India Acetic Acid Market Size, Share, Trends and Forecast by Application, End Use Industry, and Region, 2026-2034

India Acetic Acid Market Summary:

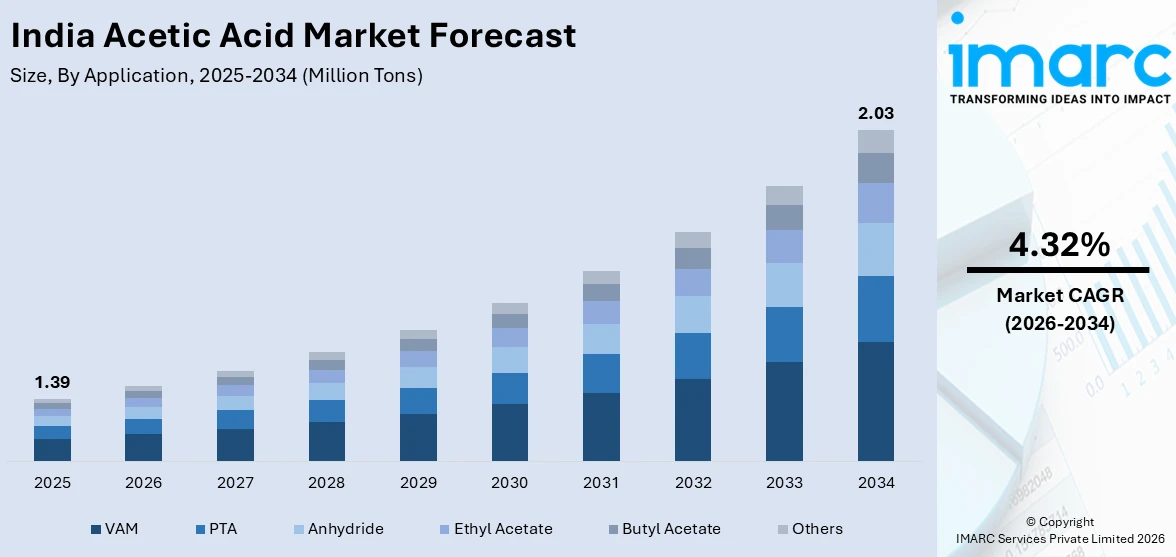

The India acetic acid market size reached 1.39 Million Tons in 2025 and is projected to reach 2.03 Million Tons by 2034, growing at a compound annual growth rate of 4.32% from 2026-2034.

The India acetic acid market is driven by rising demand from downstream industries such as textiles, paints and coatings, adhesives, and packaging, where acetic acid is widely used as a key chemical intermediate. Expanding chemical manufacturing and increasing consumption of derivatives like vinyl acetate monomer and purified terephthalic acid are further supporting market growth. Additionally, the rapid development of the food processing sector and the growing use of preservatives and vinegar-based ingredients are contributing to the increasing demand for acetic acid across the country.

Key Takeaways and Insights:

- By Application: VAM dominated the market with a 42% share in 2025. This leading position is driven by high demand for VAM-derived adhesives and paints in the construction and automotive sectors.

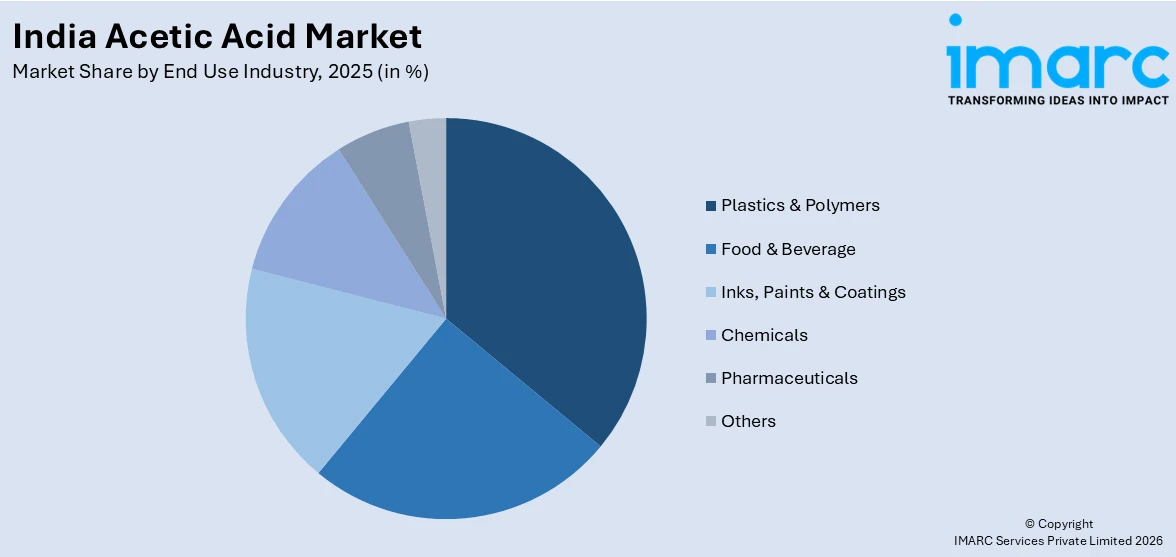

- By End Use Industry: Plastics & polymers represent the largest revenue share of 36% in 2025. Its dominating presence is attributed to the extensive use of acetic acid in producing PET resins and polyester fibers.

- Key Players: The India acetic acid market features a competitive mix of domestic manufacturers and global chemical companies. Competition is driven by production capacity, cost efficiency, and integration with downstream derivatives. Market participants focus on technology upgrades, supply chain strengthening, and expanding domestic manufacturing capabilities to improve competitiveness and meet growing industrial demand.

To get more information on this market Request Sample

The India acetic acid market is primarily driven by strong demand from key downstream industries such as textiles, chemicals, plastics, paints and coatings, and adhesives. Acetic acid serves as a critical intermediate in the production of several derivatives, including vinyl acetate monomer, acetic anhydride, and acetate esters, which are widely used in industrial manufacturing processes. As India’s industrial base continues to expand, the need for these chemical intermediates is increasing, supporting higher acetic acid consumption across multiple sectors. Another major growth driver is the expansion of the food processing and packaging industries, where food-grade acetic acid is used in vinegar production and as a preservative in packaged foods. Additionally, ongoing investments in domestic chemical manufacturing and improvements in industrial infrastructure are encouraging local production and strengthening supply chains. Rising demand from pharmaceuticals, solvents, and specialty chemicals further contributes to market growth, as manufacturers increasingly rely on acetic acid as a versatile building block in a wide range of chemical formulations and industrial applications.

India Acetic Acid Market Trends:

Rising Bio-based Production:

Sustainability considerations are increasingly influencing production strategies in the India acetic acid market. Manufacturers are exploring bio-based production pathways that utilize renewable feedstocks such as agricultural residues and other biomass resources. This shift reflects a broader industry effort to lower environmental impact, reduce reliance on fossil-based raw materials, and align with global decarbonization goals. As environmental awareness grows and industries pursue greener chemical inputs, bio-based acetic acid is gaining attention as a viable alternative. Continued research and process innovation are expected to gradually support the adoption of more sustainable production methods within the market.

Technological Advancements in VAM:

Advancements in chemical processing and polymer technologies are strengthening the demand for vinyl acetate monomer (VAM), one of the most significant downstream applications of acetic acid. Improvements in catalyst efficiency, process optimization, and polymer formulation are enhancing the performance and versatility of VAM-based products. These developments are expanding the use of VAM in applications such as adhesives, coatings, sealants, and packaging materials. As industries continue to prioritize high-performance materials and efficient manufacturing processes, technological innovation in VAM production and utilization is expected to remain an important trend influencing acetic acid consumption in India.

Expanding Pharmaceutical Applications:

The pharmaceutical industry is emerging as an increasingly important end-use segment for acetic acid in India. The India pharmaceutical market size was valued at USD 68.38 Billion in 2025 and is projected to reach USD 174.67 Billion by 2034, growing at a compound annual growth rate of 10.98% from 2026-2034. The compound is widely used as a chemical intermediate in the synthesis of various active pharmaceutical ingredients and specialty formulations. As the country continues to strengthen its pharmaceutical manufacturing capabilities and expand healthcare production, the demand for reliable chemical building blocks is rising. Acetic acid’s versatility in chemical reactions makes it valuable in multiple stages of drug synthesis and formulation development. This growing integration of acetic acid in pharmaceutical processes is expected to support broader application opportunities within the sector.

Market Outlook 2026-2034:

The India acetic acid market is expected to witness steady growth over the coming years, supported by expanding demand from key industries such as textiles, chemicals, pharmaceuticals, and food processing. Increasing consumption of acetic acid derivatives, including vinyl acetate monomer and acetate esters, will continue to strengthen market prospects. In addition, ongoing investments in domestic chemical manufacturing and improvements in industrial infrastructure are enhancing production capabilities and supply reliability. Growing emphasis on sustainable production methods and the development of bio-based alternatives are also expected to shape the long-term outlook of the market. The market size was estimated at 1.39 Million Tons in 2025 and is expected to reach 2.03 Million Tons by 2034, reflecting a compound annual growth rate of 4.32% over the forecast period 2026-2034.

India Acetic Acid Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Application |

VAM |

42% |

|

End Use Industry |

Plastics & Polymers |

36% |

Application Insights:

- VAM

- PTA

- Anhydride

- Ethyl Acetate

- Butyl Acetate

- Others

VAM dominates with a market share of 42% of the total India acetic acid market in 2025.

Vinyl acetate monomer (VAM) accounts for the largest share of acetic acid consumption in India because it serves as a key intermediate in producing a wide range of polymers and resins. The India vinyl acetate monomer market size reached USD 300.0 Million in 2024. Looking forward, IMARC Group expects the market to reach USD 450.0 Million by 2033, exhibiting a growth rate (CAGR) of 4.51% during 2025-2033. VAM is widely used to manufacture polyvinyl acetate and polyvinyl alcohol, which are essential components in adhesives, paints, coatings, and packaging materials. Rapid growth in construction, furniture manufacturing, packaging, and consumer goods industries has significantly increased demand for these applications. As these sectors continue to expand, the requirement for VAM-based polymers remains strong, sustaining its dominant position in acetic acid utilization.

Another major factor supporting the dominance of VAM is its broad application in construction materials, textile processing, and paper manufacturing. VAM-derived polymers are widely used in emulsion adhesives, sealants, and coatings that enhance durability, flexibility, and bonding strength in construction and industrial products. In the textile sector, VAM-based chemicals are used in fabric finishing and coating processes. The continuous expansion of infrastructure development, housing projects, and textile production in India is therefore driving consistent demand for VAM, reinforcing its role as the leading application segment in the acetic acid market.

End Use Industry Insights:

Access the comprehensive market breakdown Request Sample

- Plastics & Polymers

- Food & Beverage

- Inks, Paints & Coatings

- Chemicals

- Pharmaceuticals

- Others

Plastics & polymers leads with a share of 36% of the total India acetic acid market in 2025.

Plastics and polymers represent the largest application segment in the India acetic acid market because acetic acid is a key raw material in the production of several polymer intermediates. It is widely used to manufacture derivatives such as vinyl acetate monomer and acetate esters, which serve as important building blocks for polymer resins, coatings, adhesives, and films. These materials are essential in a wide range of manufacturing processes. As polymer production continues to expand to meet industrial and consumer demand, the requirement for acetic acid as a chemical feedstock remains consistently strong.

The growing consumption of plastic materials across packaging, consumer goods, automotive components, and construction products further strengthens the dominance of this segment. Polymer-based materials are valued for their durability, flexibility, and lightweight characteristics, making them suitable for diverse applications. Industries involved in packaging films, containers, and protective materials rely heavily on polymer compounds derived from acetic acid intermediates. As demand for packaged products, durable goods, and industrial materials continues to increase in India, plastics and polymers remain a major driver of acetic acid consumption.

Region Insights:

- North India

- West and Central India

- South India

- East India

The acetic acid market in North India is driven by strong demand from textile processing, pharmaceuticals, and food processing industries across states such as Uttar Pradesh, Haryana, and Punjab. The region’s growing packaging and chemical manufacturing base also supports consumption of acetic acid derivatives used in adhesives, coatings, and solvents, contributing to steady industrial demand.

West and Central India represent a major hub for chemical manufacturing, with strong demand generated by large petrochemical, polymer, and specialty chemical industries. The presence of well-developed industrial corridors, refineries, and chemical processing clusters supports large-scale production and consumption of acetic acid and its derivatives for plastics, coatings, and industrial solvents.

In South India, the acetic acid market is supported by expanding pharmaceutical manufacturing, textile production, and food processing industries. The region also hosts several chemical and industrial manufacturing facilities that rely on acetic acid as an intermediate for producing coatings, solvents, and specialty chemicals, creating consistent demand across multiple sectors.

The market in East India is driven by the gradual expansion of chemical processing, packaging, and textile industries. Increasing industrial development and growing consumption of adhesives, coatings, and solvents in manufacturing activities are supporting acetic acid demand. Improving infrastructure and industrial investments are also contributing to the region’s emerging role in the market.

Market Dynamics:

Growth Drivers:

Why is the India Acetic Acid Market Growing?

Robust Downstream Industrial Demand

Strong expansion across several industrial sectors is creating sustained demand for acetic acid and its derivatives in India. Industries such as textiles, automotive manufacturing, paints and coatings, and construction increasingly rely on acetic acid–based intermediates for applications including solvents, adhesives, and surface treatment chemicals. As manufacturing activity continues to diversify and scale up, the need for reliable chemical inputs used in dyeing, coatings, and industrial formulations is also rising. This broadening industrial base is encouraging greater consumption of acetic acid across multiple value chains, reinforcing its importance as a key intermediate supporting growth in various downstream manufacturing segments.

Government “Make in India” Initiative

Domestic production policy efforts are also contributing to the empowerment of the ecosystem of chemical production in India, such as the acetic acid industry. The initiatives undertaken by the government to increase the domestic industrial capacity and decrease reliance on foreign chemicals are stimulating investments in the new production plants and renewal of technologies. These programs help in building modern chemical value chains across the nation, which enhances the stability of supply to the downstream sectors. With the development of domestic manufacturing and the ongoing enhancement of industrial infrastructure, chemical manufacturers are starting to take a closer look at ways of developing local production capacity and reinforcing the role of India as a force in the international chemical market.

Growing Food Processing Sector

The steady expansion of India’s food processing industry is contributing to rising demand for food-grade acetic acid. The compound finds many applications as a primary ingredient in the manufacturing of vinegar and as a good preservative in many packaged and processed food items. Due to the changing tastes of consumers who prefer convenient and shelf-stable foods and ready-to-prepare foods, manufacturers are increasingly considering ways to add preservation solutions that can preserve the quality of the product and add shelf life. This changing consumption trend, along with the increase in the number of organized food processing and packaged food distribution, is providing more opportunities for the use of acetic acid in food-related formulations.

Market Restraints:

What Challenges the India Acetic Acid Market is Facing?

Raw Material Price Volatility

The India acetic acid market is very sensitive to changes in the prices of the feedstocks at which it is very sensitive like methanol and natural gas. Fluctuations in these input prices directly influence manufacturing expenses and can significantly affect the profit margins of producers. The fluctuation of raw material prices may also affect the long-term plans of procurement by establishing a problem of uncertainty in the supply contracts and the general pricing trend in the domestic acetic acid industry.

Stringent Environmental Regulations

Manufacturers operating in the India acetic acid industry must comply with increasingly strict environmental regulations related to emissions, wastewater discharge, and chemical waste management. To fulfill these compliance requirements, investments in pollution control mechanisms, cleaner production technologies, and monitoring infrastructure are usually required. Such regulations may increase the expense of operation and pose a financial burden, especially to the small producers who want to remain competitive.

Supply Chain and Logistic Challenges

The acetic acid supply chain can face disruptions due to transportation delays, port congestion, and broader geopolitical uncertainties affecting trade routes. Such challenges may lead to inconsistent raw material availability and increased freight and logistics expenses. As a result, manufacturers and downstream users may encounter procurement difficulties, which can influence production schedules and overall supply stability in the domestic market.

Competitive Landscape:

The India acetic acid market features a moderately consolidated competitive landscape, with a mix of domestic chemical manufacturers and multinational companies competing across production, technology, and supply capabilities. Major domestic producers focus on integrated manufacturing, cost-efficient feedstock sourcing, and strong distribution networks to maintain market presence. Companies are increasingly investing in capacity expansion, process optimization, and downstream derivative production to strengthen their value chain position. Competition is further shaped by the presence of global acetyl chain producers that bring advanced technologies and high-purity product offerings to the market. Market participants are also emphasizing sustainability initiatives, including bio-based acetic acid production and energy-efficient manufacturing processes. Strategic collaborations, technology partnerships, and product diversification across end-use sectors such as textiles, pharmaceuticals, and chemicals are emerging as key competitive strategies in the evolving market landscape

Recent Developments:

- November 2024: INEOS Acetyls and Gujarat Narmada Valley Fertilizers & Chemicals Ltd entered a memorandum of understanding to jointly assess the feasibility of establishing a large-scale acetic acid facility with a capacity of 600 kilotonnes per year. The proposed plant is planned for GNFC’s manufacturing complex located in Bharuch, Gujarat, India.

India Acetic Acid Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million Tons |

| Scope of The Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Applications Covered | VAM, PTA, Anhydride, Ethyl Acetate, Butyl Acetate, Others |

| End Use Industries Covered | Plastics & Polymers, Food & Beverage, Inks, Paints & Coatings, Chemicals, Pharmaceuticals, Others |

| Region Covered | North India, West and Central India, South India, East India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Acetic Acid Market Report

The India acetic acid market reached a volume of 1.39 Million Tons in 2025.

The India acetic acid market is expected to grow at a compound annual growth rate of 4.32% from 2026-2034 to reach 2.03 Million Tons by 2034.

VAM application held the largest share of 42% in 2025, driven by its extensive use in adhesives and paints.

Key factors driving the India acetic acid market include rising demand from the plastics, textile, and pharmaceutical industries, alongside government initiatives like "Make in India" that promote domestic chemical manufacturing.

Major challenges include the high volatility of raw material prices (such as methanol), stringent environmental compliance requirements, and logistical constraints that lead to supply chain uncertainties.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade