Hydrogen Generation Market Size, Share, Trends and Forecast by Technology, Application, Systems Type, and Region, 2026-2034

Hydrogen Generation Market Size and Share:

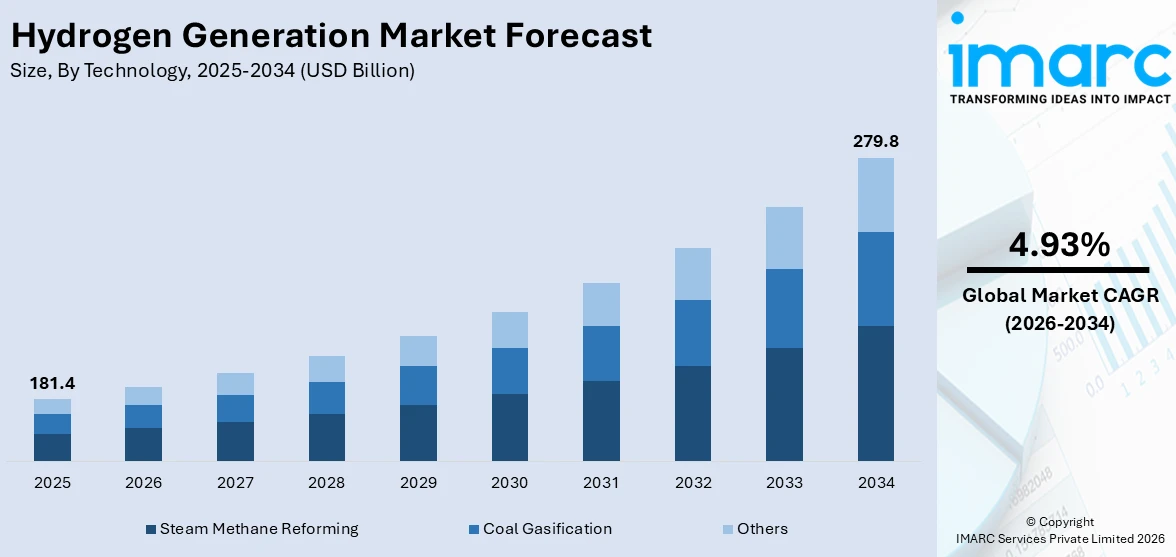

The global hydrogen generation market size was valued at USD 181.4 Billion in 2025. Looking forward, IMARC Group estimates the market to reach USD 279.8 Billion by 2034, exhibiting a CAGR of 4.93% during 2026-2034. Asia-Pacific currently dominates the market, holding a significant market share of over 35.4% in 2025. The rising environmental concerns, increasing need for sustainable energy sources, and the escalating demand for renewable energy across the globe represent some of the key factors driving the market.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

|

Market Size in 2025

|

USD 181.4 Billion |

|

Market Forecast in 2034

|

USD 279.8 Billion |

| Market Growth Rate 2026-2034 | 4.93% |

The global market is primarily driven by the increasing demand for clean energy solutions to minimize greenhouse gas emissions while combating climate change. Governments across the globe are promoting hydrogen as a sustainable energy carrier through supportive policies, subsidies, and investments in infrastructure development which is driving the market. Technological advancements in hydrogen production, such as electrolysis and carbon capture, have significantly improved efficiency and cost-effectiveness, further accelerating market growth. Rising adoption across industries such as transportation, power generation, and chemicals enhances demand, while the growing integration of hydrogen into renewable energy projects propels its market appeal. On February 14, 2024, the Ministry of New & Renewable Energy (MNRE), India, released scheme guidelines to facilitate pilot projects for the use of green hydrogen as fuel in buses, trucks, and four-wheelers under National Green Hydrogen Mission. The total budgetary outlay under this scheme would be Rs 496 crore till the financial year 2025-26. Additionally, the increasing focus on energy independence and the global push for decarbonization is providing an impetus to the market.

