India Air Conditioning Market Size, Share, Trends and Forecast by Type, Application, and Region, 2026-2034

India Air Conditioning Market Size, Share, Trends & Forecast (2026-2034)

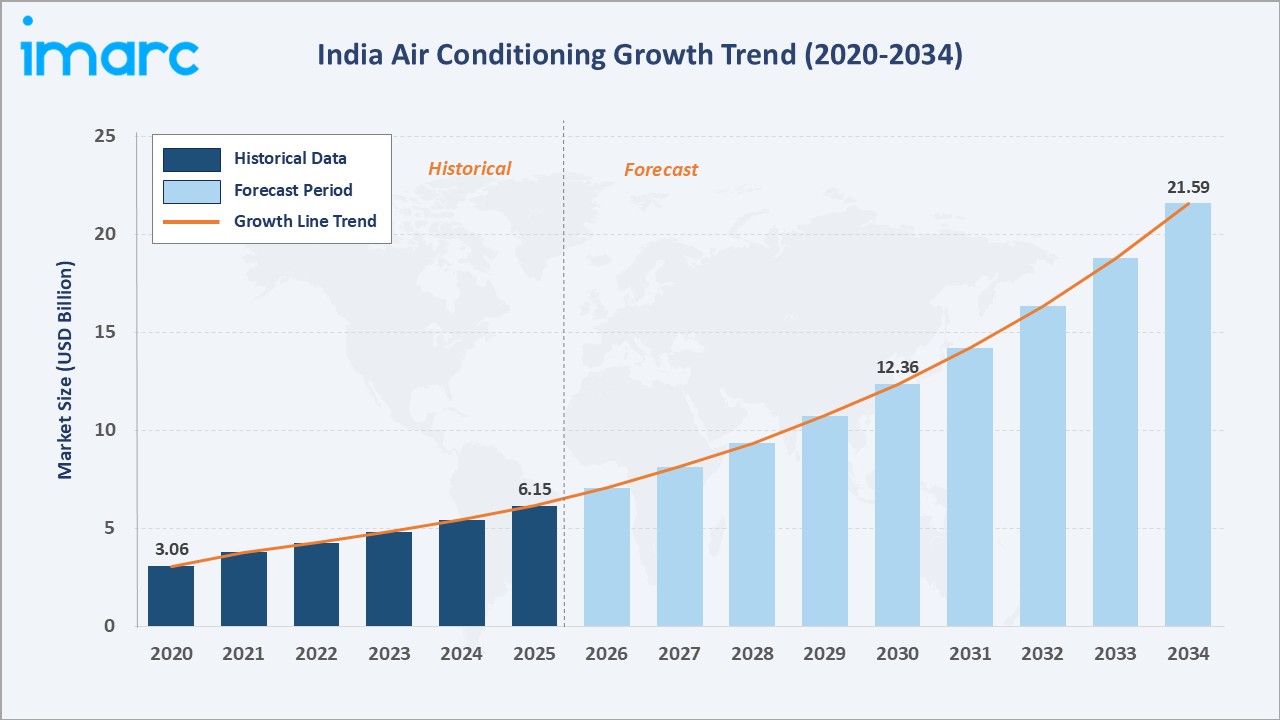

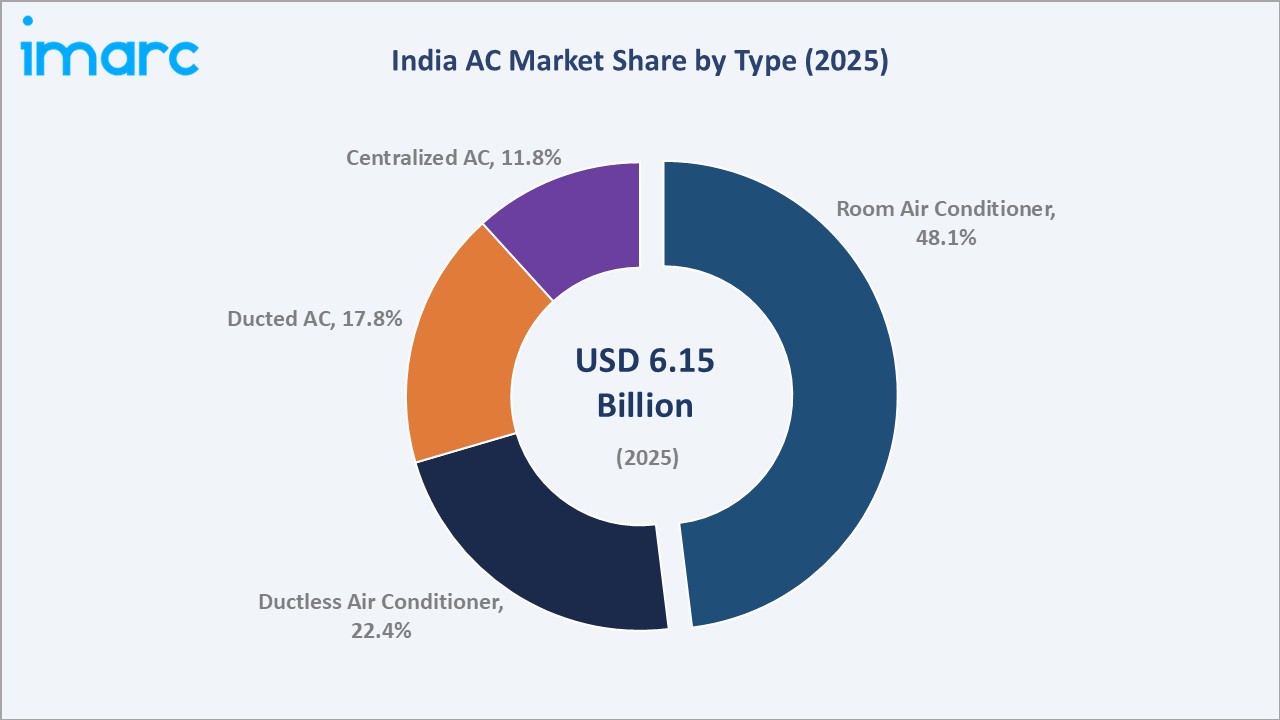

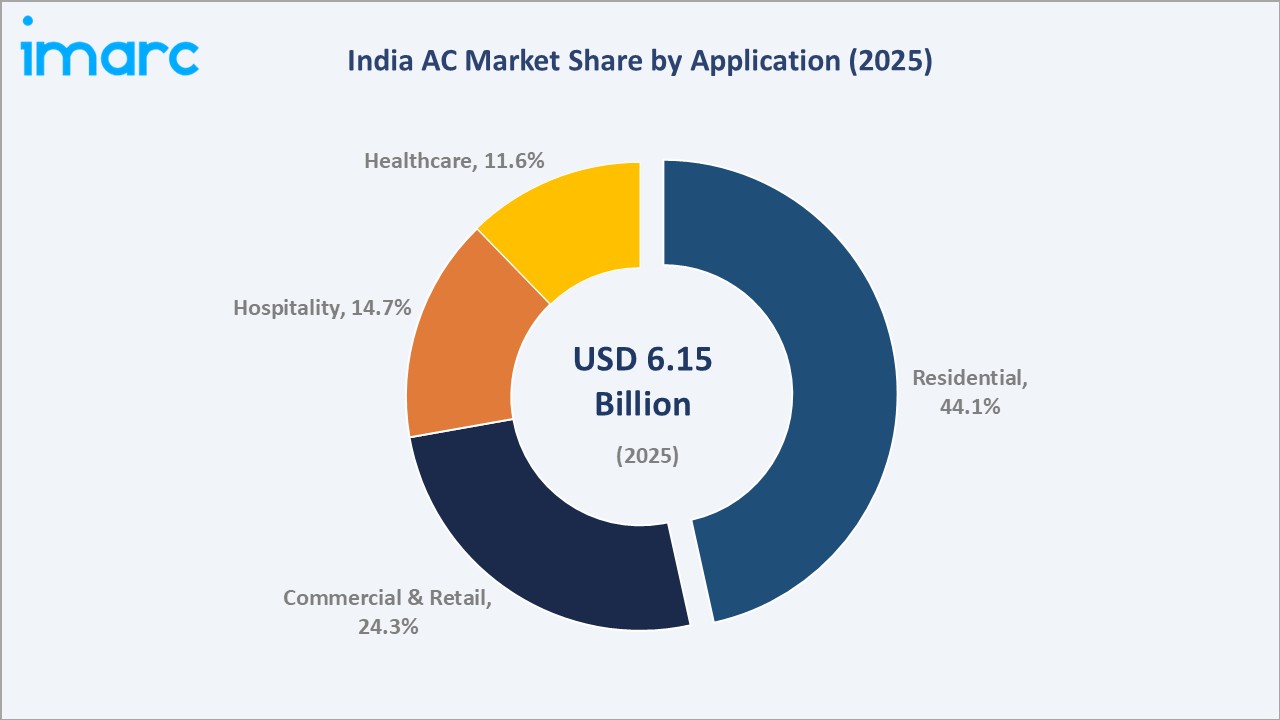

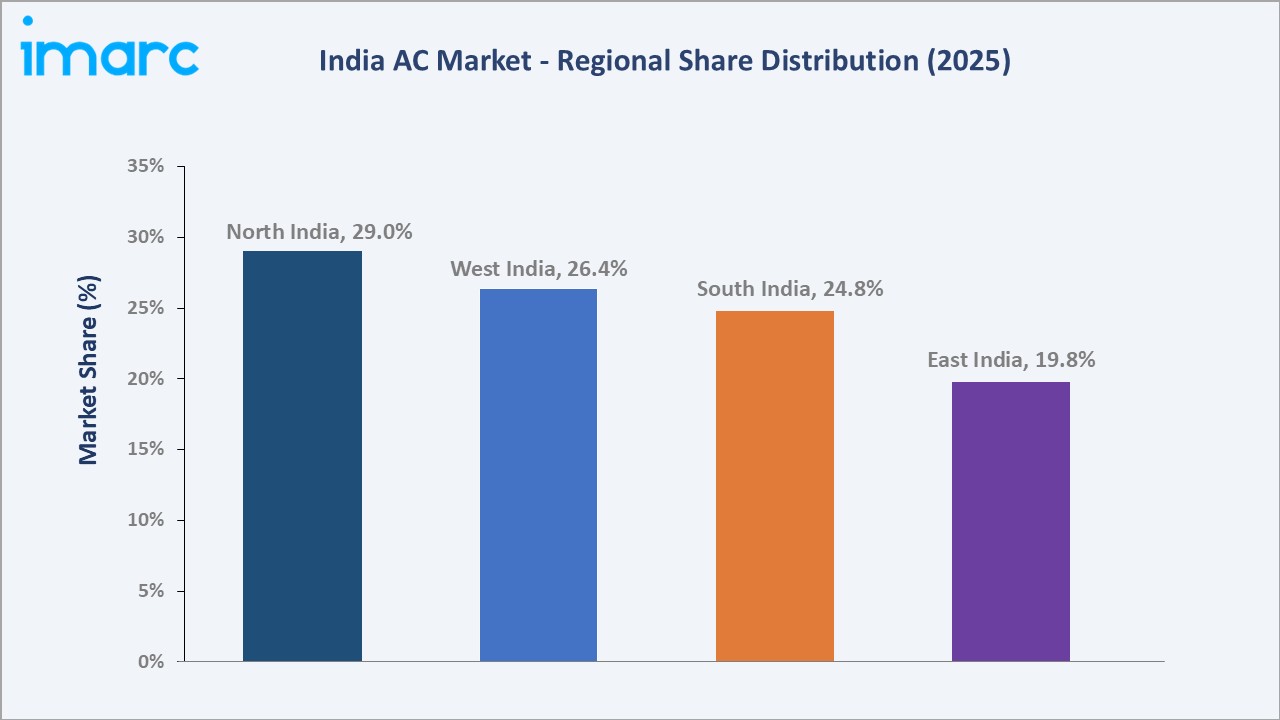

The India air conditioning market size was valued at USD 6.15 Billion in 2025 and is projected to reach USD 21.59 Billion by 2034, growing at a CAGR of 14.98% during 2026-2034. Rising temperatures, rapid urbanization, and expanding real estate construction are the primary growth drivers. Room Air Conditioners lead with a 48.05% share in 2025, while Residential applications dominate at 44.05%. North India commands the largest regional share at 29%, supported by climatic conditions and growing urban middle-class demand.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 6.15 Billion |

|

Forecast Market Size (2034) |

USD 21.59 Billion |

|

CAGR (2026-2034) |

14.98% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North India (29% share, 2025) |

|

Fastest Growing Region |

South India |

|

Leading Type |

Room Air Conditioner (48.05%, 2025) |

|

Leading Application |

Residential (44.05%, 2025) |

The chart below tracks India's air conditioning market growth from 2020–2034, illustrating post-pandemic demand recovery in the historical period and sustained CAGR-driven expansion across the forecast horizon.

