India Air Quality Monitoring Market Size, Share, Trends and Forecast by Product Type, Pollutant, Sampling Method, End User, and Region, 2026-2034

India Air Quality Monitoring Market Summary:

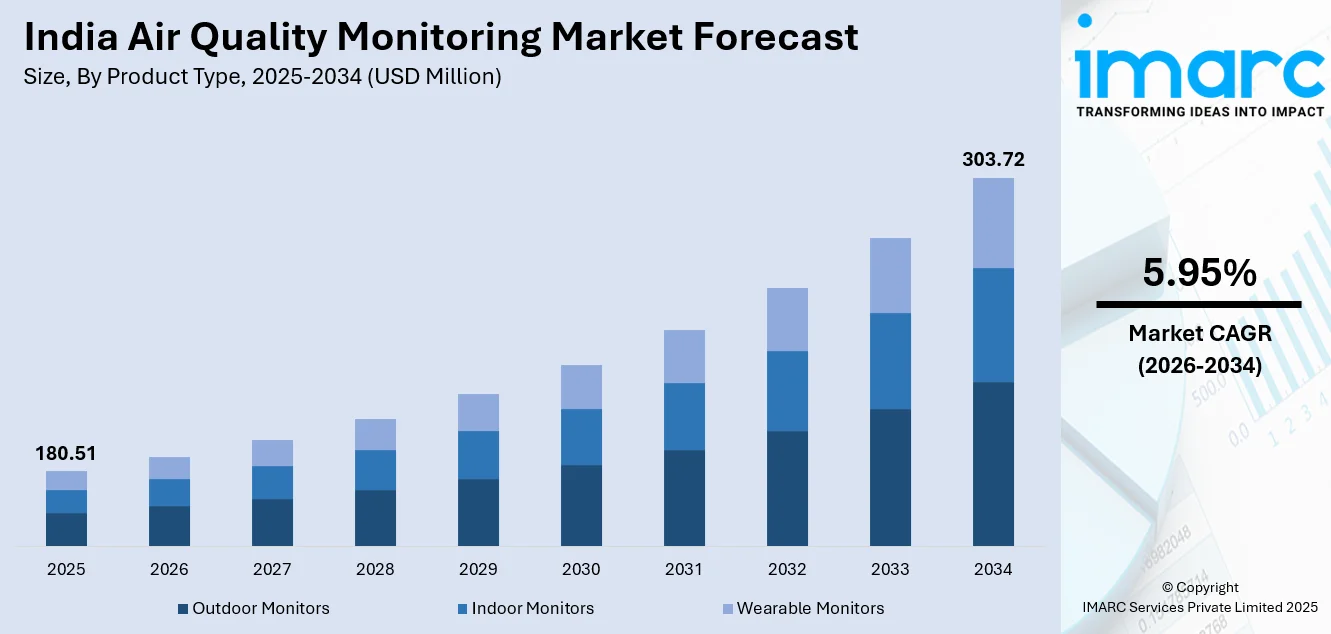

The India air quality monitoring market size was valued at USD 180.51 Million in 2025 and is projected to reach USD 303.72 Million by 2034, growing at a compound annual growth rate of 5.95% from 2026-2034.

The India air quality monitoring market is experiencing significant momentum as the nation intensifies its environmental surveillance efforts. Expanding urbanization, growing industrial activity, and heightened public consciousness about pollution-related health risks are accelerating the deployment of advanced monitoring solutions. Supportive regulatory frameworks, smart city development initiatives, and technological advancements in sensor-based platforms are further reinforcing the adoption of air quality monitoring infrastructure across government, industrial, and residential sectors nationwide.

Key Takeaways and Insights:

-

By Product Type: Outdoor monitors dominate the market with a share of 45% in 2025, driven by their essential role in regulatory compliance, ambient pollution tracking, and government-mandated deployment across urban centers and industrial corridors nationwide.

- By Pollutant: Chemical pollutant leads the market with a share of 40% in 2025, due to extensive monitoring requirements for gaseous emissions such as sulfur dioxide, nitrogen dioxide, carbon monoxide, and volatile organic compounds across industrial and urban environments.