To get more information on this market Request Sample

The United States stands out as a key regional market, primarily driven by increasing industrial demand for hydrogen in refining, ammonia production, and methanol synthesis. The growth of renewable energy projects, such as solar and wind, improves the production of green hydrogen, which is in line with sustainability goals. Hydrogen storage and distribution infrastructure, including pipelines and fueling stations, is being developed to create a strong supply chain for growing adoption. Public-private partnerships and cooperation between energy companies, technology developers, and government agencies are escalating innovation and market access. In addition, increased interest in hydrogen as a backup power source for grid resilience and its potential to be used in heavy industries including steel and cement is increasing its presence in the energy space.

Hydrogen Generation Market Trends:

Transition to Sustainable Energy Sources

Governments worldwide are implementing robust measures to reduce carbon emissions in sectors such as the automotive industry, fostering an uptick in the adoption of clean energy solutions. In 2023, nearly 20% of all cars sold globally were electric vehicles (EVs). Concurrently, hydrogen's role as a coolant in power plant generators is emerging as a pivotal growth driver. Projects aimed at minimizing the costs and ecological footprint of hydrogen production technologies are on the rise, with nuclear energy-based hydrogen generation gaining traction as an economical, low-carbon alternative. This development is fueling the demand for hydrogen in key applications including glass purification, fertilizer production, and semiconductor manufacturing globally.

Economic and Policy Catalysts

The rising costs of conventional fuels such as oil and natural gas, combined with escalating electricity prices, are increasing the appeal of hydrogen-based energy sources across industries. In 2022, global fossil fuel subsidies surpassed USD 1 trillion for the first time, according to the International Energy Agency (IEA). Meanwhile, the adoption of clean energy by governments is enhancing the positive outlook in the market. Hydrogen is, for instance widely used in the production of new materials including hydrogenated polymers and metals which show better performance and value added compared to the old alternative. All these innovations are further propelled by the hydrogen refueling stations, designed to be energy-efficient and cost-effective. As of September 2023, India has 2 hydrogen refuelling stations, located at Indian Oil's R&D Centre and the National Institute of Solar Energy in Faridabad and Gurugram respectively.

Continuous Technological Advancements

Advances in technology and cost reductions are continually making hydrogen generation more affordable and accessible, thereby creating investments in the sector. This is further catalyzing new markets for hydrogen-based products and services. Hydrogen integration into various industry verticals from energy to manufacturing is propelling its adoption rate. The market is also benefiting from the growing trend of sustainable infrastructure, such as efforts to increase the capacities of hydrogen production and fine-tune the efficiency of hydrogen power systems. These developments enhance the global appeal of hydrogen as a clean source of energy and position it as a cornerstone for addressing the challenges of climate change.

Hydrogen Generation Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global hydrogen generation market, along with forecast at the global, regional, and country levels from 2026-2034. The market has been categorized based on technology, application, and systems type.

Analysis by Technology:

- Coal Gasification

- Steam Methane Reforming

- Others

Steam methane reforming stands as the largest component in 2025, holding around 64.5% of the market. This is due to its economical and efficient production of large-scale hydrogen. SMR relies on natural gas as the main feedstock that is reacted with steam at high temperatures to produce hydrogen and carbon monoxide, which undergo a water-gas shift reaction to provide more hydrogen. Although there are environmental concerns related to carbon emissions, the technology is widely used due to the established infrastructure and the capacity to fulfill industrial hydrogen requirements. Many industries use SMR for refining, ammonia production, and methanol synthesis. Further, developments in CCS technologies are also helping mitigate environmental concerns, thus ensuring SMR remains a continued preferred choice in the transition toward low-carbon hydrogen solutions.

