Implantable Drug Delivery Devices Market Size, Share, Trends and Forecast by Product Type, Technology, Application, End User, and Region, 2026-2034

Implantable Drug Delivery Devices Market Size and Share:

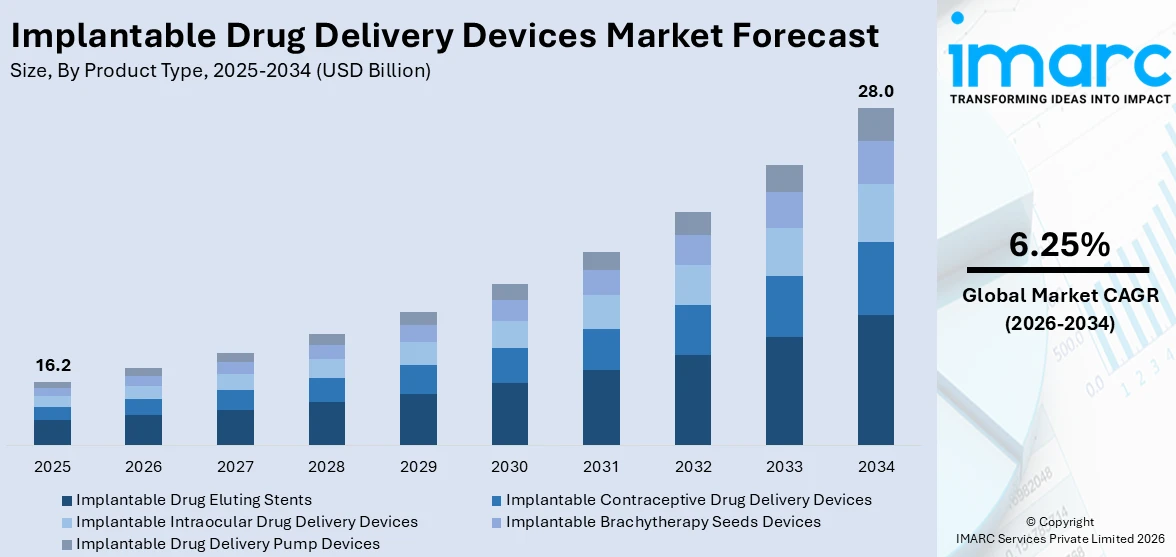

The global implantable drug delivery devices market size was valued at USD 16.2 Billion in 2025. Looking forward, IMARC Group estimates the market to reach USD 28.0 Billion by 2034, exhibiting a CAGR of 6.25% during 2026-2034. North America currently dominates the market, holding a significant market share of over 40.7% in 2025. The heightened usage of artificial intelligence (AI)-enabled smart sensors, biodegradable materials, and miniaturized long-acting implants is supporting the market growth. Additionally, real-time dosing algorithms and cloud connectivity improve accuracy and cut medication errors, while biodegradable systems eliminate removal surgeries and expand therapeutic applications. Miniaturized, long-duration implants enhance adherence in chronic disease management and support outpatient care. Furthermore, the growing research and development (R&D) investments, clinical trial progress, and new product launches from leading companies are expanding the implantable drug delivery devices market share.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

|

Market Size in 2025

|

USD 16.2 Billion |

|

Market Forecast in 2034

|

USD 28.0 Billion |

| Market Growth Rate (2026-2034) | 6.25% |

The global implantable drug delivery devices market is principally bolstered by numerous critical factors, majorly encompassing the burgeoning cases of chronic conditions, which generally include cardiovascular issues, diabetes, or cancer. Besides this, the amplifying requirement for minimally invasive surgeries or procedures and the notable boost in geriatric population, which is comparatively more prone to chronic disorders, are significantly fueling market expansion. In addition to this, global focus on technological enhancements in implantable devices, like the designing of programmable or biodegradable drug delivery systems, and the accelerating need for prolonged therapeutic solutions are expanding the implantable drug delivery devices market share. Apart from this, the bolstering necessity to lower expenditure in healthcare landscape and the easy accessibility of profitable reimbursement regulations are impacting the market growth intensely. In line with this, governments of several countries are currently launching ventures to incentivize leading-edge technologies for healthcare, which, as a consequence, is heightening the market demand worldwide. Moreover, the significant elevation in research and development (R&D) efforts targeted at launching innovative and novel implantable drug delivery devices are also influencing market dynamics. Other pivotal factors, enveloping the magnifying consciousness associated with the advantages of utilizing implantable drug delivery devices along with the robust emphasis on targeted drug delivery as well as personalized medicine, are notably contributing to the implantable drug delivery devices market growth.