To get more information on this market, Request Sample

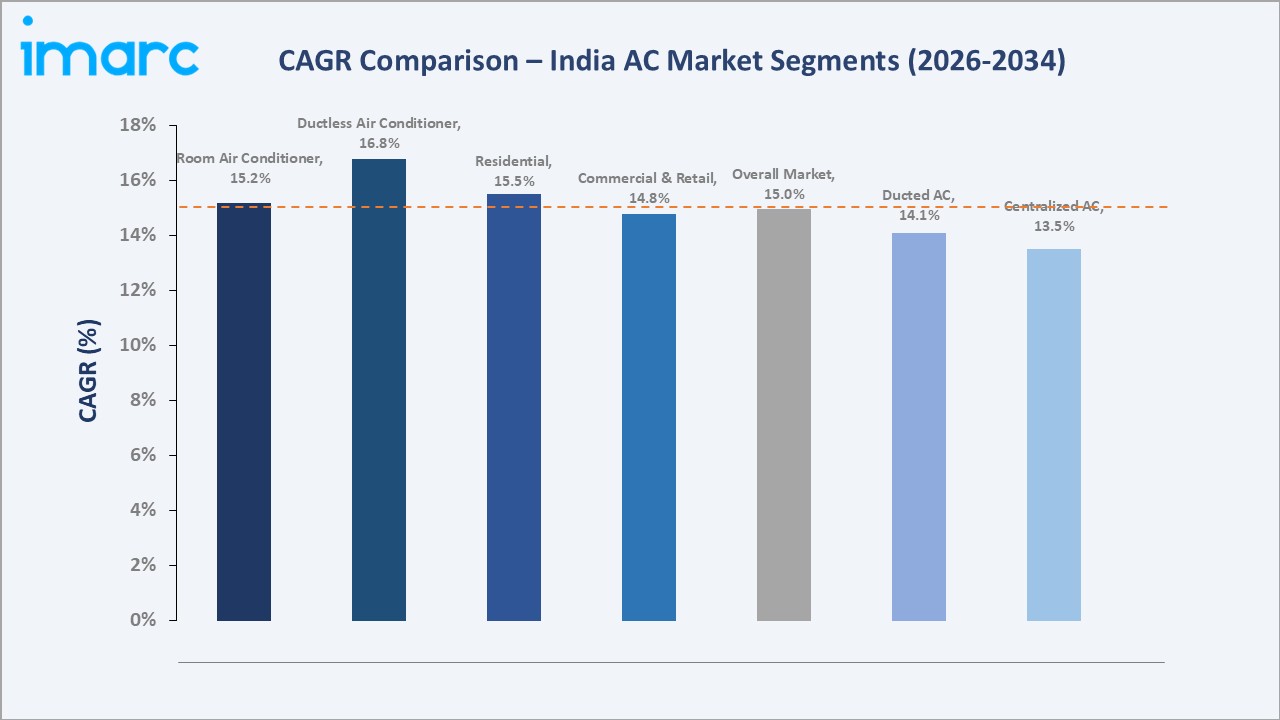

CAGR analysis across key segments reveals Room AC and Ductless AC as the fastest-growing product categories, with the Residential segment sustaining the highest application-level growth through 2034.

Executive Summary

India’s air conditioning market is one of the fastest-growing HVAC markets globally, projected to grow from USD 6.15 billion in 2025 to USD 21.59 billion by 2034 at a CAGR of 14.98%. Growth is driven by rapid urbanization, rising incomes, increasing heatwaves, expanding commercial real estate, and government support through the PLI scheme for white goods boosting domestic manufacturing.

Room Air Conditioners account for 48.05% market share in 2025, driven by rising urban housing and electrification. Ductless ACs hold 22.4%, gaining traction in commercial and hospitality segments. Residential leads with 44.05%, while Commercial and Retail contribute 24.3%, supported by strong construction activity in Tier-1 and Tier-2 cities.

North India leads with a 29% share in 2025, driven by extreme heat and strong demand across Delhi-NCR, Uttar Pradesh, and Punjab. West India holds 26.4%, supported by Mumbai and Pune’s commercial hubs, while South India, at 24.8%, is the fastest growing due to IT expansion in Bengaluru, Hyderabad, and Chennai. Key players include Daikin Industries, Voltas Limited, Blue Star Limited, LG Electronics, and Carrier Global Corporation.

Key Market Insights

|

Insight |

Data |

|

Largest Type Segment |

Room Air Conditioner – 48.05% share (2025) |

|

Second Type Segment |

Ductless Air Conditioner – 22.4% share (2025) |

|

Leading Application Segment |

Residential – 44.05% share (2025) |

|

Leading Region |

North India – 29% revenue share (2025) |

|

Fastest Growing Region |

South India (IT corridor expansion) |

|

Top Companies |

Daikin Air Conditioning India Pvt. Ltd., Voltas Limited, Blue Star Limited, Carrier Airconditioning & Refrigeration Ltd., LG Electronics India Pvt. Ltd., Bosch Home Comfort India Limited, Panasonic Life Solutions India Pvt. Ltd., Samsung India Electronics Pvt. Ltd., Godrej & Boyce Mfg. Co. Ltd., and Fujitsu General (India) Private Limited |

|

Market Opportunity |

Smart/Inverter AC penetration in Tier-2 & Tier-3 cities |

Key Analytical Observations Supporting the Above Data:

- Room Air Conditioners' 48.05% dominance in 2025 reflects mass-market penetration across urban and semi-urban housing, driven by declining inverter AC prices and aggressive retail distribution by leading brands.

- Ductless Air Conditioners at 22.4% in 2025 are gaining commercial momentum as office developers and hospitality operators prefer zoned cooling solutions offering energy flexibility and zone-level temperature control.

- Residential application's 44.05% share validates India's structural housing demand – under PM Awas Yojana, over 11.8 million homes were built by 2024, each representing a potential AC installation opportunity.

- North India's 29% share reflects the region's long summer season, averaging 40–48°C peak temperatures across Rajasthan, UP, and Delhi-NCR – among the highest heat stress zones globally.

- South India is the fastest-growing region, driven by tech hub expansion in Bengaluru and Hyderabad, growing commercial real estate, and increasing residential AC adoption in Tamil Nadu and Andhra Pradesh.

- Daikin and Voltas are leading players in India’s room AC market, each holding an estimated 35–40% share, supported by strong inverter AC offerings and extensive nationwide distribution.

India Air Conditioning Market Overview

India’s AC market includes split, window, ducted, VRF/VRV, and centralized HVAC systems across residential and commercial applications such as retail, offices, healthcare, and data centres. The ecosystem spans component suppliers, OEMs, service providers, and regulators like the Bureau of Energy Efficiency, with growth driven by 6.5–7% GDP expansion, rising heatwaves, and increasing construction activity.

Market Dynamics

To evaluate market opportunities, Request Sample

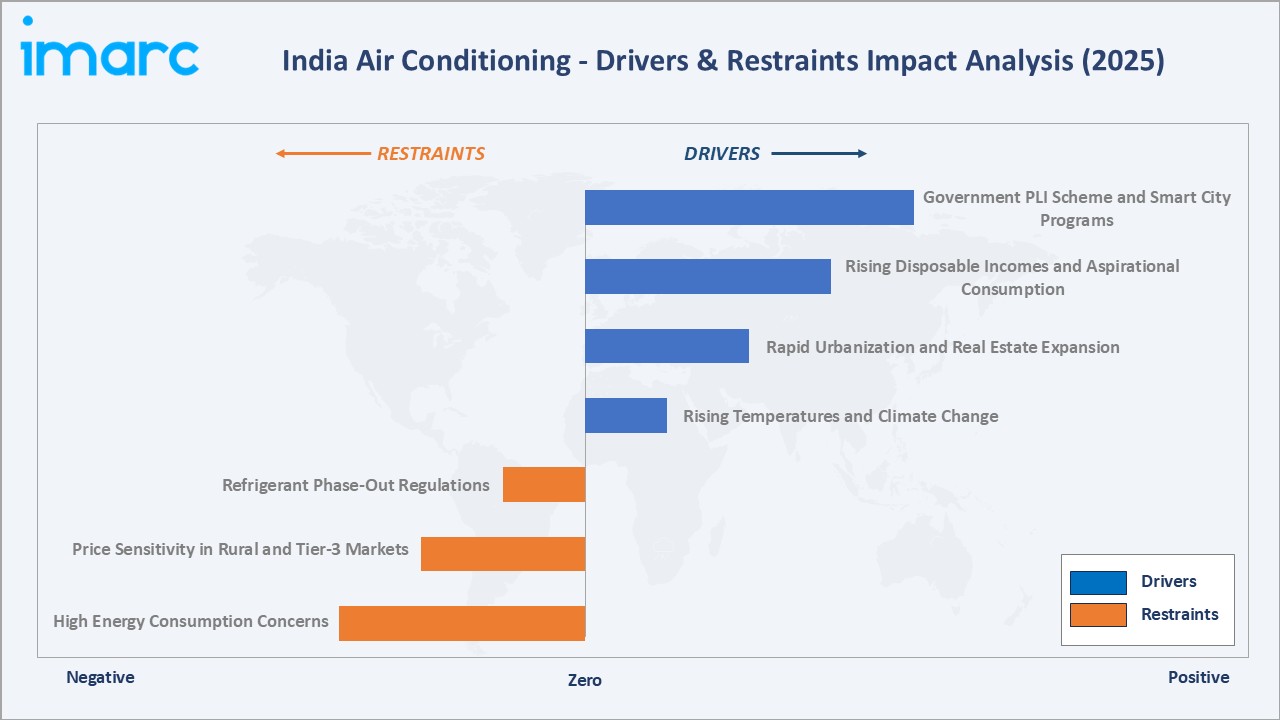

Market Drivers

- Rising Temperatures and Climate Change: India has experienced more frequent and intense heatwaves in recent years, with 2024 among the warmest years recorded, increasing cooling demand across residential and commercial segments.

- Rapid Urbanization and Real Estate Expansion: India’s urban population is projected to reach ~600 million by 2031, while strong growth in commercial and residential construction continues to drive demand for air conditioning systems.

- Rising Disposable Incomes and Aspirational Consumption: India’s per capita income has been steadily increasing, and low AC penetration levels compared to developed markets indicate significant growth potential.

- Government PLI Scheme and Smart City Programs: The government’s PLI scheme for white goods and the Smart Cities Mission are supporting domestic manufacturing and boosting HVAC demand through infrastructure development.

Market Restraints

- High Energy Consumption Concerns: Air conditioners are a major contributor to peak electricity demand in Indian cities, and rising power costs along with grid stress concerns make consumers sensitive to operating expenses.

- Price Sensitivity in Rural and Tier-3 Markets: Entry-level split ACs range from INR 28,000 to INR 45,000, remaining unaffordable for a significant share of semi-urban and rural households. This limits market depth beyond Tier-1 and Tier-2 urban centres.

- Refrigerant Phase-Out Regulations: India, under the Kigali Amendment, is phasing down HFC refrigerants, requiring a transition to low-GWP alternatives and increasing compliance and technology costs for manufacturers.

Market Opportunities

- Smart and Inverter AC Adoption: Inverter ACs now dominate split AC sales in India, supported by rising demand for energy efficiency, higher star ratings, and smart/AI-enabled features, which are driving premiumization.

- Data Center and IT Infrastructure Cooling: India’s data centre capacity is expanding rapidly, with total capacity expected to more than double in the coming years, creating strong demand for precision cooling and advanced HVAC systems.

- Tier-2 and Tier-3 City Expansion: Growing urbanization and rising incomes in Tier-2 and Tier-3 cities are driving first-time AC adoption, with penetration levels still significantly lower than metro cities, indicating strong future growth potential.

Market Challenges

- Seasonal Demand Concentration: AC sales in India are highly seasonal, with a significant share occurring during peak summer months, leading to inventory pressure, supply chain constraints, and pricing volatility.

- Skilled Installation and Service Workforce Shortage: India faces a shortage of trained HVAC technicians, impacting installation quality and after-sales service, particularly in smaller cities and rural areas.

- Competition from Chinese Imports and Low-Cost Brands: Dependence on imported components, particularly from China, and the presence of low-cost brands continue to create pricing pressure and margin challenges for domestic manufacturers.