Analysis by Application:

Access the comprehensive market breakdown Request Sample

- Methanol Production

- Ammonia Production

- Petroleum Refinery

- Transportation

- Power Generation

- Others

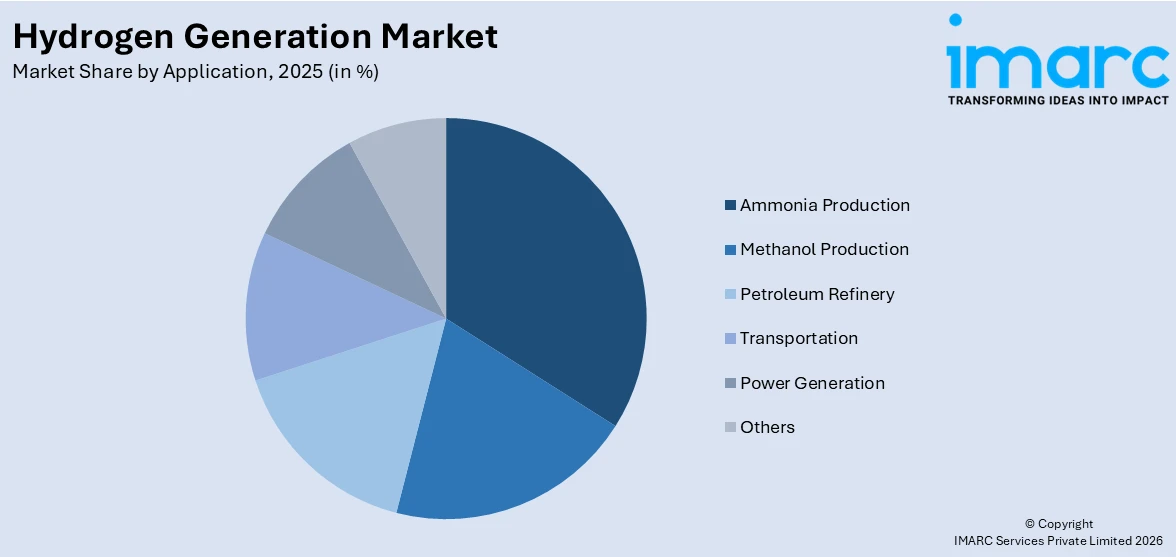

Ammonia production leads the market with around 21.6% of market share in 2025 due to its extensive use in fertilizer manufacturing and other industrial processes. Ammonia is produced via the Haber-Bosch process, which requires hydrogen as a crucial feedstock. As more food is demanded globally, fertilizers used in agriculture increase their demand for ammonia, thereby increasing their consumption of hydrogen. Additionally, ammonia is also emerging as an excellent hydrogen carrier and clean source of energy in the market. The increasing need for greener ammonia with renewable hydrogen is further encouraging the use of ammonia, enhancing its dominance in hydrogen applications as well as its criticality in energy transition strategies all over the world.

Analysis by System Type:

- Merchant

- Captive

Merchant reforming leads the market with around 62.5% of market share in 2025, primarily due to its scalability and ability to cater to a wide range of industries. Hydrogen is generated through methods such as steam methane reforming in centralized facilities, which then provide it to the end-users. This system does not rely on a significant on-site production infrastructure and thus represents one of the more economical approaches for industries needing significant amounts of hydrogen. Merchant reforming supports applications in the refining, chemical production, and energy sectors, among others. Its dominance is further bolstered by advancements in transportation technologies, such as high-pressure tube trailers and liquefied hydrogen carriers, which enhance distribution efficiency. This system type is instrumental in meeting rising hydrogen demands globally.

Regional Analysis:

To get more information on the regional analysis of this market Request Sample

- North America

- United States

- Canada

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

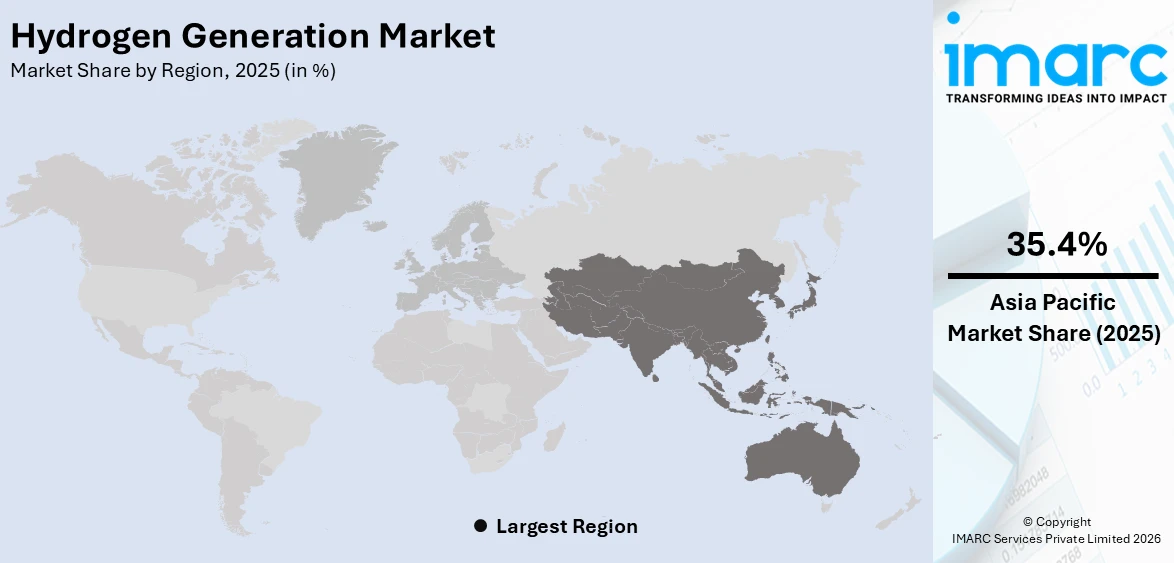

In 2025, Asia-Pacific accounted for the largest market share of over 35.4%. This is due to rapid industrialization, rising energy consumption, and government policies in these countries for clean energy alternatives. China, Japan, South Korea, and India are the major economies that have been at the forefront of hydrogen adoption across refining, transportation, and manufacturing sectors. Hydrogen production is dominated by China due to its robust industrial base and its reliance on coal gasification, whereas Japan and South Korea are investing in hydrogen-based fuel cells and infrastructure development. India is advancing green hydrogen projects to reduce carbon footprints. The region is receiving major investments in hydrogen technologies and large-scale production facilities. Policies promoting renewable hydrogen in support of global climate goals strengthen Asia-Pacific's leadership.

Key Regional Takeaways:

United States Hydrogen Generation Market Analysis

The hydrogen generation market in the United States is driven by the country’s growing commitment to clean energy and decarbonization. Federal and state-level initiatives, such as the Infrastructure Investment and Jobs Act and the Clean Energy Standard, are promoting the development of hydrogen technologies and infrastructure. With a strong emphasis on renewable energy sources, the U.S. is increasingly investing in green hydrogen production, supported by advancements in electrolysis technology and renewable power integration. The transportation sector, which contributed 6.7% to the U.S. GDP in 2022, or approximately USD 1.7 Trillion, is a major driver of hydrogen demand. The adoption of hydrogen fuel cell vehicles (FCVs) is particularly prominent in states like California, where regulatory frameworks encourage clean mobility. Additionally, hydrogen plays a key role in industrial applications such as refining, steel manufacturing, and ammonia production. Partnerships between private companies, government bodies, and research institutions are further accelerating advancements in hydrogen storage, transport, and distribution. The potential for hydrogen to support the U.S. in achieving net-zero emissions by mid-century solidifies its role in the country’s energy future.

Asia Pacific Hydrogen Generation Market Analysis

The Asia-Pacific (APAC) region is witnessing significant growth in the hydrogen generation market due to its increasing focus on reducing carbon emissions and meeting energy demands. Key countries like Japan, South Korea, and China are at the forefront, investing in hydrogen as a clean fuel alternative, particularly in industries such as transportation and manufacturing. Notably, 50% of the world’s top 10 economies for manufacturing are located in APAC, creating substantial demand for hydrogen in sectors like steel production, chemicals, and refining. Japan's commitment to hydrogen fuel cell vehicles (FCVs) and South Korea’s green hydrogen initiatives are notable examples. Additionally, China’s push for carbon neutrality by 2060 further fuels the adoption of hydrogen technologies. The region’s growing investments in hydrogen infrastructure, including storage and transport networks, and strong government-private sector collaborations, are driving the market’s expansion in APAC.

