India Air Cooler Market Size, Share, Trends and Forecast by Organized/Unorganized, End Use, Tank Capacity, Distribution Channel, and Region, 2026-2034

India Air Cooler Market Size, Share, Trends & Forecast (2026-2034)

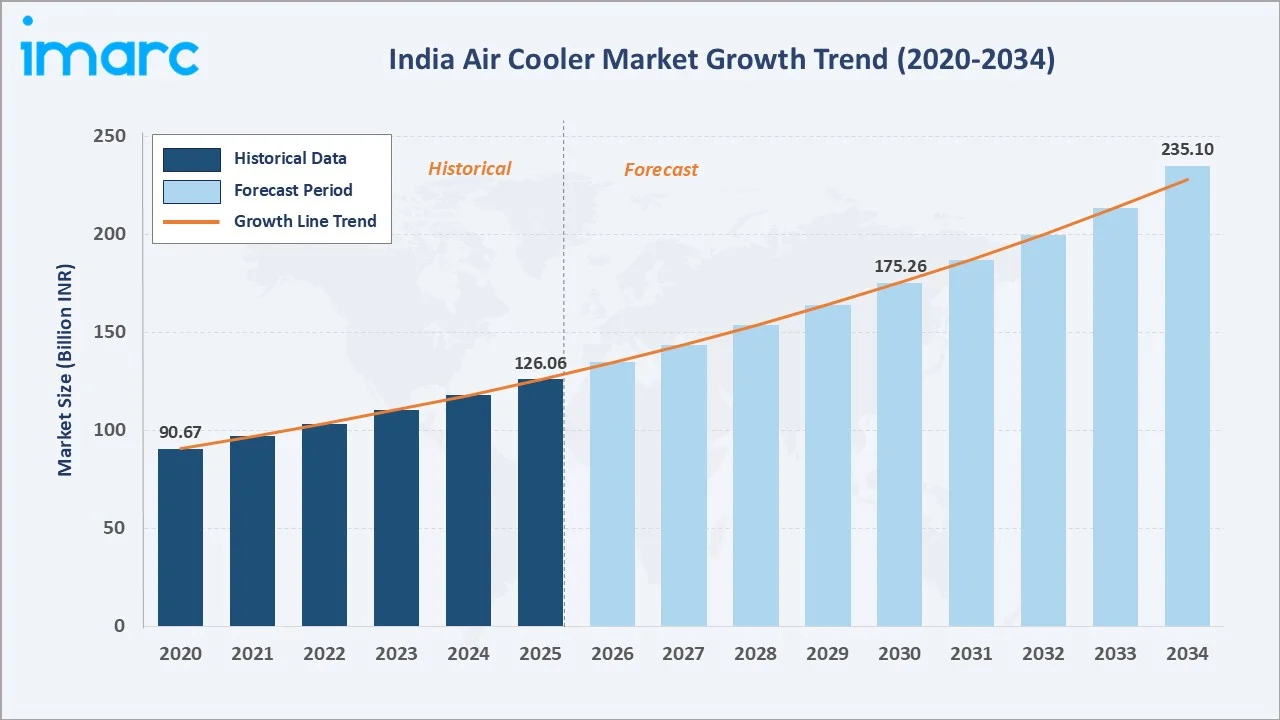

The India air cooler market size reached INR 126.06 Billion in 2025 and is projected to reach INR 235.10 Billion by 2034, exhibiting a CAGR of 6.81% during 2026-2034. Rising temperatures, rapid urbanization, expanding e-commerce channels, and energy-efficient cooling preferences are primary growth drivers.