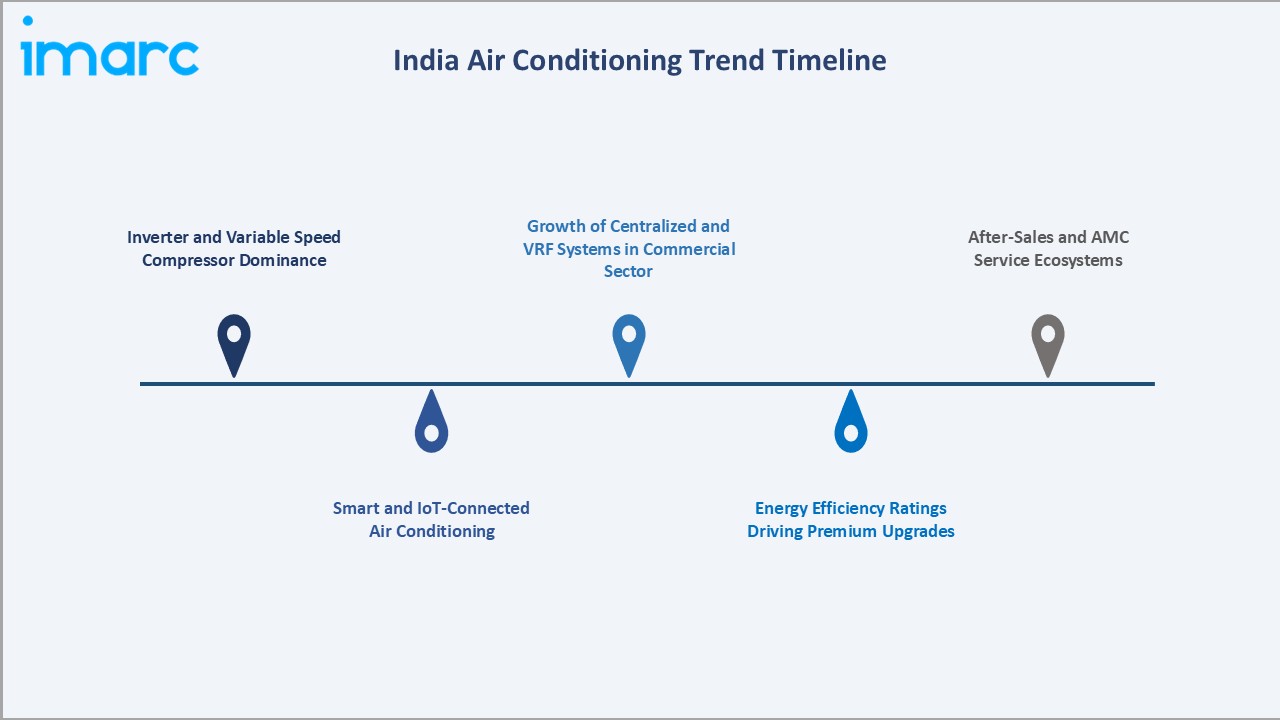

Emerging Market Trends

1. Inverter and Variable Speed Compressor Dominance

Inverter ACs have become the dominant segment in India, with major brands such as Daikin, LG Electronics, and Voltas reporting that inverter models account for most of their sales. These systems offer significantly higher energy efficiency than fixed-speed units, driving replacement demand.

2. Smart and IoT-Connected Air Conditioning

Smart ACs with Wi-Fi, app control, and voice assistant integration (e.g., Amazon Alexa, Google Assistant) are witnessing strong growth, especially in premium segments. Rising smartphone penetration and smart home adoption are supporting this trend in India.

3. Energy Efficiency Ratings Driving Premium Upgrades

The updated energy efficiency norms by Bureau of Energy Efficiency are pushing demand for higher star-rated ACs. Consumers are increasingly opting for energy-efficient models, encouraging manufacturers to expand premium offerings.

4. Growth of Centralized and VRF Systems in Commercial Sector

Variable Refrigerant Flow (VRF) and centralized HVAC systems are gaining traction in commercial buildings such as offices, malls, and hotels due to energy efficiency and flexible cooling control. This is driving growth in the commercial AC segment.

5. After-Sales and AMC Service Ecosystems

After-sales services, including Annual Maintenance Contracts (AMC) and extended warranties, are becoming increasingly important for AC brands. Companies like Blue Star Limited, Daikin, and Carrier are strengthening service networks to enhance customer retention and recurring revenue.

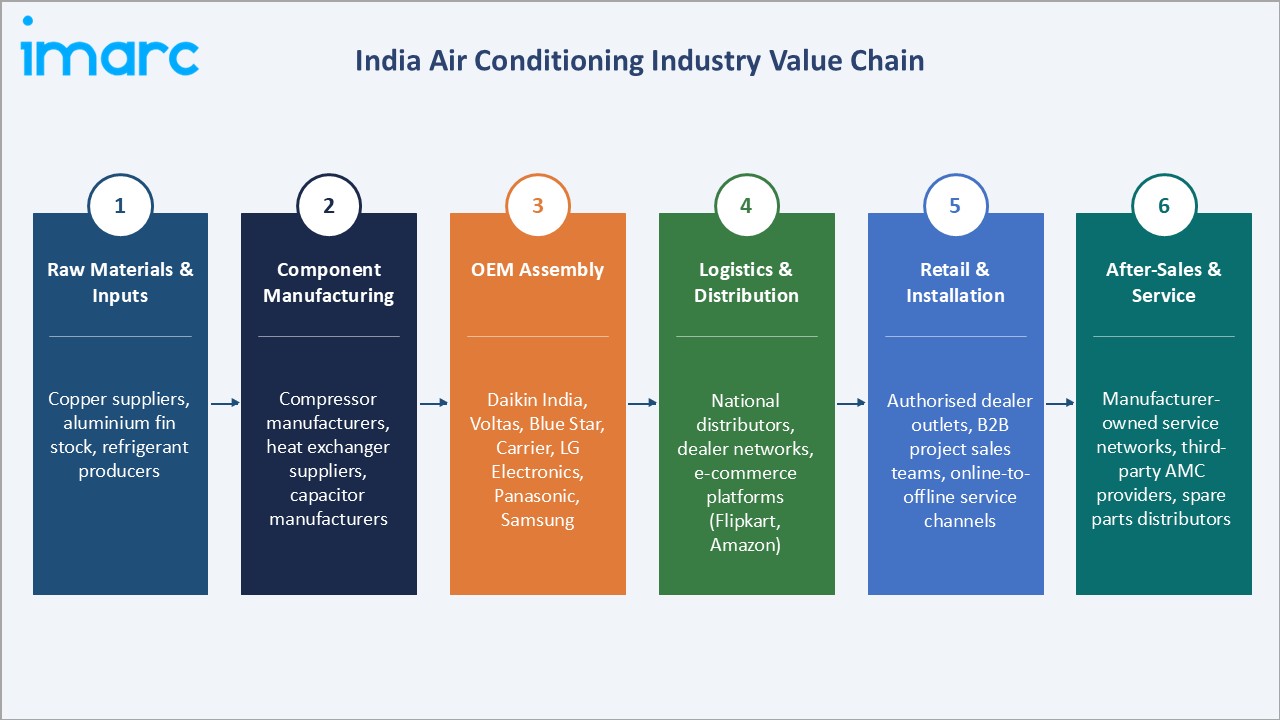

Industry Value Chain Analysis

The India air conditioning value chain spans six stages from raw material procurement to end-consumer service, with distinct competitive dynamics and margin structures at each level.

|

Stage |

Key Players / Examples |

|

Raw Materials & Inputs |

Copper suppliers, aluminium fin stock, refrigerant producers |

|

Component Manufacturing |

Compressor manufacturers, heat exchanger suppliers, capacitor manufacturers |

|

OEM Assembly |

Daikin India, Voltas, Blue Star, Carrier, LG Electronics, Hitachi, Panasonic, Samsung |

|

Logistics & Distribution |

National distributors, state dealer networks, e-commerce platforms (Flipkart, Amazon), modern retail |

|

Retail & Installation |

Authorised dealer outlets, B2B project sales teams, online-to-offline service channels |

|

After-Sales & Service |

Manufacturer-owned service networks, third-party AMC providers, spare parts distributors |

Established OEMs hold the strongest value position through brand equity, distribution control, and proprietary inverter compressor technology. Domestic manufacturers benefiting from PLI incentives are emerging as cost-competitive challengers to imported brands.

