India 3D Animation Market Size, Share, Trends and Forecast by Technique, Component, Deployment, Organization Size, End Use, and Region, 2026-2034

India 3D Animation Market Summary:

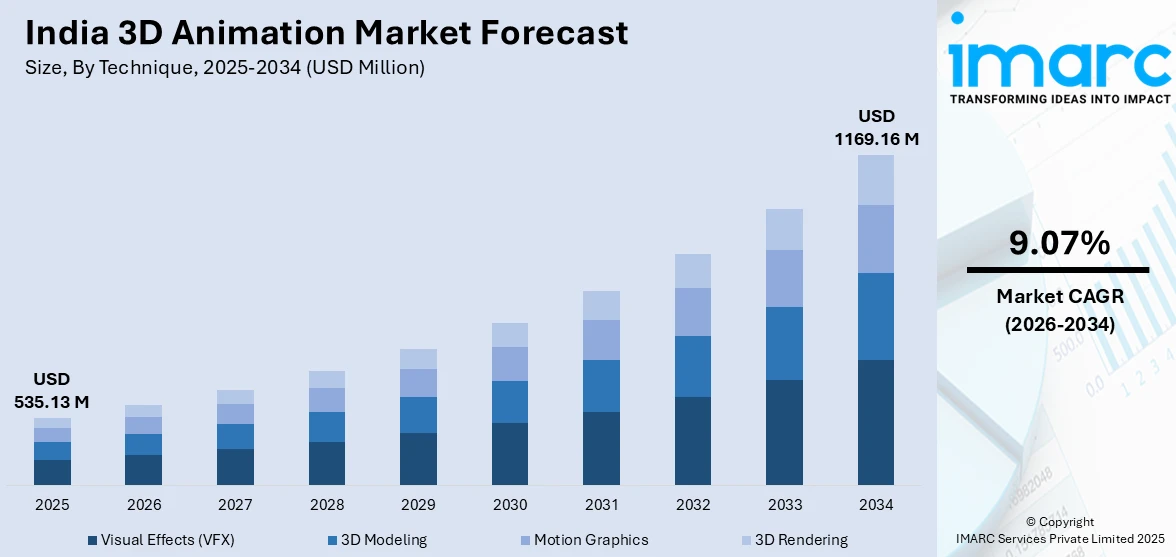

The India 3D animation market size was valued at USD 535.13 Million in 2025 and is projected to reach USD 1169.16 Million by 2034, growing at a compound annual growth rate of 9.07% from 2026-2034.

The India 3D animation industry is witnessing strong growth due to the increasing adoption of digital content consumption, growing demand for high-quality visual effects in the entertainment and advertising sectors, and the adoption of cloud-based animation solutions. The adoption of advanced rendering technologies, the growing gaming industry, and government initiatives to develop the creative economy of the country are driving the growth of the industry. The increasing investment in immersive storytelling, the adoption of artificial intelligence in animation, and the growing popularity of India as an outsourcing destination for global animation studios are collectively transforming the industry landscape and driving the India 3D animation market share.

Key Takeaways and Insights:

- By Technique: Visual effects (VFX) dominates the market with a share of 34.8% in 2025, driven by the surging demand for high-quality post-production services across feature films, streaming content, and advertising campaigns.

- By Component: Software leads the market with a share of 46.5% in 2025, supported by the increasing adoption of advanced modeling, rendering, and compositing tools that enhance creative workflows and production efficiency.

- By Deployment: On-demand dominates the market with a share of 58.9% in 2025, reflecting the growing preference for cloud-based animation platforms that offer scalable resources, remote collaboration capabilities, and cost-effective production solutions.

- By Organization Size: Large enterprises lead the market with a share of 62.4% in 2025, owing to their substantial content production budgets, established partnerships with global studios, and early adoption of cutting-edge animation technologies.