- By Sampling Method: Active/continuous monitoring holds the largest share of 49% in 2025, reflecting the growing mandate for real-time, uninterrupted data collection to support regulatory enforcement, public health alerts, and environmental governance across the country.

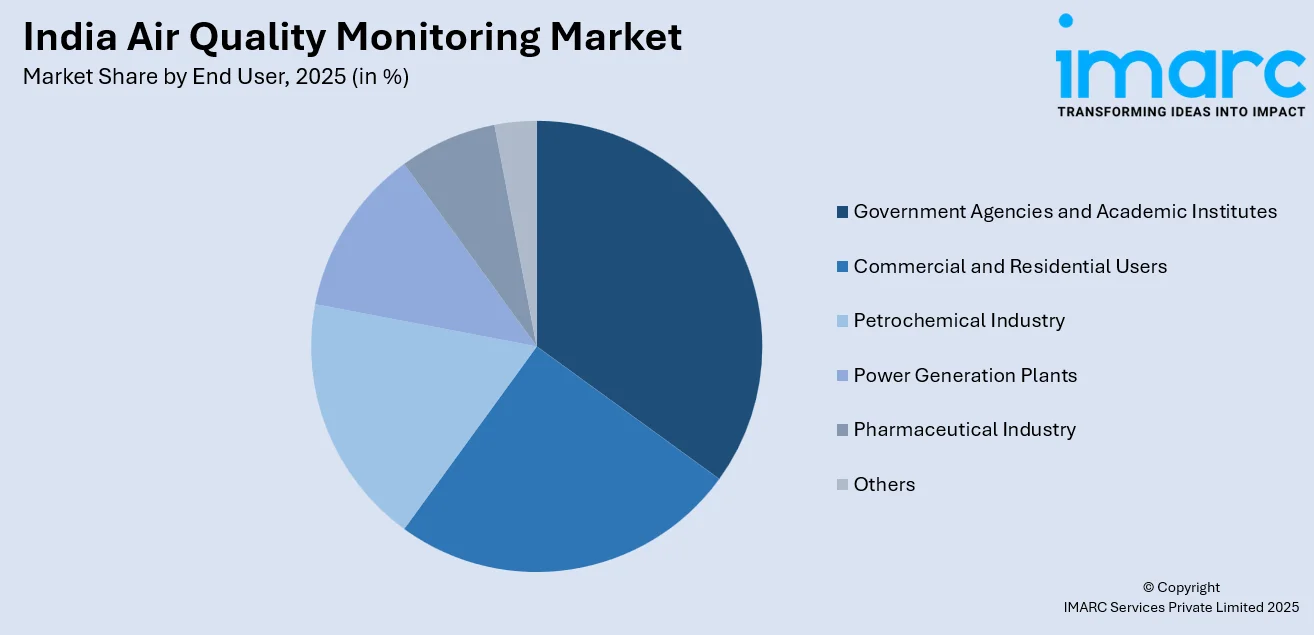

- By End User: Government agencies and academic institutes dominate the market with a share of 28% in 2025, underscoring the critical role of public sector investment and research-driven initiatives in expanding national air quality monitoring infrastructure.

- By Region: North India leads the market with a 31% share in 2025, attributed to the region's elevated pollution levels, dense industrial clusters, high population density, and concentrated regulatory monitoring activities across the Indo-Gangetic Plain.

- Key Players: The India air quality monitoring market features a competitive landscape with both multinational technology providers and domestic environmental solution companies expanding product portfolios, investing in localized manufacturing capabilities, and forming strategic partnerships to strengthen market positioning.

To get more information on this market Request Sample

The India air quality monitoring market is expanding steadily as the country addresses its pressing air pollution challenges through a combination of regulatory enforcement, technological modernization, and public health awareness campaigns. For example, in March 2025 the Delhi government announced plans to install six new continuous ambient air quality monitoring stations, expanding the city’s network to improve spatial coverage and real‑time pollution tracking. The central and state governments continue to strengthen ambient air monitoring networks by deploying continuous monitoring stations across urban and industrial zones, guided by national programmes aimed at reducing particulate matter concentrations in non-attainment cities. Simultaneously, advancements in sensor technologies, Internet of Things integration, and artificial intelligence-driven analytics are transforming traditional monitoring approaches into intelligent, real-time environmental surveillance systems. The growing emphasis on smart city infrastructure is further catalyzing demand for interconnected monitoring solutions that provide granular, location-specific air quality data. Industrial compliance requirements, expanding urban footprints, and rising public demand for transparent environmental data continue to create sustained growth opportunities across the market.