Technology Landscape in the India Air Conditioning Industry

Inverter Compressor Technology

Inverter-driven variable-speed compressors are now the industry standard for energy-efficient ACs in India. Companies like LG Electronics and Daikin offer advanced inverter technologies that significantly improve efficiency compared to fixed-speed systems and help comply with updated norms by the Bureau of Energy Efficiency.

Smart Connectivity and AI Integration

IoT-enabled ACs with app control, voice assistants, and AI-based features such as auto-cleaning and adaptive cooling are expanding in the premium segment. Brands like Samsung Electronics and Daikin are integrating airflow optimization and smart climate control technologies to enhance user comfort and efficiency.

Low-GWP Refrigerant Transition

India is transitioning toward lower global warming potential (GWP) refrigerants such as R-32 and R-290, replacing high-GWP options like R-22. This shift aligns with commitments under the Kigali Amendment and national cooling policies promoting sustainable cooling technologies.

Solar-Hybrid and Energy Storage AC Systems

Solar-compatible and DC inverter AC systems are emerging in niche applications such as rural, telecom, and off-grid use cases. Supported by India’s renewable energy push, companies like Voltas and Blue Star Limited are exploring energy-efficient and hybrid cooling solutions.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Room Air Conditioners |

48.05% |

2025 |

|

Applications |

Residential |

44.05% |

2025 |

|

Region |

North India |

29.0% |

2025 |

By Type

To access detailed market analysis, Request Sample

Room Air Conditioners hold a 48.05% share in 2025, supported by rising urban household penetration, increasing affordability of inverter ACs, and strong marketing by brands such as Daikin, Voltas, LG Electronics, and Samsung Electronics. Split Acs particularly the 1.5-ton category dominate demand, with replacement of older window AC units contributing to growth.

Ductless Air Conditioners at 22.4% in 2025 are the second-largest category, driven by adoption in offices, hotels, and multi-room homes due to flexible, duct-free installation. Ducted AC systems represent 17.8%, mainly used in commercial and premium residential projects, while Centralized AC holds an 11.75% share, serving large facilities such as malls, campuses, and institutional buildings.

By Application

Residential applications account for 44.05% of the India AC market in 2025, driven by rising household incomes, improving affordability of inverter ACs, and growth in housing under government initiatives. AC penetration in India remains relatively low but is steadily increasing, particularly in urban areas.

Commercial and Retail applications account for 24.3%, driven by expansion of organized retail, office spaces, and IT parks across India. Hospitality at 14.7% is supported by strong hotel development and rising tourism demand, while Healthcare at 11.6% is growing due to increasing need for controlled environments in hospitals and diagnostic centres. Others account for 5.35%, backed by digital infrastructure and institutional growth.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

North India |

29.0% |

Extreme summer heat (40–48°C), dense urban populations in Delhi-NCR, UP, Punjab; strong retail and residential demand |

|

West India |

26.4% |

Mumbai and Pune commercial expansion, Gujarat industrial corridors, high-humidity coastal demand, robust retail growth |

|

South India |

24.8% |

Fastest-growing; IT corridor expansion in Bengaluru, Hyderabad, Chennai; data center cooling, residential AC adoption |

|

East India |

19.8% |

Emerging demand from Kolkata, Odisha, Jharkhand; rising incomes, improving electricity infrastructure, healthcare sector growth |

North India commands a 29% share in 2025, driven by extreme summer temperatures across states such as Rajasthan, Uttar Pradesh, Haryana, and Delhi-NCR. The region represents a major share of seasonal AC demand, with peak sales concentrated during the summer months.

West India at 26.4% benefits from Mumbai's commercial construction activity and Gujarat's industrial growth under the DMIC corridor. South India, contributing 24.8%, is the fastest-growing region with Bengaluru and Hyderabad's IT campuses driving large commercial HVAC procurement. East India at 19.8% remains underpenetrated, representing the highest long-term growth potential as electrification and urbanization accelerate across West Bengal, Odisha, and Bihar through 2034.

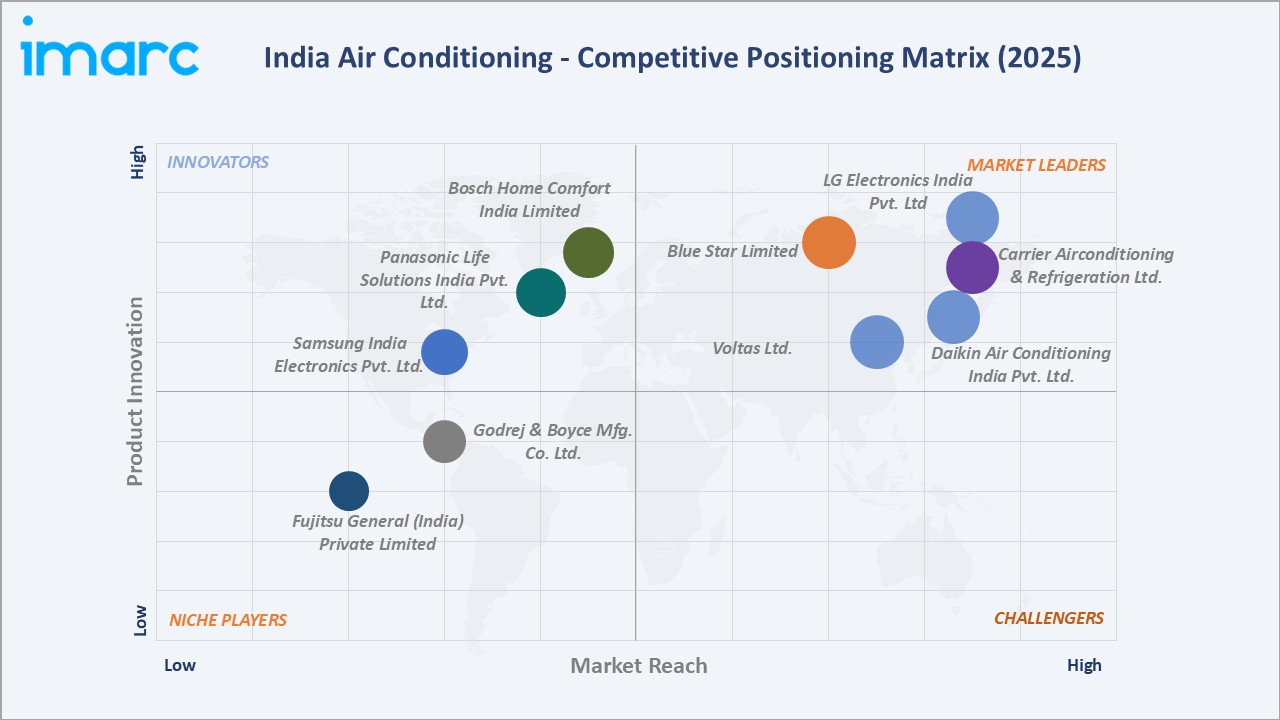

Competitive Landscape

|

Company Name |

Key Brand |

Market Position |

Core Strength |

|

Daikin Air Conditioning India Pvt. Ltd. |

Daikin |

Leader |

Inverter technology, Streamer air purification, premium segment dominance |

|

Voltas Limited |

Voltas |

Leader |

India's #1 AC brand by volume; deep retail distribution; strong Tier-2 presence |

|

Blue Star Limited |

Blue Star |

Leader |

Commercial HVAC leadership; expanding residential; premium inverter portfolio |

|

Carrier Airconditioning & Refrigeration Ltd. |

Carrier |

Leader |

Global engineering expertise; strong commercial and chillers; B2B projects |

|

LG Electronics India Pvt. Ltd. |

LG |

Leader |

Dual Inverter compressor technology; broad product range; electronics brand synergy |

|

Bosch Home Comfort India Limited |

Hitachi |

Challenger |

AI-powered smart AC; Kashikoi 5100X IoT platform; premium Japanese brand equity |

|

Panasonic Life Solutions India Pvt. Ltd. |

Panasonic |

Challenger |

Nanoe-X air purification; energy efficiency; expanding retail presence |

|

Samsung India Electronics Pvt. Ltd. |

Samsung |

Challenger |

WindFree technology; smartphone ecosystem integration; strong brand pull |

|

Godrej & Boyce Mfg. Co. Ltd. |

Godrej |

Emerging |

Strong domestic brand; expanding inverter range; value-for-money positioning |

|

Fujitsu General (India) Private Limited |

O General |

Emerging |

Niche premium segment; strong South India commercial base; energy efficiency |

The India air conditioning market is led by Voltas Limited and Daikin Industries Ltd. in terms of market presence and influence. Voltas remains a leading player in the split AC segment by sales volume, while Daikin holds a strong position in the premium inverter category, supported by its advanced technology, strong brand reputation, and extensive service network across India.

Key Company Profiles

Daikin Air Conditioning India Pvt. Ltd.

Daikin India, a subsidiary of Japan-based Daikin Industries Ltd., operates manufacturing and R&D facilities in Neemrana and Hyderabad, focusing on energy-efficient HVAC solutions while expanding localization and innovation to strengthen its leadership in India’s residential and commercial AC markets.

- Product Portfolio: Daikin India offers split and inverter ACs, cassette, ducted and VRV systems, chillers, air purifiers, refrigeration solutions, and after-sales services including maintenance and AMC support.

- Recent Developments: In 2026, Daikin Industries has announced a ₹1,000 crore investment to establish its first global R&D centre outside Japan in India, focusing on advanced HVAC solutions including chillers and air-conditioning systems for residential, commercial, and data centre applications worldwide.

- Strategic Focus: Daikin focuses on India as a global manufacturing and innovation hub, emphasizing energy-efficient technologies, localization, and R&D-led product development for both domestic and export markets.

Voltas Ltd.

Voltas Ltd., a Tata Group company headquartered in Mumbai, is India’s leading air conditioning brand by volume, supported by a strong distribution network and growing demand, achieving over 2 million AC unit sales and ₹12,400 crore revenue in FY2024.

- Product Portfolio: Voltas offers room air conditioners (split and window), air coolers, commercial refrigeration, HVAC solutions, and home appliances through its Voltas Beko joint venture, along with engineering and project services.

- Recent Developments: In 2026, Voltas, holding around 18% share in India’s AC market, is focusing on first-time buyers—who account for nearly 85% of demand—to drive double-digit growth and expand its market position amid rising competition. In 2024, Voltas achieved a landmark milestone by selling over 2 million air conditioners in FY2024, becoming the first company in India to reach this level, driven by strong demand, distribution strength, and product innovation.

- Strategic Focus: Voltas focuses on expanding market leadership through deeper distribution, first-time buyer penetration, premium inverter AC portfolio growth, and leveraging the Tata ecosystem to strengthen manufacturing and innovation capabilities.

Blue Star Ltd.

Blue Star Ltd., headquartered in Mumbai, is a leading Indian air conditioning and commercial refrigeration company with over 75 years of expertise, reporting FY2024 revenues of ₹11,229 crore and expanding its presence in both residential and commercial cooling segments.

- Product Portfolio: Blue Star offers room ACs, inverter split ACs, VRF/VRV systems, chillers, ducted and packaged ACs, commercial refrigeration, cold chain solutions, and provides engineering, procurement, and after-sales services.

- Recent Developments: In 2026, Blue Star announced a ₹200 crore capex plan to expand manufacturing, R&D, and marketing, while signalling AC price hikes due to rising commodity costs and new energy-efficiency norms, which could increase prices by up to 13–15%. In 2025, Blue Star projected up to 20% growth in room AC sales, driven by expected GST reductions, with its unitary cooling segment contributing nearly half of revenue and the company holding around 14% market share in India.

- Strategic Focus: Blue Star focuses on strengthening its leadership in commercial HVAC, expanding residential AC market share, investing in manufacturing and R&D, and capitalizing on demand growth in Tier-2/3 cities and infrastructure sectors.

Market Concentration Analysis

The India air conditioning market is moderately concentrated at the top, with the five leading brands – Voltas, Daikin, LG, Blue Star, and Samsung – collectively accounting for approximately 55–60% of total unitary AC sales by volume in FY2024. Daikin and Voltas alone hold a combined 35–40% share, reflecting their leadership in the high-volume split AC category.

Lower-tier segments remain highly fragmented, with numerous domestic and global brands competing across price categories, alongside emerging entrants and unorganized players, leading to intense competition and limited brand consolidation in the entry-level AC market.