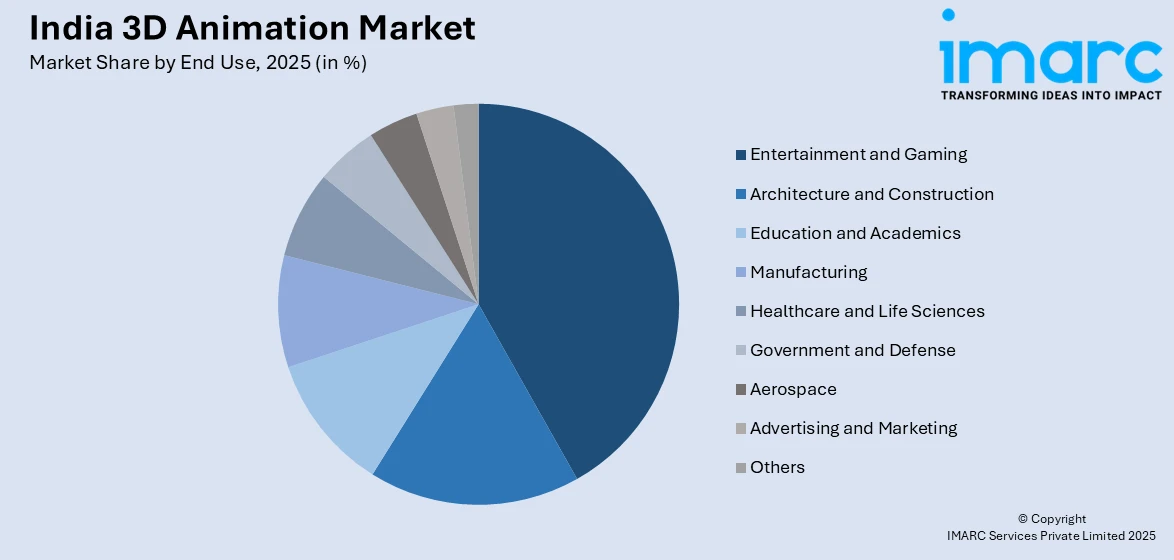

- By End Use: Entertainment and gaming represent the largest segment with a share of 41.7% 2025, fueled by the expanding OTT ecosystem, rising mobile gaming penetration, and growing consumer appetite for immersive visual experiences.

- By Region: West India dominates the market with a share of 36.2% in 2025, attributed to the concentration of leading animation and VFX studios in Mumbai and Pune, strong media infrastructure, and proximity to the country’s entertainment industry hub.

- Key Players: The India 3D animation market features a dynamic competitive landscape with established studios, emerging independent creators, and global service providers competing across segments through technological innovation, IP creation, and strategic international co-production partnerships.

To get more information on this market Request Sample

The India 3D animation market is witnessing transformative growth as the convergence of technological innovation, expanding digital infrastructure, and rising content demand reshapes the industry landscape. In December 2025, Green Gold Animation, the creator of the Chhota Bheem franchise, announced an ambitious ₹250 crore funding drive to expand content production and IP development, signaling strong investor confidence in Indian animation capabilities. The proliferation of OTT platforms and streaming services has created unprecedented opportunities for animated content production, while advancements in real-time rendering, motion capture, and virtual production technologies are elevating the quality and efficiency of domestic output. Government initiatives aimed at positioning India as a global hub for animation, visual effects, gaming, and extended reality are strengthening the ecosystem through skill development programs, dedicated infrastructure investments, and favorable policy frameworks. Meanwhile, the increasing integration of artificial intelligence and machine learning into animation pipelines is accelerating production timelines, enabling studios to handle larger and more complex projects.

India 3D animation Market Trends:

Integration of Artificial Intelligence in Animation Workflows

The adoption of artificial intelligence and machine learning technologies is rapidly transforming animation production pipelines across India. In September 2025, Singapore‑based creator‑tech company Animeta launched an AI Film Studio in Mumbai that blends human creativity with scalable AI tools to accelerate content creation and hybrid storytelling workflows, highlighting how Indian studios and ventures are operationalizing AI in animation production. Studios are leveraging AI-powered tools for automated character rigging, motion prediction, and intelligent rendering optimization, significantly reducing production timelines and costs. This technological shift is enabling creators to focus more on artistic storytelling while automating repetitive tasks, driving India 3D animation market growth.

Rise of Real-Time Rendering and Virtual Production

Real-time rendering engines are gaining significant traction among Indian animation studios, enabling instant visualization and iterative creative decision-making during production. According to reports, Epic Games’ Unreal Engine Shorts India Program concluded its inaugural edition in India, training animators and VFX creators from studios and production houses in real‑time rendering workflows and advanced engine tools, highlighting the rising local adoption of real‑time engines in professional pipelines. Virtual production techniques are being increasingly adopted for film, advertising, and gaming applications, allowing seamless integration of live-action footage with computer-generated environments. This trend is enhancing creative flexibility and accelerating content delivery across multiple industry verticals.

Expansion of Cloud-Based Collaborative Animation Platforms

Cloud-based animation platforms are experiencing accelerated adoption as studios embrace distributed workflows and remote collaboration capabilities. In August 2025, Yotta Data Services launched Urja, India’s first cloud‑native renderfarm‑as‑a‑service and media asset management platform built on sovereign hyperscale infrastructure, enabling animation and VFX studios to render complex 3D content and manage assets without costly on‑premises hardware. These platforms provide scalable computing resources for rendering, centralized asset management, and real-time multi-user editing environments. The shift toward cloud infrastructure is democratizing access to high-end animation tools, empowering smaller studios and independent creators to compete effectively with established industry players.

Market Outlook 2026-2034:

The India 3D animation market is expected to grow at a considerable pace during the forecast period due to strong government support for the creative sector, growing demand from the entertainment, gaming, and advertising sectors, and the growing popularity of India as a preferred outsourcing destination for animation and VFX services. The growing adoption of streaming services, the increasing adoption of smartphones in tier-two and tier-three cities, and the growing adoption of immersive technologies such as augmented and virtual reality are expected to create new revenue streams. The market generated a revenue of USD 535.13 Million in 2025 and is projected to reach a revenue of USD 1169.16 Million by 2034, growing at a compound annual growth rate of 9.07% from 2026-2034.

India 3D Animation Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Technique |

Visual Effects (VFX) |

34.8% |

|

Component |

Software |

46.5% |

|

Deployment |

On-Demand |

58.9% |

|

Organization Size |

Large Enterprises |

62.4% |

|

End Use |

Entertainment and Gaming |

41.7% |

|

Region |

West India |

36.2% |

Technique Insights:

- 3D Modeling

- Motion Graphics

- 3D Rendering

- Visual Effects (VFX)

The visual effects (VFX) dominates with a market share of 34.8% of the total India 3D animation market in 2025.

The visual effects segment commands the largest share of the India 3D animation market, driven by the escalating demand for cinematic-quality post-production services across Bollywood, regional cinema, and international co-productions. Indian VFX studios are increasingly collaborating on global blockbusters, for instance, London‑based DNEG (with a significant Indian creative workforce) is partnering on an ambitious Ramayana film project directed by Nitesh Tiwari, signaling India’s growing role in high‑end visual effects on the world stage. The growing volume of VFX-intensive content for OTT platforms and advertising campaigns is further reinforcing this segment’s dominance.

In addition, the rising trend of outsourcing VFX work from foreign studios to India, due to the cost advantage and talent pool available in the country, is further adding to the growth of the segment. The development of compositing software, particle simulation, and digital matte painting is making it possible for studios to create complex visual effects. The integration of VFX with virtual production is also opening up new avenues for creativity and making visual effects the backbone of the animation industry in India.

Component Insights:

- Hardware

- Software

- Consulting

- Support and Maintenance

- Integration and Deployment

- Education and Training

- Services

The software leads with a share of 46.5% of the total India 3D animation market in 2025.

The software segment holds the largest market share, underpinned by the widespread adoption of professional-grade animation, rendering, and compositing tools across studios of all sizes. The growing availability of subscription-based licensing models has lowered entry barriers, enabling a broader range of creative professionals to access industry-standard software platforms. Continuous upgrades incorporating real-time rendering capabilities, AI-assisted workflows, and cloud-based collaboration features are strengthening the value proposition of animation software solutions.

Furthermore, the expansion of educational institutions offering animation and VFX courses is driving sustained demand for specialized software licenses. Indian studios are increasingly investing in integrated software ecosystems that streamline the entire production pipeline from pre-visualization through final output. The rising adoption of open-source and hybrid software solutions is also reshaping competitive dynamics, providing studios with greater flexibility in customizing their creative toolsets to meet diverse project requirements.

Deployment Insights:

- On-Premise

- On-Demand

The on-demand dominates with a market share of 58.9% of the total India 3D animation market in 2025.

The on-demand deployment model commands the largest market share, driven by the increasing preference for cloud-based infrastructure that offers scalable rendering capacity, flexible resource allocation, and reduced upfront capital expenditure. Studios are migrating to on-demand platforms to enable seamless remote collaboration, particularly as distributed production workflows have become standard industry practice. The ability to scale computing resources dynamically based on project requirements provides significant cost efficiency advantages.

The growing availability of high-speed internet connectivity across Indian cities and the maturation of cloud rendering services are accelerating adoption of on-demand solutions. These platforms facilitate real-time project management, centralized asset storage, and secure content delivery, making them particularly attractive for studios handling multiple concurrent projects. The on-demand model is also enabling smaller studios and freelance animators to access enterprise-grade infrastructure without significant hardware investments.

Organization Size Insights:

- Small and Medium-sized Enterprises (SMEs)

- Large Enterprises

The large enterprises leads with a share of 62.4% of the total India 3D animation market in 2025.

Large enterprises dominate the India 3D animation market, leveraging their substantial production budgets, advanced technological infrastructure, and established relationships with global content distributors and streaming platforms. These organizations maintain dedicated in-house animation teams equipped with state-of-the-art hardware and software, enabling them to undertake complex, high-volume production projects that require consistent quality standards and timely delivery across multiple content formats.

The strategic advantage of large enterprises extends to their capacity for significant research and development investments, facilitating the early adoption of emerging technologies such as virtual production, AI-driven animation, and immersive content creation. Their ability to secure large-scale international outsourcing contracts and co-production partnerships further strengthens their market position. Additionally, large enterprises benefit from established intellectual property portfolios and distribution networks that generate recurring revenue streams.

End Use Insights:

Access the comprehensive market breakdown Request Sample

- Entertainment and Gaming

- Architecture and Construction

- Education and Academics

- Manufacturing

- Automotive

- Electronics

- Others

- Healthcare and Life Sciences

- Government and Defense

- Aerospace

- Advertising and Marketing

- Others

The entertainment and gaming dominates with a market share of 41.7% of the total India 3D animation market in 2025.

The entertainment and gaming segment represents the largest end-use category in the India 3D animation market, propelled by the explosive growth of over-the-top streaming platforms, the expanding domestic film industry, and the rapid proliferation of mobile gaming across the country. Indian streaming platforms have even begun tapping into the gaming craze by featuring gaming‑centric reality shows and scripted series to broaden viewership and engagement among younger audiences, reflecting how entertainment and gaming are increasingly intersecting in content strategies. The demand for high-quality animated content spanning feature films, television series, web series, and interactive gaming experiences has surged as digital content consumption patterns continue to evolve among Indian audiences.

The gaming sub-segment is emerging as a particularly dynamic growth driver, with the increasing penetration of smartphones and affordable mobile internet catalyzing demand for visually sophisticated gaming content. The growing trend of Indian studios developing original intellectual properties for both domestic and international audiences is creating new opportunities. Additionally, the convergence of animation with live-action content through VFX-intensive productions continues to expand the addressable market for entertainment-focused animation services.

