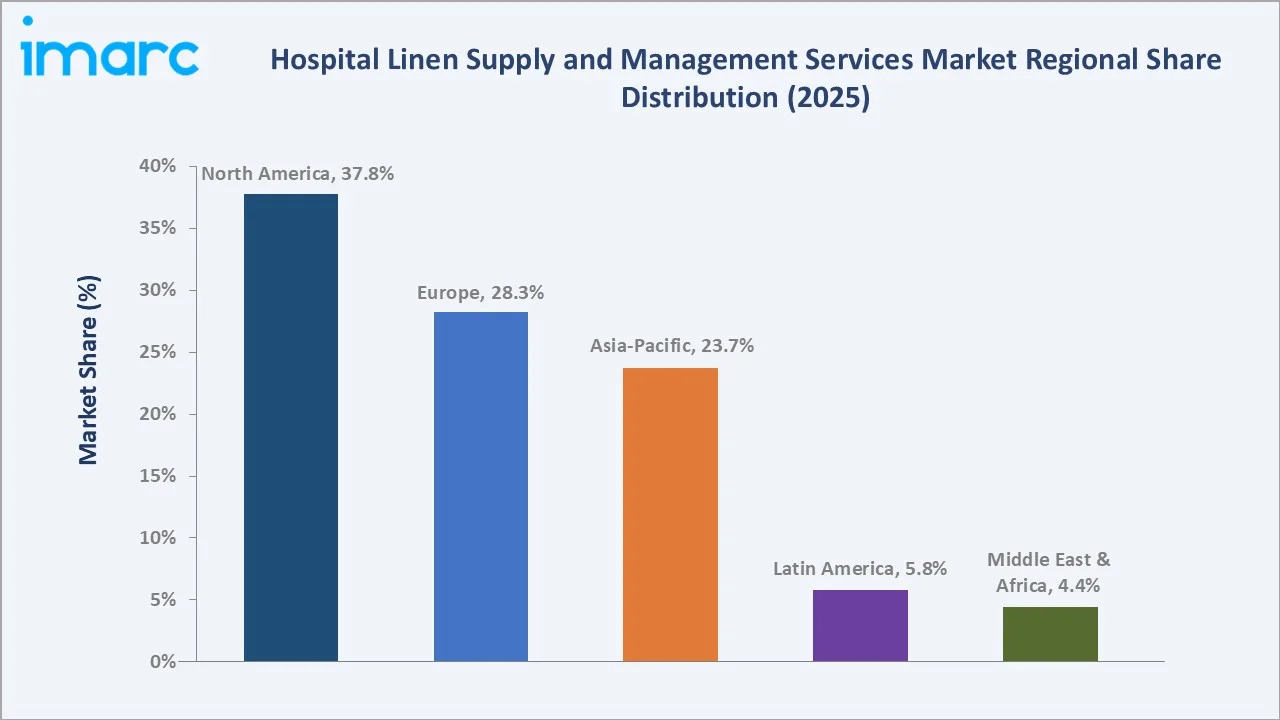

Non-woven leads the material segment at 56.7%, contractual dominates the service provider segment at 61.4%, and North America commands 37.8% regional share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 11.10 Billion |

|

Forecast Market Size (2034) |

USD 14.65 Billion |

|

CAGR (2026-2034) |

3.04% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North America (37.8%, 2025) |

|

Fastest Growing Region |

Asia-Pacific (23.7%, 2025) |

|

Leading Material |

Non-Woven (56.7%, 2025) |

|

Leading Service Provider |

Contractual (61.4%, 2025) |

The hospital linen supply and management services market expanded from USD 9.56 Billion in 2020 to USD 11.10 Billion in 2025, supported by rising patient volumes, infection-control needs, and a steady shift toward outsourced laundry. Anchored at USD 12.89 Billion in 2030, the forecast to USD 14.65 Billion by 2034 reflects sustained demand for hygienically processed healthcare textiles.