Consolidation activity is accelerating through strategic acquisitions, joint ventures, and PLI-driven capacity investments that favour scale players. Technology investment requirements – particularly in inverter compressor development, IoT connectivity, and refrigerant transition R&D are creating competitive barriers that are progressively squeezing sub-scale operators out of profitable premium segments.

Investment & Growth Opportunities

Fastest-Growing Segments

Smart and AI-integrated inverter ACs represent a key premium growth opportunity in India, driven by increasing smartphone usage, expanding smart home ecosystems, and rising awareness of energy efficiency and electricity cost savings among urban consumers.

Data center cooling is a rapidly expanding B2B segment, supported by large-scale investments from companies like Microsoft, Amazon Web Services, and Google in India’s data center infrastructure.

Emerging Market Expansion

Tier-2 and Tier-3 cities such as Lucknow, Jaipur, Coimbatore, Surat, and Nagpur are key growth markets, driven by low AC penetration and rising disposable incomes. Industry reports highlight that AC penetration in India remains in single digits overall, with significantly lower adoption in smaller cities, creating strong long-term demand potential.

Venture & Strategic Investment Trends

Government initiatives like the Production Linked Incentive (PLI) scheme are driving investments in domestic AC component manufacturing, including compressors. Companies such as Voltas Limited and Daikin Air Conditioning India Pvt. Ltd. are expanding local manufacturing capacity. Additionally, increasing investment interest in IoT-enabled HVAC solutions reflects growing demand for smart monitoring and predictive maintenance in commercial buildings.

Future Market Outlook (2026-2034)

The India air conditioning market is projected to grow from USD 6.15 Billion in 2025 to USD 21.59 Billion by 2034, representing value creation of over USD 15 Billion, driven by urbanization, rising temperatures, increasing incomes, and expansion in commercial real estate.

Three transformational forces will reshape the competitive landscape through 2034. First, the AI-powered smart AC will transition from a premium add-on to a mainstream expectation, with auto-learning temperature management and predictive service becoming table-stakes features. Second, the mandatory shift to ultra-low-GWP natural refrigerants (R-290, CO2) will require fundamental product redesigns, rewarding early movers. Third, solar-hybrid and energy-storage-integrated AC systems will gain material share as India's distributed renewable energy infrastructure expands.

By 2034, India is projected to become one of the largest air conditioner markets globally over the long term, driven by rising incomes, urbanization, and increasing cooling demand. Industry sources such as the International Energy Agency highlight strong growth in AC ownership, though exact future stock estimates vary. Companies with strong distribution, energy-efficient products, and service networks are well positioned to benefit.

Research Methodology

Primary Research

Primary research was conducted in 2024–2025 through structured interviews with 120+ stakeholders including procurement heads at leading real estate developers, operations managers at AC manufacturers, senior dealers in key cities, HVAC contractors, and institutional buyers in healthcare and hospitality. Surveys covering brand preference, energy sensitivity, and smart feature adoption were completed across 8 Indian cities.

Secondary Research

Secondary sources include company annual reports (Voltas, Blue Star, Daikin India, LG Electronics India), BEE AC sales registration data, Bureau of Indian Standards (BIS) market reports, Ministry of Commerce trade data, MoSPI GDP and income statistics, FIEO AC export data, and industry publications including Business Standard and the Air Conditioning and Refrigeration Industry trade media.

Forecasting Models

Market size estimations and forecasts were derived using a combination of bottom-up (brand-level sales aggregation, dealer interview triangulation) and top-down (household penetration modeling, real estate construction forecasts, per-capita income elasticity analysis) methodologies, cross-validated against GDP growth trajectories, climate projection data, and historical market CAGR under base, optimistic, and conservative scenarios.

India Air Conditioning Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Room Air Conditioner, Ducted Air Conditioner, Ductless Air Conditioner, Centralized Air Conditioner |

| Applications Covered | Residential, Healthcare, Commercial and Retail, Hospitality, Others |

| Regions Covered | North India, South India, East India, West India |

| Companies Covered | Daikin Air Conditioning India Pvt. Ltd., Voltas Limited, Blue Star Limited, Carrier Airconditioning & Refrigeration Ltd., LG Electronics India Pvt. Ltd., Bosch Home Comfort India Limited, Panasonic Life Solutions India Pvt. Ltd., Samsung India Electronics Pvt. Ltd., Godrej & Boyce Mfg. Co. Ltd., Fujitsu General (India) Private Limited, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Air Conditioning Market Report

The India air conditioning market was valued at USD 6.15 Billion in 2025, driven by extreme heat events, urbanization, rising incomes, and expanding residential and commercial construction activity.

The market is projected to reach USD 21.59 Billion by 2034, growing at a 14.98% CAGR during 2026-2034, supported by smart AC adoption, Tier-2 city penetration, and data center cooling demand.

Room Air Conditioners lead with a 48.05% share in 2025, driven by urban housing growth, declining inverter AC prices, and aggressive retail distribution by leading domestic and international brands.

Residential applications command a 44.05% share in 2025, driven by household income growth, government housing schemes, and increasing heat wave frequency accelerating household AC adoption.

North India leads with a 29% share in 2025, anchored by extreme summer heat across Delhi-NCR, UP, and Rajasthan, along with the region's high density of urban residential and commercial activity.

Key drivers include rising temperatures, rapid urbanization, rising disposable incomes, the PLI scheme for white goods manufacturing, commercial real estate expansion, and smart AC technology adoption.

South India is the fastest-growing region, driven by rapid IT corridor expansion in Bengaluru, Hyderabad, and Chennai, alongside growing residential AC penetration in Tamil Nadu and Andhra Pradesh.

Leading companies include Daikin Air Conditioning India Pvt. Ltd., Voltas Limited, Blue Star Limited, Carrier Airconditioning & Refrigeration Ltd., LG Electronics India Pvt. Ltd., Bosch Home Comfort India Limited, Panasonic Life Solutions India Pvt. Ltd., Samsung India Electronics Pvt. Ltd., Godrej & Boyce Mfg. Co. Ltd., and Fujitsu General (India) Private Limited.

The India air conditioning market was valued at approximately USD 3.06 Billion in 2020, reflecting suppressed demand due to COVID-19 disruptions and the associated economic slowdown in India.

The PLI scheme for white goods with a USD 840 million outlay is boosting domestic AC manufacturing, attracting USD 900+ million in committed investments, and supporting local compressor and component production.

Key technologies include AI-powered inverter compressors, IoT smart connectivity, R-32 and R-290 low-GWP refrigerant transition, solar-hybrid AC systems, and BEE 5-Star energy management platforms.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade