Hybrid Operating Room Market Report by Component (Intraoperative Diagnostic Imaging Systems, Operating Room Fixtures, Surgical Instruments, Audiovisual Display Systems and Tools, and Others), Application (Cardiovascular Applications, Neurosurgical Applications, Thoracic Applications, Orthopedic Applications, and Others), End User (Hospital and Surgical Centers, Ambulatory Surgical Centers), and Region 2026-2034

Market Overview:

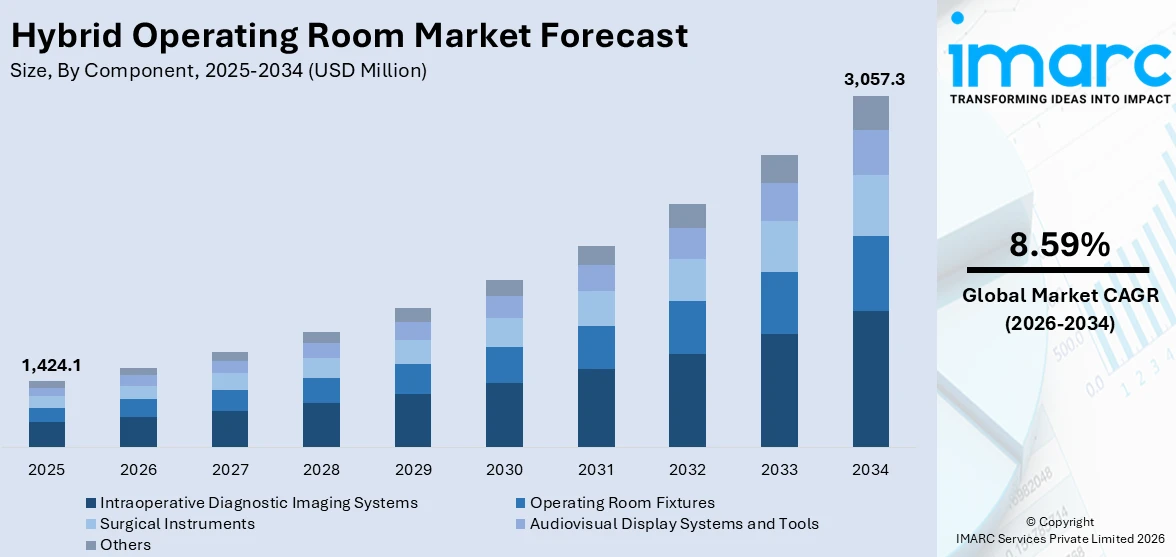

The global hybrid operating room market size reached USD 1,424.1 Million in 2025. Looking forward, IMARC Group expects the market to reach USD 3,057.3 Million by 2034, exhibiting a growth rate (CAGR) of 8.59% during 2026-2034. North America represents the largest market share due to its strong infrastructure for medical research and development (R&D) and integration systems. Moreover, the growing occurrence of various chronic ailments, rising popularity of minimally invasive surgical procedures, and increasing technological advancements in imaging modalities, such as 3D visualization, robotic-assisted surgery, and augmented reality (AR), are some of the major factors propelling the market.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025 |

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 1,424.1 Million |

| Market Forecast in 2034 | USD 3,057.3 Million |

| Market Growth Rate (2026-2034) | 8.59% |

A hybrid operating room (OR) is an advanced medical facility that combines the capabilities of a traditional surgical suite with state-of-the-art imaging technology, such as fluoroscopy, computed tomography (CT), and magnetic resonance imaging (MRI). It provides a versatile platform for performing complex surgical procedures that require real-time imaging guidance and intervention. It also offers a sterile surgical environment while integrating advanced imaging modalities within the same space, enabling surgeons to perform precise and minimally invasive interventions. It eliminates the need for patient transfers to different areas of the hospital, streamlining the workflow and minimizing the risk of complications associated with transportation.

To get more information on this market Request Sample

At present, the increasing demand for hybrid ORs due to the rising focus on improved patient outcomes is impelling the growth of the market. Besides this, the increasing occurence of cardiovascular diseases and the subsequent need for complex surgeries, such as cardiac catheterizations, angioplasties, and heart valve replacements is contributing to the market growth. In addition, the growing technological advancements in imaging modalities, such as 3D visualization, robotic-assisted surgery, and augmented reality (AR), are offering a favorable market outlook. Apart from this, the increasing focus on value-based healthcare and cost containment is supporting the growth of the market. Additionally, the rising utilization of hybrid ORs, as they facilitate multidisciplinary collaboration among surgeons, radiologists, and other specialists, leading to improved efficiency and accurate diagnosis, is strengthening the growth of the market.

Hybrid Operating Room Market Trends:

Rising Need for Minimally Invasive Procedures

The industry share is expanding as clinics and hospitals are offering minimally invasive procedures. Doctors are always looking for sophisticated instruments that minimize trauma, decrease risks of infection, and quicken recovery periods. Hybrid operating rooms are facilitating this movement by merging imaging systems with surgical installations, allowing for accurate and less invasive procedures. Patients are picking hospitals that have these options available, and this is compelling healthcare providers to invest in hybrid rooms. Insurance companies and healthcare systems are also catching on, as reducing hospital stays is decreasing the overall expense. This is developing a feedback loop where patient demand, clinical outcomes, and economic incentives are all moving toward the support of the adoption hybrid operating rooms. Hospitals are repeatedly upgrading to more patients and improve their reputation for advanced care. In 2025, HCA Florida Mercy Hospital launched four new operating rooms (ORs), representing a major achievement in the hospital’s $100 million capital investment plan. The addition of the new operating rooms raises the overall count of ORs at HCA Florida Mercy Hospital to 16, boosting the facility’s ability to cater to its patients. Three of these new operating rooms are assigned to orthopedic surgeries, freeing up more capacity in the main OR for additional vital surgical services. Furthermore, the fourth operating room is a cutting-edge hybrid suite specifically intended for cardiac and vascular operations.

Increasing Integration of Advanced Imaging Technologies

The market is growing because hospitals are increasingly integrating advanced imaging systems like CT, MRI, and angiography directly into operating suites. Surgeons are also relying on real-time imaging to make informed decisions throughout intricate procedures, minimizing the necessity for independent diagnostic sessions. This combination is assisting in cardiovascular, orthopedic, and neurosurgical procedures where accuracy is paramount. Hybrid operating rooms are being installed in hospitals to prevent moving patients from department to department, cutting risk and enhancing workflow. Imaging manufacturers are ongoingly creating smaller, higher-resolution systems that can be placed within these specialty operating rooms. Governments and private healthcare networks are investing in upgrades to make sure surgeons have access to the best imaging solutions. With increasing demand for personalization and image-guided surgery, healthcare facilities are always making hybrid operating rooms a priority in order to stay competitive, which is driving the market. IMARC Group predicts that the global medical imaging market is projected to attain USD 70.8 Billion by 2033.

Increasing Investment in Hospital Infrastructure

The market is growing as governments, private hospitals, and healthcare investors are always spending their budgets on upgrading medical infrastructure. Hybrid operating rooms are being viewed as strategic investments that optimize hospital capacity and reputation. Administrators are acknowledging the fact that hybrid operating rooms are drawing the best surgeons and patients seeking sophisticated procedures. Construction of multi-specialty hospitals is on the increase, and hybrid operating rooms are being incorporated in the planning stage. Healthcare providers are constantly upgrading to stand out in competitive urban areas. In the developing world, international financing and collaborations are facilitating hospitals to add these sophisticated facilities to help fill healthcare gaps. Return on investment (ROI) is more apparent as hybrid operating rooms are facilitating various surgical procedures in a single venue, which is enhancing efficiency. Hospitals are not only increasing physical capacity but also constantly embracing new designs that incorporate hybrid rooms as centers of surgical excellence. in 2025, York Hospital has begun building a new hybrid theater and MRI center. The two-level building, situated close to the hospital's South Entrance, will include a cutting-edge hybrid theater and an up-to-date high-tech MRI facility, greatly improving access to advanced diagnostic and vascular services. Upon completion, this £8m funding will establish a custom-designed space, specifically aimed at addressing the needs of the local community

Hybrid Operating Room Market Growth Drivers:

Rising Occurrence of Chronic Illnesses

The demand is increasing as the incidence of cardiovascular diseases, neurological diseases, and cancer is progressively on the rise globally. These patients with long-term illnesses are demanding intricate surgeries that are advantageous with real-time imaging and multishield care. Hybrid operating rooms are aiding surgeons in dealing with complicated cases by offering flexibility to transform from minimally invasive to open procedures. Aging populations are constantly adding to increased volumes of cases, as elderly patients are coming in with complex comorbidities that require precision care. Lifestyle diseases are also adding to the surgical demand, particularly among urban populations. Hospitals are constantly incorporating hybrid operating rooms to manage such cases better to ensure improved clinical outcomes. Governments and healthcare systems are identifying the necessity to be ready to meet the increasing burden of chronic illnesses, which is driving investments into sophisticated surgical environments.

Increased Adoption of Smart and Digital Health Technologies

The market is growing as hospitals are increasingly incorporating digital health technologies, artificial intelligence (AI), and data analytics into hybrid operating rooms. Surgeons are repeatedly leveraging AI-enabled imaging, navigation, and robotics to enhance surgery accuracy. Hospitals are implementing software that harmonizes information between multiple devices in real-time, making smarter workflows. Remote teamwork capabilities are allowing specialists to remotely lead procedures across geographies, which is broadening the value of hybrid operating rooms. Healthcare professionals are always looking for ways to minimize human error and increase consistency, and digital technologies are facilitating that transition. Equipment makers are building in connectivity features to enable predictive maintenance and system optimization. Hospitals are themselves branding themselves as smart hospitals, and hybrid operating rooms are at the heart of that image. With digital adoption accelerating, hybrid operating rooms are changing constantly into centers of innovation.

Increased Emphasis on Patient Safety and Outcomes

The market is growing as healthcare professionals are increasingly focusing on patient safety, infection prevention, and better results. Hybrid operating rooms are allowing surgeons to finish complicated procedures without repositioning patients from one department to another, which is cutting down on exposure to danger. Hospitals are constantly tracking outcome-based measures, and HORs are repeatedly showing better outcomes. Patients are more and more opting for centers that promote lower rates of complications and quicker recovery, which is driving adoption further. Accreditation agencies and health officials are encouraging the adoption of sophisticated facilities that reduce surgery mistakes. Healthcare professionals are constantly applying best practice in sterility, air circulation, and workflow optimization in hybrid ORs. The possibility of conducting emergency conversions between minimally invasive and open surgery in the same room is also building confidence. Through their focus on patient safety, hospitals are building their reputation, and this is driving continuous investments in hybrid operating room infrastructure.

Hybrid Operating Room Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global hybrid operating room market report, along with forecasts at the global, regional and country levels from 2026-2034. Our report has categorized the market based on component, application and end user.

Breakup by Component:

- Intraoperative Diagnostic Imaging Systems

- Angiography Systems

- MRI Systems

- CT Systems

- Others

- Operating Room Fixtures

- Operating Tables

- Operating Room Lights

- Surgical Booms

- Radiation Shields

- Surgical Instruments

- Audiovisual Display Systems and Tools

- Others

Intraoperative diagnostic imaging systems dominate the market

The report has provided a detailed breakup and analysis of the market based on the component. This includes intraoperative diagnostic imaging systems (angiography systems, MRI systems, CT systems, and others), operating room fixtures (operating tables, operating room lights, surgical booms, and radiation shields), surgical instruments, audiovisual display systems and tools, and others. According to the report, intraoperative diagnostic imaging systems (angiography systems, MRI systems, CT systems, and others) represented the largest segment.

Intraoperative diagnostic imaging systems refer to a range of technologies and tools employed within the operating room to acquire high-quality images of the anatomy of patients during surgery. These systems are often integrated into surgical suites and can include various imaging modalities, such as X-ray, ultrasound, magnetic resonance imaging (MRI), computed tomography (CT), and fluoroscopy. They provide surgeons with precise real-time imaging during complex procedures. They help in identifying the location and extent of tumors, anatomical abnormalities, or other critical structures, enabling surgeons to navigate and manipulate delicate tissues more accurately. They also aid in the identification and localization of tumors within the body. Surgeons can use imaging techniques like intraoperative MRI or ultrasound to precisely locate tumors and ensure their complete removal while minimizing damage to healthy surrounding tissues.

Breakup by Application:

Access the comprehensive market breakdown Request Sample

- Cardiovascular Applications

- Neurosurgical Applications

- Thoracic Applications

- Orthopedic Applications

- Others

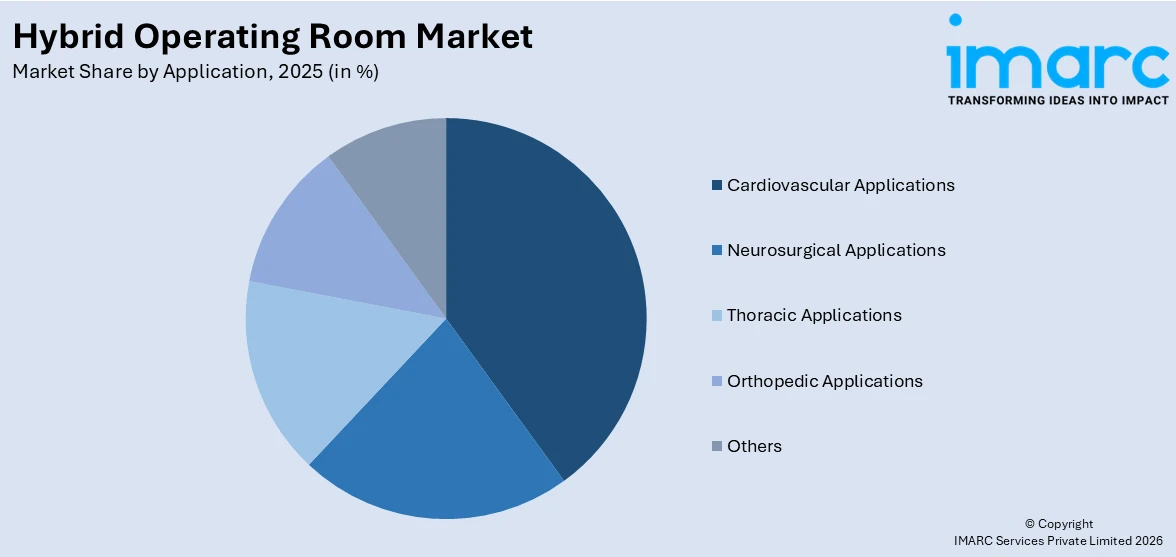

Cardiovascular applications hold the largest share in the market

A detailed breakup and analysis of the market based on the application have also been provided in the report. This includes cardiovascular applications, neurosurgical applications, thoracic applications, orthopedic applications, and others. According to the report, cardiovascular applications accounted for the largest market share.

The use of a hybrid operating room (OR) in cardiovascular applications is revolutionizing the field of cardiovascular surgery by combining the benefits of traditional surgical techniques with advanced imaging and minimally invasive interventions. It is particularly beneficial for complex cardiac procedures, consisting transcatheter aortic valve replacement (TAVR), mitral valve repair, or complex coronary artery bypass grafting (CABG). The integrated imaging systems enable real-time visualization of the heart and blood vessels, allowing surgeons to perform minimally invasive interventions with high precision. It also facilitates minimally invasive procedures, reducing the need for open-heart surgery and its associated risks. It allows for seamless integration between imaging and surgical procedures. Furthermore, it facilitates a hybrid approach, combining both surgical and interventional techniques in a single procedure.

Breakup by End User:

- Hospital and Surgical Centers

- Ambulatory Surgical Centers

Hospital and surgical centers hold the largest share in the market

A detailed breakup and analysis of the market based on the end-user have also been provided in the report. This includes hospital and surgical centers and ambulatory surgical centers. According to the report, hospital and surgical centers accounted for the largest market share.

Hospitals and surgical centers require hybrid ORs for several reasons, as they offer numerous advantages that significantly enhance patient care and surgical outcomes. Hybrid ORs are equipped with state-of-the-art imaging technologies, such as fluoroscopy, angiography, CT, or MRI. These imaging modalities provide real-time visualization of anatomical structures, blood flow, and device placement during surgical procedures. The availability of advanced imaging capabilities within the OR allows for precise diagnosis, accurate guidance during interventions, and immediate assessment of treatment effectiveness. Hybrid ORs are also suitable for performing minimally invasive procedures. The advanced imaging systems enable surgeons to visualize and navigate through complex anatomical structures using catheters, guidewires, or other specialized instruments. Moreover, minimally invasive techniques reduce patient trauma, promote faster recovery times, and decrease the risk of complications compared to traditional open surgeries.

Breakup by Region:

- North America

- United States

- Canada

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

North America exhibits a clear dominance, accounting for the largest hybrid operating room market share

The report has also provided a comprehensive analysis of all the major regional markets, which include North America (the United States and Canada); Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, and others); Europe (Germany, France, the United Kingdom, Italy, Spain, Russia, and others); Latin America (Brazil, Mexico, and others); and the Middle East and Africa. According to the report, North America accounted for the largest market share.

North America held the biggest market share since the region has a robust infrastructure for medical research and development (R&D), leading to the creation of innovative imaging technologies, surgical equipment, and integration systems.

Another contributing aspect is the increasing demand for minimally invasive procedures. Besides this, the increasing occurrence of various chronic ailments due to the rising adoption of sedentary lifestyle habits is propelling the growth of the market.

Asia Pacific is estimated to expand further due to the increasing focus on value-based healthcare to achieve better outcomes at lower costs. Moreover, the increasing construction of hospitals, nursing homes, and clinics to provide quality healthcare services to patients is strengthening the growth of the market.

Competitive Landscape:

Key market players are focusing on developing innovative imaging and diagnostic solutions, such as advanced imaging modalities, robotic-assisted surgery technologies, and integrated clinical applications. They are also investing in research and development (R&D) to introduce new products with improved performance, workflow efficiency, and patient safety features. Top companies are offering comprehensive hybrid OR solutions, including imaging systems, surgical tools, and data management platforms. They are focusing on interoperability, integrating their devices and software into a unified ecosystem to enhance workflow efficiency and facilitate data sharing. Leading companies are developing hybrid OR workflow optimization tools and surgical planning software. They are providing surgeons with comprehensive control and access to advanced visualization tools during procedures.

The report has provided a comprehensive analysis of the competitive landscape in the market. Detailed profiles of all major companies have also been provided. Some of the key players in the market include:

- ALVO Medical

- General Electric Company

- Getinge AB

- Hill-Rom Holdings Inc. (Baxter International Inc.)

- IMRIS

- Koninklijke Philips N.V.

- Siemens Healthineers AG (Siemens AG)

- Steris Corporation

- Toshiba Corporation

Recent Developments:

- August 2025: The Jenkins Charitable Foundation made a significant donation to the Tampa General Hospital (TGH) Foundation to finance a new hybrid operating room at Tampa General. The donation will facilitate the creation of another area within the academic medical center on Davis Islands that combines a cutting-edge surgical environment with the sophisticated imaging features of an interventional suite, an essential blend for conducting highly intricate vascular surgeries. The expense to construct the new hybrid operating room is slightly less than $10 million.

- August 2025: Abrazo West finishes building its new state-of-the-art hybrid operating room (OR), representing an investment of almost $7 million that merges the sterile setting of a conventional OR with the sophisticated features of a cardiac catheterization lab. It enables surgeons to conduct intricate, minimally invasive cardiovascular and vascular surgeries as well as electrophysiology procedures within one location. Surgical procedures for patients in the new operating room will start in August.

- June 2025: Construction is underway for 15 new operating rooms and an upgrade to one hybrid operating room as part of Phase 2 of the expansion at Vancouver General Hospital (VGH). The completion of both segments of the operating-room expansion is anticipated to boost the annual number of surgeries from 16,800 to over 19,000. The new surgical suites will feature a universal design, enabling any procedure to be conducted in any room. They will be designed to enhance equipment and storage, facilitating a logical sequence of tasks and activities in surgeries and increasing efficiency.

- April 2025: HaysMed is establishing a new benchmark in cardiac care by launching its Hybrid Operating Room (OR), which integrates the functions of a cardiac catheterization lab (Cath Lab) and a conventional OR to manage conditions that were once only treatable through open-heart surgery. The Hybrid OR integrates a cardiac surgery operating room with a state-of-the-art diagnostic imaging facility.

Hybrid Operating Room Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Components Covered |

|

| Applications Covered | Cardiovascular Applications, Neurosurgical Applications, Thoracic Applications, Orthopedic Applications, Others |

| End Users Covered | Hospital and Surgical Centers, Ambulatory Surgical Centers |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | ALVO Medical, General Electric Company, Getinge AB, Hill-Rom Holdings Inc. (Baxter International Inc.), IMRIS, Koninklijke Philips N.V., Siemens Healthineers AG (Siemens AG), Steris Corporation, Toshiba Corporation, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the hybrid operating room market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global hybrid operating room market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the hybrid operating room industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Hybrid Operating Room Market Report

The global hybrid operating room market was valued at USD 1,424.1 Million in 2025.

We expect the global hybrid operating room market to exhibit a CAGR of 8.59% during 2026-2034.

The rising adoption of hybrid operating rooms, as they assist clinicians in diagnosing and treating patients in a single location while improving efficiency, minimizing risks, enhancing safety, etc., is primarily driving the global hybrid operating room market.

The sudden outbreak of the COVID-19 pandemic had led to the postponement of various elective minimally invasive and highly complex open surgical procedures to reduce the risk of the coronavirus infection upon hospital visits and interaction with healthcare professionals, thereby negatively impacting the global market for hybrid operating room.

Based on the component, the global hybrid operating room market can be categorized into intraoperative diagnostic imaging systems, operating room fixtures, surgical instruments, audiovisual display systems and tools, and others. Currently, intraoperative diagnostic imaging systems account for the majority of the total market share.

Based on the application, the global hybrid operating room market has been segregated into cardiovascular applications, neurosurgical applications, thoracic applications, orthopedic applications, and others. Among these, cardiovascular applications currently exhibit a clear dominance in the market.

Based on the end user, the global hybrid operating room market can be bifurcated into hospital and surgical centers and ambulatory surgical centers. Currently, hospital and surgical centers hold the largest market share.

On a regional level, the market has been classified into North America, Asia-Pacific, Europe, Latin America, and Middle East and Africa, where North America currently dominates the global market.

Some of the major players in the global hybrid operating room market include ALVO Medical, General Electric Company, Getinge AB, Hill-Rom Holdings Inc. (Baxter International Inc.), IMRIS, Koninklijke Philips N.V., Siemens Healthineers AG (Siemens AG), Steris Corporation, and Toshiba Corporation.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)