To get more information on this market, Request Sample

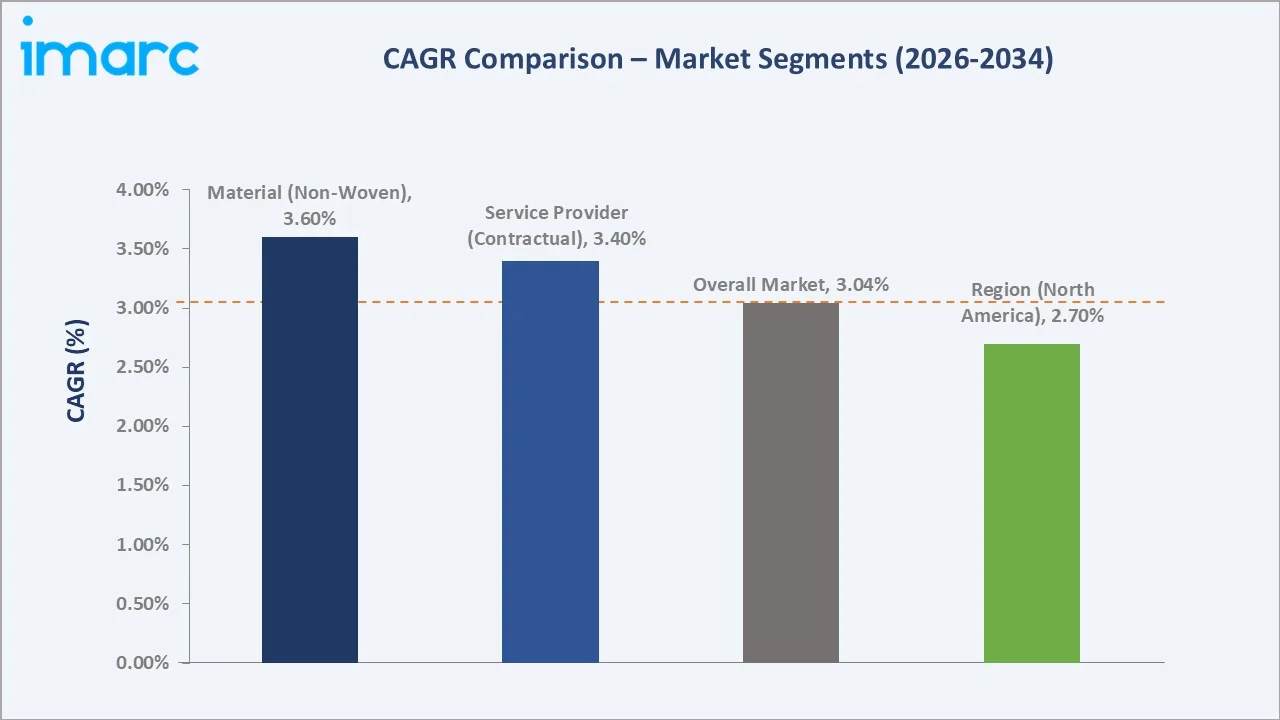

CAGR trajectories across material and service provider sub-segments show non-woven and contractual expanding faster than the overall 3.04% market CAGR, driven by single-use infection-control demand and the move to managed laundry programs.

Executive Summary

The hospital linen supply and management services market is on a steady growth path from USD 9.56 Billion in 2020 to USD 14.65 Billion by 2034. Hospital linen has shifted from a back-office function to a managed service tied to patient safety. Reliable supply of clean bed linen, gowns, and surgical textiles supports infection prevention and smooth clinical operations. Aging population and rising surgical volumes are sustaining demand worldwide.

Non-woven dominates the material segment at 56.7% in 2025, supported by single-use drapes and gowns that simplify infection control. Contractual leads the service provider segment at 61.4%, fueled by hospitals outsourcing laundry to specialized, accredited operators. North America commands 37.8%, led by the United States, on the back of mature outsourcing and strict accreditation. According to the American Hospital Association, as of January 2026, there were 6,100 hospitals in the United States, providing a large installed base of facilities that anchors North American demand for managed linen services.

Key Market Insights

|

Insight |

Data |

|

Leading Material |

Non-Woven - 56.7% share (2025) |

|

Second Material |

Woven - 43.3% share (2025) |

|

Leading Service Provider |

Contractual - 61.4% share (2025) |

|

Second Service Provider |

In-house - 38.6% share (2025) |

|

Leading Region |

North America - 37.8% share (2025) |

|

Fastest Growing Region |

Asia-Pacific - 23.7% share (2025) |

|

Top Companies |

Vestis, Cintas Corporation, Alsco Inc., Unitex Healthcare Laundry Services, Inc. |

Key Analytical Observations Expanding on the Data Above:

- Non-woven leadership at 56.7% is driven by single-use surgical drapes, gowns, and procedure packs that remove laundering from operating-room schedules and lower cross-contamination risk in high-acuity settings.

- Woven share at 43.3% remains essential for reusable bed linen, towels, and patient gowns, where comfort, durability, and lower cost per use keep cotton and blended textiles central to daily ward operations.

- Contractual leadership at 61.4% reflects hospitals shifting laundry to accredited third-party operators to cut capital outlay, ensure compliance, and free clinical staff, while also enabling scalable service capacity across multi-facility healthcare networks.

- In-house share at 38.6% persists in large hospital systems and regions where on-premises laundries offer control over turnaround, specialty textiles, and supply security despite higher fixed costs.

- North America at 37.8% dominates owing to high outsourcing penetration, established accreditation frameworks, and a dense network of specialized healthcare laundries across the United States and Canada. The United States hospital spending reached about USD 1,634.7 Billion in 2024, per the Centers for Medicare & Medicaid Services, reflecting the scale of the regional healthcare base that drives linen demand.

Hospital Linen Supply and Management Services Market Overview

Hospital linen supply and management services cover the sourcing, laundering, distribution, and inventory control of healthcare textiles, including bed linen, towels, patient gowns, scrubs, and surgical drapes used across care settings.

The ecosystem integrates textile and fiber suppliers, linen and apparel manufacturers, commercial healthcare laundries, accreditation bodies, logistics providers, and end users, such as hospitals and long-term care facilities, together ensuring a reliable flow of hygienically clean textiles aligned with infection-control standards.

Market Dynamics

To evaluate market opportunities, Request Sample

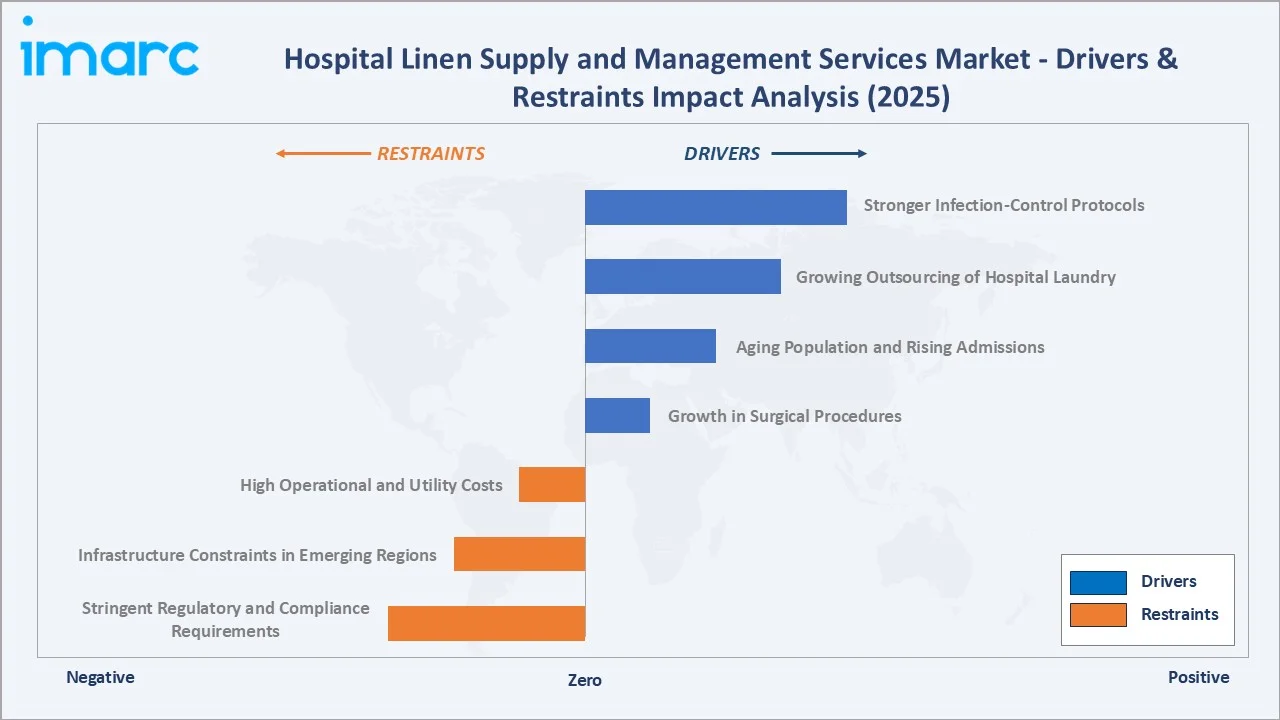

Market Drivers

- Stronger Infection-Control Protocols: Heightened focus on healthcare-associated infection prevention is increasing demand for hygienically processed and accredited linen across hospitals, surgical centers, and clinics.

- Growing Outsourcing of Hospital Laundry: Hospitals are shifting from on-premises laundries to specialized service providers to reduce capital costs, ensure compliance, and improve linen availability and turnaround.

- Aging Population and Rising Admissions: An expanding elderly population and longer inpatient stays are lifting bed occupancy and linen-change frequency, driving sustained textile throughput across care facilities. As per PIB, the elderly population in India is expected to rise to approximately 230 Million by 2036, constituting roughly 15% of the overall population.

- Growth in Surgical Procedures: Rising volumes of surgical procedures worldwide are increasing demand for surgical drapes, gowns, and procedure packs across hospitals and operating rooms.

Market Restraints

- High Operational and Utility Costs: Commercial laundering is water-, energy-, and labor-intensive, and rising utility prices compress operator margins, constraining adoption in cost-sensitive markets and smaller facilities.

- Infrastructure Constraints in Emerging Regions: Based on the findings of the WHO/UNICEF Joint Monitoring Programme (JMP), as of 2023, more than one-third of health care facilities in fragile contexts—37%—were without essential water services, while over half (54%) lacked fundamental hygiene. These deficiencies limit reliable laundry infrastructure and hinder the adoption of outsourced linen management services across parts of Asia, Africa, and Latin America.

- Stringent Regulatory and Compliance Requirements: Healthcare linen providers must comply with strict infection-control, sanitation, and occupational safety standards, increasing operational complexity and compliance-related costs for service operators.

Market Opportunities

- Outsourcing in Emerging Markets: Rising hospital construction and bed capacity across Asia-Pacific, Latin America, and the Middle East and Africa are opening large opportunities for accredited managed-linen programs.

- Technology-Enabled Linen Management: RFID tracking, data dashboards, and automated inventory systems are creating value through loss reduction, utilization analytics, and transparent, usage-based billing for healthcare clients.

Market Challenges

- Linen Loss and Inventory Shrinkage: High rates of misplaced, discarded, or off-site linen erode profitability and complicate par-level management for both providers and hospital customers.

- Workforce Shortages in Laundry Operations: Persistent labor shortages and turnover in processing facilities raise wage pressure and threaten consistent service levels across the industry.

Emerging Market Trends

1. RFID-Enabled Linen Tracking and Inventory Analytics

Radio-frequency identification tags are increasingly embedded in healthcare textiles to track usage, location, and wash cycles. This shift reduces linen loss, supports accurate par levels, and enables usage-based billing and data-driven utilization programs for hospitals.

2. Shift Toward Reusable Surgical Textiles

Reusable surgical gowns and drapes are gaining traction as hospitals increasingly balance cost efficiency and sustainability objectives against reliance on single-use products. Growing emphasis on waste reduction and resource conservation is strengthening the adoption of managed reusable textile programs across healthcare facilities.

3. Sustainability and Circular Textile Programs

Operators are adopting low-temperature and ozone wash processes, water-recovery systems, and end-of-life textile recycling. These initiatives lower environmental impact, support hospital sustainability targets, and respond to tightening effluent and emissions regulations across major markets.

4. Automation and Digital Service Platforms

Automated sorting, robotic handling, and cloud-based customer portals are streamlining laundry operations. Digital platforms give hospitals real-time visibility into deliveries, inventory, and billing, improving transparency and supporting consistent service across multi-site networks.

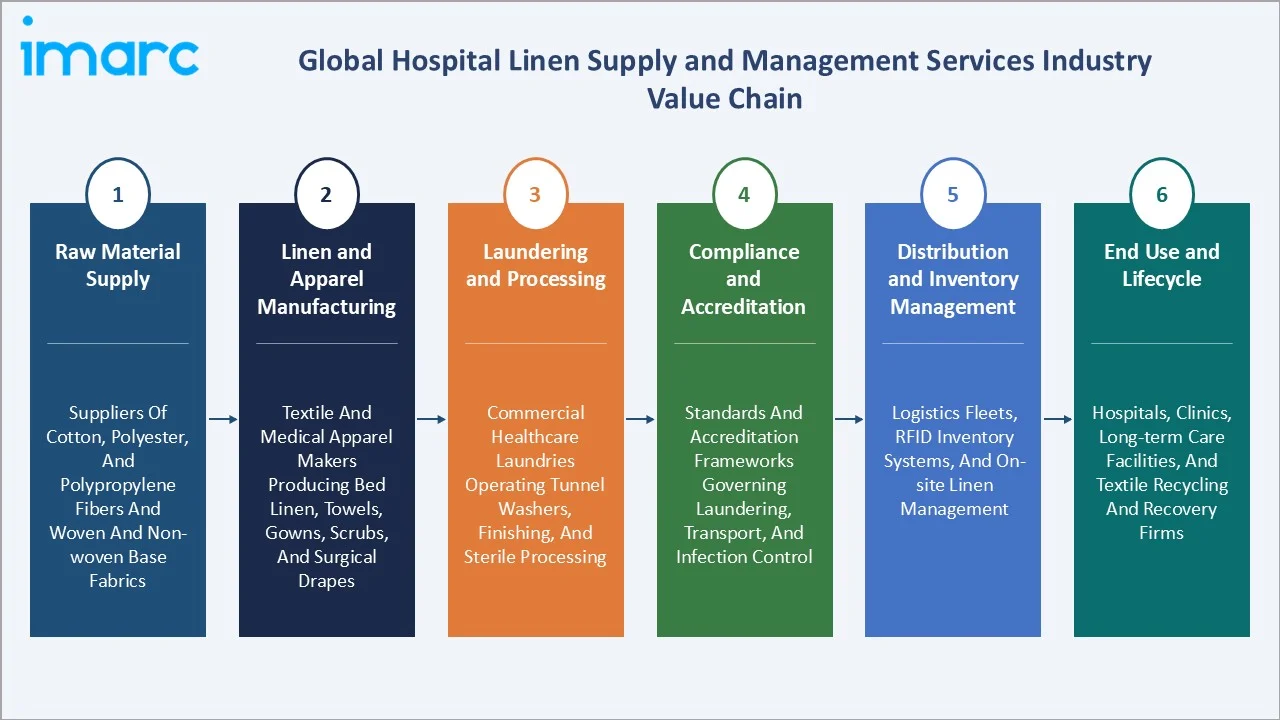

Industry Value Chain Analysis

The hospital linen value chain spans six stages from textile supply through end-of-life recovery. Laundering, processing, and accredited service delivery capture the highest value-add, while inventory management and customer relationships generate downstream competitive advantage in this compliance-driven category.

|

Stage |

Key Players / Examples |

|

Raw Material Supply |

Suppliers of cotton, polyester, and polypropylene fibers and woven and non-woven base fabrics used for healthcare textiles |

|

Linen and Apparel Manufacturing |

Textile and medical apparel makers producing bed linen, towels, gowns, scrubs, and surgical drapes to clinical specifications |

|

Laundering and Processing |

Commercial healthcare laundries operating tunnel washers, finishing, and sterile processing under hygiene-controlled conditions |

|

Compliance and Accreditation |

Standards and accreditation frameworks governing laundering, transport, and infection control for healthcare textiles |

|

Distribution and Inventory Management |

Logistics fleets, RFID inventory systems, and on-site linen management supporting reliable, par-based delivery |

|

End Use and Lifecycle |

Hospitals, clinics, long-term care facilities, and textile recycling and recovery firms |

Vertically integrated operators that combine textile sourcing, laundering, and on-site linen management achieve stronger cost control and supply security than firms relying on fragmented, single-stage offerings.

Technology Landscape in the Hospital Linen Supply and Management Services Industry

RFID and Inventory Tracking

RFID tags and reader gateways allow operators to track each textile across wash cycles, deliveries, and facility zones. This technology reduces shrinkage, supports accurate par levels, and enables transparent, usage-based billing for hospital customers.

Wash Process and Water-Recovery Innovation

Tunnel washers, low-temperature chemistries, and ozone disinfection improve hygiene outcomes while cutting water and energy use. Closed-loop water-recovery systems further reduce consumption and help operators meet tightening effluent and sustainability requirements.