India Air Quality Monitoring Market Trends:

Integration of IoT and Artificial Intelligence in Monitoring Systems

The India air quality monitoring market is witnessing a transformative shift with the integration of Internet of Things and artificial intelligence technologies into environmental surveillance platforms. For instance, in 2025 the Brihanmumbai Municipal Corporation (BMC), in collaboration with IIT Kanpur, launched the AI‑powered Mumbai Air Network for Advanced Sciences (MANAS), a hyperlocal air quality monitoring platform using sensor networks and machine learning to provide real‑time, localized AQI data across the city. Smart sensor networks capable of autonomous data collection, cloud-based analytics, and predictive modelling are replacing traditional manual sampling approaches. These intelligent systems enable real-time pollutant tracking, early warning generation, and data-driven policy formulation, significantly enhancing the efficiency and accuracy of air quality management across urban and industrial settings.

Widespread Adoption of Portable and Wearable Air Quality Monitors

Increasing public awareness about the health impacts of air pollution is driving the growing adoption of portable and wearable air quality monitors across India. As air quality in Indian metros reaches critical levels, a new market for wearable and portable anti‑pollution gadgets, including personal air trackers and wearable purifiers, has been emerging rapidly, with brands such as Oxyhola and NewDru gaining traction among consumers seeking real‑time exposure data. Individuals, institutions, and small businesses are seeking personalized, real-time pollution data beyond what traditional fixed stations provide. Compact, sensor-based devices that measure particulate matter and gaseous pollutants are enabling users to make informed decisions about outdoor activities, commuting routes, and indoor air management, reflecting a broader democratization of environmental data access.

Expansion of Smart City-Driven Environmental Monitoring Networks

India's ambitious smart city development initiatives are catalyzing the deployment of extensive environmental monitoring networks across urban centers. In August 2025, the Greater Chennai Corporation is set to install 75 Internet of Things (IoT)‑based air quality sensors that will feed real‑time pollutant data into the city’s Integrated Command and Control Centre (ICCC) for centralized tracking and public dissemination. Municipal corporations are integrating air quality sensors into city command and control centers, enabling centralized surveillance, automated alerting, and data visualization for both administrators and residents. These interconnected monitoring frameworks support pollution hotspot identification, traffic emission management, and evidence-based urban planning, positioning air quality monitoring as a foundational element of intelligent urban infrastructure.

Market Outlook 2026-2034:

The India air quality monitoring market is poised for sustained growth as regulatory frameworks tighten, urban populations expand, and industrial activities intensify across the nation. Continued government investment in national clean air programmes, expansion of continuous monitoring station networks, and increasing adoption of advanced sensor technologies will serve as primary growth catalysts. The convergence of environmental awareness, digital transformation, and public health priorities is expected to drive robust demand for comprehensive monitoring solutions. The market generated a revenue of USD 180.51 Million in 2025 and is projected to reach a revenue of USD 303.72 Million by 2034, growing at a compound annual growth rate of 5.95% from 2026-2034.

India Air Quality Monitoring Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Product Type |

Outdoor Monitors |

45% |

|

Pollutant |

Chemical Pollutant |

40% |

|

Sampling Method |

Active/Continuous Monitoring |

49% |

|

End User |

Government Agencies and Academic Institutes |

28% |

|

Region |

North India |

31% |

Product Type Insights:

- Indoor Monitors

- Outdoor Monitors

- Wearable Monitors

The outdoor monitors dominates with a market share of 45% of the total India air quality monitoring market in 2025.