To get more information on this market Request Sample

The United States is a prominent market for implantable drug delivery devices, driven by a high prevalence of chronic diseases and a strong focus on innovative healthcare solutions. For instance, according to the chronic diseases, including diabetes, heart conditions, and cancer, are the major causes of both disability and death across the U.S., accounting for USD 4.5 trillion annually in nation's health care expenditure. Moreover, the country's well-established pharmaceutical and medical device industries facilitate the development and adoption of these devices. Furthermore, advanced research and development initiatives, coupled with a favorable regulatory environment, support the growth of this market. Additionally, the increasing demand for targeted and personalized therapies, as well as the need for improved patient outcomes, contribute to the rising adoption of implantable drug delivery devices in the United States. This fuels market expansion and innovation.

Implantable Drug Delivery Devices Market Trends:

Integration Of Artificial Intelligence (AI) and Smart Sensors for Personalized Drug Delivery

The implantable drug delivery devices market growth is experiencing transformation through AI integration and smart sensor technologies. Moreover, there is an increase in research and development (R&D) investments for advanced sensor miniaturization and wireless power capabilities. Modern smart pumps incorporate AI-driven algorithms processing patient data at one-second intervals for real-time dosage adjustments. Cloud connectivity enables remote therapy management with clinicians modifying treatment protocols without physical consultations. Research demonstrates these systems reduce medication errors by 15-25% through optimized dosage control. Scientific publications confirm smart infusion devices with automated replacement mechanisms significantly enhance drug delivery continuity and accuracy. Studies showed automated vasoactive drug replacement systems maintaining consistent therapeutic levels while eliminating manual assessment requirements. Furthermore, companies are launching various smart health sensors in the form of wearables. In 2024, HUAWEI TruSense System was launched which provided accurate and science-based health and fitness technology to users.

Biodegradable And Bioresorbable Materials Revolutionizing Device Design

Biodegradable materials are fundamentally changing implantable device architectures eliminating surgical removal requirements. Scientists developed implantable biodegradable triboelectric nanogenerators generating electrical stimulation through wireless ultrasound activation. These devices deliver anti-mitotic drugs while disrupting cancer cell microtubule assembly through electrical fields. Complete device degradation occurs post-therapy without secondary extraction procedures. NIH's 2025 DEBUT Challenge supports biodegradable implant innovations through targeted funding programs. Material advances include biocompatible polymers maintaining structural integrity during therapy then safely dissolving. Research explores silk fibroin proteins and biodegradable elastomers for pressure sensors and drug reservoirs. These materials minimize foreign body reactions while providing controlled degradation profiles. Academic-industry collaborations delivered coin-sized biosensors with enhanced wearability and accuracy. Biodegradable power sources using energy harvesting eliminate battery replacement surgeries. The technology enables temporary therapeutic implants for post-surgical recovery or acute condition management. In 2024, Stryker, a worldwide leader in medical technology, declared the introduction of InSpace, the initial balloon implant designed for arthroscopic treatment of massive irreparable rotator cuff tears (MIRCTs)*, in India. MIRCTs are among the leading factors contributing to shoulder problems. 1,2,3 InSpace offers a fresh alternative for surgeons in the shoulder care continuum, helping them address their patients' needs more effectively.