Europe Hydrogen Generation Market Analysis

Europe is a leading region in the hydrogen generation market, driven by ambitious green energy policies and a focus on decarbonizing various sectors. The European Union's Green Deal and its hydrogen strategy aim to significantly scale up clean hydrogen production, with the goal of producing 10 Million Tons of renewable hydrogen by 2030. Countries such as Germany, the Netherlands, and France are at the forefront of large-scale hydrogen projects focusing on green hydrogen as part of their energy transition agenda. European manufacturers are investing in advanced electrolysis technologies with significant support from national and EU funding programs. Further, Europe's strong industrial base, including heavy industries such as steel, chemicals, and refining, creates a huge demand for hydrogen as a cleaner energy source. Furthermore, growing concerns about energy security and dependence on imports of fossil fuels are driving the change in Europe toward self-sufficient hydrogen production. Beside this, cross-border hydrogen infrastructure developments are also gaining momentum as they enable a more integrated hydrogen economy and foster regional cooperation, which in turn expands the growth potential of this European market.

Latin America Hydrogen Generation Market Analysis

Latin America’s hydrogen generation market is driven by the region’s vast renewable energy resources, particularly in countries like Brazil, Chile, and Argentina. Brazil stands out with 89% renewable penetration, just behind Norway’s 98.5%, making it a leading market for green hydrogen. Among the largest markets in the region, Colombia and Chile are also notable players, with renewable energy shares of around 75% and 55%. These nations are leveraging their wind and solar potential to develop green hydrogen projects, accelerating the region’s transition to cleaner energy. International investments and regional partnerships further enhance the market’s growth in Latin America.

Middle East and Africa Hydrogen Generation Market Analysis

The hydrogen generation market in the Middle East and Africa is propelled by the region's rich natural resources and its push toward diversifying energy sources. The Middle East produces approximately 30% of the world's oil, and oil-based revenue is a huge driver for the governments. Several countries, including Saudi Arabia and the UAE, are investing in green hydrogen production as part of their economic diversification plans and in their commitment to reducing carbon emissions. The region is apt for renewable energy, and the availability of solar power, among other conditions, supports the green hydrogen project.

Competitive Landscape:

The competitive landscape in the hydrogen generation market is intensely innovative and strategically collaborative between key players looking to take a share of growing demand. Key companies are investing significantly in research and development to move forward with hydrogen production technologies: green hydrogen from renewable sources and blue hydrogen with carbon capture capabilities. They are partnering and entering into joint ventures to increase their production capacities and establish hydrogen ecosystems worldwide. Market leaders are also setting up low-cost hydrogen re-fueling infrastructure and streamlining transportation logistics for the establishment of hydrogen across all markets. Strategic acquisitions and portfolio diversification are other leading trend, that helps companies enlarge their footprint in new geographies and meet the rising need for clean energy solutions.

The report provides a comprehensive analysis of the competitive landscape in the hydrogen generation market with detailed profiles of all major companies, including:

- Air Liquide International S.A.

- Air Products Inc.

- CLAIND srl

- INOX Air Products Ltd.

- Linde Plc

- Mahler AGS GmbH

- McPhy Energy S.A.

- Messer Group GmbH

- NEL Hydrogen

- Taiyo Nippon Sanso Corporation

- Weldstar Inc.

- Xebec Adsorption Inc.

Latest News and Developments:

- November 2024: Hybitat Srl, a unit of SIT Group, launched a green hydrogen generation and storage system for residential, commercial, and public use. The first 200 kWh system, sold recently, will be installed in an 18th-century residence in 2025. It uses excess solar power to produce hydrogen, which can be stored and later converted into electricity or used in gaseous form.

- October 2024: Adani Group has begun blending 2.2-2.3% green hydrogen into the natural gas supplied to households in Shantigram, Ahmedabad, as part of its efforts to reduce emissions and achieve net-zero targets. The initiative, led by Adani Total Gas Ltd, a joint venture with TotalEnergies, uses hydrogen produced through clean methods, which is injected into natural gas pipelines to generate heat and power with lower emissions.

- July 2024: Tecnimont Private Limited, the Indian subsidiary of Tecnimont, and NEXTCHEM have inaugurated India's first green hydrogen production plant for GAIL (India) Limited at Vijaipur, Madhya Pradesh. The plant, awarded in May 2022, will produce 4.3 Tons of green hydrogen per day using 10 megawatt electrolysers. This marks a significant milestone as GAIL becomes the first company in India to begin megawatt-scale green hydrogen production, advancing the country’s transition to low-carbon energy solutions.

- April 2024: Panasonic’s Electric Works Company announced to launch a new pure hydrogen fuel cell generator, PH3, for Europe, Australia, and China. The generator uses a chemical reaction between high-purity hydrogen and oxygen to generate power. This follows the 2021 launch of the PH1, a 5 kW model, and marks Panasonic's efforts to expand its hydrogen business outside Japan.

- February 2024: Hygenco, based in Haryana, India, announced to build India’s first operational green hydrogen plant in Hisar. The facility will produce green hydrogen, generating energy without carbon dioxide emissions. This marks a significant step towards sustainable energy solutions in India. The project aims to support the country's transition to a low-carbon economy.

Hydrogen Generation Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Technologies Covered | Coal Gasification, Steam Methane Reforming, Others |

| Applications Covered | Methanol Production, Ammonia Production, Petroleum Refinery, Transportation, Power Generation, Others |

| System Types Covered | Merchant, Captive |

| Region Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Air Liquide International S.A., Air Products Inc, CLAIND srl, INOX Air Products Ltd., Linde plc, Mahler AGS GmbH, McPhy Energy S.A., Messer Group GmbH, NEL Hydrogen, Taiyo Nippon Sanso Corporation, Weldstar Inc., Xebec Adsorption Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the hydrogen generation market from 2020-2034.

- The hydrogen generation market research report provides the latest information on the market drivers, challenges, and opportunities in the global market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the hydrogen generation industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Hydrogen Generation Market Report

Hydrogen generation refers to the production of hydrogen gas, primarily used as a clean energy carrier and industrial feedstock. It is generated through various technologies, including steam methane reforming, electrolysis, and coal gasification, supporting applications in transportation, power generation, refining, and manufacturing.

The hydrogen generation market was valued at USD 181.4 Billion in 2025.

IMARC estimates the global hydrogen generation market to exhibit a CAGR of 4.93% during 2026-2034.

The market is driven by increasing demand for clean energy to reduce greenhouse gas emissions, supportive government policies, investments in hydrogen infrastructure, technological advancements in hydrogen production, and its adoption in key sectors such as transportation, power generation, and manufacturing.

Steam methane reforming represented the largest segment by technology, driven by its cost-effectiveness and efficiency in producing large-scale hydrogen.

Ammonia production leads the market by application due to its extensive use in fertilizer manufacturing and emerging role as a hydrogen carrier.

Merchant reforming is the leading segment by systems type, driven by its scalability and ability to cater to industries without on-site production infrastructure.

On a regional level, the market has been classified into North America, Asia Pacific, Europe, Latin America, and Middle East and Africa, wherein Asia Pacific currently dominates the market.

Some of the major players in the global hydrogen generation market include Air Liquide International S.A., Air Products Inc, CLAIND srl, INOX Air Products Ltd., Linde plc, Mahler AGS GmbH, McPhy Energy S.A., Messer Group GmbH, NEL Hydrogen, Taiyo Nippon Sanso Corporation, Weldstar Inc. and Xebec Adsorption Inc., among others.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)