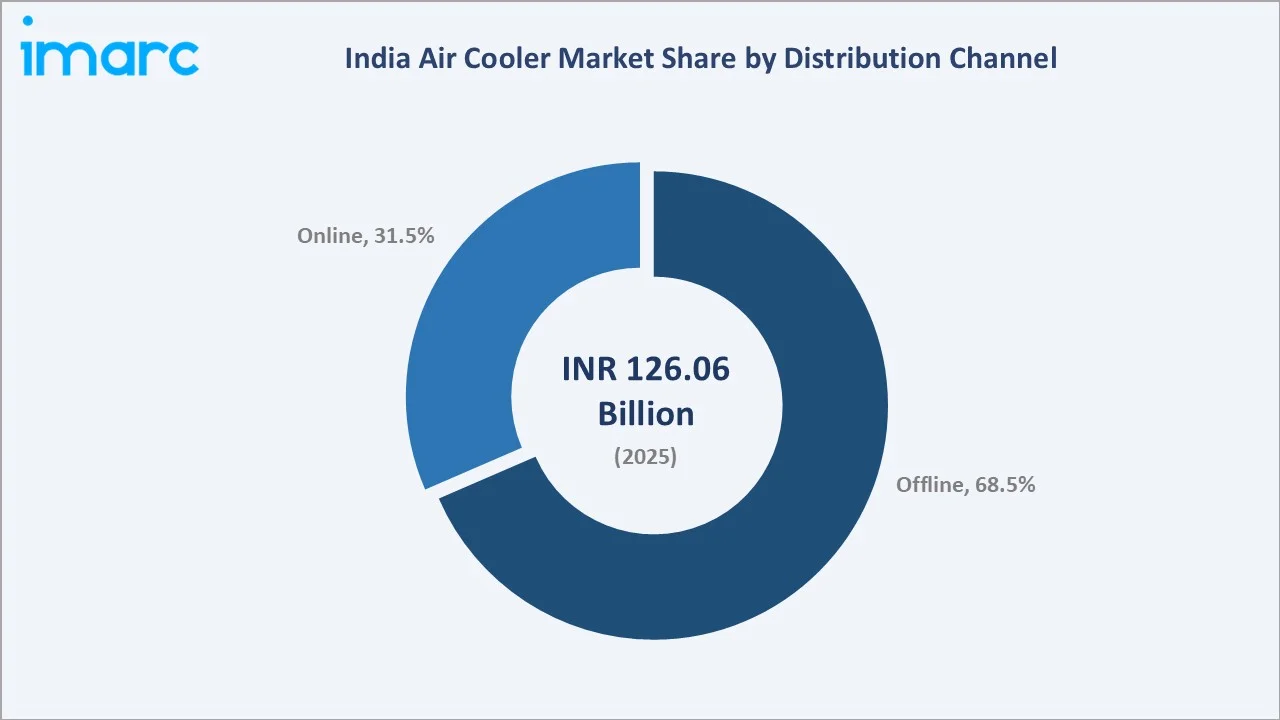

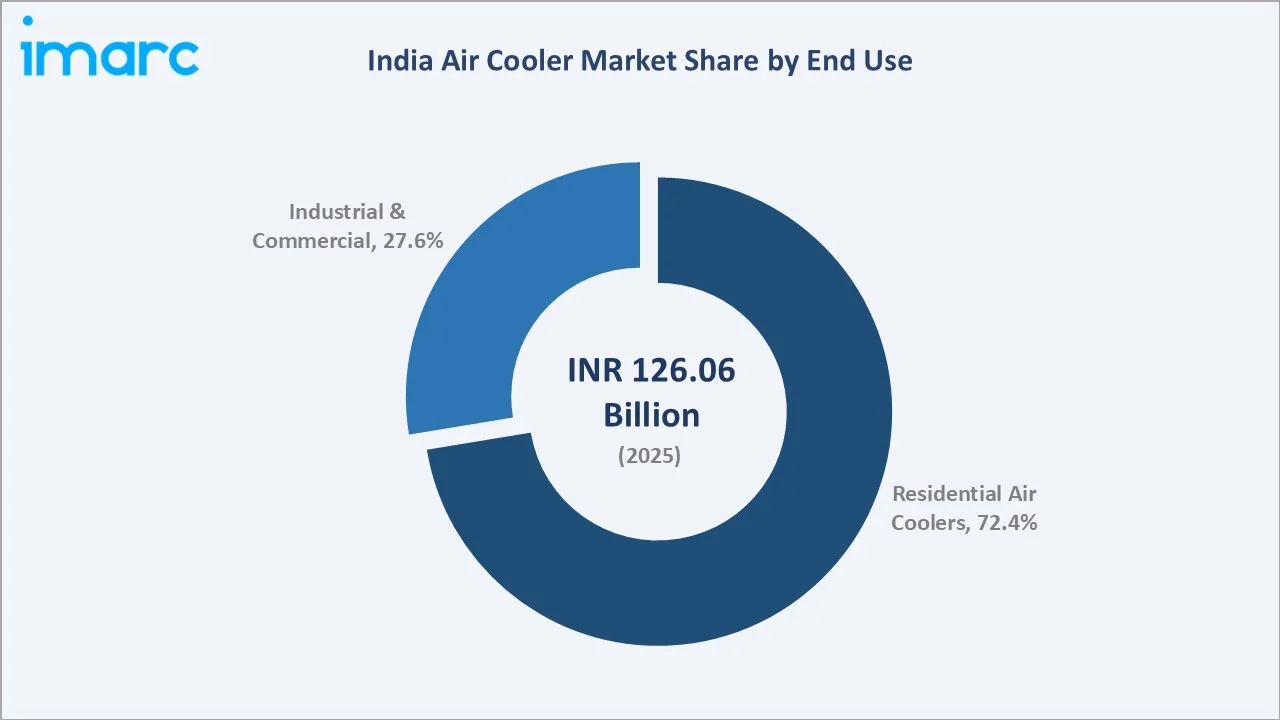

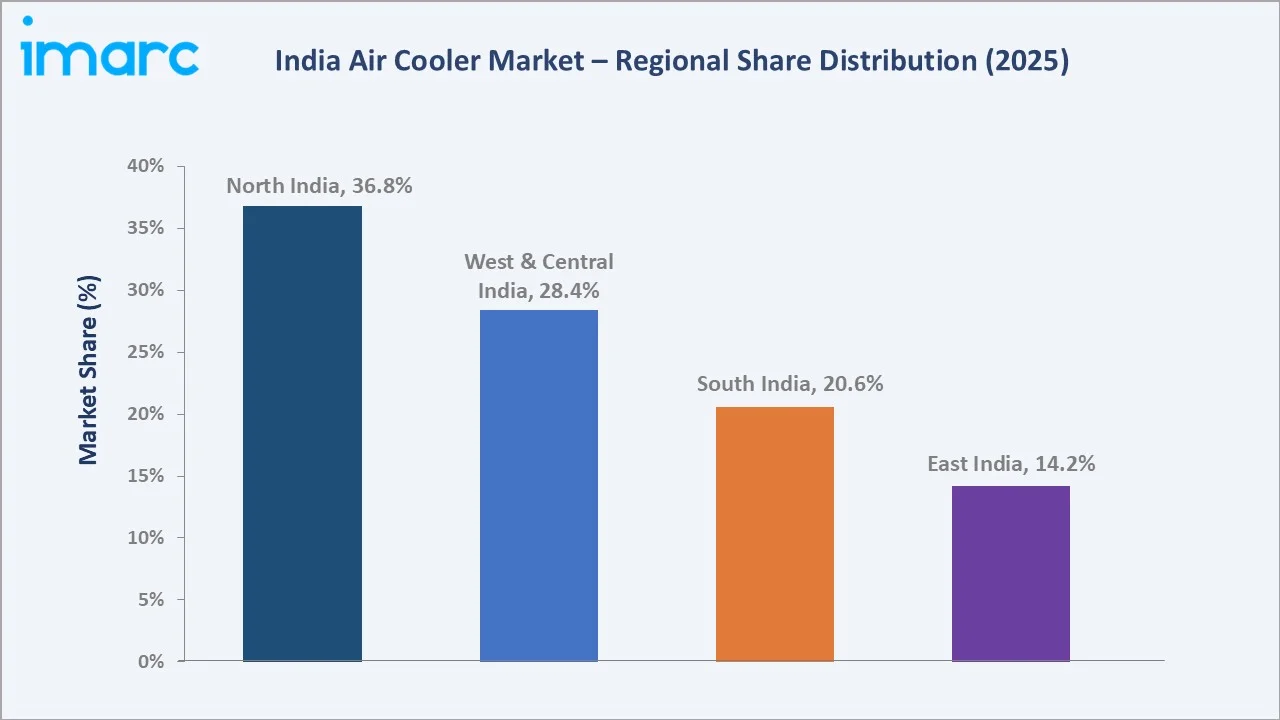

Offline distribution commands 68.5% share in 2025, residential end use leads at 72.4%, and North India dominates regional demand at 36.8%.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

INR 126.06 Billion |

|

Forecast Market Size (2034) |

INR 235.10 Billion |

|

CAGR (2026-2034) |

6.81% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Leading Distribution Channel |

Offline (68.5% share, 2025) |

|

Leading End Use Segment |

Residential Air Coolers (72.4% share, 2025) |

|

Dominant Region |

North India (36.8% share, 2025) |

The growth trajectory from 2020 through 2034, with historical expansion to INR 126.06 Billion in 2025, reflects consistent climate-driven demand. The forecast to INR 235.10 Billion