Regional Insights:

- North India

- South India

- East India

- West India

West India exhibits a clear dominance with a 36.2% share of the total India 3D animation market in 2025.

West India commands the largest regional share in the India 3D animation market, anchored by the presence of a well-established media and entertainment ecosystem concentrated in Mumbai and Pune. The region hosts a significant concentration of leading animation studios, VFX facilities, and post-production houses that serve both the domestic film industry and international clients. The strong infrastructure for content creation, including dedicated animation parks and technology hubs, provides a competitive advantage for studios operating in the region.

The regional government’s proactive policy support for the animation, visual effects, gaming, comics, and extended reality sector is further strengthening the ecosystem by providing financial incentives, infrastructure development, and workforce training initiatives. West India’s proximity to the commercial heart of the Indian entertainment industry, combined with robust digital connectivity and a deep talent pool from established educational institutions, continues to attract investments and reinforce its leadership position in the national market.

Market Dynamics:

Growth Drivers:

Why is the India 3D Animation Market Growing?

Expanding Digital Content Ecosystem and OTT Platform Proliferation

The rapid expansion of India’s digital content ecosystem, led by the proliferation of over-the-top streaming platforms and the growing consumption of video content across mobile devices, is driving substantial demand for high-quality 3D animation services. In November 2025, Indian OTT aggregator OTTplay partnered with Studio Jadu to syndicate a lineup of AI‑enabled animated series, one of the first OTT animation syndication deals of its kind globally, signaling how digital platforms are accelerating the distribution of innovative animated content. The increasing number of streaming platforms commissioning original animated series, feature films, and interactive content has created a sustained pipeline of production opportunities for domestic studios. This content boom extends beyond traditional entertainment into advertising, where brands are leveraging animated content for digital marketing campaigns to engage increasingly connected consumer audiences. The shift from traditional broadcast to digital-first content strategies is reshaping production budgets and priorities, with animation emerging as a preferred medium for storytelling that transcends language barriers and appeals to diverse demographic segments across the country.

Government Initiatives and Policy Support for Creative Industries

The Indian government’s strategic focus on developing the animation, visual effects, gaming, comics, and extended reality sector as a cornerstone of the national creative economy is providing substantial impetus to market growth. In September 2024, the Union Cabinet approved the establishment of the National Centre of Excellence (NCoE) for Animation, Visual Effects, Gaming, Comics and Extended Reality, a dedicated apex institution to anchor skills development, industry standards, and global collaboration on par with premier technical institutes. National and state-level policy frameworks are being implemented to create dedicated infrastructure, establish centers of excellence, and develop structured skill development programs aimed at building a globally competitive workforce. These initiatives include financial incentives for studios, capital subsidies for equipment and technology acquisition, and support for international participation at global content markets. The recognition of creative industries as essential services and the establishment of dedicated institutional frameworks for talent development are creating a favorable environment for investment, innovation, and the long-term sustainability of the animation ecosystem.

Rising Global Outsourcing Demand and India’s Cost Competitiveness

India’s position as a preferred destination for global animation and VFX outsourcing continues to strengthen, driven by the country’s significant cost advantages, large pool of skilled creative professionals, and improving technical infrastructure. Major international studios are increasingly expanding their footprint in India, for example, British‑Indian visual effects and animation giant DNEG, which already employs around 3,000 people in India across VFX and animation, announced plans to hire 300 additional staff as part of its India expansion efforts, underscoring growing confidence in local talent and capabilities. International studios and production houses are increasingly routing complex animation and post-production work to Indian facilities, attracted by cost savings that do not compromise quality standards. The maturation of Indian studios from service-only operations to creative co-production partners capable of developing original intellectual property is further enhancing the country’s value proposition. The diversification of outsourcing relationships beyond traditional Hollywood partnerships to include studios from Europe, Asia, and emerging content markets is broadening revenue streams.