Automation and Digital Platforms

Automated sorting, folding, and robotic handling raise throughput and consistency in large processing plants. Cloud-based portals give hospitals real-time visibility into inventory, deliveries, and compliance, supporting coordinated service across multi-site healthcare networks.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product |

🔒 |

🔒 |

2025 |

|

Material |

Non-Woven |

56.7% |

2025 |

|

Service Provider |

Contractual |

61.4% |

2025 |

|

End Use |

🔒 |

🔒 |

2025 |

|

Region |

North America |

37.8% |

2025 |

By Material

Non-woven commands a 56.7% majority share in 2025, driven by single-use surgical drapes, gowns, and procedure packs that remove laundering from operating-room workflows and lower cross-contamination risk in high-acuity care.

To access detailed market analysis, Request Sample

Woven at 43.3% in 2025 remains essential for reusable bed linen, towels, and patient gowns, where comfort, moisture absorption, and durability sustain demand for cotton and blended textiles across daily ward use.

By Service Provider

Contractual dominates with 61.4% share in 2025, reflecting hospitals outsourcing laundry to accredited specialists to reduce capital investment, ensure compliance, and improve linen availability. This model lets clinical teams focus on patient care while operators manage processing, logistics, and inventory at scale.

In-house at 38.6% in 2025 persists across large hospital systems that maintain on-premises laundries for direct control over turnaround, specialty textiles, and supply security, despite higher fixed and utility costs.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

North America |

37.8% |

High outsourcing penetration, established accreditation frameworks, and strong infection-control standards across acute and long-term care settings |

|

Europe |

28.3% |

Mature healthcare systems, stringent sustainability mandates, and growing adoption of reusable, low-impact textile programs |

|

Asia-Pacific |

23.7% |

Rapid hospital construction, expanding bed capacity, rising healthcare spending, and increasing adoption of outsourced laundry services |

|

Latin America |

5.8% |

Growing private healthcare investment, rising hygiene awareness, and gradual shift toward professional managed-linen programs |

|

Middle East and Africa |

4.4% |

Expanding hospital infrastructure, medical-tourism growth, and increasing focus on accredited infection-control practices |

North America at 37.8% in 2025 leads the global market, supported by deep outsourcing penetration, dense networks of specialized healthcare laundries, and well-established accreditation frameworks. Mature procurement structures and strict hygiene standards continue to anchor demand across the United States and Canada.

Asia-Pacific at 23.7% in 2025 is the highest-growth region through 2034. Rapid hospital construction, expanding bed capacity, and rising healthcare spending are accelerating the shift toward outsourced, accredited linen management across the region.

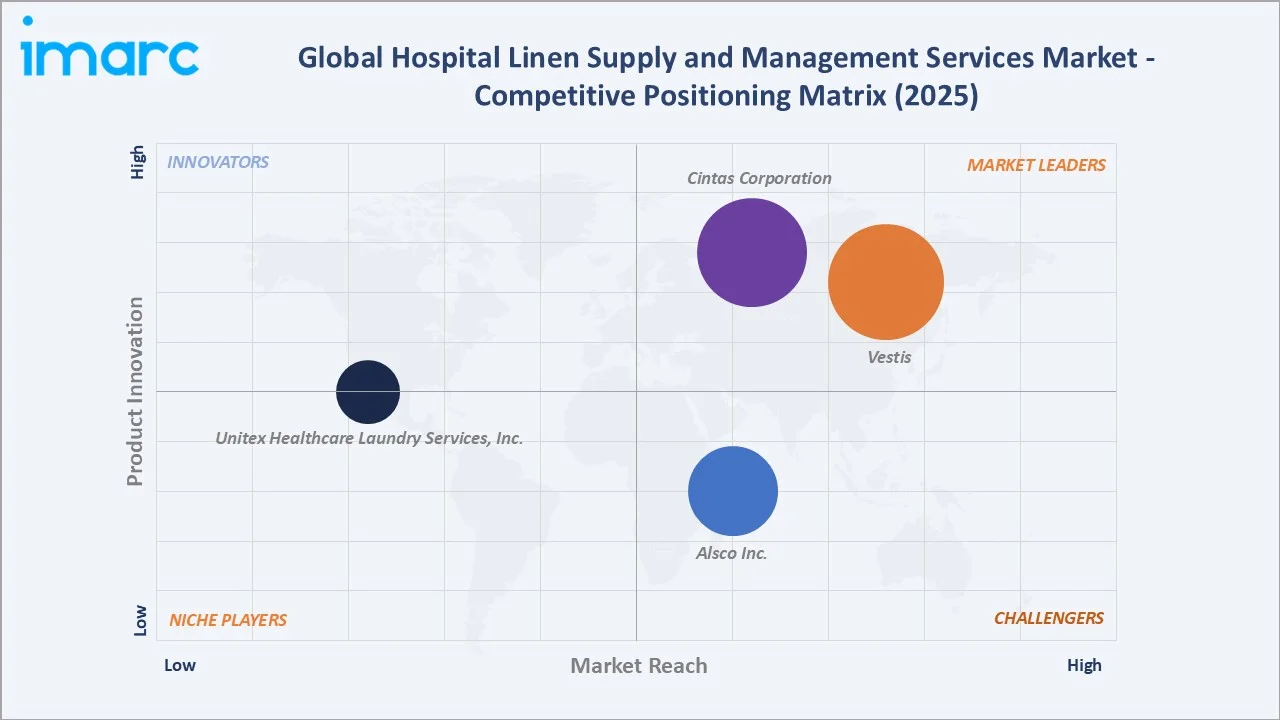

Competitive Landscape

The hospital linen supply and management services market is moderately fragmented, with large multi-country operators competing alongside regional and specialist healthcare laundries. Accreditation, plant network density, and service reliability form the key competitive moats.

|

Company Name |

Brand / Key Product |

Position |

Strategic Focus |

|

Vestis |

Vestis Unisex Scrub Top, Vestis Unisex Scrub Pant, Vestis Women’s Tunic Scrub Top, Vestis Warm Up Scrub Jacket |

Leader |

Route-based service network and bundled rental programs |

|

Cintas Corporation |

Garment Dispensing Solutions, Non-Surgical Isolation Gowns |

Leader |

Dense distribution routes and integrated facility services |

|

Alsco Inc. |

Alsco Uniforms |

Challenger |

Hygienic processing standards and broad regional coverage |

|

Unitex Healthcare Laundry Services, Inc. |

Patient Linen and Apparel (Cardiology Capes, Patient Gowns, Pillowcase Services) |

Emerging |

Family-owned regional healthcare specialization |

Key players include Vestis, Cintas Corporation, Alsco Inc., and Unitex Healthcare Laundry Services, Inc., among others.

Key Company Profiles

Vestis

Vestis is a leading provider of uniform rentals and workplace supplies, serving healthcare facilities with scrubs, linens, gowns, and managed laundering services. The company supports hospitals and clinical facilities through integrated textile management, inventory control, and hygiene-focused service solutions.

- Product Portfolio: Vestis Unisex Scrub Top, Vestis Unisex Scrub Pant, Vestis Women's Tunic Scrub Top, and Vestis Warm Up Scrub Jacket.

- Recent Developments: Vestis continues to strengthen its healthcare service portfolio through investments in textile management capabilities, route optimization, and customer-focused rental and laundering solutions across hospital and clinical settings.

- Strategic Focus: Route-based service network and bundled rental programs.

Cintas Corporation

Cintas Corporation is a major North American provider of uniform and facility services, supplying healthcare clients with apparel, linens, and related laundering and supply programs through an extensive route network.

- Product Portfolio: Garment dispensing solutions, non-surgical isolation gowns, scrub rental, privacy curtain service, towels and linens, and managed rental and laundering services for healthcare facilities.

- Recent Developments: In March 2026, Cintas Corporation entered into a definitive agreement to acquire UniFirst Corporation in a transaction valued at approximately USD 5.5 Billion, expected to close in the second half of 2026, subject to regulatory and shareholder approvals.

- Strategic Focus: Dense distribution routes and integrated facility services.

Alsco Inc.

Alsco Inc. is a privately held provider of uniform and linen rental and laundering services with more than 135 years of operating history, serving healthcare facilities across several regions. The company offers healthcare textile solutions, including patient linens, staff apparel, floor care products, and infection-control-focused laundry services.

- Product Portfolio: Healthcare linen rental and laundering under Alsco Uniforms, including operating-room towels, surgical drapes and wrappers, thermal and bath blankets, patient gowns, scrubs, and bedding.

- Recent Developments: Alsco Inc. continues to expand its healthcare linen and uniform service capabilities through ongoing investments in hygienic processing technologies, regional service infrastructure, and sustainable laundry operations.

- Strategic Focus: Hygienic processing standards and broad regional coverage.

Market Concentration Analysis

The hospital linen supply and management services market is moderately fragmented. A handful of large multi-country and national operators hold significant share, while numerous regional and specialist healthcare laundries serve local hospital networks and care facilities.

Barriers to entry include accreditation requirements such as HLAC and TRSA Hygienically Clean certification, capital-intensive processing plants, and the route density and service reliability needed to win multi-site hospital contracts, favoring well-capitalized operators with established networks.

Consolidation is accelerating through acquisitions of regional laundries, plant network expansion, and bundling of linen with broader facility services. Scale advantages in processing, logistics, and compliance continue to reinforce the position of established providers.

Investment & Growth Opportunities

Fastest-Growing Segments

Non-woven at 56.7% expands faster than the overall 3.04% market CAGR through 2034, driven by single-use infection-control demand. Contractual at 61.4% is the fastest-growing service provider as hospitals continue shifting laundry to accredited operators.

Emerging Markets

Asia-Pacific at 23.7% is the highest-growth region, led by rapid hospital construction and expanding bed capacity. Latin America and the Middle East and Africa represent sizeable untapped opportunities as outsourcing penetration rises from a low base.

Venture & Investment Trends

Investment is concentrated in plant modernization, RFID and inventory technology, water-recovery and energy-efficient processing, and acquisitions of regional laundries. Capital is also flowing into digital service platforms that improve transparency and multi-site coordination.

Future Market Outlook (2026-2034)

The hospital linen supply and management services market is forecast to expand from USD 11.10 Billion in 2025 to USD 14.65 Billion by 2034 at a CAGR of 3.04%, adding roughly USD 3.55 Billion in incremental market value over the forecast period.

Four forces will shape the market through 2034: tighter infection-control standards; continued outsourcing of hospital laundry; technology-led inventory and process optimization; and sustainability pressure favoring efficient, circular textile programs.

By 2034, outsourced and technology-enabled linen management is expected to account for a growing majority of healthcare textile processing in leading markets, while emerging regions drive the fastest incremental volume gains.

Research Methodology

Primary Research

Primary research included interviews with healthcare laundry operators, hospital procurement and facilities managers, textile manufacturers, and accreditation specialists, validating market sizing, regional demand, material splits, and service-provider dynamics.

Secondary Research

Secondary sources included company annual reports, press releases and investor presentations, industry association publications, accreditation body resources, government health statistics, and trade data, used to triangulate market structure and competitive positioning.

Forecasting Models

Market forecasts combined top-down and bottom-up models using hospital bed capacity, occupancy rates, linen throughput per bed, outsourcing penetration, and price trends. Scenario analysis addressed utility cost and outsourcing-rate variation.

Hospital Linen Supply and Management Services Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered | Bed Sheet and Pillow Covers, Blanket, Bed Covers, Bathing and Cleaning Accessories, Patient Repositioner |

| Materials Covered | Woven, Non-Woven |

| Service Providers Covered | In-house, Contractual |

| End Uses Covered | Hospitals and Clinics, Diagnostic Centers, Others |

| Region Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Vestis, Cintas Corporation, Alsco Inc., Unitex Healthcare Laundry Services, Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Hospital Linen Supply and Management Services Market Report

The market was valued at USD 11.10 Billion in 2025, driven by rising hospital admissions, infection-control needs, and growing outsourcing of healthcare laundry services.

The market is projected to grow at a 3.04% CAGR from 2026 to 2034, reaching USD 14.65 Billion, supported by outsourcing and stricter hygiene standards.

Non-woven leads at 56.7% in 2025, driven by single-use surgical textiles. Woven at 43.3% remains essential for reusable bed linen and patient gowns.

Contractual dominates at 61.4% in 2025 as hospitals outsource laundry to accredited specialists. In-house holds 38.6%, retained by systems seeking direct operational control.

North America commands 37.8% in 2025, led by the United States and high outsourcing penetration. Asia-Pacific at 23.7% is the fastest-growing region through 2034.

Leading players include Vestis, Cintas Corporation, Alsco Inc., and Unitex Healthcare Laundry Services, Inc.

Outsourcing reduces capital investment, ensures accreditation compliance, improves linen availability, and lets clinical staff focus on patient care rather than laundry operations.

Accredited laundering, hygienic processing, and reliable supply of clean textiles reduce cross-contamination risk and support healthcare-associated infection prevention across care settings.

RFID tracking, inventory analytics, and digital portals reduce linen loss, improve par-level accuracy, enable usage-based billing, and provide transparency across multi-site networks.

Key challenges include high water, energy, and labor costs, linen loss and inventory shrinkage, workforce shortages, and infrastructure constraints in emerging regions.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)