captures accelerating rural penetration, smart product adoption, and India's fast-growing e-commerce ecosystem enabling broader consumer access.

To get more information on this market, Request Sample

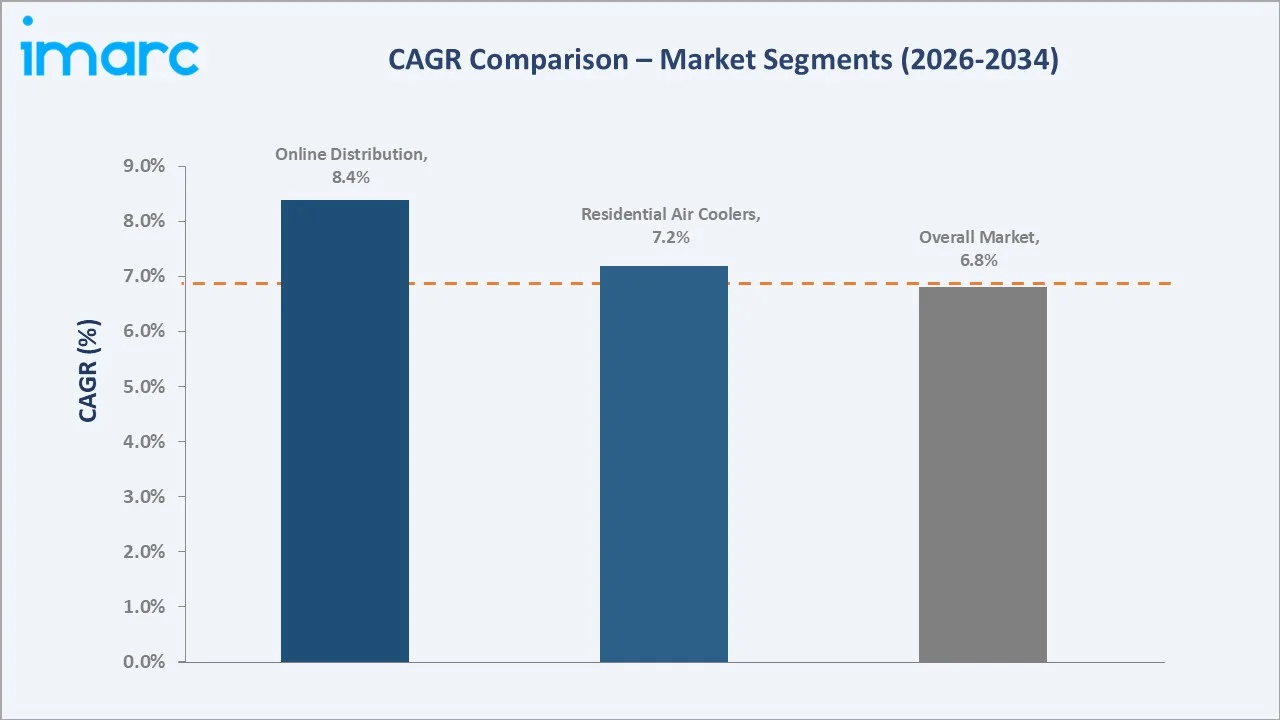

CAGR trajectories across key segments indicate online distribution at approximately 8.4% CAGR and residential air coolers at approximately 7.2% CAGR as the fastest-growing categories within the India air cooler industry analysis through 2034.

Executive Summary

The India air cooler market is on a sustained growth trajectory from INR 126.06 Billion in 2025 to INR 235.10 Billion by 2034. Air coolers serve as an affordable, energy-efficient alternative to air conditioners, benefiting from the non-discretionary cooling needs of India's large heat-exposed population across residential and industrial segments.

Offline distribution dominates at 68.5% in 2025 through the extensive dealer and retail network across tier II and III cities. Online channels are the fastest-growing distribution route, driven by e-commerce platform expansion, competitive pricing, and improved digital access in rural and semi-urban India.

Residential air coolers lead end-use at 72.4% in 2025, driven by cost-conscious households seeking energy-efficient cooling. Industrial and commercial segments at 27.6% are growing with adoption in warehouses, factories, and commercial spaces as a cost-effective alternative to centralized air conditioning systems.

North India commands 36.8% regional share in 2025, reflecting the dry and semi-arid climate of the northern states. West and Central India follows at 28.4%, South India at 20.6%, and East India at 14.2%, with the latter emerging as the fastest-growing region.

Key Market Insights

|

Insight |

Data |

|

Leading Distribution Channel |

Offline – 68.5% share (2025) |

|

Fastest-Growing Channel |

Online – ~8.4% CAGR (2026-2034) |

|

Leading End Use Segment |

Residential Air Coolers – 72.4% share (2025) |

|

Second End Use Segment |

Industrial & Commercial – 27.6% share (2025) |

|

Dominant Region |

North India – 36.8% share (2025) |

|

Top Companies |

Symphony, Havells India Ltd., Crompton Greaves Consumer Electricals Limited, Usha International Ltd., NOVAMAX INDUSTRIES LLP, Blue Star Limited |

Key Analytical Observations Expanding on the Above Data:

- Offline distribution, with 68.5% in 2025, dominates because of the extensive dealer network in tier II and III cities and semi-urban areas, strong after-sales service networks, and consumer preference for physical product demonstration before purchase in non-metro markets.

- Residential air coolers, with 72.4% in 2025, lead due to India's large lower- and middle-income consumer base requiring affordable cooling. Air coolers consume significantly less electricity than air conditioners, making them the default choice for budget-conscious households across North and Central India.

- North India's 36.8% dominance in 2025 reflects the region's hot, dry climate where evaporative cooling is highly effective. The northern states collectively represent the country's largest air cooler consumption base by population and climate suitability.

India Air Cooler Market Overview

An air cooler is an evaporative cooling device that cools air by passing it over water-saturated pads, leveraging the natural evaporation process. Air coolers are categorized as personal, desert, window, and tower types, varying in tank capacity and airflow volume suited for different room sizes and applications.

India's air cooler ecosystem integrates raw material suppliers, component manufacturers, organized and unorganized product assemblers, quality certification bodies, pan-India distribution networks, modern retail and e-commerce platforms, and diverse residential, commercial, and industrial end users across all geographies.

Market Dynamics

To evaluate market opportunities, Request Sample

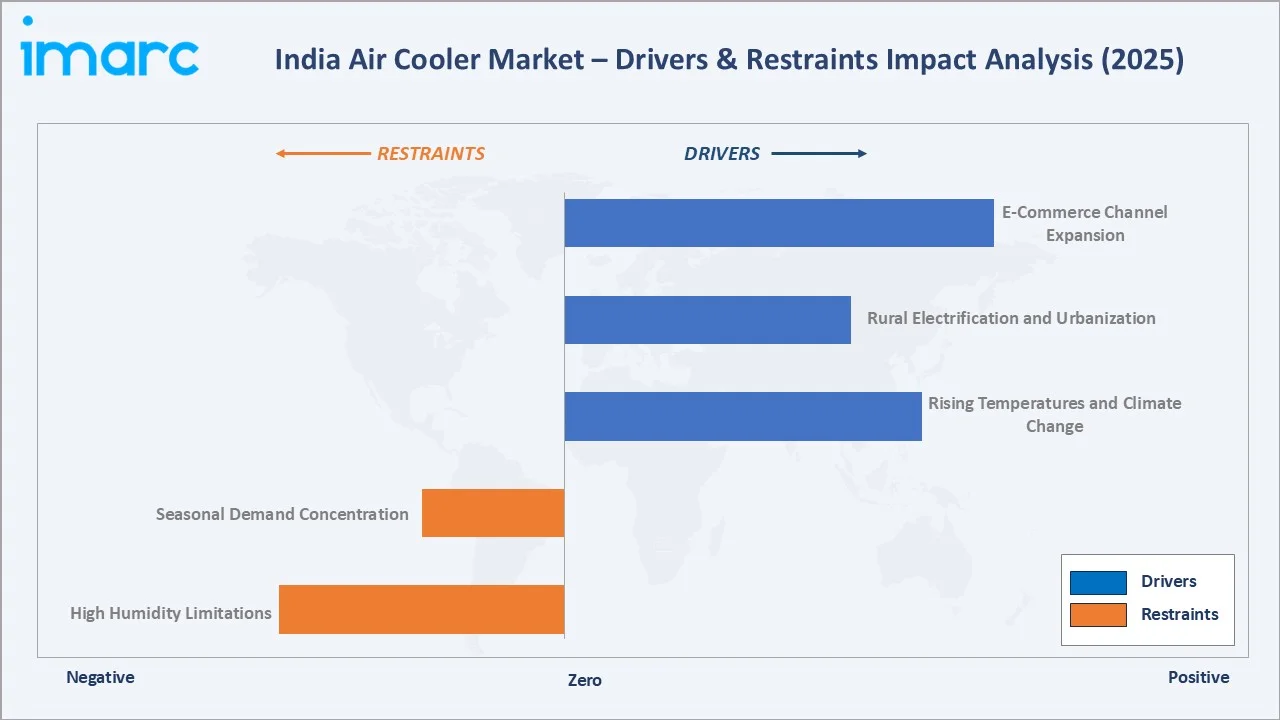

Market Drivers

- Rising Temperatures and Climate Change: India has recorded increasingly severe heat wave events across multiple states, significantly increasing residential and commercial cooling demand. The consistent rise in mean annual temperatures is making affordable cooling solutions a non-discretionary necessity rather than a discretionary purchase for millions of households.

- Rural Electrification and Urbanization: Government electrification programs have brought electricity to previously unserved villages, directly creating addressable demand for affordable cooling appliances. Air coolers are the primary beneficiary given their significant price and energy-cost advantage over air conditioners.

- E-Commerce Channel Expansion: India's rapidly expanding e-commerce market is extending product reach to semi-urban and rural consumers, offering a wider range of air cooler options at competitive prices. Platform-driven discounting during summer seasons is driving volume growth for mass-market brands.

Market Restraints

- High Humidity Limitations: Air coolers function effectively only in low-humidity dry conditions. In coastal states, evaporative cooling becomes ineffective, limiting market penetration in humid regions and constraining the overall India-wide addressable market size for conventional evaporative air coolers.

- Seasonal Demand Concentration: A significant majority of annual air cooler sales are concentrated during the summer season, creating cash-flow and inventory management challenges for manufacturers and distributors, and limiting year-round revenue visibility for organized branded players in the market.

Market Opportunities

- Smart and IoT-Enabled Air Coolers: Growing urban consumer demand for smart home-compatible appliances creates a premium product opportunity. Models with Wi-Fi connectivity, app control, voice assistant compatibility, and air purification integration can command meaningful price premiums over conventional mass-market cooler designs.

- Industrial and Commercial Segment Expansion: Large warehouses, automotive workshops, textile units, and commercial spaces are adopting industrial-capacity air coolers as cost-effective alternatives to centralized air conditioning, opening a high-volume growth avenue beyond the residential segment with higher average selling prices.

Market Challenges

- Intense Price Competition and Commoditization: The presence of numerous unorganized local manufacturers creates severe price pressure, compressing margins for branded players. Unorganized manufacturers dominate rural and semi-urban geographies with lower-cost products that undercut organized brand pricing.

- Water Consumption and Sustainability Concerns: Growing water scarcity in North and Central India raises concerns about air cooler water usage. Regulatory pressure and consumer awareness may limit adoption in water-stressed districts, potentially driving consumers toward inverter air conditioners as an alternative.

Emerging Market Trends

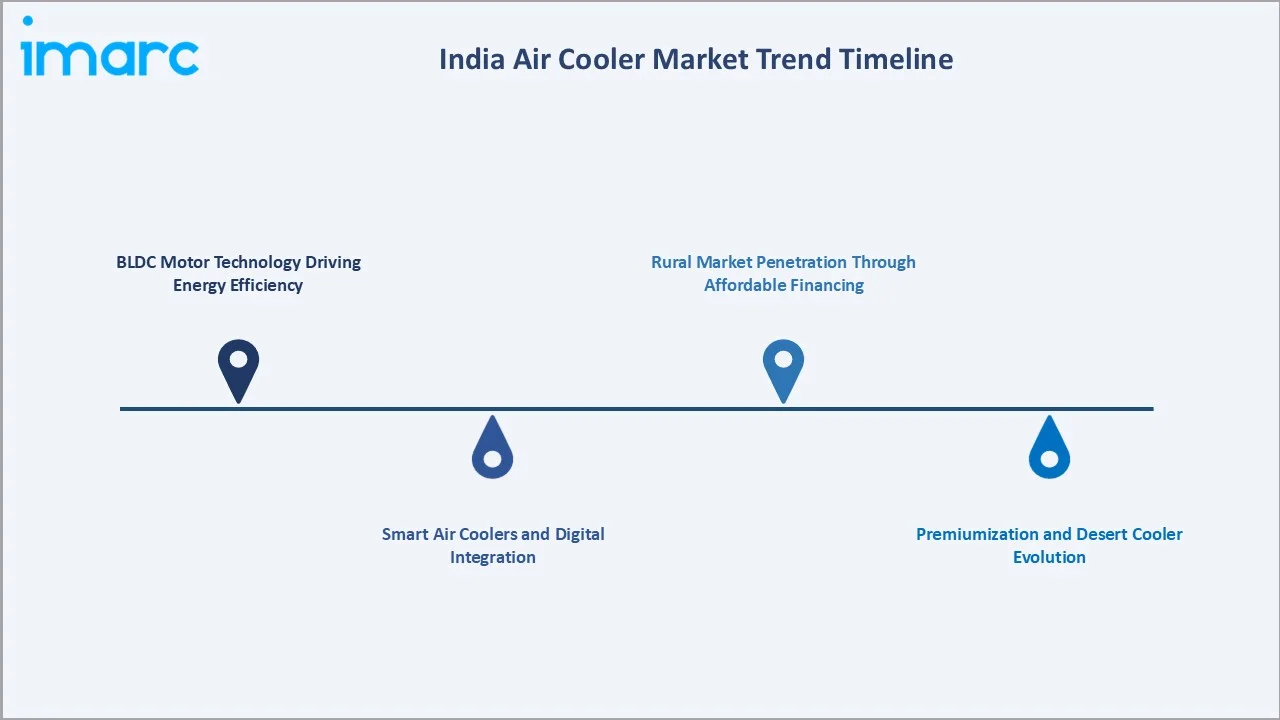

1. BLDC Motor Technology Driving Energy Efficiency

Brushless Direct Current motors are replacing conventional induction motors in premium air coolers, significantly reducing power consumption. As BEE star rating frameworks extend to air coolers, BLDC-equipped models are gaining regulatory preference and consumer adoption across urban markets seeking lower electricity bills.

2. Smart Air Coolers and Digital Integration

Manufacturers are integrating digital touch screens, mobile app controls, IoT connectivity, and air purification into cooler design. Virtual product specialists and digital engagement tools are transforming the consumer purchase journey, improving customer satisfaction and driving online sales conversion for leading brands.

3. Premiumization and Desert Cooler Evolution

Desert coolers with large-capacity tanks are evolving into feature-rich products with honeycomb pads, auto-fill functions, humidity control, and dual-blower designs. Premium models are growing fastest in Tier I urban markets, improving overall market revenue realization and average selling prices.

4. Rural Market Penetration Through Affordable Financing

EMI schemes, BNPL options, and rural microfinance partnerships are enabling affordable cooler ownership in income-constrained rural households. Localized manufacturing initiatives are reducing logistics costs and improving product affordability for non-metro consumers in underserved geographies.

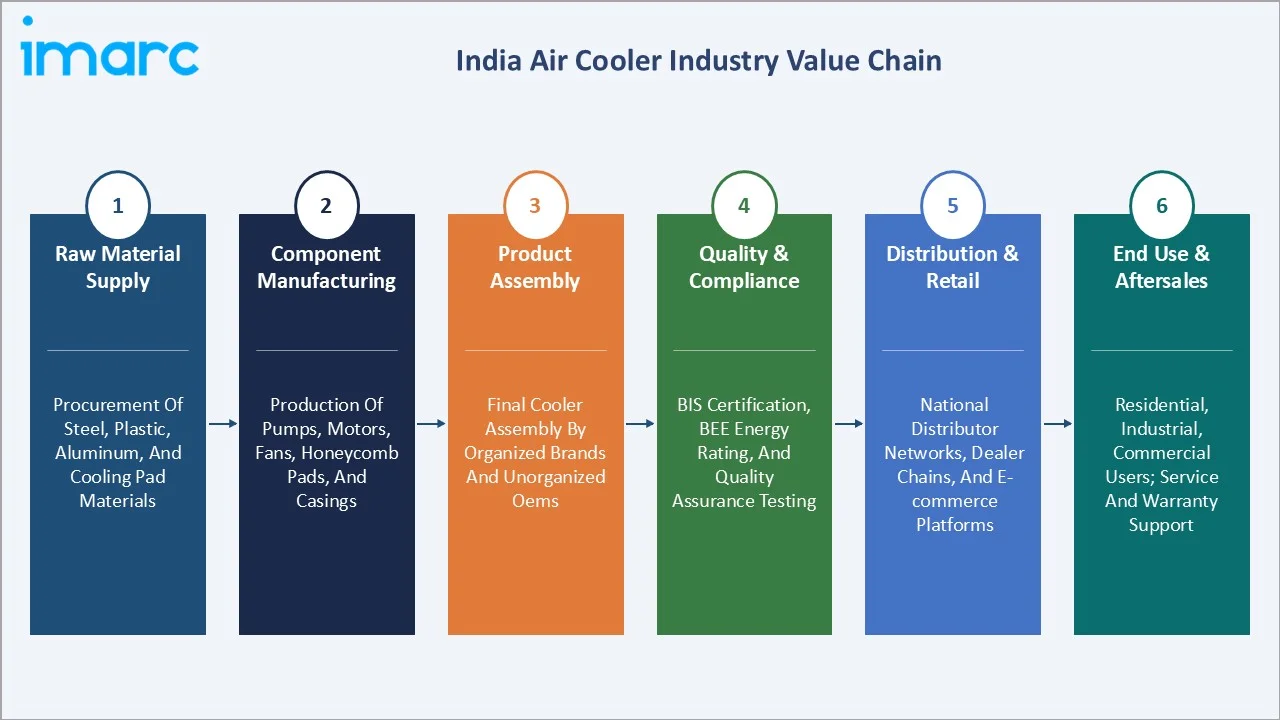

Industry Value Chain Analysis

The India air cooler value chain spans six stages from raw material procurement to after-sales service. Product assembly and brand distribution capture the highest value-add margins, while organized players leverage channel strength and brand equity to differentiate from unorganized local manufacturers.

|

Stage |

Description |

|

Raw Material Supply |

Procurement of steel, plastic, aluminum, and cooling pad materials |

|

Component Manufacturing |

Production of pumps, motors, fans, honeycomb pads, and casings |

|

Product Assembly |

Final cooler assembly by organized brands and unorganized OEMs |

|

Quality & Compliance |

BIS certification, BEE energy rating, and quality assurance testing |

|

Distribution & Retail |

National distributor networks, dealer chains, and e-commerce platforms |

|

End Use & Aftersales |

Residential, industrial, commercial users; service and warranty support |

Technology Landscape in the India Air Cooler Industry

Evaporative Cooling Technology: Honeycomb vs. Wood Wool Pads

Honeycomb cellulose pads have become the industry standard for evaporative cooling efficiency, offering superior cooling performance versus traditional wood wool pads. Their cross-fluted structure maximizes surface area, improves airflow, and extends pad lifespan significantly, reducing maintenance frequency and total cost of ownership.

Motor Technology: Induction to BLDC

BLDC motor technology reduces power consumption substantially versus conventional induction motors. Leading manufacturers including Symphony Limited, Bajaj Electricals, and Havells India have launched BLDC-equipped product lines targeting energy-conscious urban consumers seeking lower electricity bills without compromising on cooling performance.

Smart Connectivity and Air Purification Integration

Wi-Fi and Bluetooth connectivity, voice control compatibility with smart home ecosystems, and app-based scheduling are being integrated into premium cooler models. HEPA filter integration for dual cooling-purification functionality is emerging as a differentiator in urban markets with high ambient pollution levels.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Organized/Unorganized |

🔒 |

🔒 |

2025 |

|

End Use |

Residential Air Coolers |

72.4% |

2025 |

|

Tank Capacity |

🔒 |

🔒 |

2025 |

|

Distribution Channel |

Offline |

68.5% |

2025 |

|

Region |

North India |

36.8% |

2025 |

By Distribution Channel

Offline distribution commands a dominant 68.5% share in 2025, anchored by the extensive multi-brand dealer, general trade, and modern retail network spanning metro, tier I, II, and III cities. Large-format electronics chains and brand-exclusive outlets in urban centers reinforce the offline channel's continued dominance.

To access detailed market analysis, Request Sample

Online distribution at 31.5% in 2025, growing at approximately 8.4% CAGR, is the fastest-expanding channel driven by major e-commerce platforms and direct-to-consumer brand websites. Online channel enables year-round discounting, wider SKU availability, and rural consumer access beyond the geographic limitations of physical dealer networks.

By End Use

Residential air coolers dominate at 72.4% in 2025, reflecting the enormous Indian household cooling need. A significant proportion of Indian households lack air conditioning access, and air coolers serve as the primary affordable cooling solution at a fraction of the purchase cost and electricity consumption of a split air conditioner.

Industrial and commercial air coolers at 27.6% in 2025 address warehouses, factories, textile mills, and large commercial spaces. Industrial coolers serve as a cost-effective evaporative cooling solution for large-space temperature management, at significantly lower operating costs than centralized HVAC systems.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

North India |

36.8% |

Dry, hot climate; high seasonal demand; dense population base |

|

West & Central India |

28.4% |

Semi-arid zones; industrial cooling demand; manufacturing hubs |

|

South India |

20.6% |

Urban commercial adoption; tower coolers growing in metro areas |

|

East India |

14.2% |

Emerging urbanization; rural electrification; rising incomes |

North India's 36.8% market dominance in 2025 stems from the region's hot, dry climate where evaporative cooling delivers maximum efficiency. Northern states record extreme summer temperatures and house large populations that rely on air coolers as the primary household cooling solution.

West and Central India at 28.4% benefits from semi-arid climatic conditions across multiple states that support effective evaporative cooling. The region's growing industrial base and expanding middle-class population are driving sustained demand growth across both residential and commercial air cooler segments.

South India at 20.6% is witnessing growing urban adoption in major metropolitan areas, particularly in the commercial and office space segment. Tower coolers and personal coolers are gaining traction despite the region's higher humidity index, which limits the effectiveness of traditional large-capacity desert coolers.

Competitive Landscape

The India air cooler market is moderately fragmented, with organized branded players holding approximately 60–65% of market value and unorganized local manufacturers accounting for the balance.

|

Company Name |

Key Products |

Market Position |

Strategic Focus |

|

Symphony |

Desert coolers, Tower coolers, commercial coolers |

Leader |

Market leader; smart coolers; global exports |

|

Havells India Ltd. |

Desert Coolers, Tower Coolers, Personal Coolers, Window Coolers, Commercial Coolers |

Challenger |

Premium urban segment; BLDC technology |

|

Crompton Greaves Consumer Electricals Limited |

Desert Coolers, Tower Coolers, Personal Coolers, Window Coolers |

Challenger |

Energy-efficient models; pan-India distribution |

|

Usha International Ltd. |

Desert Coolers, Tower Coolers, Personal Coolers, Window Coolers |

Challenger |

Brand heritage; Tier II household segment |

|

NOVAMAX INDUSTRIES LLP |

Desert coolers, personal & tower coolers, commercial-grade air coolers |

Emerging |

Value segment; industrial and commercial cooling focus |

|

Blue Star Limited |

Desert Coolers, Tower Coolers, Personal Coolers, Window Coolers |

Challenger |

Commercial cooling solutions; institutional segment focus |

Key players include Symphony, Havells India Ltd., Crompton Greaves Consumer Electricals Limited, Usha International Ltd., NOVAMAX INDUSTRIES LLP, Blue Star Limited, and others.

Key Company Profiles

Symphony

Symphony operates across domestic and international markets, holding a leadership position in India's organized air cooler segment through a diversified product portfolio covering personal, desert, tower, window, and industrial air cooler categories.

- Product Portfolio: Desert coolers, tower coolers, personal coolers, commercial coolers, and others.

- Recent Developments: In April 2023, Symphony Limited introduced the range of air coolers powered by BLDC (Brushless DC) technology, aimed at significantly improving energy efficiency and reducing electricity consumption. The new product line consumes up to 60% less power than conventional air coolers and includes features such as multiple speed settings, sleep mode, touchscreen controls, and water tank alerts.

- Strategic Focus: Symphony Limited focuses on sustaining global market leadership through continuous product innovation, BLDC technology advancement, and smart connectivity integration, while expanding its industrial cooler portfolio and strengthening international export presence across emerging and developed markets.

Havells India Ltd.

Havells is a leading fast-moving electrical goods company in India with a growing premium air cooler portfolio. Havells targets the urban upper-middle income consumer segment with design-forward, energy-efficient air cooler products that command premium pricing over mass-market alternatives.

- Product Portfolio: Desert coolers, tower coolers, personal coolers, window coolers, commercial coolers, and others.

- Strategic Focus: Havells India Limited focuses on premiumization through BLDC motor technology, smart home connectivity, and design-led product differentiation, targeting urban upper-income consumers seeking energy-efficient and feature-rich air-cooling solutions at premium price points.

Usha International Ltd.