Outdoor air quality monitors represent the cornerstone of India's environmental surveillance infrastructure, serving as the primary instruments for regulatory compliance and public air quality index reporting. In 2025, the Andhra Pradesh Pollution Control Board announced plans to add 62 new air quality monitoring stations statewide, including 9 new continuous ambient air quality monitoring stations equipped for real‑time AQI reporting, to create one of the most comprehensive regional observation networks in South India. These systems are deployed across cities, industrial zones, and transport corridors to enable continuous tracking of ambient pollutant concentrations. Government agencies rely extensively on outdoor monitoring stations to enforce emission standards, assess environmental quality, and generate real-time data for public health advisories and policy interventions.

The sustained demand for outdoor monitors is further reinforced by national programmes mandating the establishment of continuous ambient air quality monitoring stations across non-attainment cities. The expansion of monitoring networks into semi-urban and peri-urban areas, combined with the growing need for high-precision equipment capable of tracking multiple pollutants simultaneously, is strengthening the dominance of outdoor monitoring solutions within India's air quality monitoring ecosystem.

Pollutant Insights:

- Chemical Pollutant

- Physical Pollutant

- Biological Pollutant

The chemical pollutant leads with a share of 40% of the total India air quality monitoring market in 2025.

Chemical pollutant monitoring holds the largest revenue share within the India air quality monitoring market, reflecting the critical need to track gaseous emissions including sulfur dioxide, nitrogen dioxide, carbon monoxide, ozone, and volatile organic compounds. Industrial activities spanning power generation, petrochemical processing, manufacturing, and transportation generate substantial chemical emissions that require continuous surveillance to ensure compliance with national ambient air quality standards.

The regulatory mandate for industries to install continuous emission monitoring systems and report real-time pollutant data to central and state pollution control boards is sustaining robust demand for chemical pollutant monitoring equipment. Additionally, the growing deployment of gas analyzers and multi-parameter sensors across urban monitoring stations is reinforcing the segment's prominence, as authorities prioritize comprehensive chemical pollutant tracking for public health protection and environmental governance.

Sampling Method Insights:

- Active/Continuous Monitoring

- Passive Monitoring

- Intermittent Monitoring

- Stack Monitoring

The active/continuous monitoring dominates with a market share of 49% of the total India air quality monitoring market in 2025.

Active and continuous monitoring methods account for the highest revenue share in the India air quality monitoring market, driven by the increasing regulatory emphasis on real-time, uninterrupted environmental data collection. Continuous ambient air quality monitoring stations deployed across urban centers and industrial zones provide round-the-clock measurements of particulate matter, gaseous pollutants, and meteorological parameters, forming the backbone of India's national air quality surveillance network.

The increasing mandate for automated data transmission to centralized pollution monitoring portals, combined with expanding smart city infrastructure, is driving the widespread adoption of continuous monitoring solutions across India. Active sampling methodologies deliver superior accuracy, higher temporal resolution, and more reliable pollutant detection compared to passive techniques, positioning them as indispensable tools for regulatory enforcement and compliance verification. These capabilities support early warning system activation, real-time public health advisories, and evidence-based environmental policy formulation, reinforcing their critical role in national air quality governance.

End User Insights:

Access the comprehensive market breakdown Request Sample

- Government Agencies and Academic Institutes

- Commercial and Residential Users

- Petrochemical Industry

- Power Generation Plants

- Pharmaceutical Industry

- Others

The government agencies and academic institutes leads with a share of 28% of the total India air quality monitoring market in 2025.

Government agencies and academic institutes account for the highest share in the market, establishing themselves as the largest end-user segment. For example, in February 2026, the Uttar Pradesh Pollution Control Board signed a memorandum of understanding with the Indian Institute of Information Technology (IIIT) Lucknow to jointly develop an AI‑based air pollution monitoring and analytics system, demonstrating how regulatory bodies and academic research institutions are collaborating to enhance real‑time pollution tracking and enforcement. Central and state pollution control boards serve as the primary procurers of ambient monitoring equipment, deploying extensive station networks as part of national environmental programmes and regulatory enforcement mandates. Municipal authorities across non-attainment cities are continuously expanding their monitoring infrastructure to meet compliance targets and generate real-time environmental data for public health governance.

Academic and research institutions further strengthen this segment through air quality studies, source apportionment analyses, and sensor validation projects that advance monitoring capabilities. Universities and government-funded laboratories are actively developing indigenous, cost-effective monitoring technologies to support broader network deployment across underserved regions. The consistent allocation of public sector funding for expanding monitoring coverage, strengthening data collection systems, and supporting research-driven environmental initiatives ensures sustained procurement demand from this segment.

Regional Insights:

- North India

- South India

- East India

- West India

North India exhibits a clear dominance with a 31% share of the total India air quality monitoring market in 2025.

North India represents the largest regional segment owing to the severe air pollution challenges concentrated across the Indo-Gangetic Plain drive disproportionately higher deployment of continuous ambient monitoring stations. Dense industrial clusters, thermal power generation activities, seasonal agricultural stubble burning, and heavy vehicular traffic in states spanning the national capital region and surrounding areas generate persistently elevated pollutant concentrations that necessitate extensive monitoring infrastructure.

The high concentration of non-attainment cities designated under national clean air programmes in North India has resulted in significant government investment in monitoring network expansion across the region. The presence of key regulatory bodies, pollution control authorities, and premier research institutions in the national capital territory further reinforces demand for sophisticated monitoring equipment. Additionally, growing public awareness about pollution-related health impacts in densely populated northern cities is accelerating the adoption of both institutional and community-level monitoring solutions.

Market Dynamics:

Growth Drivers:

Why is the India Air Quality Monitoring Market Growing?

Stringent Government Regulations and National Environmental Programs

The Indian government has established a comprehensive regulatory framework to address the nation's deteriorating air quality, creating sustained demand for monitoring equipment and solutions. As part of this effort, in December 2025, the Central Pollution Control Board (CPCB) directed states in the Delhi‑NCR region to ensure that over 2,000 highly polluting industrial units install and connect real‑time emission monitoring systems (OCEMS) to its central server by December 31, 2025, with strict penalties for non‑compliance, underscoring stronger enforcement mechanisms for industrial emissions monitoring. National programmes targeting the reduction of particulate matter concentrations across non-attainment cities mandate the establishment of ambient monitoring stations, real-time data reporting systems, and compliance enforcement mechanisms. Central and state pollution control boards require industries across highly polluting sectors to install continuous emission monitoring systems and submit automated pollutant data, driving consistent procurement of monitoring technologies.

Rapid Urbanization and Industrial Expansion Across Major Economic Corridors

India's accelerating urbanization trajectory and expanding industrial footprint are generating concentrated emission sources that necessitate comprehensive air quality monitoring coverage. In November 2025, the West Bengal government announced plans to implement real‑time pollution tracking systems across key industrial parks, including Manikanchan SEZ, Shilpangan, Paridhan Garment Park, Rishi Bankim Shilpaudyan, and the Haldia Industrial Park, to strengthen environmental surveillance in rapidly growing manufacturing hubs. Growing urban populations are intensifying pollution from vehicular traffic, construction activities, energy consumption, and commercial operations, making periodic monitoring insufficient for effective environmental management. The development of industrial corridors, manufacturing clusters, special economic zones, and logistics hubs across the country is creating new emission hotspots that require dedicated monitoring infrastructure. The convergence of urban growth and industrial expansion is transforming air quality monitoring from an advisory function into essential urban and industrial infrastructure, sustaining demand for equipment, software, and maintenance services.

Rising Public Health Awareness and Growing Concerns About Respiratory Diseases

Increasing evidence linking poor air quality to respiratory illnesses, cardiovascular diseases, and other chronic health conditions is significantly amplifying public demand for transparent environmental data and effective pollution monitoring. A 2025 report on India’s air pollution burden found that more than two million lives were lost in 2023 due to air pollution‑linked illnesses, with around 89% of these deaths tied to non‑communicable diseases such as heart disease, lung cancer, COPD, and diabetes, underscoring how deeply air quality affects public health. Heightened media coverage of pollution episodes, scientific research on health impacts, and educational campaigns by public health organizations are raising awareness among citizens, communities, and institutions. This growing consciousness is driving demand for both residential and commercial air quality monitors while simultaneously influencing policy changes that mandate stricter air quality standards and expanded monitoring networks.

Market Restraints:

What Challenges the India Air Quality Monitoring Market is Facing?

High Equipment Procurement and Maintenance Costs

The substantial capital investment required for procuring high-precision air quality monitoring equipment, along with ongoing operational and maintenance expenses, poses a significant barrier to widespread market adoption. Advanced continuous ambient monitoring stations require regular calibration, sensor replacement, and technical upkeep that strain budgets of municipal bodies and smaller industrial units. The reliance on imported components and specialized technical expertise further escalates the total cost of ownership, limiting the pace of network expansion particularly in resource-constrained regions.

Insufficient Monitoring Coverage in Rural and Semi-Urban Areas

Despite growing investments in urban monitoring infrastructure, vast rural and semi-urban regions across India remain significantly underserved with limited or no air quality monitoring capabilities. The logistical challenges of deploying and maintaining sophisticated equipment in remote locations, combined with inadequate power supply and connectivity infrastructure, restrict the expansion of monitoring networks beyond major cities. This coverage gap hinders comprehensive national air quality assessment and limits data-driven policy interventions in regions experiencing agricultural and industrial pollution.

Data Quality and Standardization Challenges Across Monitoring Networks

Inconsistencies in data quality, calibration standards, and reporting protocols across different monitoring stations and networks present a significant challenge to the India air quality monitoring market. The integration of data from continuous monitoring stations and manual sampling stations raises concerns about data integrity and comparability. Poor maintenance practices, non-compliance with siting guidelines, and variations in equipment quality across installations undermine the reliability of aggregated air quality assessments, affecting the credibility and utility of monitoring data for policy formulation.

Competitive Landscape:

The India air quality monitoring market is characterized by a dynamic competitive environment featuring a mix of established multinational corporations and emerging domestic technology providers. Market participants are actively investing in research and development to introduce innovative sensor technologies, portable monitoring devices, and integrated software platforms that offer enhanced precision and real-time data analytics capabilities. Strategic emphasis on local manufacturing, product localization, and cost optimization is enabling companies to address the price-sensitive Indian market while meeting stringent quality requirements. Partnerships with government agencies, pollution control boards, and smart city development authorities are serving as key channels for market penetration and revenue generation. The competitive landscape is further shaped by companies expanding service offerings to include installation, calibration, maintenance, and data management solutions, creating comprehensive value propositions that strengthen customer retention and long-term market positioning.

Recent Developments:

- In December 2025, The World Bank approved financing for two major clean‑air programs in Uttar Pradesh and Haryana, targeting improved air quality for 270 million people. Initiatives include electric transport, cleaner technologies for agriculture and industry, and advanced monitoring systems. The projects aim to boost health, productivity, and green jobs.

India Air Quality Monitoring Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Indoor Monitors, Outdoor Monitors, Wearable Monitors |

| Pollutants Covered | Chemical Pollutant, Physical Pollutant, Biological Pollutant |

| Sampling Methods Covered | Active/Continuous Monitoring, Passive Monitoring, Intermittent Monitoring, Stack Monitoring |

| End Users Covered | Government Agencies and Academic Institutes, Commercial and Residential Users, Petrochemical Industry, Power Generation Plants, Pharmaceutical Industry, Others |

| Regions Covered | North India, South India, East India, West India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Air Quality Monitoring Market Report

The India air quality monitoring market size was valued at USD 180.51 Million in 2025.

The India air quality monitoring market is expected to grow at a compound annual growth rate of 5.95% from 2026-2034 to reach USD 303.72 Million by 2034.

Outdoor monitors, holding the largest revenue share of 45%, remain central to India's air quality monitoring efforts, supporting regulatory compliance, ambient pollution tracking, and continuous public air quality index dissemination across urban and industrial areas.

Key factors driving the India air quality monitoring market include stringent government regulations, expanding national clean air programmes, rapid urbanization, industrial growth, rising public health awareness, advancements in sensor technologies, and smart city development initiatives.

Major challenges include high equipment procurement and maintenance costs, insufficient monitoring coverage in rural and semi-urban areas, data quality inconsistencies across monitoring networks, limited standardization protocols, and dependence on imported components.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)