Miniaturized Long-Acting Implants for Chronic Disease Management

Miniaturization technologies enable matchstick-sized implants delivering medications for six months to one year. Vivani Medical's GLP-1 exenatide implant achieved rapid LIBERATE-1 trial enrollment with 24 subjects recruited within four weeks. The subdermal device addresses medication non-adherence affecting 50% of chronic disease patients. The implant maintains consistent drug levels avoiding peaks and troughs associated with injections. Moreover, miniaturized pumps weighing under 45 grams deliver micro-doses at 0.05 mL/hour precision. Modern devices incorporate magnetic induction charging through 10 to 20mm tissue depth enabling non-invasive power transfer. Clinical evidence demonstrates six-month implants reducing hospital visits while improving adherence rates. Development focuses on once-yearly administration possibilities for diabetes and obesity management. The technology particularly benefits elderly patients struggling with daily medication regimens. Implantable drug delivery devices market growth accelerates as miniaturization enables outpatient procedures reducing healthcare costs. Companies report a higher percentage of patient preference for long-acting implants over daily medications.

Implantable Drug Delivery Devices Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global implantable drug delivery devices market, along with forecast at the global, regional, and country levels from 2026-2034. The market has been categorized based on product type, technology, application, and end user.

Analysis by Product Type:

- Implantable Drug Eluting Stents

- Implantable Contraceptive Drug Delivery Devices

- Implantable Intraocular Drug Delivery Devices

- Implantable Brachytherapy Seeds Devices

- Implantable Drug Delivery Pump Devices

Implantable drug eluting stents lead the market with around 32.2% of market share in 2025, driven by their role in preventing restenosis in coronary arteries. These devices are designed to release drugs directly at the site of arterial blockages, reducing the risk of re-narrowing after stent implantation. The integration of drug-eluting technology with stents enhances the efficacy of cardiovascular treatments, addressing critical challenges in managing coronary artery disease. The growing prevalence of heart-related conditions, coupled with advancements in stent design and drug formulations, is fueling market growth. Additionally, the shift toward minimally invasive procedures and the increasing preference for DES over bare-metal stents, due to their reduced risk of complications, further supports market expansion. As the demand for more effective treatments rises, implantable drug-eluting stents continue to dominate as a leading choice in the cardiovascular sector.

Analysis by Technology:

- Biodegradable Implants

- Non-Biodegradable Implants

Non-biodegradable leads the market in 2025. These devices are designed to release therapeutics over extended periods, offering controlled and sustained release without the need for frequent re-administration. Non-biodegradable systems, often used in the treatment of chronic conditions such as diabetes, cancer, and pain management, are durable and provide long-term therapeutic benefits. These devices typically include materials like metals, polymers, or ceramics, which ensure stability and longevity in the human body. Additionally, the demand for non-biodegradable drug delivery systems is driven by their ability to maintain consistent drug levels, improving patient compliance and reducing the need for repeated interventions. With advancements in materials science and device engineering, the market for non-biodegradable systems is expected to grow, offering significant potential for pharmaceutical companies seeking to enhance therapeutic delivery while minimizing side effects.

Analysis by Application:

Access the comprehensive market breakdown Request Sample

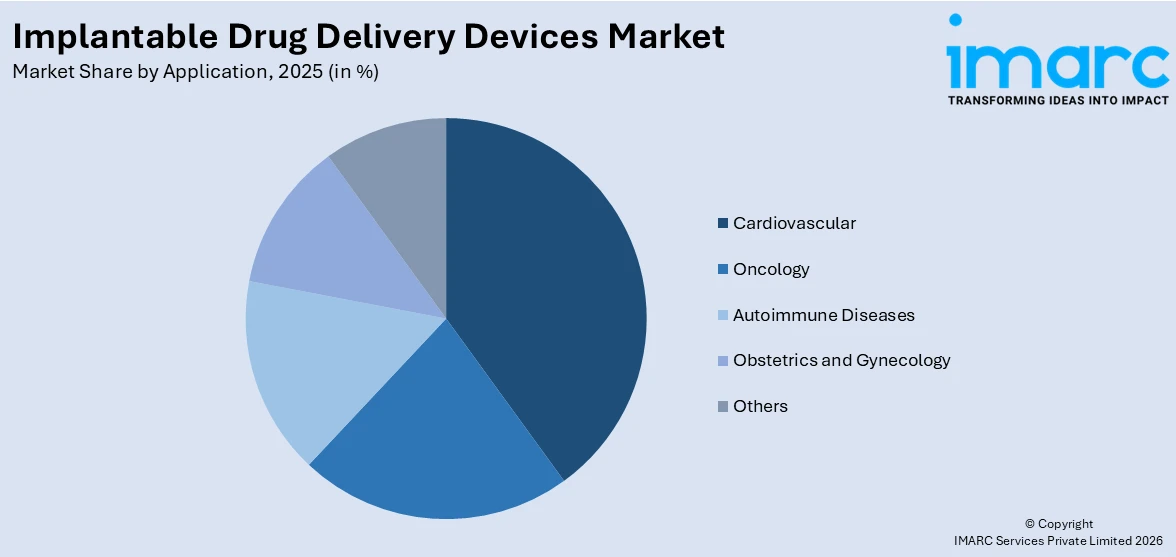

- Oncology

- Cardiovascular

- Autoimmune Diseases

- Obstetrics and Gynecology

- Others

Cardiovascular leads the market in 2025 by application, driven by the widespread occurrence of heart-related conditions and the growing need for advanced and effective treatment options. Devices used in cardiovascular applications, such as drug-eluting stents and pacemakers, play a crucial role in managing conditions like coronary artery disease, arrhythmias, and heart failure. The growing aging population, coupled with unhealthy lifestyle habits, has contributed to an increase in cardiovascular diseases, driving demand for innovative therapeutic solutions. Implantable drug delivery systems in this category enable precise medication release, which enhances treatment effectiveness, minimizes potential complications, and contributes to better patient outcomes. Furthermore, technological advancements in the design and material properties of cardiovascular devices are contributing to the growth of this segment. As healthcare systems focus on improving heart disease management, cardiovascular applications will remain at the forefront of market development.

Analysis by End User:

- Hospitals

- Ambulatory Surgery Centers

- Others

Hospitals lead the market in 2025, accounting for a significant share due to their central role in patient treatment and care. Hospitals are primary settings for the implantation of drug delivery systems, particularly for patients requiring specialized procedures like stent placement or pain management devices. These institutions benefit from the latest innovations in implantable devices, offering targeted therapies for chronic conditions such as diabetes, cancer, and cardiovascular diseases. Additionally, hospitals are equipped with advanced medical technologies and skilled professionals necessary for the successful administration and monitoring of these devices. With the ongoing enhancement of healthcare infrastructure worldwide, hospitals continue to serve as the primary users of implantable drug delivery systems. Furthermore, their ability to integrate new technologies into routine care, combined with rising patient volumes and the increasing complexity of treatments, ensures that hospitals will continue to dominate the market share in the years to come and will contribute to a positive implantable drug delivery devices market outlook.

Regional Analysis:

To get more information on the regional analysis of this market Request Sample

- North America

- United States

- Canada

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

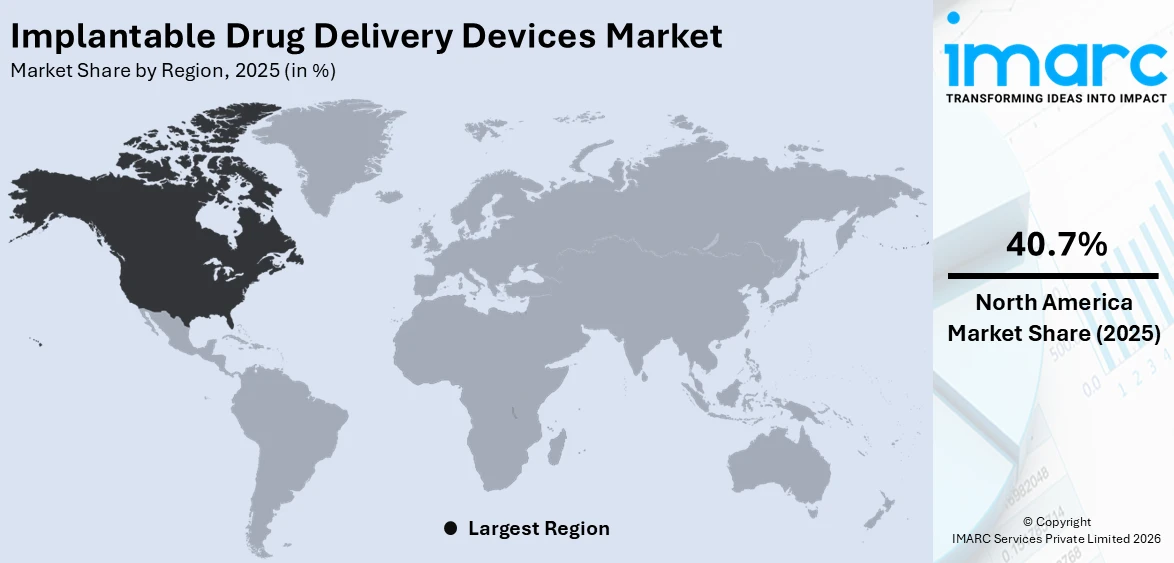

In 2025, North America accounted for the largest market share of over 40.7%. This region is chiefly influenced by highly robust healthcare ecosystem, substantial efforts and investments pertaining to research and development programs, and elevated requirement for cutting-edge treatment methodologies. The region heavily profits from resilient regulatory aid, facilitating quick utilization leading-edge technologies. In addition to this, the establishment of leading pharmaceutical firms and device producers in Canada as well as the United States further prompts significant growth in this market, with an active emphasis on enhancing patient outcomes by leveraging targeted therapies. Besides this, the magnification of chronic diseases prevalence, for instance cancer, diabetes, or cardiovascular disorders, is escalating requirement for implantable drug delivery methods. For instance, as per industry reports, in 2024, around 70% of individuals in Canada were suffering from type 2 diabetes, while 90% of individuals were suffering from type 1 diabetes. Furthermore, North America’s well-structured reimbursement policy framework and boosting awareness regarding the profits of implantable systems also strengthens its domination in the global industry, prompting constant innovations in this segment.

Key Regional Takeaways:

United States Implantable Drug Delivery Devices Market Analysis

The United States drives global innovation through FDA's progressive regulatory approach balancing safety with timely market access. Orchestra BioMed received IDE approval in 2025 initiating a 740-patient pivotal trial for Virtue SAB. The sirolimus-angioinfusion balloon addresses coronary restenosis affecting 325,000 patients annually. FDA breakthrough designations expedite development timelines for devices addressing unmet medical needs. Government healthcare programs including Medicare provide coverage for approved implantable devices supporting market growth. Academic medical centers conduct pioneering research advancing drug delivery technologies through federal grants. The country hosts headquarters of major device manufacturers investing billions in R&D annually. Clinical trial infrastructure supports rapid patient enrollment accelerating product development cycles. Specialized manufacturing facilities produce implantable devices meeting stringent quality requirements. Healthcare provider training programs ensure proper device implantation and patient management protocols.

Europe Implantable Drug Delivery Devices Market Analysis

European markets demonstrate strong adoption driven by universal healthcare systems prioritizing cost-effective chronic disease management. Strategic partnerships between pharmaceutical and device companies accelerate innovation in drug-device combinations. Government initiatives promote digital health transformation integrating smart implantable devices into care pathways. Nordic countries lead adoption rates with comprehensive reimbursement covering advanced drug delivery systems. Research consortiums combining academic and industry partners receive EU funding for collaborative projects. Regulatory harmonization across member states simplifies multi-country clinical trials and market launches. Patient advocacy groups influence policy decisions supporting access to innovative implantable therapies. In 2025, Roche announced that it has obtained the EU CE mark for its Port Delivery Platform with Susvimo, to be marketed in the EU as Contivue®. The system consists of the implantable device through which Susvimo is administered, and four supportive devices used to initially fill, insert, refill, and remove the implant (if needed). Susvimo® (ranibizumab injection) 100 mg/mL for intravitreal use via the Susvimo eye implant is currently under review with the European Medicines Agency (EMA) for the treatment of nAMD. With immediate and predictable durability, Contivue with Susvimo provides continuous delivery of a customized formulation of ranibizumab directly to the eye.

Asia Pacific Implantable Drug Delivery Devices Market Analysis

Asia Pacific emerges as the fastest-growing region driven by massive diabetic populations requiring advanced management solutions. China's diabetes market is projected to attain USD 9.81 Billion by 2033 according to the predictions of IMARC Group. Government healthcare reforms expand insurance coverage for implantable devices improving patient access. Joint ventures between international and local companies facilitate technology transfer and market entry. The rise in disposable income among Indians also drives the demand for premium healthcare including advanced drug delivery options. Japan's aging population creates opportunities for implantable devices managing multiple chronic conditions simultaneously. Manufacturing capabilities in the region reduce production costs making devices more affordable. Regulatory authorities streamline approval processes attracting clinical trials and product launches. Hospital infrastructure investments support adoption of sophisticated implantable technologies requiring specialized facilities. Digital health initiatives integrate implantable devices with telemedicine platforms enabling remote monitoring.

Latin America Implantable Drug Delivery Devices Market Analysis

Latin America demonstrates increasing adoption driven by public health initiatives addressing chronic disease burdens. Brazilian research institutions partner with European companies advancing flow chemistry for device manufacturing. Local production capabilities reduce import dependencies making implantable devices more accessible. Government programs in Mexico and Colombia expand healthcare coverage including advanced medical devices. Private healthcare sectors in major cities adopt latest implantable technologies attracting medical tourism. Regulatory harmonization initiatives facilitate multi-country product registrations reducing market entry barriers. Academic institutions develop local expertise through international collaborations and training programs. Infrastructure improvements support distribution networks ensuring device availability in remote areas. Economic growth enables middle-class expansion increasing demand for quality healthcare including implantable solutions.

Middle East and Africa Implantable Drug Delivery Devices Market Analysis

Middle East markets advance through government visions prioritizing healthcare sector development and medical device manufacturing. Saudi Aramco's collaboration developing modular flow reactors demonstrates commitment to advanced technology adoption. Gulf countries invest heavily in healthcare infrastructure including specialized centers for device implantation. African markets show potential with South Africa leading adoption of implantable technologies through private healthcare. International partnerships bring expertise and investment supporting local capacity building initiatives. Medical training programs develop skilled healthcare professionals capable of managing complex implantable devices. Regulatory frameworks evolve to balance patient access with safety requirements for new technologies. Disease burden from diabetes and cardiovascular conditions drives demand for long-term therapeutic solutions.

Competitive Landscape:

The global implantable drug delivery devices market is highly competitive, with numerous key players focusing on technological advancements, strategic partnerships, and product innovation to enhance market position. For instance, in October 2024, Silo Pharma, Inc., a biopharmaceutical firm focused on designing drug delivery systems, announced positive results for its recent dissolution and sterilization tests of its new implant SP-26 ketamine-loaded, developed for fibromyalgia and chronic pain. These tests were carried out as per the development agreement with Sever Pharma Solutions. As these conditions become more widespread, the necessity for efficient and enduring treatment options is steadily increasing. Additionally, the market is influenced by increasing regulatory requirements, with manufacturers striving to meet stringent safety and quality standards. Competition is also shaped by pricing strategies, market penetration, and the ability to secure partnerships with healthcare providers and pharmaceutical companies to expand distribution channels globally.

The report provides a comprehensive analysis of the competitive landscape in the implantable drug delivery devices market with detailed profiles of all major companies, including:

- Abbott Laboratories

- Boston Scientific Corporation

- Delpor Inc.

- Koninklijke DSM N.V.

- Medtronic plc

- Theragenics Corporation

Latest News and Developments:

- September 2025: Biogen Inc. declared that it has finalized a deal to purchase Alcyone Therapeutics, located in Massachusetts. In collaboration with Alcyone Therapeutics, the companies are progressing ThecaFlex DRx™, an implantable subcutaneous port and catheter device that is being explored for the intrathecal administration of antisense oligonucleotides (ASOs). ThecaFlex DRx™ offers a solution to repeated lumbar punctures for continuous intrathecal drug delivery, potentially enhancing patient comfort and expanding availability for a larger group of individuals with neurological conditions.

- May 2025: AMW GmbH, a specialized pharmaceutical firm concentrating on biodegradable controlled-release drug delivery systems, and AdhexPharma SAS, an independent pharmaceutical company known for developing and producing patches and oral films, announced today the successful completion of the transfer of transdermal delivery systems (TDS) as part of their strategic partnership. Following the partnership's initiation in 2021, AMW dedicated itself to its core business, while AdhexPharma assumed responsibility for the commercial manufacturing and lifecycle management of TDS products. After a 30-month transition phase, AdhexPharma acquired AMW's TDS manufacturing machinery and equipment, along with intellectual property for Buprenorphine and Rivastigmine, TDS products initially sourced from AMW's pipeline. The completion of this process was celebrated by both companies at AMW’s headquarters in Warngau on May 26, 2025.

- April 2025: Orchestra BioMed received FDA approval for its IDE amendment initiating the Virtue SAB pivotal trial for coronary in-stent restenosis treatment. The trial will randomize 740 patients comparing the sirolimus-angioinfusion balloon against Boston Scientific's AGENT paclitaxel-coated balloon with initiation targeted for second half 2025.

- March 2025: Vivani Medical announced successful first implant administration in its LIBERATE-1 trial evaluating NPM-115 GLP-1 exenatide implant for obesity and overweight patients. The company achieved full 24-patient enrollment within four weeks signaling strong interest in the six-month subdermal device addressing medication adherence challenges in metabolic diseases.

- March 2025: ANI Pharmaceuticals secured FDA approval for expanded ILUVIEN label adding chronic non-infectious uveitis affecting posterior segment indication. The fluocinolone acetonide intravitreal implant delivers sustained drug release up to 36 months reducing injection frequency for patients with retinal conditions.

Implantable Drug Delivery Devices Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Implantable Drug Eluting Stents, Implantable Contraceptive Drug Delivery Devices, Implantable Intraocular Drug Delivery Devices, Implantable Brachytherapy Seeds Devices, Implantable Drug Delivery Pump Devices |

| Technologies Covered | Biodegradable Implants, Non-Biodegradable Implants |

| Applications Covered | Oncology, Cardiovascular, Autoimmune Diseases, Obstetrics and Gynecology, Others |

| End Users Covered | Hospitals, Ambulatory Surgery Centers, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Abbott Laboratories, Boston Scientific Corporation, Delpor Inc., Koninklijke DSM N.V., Medtronic plc, Theragenics Corporation, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the implantable drug delivery devices market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global implantable drug delivery devices market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the implantable drug delivery devices industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Implantable Drug Delivery Devices Market Report

The implantable drug delivery devices market was valued at USD 16.2 Billion in 2025.

IMARC Group estimates the market to reach USD 28.0 Billion by 2034, exhibiting a CAGR of 6.25% during 2026-2034.

The market for implantable drug delivery devices is swiftly evolving due to AI-driven smart sensors, eco-friendly materials, and compact long-lasting implants. Real-time dosing algorithms and cloud connectivity enhance precision and reduce medication mistakes, while biodegradable systems remove the need for surgery and broaden therapeutic uses. Small, long-lasting implants improve compliance in managing chronic illnesses and aid outpatient treatment. Rising R&D expenditures, advancements in clinical trials, and the introduction of new products by top firms are jointly speeding up global market acceptance and defining the next wave of patient-focused treatments.

North America currently dominates the implantable drug delivery devices market, accounting for a share exceeding 40.7%. This dominance is fueled by presence of advanced healthcare infrastructure, high healthcare expenditure, and a strong focus on research and development in the region.

Some of the major players in the implantable drug delivery devices market include Abbott Laboratories, Boston Scientific Corporation, Delpor Inc., Koninklijke DSM N.V., Medtronic plc, Theragenics Corporation, etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)