Usha International Limited is a diversified consumer goods company with a heritage spanning over nine decades in the Indian market. The company's air cooler portfolio serves residential consumers across all geographies, with a focus on delivering reliable, energy-efficient cooling solutions backed by an extensive nationwide service and distribution network.

- Product Portfolio: Desert Coolers, Tower Coolers, Personal Coolers, Window Coolers.

- Strategic Focus: Usha International Limited leverages its long-standing brand heritage and extensive nationwide service network to sustain a strong presence in the residential air cooler segment, targeting tier II and tier III city households seeking reliable, affordable, and energy-efficient cooling solutions.

Market Concentration Analysis

India's air cooler market is moderately fragmented at the national level, with organized players holding the majority of value share and unorganized local manufacturers accounting for a significant volume share. No single company dominates the entire market, though Symphony Limited approaches leadership in the organized desert and industrial cooler segments.

Regional concentration is more pronounced. Symphony Limited leads in the desert cooler segment across North and West India. Bajaj Electricals leads volume in mass-market categories across regions. Consolidation among branded players is accelerating through new product launches, digital marketing investment, and distribution network expansion displacing unorganized local manufacturers.

Investment & Growth Opportunities

Fastest-Growing Segments

Online distribution is the highest-growth channel through 2034, driven by e-commerce penetration in rural areas and direct-to-consumer brand expansion. Smart and BLDC-powered cooler products represent the highest-value premium opportunity within the residential segment, commanding significantly higher pricing than conventional models.

Emerging Markets

East India is the fastest-growing region for air coolers through 2034, driven by improving rural electrification and rising disposable incomes. The region's expanding urban middle class and ongoing industrial corridor development are creating new addressable demand in a previously underserved geography.

Venture & Investment Trends

Manufacturing investment is being directed toward BLDC motor production localization and smart product R&D. Government PLI scheme benefits for white goods and policy support for energy-efficient appliances are creating tailwinds for capital investment in modern air cooler manufacturing facilities and product innovation.

Future Market Outlook (2026-2034)

The India air cooler market is forecast to expand from INR 126.06 Billion in 2025 to INR 235.10 Billion by 2034 at a CAGR of 6.81%, reflecting consistent non-discretionary summer cooling demand, rising disposable incomes, and rural market expansion. The market adds significant incremental annual value through the forecast period.

Three structural forces will shape the market through 2034: continued rural electrification enabling first-time cooler ownership, premiumization driving BLDC and smart cooler adoption in urban markets, and the industrial cooling segment's rapid uptake of high-capacity coolers as a cost-effective alternative to centralized HVAC systems.

Online channels are expected to represent a significantly larger share of market by 2034, reflecting direct-to-consumer brand growth and e-commerce penetration in tier III cities. North India will retain regional dominance, while East India will emerge as the fastest-growing region through sustained rural development and urbanization investment.

Research Methodology

Primary Research

Primary research encompassed structured interviews with senior officials at air cooler manufacturers, organized retail buyers, regional distributors, and industry association representatives including CEAMA. Primary data validated market sizing, segment shares, regional demand estimates, and technology adoption timelines.

Secondary Research

Key secondary sources include CEAMA industry data, Bureau of Energy Efficiency appliance market reports, Ministry of Power rural electrification data, India Brand Equity Foundation e-commerce projections, and trade publications covering the Indian consumer appliance and electrical goods sectors.

Forecasting Models

Market size estimations and growth projections combine top-down macroeconomic modeling and bottom-up segment-level demand analysis, incorporating GDP growth rates, rural electrification progress, consumer expenditure data, per capita disposable income trends, and historical market evolution patterns.

India Air Cooler Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion INR |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Organized/ Unorganized Covered | Organized, Unorganized |

| End-Uses Covered |

|

| Tank Capacities Covered | Low, Medium, High |

| Distribution Channels Covered | Online, Offline |

| Region Covered | North India, East India, West and Central India, South India |

| Companies Covered | Symphony, Havells India Ltd., Crompton Greaves Consumer Electricals Limited, Usha International Ltd., NOVAMAX INDUSTRIES LLP, Blue Star Limited, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India air cooler market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the India air cooler market.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India air cooler industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India Air Cooler Market Report

The India air cooler market reached INR 126.06 Billion in 2025, reflecting consistent demand from rising temperatures, rural electrification, and expanding middle-class adoption of affordable cooling solutions.

The market is projected to reach INR 235.10 Billion by 2034, growing at a CAGR of 6.81% during 2026-2034, driven by online channel expansion, rural market penetration, and smart air cooler adoption.

Offline distribution leads with 68.5% market share in 2025, supported by the extensive dealer and retail network across tier I, II, and III cities. Online channels are the fastest-growing at approximately 8.4% CAGR.

Residential air coolers dominate with 72.4% market share in 2025, driven by the large cost-conscious Indian household base requiring affordable cooling alternatives to energy-intensive air conditioners.

North India commands 36.8% market share in 2025, driven by the region's hot, dry climate where evaporative cooling delivers maximum efficiency for residential and commercial users.

Online distribution is the fastest-growing channel at approximately 8.4% CAGR through 2034, driven by e-commerce platform penetration in rural India, competitive online pricing, and direct-to-consumer brand expansion.

Leading companies include Symphony, Havells India Ltd., Crompton Greaves Consumer Electricals Limited, Usha International Ltd., NOVAMAX INDUSTRIES LLP, Blue Star Limited, and others.

Key drivers include rising summer temperatures, government rural electrification programs, expanding e-commerce channels, energy cost advantages over air conditioners, and growing disposable incomes across rural and semi-urban India.

Key challenges include high-humidity limitations, intense price competition from unorganized manufacturers, seasonal demand concentration, and growing water scarcity concerns in key northern consuming regions.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade