India Airless Tires Market Size, Share, Trends and Forecast by Vehicle Type, Sales Channel, and Region, 2026-2034

India Airless Tires Market Size, Share, Trends & Forecast (2026-2034)

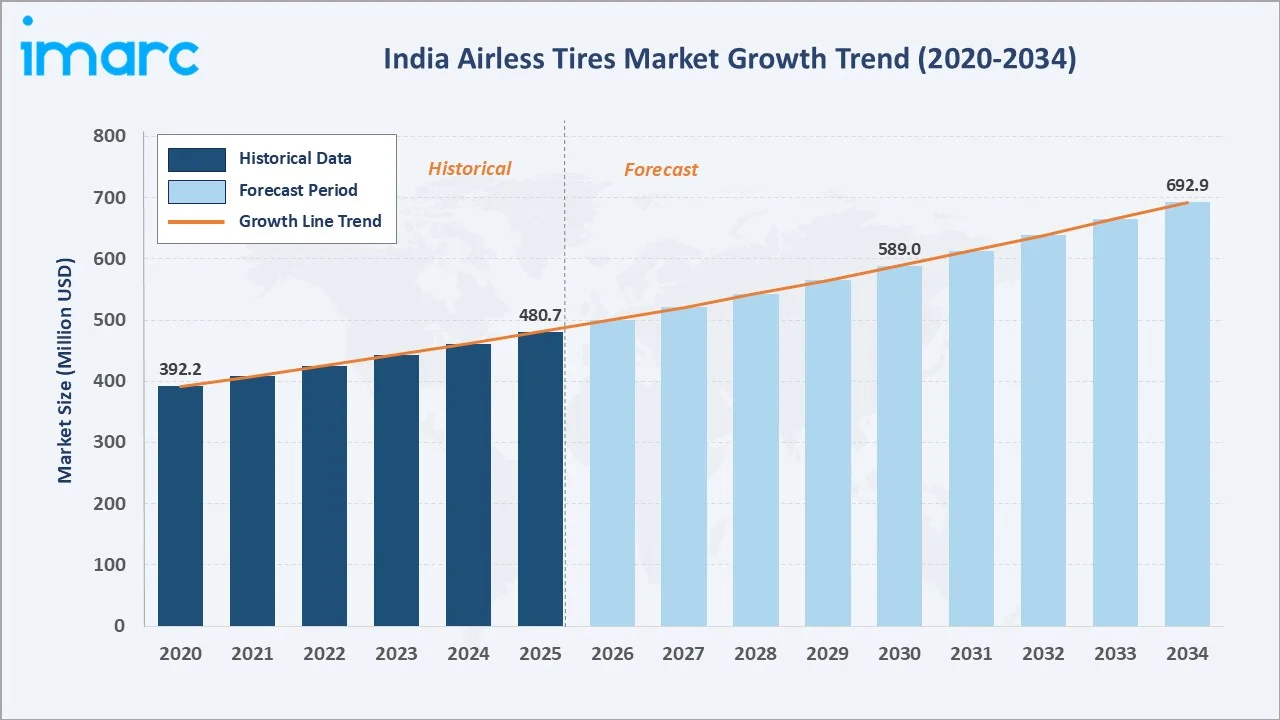

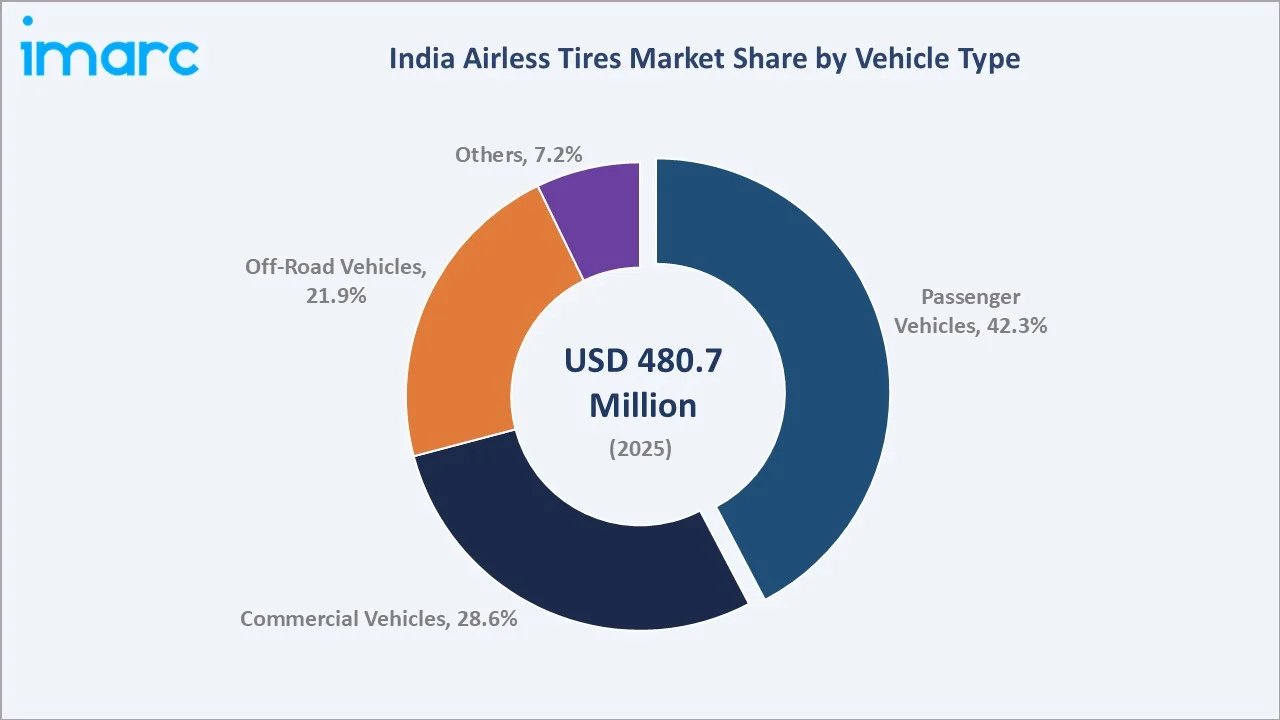

The India airless tires market reached USD 480.7 Million in 2025 and is projected to reach USD 692.9 Million by 2034, growing at a CAGR of 4.15% during 2026-2034. The market is driven by the growing demand for low-maintenance and puncture-proof tire solutions across construction equipment, military vehicles, utility vehicles, and last-mile mobility applications. Increasing infrastructure development, rising adoption of electric vehicles, and the need for enhanced durability and operational efficiency further support market growth. India aims to significantly increase EV adoption by 2030, targeting EV sales shares of 30% in private cars, 70% in commercial vehicles, 40% in buses, and 80% in two- and three-wheelers, equivalent to nearly 80 million EVs on the road, while promoting complete domestic EV manufacturing under the ‘Make in India’ initiative. Passenger vehicles lead vehicle type at 42.3%. OEM leads sales channel at 80.0%. North India leads at 33.7%.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 480.7 Million |

|

Forecast Market Size (2034) |

USD 692.9 Million |

|

CAGR (2026-2034) |

4.15% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Vehicle Type |

Passenger Vehicles (42.3%, 2025) |

|

Dominant Sales Channel |

OEM (80.0%, 2025) |

|

Leading Region |

North India (33.7%, 2025) |

India airless tires market is showing steady growth, rising from USD 392.2 Million in 2020 to USD 480.7 Million in 2025, anchored at USD 589.0 Million in 2030, and forecast to reach USD 692.9 Million by 2034, supported by increasing demand for puncture-proof, durable, and low-maintenance tires across EVs, utility vehicles, and industrial applications.

To get more information on this market, Request Sample

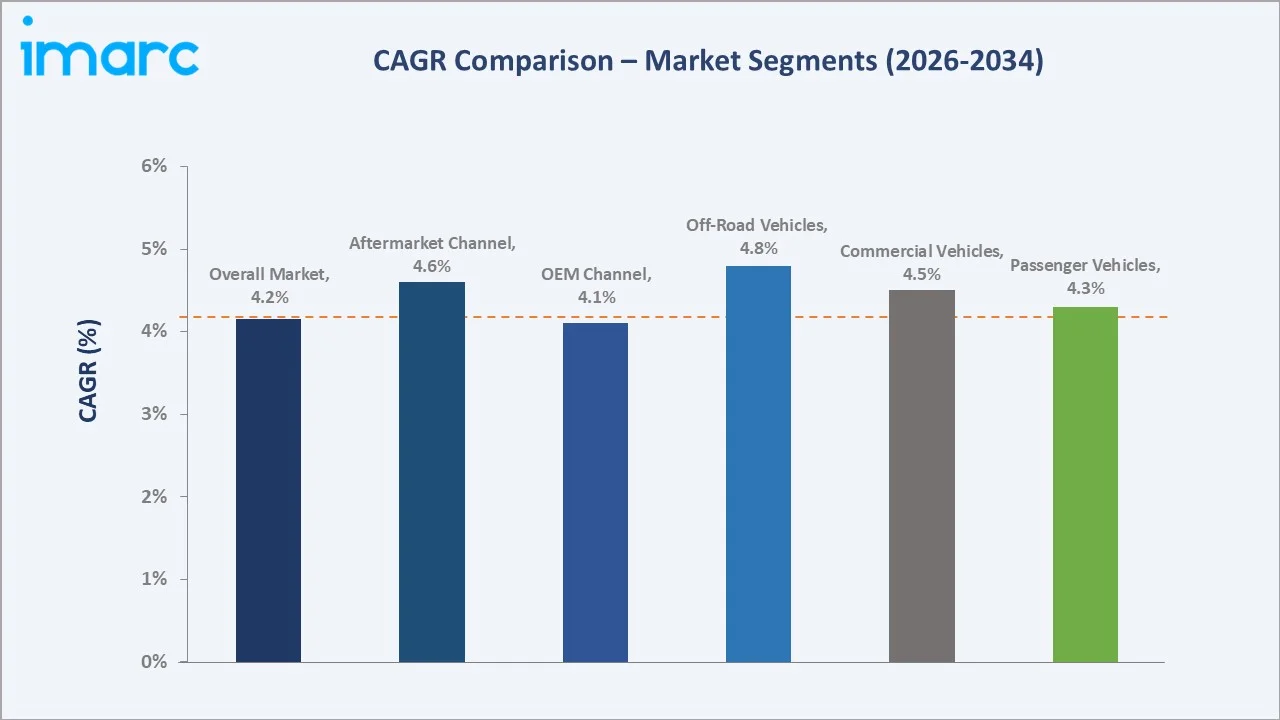

Off-road vehicles grow fastest at ~4.8% CAGR through Jharkhand and Odisha mining equipment, patrol vehicle fitment, and construction equipment in India's infrastructure investment program. Aftermarket grows at ~4.6% CAGR through government fleet replacement, golf course cart maintenance, and the industrial equipment service market.

Executive Summary

The India airless tires market is witnessing steady growth, supported by rising demand for puncture-proof, durable, and low-maintenance tire solutions. Market value increased from USD 392.2 Million in 2020 to USD 480.7 Million in 2025 and is projected to reach USD 692.9 Million by 2034. Growth is driven by expanding EV adoption, infrastructure development, and increasing use of utility, construction, and last-mile delivery vehicles. Airless tires are gaining traction due to reduced downtime, improved safety, and lower maintenance needs. The market outlook remains positive as domestic manufacturing, fleet electrification, and innovation in tire materials continue to advance.

Passenger vehicles at 42.3% lead through urban commuter EV and premium passenger car niche fitment. OEM at 80.0% dominates through golf cart, EV two-wheeler, and defence vehicle factory fitment. North India leads at 33.7% through the Delhi NCR automotive cluster and defence procurement.

Key Market Insights

|

Insight |

Data |

|

Dominant Vehicle Type |

Passenger Vehicles - 42.3% share (2025) |

|

Dominant Sales Channel |

OEM - 80.0% market share (2025) |

|

Leading Region |

North India - 33.7% share (2025) |

|

Market Opportunity |

EV two-wheeler OEM bundling; defence MRAP and military vehicle airless supply; smart city golf cart and micro-mobility; mining Jharkhand and Odisha off-road fleet |

Key Analytical Observations Supporting The Above Data:

- Passenger Vehicles at 42.3%: Passenger vehicles dominate due to the country’s large car parc, rising urban mobility demand, and growing preference for safer, puncture-resistant tires. Increasing EV passenger car adoption further supports demand for durable and low-maintenance tire solutions.

- OEM at 80.0%: The OEM dominates as vehicle manufacturers increasingly integrate advanced tire technologies during production to enhance safety, durability, and maintenance efficiency. Growing EV manufacturing and the push for factory-fitted innovative components further strengthen OEM demand.

- North India at 33.7%: North India dominates due to its strong automotive manufacturing base, high vehicle ownership, and growing logistics and construction activity. Rising EV adoption and industrial vehicle demand across key states further support regional growth.

India Airless Tires Market Overview

India airless tires market operates within the broader India tire market as the fastest-growing new-technology tire segment through airless tire's premium-innovation positioning above commodity replacement tire. The India airless tires market is commercially unique because it addresses a critical pain point of conventional tires, while offering longer service life and improved operational reliability. Its value proposition is particularly strong for fleet operators, construction equipment, utility vehicles, and emerging EV applications where uptime and cost efficiency are essential. The market also benefits from increasing interest in sustainable and maintenance-free mobility solutions, differentiating it from the traditional tire industry.

India airless tires ecosystem integrates polymer and rubber raw material supply, airless tire manufacturing and R&D, certification and testing, OEM fitment and bundling, dealer and aftermarket sales, and fleet operators and end-users. Macroeconomic factors include rapid urbanization, rising infrastructure spending, expanding logistics activity, and strong growth in vehicle ownership.

Market Dynamics

To evaluate market opportunities, Request Sample

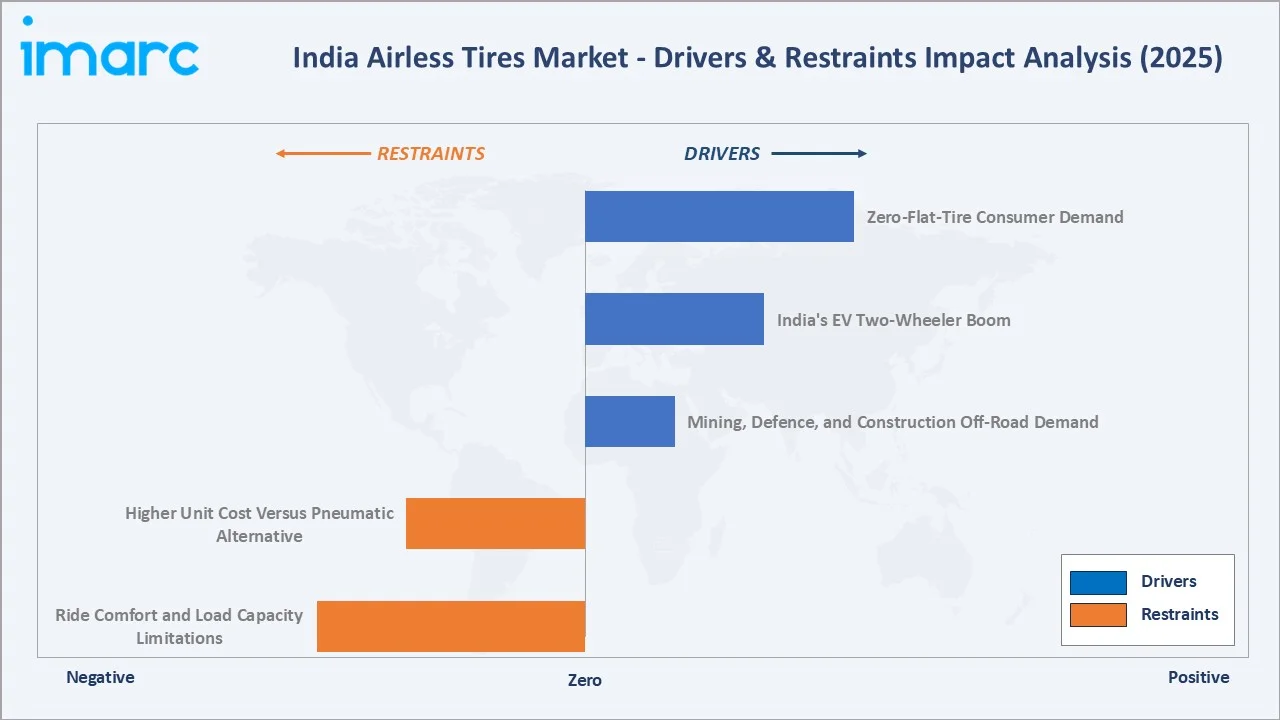

Market Drivers

- Zero-Flat-Tire Consumer Demand: Zero-flat-tire consumer demand is driving the market as users increasingly seek puncture-proof and low-maintenance mobility solutions. Poor road conditions, frequent tire damage, and high replacement costs are encouraging interest in durable alternatives. This demand is especially strong among daily commuters, fleet operators, delivery vehicles, and utility users, where downtime directly impacts productivity. As awareness of safety, convenience, and long-term cost savings rises, airless tires are gaining stronger commercial relevance.

- India's EV Two-Wheeler Boom: India's rapid EV two-wheeler adoption is creating strong demand for airless tires that offer enhanced durability, puncture resistance, and reduced maintenance requirements. Since electric scooters and motorcycles are widely used for daily commuting and last-mile delivery services, minimizing downtime is a key operational priority. Airless tires help improve vehicle availability and lower lifecycle costs, making them attractive for both individual users and commercial fleets. India’s electric two-wheeler penetration increased to 6.5% in FY26, compared with 6.1% in FY25, while retail sales grew 21.8% year-on-year, according to the Federation of Automobile Dealers Associations (FADA). Segment sales rose to 14,01,818 units in FY26 from 11,50,790 units in FY25. As EV two-wheeler production and sales continue to expand, the potential adoption of airless tire technology is expected to increase significantly.

- Mining, Defence, and Construction Off-Road Demand: Demand from the mining, defence, and construction sectors is supporting the growth of the India airless tires market, as vehicles operating in harsh terrains require highly durable and puncture-resistant tire solutions. Airless tires reduce the risk of tire failure, improve operational reliability, and minimize maintenance-related downtime in remote locations. Their ability to withstand heavy loads and challenging operating conditions makes them well-suited for off-road equipment and specialized vehicles. Rising investments in infrastructure, mining activities, and defence modernization are further expanding the market opportunity for airless tire manufacturers.

Market Restraints

- Higher Unit Cost Versus Pneumatic Alternative: Higher unit cost versus pneumatic tires limits adoption among price-sensitive consumers and fleet operators. Airless tires require advanced materials, specialized design, and newer manufacturing processes, making them costlier than conventional options. This creates a higher upfront purchase barrier, especially in mass-market two-wheelers, passenger vehicles, and small commercial fleets. Until economies of scale improve, conventional pneumatic tires may remain the preferred choice for cost-focused buyers.

- Ride Comfort and Load Capacity Limitations: Ride comfort and load capacity limitations are hampering the market, as some designs may deliver a firmer ride compared to pneumatic tires. This can reduce consumer acceptance in passenger vehicles and two-wheelers, where comfort is a key purchase factor. Limited suitability for high-speed, heavy-load, or long-distance applications may also restrict wider adoption. As a result, airless tires are currently more attractive for niche use cases than mass-market mobility.

Market Opportunities

- Electric Three-Wheeler Last-Mile Delivery: Electric three-wheelers are becoming a preferred choice for last-mile delivery services due to their low operating costs and suitability for urban logistics. Airless tires offer a significant advantage in this segment by eliminating puncture-related downtime and reducing maintenance expenses, which are critical for high-utilization delivery fleets. The rapid expansion of e-commerce, food delivery, and hyperlocal logistics networks is increasing the deployment of electric three-wheelers across Indian cities. Electric three-wheelers operate at around Rs 0.50 to Rs 1.30 per km on energy, versus Rs 4 to Rs 5 per km for diesel or CNG. This creates a strong opportunity for airless tire manufacturers to provide durable, cost-efficient tire solutions tailored to commercial fleet operations.

- Rising Demand for Low-Maintenance Mobility Solutions: Consumers and fleet operators are increasingly seeking products that reduce repair frequency, maintenance costs, and vehicle downtime. Airless tires eliminate the risk of punctures and do not require regular air-pressure monitoring, making them particularly attractive for commercial fleets, EVs, and utility vehicles. As the total cost of ownership becomes a key purchasing consideration, demand for airless tire technology is expected to strengthen across multiple vehicle segments.

Market Challenges

- Compatibility Issues with Existing Vehicle Platforms: Compatibility issues with existing vehicle platforms present a key challenge, as most vehicles are designed and optimized for conventional pneumatic tires. Airless tires may require modifications to suspension systems, wheel assemblies, and vehicle dynamics to ensure optimal performance and ride quality. These additional engineering requirements can increase adoption costs and slow aftermarket acceptance. As a result, widespread deployment may depend on greater collaboration between tire manufacturers and OEMs to develop vehicle-specific solutions.

- Lack of Large-Scale Domestic Manufacturing Capabilities: Lack of large-scale domestic manufacturing capabilities limits product availability and increases dependence on imports or pilot-scale production. Advanced materials, specialized molds, and precision engineering requirements make mass production more complex than conventional tires. This keeps costs high and delays wider commercialization across price-sensitive vehicle segments. Building local manufacturing capacity will be essential for improving affordability, supply reliability, and OEM adoption.

Emerging Market Trends

1. EV Two-Wheeler OEM Bundling as Primary Commercial Entry Point

EV two-wheeler OEM bundling is emerging as manufacturers seek differentiated, low-maintenance components for electric scooters and bikes. Airless tires can be factory-fitted to improve puncture resistance, reduce service visits, and enhance ownership convenience. This approach helps overcome aftermarket awareness barriers by introducing the technology directly through new EV models. As OEMs focus on durability and lower lifecycle costs, bundled airless tire solutions can become a practical commercial entry point.

2. Defence and Paramilitary Procurement Programs

Defence and paramilitary procurement programs are emerging due to the need for highly reliable, puncture-proof mobility solutions in demanding operational environments. Airless tires offer enhanced durability and mission readiness by reducing the risk of tire failures in remote or hostile terrains. India achieved record defence production of ₹1.54 lakh crore in FY 2024-25. Indigenous defence output also reached ₹1,27,434 crore in FY 2023-24, marking a 174% increase from ₹46,429 crore in 2014-15, while nearly 16,000 MSMEs are playing a key role in strengthening domestic defence capabilities. As defence modernization and local production expand, airless tires can gain adoption in tactical vehicles, off-road platforms, and support equipment requiring high reliability in harsh operating conditions.

3. Golf Course and Specialty Vehicle Niche Expansion

Vehicles such as golf carts, resort transport vehicles, utility carts, and campus mobility solutions benefit from airless tires due to their puncture-proof design and minimal maintenance requirements. These controlled operating environments provide an ideal setting for early adoption of airless tire technology. As hospitality, recreational, industrial, and institutional facilities expand, demand for reliable specialty mobility solutions is expected to create new market opportunities.

4. India Material Innovation: Domestic Polymer and Rubber R&D

India’s domestic polymer and rubber R&D is emerging as manufacturers seek cost-effective, durable materials for airless tire production. Local material innovation can improve load-bearing strength, heat resistance, ride comfort, and product lifespan. It also supports import substitution and aligns with Make in India manufacturing goals. As advanced rubber compounds and engineered polymers mature, airless tires can become more affordable and suitable for Indian roads and climate conditions.

Industry Value Chain Analysis

India airless tires value chain integrates raw material supply, material processing & compound development, airless tire design, engineering & manufacturing, certification, testing & regulatory compliance, distribution & aftermarket sales, and end users.

|

Stage |

Key Participants |

|

Raw Material Supply |

Natural rubber suppliers, synthetic rubber manufacturers, polymer compound producers, specialty elastomer suppliers, reinforcing material providers, and chemical additive manufacturers. |

|

Material Processing & Compound Development |

Rubber compound formulators, polymer engineering companies, material testing laboratories, R&D institutions, and advanced material technology providers. |

|

Airless Tire Design, Engineering & Manufacturing |

Airless tire manufacturers, tire technology developers, mold and tooling suppliers, product design teams, testing facilities, and production plants. |

|

Certification, Testing & Regulatory Compliance |

Automotive testing agencies, certification bodies, quality assurance laboratories, safety regulators, and industry standards organizations. |

|

Distribution & Aftermarket Sales |

Authorized distributors, tire dealers, automotive retailers, e-commerce platforms, fleet solution providers, and service networks. |

|

End Users |

Individual vehicle owners, EV users, commercial fleet operators, government agencies, defence organizations, industrial vehicle operators, and specialty mobility users. |

The most value-added segment is airless tire design, engineering, and manufacturing. This stage captures the highest value because it involves proprietary tire architecture, advanced polymer/rubber formulation, product testing, and performance optimization. It directly determines durability, ride comfort, load capacity, and OEM acceptance, making it the core differentiator in the Indian airless tires market.

Technology Landscape in the India Airless Tires Industry

Spoke and Lattice Structure Airless Tire Technology

Spoke and lattice structure airless tire technology replaces compressed air with engineered load-bearing structures that provide support and shock absorption. These designs enhance puncture resistance, durability, and operational reliability while reducing maintenance requirements. Manufacturers are investing in advanced polymers, computational design tools, and material optimization to improve ride comfort and load-carrying performance. The technology is gaining interest across EVs, defence vehicles, construction equipment, and specialty mobility applications where tire failure can significantly impact operations.

Composite Polymer Material for the Indian Climate

Manufacturers are developing advanced rubber-polymer blends that can withstand high temperatures, heavy monsoon exposure, UV radiation, and diverse road conditions. These materials improve durability, load-bearing capacity, wear resistance, and ride performance while extending tire lifespan. Ongoing R&D in engineered elastomers and reinforced composites is helping make airless tires more practical and cost-effective for Indian operating environments.

Lightweight Tire Design for EV Range Efficiency

Lightweight tire design for EV range efficiency, reducing overall vehicle weight and improving energy efficiency. In EVs, lighter airless tire structures can help lower rolling resistance, support better battery performance, and extend driving range. This is especially important for electric two-wheelers, three-wheelers, and delivery fleets operating on tight cost-per-kilometer economics. E3W sales rose to 88,272 units in December 2025, up 48.58% year-on-year from 59,412 units and 5.51% month-on-month. Electric car sales also increased to 30,314 units in January 2026, growing 51% year-on-year from 20,088 units and 27% month-on-month. As EV adoption grows, manufacturers are focusing on lightweight polymers, optimized lattice structures, and durable designs suited to Indian roads.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Vehicle Type |

Passenger Vehicles |

42.3% |

2025 |

|

Sales Channel |

OEM |

80.0% |

2025 |

|

Region |

North India |

33.7% |

2025 |

By Vehicle Type

Passenger vehicles lead at 42.3% (2025), through India's urban EV two-wheeler OEM bundling, premium passenger car niche fitment, and golf cart airless standard fitment.

To access detailed market analysis, Request Sample

Commercial vehicles at 28.6% encompass last-mile delivery electric three-wheeler, urban bus pilot, and highway truck airless tires. Off-road vehicles at 21.9% grow fastest at ~4.8% CAGR through Jharkhand-Odisha mining equipment, Indian Army patrol vehicles, and construction equipment. Others at 7.2% include warehouse AGV, golf maintenance equipment, and specialty industrial vehicles.

By Sales Channel

OEM leads at 80.0% (2025), through factory-fitted airless tire for golf carts, EV two-wheeler, and defence vehicles.

Aftermarket at 20.0% grows at ~4.6% CAGR through government fleet replacement, golf course maintenance, and growing industrial equipment replacement.

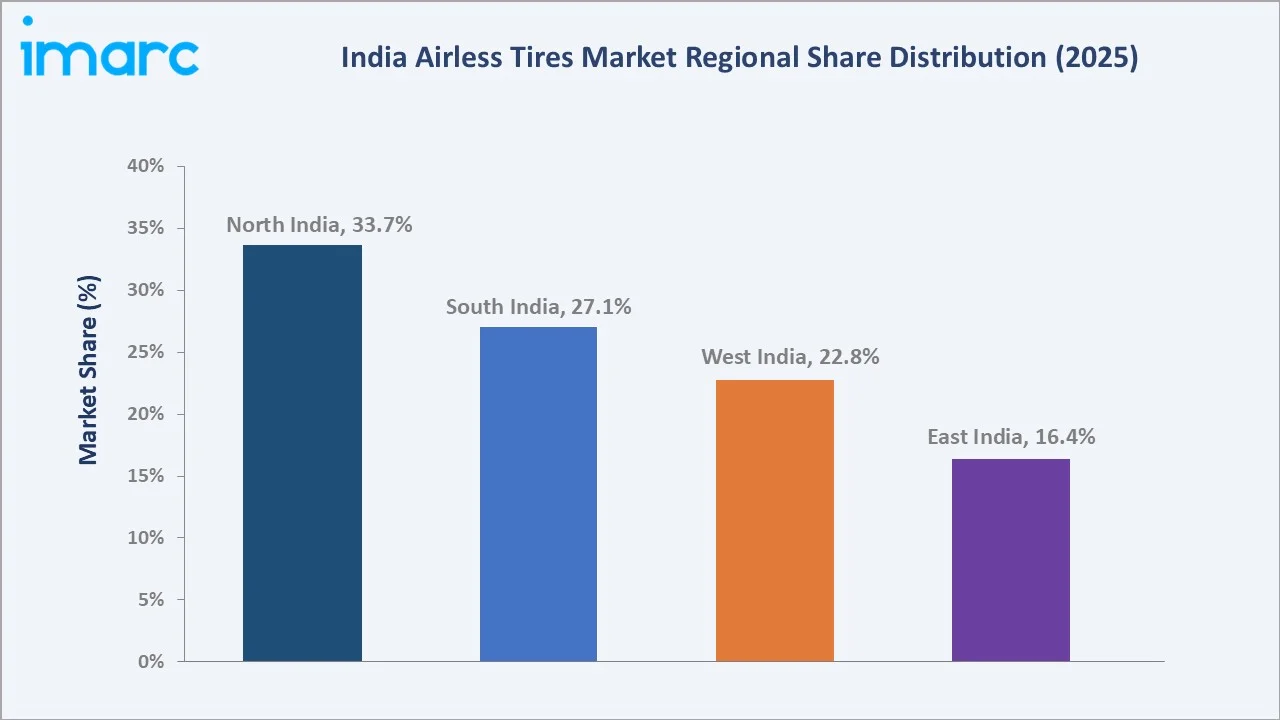

Regional Market Insights

|

Region |

Share (2025) |

Key India Airless Tires Market Drivers & Characteristics |

|

North India |

33.7% |

Reflecting its strong automotive manufacturing base, high vehicle ownership, expanding logistics sector, and increasing adoption of EVs. |

|

South India |

27.1% |

Strong presence of automotive OEMs, growing electric two-wheeler adoption, and expanding industrial and commercial vehicle fleets are driving demand for advanced airless tire technologies. |

|

West India |

22.8% |

Rising fleet operations and increasing investments in EV infrastructure support airless tire adoption across commercial applications. |

|

East India |

16.4% |

Growing demand for rugged, puncture-resistant tires in off-road and utility vehicle applications is creating opportunities for airless tire manufacturers in the region. |

North India leads the India airless tires market with a 33.7% share, supported by strong automotive activity, logistics growth, EV adoption, and defence procurement. South India follows with 27.1%, driven by EV manufacturing hubs, two-wheeler adoption, and industrial fleets.

West India holds 22.8%, supported by logistics, warehousing, construction, and industrial demand. East India accounts for 16.4%, with growth linked to mining, infrastructure development, agriculture, and off-road utility applications.

Competitive Landscape

India airless tires competitive landscape is commercially stratified between global multinational technology leaders, domestic Indian tire majors, and international second-tier brands.

|

Company |

Key Products |

Market Position |

Core Strength |

|

Michelin |

MICHELIN UPTIS, MICHELIN Tweel airless tyre |

Market Leader |

Michelin is actively positioning itself as a leader in sustainable mobility in India through its pioneering airless tire technology, notably the MICHELIN UPTIS and the commercial-grade Tweel. |

|

Bridgestone Corporation |

Air-free Concept Tires |

Market Leader |

Bridgestone Corporation’s Air-Free Concept tires aim to revolutionize Indian mobility by eliminating punctures and reducing maintenance through a spoke-structured, non-pneumatic design made from recyclable thermoplastic resins. |

|

Sumitomo Group |

GYROBLADE |

Niche Player |

Sumitomo Group, through its Sumitomo Rubber Industries (SRI), is known for its airless tire technology for the Indian market. Through their SMART TYRE CONCEPT, they are focusing on sustainable, maintenance-free mobility solutions. |

India's airless tires competitive landscape is evolving through domestic Indian tire companies’ above-standard R&D investment, EV two-wheeler OEM bundling, and defence procurement preference.

Key Company Profiles

Michelin

Michelin is one of the leading tire manufacturers and a pioneer in sustainable mobility solutions, with a strong presence across passenger vehicles, commercial vehicles, specialty tires, and advanced tire technologies. The company is at the forefront of airless tire innovation through its MICHELIN Uptis technology, designed to eliminate punctures, reduce maintenance requirements, and improve tire lifespan.

- Key Products: MICHELIN UPTIS, MICHELIN Tweel airless tyre.

- Strategic Focus: Emphasizing lightweight tire structures and advanced composite materials to improve durability, ride performance, and EV efficiency.

Bridgestone Corporation

Bridgestone Corporation is one of the largest tire and rubber companies, offering a broad portfolio of tires for passenger vehicles, commercial vehicles, off-road equipment, and specialty mobility applications. The company is actively developing next-generation airless tire solutions through its Air Free Concept, which eliminates the need for air pressure by utilizing a unique spoke structure made from advanced materials.

- Key Products: Air-free Concept Tires

- Strategic Focus: Centered on advancing its Air Free Concept technology to provide puncture-proof, maintenance-free, and durable tire solutions. The company is investing in lightweight spoke-structure designs and sustainable materials to enhance ride performance, energy efficiency, and product longevity.

Market Concentration Analysis

The India airless tires market is moderately concentrated, with competition led by global tire manufacturers and other companies investing in advanced non-pneumatic tire technologies. Market entry barriers are relatively high due to specialized design requirements, proprietary materials, extensive testing needs, and significant R&D investments. Established tire manufacturers benefit from strong engineering capabilities, intellectual property portfolios, and OEM relationships. However, the market remains in an early commercialization stage, creating opportunities for technology-focused startups and niche manufacturers. As EV adoption, defence modernization, and industrial mobility applications expand, competition is expected to intensify with increased focus on innovation, localization, and strategic partnerships.

Investment & Growth Opportunities

Highest Growth Segments

Off-road vehicles (~4.8% CAGR), aftermarket (~4.6% CAGR), EV two-wheeler OEM bundling (~6-8% CAGR from smaller base), electric three-wheeler last-mile delivery (~8-10% CAGR from small base), golf course and micro-mobility (~5-6% CAGR), and defence procurement (~7-9% CAGR) represent India airless tires highest-growth investment vectors through 2034.

Investment Themes

- EV two-wheeler OEM bundling: As EV scooter and motorcycle sales continue to grow in India, OEM partnerships can provide scalable volume growth, recurring demand, and faster market penetration while reducing reliance on aftermarket adoption.

- Mining equipment airless for coal and iron ore fleet: This investment theme targets heavy-duty mining vehicles operating in coal and iron ore mines, where tire punctures and downtime can significantly impact productivity. Airless tires offer enhanced durability, lower maintenance requirements, and improved operational reliability, making them attractive for mining fleets working in harsh and abrasive environments.

Future Market Outlook (2026-2034)

India airless tires market is projected to grow from USD 480.7 Million in 2025 to USD 692.9 Million by 2034, delivering a 4.15% CAGR over the forecast period. The market's anchor value of USD 589.0 Million in 2030 represents India's airless tire market at the commercial transition phase, where airless tires move from niche and pilot applications toward broader adoption. Growth will be supported by EV two-wheeler expansion, last-mile delivery fleets, defence procurement, and off-road industrial use. Rising demand for puncture-proof, low-maintenance, and durable tire solutions will strengthen adoption. However, higher costs and platform compatibility challenges may keep growth gradual rather than rapid.

Three structural forces define India’s airless tires market through 2034: EV-led mobility growth, rising demand for puncture-proof fleet operations, and expanding off-road use in defence, mining, and construction. EV two-wheelers and three-wheelers create demand for lightweight, low-maintenance tire solutions. Logistics and last-mile delivery fleets require reduced downtime and lower lifecycle costs. Meanwhile, harsh operating environments in industrial and defence applications support the adoption of durable, airless tire technologies.

Research Methodology

Primary Research

Primary research comprised interactions with tire manufacturers, automotive OEMs, EV producers, fleet operators, distributors, and industry experts. It helped assess adoption readiness, pricing expectations, technology preferences, and demand across passenger, commercial, defence, and off-road vehicle segments. Insights from these stakeholders supported validation of market trends, growth drivers, challenges, and future opportunities.

Secondary Research

Secondary research encompassed the analysis of company annual reports, investor presentations, industry publications, government policy documents, automotive association data, and EV market statistics. It also included the review of technical papers, tire technology developments, regulatory frameworks, and trade data related to non-pneumatic tires. These sources were used to evaluate market size, competitive dynamics, technological advancements, and long-term growth prospects in the India airless tires market.

Forecasting Models

India airless tires market revenue forecasts developed using a vehicle fleet penetration model: India new vehicle annual registrations by category multiplied by airless tire OEM adoption rate per vehicle category multiplied by average per-unit airless tire selling price by vehicle category.

India Airless Tires Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Vehicle Types Covered | Passenger Vehicles, Commercial Vehicles, Off-road Vehicles, Others |

| Sales Channels Covered | OEM, Aftermarket |

| Regions Covered | North India, South India, East India, West India |

| Companies Covered | Michelin, Bridgestone Corporation, Sumitomo Group, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Airless Tires Market Report

The India airless tires market reached USD 480.7 Million in 2025, driven by rising demand for puncture-proof, durable, and low-maintenance tire solutions across EVs, passenger vehicles, fleets, and off-road applications. Growth in electric two-wheelers, last-mile delivery, construction, mining, and defence mobility is increasing the need for tires that reduce downtime and maintenance costs. Support for domestic manufacturing and advanced mobility technologies further strengthens market expansion.

The India airless tires market grows at 4.15% CAGR during 2026-2034, reaching USD 692.9 Million by 2034. The CAGR reflects EV two-wheeler OEM bundling, mining operational necessity, defence procurement, and road infrastructure investment, creating India's multi-driver airless tire growth trajectory.

Passenger vehicles lead at 42.3% through India's urban EV two-wheeler OEM bundling, premium passenger car niche fitment, and golf cart standard fitment.

OEM leads at 80.0% as vehicle manufacturers are best positioned to integrate airless tires during the design and production stage. Factory-fitment supports better compatibility, safety validation, and performance optimization compared to aftermarket adoption. Rising EV production and OEM focus on differentiated, low-maintenance mobility solutions further strengthen segment dominance.

North India leads at 33.7% due to its strong automotive base, high vehicle ownership, and expanding EV adoption. The region also benefits from growing logistics, warehousing, infrastructure, and construction activity. Defence procurement and industrial mobility demand further support the use of durable, puncture-proof tire solutions.

Leading companies include Michelin, Bridgestone Corporation, and Sumitomo Group, among others.

The market is projected to reach approximately USD 589.0 Million by 2030, with EV two-wheeler OEM bundling, EV scooter standard fitment, mining equipment commercial adoption, and passenger car airless standard.

Priority investment opportunities include EV two-wheeler OEM bundling, mining and industrial off-road applications, and defence mobility programs. These areas offer strong potential because they require durable, puncture-proof, and low-maintenance tire solutions that reduce downtime, improve operating efficiency, and support India’s shift toward electrification, infrastructure growth, and indigenous defence production.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)