Market Restraints:

What Challenges the India 3D Animation Market is Facing?

Persistent Talent Shortage and Skill Gap

Despite a large young population, the India 3D animation market faces a significant shortage of highly skilled professionals capable of meeting the quality demands of international productions. The gap between academic training and industry-ready skills remains substantial, with many graduates lacking proficiency in advanced tools, real-time rendering workflows, and specialized disciplines such as character animation, procedural effects, and virtual production. This talent constraint limits the capacity of studios to scale operations and undertake high-value projects efficiently.

High Infrastructure and Technology Acquisition Costs

The significant capital investment required for establishing and maintaining state-of-the-art animation production infrastructure poses a barrier, particularly for small and medium-sized studios. The costs associated with high-performance computing hardware, professional software licenses, rendering farms, and motion capture equipment remain substantial. While cloud-based alternatives are emerging, the recurring costs of bandwidth and cloud computing at production scale can strain operational budgets, limiting the ability of emerging studios to compete effectively against larger, well-capitalized enterprises.

Intellectual Property Protection Challenges

Concerns over intellectual property security and content piracy continue to challenge the India 3D animation market. International clients often require stringent content protection protocols that smaller Indian studios may struggle to implement comprehensively. The evolving nature of digital content distribution creates ongoing vulnerabilities, and the complexity of enforcing IP rights across multiple jurisdictions discourages some international partners from engaging in full co-production arrangements, limiting the scope of collaborative opportunities for Indian studios.

Competitive Landscape:

The India 3D animation market exhibits a moderately fragmented competitive landscape characterized by a diverse mix of established domestic studios, international production houses with Indian operations, and a growing number of emerging independent creators and boutique studios. Competition is primarily driven by technological capabilities, creative quality, pricing strategies, and the ability to deliver content within tight production timelines. Market participants are increasingly investing in advanced production technologies, including real-time rendering engines, artificial intelligence-assisted workflows, and virtual production pipelines, to differentiate their service offerings and secure higher-value projects. Strategic partnerships and international co-production arrangements are becoming central to competitive positioning, enabling studios to access global markets and diversify revenue streams. The market is also witnessing a notable shift from purely service-oriented models toward original intellectual property development, as studios seek to capture greater value from their creative output and establish sustainable competitive advantages.

Recent Developments:

-

In February 2026, Union Budget highlights the expansion of the AVGC sector (Animation, Visual Effects, Gaming & Comics), allocating funds to set up creator labs in 15,000 schools and 500 colleges. This initiative aims to nurture digital talent and position India as a global creative tech hub.

India 3D Animation Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

Million USD |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Techniques Covered |

3D Modeling, Motion Graphics, 3D Rendering, Visual Effects (VFX) |

|

Components Covered |

|

|

Deployments Covered |

On-Premise, On-Demand |

|

Organization Sizes Covered |

Small and Medium-sized Enterprises (SMEs), Large Enterprises |

|

End Uses Covered |

|

|

Regions Covered |

North India, South India, East India, West India |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India 3D Animation Market Report

The India 3D animation market size was valued at USD 535.13 Million in 2025.

The India 3D animation market is expected to grow at a compound annual growth rate of 9.07% from 2026-2034 to reach USD 1169.16 Million by 2034.

Visual effects (VFX) holds the largest share at 34.8%, driven by surging demand for cinematic-quality post-production services across domestic and international film productions, OTT content, and digital advertising.

Key factors driving the India 3D animation market include expanding digital content consumption through OTT platforms, government policy support for creative industries, rising global outsourcing demand, technological advancements in AI and real-time rendering, and growing mobile gaming penetration.

Major challenges include persistent talent shortages and skill gaps, high infrastructure and technology acquisition costs, intellectual property protection concerns, inconsistent quality standards across smaller studios, and limited access to financing for independent creators.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)